Market Overview

| Study Period | 2021 - 2031 |

|---|---|

| Forecast Data Period | 2026 - 2031 |

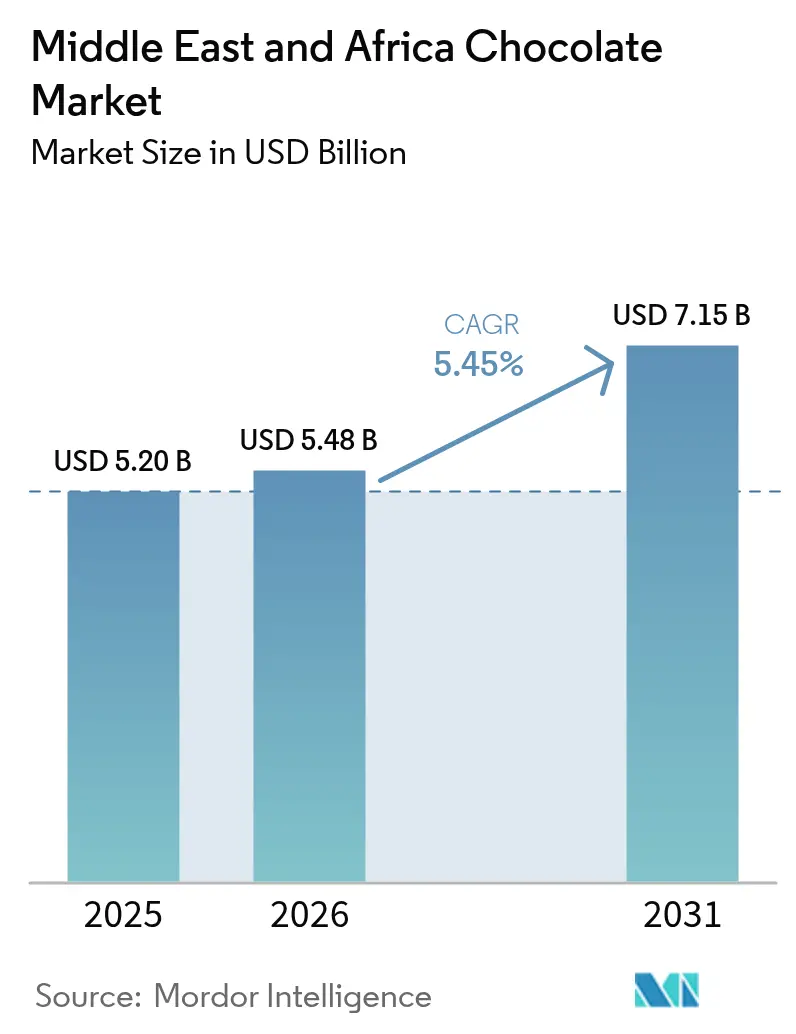

| Base Year Market Size (2025) | USD 5.20 Billion |

| Market Size (2026) | USD 5.48 Billion |

| Market Size (2031) | USD 7.15 Billion |

| Growth Rate (2026 - 2031) | 5.45% CAGR |

| Market Concentration | Medium |

Major Players

*Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. |

|

Middle East And Africa Chocolate Market Analysis by Mordor Intelligence

The Middle East and Africa chocolate market size was valued at USD 5.20 billion in 2025 and estimated to grow from USD 5.48 billion in 2026 to reach USD 7.15 billion by 2031, at a CAGR of 5.45% during the forecast period (2026-2031). Revenue growth is being driven by several key factors, including the seasonal surge in demand during Ramadan and Eid, which significantly boosts sales during these periods. The rapid expansion of quick-commerce platforms is also playing a pivotal role, as these platforms enable faster and more convenient access to products, catering to the evolving consumer preference for instant delivery. Additionally, the introduction of premium single-origin products is attracting a niche but growing segment of consumers who value high-quality and unique offerings. On the other hand, challenges such as cocoa supply constraints are impacting the availability and pricing of raw materials, while the implementation of new sugar-label regulations is compelling manufacturers to adapt their cost structures and reformulate products to comply with these guidelines.

Key Report Takeaways

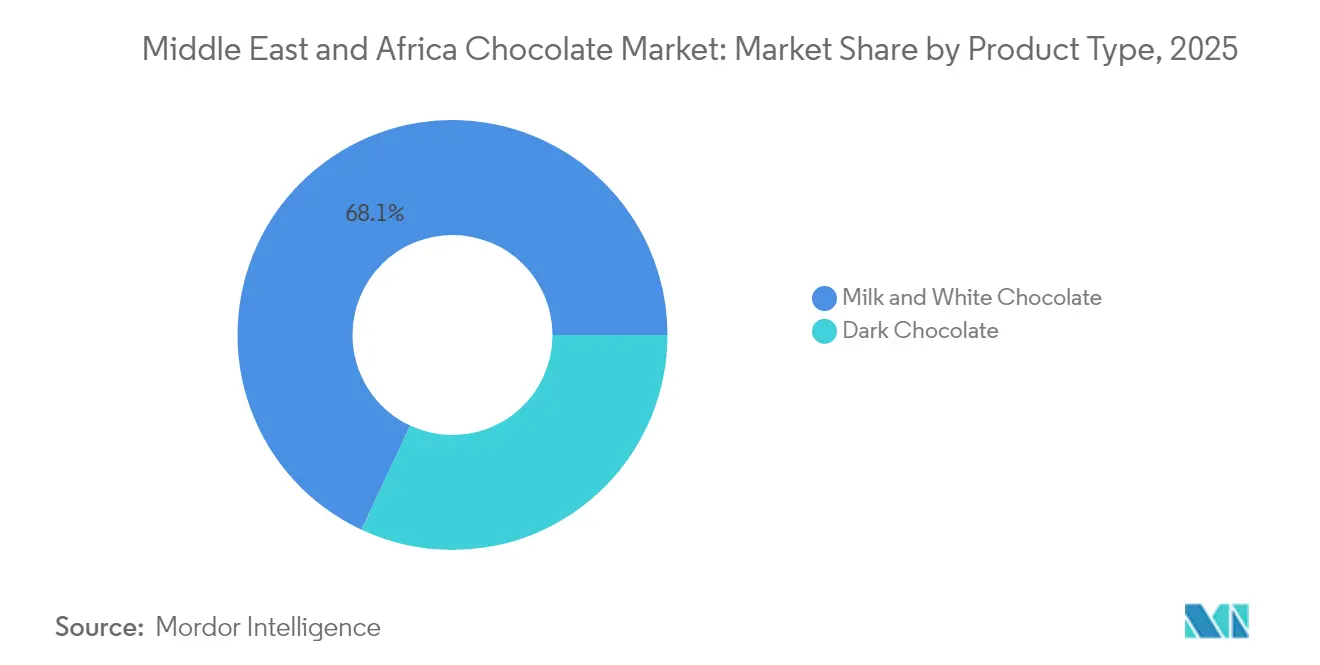

- By type, milk and white chocolate led with 68.05% of 2025 revenue and dark chocolate is forecast to expand at a 6.92% CAGR through 2031.

- By form, tablets and bars claimed 81.85% of 2025 volume, while pralines and truffles are advancing at a 5.72% CAGR to 2031.

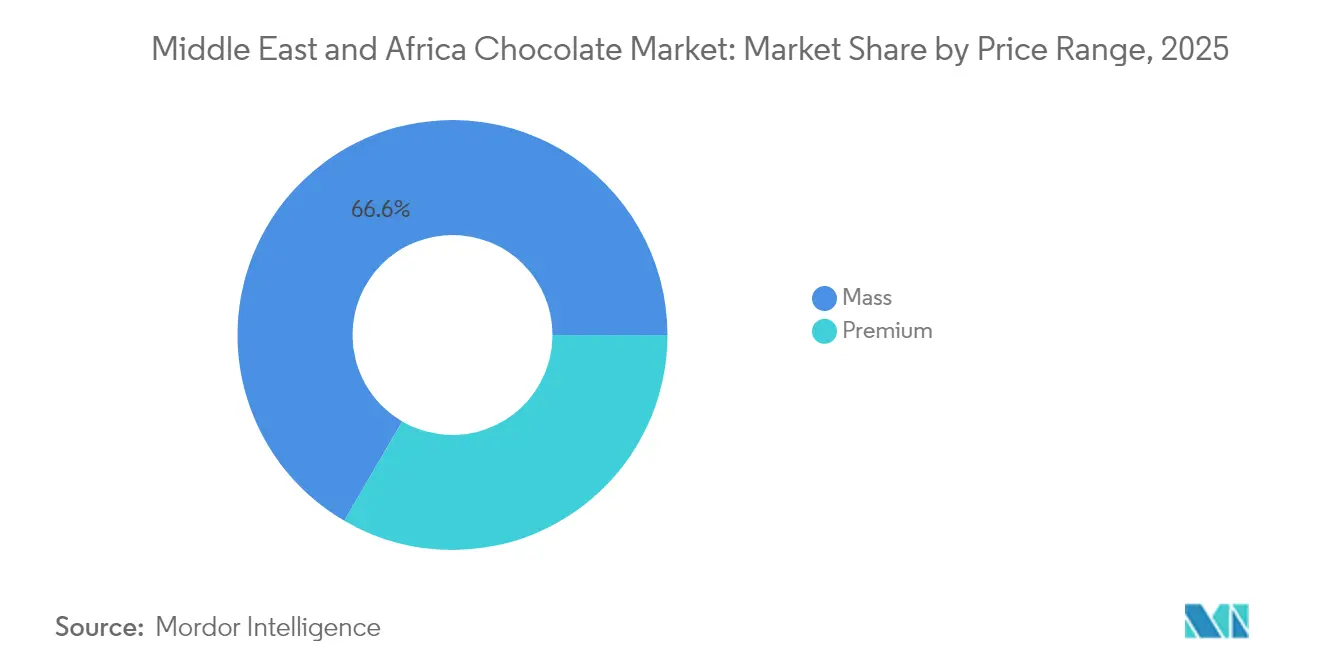

- By price range, mass products captured 66.60% of 2025 sales, yet the premium segment is set to grow at 7.78% CAGR from 2026-2031.

- By ingredient, dairy-based lines dominated 2025, whereas plant-based and single-origin variants post double-digit gains, leading the sub-segment at 11.96% global CAGR.

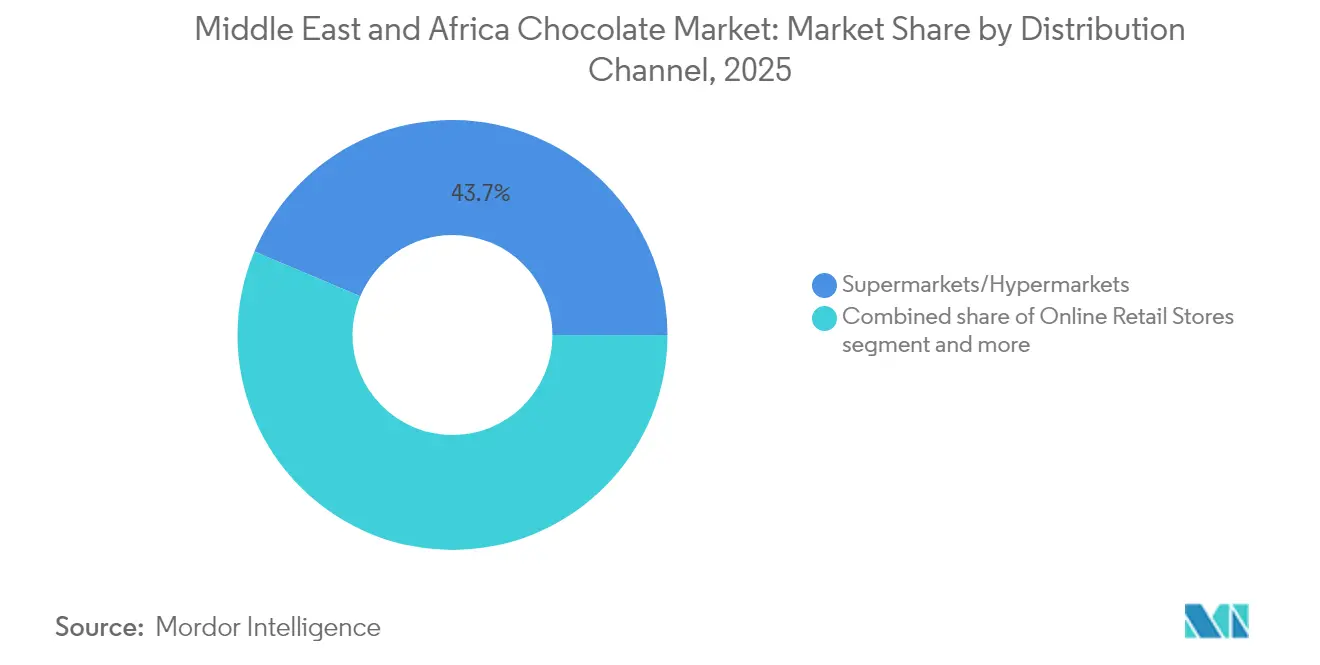

- By distribution channel, supermarkets and hypermarkets held 43.65% share in 2025 and online retail is positioned for a 6.84% CAGR by 2031.

- By geography, Saudi Arabia held 42.70% market share in 2025; South Africa records the fastest geographic expansion with 5.98% CAGR to 2031.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of 2026.

Middle East And Africa Chocolate Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Rising demand for premium and artisanal chocolates | +1.2% | GCC core (Saudi Arabia, UAE, Qatar, Kuwait), South Africa urban centers | Medium term (2-4 years) |

| Gifting peaks during Ramadan, Eid and wedding seasons | +0.9% | Saudi Arabia, UAE, Qatar, Kuwait, Egypt, with spillover to broader Middle East | Short term (≤ 2 years) |

| E-commerce apps' dark-store model boosting impulse sales | + 0.8% | UAE, Saudi Arabia, South Africa metro areas, expanding to Egypt and Kenya | Short term (≤ 2 years) |

| Mandatory front-of-pack 'High-Sugar' labels in Saudi and UAE | +0.5% | Saudi Arabia, UAE (national), potential adoption in Qatar, Kuwait | Medium term (2-4 years) |

| Innovation in flavors, formats and occasions | +0.6% | Global across MEA, strongest in GCC and South Africa | Medium term (2-4 years) |

| Youthful demographics and snacking behavior | +0.7% | Saudi Arabia, UAE, Africa-wide (60% under 25), Nigeria, Kenya | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

Rising demand for premium and artisanal chocolates

In GCC cities and South African metros, affluent households are increasingly gravitating towards premium offerings. They're opting for single-origin bars, camel-milk recipes, and craft lines that follow the bean-to-bar philosophy. These premium products command a price premium of 30-50% over mainstream tablets. Brands bolster their authenticity through provenance storytelling and halal certification. This strategy has enabled premium labels to outpace the market average by 240 basis points. Take Mirzam, for example. They weave heritage narratives around Ethiopian or Tanzanian cocoa, securing duty-free listings in the process. Meanwhile, Al Nassma distinguishes itself by transforming camel milk into unique flavors, a feat that's challenging for global giants to replicate. This premium surge acts as a buffer for some manufacturers against commodity price spikes. Their loyal clientele willingly pays higher shelf prices for these limited-edition runs. In response, competitors are either making acquisitions or launching artisanal SKUs, strategically timed for seasonal gifting opportunities.

Gifting peaks during Ramadan, Eid and wedding seasons

In 2024, Ramadan and Eid accounted for 45-53% of the annual chocolate gifting in Saudi Arabia and the UAE[1]Source: Visa Foundation, " The bustling Ramadan night-time economy" , usa.visa.com. This trend has heightened the urgency for manufacturers to stock up their inventories months in advance. Additionally, wedding seasons in the region trigger another surge in demand, as ornate favor boxes gain prominence as a social currency. While Patchi adeptly adjusts its production schedules and Arabic-calligraphy gift sets to align with these peak times, smaller brands grapple with the challenge of unsold stock, finding it difficult to repurpose their seasonal offerings. This cash-flow unpredictability compels companies to seek extended payment terms from retailers. In contrast, multinational corporations capitalize on their global supply networks, strategically dispersing excess inventory across various markets.

E-commerce apps’ dark-store model boosting impulse sales

Quick-commerce platforms like Talabat, Noon, and Checkers Sixty60 are turning late-night cravings into completed baskets with their promise of 15-minute delivery. This push has driven online penetration in the UAE, projecting chocolate transactions to hit 50% by 2024, a significant leap from the low single digits just five years prior. These platforms rely on dark stores, which are strategically located warehouses designed to stock high-velocity SKUs, ensuring faster delivery times and a seamless customer experience. This shift has moved product visibility from traditional physical shelves to app search results, fundamentally altering consumer purchasing behavior. In South Africa, the online grocery market is set to expand significantly, with its value projected to rise from USD 22.3 million in 2025 to USD 59.1 million by 2029. This growth highlights the scalability of the channel and its potential to capture a larger share of the grocery market. To adapt to this evolving landscape, brands are now investing in sponsored placements and optimizing metadata, extending their focus beyond just end-cap displays. These strategies are becoming essential for maintaining visibility and ensuring they remain top-of-mind for consumers in an increasingly digital marketplace.

Mandatory front-of-pack “high-sugar” labels in Saudi and UAE

Starting mid-2025, Saudi Arabia's SFDA and the UAE's climate ministry will mandate front-of-pack warning icons on products that exceed 15g of sugar per 100g[2]Source: United States Dairy Export Council, " Saudi Arabia Proposes Salt and Sugar Upper Limits in Foods" , usdec.org. This regulation aims to address rising health concerns related to high sugar consumption and encourage healthier consumer choices. Following similar moves in Chile and the UK, which saw sugary snack sales plummet by double digits within the first that market's first 18 months of implementation, many brands are reformulating their products to comply with the new guidelines. In a strategic move, Ferrero and Lindt have rolled out 70% cocoa bars, positioning their dark chocolate lines as guilt-free indulgences to sidestep label penalties. However, brands that can't adapt to using stevia, erythritol, or absorb the costs of shrinking portions might find their profit margins squeezed and risk losing valuable shelf space, potentially impacting their market presence and competitiveness.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Rising health consciousness and awareness of obesity/diabetes risks | -0.8% | Saudi Arabia, United Arab Emirates, Qatar, Kuwait, South Africa | Short term (≤ 2 years) |

| Competition from traditional sweets and other snacks | -0.5% | Middle East-wide (dates, kunafa, baklava), North Africa (halva, lokum) | Medium term (2-4 years) |

| Cocoa-yield losses from swollen-shoot spread in Ghana | -1.1% | Global supply chain, acute impact on West Africa-sourced brands | Short term (≤ 2 years) |

| Limited availability of premium raw materials | -0.6% | Premium segment across Middle East and Africa, single-origin sourcing in Ethiopia, Tanzania | Medium term (2-4 years) |

| Source: Mordor Intelligence | |||

Rising health consciousness and awareness of obesity/diabetes risks

In 2024, Saudi Arabia reported an adult obesity rate of 27.8%, while the UAE noted that 67.9% of its population was classified as overweight[3]Source: World Health Organization, " Epidemiology of obesity and control interventions in Saudi Arabia" , emro.who.int. These alarming statistics have spurred government campaigns in both nations, particularly targeting sugary foods. In response, consumers are adjusting their habits: they're downsizing portion sizes, gravitating towards dark chocolate, and opting for alternative snacks such as nuts, seeds, and low-sugar bars. Given the historical taxation on carbonated drinks, there's growing speculation about potential levies on confectionery items, which could further impact consumer behavior and market dynamics. This has led many brands to hasten their reformulation efforts, focusing on reducing sugar content and introducing healthier product lines. While premium buyers indulge in chocolate as an acceptable luxury, mainstream consumers are reducing their purchase frequency due to health concerns and potential cost increases. This shift presents a pronounced volume risk for brands targeting the mass market, compelling them to reassess their strategies to maintain competitiveness.

Competition from traditional sweets and other snacks

In the Middle East, cultural rituals celebrate regional favorites like dates, kunafa, baklava, and halva. Annually, the region consumes over 1 million tons of dates, reflecting their deep-rooted significance in traditional practices and daily life. These sweets are not only integral to cultural identity but also compete for the same gifting occasions, often being associated with perceived health benefits. Freshly baked kunafa, with its warm, rich texture and sensory appeal, offers an experience that packaged chocolate struggles to rival. This unique appeal resonates strongly with consumers, granting small local producers a distinct advantage during festivals and special occasions. Although chocolate's branding, convenience, and shelf stability cater to impulse snacking and modern gifting trends, heritage treats like kunafa, baklava, and halva dominate high-value ceremonial gifts. These traditional sweets symbolize cultural pride and are often chosen to honor significant events and relationships, reinforcing their enduring relevance in the market.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Type: Dark Chocolate Gains as Health Narratives Shift Preferences

In 2025, milk and white chocolate dominated the Middle East and Africa chocolate market, accounting for 68.05% of sales. This stronghold underscores the deep-seated consumer affinity for these flavors, especially in mass retail and gifting contexts. Yet, as health-conscious trends rise, spotlighting sugar content, there's a subtle shift. Shoppers are gravitating towards higher-cocoa options. In response, white chocolate is infusing regional flavors like saffron and rose-water, ensuring it remains relevant amidst the sugar scrutiny. This blend of tradition and innovative flavors helps milk and white chocolates maintain their stature, even as market dynamics evolve.

Dark chocolate is emerging as the fastest-growing segment, projected to grow at a 6.92% CAGR, outpacing the broader Middle East and Africa chocolate market. This surge is fueled by heightened awareness of cardiovascular health and regulatory emphasis on sugar content, steering consumers towards bars with 70% cocoa and above. Premium brands, such as Lindt and Mirzam, are capitalizing on this trend, offering single-origin dark ranges that highlight their provenance and health benefits. Concurrently, mainstream producers are experimenting with sugar substitutes in dark chocolates, aiming to cater to both price and taste-conscious consumers. With these strategies aligning, dark chocolate is poised to seize a larger share of the market's value, even as milk and white chocolates continue to lead in volume.

By Form: Tablets Dominate, Yet Pralines Capture Gifting Premiums

In 2025, tablets dominate the chocolate market in the Middle East and Africa, making up 81.85% of the volume. Their alignment with checkout merchandising and quick-commerce fulfillment boosts their popularity. Standardized sizes and consistent price points ensure tablets are pivotal for maintaining steady sales in supermarkets and on delivery apps. This format drives volume-centric strategies, promoting accessibility and encouraging repeat purchases. Tablets are particularly effective in catering to a broad consumer base, as they offer affordability and convenience, making them a staple in everyday consumption. Consequently, tablets serve as the primary growth engine for many regional chocolate brands, even as premium formats gain traction.

Pralines, on the other hand, are the market's rising star, with projections of a 5.72% CAGR. They command price premiums of 50–100%, particularly during peak times like Ramadan and wedding seasons. These elevated margins bolster brand profitability, even with pralines holding a smaller volume share. Luxury brands, such as Patchi, heavily invest in praline assortments, using them to cement their premium image and gifting appeal. Pralines are often associated with indulgence and exclusivity, making them a preferred choice for special occasions and high-end gifting. Thus, while tablets anchor brands with scale and reach, pralines carve out a niche, emphasizing differentiation and seasonal value.

By Price Range: Premium Segment Outpaces Mass Despite Smaller Base

In the Middle East and Africa, mass-priced chocolate dominates the chocolate market, making up 66.60% of sales and driving the overall category's scale. This tier's prevalence is due to its affordability, widespread distribution in supermarkets and convenience stores, and its alignment with daily consumption habits. Global giants leverage this tier to achieve high-volume sales, especially in the region's price-sensitive areas. To capitalize on the region's upgrading consumer behavior without jeopardizing their mass base, many are rolling out "premium-lite" ranges. These offerings elevate brand perception while remaining within reach of the average consumer's budget. The "premium-lite" strategy allows companies to bridge the gap between mass and premium segments, offering products that appeal to aspirational consumers while maintaining affordability. This approach helps brands retain their core customer base while attracting new consumers seeking a more refined experience.

Meanwhile, the premium tier is witnessing the fastest growth, boasting an 7.78% CAGR. This surge is attributed to income stratification and the emergence of affluent clusters in cities such as Dubai, Riyadh, and Johannesburg. Shoppers in these urban centers value craftsmanship, origin narratives, and the aesthetics of gifting. This focus allows brands to command significantly higher margins per unit. Furthermore, premium consumers have a strong affinity for limited editions and boutique experiences, enhancing brand loyalty and justifying elevated prices. The premium segment's growth is also fueled by increasing consumer awareness of high-quality ingredients and ethical sourcing, which resonate strongly with affluent buyers. However, companies that attempt to navigate both the mass and premium tiers face the risk of brand dilution. This challenge necessitates a strategic decision: pursue a cost-leadership scale or distinctly position as artisanal or luxury.

By Ingredient Type: Plant-Based and Single-Origin Gain Traction

In the Middle East and Africa, dairy-based chocolate leads the chocolate market, thanks to its familiar taste, creamy texture, and prominent presence in mainstream tablets, bars, and gift assortments. Supermarkets and convenience stores widely stock it, and it resonates strongly with traditional taste preferences. Single-origin dairy bars, priced between USD 8–12, appeal to affluent consumers by emphasizing their unique provenance and traceability. These bars often highlight the origin of the cocoa beans, creating a premium perception among consumers who value authenticity and quality. Yet, this focus on specific cocoa origins poses a risk: supply constraints and market volatility can jeopardize profit margins and product availability. Additionally, fluctuations in cocoa prices and geopolitical factors in cocoa-producing regions further exacerbate these challenges, making supply chain management critical for manufacturers.

Plant-based chocolate is rapidly emerging as the fastest-growing segment. Its ascent is fueled by the convergence of vegan, lactose-free, and halal positioning in major markets. Brands leverage oat and almond milk alternatives to cater to lactose-intolerant and ethically-conscious consumers, all while preserving indulgent flavors. These alternatives not only address dietary restrictions but also align with the growing consumer preference for sustainable and environmentally friendly products. Tightening halal documentation rules play to the advantage of these products. Regulators like ESMA are leaning towards manufacturers with stringent, auditable supply chains. Consequently, companies boasting robust certification and traceability systems are poised to expand their plant-based offerings, aligning with both regulatory standards and consumer demands. This shift also opens opportunities for innovation in flavors and formats, enabling brands to differentiate themselves in an increasingly competitive market.

By Distribution Channel: Online Retail Surges as Dark Stores Redefine Convenience

Supermarkets dominate the chocolate market in the Middle East and Africa, commanding a 43.65% share by offering a wide range of products, promotions, and price points all in one location. This dominance underscores the importance of physical aisle visibility, secondary displays, and in-store promotions in brand strategy. Supermarkets provide consumers with the convenience of accessing diverse chocolate options, catering to both everyday consumption and special occasions. Specialty stores and duty-free outlets cater to luxury gifting, offering premium and exclusive chocolate products that appeal to high-end consumers. Meanwhile, convenience stores serve as impulse-buy spots near workplaces, transit hubs, and fuel stations, targeting on-the-go customers with smaller, ready-to-eat chocolate packs. Collectively, these brick-and-mortar outlets maintain a steady flow of sales, even as online channels grow.

Online retail is rapidly emerging as the leading channel, growing at a 6.84% CAGR, indicating a fundamental shift in chocolate discovery and purchasing. Brands now prioritize sponsored placements and algorithm-driven search optimization, equating their importance to traditional eye-level shelf space. The convenience of online shopping, coupled with personalized recommendations and exclusive online discounts, is driving consumer adoption of digital platforms. Given the region's extreme climates, ensuring fast delivery of chocolate necessitates thermal-shielded packaging and enhanced last-mile logistics, favoring larger players with the resources to invest. As these digital capabilities evolve, online platforms are set to play a pivotal role in determining brand visibility, pricing strategies, and customer loyalty in the Middle East and Africa's chocolate market.

Geography Analysis

Saudi Arabia, accounting for 42.70% of 2025's revenue, capitalizes on its high per-capita incomes and cultural norms that elevate chocolate's status, placing it alongside dates during Ramadan and Eid celebrations, as reported by VISA.COM. The country's strong gifting culture and preference for premium products further bolster its chocolate market. While mandatory sugar labels set to roll out in July 2025 might curtail sales of mass-market tablets, they are expected to steer demand towards premium dark bars, which are perceived as healthier alternatives. The UAE, echoing Saudi trends, sees its tourism-driven duty-free channels amplifying the allure of premium offerings, with international travelers contributing significantly to sales. Both Qatar and Kuwait, despite their smaller sizes, mirror the GCC's wealth and penchant for premium products, driven by high disposable incomes and a growing inclination toward luxury goods. Meanwhile, Egypt boasts a larger populace, but currency challenges and inflationary pressures temper its per-capita spending, limiting the market's growth potential.

South Africa, enjoying a 5.98% CAGR, attributes its growth to rising urban incomes and the deepening reach of e-commerce, both of which are fostering a shift towards premium products. The increasing availability of online platforms has made premium chocolates more accessible to a broader audience. While its per-capita consumption lags behind the GCC, it outpaces its sub-Saharan counterparts, positioning South Africa as a bridge between mass-market volumes and premium explorations. Though Nigeria and Kenya show promise for the long haul, challenges like infrastructure deficits, high tariffs, and limited cold chain logistics are hindering their immediate mainstream adoption. However, their young and growing populations present significant opportunities for future market expansion.

In summary, while GCC markets offer short-term profitability, they grapple with regulatory and health challenges, such as the upcoming sugar labeling regulations. In contrast, African nations, despite their hurdles, present a demographic advantage in the long run, with rising urbanization and a growing middle class driving demand. Across the chocolate landscape of the Middle East and Africa, essentials like flavor localization, halal adherence, and a robust omni-channel strategy are paramount to capturing market share and ensuring sustained growth.

Regulatory Landscape

Chocolate manufacturers and importers across MEA operate under a mix of national food-control regimes. In the Gulf, enforcement is anchored by Gulf Standards Organization requirements, with country-level implementation shaping how companies manage labeling and documentation. In Saudi Arabia, the Saudi Food and Drug Authority (SFDA) ties imported pre-packaged foods to GSO 9 labeling compliance, with related technical regulations referenced via the Mwasfah portal and food-clearance documentation requirements updated in April 2025. These controls intersect with the report scope shift toward sugar scrutiny in the GCC, where front-of-pack “high-sugar” warnings and tighter substantiation for nutrition and health claims push manufacturers to reformulate and adjust packaging for mainstream tablets and bars.

In Africa, regulators and standards bodies are tightening product definitions and labeling rules that affect formulations, cocoa solids declarations, and quality parameters. The African Organization for Standardisation (ARSO) published CD ARS 1816:2025, aligning chocolate specifications to Codex Alimentarius (CODEX STAN 87-1981) and requiring cocoa solids percentage declaration (except white chocolate), while the East African Community standardization process is reflected in DEAS 38 labeling requirements for pre-packaged foods. South Africa continues to regulate labeling under the Foodstuffs, Cosmetics and Disinfectants Act, 1972, and the 2026 Mycotoxins Regulations (R. 7091) add another compliance layer for imported and locally manufactured cocoa and chocolate products.

Competitive Landscape

The chocolate market in the Middle East and Africa is moderatelyconcentrated. While global giants like Nestlé, Mondelēz, Mars, and Ferrero utilize worldwide procurement and marketing strategies, regional experts carve out niches by offering localized flavors and obtaining halal certifications. These regional players cater to specific consumer preferences, which helps them maintain a competitive edge despite the dominance of multinational corporations.

Al Nassma’s camel-milk chocolates, Patchi’s expansive 160-store luxury network, and Mirzam’s artisanal bean-to-bar studios highlight the power of cultural resonance over sheer scale in premium markets. Al Nassma, for instance, taps into the region’s heritage by using camel milk, a culturally significant ingredient, while Patchi’s luxury offerings appeal to high-end consumers seeking exclusivity. Meanwhile, Barry Callebaut plays a pivotal role in B2B supply, ensuring stability even amidst cocoa shortages in Ghana, which is a critical supplier of raw materials for the chocolate industry.

Strategic maneuvers focus on premium offerings, aligning with rapid commerce, and innovating seasonally. Ferrero’s Thorntons making inroads into UAE's duty-free market, Lindt’s flagship store in Riyadh offering customized pralines, and Mondelēz’s collaboration with Talabat for swift deliveries underscore the push for premium positioning and immediate accessibility. These strategies not only enhance brand visibility but also cater to evolving consumer demands for convenience and personalization. While smaller brands harness platforms like Instagram and pop-up events to carve out their niche, challenges like compliance costs and cocoa market volatility often lead them to be acquired by larger multinationals in pursuit of cultural authenticity. Such acquisitions allow global players to integrate local expertise and strengthen their foothold in the region.

Middle East And Africa Chocolate Industry Leaders

-

Nestle S.A.

-

Mondelez International Inc.

-

Mars Incorporated

-

Ferrero Group

-

Barry Callebaut

- *Disclaimer: Major Players sorted in no particular order

Market Opportunities and Future Outlook

Opportunities are centered on local and regional value addition as cocoa-origin countries connect more directly with Gulf demand centers and expand processing capacity. Egypts chocolate export performance provides a concrete signal of this trade pull, with exports reaching USD 273.4 million in 2025 (up 53% from 2024) and Saudi Arabia cited as the top destination. That outcome supports the case for Egypt-based manufacturers to deepen GCC-focused assortments and private-label supply. On the ingredient side, West African and Nigerian initiatives to finance and build processing facilities create nearer-to-market access to semi-finished cocoa inputs for MEA chocolate makers, which can reduce exposure to finished-product import costs and improve responsiveness for seasonal peaks (Ramadan and Eid gifting).

The pipeline also shows up in new financing and announced processing projects. In Nigeria, the Bank of Industry secured a 60 million euro facility from the European Investment Bank to support cocoa processing, ingredient manufacturing, packaging, and chocolate production, pointing to scaling potential for domestically produced chocolate and compound products across local and export channels. Sunbeth Global Concepts announced a 70,000-metric-ton cocoa processing facility in Akure, Ondo State, with inauguration scheduled for March 2027, adding another potential source of regional cocoa liquor, butter, and powder that fits manufacturers reformulating amid Saudi Arabia and UAE sugar and label scrutiny. Across channels, quick-commerce platforms and dark-store models (Talabat, Noon, Checkers Sixty60) continue to reward brands that invest in heat-resilient last-mile packaging, sponsored search, and high-velocity SKUs, particularly for tablets and bars that lead volume, while premium pralines capture gifting margins.

Recent Industry Developments

- July 2026: Barry Callebaut reported a return to volume growth in Q3 of fiscal year 2025/26, highlighting the Asia Pacific, Middle East, and Africa region as a leading contributor to its performance over the first nine months. The update reinforces Barrys role as a key B2B supplier for MEA chocolate makers navigating cocoa availability and cost volatility.

- October 2025: Barry Callebaut launched its plant-based, dairy-free tasting chocolate line, NXT, in Saudi Arabia, broadening professional and industrial-grade options for plant-based chocolate and dairy-alternative applications. The move supports manufacturers targeting lactose-free and vegan positioning while maintaining halal-compliant, auditable supply chains.

- July 2024: Mondelēz International invested USD 5 million in its Pakistan subsidiary to expand local capabilities and increase exports to GCC markets, alongside a push to raise local raw material sourcing. The investment strengthens a nearby manufacturing and export base that can supply Gulf demand during seasonal gifting peaks and manage lead times versus longer-haul imports.

Research Methodology Framework and Report Scope

Market Definition and Coverage

This market is measured as the value of chocolate products sold across the Middle East and Africa through retail and similar channels. Coverage includes common chocolate formats made with cocoa ingredients and consumed as confectionery.

Scope exclusions: We exclude cocoa raw materials that are traded for further processing and any non-chocolate sugar confectionery products that do not contain chocolate.

Segmentation Overview

-

By Product Type

-

Chocolate

- Dark Chocolate

- Milk and White Chocolate

-

By Form

- Tablets and Bars

- Molded Blocks

- Pralines and Truffles

- Other Forms

-

By Price Range

- Mass

- Premium

-

By Ingredient Type

- Dairy-based

- Plant-based

- Single-origin

-

By Distribution Channel

- Supermarket/Hypermarket

-

Convenience Store

- Sugar Chewing Gum

-

Online Retail

- Sugar-free Chewing Gum

- Others

-

Chocolate

-

By Geography

- South Africa

- Egypt

- Nigeria

- Kenya

- Saudi Arabia

- United Arab Emirates

- Qatar

- Kuwait

- Rest of Middle East and Africa

Data Sources, Market Sizing, and Validation

Desk Research

Desk research starts by building the demand picture and the country coverage using public sources that are easy to trace. We use national statistics offices and customs authorities for import and export series, central bank and IMF macro indicators for currency and inflation context, and FAOSTAT for cocoa and related agricultural baselines.

To link supply signals with consumption, we also review materials from food and confectionery associations, peer-reviewed journal articles on chocolate consumption trends and formulation changes, and official tariff schedules and trade notices. Company annual reports, investor presentations, and reputable press are then used to map brand presence, channel shifts, and pricing actions. Paid subscriptions are used selectively for company financials and intelligence, patent screening, and shipment-level trade checks where the public trail is incomplete. These examples are not exhaustive, and other public sources were also consulted for collection, cross-checking, and clarification.

Primary Interviews and Surveys

Primary work is used to pressure-test the desk assumptions that most affect value, especially price progression, channel mix, and the weight of gifting and seasonal demand in key Middle East and Africa countries. We speak with manufacturers, distributors, large retailers, and category specialists across the Gulf, North Africa, and Sub-Saharan Africa to reflect real stocking patterns and promotion intensity. Where the desk view conflicts with what respondents report, we revisit the relevant assumptions with follow-up calls.

Distribution of primary research fieldwork respondents

| Company type | Respondent position | Region |

|---|---|---|

| Top tier: 29% | CXOs: 14% | |

| Mid tier: 56% | Functional/Unit leaders: 36% | |

| Smaller Players: 15% | Managers: 50% |

Market-Sizing & Forecasting

The core model is built using a top-down demand pool approach where retail confectionery value is reconstructed country by country using consumption indicators, trade inflows for finished chocolate, and observable price and mix movements, then rolled up to the MEA total. After the first cut is formed, we corroborate it with selective bottom-up checks such as sampled price per pack by format and distributor-level channel checks. We also run sanity checks against major category revenue disclosures to adjust totals when the narrative does not fit.

Model inputs include chocolate import values and unit trends, household income and urbanization signals, inflation and currency movements that change shelf pricing, modern trade and e-commerce penetration, and seasonal gifting intensity that lifts boxed assortments and premium packs. For forecasting, scenario analysis is applied around the variables that tend to swing demand across MEA, and the final path is selected after primary discussions align on realistic price pass-through, promotion depth, and channel expansion. Where a country has patchy data, we interpolate using nearby market analogs and then scale back based on retailer feedback so the estimate stays practical.

Data Validation & Update Cycle

Validation is done through multiple checks so no single data line drives the final number. We compare country outputs against independent signals such as trade direction, inflation-adjusted spend trends, and channel expansion patterns, and then investigate large variances before sign-off.

A second analyst reviews the working sheet logic, assumptions, and conversions, followed by a final consistency pass across the country roll-ups. The report is refreshed annually, and interim updates are triggered when material events occur, such as sharp currency resets, major tax changes, or trade disruptions that visibly affect shelf pricing and product availability. Before delivery, the latest public releases are rechecked so clients receive an up-to-date view.

Mordor Intelligence's Middle East and Africa Chocolate Market Size Compared With Other Published Estimates

Published market sizes for chocolate in the Middle East and Africa can look far apart because the scope is not always described consistently, and the year and currency treatment can differ as well. Differences usually come from what is counted as chocolate, how retail pricing and inflation are applied, and whether country coverage is complete or supplemented using broad assumptions.

Some published figures appear to include a wider confectionery basket or count adjacent categories without a clear split, and they may apply a single regional price progression across different currencies. In Mordor Intelligence, the value is limited to chocolate products in MEA and is built from country level demand signals, with explicit currency timing and channel mix checks to avoid overstating the total.

Benchmark comparison

| Source | Market Size | Gaps in Research Methodology |

|---|---|---|

| Mordor Intelligence | USD 5.20 B (2025) | |

| Trade Publisher A | USD 8.42 B (2024) | The published note set does not clearly separate chocolate from adjacent confectionery or explain currency timing, which can inflate value when converted from local currencies and reported at a different base year. |

| Industry Data Site B | USD 14.22 B (2025) | This figure is labeled as chocolate confectionery and likely uses a broader basket and looser category boundaries, which can pull in non-chocolate confectionery and double count overlapping retail lines in mixed assortments. |

The spread in the table mainly comes from category scope and how price and currency effects are handled across different MEA markets. When the market is tied to clear product inclusion and country level checks, the number becomes easier to trace back to trade, pricing, and channel realities, and it remains repeatable when the model is refreshed.

Key Questions Answered in the Report

What is the expected value of the Middle East and Africa chocolate market in 2031?

The market is forecast to reach USD 7.15 billion by 2031 on a 5.45% CAGR.

Which country currently leads regional chocolate revenue?

Saudi Arabia, with 42.70% of 2025 revenue thanks to Ramadan and Eid gifting peaks.

Which chocolate type is expanding fastest in the region?

Dark chocolate is projected to grow at 6.92% CAGR between 2026 and 2031 as health concerns rise.

How quickly is online chocolate retail growing in the region?

Online sales are set to advance at a 6.84% CAGR, fueled by 15-minute quick-commerce delivery.

Page last updated on: