Market Overview

| Study Period | 2021 - 2031 |

|---|---|

| Forecast Data Period | 2026 - 2031 |

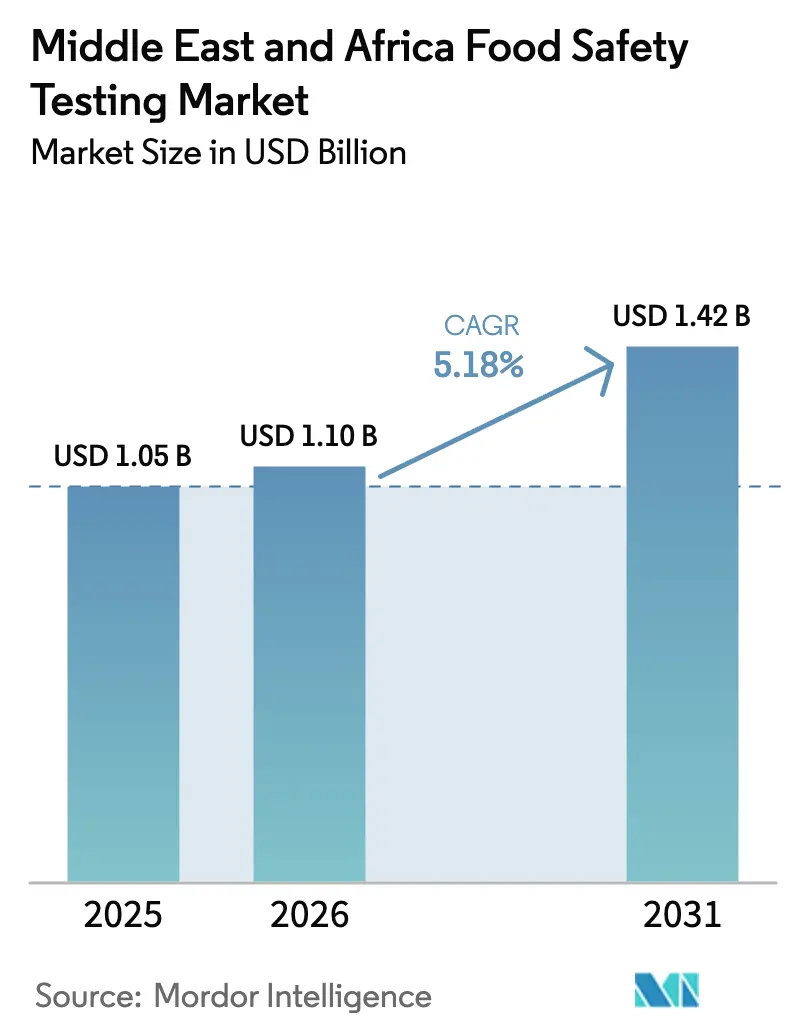

| Base Year Market Size (2025) | USD 1.05 Billion |

| Market Size (2026) | USD 1.1 Billion |

| Market Size (2031) | USD 1.42 Billion |

| Growth Rate (2026 - 2031) | 5.18% CAGR |

| Market Concentration | Medium |

Major Players

*Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. |

|

Middle East And Africa Food Safety Testing Market Analysis by Mordor Intelligence

The Middle East and Africa food safety testing market size is expected to grow from USD 1.05 billion in 2025 to USD 1.10 billion in 2026 and is forecast to reach USD 1.42 billion by 2031 at 5.18% CAGR over 2026-2031. The increasing incidence of foodborne illnesses, higher import volumes, and stricter halal compliance regulations drive the demand for accredited laboratories in the region. Laboratory capacity expansion occurs through public sector investments, private equity funding, and international donor support, while technology providers introduce cost-effective rapid testing methods. Testing volumes are primarily driven by Saudi Arabia's import regulations and Egypt's export initiatives, with additional testing requirements from emerging pet food and animal feed supply chains. The market maintains moderate competition, with regional laboratories leveraging local regulatory expertise, while international companies emphasize network coverage, digital solutions, and rapid pathogen detection services.

Key Report Takeaways

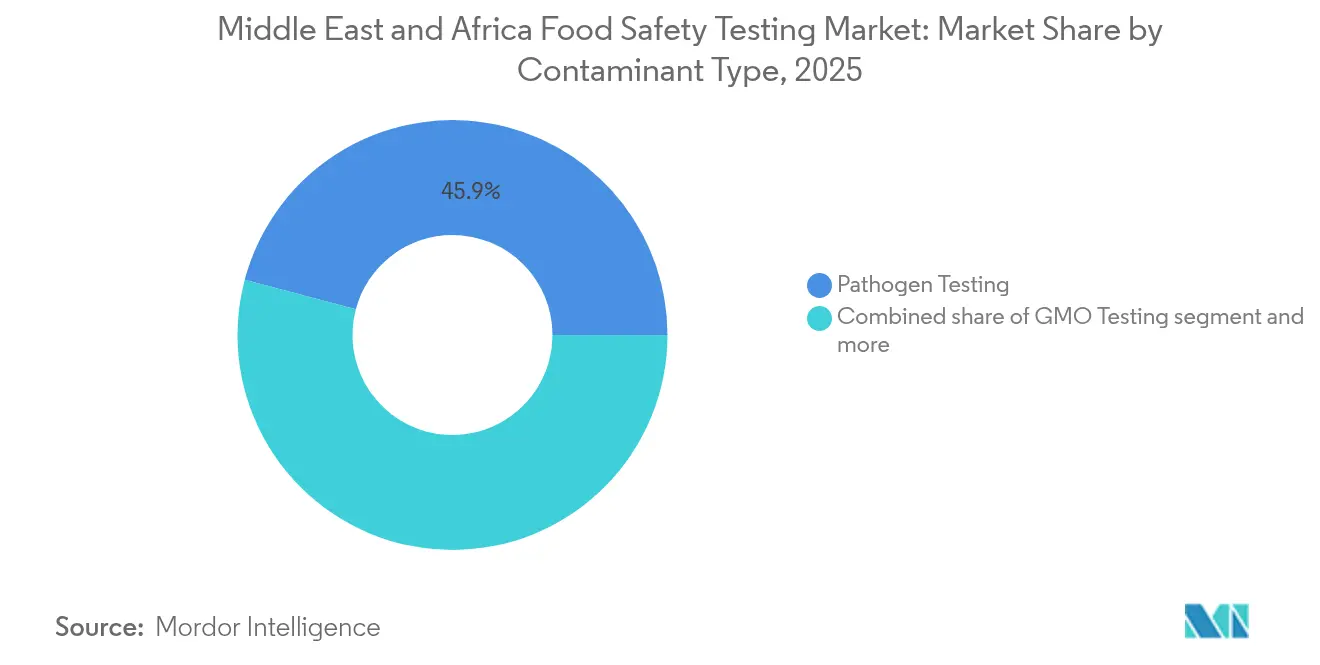

- By contaminant type, pathogen testing captured 45.86% of the food safety testing market share in 2025; GMO testing is projected to expand at a 6.55% CAGR between 2026-2031.

- By technology, immunoassay platforms held 38.25% revenue share of the food safety testing market in 2025, while PCR techniques are forecast to grow at an 7.93% CAGR through 2031.

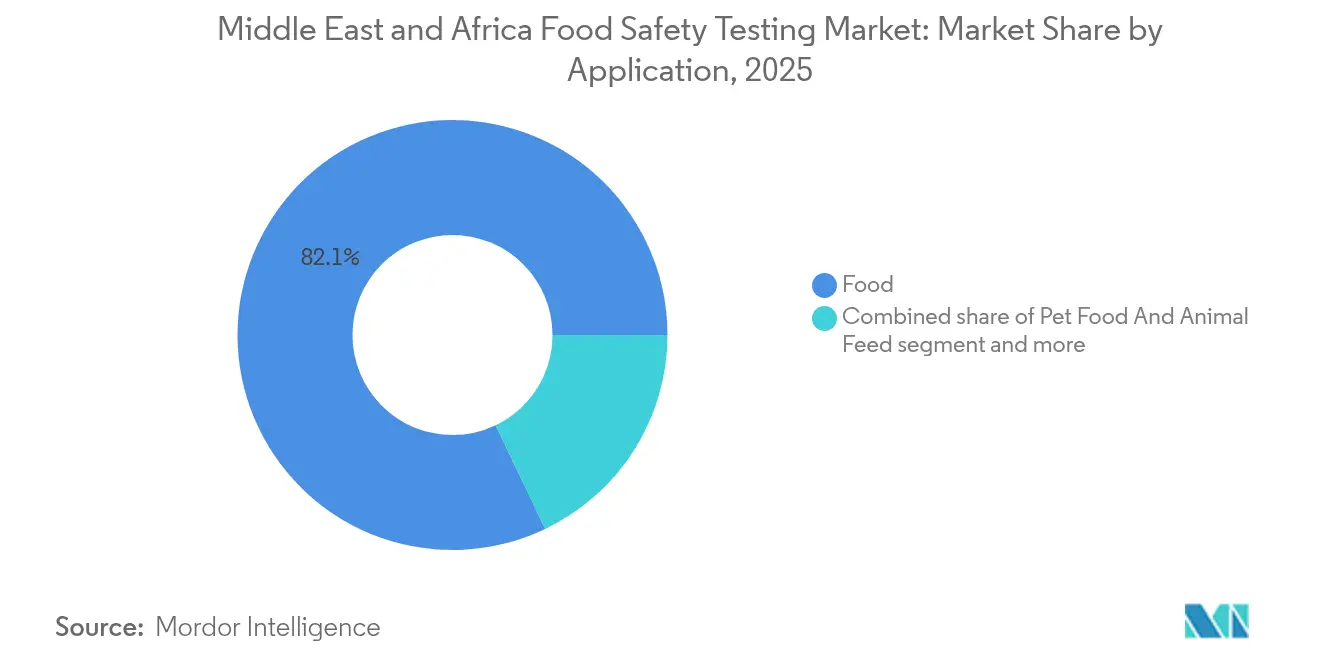

- By application, food products accounted for 82.10% of the food safety testing market size in 2025; pet-food and feed testing is advancing at a 7.05% CAGR to 2031.

- By geography, Saudi Arabia led with 27.88% of the food safety testing market in 2025, whereas Egypt is on track for the fastest 7.74% CAGR during the outlook period.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of 2026.

Middle East And Africa Food Safety Testing Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Heightened burden of foodborne diseases and public health impact | +1.2% | Global, with acute impact in Egypt, Nigeria, Morocco | Short term (≤ 2 years) |

| Stringent food-safety regulations across Gulf Cooperation Council (GCC) and Africa | +1.8% | Gulf Cooperation Council (GCC) core, expanding to North Africa | Medium term (2-4 years) |

| Rising importance of food safety and food issues | +0.9% | Global | Long term (≥ 4 years) |

| Expansion of international trade and food imports/exports | + 1.1% | Saudi Arabia, United Arab Emirates, Egypt, South Africa | Medium term (2-4 years) |

| Halal-integrity convergence with contaminant testing | +0.8% | Gulf Cooperation Council (GCC), North Africa, Nigeria | Short term (≤ 2 years) |

| Increase in non-compliant food products to fuel market demand | +0.7% | Regional, with concentration in major import hubs | Short term (≤ 2 years) |

| Source: Mordor Intelligence | |||

Heightened burden of foodborne diseases and public health impact

The increasing incidence of foodborne illnesses across Middle East and Africa (MEA) necessitates robust testing protocols to ensure food safety and public health protection. According to WHO EMRO, contaminated food causes illness in approximately 100 million people annually in the Eastern Mediterranean Region, with children under five being the most affected[1]Source: World Health Organization, "Food safety," who.int. Recent outbreaks in Jordan and Sudan highlight regional vulnerabilities, particularly from Salmonella and E. coli contamination, leading to increased hospitalization rates and strain on healthcare systems. Egypt's National Food Safety Authority has intensified the implementation of its 2023-2026 strategic plan, focusing on rapid detection capabilities and laboratory network expansion to address these challenges[2]Source: National Food Safety Authority, "The National Food Safety Authority's Media Center issues its 34th weekly report," nfsa.gov. This significant public health challenge requires substantial government investment in testing infrastructure and regulatory frameworks, while food companies implement thorough testing protocols throughout their supply chains to prevent recalls, maintain consumer trust, and ensure compliance with regional food safety standards.

Stringent food-safety regulations across Gulf Cooperation Council (GCC) and Africa

The regulatory environment in the Middle East and Africa continues to drive the expansion of food safety testing requirements through stringent policies and standards. The United Arab Emirates Federal Law on Food Safety mandates comprehensive testing protocols for imported products, establishing strict quality control measures at entry points. Saudi Arabia's SFDA implements rigorous requirements for laboratory verification and detailed documentation for all food imports entering the kingdom. Egypt's decision to extend its halal dairy certification deadline to December 31, 2025, demonstrates the ongoing balance between implementing new testing requirements and maintaining efficient trade flows. The African Continental Free Trade Area implements extensive sanitary and technical standards across member states, with its Guided Trade Initiative now encompassing 24 countries and including a wide range of processed foods such as instant coffee, dried fruits, and meat products[3]Source: ITC Trade Map, "African Continental Free Trade Area (AfCFTA)," macmap.org. These evolving regulations require accredited testing services and sophisticated laboratory infrastructure, leading to significant capacity development across member countries to meet compliance standards.

Expansion of international trade and food imports/exports

The increasing food trade volumes across the Middle East and Africa (MEA) region drive the demand for food safety testing services due to stringent import-export requirements. The complexity of these requirements continues to evolve as countries implement more comprehensive food safety standards and quality control measures. Russia's grain exports to the Middle East and Africa (MEA) constitute approximately 70% of its total grain shipments, with projections indicating 55-57 million tonnes for 2024. This substantial volume requires extensive testing for mycotoxins, pesticide residues, and quality parameters to ensure compliance with international standards and regional regulations. The BRICS Grain Exchange initiative, connecting Russia, Brazil, India, China, and South Africa with East African buyers, aims to consolidate trade flows and establish uniform testing requirements across member markets. This standardization effort is expected to streamline the testing processes and enhance trade efficiency. Tunisia's infrastructure development, including the modernization of 206,000 tonnes of existing silo capacity and the addition of 181,000 tonnes of new storage facilities, necessitates comprehensive grain quality monitoring and testing protocols throughout the supply chain. These protocols encompass various stages from receipt and storage to pre-shipment verification, ensuring consistent grain quality and safety standards.

Halal-integrity convergence with contaminant testing

The combination of halal certification and traditional contaminant testing has established specialized market segments that command premium prices. The United Arab Emirates's halal certification requirements under UAE.S 2055 series mandate comprehensive testing for prohibited substances along with standard safety parameters. Egypt's halal dairy certification program, which extends through December 2025, requires laboratories to verify both microbiological safety and halal compliance. This integration increases the demand for multi-parameter testing capabilities and specialized analytical methods. The halal certification frameworks of Indonesia and Malaysia function as models for other Middle East and Africa countries developing similar programs, generating opportunities for technology transfer and laboratory capacity building.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| High cost of advanced testing equipment | -0.8% | Sub-Saharan Africa, smaller Gulf Cooperation Council (GCC) markets | Long term (≥ 4 years) |

| Scarcity of ISO 17025-accredited local labs | -1.1% | Africa excluding South Africa, and smaller Middle East and Africa markets | Medium term (2-4 years) |

| Dependence on imported testing reagents and kits | -0.6% | Global | Medium term (2-4 years) |

| Resistance to change in traditional practices | -0.4% | Rural areas across Middle East and Africa | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

High cost of advanced testing equipment

The high costs of laboratory equipment create barriers to market entry and expansion in Sub-Saharan Africa, where foreign exchange limitations restrict equipment purchases. While MALDI-TOF MS systems provide rapid bacterial identification, their significant initial investment requirements exceed many regional laboratories' budgets. The reliance on imported analytical instruments makes laboratories vulnerable to currency fluctuations and supply chain disruptions. The African Development Bank's commitment to food safety laboratory infrastructure development, along with emerging financing models and government procurement programs, helps address these challenges. Additionally, leasing arrangements and shared laboratory facilities enable cost distribution while maintaining access to advanced testing capabilities.

Scarcity of ISO 17025-accredited local labs

The limited availability of internationally accredited testing facilities creates bottlenecks and increases testing costs across the region. South Africa's food safety testing laboratories are concentrated primarily in Gauteng and Western Cape provinces, resulting in uneven geographic distribution and creating challenges for food producers in other regions to access testing services. The IAEA and FAO support Zimbabwe's Central Veterinary Laboratory and Uganda's Directorate of Government Analytical Laboratory to achieve ISO 17025 accreditation, highlighting the regional capacity limitations and the need for enhanced testing infrastructure. SADC and COMESA are working toward regional harmonization through mutual recognition agreements to reduce duplicate testing while maintaining quality standards, which could potentially improve testing efficiency and reduce costs for food manufacturers across member states.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Contaminant Type: Pathogen Testing Dominates Amid Growing GMO Concerns

Pathogen testing dominates with a 45.86% market share in 2025, as the region focuses on microbiological safety following significant foodborne illness outbreaks. Egyptian laboratories' implementation of MALDI-TOF MS technology for bacterial identification has achieved 75.8% species-level accuracy while reducing identification time to less than one hour. The demand for pesticide and residue testing remains consistent, driven by EU RASFF notifications and export market requirements. Allergen testing demand increases with the growth in processed food manufacturing.

GMO testing represents the fastest-growing segment with a 6.55% CAGR (2026-2031), due to increased use of bioengineered ingredients and export compliance requirements. The adoption of digital PCR technology for authenticity testing, as shown in oregano purity assessment studies, demonstrates the advanced analytical methods needed for GMO detection. Testing for other contaminants, including heavy metals and chemical residues, has improved through updates to the Codex Alimentarius MRL framework and regional standards harmonization. The integration of halal certification with traditional contaminant testing has created specialized testing protocols that generate higher pricing in the region's Muslim-majority markets.

By Technology: Immunoassay Leadership Challenged by PCR Innovation

Immunoassay-based technologies hold a 38.25% market share in 2025, driven by their cost-effectiveness and rapid turnaround times in resource-constrained laboratory environments across MEA. Lateral flow assays and ELISA platforms enable smaller laboratories to conduct reliable routine screening applications. The widespread adoption of these technologies is supported by established supply chains and minimal training requirements. Advanced immunoassay platforms with digital readout systems and multiplexed detection capabilities are gaining adoption in high-volume laboratories seeking enhanced throughput and data management capabilities. Polymerase Chain Reaction (PCR) technology shows the highest growth rate at 7.93% CAGR, expanding its applications in pathogen detection, GMO identification, and food authenticity verification.

Egyptian laboratories increasingly use real-time PCR for Salmonella detection, while multiplex PCR enables simultaneous species identification in meat products. Digital PCR represents an emerging technology frontier for quantitative applications, including oregano purity assessment and GMO quantification, offering improved precision and sensitivity. Chromatography and spectrometry maintain stable market positions through their essential role in pesticide residue analysis and nutritional labeling verification. Additional technologies, including biosensors and portable testing devices, are gaining market share by providing field-deployable solutions that reduce laboratory dependence and speed up decision-making processes.

By Application: Food Segment Dominance with Emerging Pet Food Growth

The food application segment holds 82.10% market share in 2025, encompassing comprehensive testing across meat and poultry, dairy, fruits and vegetables, processed foods, and crops. Meat and poultry testing generates significant volume through pathogen detection requirements, with Saudi Arabian slaughterhouse studies revealing high E. coli prevalence rates and antimicrobial resistance patterns that necessitate continuous monitoring and surveillance protocols.

Pet food and animal feed testing grows at a 7.05% CAGR, driven by premiumization trends. The incorporation of new ingredients, including insect proteins and algae-derived omega-3s, requires specialized testing for allergenicity, digestibility, and stability parameters. Kormotech's entry into Qatar and Nigeria demonstrates the regional expansion driving testing demand across the region. Modern processing technologies, including twin-screw extrusion and thermal retorting, create additional testing requirements for palatant stability and probiotic viability. The segment benefits from stringent import controls and growing consumer awareness of pet nutrition quality, driving demand for comprehensive analytical services, including mycotoxin detection, heavy metal analysis, and nutritional verification.

Geography Analysis

Saudi Arabia holds 27.88% market share in 2025, driven by comprehensive regulatory frameworks and high import volumes requiring testing verification. The Saudi Food and Drug Authority implements strict import control procedures, generating consistent testing demand across product categories. Halal certification requirements create additional testing needs. The kingdom's Vision 2030 economic diversification plans focus on food security and local production capacity, leading to increased testing infrastructure investment. ALS Arabia's network of five laboratories in Saudi Arabia and additional facilities in Oman and Bahrain indicates strong market demand for testing services in the GCC region.

Egypt records the highest growth rate at 7.74% CAGR, driven by processed food exports reaching USD 6.1 billion in 2024, representing 21% year-over-year growth. The National Food Safety Authority's 2023-2026 strategic plan strengthens laboratory capacity and regulatory enforcement. The establishment of Zewail City's food research center and the implementation of MALDI-TOF MS technology in laboratories reflect Egypt's investment in advanced testing capabilities. The country's position as a trade hub connecting Africa, Asia-Pacific, and Europe generates significant transit testing requirements.

The United Arab Emirates maintains market strength through Dubai's position as a regional trade center and Federal Law food safety regulations. Nigeria's market growth stems from population expansion and increasing food imports, while Morocco benefits from agricultural exports and European market access. Turkey's geographical position between Europe and Asia-Pacific creates specific testing needs for transit and re-export activities. The Rest of Middle East and Africa includes diverse markets ranging from established South African laboratories to developing Sub-Saharan African facilities supported by international development funding and technical assistance.

Competitive Landscape

The Middle East and Africa food safety testing market demonstrates moderate fragmentation, enabling both established global testing companies and specialized regional players to effectively gain and maintain market share. The market's diverse landscape creates opportunities for various participants to establish their presence while maintaining competitive dynamics that benefit end-users through service innovation and price competition.

Market leaders successfully utilize their extensive service portfolios and international accreditation standards to serve multinational food companies and export-oriented businesses, while regional firms strategically focus on their deep understanding of local regulatory frameworks and the provision of cost-competitive services. These distinct approaches to market participation ensure comprehensive coverage of testing needs across different market segments, from large-scale industrial operations to local food producers and processors.

Government certification programs create significant competitive advantages in the market, as evidenced by Intertek's strategic authorization as a Conformity Assessment Body by Iraq's COSQC and Saudi Arabia's SASO for vehicle inspection services, which clearly indicates the substantial expansion of regulatory compliance services throughout the region. Notable growth opportunities exist in mobile testing services, specialized halal certification testing, and comprehensive digital traceability solutions that effectively address and accommodate the region's specific regulatory requirements and unique cultural considerations. These emerging opportunities represent key areas for market expansion and service differentiation in the evolving Middle East and Africa (MEA) food safety testing landscape.

Middle East And Africa Food Safety Testing Industry Leaders

-

ALS Limited

-

Bio-Rad Laboratories

-

Eurofins Scientific S.E

-

Intertek Group plc

-

TÜV SÜD AG

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- October 2025: AmSpec Agri & Food plans to open a food safety testing laboratory in Dubai by autumn 2025. The facility, strategically positioned to serve the Middle East, Africa, and Asia-Pacific regions, will deliver local processing with reduced turnaround times. The laboratory will provide comprehensive testing services including microbiology, nutrition, and contaminant analysis using ISO-compliant methodologies. The facility will support food safety and product integrity through its advanced technical capabilities and expert regulatory support to deliver timely, reliable, and science-driven solutions.

- March 2025: SGS launched food safety testing services for lactic acid, acetic acid, and lactic acid bacteria in South Africa. These services enable food manufacturers to monitor and leverage fermentation processes that help inhibit spoilage pathogens such as Salmonella, E. coli, and Listeria. The testing capabilities support shelf life extension and food waste reduction through organic preservation methods, strengthening SGS's service offering in food safety, spoilage control, and sustainable preservation solutions.

- January 2024: Qiagen announced the establishment of its regional headquarters in Riyadh, Saudi Arabia. The company signed a Memorandum of Understanding with Saudi Arabia's Ministry of Health to support several public health and infection-control initiatives. The agreement includes developing a localized bioinformatics data center, implementing rapid diagnostic platforms, establishing preventative screening programs for cervical cancer and latent tuberculosis, and contributing to national health objectives.

Middle East And Africa Food Safety Testing Market Report Scope

Food safety testing is a scientific-based process that evaluates the safety of food based on microbiological, physical, or chemical composition. The Middle East & Africa Food Safety Testing Market is segmented by contaminant type into pathogen Testing, GMOs, pesticides, residue testing, and others. Based on the application the market studied is segmented into Pet Food & Animal Feed and Food. Based on technology, the market has been segmented into HPLC-based, LC-MS/MS-based, immunoassay-based, and other technologies. Based on geography the market has been segmented into Saudi Arabia, United Arab Emirates, Qatar, Egypt, South Africa, and the Rest of Middle East and Africa. The report offers market size and values in (USD million) during the forecasted years for the above segments.

By Contaminant Type

| Pathogen Testing |

| Pesticide and Residue Testing |

| GMO Testing |

| Allergen Testing |

| Other Contaminant Testing |

By Technology

| Polymerase Chain Reaction |

| Immunoassay-based |

| Chromatography and Spectrometry |

| Other Technologies |

By Application

| Pet Food And Animal Feed | |

| Food | Meat And Poultry |

| Dairy | |

| Fruits And Vegetables | |

| Processed Food | |

| Crops | |

| Other Foods |

By Geography

| South Africa |

| Saudi Arabia |

| United Arab Emirates |

| Nigeria |

| Egypt |

| Morocco |

| Turkey |

| Rest of Middle East and Africa |

| By Contaminant Type | Pathogen Testing | |

| Pesticide and Residue Testing | ||

| GMO Testing | ||

| Allergen Testing | ||

| Other Contaminant Testing | ||

| By Technology | Polymerase Chain Reaction | |

| Immunoassay-based | ||

| Chromatography and Spectrometry | ||

| Other Technologies | ||

| By Application | Pet Food And Animal Feed | |

| Food | Meat And Poultry | |

| Dairy | ||

| Fruits And Vegetables | ||

| Processed Food | ||

| Crops | ||

| Other Foods | ||

| By Geography | South Africa | |

| Saudi Arabia | ||

| United Arab Emirates | ||

| Nigeria | ||

| Egypt | ||

| Morocco | ||

| Turkey | ||

| Rest of Middle East and Africa | ||

Key Questions Answered in the Report

How big is the food safety testing market in Middle East and Africa today?

The food testing market size in the region reached USD 1.10 billion in 2026 and is forecast to climb to USD 1.42 billion by 2031.

Which contaminant category is currently tested the most?

Pathogen assays lead, accounting for 45.86% of 2025 revenue, reflecting urgent efforts to curb Salmonella, Listeria, and E. coli outbreaks.

What technology is growing the fastest for food analysis?

PCR platforms, especially real-time and digital PCR, are projected to expand at an 7.93% CAGR owing to precision in pathogen and GMO detection.

Which country is the fastest-growing market for food testing services?

Egypt is expected to post an 7.74% CAGR over 2026-2031 as exports surge and the National Food Safety Authority scales lab capacity.

Page last updated on: