Market Overview

| Study Period | 2021 - 2031 |

|---|---|

| Forecast Data Period | 2026 - 2031 |

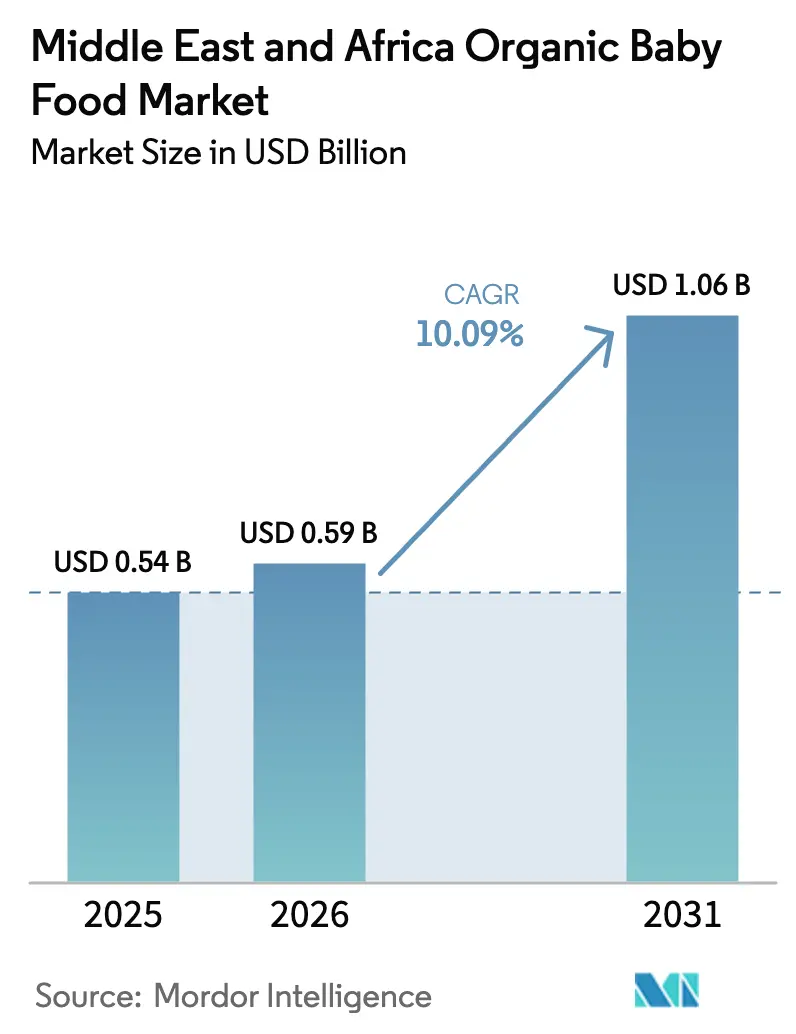

| Base Year Market Size (2025) | USD 0.54 Billion |

| Market Size (2026) | USD 0.59 Billion |

| Market Size (2031) | USD 1.06 Billion |

| Growth Rate (2026 - 2031) | 10.09% CAGR |

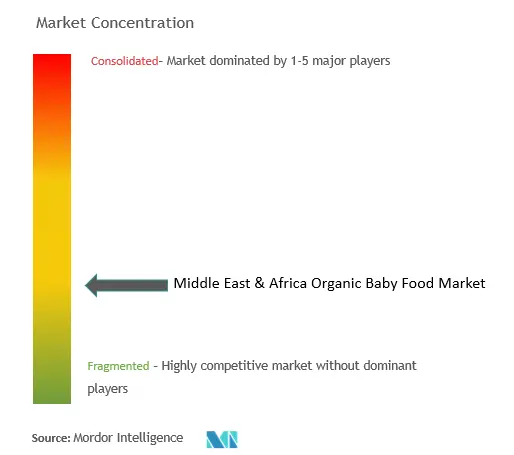

| Market Concentration | Medium |

Major Players

*Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. |

|

Middle East & Africa Organic Baby Food Market Analysis by Mordor Intelligence

The Middle East and Africa organic baby food market reached USD 542 million in 2025, is valued at USD 598 million in 2026, and is forecast to reach USD 1.06 billion by 2031, expanding at a CAGR of 13.18% over 2026-2031. Affluence is rising in the Gulf Cooperation Council (GCC) nations, and a budding middle class is emerging in Nigeria, Egypt, and South Africa. These shifts are steering infant nutrition priorities towards clean-label, pesticide-free products. In the Middle East and Africa's organic baby food market, premium organic milk formulas take center stage. Hospitals and pediatricians are now aligning their feeding guidelines with global protocols aimed at allergy prevention. E-commerce subscriptions, which bundle cross-border European brands with efficient last-mile delivery, have made it easier for millennial parents to search and switch. Meanwhile, in Saudi Arabia and the UAE, government incentives are promoting domestic organic farming, reducing reliance on imports. However, challenges remain: persistent price gaps, cold-chain bottlenecks in Sub-Saharan Africa, and the complexities of obtaining dual halal-organic certification. These factors segment demand based on income and geography. Yet, with rising health literacy and modernized retail, the potential market continues to expand.

Key Report Takeaways

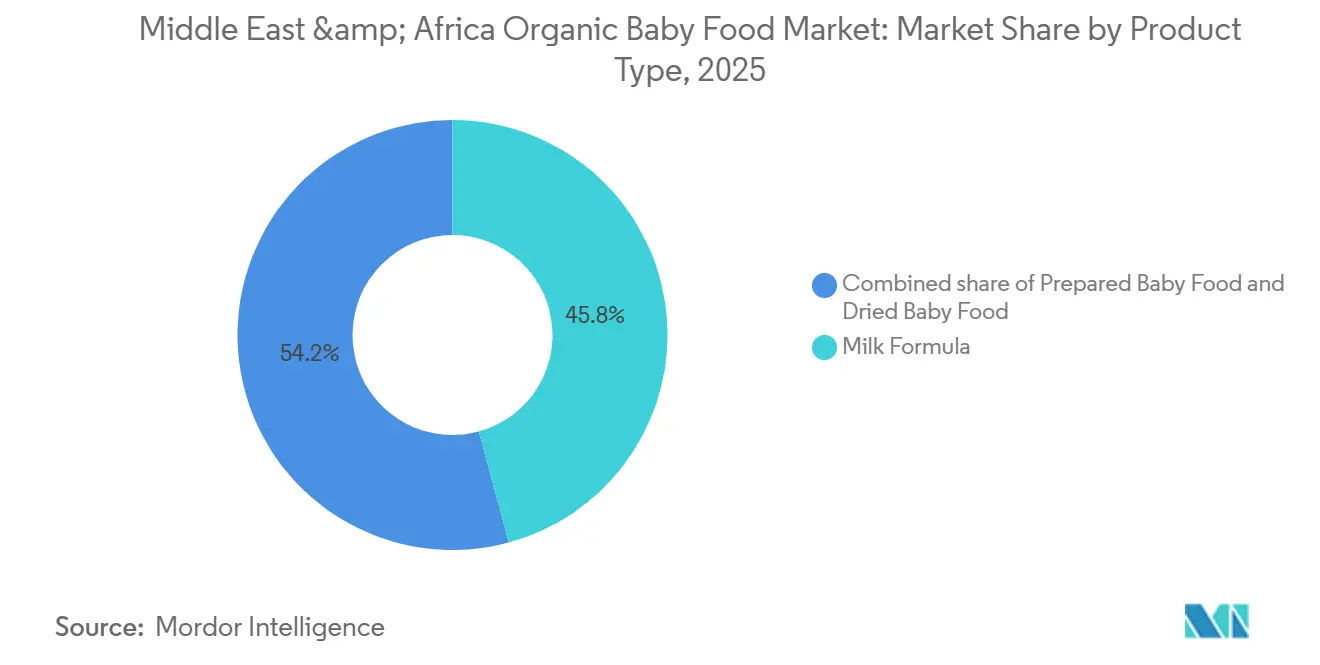

- By product type, milk formula led with a 46.24% share of the Middle East and Africa organic baby food market in 2025, while dried baby food is on track for the fastest 14.12% CAGR during 2026-2031.

- By age group, infants aged 6-12 months held 41.83% volume share in 2025; the 12-24 months cohort is projected to rise at a 13.71% CAGR through 2031.

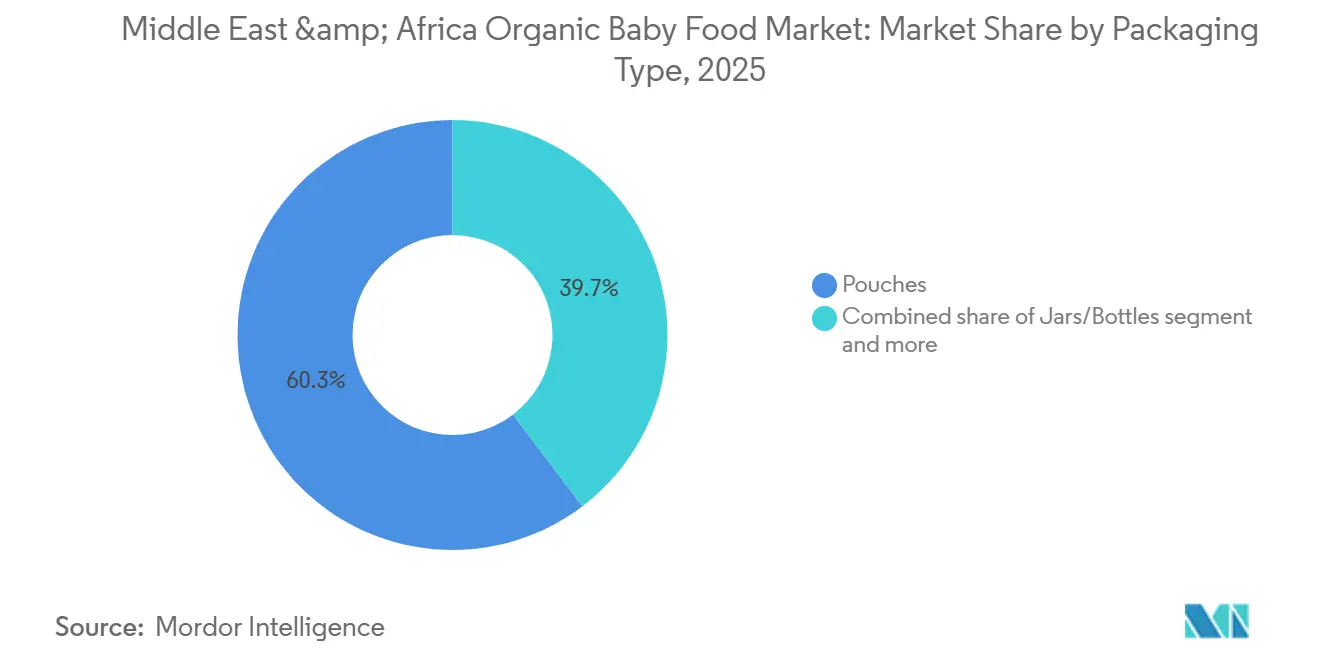

- By packaging, pouches captured 60.34% of 2025 revenue, whereas ambient-stable cartons are forecast to advance at 13.25% CAGR over 2026-2031.

- By distribution, supermarkets and hypermarkets retained 59.35% share in 2025, but online retail is expanding at a 14.35% CAGR through 2031.

- By geography, Saudi Arabia dominated with 32.46% share in 2025, and Nigeria is set for the region’s quickest 13.21% CAGR to 2031.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of January 2026.

Middle East & Africa Organic Baby Food Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Rising disposable incomes and urbanisation in GCC/African metros | +2.8% | Saudi Arabia, UAE, Nigeria, Egypt | Medium term (2-4 years) |

| Increasing female workforce participation boosting convenience demand | +2.4% | GCC, South Africa, urban Egypt | Short term (≤2 years) |

| Retail and e-commerce channel expansion widening organic reach | +2.1% | UAE, Saudi Arabia, Nigeria | Short term (≤2 years) |

| Heightened health-nutrition awareness over pesticides/additives | +1.9% | GCC, South Africa, urban Nigeria | Medium term (2-4 years) |

| GCC government incentives for domestic organic farming | +1.5% | Saudi Arabia, UAE, Oman | Long term (≥4 years) |

| Expat-led cross-border DTC brands targeting African diaspora | +1.2% | UAE, Saudi Arabia, South Africa | Medium term (2-4 years) |

| Source: Mordor Intelligence | |||

Rising disposable incomes and urbanization in GCC/African metros

Between 2020 and 2025, the GCC's per-capita GDP grew at an annual rate of 3.2%, outpacing global averages[1]Source: International Monetary Fund, Regional Economic Outlook, " elibrary.imf.com. This economic momentum has led to the emergence of dense retail hubs in cities like Riyadh, Dubai, Doha, Lagos, and Cairo. These hubs have become focal points for premium organic brands, which are increasingly securing prime shelf space due to rising consumer demand. Urban parents, especially those with dual incomes, are progressively viewing organic labels as a safeguard against food-safety recalls, driven by concerns over the quality and safety of conventional food products. This sentiment was notably heightened following an aflatoxin incident in Egypt in 2024, which underscored the risks associated with non-organic food options. In response to this growing demand, European firms, including HiPP and Holle, have strategically set up fulfillment hubs in Dubai. These hubs enable them to streamline their supply chains and reduce delivery times to just 24 hours, ensuring faster access to organic products for consumers. With an income elasticity of 1.4, a 10% increase in disposable income translates to a 14% surge in spending on organic products, highlighting the strong correlation between income growth and organic consumption. As a result, the organic baby food market in the Middle East and Africa is outpacing traditional staple categories, closely mirroring broader macro-economic trends and reflecting the region's evolving consumer preferences.

Increasing female workforce participation boosting convenience demand

From 2020 to 2025, female labor-force participation in the GCC surged from 23% to 37%[2]Source: GASTAT, "GASTAT Labor force participation rate of Saudi females reaches 36.2%, " stats.gov.sa . This significant increase reflects broader socio-economic changes, including evolving gender roles and government initiatives to encourage women’s employment. This shift has shortened household meal-preparation times, boosting the popularity of single-serve organic pouches, which offer a convenient and nutritious solution for busy families. In Saudi Arabia, the UAE, and urban Nigeria, working mothers are willing to pay a 25-30% premium for ready-to-feed formats that align with their daycare drop-off schedules, highlighting the growing demand for time-saving options. As a result, sales of organic pouches saw a 19% year-on-year increase in 2025, driven by their practicality and alignment with modern parenting needs. Notably, Danone’s bilingual Gerber packs found favor with expatriate caregivers, addressing the linguistic diversity of their target audience. Leading brands now offer subscriptions that auto-ship every fortnight, catering to the needs of busy households and ensuring a steady supply of essential products. This convenience is especially valued for the 6-12 months age group, fostering a cycle of repeat purchases and brand loyalty, as parents prioritize both ease and quality in their purchasing decisions.

Retail and e-commerce channel expansion widening organic reach

In 2025, hypermarkets in Saudi Arabia, the UAE, and Egypt expanded their grocery footprints by 8.3%, introducing dedicated organic aisles. In the GCC, e-commerce for baby products surged to a 22% penetration, driven by Amazon's subscribe-and-save discounts and Noon's bundled delivery offers. Cross-border platforms like iHerb enable Nigerian parents to tap into European SKUs, sidestepping hefty 40-60% distributor mark-ups. While these trends diminish the share of pharmacies and specialty stores, they simultaneously provide real-time reviews and traceability data, bolstering trust in the category. Brands harnessing omnichannel analytics are now fine-tuning promotion calendars based on shopping-cart cues, enhancing conversion rates during the crucial first-year feeding window, known for its high lifetime value. Additionally, the growing adoption of digital payment systems has further streamlined the e-commerce experience, encouraging repeat purchases.

Heightened health-nutrition awareness over pesticides/additives

Between 2020 and 2024, pediatric allergy cases in the GCC surged by 12%. In response, physicians began advocating for pesticide-free formulas. A peer-reviewed study in 2024 revealed that infants consuming organic formula had 23% fewer organophosphate metabolites in their excretions. This finding gained traction on Arabic-language parenting forums. In 2024, the Saudi Food and Drug Authority bolstered regulations by requiring on-pack disclosures of pesticide-residue tests. Influencers frequently highlight the contrast between conventional blends, often containing palm oil or added sugars, and organic lines boasting a “zero pesticide guarantee” from brands like Organix. Such health-centric narratives elevate the perceived value of these products, helping to mitigate the price sensitivity among middle- to high-income consumers. The growing awareness of pesticide-free options is reshaping purchasing decisions in the region.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Premium pricing limiting adoption among price-sensitive consumers | −1.8% | Nigeria, Egypt, Morocco | Short term (≤2 years) |

| Weak cold-chain and logistics in Sub-Saharan Africa | −1.4% | Nigeria, Kenya, wider SSA | Medium term (2-4 years) |

| Complex halal-organic dual-certification delays | −0.9% | GCC, Egypt, Morocco | Medium term (2-4 years) |

| Climate-linked volatility in organic raw-material supply | −0.7% | Morocco, Nigeria, Egypt | Long term (≥4 years) |

| Source: Mordor Intelligence | |||

Premium pricing limiting adoption among price-sensitive consumers

In Lagos and Nairobi, organic infant formula sells for USD 35-45 per 800-gram tin, nearly double the price of mainstream alternatives, limiting its adoption to the top-income quintile. A 28% surge in landed costs for European imports, due to Egypt's 2024 currency slide, led to downstream price hikes and a subsequent drop in unit sales. Smaller local processors struggle with scale efficiencies; for instance, Kenyan startup Orgaomi, hindered by working-capital gaps in raw-material procurement, operates at just 60% capacity. In both Morocco and Egypt, parents often dilute organic formula to extend its use or turn to homemade purees, undermining the formula's nutritional intent. Without significant price reductions, value-engineered SKUs, like 200-gram refill sachets, might be the sole solution to reach a wider income demographic. However, addressing supply chain inefficiencies could also help reduce costs and improve accessibility.

Weak cold-chain and logistics in Sub-Saharan Africa

Cold-chain coverage in Sub-Saharan Africa lags at just 28%, starkly contrasted by the GCC's 85%, hampering the distribution of organic yogurt and fresh purées. In Nigeria, retailers grapple with 12-hour power outages in rural areas, forcing them to limit offerings to shelf-stable pouches and powders[3]Source: International Energy Agency, " Africa Energy Outlook, " iea.org. Freight costs from Mombasa to Nairobi add an extra USD 0.80 per kilogram, and delays at customs can extend lead times by up to two weeks, straining working capital. In South Africa, episodes of load-shedding led Woolworths to adopt tetra-pak cartons. These cartons can handle ambient temperature spikes but sacrifice some flavor differentiation. Although pilot units for solar-powered refrigeration have proven technically viable, a significant funding gap of USD 200 million hinders nationwide roll-outs. Addressing these challenges is critical to improving the supply chain efficiency in the region.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Product Type: Formula Anchors, Dried Formats Accelerate

In 2025, organic milk formula accounted for 46.24% of the total revenue in the organic baby food market across the Middle East and Africa. This dominance is bolstered by robust endorsements from hospitals and ingrained infant-feeding practices, especially in the GCC region. Follow-up blends, now enriched with DHA and probiotics, are broadening the appeal of organic preferences beyond the initial breastfeeding phase, ensuring widespread acceptance among parents. Although the segment's high market penetration might temper growth rates, it's set to maintain around a 43% revenue share through 2031, thanks to ongoing medical endorsements. Specialty variants, such as hydrolyzed and lactose-free formulas, are gaining traction, albeit on a smaller scale, as they address increasing allergy concerns, further strengthening the category's resilience.

Dried baby food is the fastest-growing sub-segment, projected to expand at a 14.12% CAGR through 2031. Its popularity stems from portion-controlled cereals and freeze-dried powders, which provide shelf-stable convenience for busy households and working mothers. The market size for this category in the Middle East and Africa is anticipated to jump from USD X million in 2026 to USD Y million by 2031, with its revenue share rising from 22% to 27%. While prepared jarred purées enjoy popularity in premium retail channels across the GCC, they encounter logistical challenges in the wider Sub-Saharan markets, underscoring the scalability advantage of dried formats. This growth trajectory mirrors the increasing diversification as families introduce solid foods during their toddlers' developmental stages.

By Age Group: Weaning Peak, Toddler Momentum

In 2025, infants aged 6–12 months led the organic baby food market in the Middle East and Africa, making up 41.83% of the total volume. This surge in demand aligns with pediatricians endorsing complementary feeding, marking a pivotal shift from exclusive breastfeeding or formula. Brands adeptly seize this moment, distributing starter kits through maternity wards and hospital retail channels. Meanwhile, the 0–6 months segment bolsters this dominance by driving organic formula sales. However, campaigns promoting natural breastfeeding in South Africa and Egypt have tempered this growth slightly. Overall, the emphasis on the infant demographic underscores the region's deep-rooted commitment to early nutrition.

Meanwhile, the toddler segment, encompassing ages 12–24 months, is on a rapid ascent. It's projected to grow at a 13.71% CAGR through 2031, as parents increasingly opt for organic finger foods and snacks. This trend is a proactive measure against perceived chemical exposures, fueling demand for innovative offerings like puffed snacks, yogurt melts, and self-feeding purees. The market for this age group is poised for significant expansion, commanding more retail shelf space and branching out beyond traditional purees. As households transition from the infant to toddler stage, the younger cohort's volume share may wane, but this doesn't indicate a decline. Instead, it highlights a broader acceptance of organic baby food, solidifying its status as a staple across multiple stages of a child's growth.

By Packaging Type: Pouch Predominance, Carton Upswing

In 2025, pouches accounted for 60.34% of the revenue in the organic baby food packaging market across the Middle East and Africa. Their rise in popularity can be attributed to features like one-handed feeding convenience and resealable designs, catering to urban lifestyles. Brands such as HiPP are proactively addressing sustainability concerns with compostable innovations, countering the plastic-waste backlash while ensuring functionality remains intact. Meanwhile, glass jars bolster this leadership stance in premium retail channels within the GCC. Here, the allure of perceived purity drives shopper preference, even in the face of elevated freight and breakage costs. While bulk institutional tubs cater effectively to hospitals and daycares, their limited presence in retail underscores the dominance of pouches as the preferred format for consumers.

Ambient-stable cartons are emerging as the fastest-growing packaging choice, with projections indicating a robust 13.25% CAGR through 2031. This surge is largely a response to refrigeration challenges faced outside major metropolitan hubs, paving the way for wider market acceptance. Retailers are leaning towards cartons, not just for their recyclability but also for their visibility, with end-cap displays set to boost their market share in the Middle East and Africa's organic baby food sector into the low-to-mid-20s by 2031. While pouches will continue to lead, their dominance is expected to wane as regulatory pressures and evolving consumer sentiments push for material transitions. These trends underscore a broader evolution in packaging, steering towards sustainability while maintaining convenience across varied regional landscapes.

By Distribution Channel: Hypermarket Backbone, Digital Surge

In 2025, supermarkets and hypermarkets led the organic baby food market in the Middle East and Africa, accounting for 59.35% of the total revenue. Major chains like Carrefour, Lulu, and Panda dedicated up to 6 linear meters of shelf space to organic SKUs, enhancing visibility and driving impulse purchases. The introduction of private-label organics has not only intensified price competition but also made these products more accessible to mainstream shoppers. In urban areas of the GCC, pharmacies serve as advisory hubs, with pharmacists guiding brand choices for new parents. In contrast, specialty boutiques are losing traction, hampered by a limited product range and higher prices compared to mass retailers.

Online channels are the fastest-growing distribution segment, boasting a 14.35% CAGR through 2031. Their growth is fueled by offerings like free shipping thresholds, auto-replenishment subscriptions, and a wide variety of products, appealing to tech-savvy parents prioritizing convenience. By 2031, the e-commerce segment of the organic baby food market in the Middle East and Africa is set to surpass USD Z million, claiming an estimated 28% share of the channel. While hypermarkets will continue to be pivotal for trial purchases and bulk buys, they're increasingly adopting click-and-collect services to stay competitive with digital-only players. This trend highlights a significant shift towards omnichannel strategies, catering to the busy schedules of modern households.

Geography Analysis

Saudi Arabia, accounting for 32.46% of 2025's revenue, drives demand, thanks to Vision 2030 reforms. These reforms not only boosted the female workforce share to 37% but also introduced transparent pesticide-testing labels, favoring organic defaults. In 2025, the government allocated USD 120 million in subsidies to kick-start local ingredient cultivation, aiming for 25% self-sufficiency by 2028. However, outside major cities like Riyadh and Jeddah, price sensitivity limits market penetration. In response, brands are experimenting with refill sachets and smaller pack counts. The market's growth is further supported by increasing consumer awareness of organic product benefits.

The UAE, with a 24% market share in 2025, is driven by its 88% expatriate population's preference for familiar European labels. Dubai's robust logistics infrastructure, combined with a 26% penetration rate in baby-product e-commerce, ensures swift fulfillment cycles. Furthermore, domestic farming incentives that halve certification costs are nurturing a local supply, potentially stabilizing the market against currency fluctuations tied to imports. The UAE's strategic location as a trade hub also enhances its ability to cater to regional demand efficiently. Turkey, straddling the line as both a consumer and supplier, commands an 11% market share. This is bolstered by a 9.2% growth in organic acreage, aligning with EU subsidies. South Africa, holding a 9% share, benefits from established retail networks. However, recent load-shedding episodes have highlighted the advantages of ambient-stable packaging.

Meanwhile, Nigeria, though modest in 2025 revenue, boasts the region's most pronounced growth at a 13.21% CAGR. This surge is driven by a burgeoning middle class in Lagos and a rising advocacy for nutrition on social media. Turkey's strategic position as a bridge between Europe and Asia further strengthens its role in the market. Egypt, with a 7% share, and Morocco at 5%, grapple with currency and climatic challenges. These issues inflate import bills and diminish consumer purchasing power. The remaining dozen markets, including Kenya and Senegal, contribute an additional 12%. While they face nascent supply-chain challenges, they present significant opportunities for nimble entrants. Efforts to improve infrastructure and streamline supply chains in these markets are expected to unlock further growth potential.

Competitive Landscape

In the Middle East and Africa, the organic baby food market is moderately concentrated. While multinational giants leverage their scale, they don't monopolize the market. Nestlé, Danone, and Abbott dominate the infant formula segment, utilizing strategies like hospital sampling, halal compliance, and tailored advertising. European brands such as HiPP, Holle, and Hero Group command premium prices in GCC hypermarkets and expatriate-focused online shops. Regional players like Orgaomi from Kenya and Le Lionceau from Senegal tap into local supply chains but face challenges with working capital and fragmented farmer networks. These dynamics create a competitive environment where both global and regional players strive to maintain or grow their market share.

Technology is creating new advantages in the market. For instance, FrieslandCampina's blockchain pilot in the UAE boosts transparency at the batch level, reducing counterfeit risks. Similarly, Arla Foods employs AI for demand forecasting, cutting stock-outs in the GCC by 22% and ensuring product freshness. The focus on innovation leans heavily towards clean-label fortification: Abbott secured a patent in 2024 for an organic hydrolyzed-protein blend, while Nestlé is pursuing a probiotic-fortified cereal aimed at alleviating colic. These technological advancements not only enhance operational efficiency but also improve consumer trust and satisfaction.

While certification delays and compliance expenses pose challenges for new entrants, benefiting established players, cross-border direct-to-consumer (DTC) newcomers are reshaping the landscape. By eliminating distributor layers, they're able to offer competitive prices, capturing significant market value. This shift is particularly appealing to price-sensitive consumers who seek quality organic baby food at lower costs. As a result, the market is witnessing a gradual redistribution of value, with DTC models gaining traction and challenging traditional distribution channels.

Middle East & Africa Organic Baby Food Industry Leaders

-

Nestle SA

-

Hero Group

-

Arla Foods Group

-

Danone SA

-

Hipp Gmbh & Co.

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- February 2026: Following its halal accreditation in January 2026, Else Nutrition collaborated with Majid Al Futtaim to launch its plant-based organic toddler formula in 85 Carrefour hypermarkets across the UAE and Saudi Arabia.

- January 2026: Nestlé inaugurated a USD 45 million organic baby-food facility in Dubai Industrial City, aiming to meet the growing demand for organic baby food in the region. This investment increases the company's regional production capacity by 30% and aligns with its sustainability goals by committing to sourcing 40% of its ingredients locally by 2028.

- November 2025: Danone acquired a 60% stake in Le Lionceau, a Senegalese company specializing in baby food products. This strategic move enables Danone to strengthen its presence in the West African market by leveraging Le Lionceau's established distribution network. Additionally, the acquisition ensures a reliable supply of organic millet, a key ingredient in the company's product offerings.

- October 2025: HiPP has launched a TÜV-certified compostable pouch in the UAE, aligning with the region's increasing focus on sustainable packaging solutions. This development comes as regulators in the UAE deliberate on implementing a ban on non-recyclable food packaging by 2027.

Middle East & Africa Organic Baby Food Market Report Scope

Organic baby foods are manufactured by using ingredients that are grown or processed without synthetic fertilizers or pesticides. The Middle East and Africa organic baby food market is segmented by product type, distribution channel, and geography. By product type, the segmentation includes milk formula, prepared baby food, dried baby food, and others. By distribution channel, the market is segmented into supermarkets/hypermarkets, convenience stores, online retail stores, and other distribution channels. It provides an analysis of emerging and established economies in the Middle East and Africa, including the United Arab Emirates, Saudi Arabia, South Africa, and the Rest ofthe Middle East and Africa. For each segment, the market sizing and forecasts have been done on the basis of the value (in USD million).

By Product Type

| Milk Formula | Infant Formula |

| Follow-up Milk Formula | |

| Grow-up Milk Formula | |

| Specialty Formula | |

| Prepared Baby Food | |

| Dried Baby Food |

By Age Group

| 0-6 Months |

| 6-12 Months |

| 12-24 Months |

| More than 24 Months |

By Packaging Type

| Pouches |

| Jars/Bottles |

| Tetra-Pak/Cartons |

| Others |

By Distribution Channel

| Supermarkets/Hypermarkets |

| Pharmacies and Drugstores |

| Specialty Stores |

| Onlnie Retailers |

| Other Distribution Channels |

Geography

| Saudi Arabia |

| United Arab Emirates |

| Turkey |

| South Africa |

| Nigeria |

| Egypt |

| Morocco |

| Rest of Middle East and Africa |

| By Product Type | Milk Formula | Infant Formula |

| Follow-up Milk Formula | ||

| Grow-up Milk Formula | ||

| Specialty Formula | ||

| Prepared Baby Food | ||

| Dried Baby Food | ||

| By Age Group | 0-6 Months | |

| 6-12 Months | ||

| 12-24 Months | ||

| More than 24 Months | ||

| By Packaging Type | Pouches | |

| Jars/Bottles | ||

| Tetra-Pak/Cartons | ||

| Others | ||

| By Distribution Channel | Supermarkets/Hypermarkets | |

| Pharmacies and Drugstores | ||

| Specialty Stores | ||

| Onlnie Retailers | ||

| Other Distribution Channels | ||

| Geography | Saudi Arabia | |

| United Arab Emirates | ||

| Turkey | ||

| South Africa | ||

| Nigeria | ||

| Egypt | ||

| Morocco | ||

| Rest of Middle East and Africa |

Key Questions Answered in the Report

What market share does milk formula hold?

Milk formula leads with 64% share of the Middle East & Africa organic baby food market in 2025.

How fast is the overall market growing?

The market is expanding at a 12.4% CAGR from 2025 to 2031.

What growth is expected for infant foods?

Infant foods aged 6-12 months project 41% volume growth by 2025, while 12-24 months see 13.7% rise.

What about packaging trends?

Pouched products captured 60% of 2025 sales, with ambient stable cartons forecast to advance 13%.

Page last updated on: