Market Overview

| Study Period | 2021 - 2031 |

|---|---|

| Forecast Data Period | 2026 - 2031 |

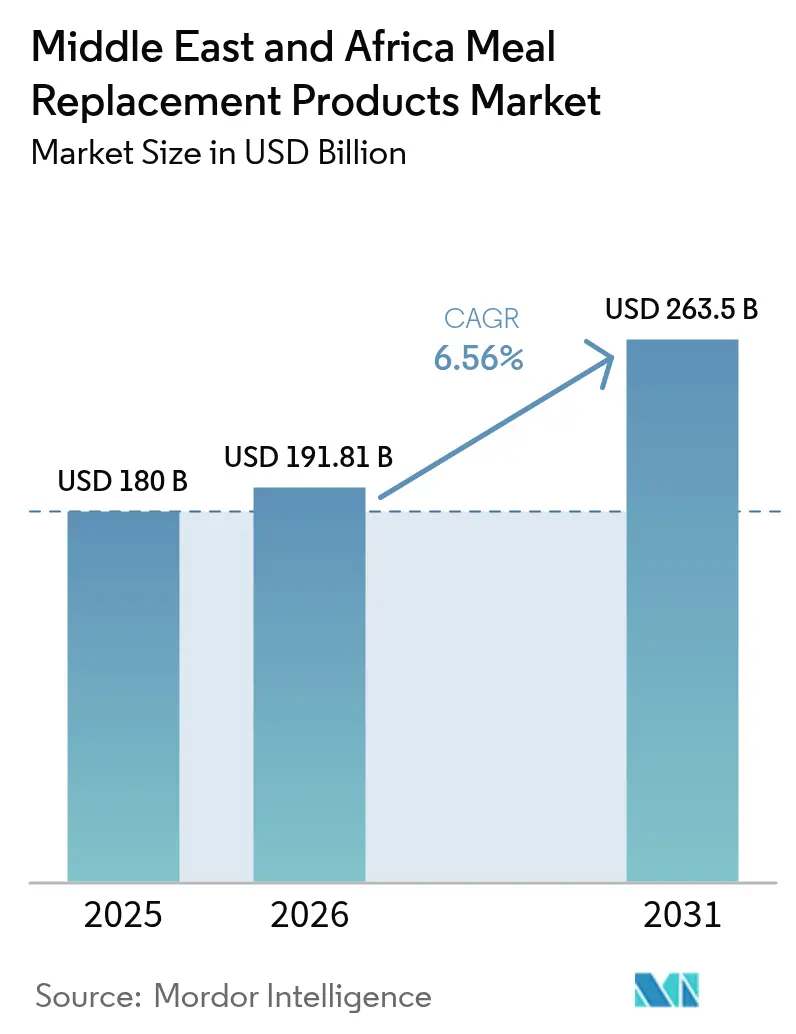

| Base Year Market Size (2025) | USD 180 Billion |

| Market Size (2026) | USD 191.81 Billion |

| Market Size (2031) | USD 263.5 Billion |

| Growth Rate (2026 - 2031) | 6.56% CAGR |

| Market Concentration | Medium |

Major Players

*Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. |

|

Middle East And Africa Meal Replacement Products Market Analysis by Mordor Intelligence

The Middle East and Africa meal replacement products market size is expected to grow from USD 180 million in 2025 to USD 191.81 million in 2026 and is forecast to reach USD 263.5 million by 2031 at 6.56% CAGR over 2026-2031. This trajectory reflects a confluence of urbanization-driven time scarcity, regulatory modernization across Gulf Cooperation Council states, and the pivot by multinational nutrition brands toward localized manufacturing footprints. Nigeria is the quickest climber, propelled by an 8.41% CAGR through 2030 as a youthful population and rising disposable incomes boost functional-food spend. South Africa retained deep-rooted momentum, supported by dense modern retail and consumer familiarity with fortified foods, while Saudi Arabia’s USD 7 billion manufacturing pledge from Nestlé signals long-term localization of supply chains. Packaging innovations that tolerate 45°C warehouse heat, plus corporate wellness programs that subsidize on-site nutrition, are widening addressable use cases and encouraging multinational brand entry.

Key Report Takeaways

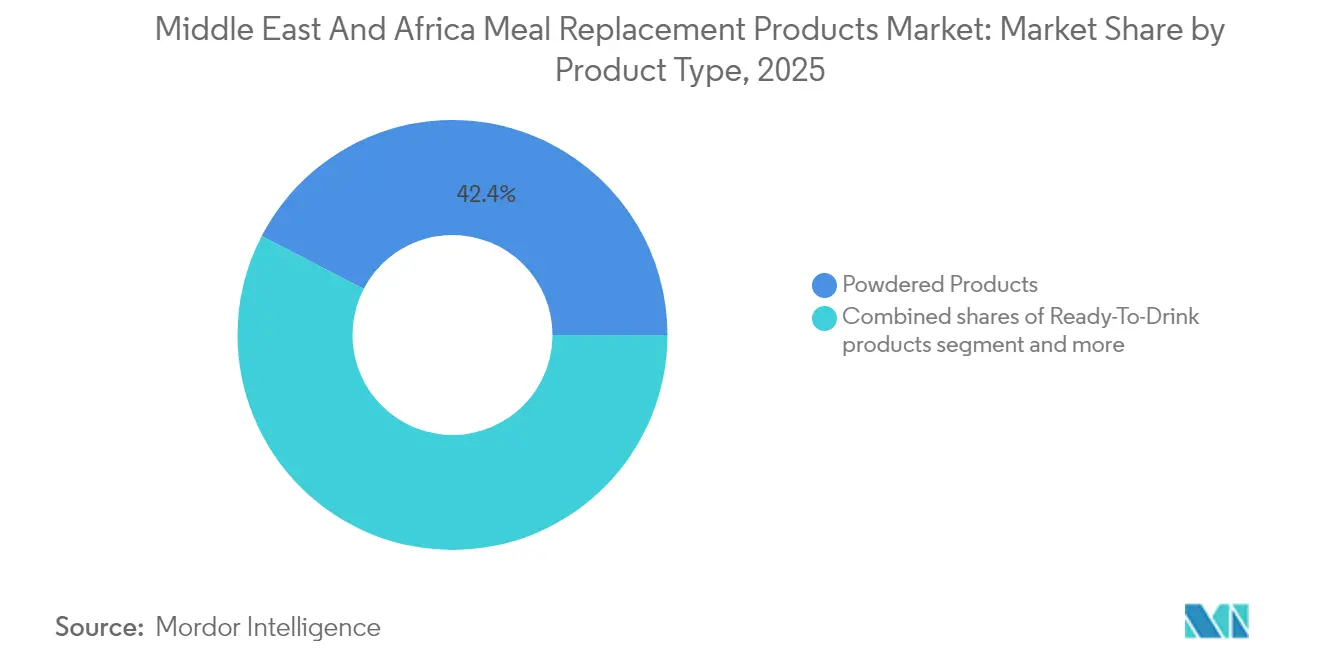

- By product type, powdered products captured 42.38% of the meal replacement products market share in 2025. Ready-to-drink formats are expanding at a 7.12% CAGR to 2031.

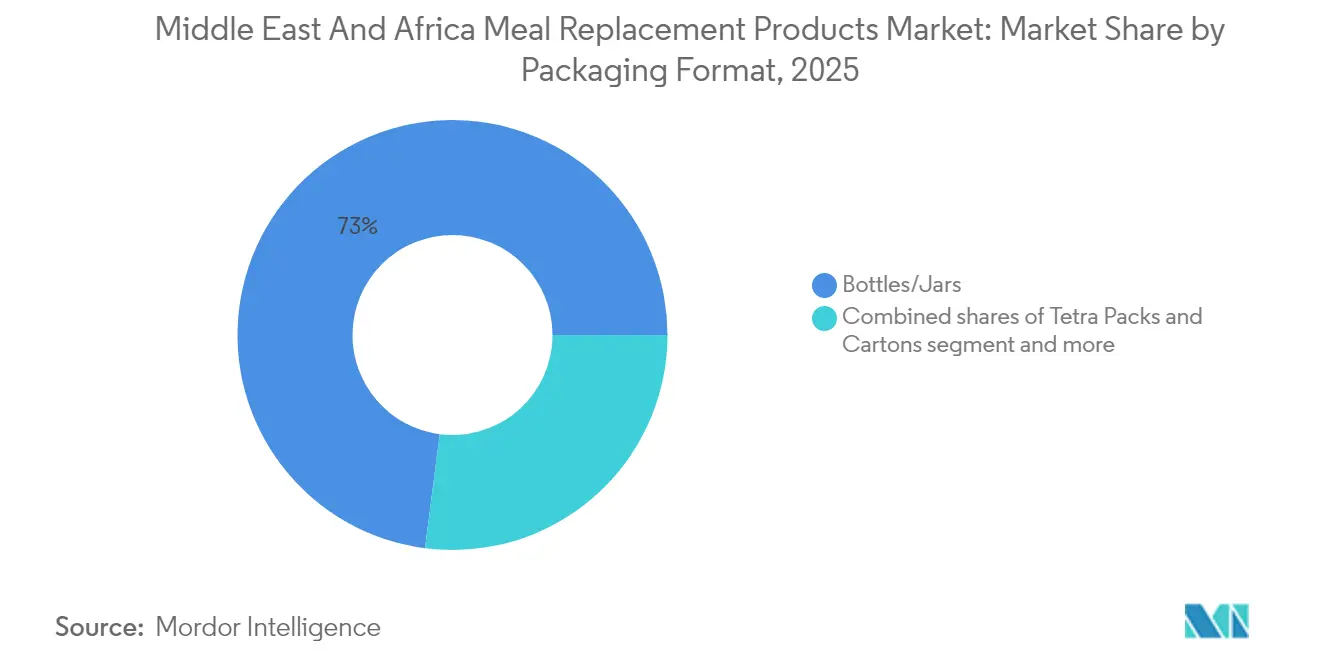

- By packaging format, bottles and jars held 72.96% of the meal replacement products market size in 2025, and Tetra packs and cartons are forecast to grow at a 6.88% CAGR to 2031.

- By distribution channel, supermarkets and hypermarkets controlled 50.61% of 2025 revenue, while online retailers recorded the highest projected 7.35% CAGR through 2031.

- By geography, Nigeria posts the strongest 8.02% CAGR through 2031; South Africa accounted for 12.31% of regional revenue in 2025.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of 2026.

Middle East And Africa Meal Replacement Products Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Demand for convenient and nutritious meal options driven by busy lifestyles | +1.8% | Global, with peak intensity in UAE, Saudi Arabia, South Africa urban centers | Medium term (2-4 years) |

| Increased health and fitness awareness spurs growth in protein-enriched meal replacements | +1.5% | Global, strongest in GCC states and South Africa | Long term (≥ 4 years) |

| Expansion of e-commerce platforms enhances global accessibility and brand visibility | +1.3% | Global, accelerating in Nigeria, Kenya, and Saudi Arabia | Short term (≤ 2 years) |

| Workplace wellness initiatives promote meal replacements as healthy on-the-go choices | +0.9% | UAE, Saudi Arabia, South Africa corporate hubs | Medium term (2-4 years) |

| Rising awareness of portion control and calorie management supports meal replacement usage | +0.8% | GCC states, South Africa, Egypt | Long term (≥ 4 years) |

| Food technology innovations enhance taste, texture, shelf life, and nutritional value | +0.7% | Global, with R&D concentration in South Africa and the UAE | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

Demand for Convenient and Nutritious Meal Options Driven by Busy Lifestyles

Urbanization rates exceeding 80% in the UAE and 67% in South Africa are compressing meal-preparation windows, indicating that Middle Eastern consumers now prioritize convenience over price when selecting packaged foods. This behavioral shift is amplified by the rise of dual-income households and extended commute times in megacities like Lagos and Johannesburg, where traffic congestion averages 2 hours daily. Tiger Brands capitalized on this trend in October 2023 by launching its Jungle Oats Drink range, a ready-to-drink, plant-based breakfast targeting snackification and affordability, positioning it as a functional on-the-go solution with five flavor variants tied to specific health claims such as heart wellness and immune support. The convergence of time scarcity and nutritional awareness is pushing brands to reformulate products with whole-grain bases and fortified micronutrient profiles, addressing the dual mandate of speed and health that traditional quick-service meals fail to satisfy. Regulatory frameworks in Saudi Arabia and the UAE, which require nutrient-density labeling under SFDA and Dubai Municipality guidelines, are further incentivizing manufacturers to elevate formulation standards rather than compete solely on convenience [1]Source: SFDA Saudi Arabia, "Regulatory frameworks", sfda.gov.sa.

Increased Health and Fitness Awareness Spurs Growth in Protein-Enriched Meal Replacements

GCC obesity prevalence, 40% among females and 24% among males, has catalyzed government-led health campaigns and private-sector wellness programs, creating a structural tailwind for protein-enriched meal replacements. Nestlé's 2024 launch of Milo Pro in Nigeria, fortified with three times the protein of standard variants, exemplifies how multinationals are leveraging sports-nutrition science to reposition legacy brands for fitness-conscious demographics. The adoption of GLP-1 medications such as Ozempic among affluent UAE consumers is paradoxically boosting demand for high-protein meal replacements. South Africa's Future Life brand has responded by expanding its High Protein Shake line, which delivers 16 grams of protein per 256-milliliter serving via a SmartProtein3D blend of soy isolate, whey concentrate, and calcium caseinate, targeting pregnant women, athletes, and executives. This protein-centric pivot is further supported by the proliferation of CrossFit gyms and boutique fitness studios across Riyadh and Cape Town, where trainers actively recommend meal replacements as post-workout recovery tools, embedding these products into daily fitness rituals rather than positioning them as emergency meal substitutes.

Expansion of E-Commerce Platforms Enhances Global Accessibility and Brand Visibility

iHerb's 2023 partnership with CJ Logistics to construct a 30,000-square-meter, climate-controlled fulfillment center in Riyadh's Integrated Logistics bonded zone represents a watershed moment for meal replacement distribution across the Middle East and Africa. The facility, operational since mid-2024, enables next-day delivery of over 30,000 SKUs to 19 MENA countries, slashing lead times from 14 days to 48 hours and reducing shipping costs by 35% through the elimination of European transshipment nodes. This infrastructure upgrade coincides with online grocery growth in the UAE through 2032, driven by 71% of consumers expressing interest in personalized digital offers and 60% seeking AI-powered nutrition recommendations. The July 2024 partnership between iHerb and The Vitamin Shoppe further densified the digital ecosystem, making 250-plus proprietary sports-nutrition and meal-replacement SKUs available across 180 countries, with staged rollouts targeting Nigeria and Kenya, where mobile-commerce penetration exceeds a significant percentage. Critically, e-commerce platforms are bypassing traditional distributor markups, which can reach 40% in sub-Saharan Africa, allowing brands to reinvest savings into localized marketing and influencer partnerships that resonate with younger, digitally native cohorts. The shift also mitigates cold-chain vulnerabilities in regions with unreliable electricity grids, as ambient-stable powdered and bar formats dominate online assortments.

Workplace Wellness Initiatives Promote Meal Replacements as Healthy On-the-Go Choices

Corporate health programs in the UAE and Saudi Arabia are mandating on-site wellness facilities and subsidized nutrition counseling, with employers increasingly stocking meal replacements in office pantries as part of broader absenteeism-reduction strategies. Mediclinic City Hospital's obesity management program in Dubai, which integrates bariatric dieticians and exercise therapists, explicitly recommends portion-controlled meal replacements for patients enrolled in its multidisciplinary weight-reduction pathway. This clinical endorsement lends credibility to products like Abbott's Ensure and Glucerna, which are positioned as medical nutrition rather than convenience foods, allowing brands to command 30% price premiums over standard meal replacements. South African mining conglomerates and logistics firms are piloting meal-replacement vending machines at remote work sites, addressing the dual challenges of limited food access and high rates of non-communicable diseases among shift workers. The integration of meal replacements into workplace wellness ecosystems is creating a recurring-revenue model, as employers negotiate bulk-purchase agreements with brands in exchange for nutritional tracking data that informs broader health interventions. This B2B channel remains underpenetrated in Nigeria and Egypt, where informal employment dominates, but represents a high-margin opportunity for brands willing to invest in corporate partnerships and compliance with occupational health standards.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Consumer concerns about artificial additives and preservatives affect product acceptance | -0.6% | Global, most acute in South Africa and UAE | Medium term (2-4 years) |

| Presence of common allergens restricts market growth | -0.5% | Global, regulatory complexity highest in GCC and South Africa | Long term (≥ 4 years) |

| Product recalls and quality issues erode consumer trust and loyalty | -0.4% | Global, reputational risk concentrated in Nigeria and Egypt | Short term (≤ 2 years) |

| Challenges in replicating traditional meal experience impact repeat purchases | -0.3% | Middle East and North Africa, less pronounced in South Africa | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

Consumer Concerns About Artificial Additives and Preservatives Affect Product Acceptance

The clean-label movement, which gained traction in Western markets, is now reshaping formulation priorities across the Middle East and Africa. Future Life's Smart Food Zero line, launched in 2024, addresses this demand by eliminating added cane sugar and incorporating natural sweeteners like erythritol and sucralose, while maintaining a low glycemic index and fortifying with 22 vitamins and minerals. However, the reformulation imperative collides with shelf-life requirements in high-temperature climates, where ambient storage can reach 45 degrees Celsius in Gulf warehouses, necessitating preservatives or advanced packaging technologies. FDA guidance on "natural" claims remains ambiguous, creating regulatory arbitrage opportunities for brands that market in multiple jurisdictions but also exposing them to consumer backlash when formulations vary by country [2]Source: U.S Food & Drug Administration, "FDA Seizes 7-OH Opioids to Protect American Consumers", fda.gov. The tension between clean-label aspirations and functional stability is pushing R&D investments toward plant-based preservatives and high-pressure processing techniques, though these innovations add to production costs, squeezing margins in a price-sensitive region where 53% of UAE consumers prioritize value over brand loyalty.

Presence of Common Allergens Restricts Market Growth

Milk, soy, and wheat, the foundational ingredients in most meal replacements, are among the nine major allergens mandated for disclosure under FDA regulations, with sesame added as the ninth allergen in 2023, complicating formulation for brands targeting Middle Eastern consumers, where tahini and sesame oil are dietary staples. Future Life's Smart Food Original contains both soy and cow's milk (sodium caseinate) and is manufactured in a facility that processes gluten and wheat, requiring prominent allergen warnings that deter an estimated 12-15% of potential buyers who self-identify as lactose intolerant or gluten sensitive. Cross-contamination risks during manufacturing further constrain market access, as even trace allergen presence can trigger recalls and liability claims in jurisdictions with strict enforcement, such as South Africa's Department of Health. The regulatory fragmentation across MENA, where Saudi Arabia's SFDA, Nigeria's NAFDAC, and Egypt's NFSA each impose distinct labeling thresholds, forces brands to maintain multiple SKU variants or accept exclusion from high-growth markets. Plant-based alternatives using pea protein and oat bases are emerging as workarounds, exemplified by Nuitree's UAE factory launch in 2024, but these formulations struggle to match the amino-acid completeness and mouthfeel of dairy-based products, limiting appeal among performance-oriented consumers who prioritize protein quality over allergen avoidance.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Product Type: Ready-to-Drink Formats Capture Urban Demand

Ready-to-drink products are expanding at a 7.12% CAGR through 2031, outpacing powdered products despite the latter's 42.38% share of 2025 revenue, as single-serve convenience aligns with the snackification trend. Huel's 2025 launch of Daily Greens RTD in GCC markets, distributed via Carrefour and Lulu Hypermarket, exemplifies how brands are leveraging modern trade's cold-chain infrastructure to position liquid formats as premium, grab-and-go solutions for office workers and gym-goers. Powdered products retain dominance through cost advantages. A 500-gram Future Life Smart Food pouch priced at ZAR 46.99 (USD 2.60) delivers 10 servings versus ZAR 9.99 (USD 0.55) per single RTD unit, making them the preferred format for price-sensitive Nigerian and Egyptian households, where bulk purchasing drives most nutrition-supplement sales. Nutritional bars and soups occupy niche positions, with bars gaining traction in South Africa's convenience-store channel as Clicks and Dis-Chem expand health-food sections, while soups remain underdeveloped due to cultural preferences for hot, freshly prepared broths that meal-replacement formats struggle to replicate authentically.

Tiger Brands' October 2023 Jungle Oats Drink launch, South Africa's first locally produced RTD oat-based meal replacement, signals a strategic pivot toward plant-based, ambient-stable liquids that bypass cold-chain constraints while capturing the majority of South Africans who value affordable, natural-ingredient foods. The five-SKU range, with functional claims spanning heart wellness to digestive health, demonstrates how incumbents are leveraging established brand equity to cross-sell into adjacent meal-replacement categories. Powdered formats are innovating through dual-pouch technology, as seen in Future Life's High Protein Shake, which pre-packages purified water and powder in a resealable pouch to eliminate mixing hassles while maintaining ambient shelf life. This hybrid approach bridges the convenience gap between traditional powders and RTD liquids, though it adds 25% to packaging costs, limiting adoption outside premium urban segments.

By Packaging Format: Tetra Packs Gain Ground in Hot Climates

Bottles and jars commanded 72.96% of 2025 packaging revenue, yet tetra packs and cartons are accelerating at 6.88% CAGR, driven by ambient-shelf-life advantages that reduce cold-chain dependency in regions where electricity access remains intermittent. Nigeria's grid reliability averages 4 hours daily in rural areas . Tetra Pak's aseptic technology, which enables 12-month ambient storage for liquid meal replacements, is particularly compelling for brands targeting sub-Saharan distribution networks where refrigerated transport adds 30-40% to logistics costs. Pouches are carving a share in e-commerce channels, where lightweight packaging reduces shipping costs by 20% and minimizes breakage during last-mile delivery, a critical consideration in Nigeria and Kenya, where road infrastructure remains underdeveloped.

The sustainability narrative is gaining regulatory tailwinds, as South Africa's Extended Producer Responsibility regulations, effective 2024, mandate that brands fund 100% of post-consumer packaging recycling, making lightweight pouches economically attractive according to the South African Department of Environment. Bottles and jars retain dominance in supermarket and hypermarket channels, where shelf presence and perceived value drive purchasing decisions, particularly for high-protein RTD shakes priced above USD 3 per unit. The packaging bifurcation mirrors broader market segmentation, with premium urban consumers gravitating toward glass bottles that signal quality and eco-consciousness, while mass-market rural buyers prioritize affordability and durability, favoring plastic jars that withstand rough handling in informal retail environments.

By Distribution Channel: Online Retailers Disrupt Traditional Trade

Online retailers are expanding at 7.35% CAGR through 2031, the fastest among all distribution channels, yet supermarkets and hypermarkets retained 50.61% of 2025 sales, underscoring the enduring importance of physical retail in a region where 60% of consumers prefer to inspect products before purchase. iHerb's Riyadh fulfillment center, operational since mid-2024, is recalibrating this dynamic by offering 48-hour delivery across 19 MENA countries, effectively collapsing geographic barriers that previously confined premium meal replacements to Dubai and Riyadh's upscale grocery chains. Convenience stores and specialty stores are losing share, pressured by limited SKU depth and inability to compete on price with online platforms that aggregate demand and negotiate bulk discounts directly with manufacturers.

Supermarkets and hypermarkets are defending their position through experiential retail, with Carrefour UAE and Lulu Hypermarket installing in-store nutrition kiosks staffed by dieticians who recommend meal replacements as part of personalized wellness plans, converting 18% of consultations into immediate purchases. Shoprite and Clicks in South Africa are leveraging loyalty programs. ClubCard members receive 3-for-2 promotions on Future Life products to lock in repeat buyers and offset online price transparency. The distribution battleground is intensifying as brands pursue omnichannel strategies, with Nestlé MENA distributing Optifast through 85,000 Moroccan retail outlets while simultaneously listing on Amazon.ae and Noon.com to capture digitally native millennials. This dual-track approach requires sophisticated inventory management and pricing discipline to prevent channel conflict, as retailers demand exclusivity or margin protection in exchange for premium shelf placement.

Geography Analysis

Nigeria's 8.02% CAGR through 2031 positions it as the region's fastest-growing market, propelled by a median age of 18 years, urbanization accelerating at 4% annually, and rising middle-class incomes in Lagos, Abuja, and Port Harcourt that are expanding the addressable consumer base for packaged nutrition, according to the World Bank. Nestlé Nigeria's 2023 expansion to 223,923 retail outlets, coupled with launches of NIDO Milk & Soya and MAGGI Soya Chunks fortified with plant protein, demonstrates how multinationals are localizing formulations to address micronutrient deficiencies. Nigeria's 2024 micronutrient survey revealed 40% of children under five suffer from vitamin A deficiency. However, price sensitivity remains acute, with powdered milk imports totaling USD 267 million in 2024 signaling consumer preference for bulk, cost-effective formats over premium RTD meal replacements, according to the USDA Nigeria.

The regulatory environment is tightening, as NAFDAC introduced stricter allergen-labeling requirements in 2024, forcing brands to reformulate or accept exclusion from formal retail channels that account for majority of urban sales. South Africa held 12.31% of regional revenue in 2025, anchored by a mature retail infrastructure spanning Shoprite, Clicks, and Dis-Chem, which collectively operate over 3,000 stores and provide unparalleled distribution reach for brands like Future Life and Tiger Brands. The market is characterized by high obesity rates (27% of adults) and sophisticated consumer awareness of nutritional labeling, creating demand for science-backed formulations such as Future Life's Moducare-infused Smart Food, which claims immune-support benefits via patented plant sterols licensed exclusively from Essential Sterolin Products.

Saudi Arabia and the UAE represent the region's highest per-capita consumption markets, driven by expatriate populations exceeding 80% in the UAE and government-led health campaigns targeting GCC obesity rates of 40% among females. The UAE's online grocery CAGR of 21.6% through 2032, coupled with 71% of consumers seeking personalized digital offers, is pushing brands to integrate AI-powered nutrition apps that recommend meal replacements based on fitness-tracker data and dietary preferences. Regulatory frameworks under SFDA and Dubai Municipality mandate nutrient-density labeling and Halal certification, creating compliance costs that favor established multinationals over smaller regional entrants but also ensuring product quality that builds consumer trust. The Rest of the Middle East and Africa, encompassing Egypt, Morocco, Algeria, and Kenya, contributes the balance of regional revenue, with distribution fragmentation and currency volatility constraining growth but offering white-space opportunities for brands willing to navigate complex import tariffs and partner with local distributors who command informal retail networks.

Competitive Landscape

The market's moderate concentration score reflects a competitive landscape where multinational nutrition conglomerates, Abbott, Nestlé, Herbalife, and Glanbia coexist with regional specialists such as Future Life, Tiger Brands, and Nutritech, each pursuing distinct strategies that range from clinical positioning to mass-market affordability. PepsiCo's 2023 acquisition of Future Life's remaining 50% stake, approved by South Africa's Competition Tribunal with employee-ownership undertakings, illustrates how global players are leveraging M&A to secure distribution access and innovation pipelines rather than building greenfield operations. Conversely, Glanbia's 2024-2025 divestitures of SlimFast and Body & Fit signal a strategic retreat from consumer-facing meal replacements toward B2B ingredients and sports-nutrition concentrates, creating market-share opportunities for brands willing to acquire orphaned SKUs and distribution contracts.

Opportunities are emerging in workplace wellness channels, where corporate bulk-purchase agreements remain underpenetrated outside South Africa and the UAE, and in plant-based formats, where Nuitree's 2024 UAE factory launch positions it to capture Halal-certified, allergen-free demand that incumbent dairy-based products cannot address. Technology deployment is bifurcating the competitive field, with leaders like Abbott investing in nutrient-stability research to extend the shelf life of liquid medical nutrition products in high-temperature climates, while challengers like Huel are leveraging direct-to-consumer e-commerce and subscription models to bypass distributor markups and capture recurring revenue.

Nestlé's Quality Assurance Center in Dubai, ISO 17025:2005 accredited and servicing 19 MENA countries, exemplifies how incumbents are using regulatory compliance infrastructure as a competitive moat, enabling faster product approvals and reducing time-to-market for localized formulations. Smaller players are responding through ingredient innovation, such as Future Life's exclusive licensing of Moducare plant sterols and Tiger Brands' whole-grain oat base, which differentiate products on functional-health claims rather than competing solely on protein content or price. The competitive intensity is likely to escalate as Saudi Arabia's USD 7 billion Nestlé investment commitment and iHerb's Riyadh fulfillment center operational scale attract new entrants seeking to capitalize on infrastructure improvements and regulatory modernization that lower barriers to market entry.

Middle East And Africa Meal Replacement Products Industry Leaders

-

Herbalife Nutrition Ltd.

-

Abbott

-

Nestlé S.A.

-

The Simply Good Foods Company

-

Glanbia plc

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- December 2024: JO-MO introduced a series of premium protein bars, unique in Israel, featuring no sugar, no dairy, and low available carbohydrates. The series included three different flavors, offered as single bars (60 grams), each containing 20 grams of high-quality soy protein, with a crunchy texture and exceptional taste: a protein bar with hazelnut butter and hazelnut pieces, a milk chocolate and hazelnut-flavored protein bar, and a protein bar with peanut butter and cacao nibs.

- April 2024: FULFIL Chocolate Protein Bars, a globally recognized brand in delicious and nutritious snacking, launched in South Africa and became available at Spar Stores and Clicks nationwide. This range of indulgent chocolate bars with zero guilt combined decadent taste with functional nutrition and aimed to revolutionize snacking for health-conscious and ‘chocaholic’ consumers worldwide, extending its reach to South Africa.

- December 2023: Carabao Energy Drink successfully expanded its international market presence in Kuwait during the fourth quarter of 2023, driven by the exponential growth in demand for energy drinks in the Middle East. A key strategy behind the successful launch of the Carabao brand in the Kuwaiti market was its sponsorship of the "Flare Festival 2023," one of the largest and most popular sports events in Kuwait. The event hosted over 3,000 athletes competing across various tournaments, with more than 7,400 attendees.

Middle East And Africa Meal Replacement Products Market Report Scope

Meal replacements are prepackaged, calorie-controlled foods (like shakes, bars, or soups) formulated to provide balanced protein, carbs, fats, vitamins, and minerals, used to substitute one or two meals for convenience or weight management by simplifying calorie tracking and controlling portions. The Middle East and Africa meal replacement products market is segmented by product type, packaging format, and distribution channel. By product type, the market is segmented into ready-to-drink products, nutritional bars, powdered products, and other product types. By packaging format, the market is segmented into bottles/jars, pouches, tetra packs, and cartons. By distribution channel, the market is segmented into convenience stores, hypermarkets/supermarkets, and more. By geography, the market is segmented into South Africa, Saudi Arabia, Nigeria, and more. The Market Forecasts are Provided in Terms of Value (USD).

By Product Type

| Powdered Products |

| Ready-to-Drink Products |

| Nutritional Bars |

| Soups |

| Other Product Types |

By Packaging Format

| Bottles/Jars |

| Pouches |

| Tetra Packs and Cartons |

| Others |

By Distribution Channel

| Supermarkets/Hypermarkets |

| Convenience Stores |

| Specialty Stores |

| Online Retailers |

| Other Distribution Channels |

By Geography

| South Africa |

| Saudi Arabia |

| Nigeria |

| United Arab Emirates |

| Rest of Middle East and Africa |

| By Product Type | Powdered Products |

| Ready-to-Drink Products | |

| Nutritional Bars | |

| Soups | |

| Other Product Types | |

| By Packaging Format | Bottles/Jars |

| Pouches | |

| Tetra Packs and Cartons | |

| Others | |

| By Distribution Channel | Supermarkets/Hypermarkets |

| Convenience Stores | |

| Specialty Stores | |

| Online Retailers | |

| Other Distribution Channels | |

| By Geography | South Africa |

| Saudi Arabia | |

| Nigeria | |

| United Arab Emirates | |

| Rest of Middle East and Africa |

Key Questions Answered in the Report

How big is the Middle East and Africa meal replacement products market in 2026?

It equals USD 191.81 million and is on track to reach USD 263.5 million by 2031 at a 6.56% CAGR.

Which country grows the fastest for meal replacements in the region?

Nigeria leads with an 8.02% CAGR through 2031, driven by rapid urbanization and a young consumer base.

What product format is gaining share quickest?

Ready-to-drink lines post a 7.12% CAGR thanks to single-serve convenience valued by urban professionals.

Page last updated on: