Online Food Delivery Market Size and Share

Market Overview

| Study Period | 2021 - 2031 |

|---|---|

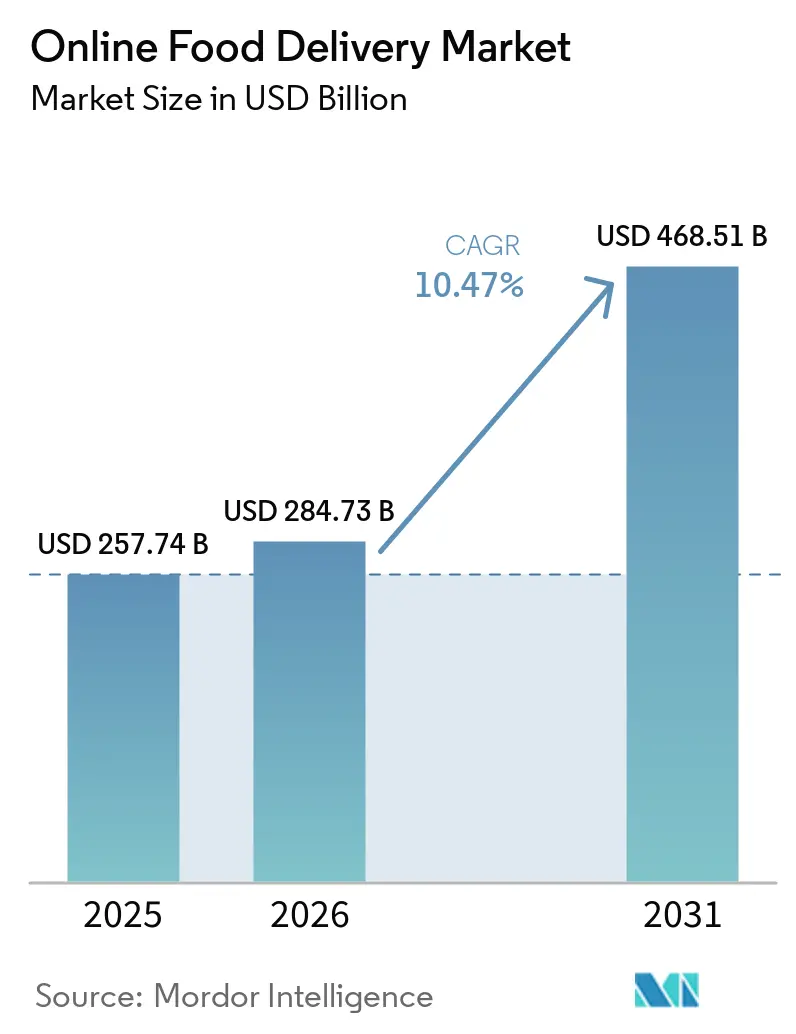

| Market Size (2026) | USD 284.73 Billion |

| Market Size (2031) | USD 468.51 Billion |

| Growth Rate (2026 - 2031) | 10.47% CAGR |

| Fastest Growing Market | Asia-Pacific |

| Largest Market | North America |

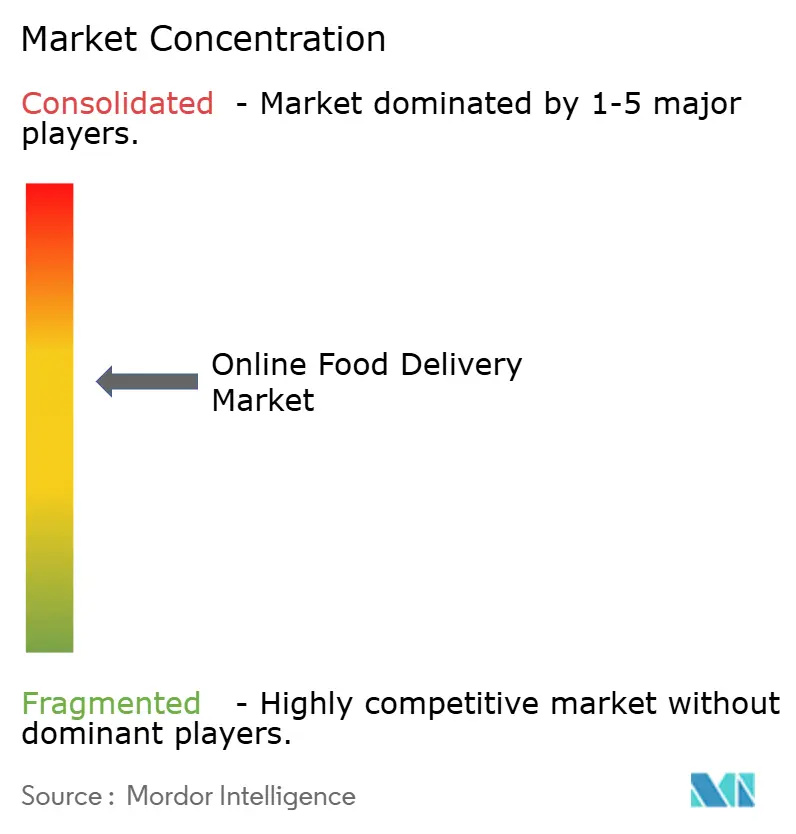

| Market Concentration | Medium |

Major Players

*Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. |

|

Online Food Delivery Market Analysis by Mordor Intelligence

The online food delivery market size was valued at USD 257.74 billion in 2025 and estimated to grow from USD 284.73 billion in 2026 to reach USD 468.51 billion by 2031, at a CAGR of 10.47% during the forecast period (2026-2031). This growth in the online food delivery market is primarily driven by rising demand for convenience and time-saving solutions as consumers face busier lifestyles and longer working hours. By business model, direct channels are gaining traction as they provide better pricing control for service providers. In terms of service type, platform delivery services are expanding rapidly as they expand their coverage and accessibility. Regarding payment modes, digital wallets dominate the market due to their ease of use, but cash payments remain popular in emerging markets where digital adoption is slower. When it comes to platforms, mobile applications lead the market, offering user-friendly interfaces and convenience, while desktop platforms remain relevant in certain high-value segments. The online food delivery market is moderately fragmented, with several players competing to capture market share and meet the evolving needs of consumers.

Key Report Takeaways

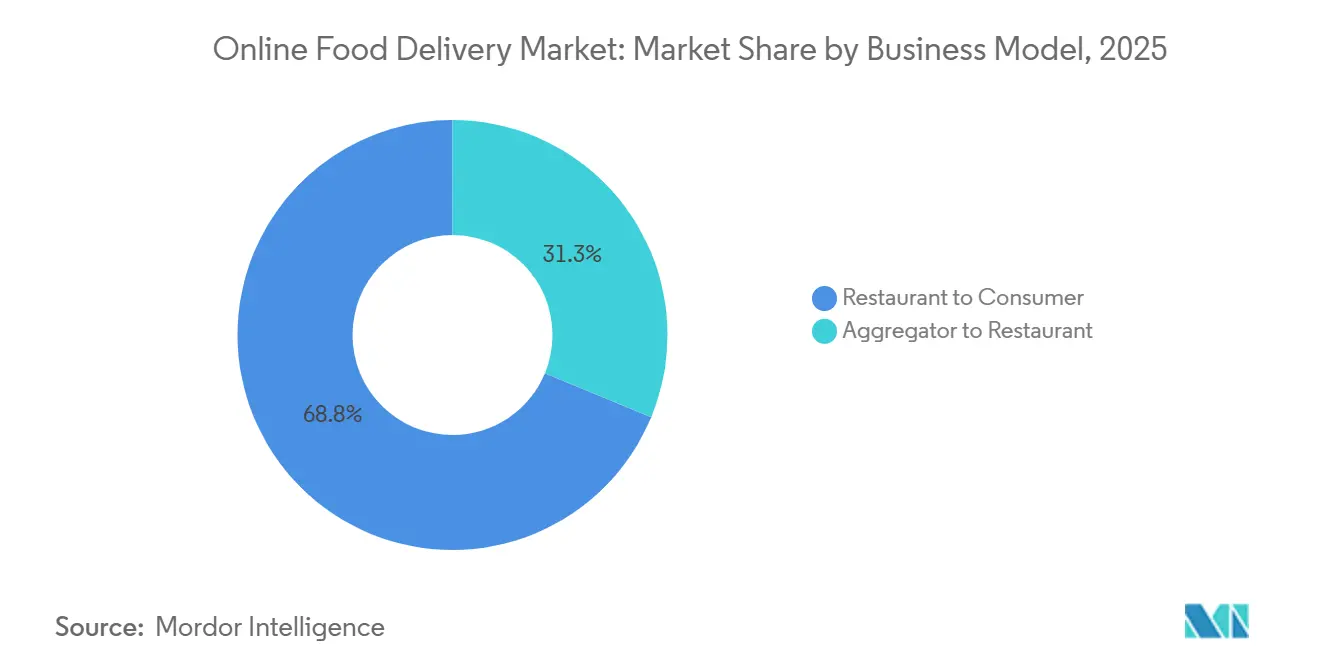

- By business model, restaurant-to-consumer channels held 68.75% of the online food delivery market share in 2025, while aggregator-to-restaurant models are expected to advance at an 11.47% CAGR through 2031.

- By service type, restaurant-managed delivery led with 37.82% of revenue in 2025; platform delivery is poised to expand at a 12.31% CAGR to 2031.

- By payment mode, online payments accounted for 67.45% of transactions in 2025, whereas cash-on-delivery transactions are growing at the fastest rate, with a 12.75% CAGR.

- By platform, mobile and tablet apps captured 82.76% of orders in 2025; desktop portals nonetheless register an 11.84% CAGR, underpinned by enterprise catering demand.

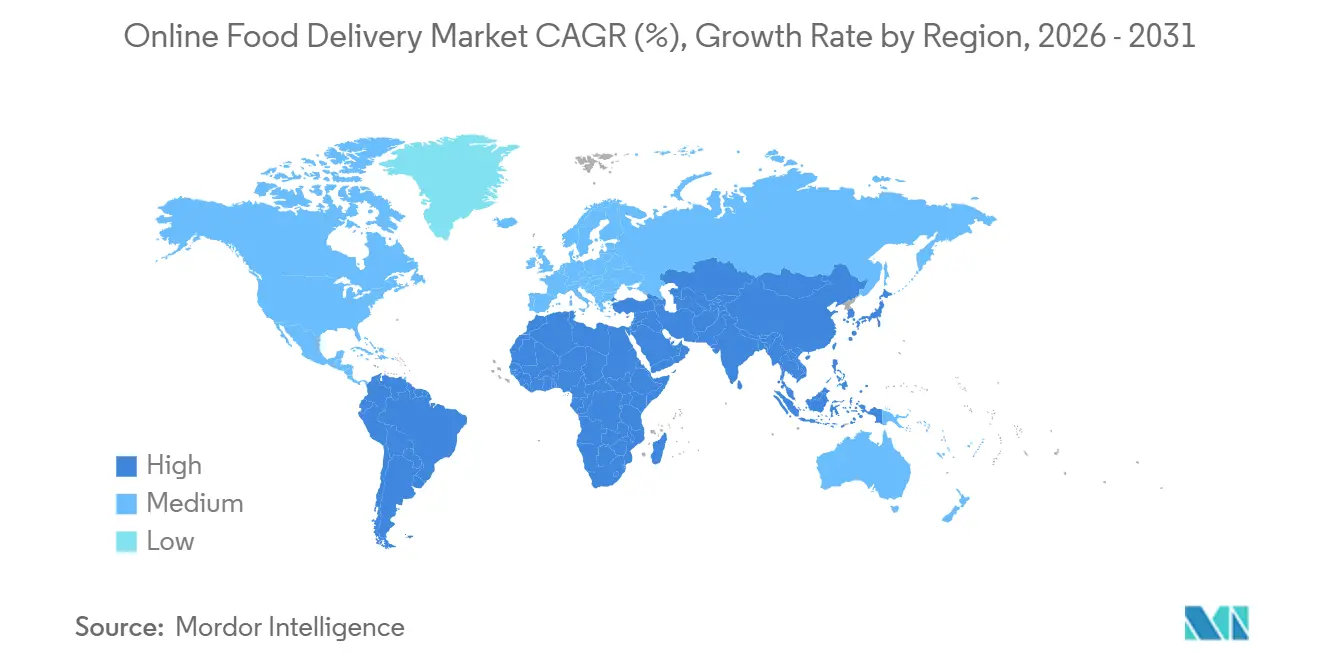

- By geography, North America topped with revenue in 2025, while the Asia-Pacific region is the quickest riser at a 12.53% CAGR through 2031.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of January 2026.

Market Trends and Insights

Drivers Impact Analysis of Online Food Delivery Market*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Demand for convenience and time saving due to busy lifestyles and long working hours | +2.3% | Global, with peak intensity in North America, Europe, and urban Asia-Pacific | Medium term (2-4 years) |

| Adoption of digital wallets, cards, and instant payment systems | +1.8% | Global, led by Asia-Pacific (India UPI, China Alipay/WeChat Pay), Latin America (Brazil Pix) | Short term (≤ 2 years) |

| Free delivery offers, app discounts, and subscription plans stimulate trial | +1.5% | North America, Europe, with spillover to urban Asia-Pacific and Latin America | Medium term (2-4 years) |

| Delivery-only kitchens expanding food supply in high-demand areas | +1.2% | Asia-Pacific core (India, China, Southeast Asia), expanding to Middle East and Latin America | Long term (≥ 4 years) |

| Popularity of contactless delivery services | +0.9% | Global, with sustained adoption in North America, Europe, and developed Asia-Pacific | Short term (≤ 2 years) |

| Growth of late-night and off-hour ordering | +0.7% | Global, concentrated in metropolitan areas across all regions | Medium term (2-4 years) |

| Source: Mordor Intelligence | |||

Demand for convenience and time saving due to busy lifestyles and long working hours

Urban consumers within the online food delivery market, who are increasingly time-constrained, are driving the growth of online food delivery services. Busy professionals and workers are choosing to order meals instead of cooking or dining out, as it helps them save valuable time. This trend in the online food delivery market is supported by high global employment levels, with the International Labour Organization estimating a 95.1% employment rate in 2024, indicating widespread workforce participation[1]Source: International Labour Organization, "World Employment and Social Outlook: May 2024 Update", ilo.org. The rapid adoption of digital platforms and mobile ordering has made food delivery a convenient solution, particularly for individuals residing in densely populated urban areas. Features like shorter delivery times and real-time tracking have encouraged repeat usage, even when menu prices increase. For example, in markets like India, the combination of rising smartphone usage and higher disposable incomes in urban areas has significantly boosted the online food delivery industry.

Adoption of digital wallets, cards, and instant payment systems

The increasing use of digital wallets in the online food delivery market is playing a significant role in boosting online food delivery services. Digital wallets make the checkout process faster and easier, encouraging more impulse purchases. In 2024, 58% of United States adults used digital wallets, with adoption even higher among younger consumers aged 18 to 34, at a rate of 72% as per the Federal Payments Improvement Organization[2]Source: Federal Payments Improvement Organization, "Federal Reserve Payments Insights Brief Consumer Payments Study", fedpaymentsimprovement.org. This indicates a strong preference for mobile and app-based payment methods among younger demographics. Features like one-click checkout on platforms such as Uber Eats and DoorDash allow customers to place orders almost instantly without needing to manually enter card details. This convenience encourages repeat orders, particularly for smaller, spontaneous food purchases. As payment processes become quicker and more user-friendly, businesses see an increase in customer lifetime value. On the other hand, platforms that fail to offer popular digital wallet options risk losing customers due to higher cart abandonment rates, even if their menus and pricing remain competitive.

Free delivery offers, app discounts, and subscription plans stimulate trial

Free delivery offers and subscription plans in the online food delivery market are making online food delivery more popular by reducing the initial cost of placing an order. These strategies encourage customers to explore new platforms and try out new restaurants. Services like DoorDash’s DashPass, Uber One, and Amazon Prime’s partnership with Grubhub+ make delivery feel more affordable and convenient. As a result, customers tend to order more frequently and remain loyal to these platforms. These subscription models work by increasing the size and frequency of orders, which helps platforms offset the cost of offering free delivery and improves their overall profitability. However, as more households subscribe to multiple services, there is a growing risk of subscription fatigue. To address this, platforms need to regularly introduce new perks, discounts, and loyalty rewards to keep users engaged and prevent them from canceling their subscriptions.

Growth of late night and off hour ordering

The growing trend of late-night and off-hour food ordering is driving the online food delivery market as more consumers seek meals outside the traditional breakfast, lunch, and dinner times. Factors such as flexible work schedules, night shifts, remote work, and the increasing popularity of streaming and gaming are driving this demand for food during late evenings and early mornings. A survey conducted by the International Journal for Multidisciplinary Research in August 2023 revealed that 29.97% of respondents ordered food 3 to 7 times per month, showing that food delivery has become a regular habit rather than an occasional indulgence[3]Source: International Journal for Multidisciplinary Research, "Survey On Ordering and Eating Food Using Online Food Delivery Applications", ijfmr.com. To cater to this shift, delivery platforms are introducing 24/7 kitchens, deploying night-time delivery fleets, and offering menus tailored for convenience. These efforts help platforms utilize their resources more effectively during off-peak hours, generating additional revenue and meeting the evolving needs of consumers.

Restraints Impact Analysis of Online Food Delivery Market*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| High commission fees charged to restaurants | -1.4% | Global, with acute pressure in North America and Europe due to regulatory caps | Short term (≤ 2 years) |

| Rising delivery and labor costs | -1.1% | Global, most severe in North America and Europe with minimum wage mandates | Medium term (2-4 years) |

| Menu price inflation on apps | -0.8% | Global, particularly impacting price-sensitive consumers in emerging markets | Short term (≤ 2 years) |

| Limited control over last-mile experience | -0.6% | Global, with higher impact in regions with fragmented logistics infrastructure | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

Limited control over last mile experience

One of the major challenges for the online food delivery market is the lack of control over the last-mile delivery process, as platforms depend heavily on third-party riders and gig workers to deliver orders. This reliance can lead to issues such as delays, incorrect orders, food arriving at the wrong temperature, or poor handling, all of which negatively impact customer satisfaction and the restaurant's or platform's reputation. Even if the food quality is excellent, problems during delivery can result in unhappy customers, negative reviews, refund requests, and even loss of repeat business. These issues also increase operational costs for both delivery platforms and restaurant partners. As the number of orders continues to grow, especially during peak times or adverse weather conditions, ensuring consistent and reliable delivery becomes even more challenging. This makes the last-mile delivery process a critical weak point in an otherwise technology-driven business model.

Menu price inflation on apps

In the online food delivery market, menu price inflation on food delivery apps poses a significant challenge, as restaurants often charge higher prices online to cover additional costs, including platform commissions, packaging, and delivery fees. This price difference has become increasingly noticeable to consumers. For instance, a 2025 Times of India survey highlighted cases where customers paid up to 81% more for the same food ordered through delivery apps compared to dining in at the restaurant. These steep price increases make customers more price-sensitive, leading many to reduce their use of delivery apps. Instead, they may opt for alternatives like in-store pickup or preparing meals at home. Over time, this trend reduces the frequency of online orders, increases customer turnover, and limits the long-term growth potential of food delivery platforms, despite the continued rise in demand for convenience. The growing awareness of these price disparities could further pressure delivery platforms and restaurants to find more cost-effective solutions to retain customers.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Online Food Delivery Market Segment Analysis

By Business Model:

Direct Channels Secure Pricing PowerRestaurant-to-consumer platforms led the online food delivery market in 2025, holding 68.75% of the total market share. This growth is driven by large restaurant chains and groups that have developed their own branded apps and delivery services. By doing so, these restaurants can directly connect with customers, manage pricing and promotions, and avoid paying high commissions to third-party aggregators. Features like loyalty programs and personalized offers further strengthen customer relationships, making these platforms a key revenue source for restaurants in the online food delivery market.

Aggregator-to-restaurant platforms in the online food delivery market are expected to grow the fastest, with a projected CAGR of 11.47% through 2031. These platforms attract consumers by offering a wide variety of food options, convenience, and coverage across multiple locations. For small and mid-sized restaurants, aggregators provide access to a larger customer base without requiring significant investment in delivery infrastructure. Advanced logistics, marketing tools, and subscription programs help increase customer engagement and frequency of orders. As more consumers prefer platforms that offer multiple restaurant choices, aggregators are becoming essential to the growth of the online food delivery market.

By Service Type:

Platform Delivery Accelerates as Coverage DeepensIn 2025, restaurant-managed delivery accounted for 37.82% of online food delivery revenue, underscoring the success of pizza chains and quick-service restaurants that operate their own delivery fleets. These businesses benefit from better control over food quality, delivery times, and customer satisfaction, which helps maintain their brand reputation and encourages repeat orders. By managing their own delivery, these restaurants avoid paying platform commissions, enabling them to offer competitive pricing and enhance their profit margins. As a result, many large quick-service restaurants and pizza chains continue to rely on in-house delivery to maintain their scale and customer loyalty.

In the online food delivery market, platform-based delivery is expected to grow at a 12.31% CAGR through 2031, driven by aggregator apps that provide extensive courier networks for quick and flexible delivery. This model allows small and medium-sized restaurants to expand their reach beyond their local areas without the need to invest in their own delivery infrastructure. Aggregators also offer tools like marketing support, customer discovery features, and subscription services, which help increase order visibility and frequency. As consumers increasingly demand faster service and more variety, platform-based delivery is becoming a key driver of growth in the online food delivery market.

By Payment Mode:

Wallets Rule, but Cash Keeps Growing in Emerging MarketsIn the online food delivery market, online payment methods, including digital wallets, cards, and instant payment systems, accounted for 67.45% of online food delivery transactions in 2025. Consumers are increasingly opting for these options because they are fast, secure, and convenient. In countries such as India and Brazil, instant payment systems have become the standard for app-based purchases, making the checkout process smoother and increasing order completion rates. These payment methods also simplify reordering and encourage the use of loyalty programs and subscriptions, helping digital payments maintain their dominance in the online food delivery market.

Cash on delivery is expected to grow at a 12.75% CAGR through 2031, especially in emerging markets where smartphone usage is rising faster than access to banking services or credit cards. Many people in these regions still rely on cash due to trust issues, habits, or limited access to digital financial tools. Delivery platforms cater to this preference by allowing customers to pay in cash upon delivery, which helps them reach a broader audience. This combination of digital and cash payment options allows platforms to expand quickly in both technologically advanced and underbanked areas.

By Platform:

Mobile Apps Dominate, Desktop Retains High-Value NichesIn 2025, mobile and tablet applications accounted for 82.76% of online food delivery orders, underscoring the increasing reliance on smartphones for meal ordering. Mobile apps provide user-friendly features such as push notifications, GPS-based tracking, saved preferences, and one-tap reordering, making the process faster and more convenient. The constant accessibility of mobile devices encourages frequent and spontaneous orders, driving higher transaction volumes. As a result, mobile platforms dominate the online food delivery market, catering to the increasing demand for quick and seamless ordering experiences.

Although desktop and web-based ordering represent a smaller share, this segment is projected to grow at a CAGR of 11.84% through 2031. This growth is driven by specific use cases, such as corporate catering, bulk orders, and group meals, where larger screens facilitate menu comparisons, budget management, and the customization of complex orders. Businesses, event organizers, and institutions are increasingly turning to web portals for planned, high-value purchases. Consequently, this channel is becoming an essential part of the online food delivery market, particularly for professional and enterprise-level needs.

Geography Analysis

North America Online Food Delivery Market

In the online food delivery market, North America contributed 37.54% of online food delivery revenue in 2025, driven by the strong presence of major platform operators and widespread use of app-based ordering by consumers. Subscription models, efficient logistics systems, and strong partnerships with restaurants have ensured steady cash flows and frequent orders. However, increasing regulatory pressure on commission rates and courier wages is impacting the profitability of platforms in some key cities. Canada and Mexico are contributing to the region's growth, while cross-border collaboration is enhancing innovation and digitization efforts in the restaurant sector.

APAC Online Food Delivery Market

The Asia-Pacific region is the fastest-growing online food delivery market for online food delivery, with a projected CAGR of 12.53%. The increasing use of smartphones fuels this growth, the adoption of digital payment systems, and the rapid development of platform ecosystems. Leading companies in the region are heavily investing in logistics, cloud kitchens, and integrating services into super-apps to expand their reach. Southeast Asia remains a competitive market due to its diverse consumer preferences and infrastructure challenges. Meanwhile, countries like India are seeing growth beyond major cities, and markets such as Japan and Australia continue to provide stable demand with high spending.

EMEA and South America Online Food Delivery Market

Europe, South America, and the Middle East and Africa present a varied growth landscape for online food delivery. Europe faces stricter regulations that influence platform operations and cost structures, but consumer demand remains strong. In South America, Brazil leads the market, with delivery platforms becoming an integral part of urban lifestyles. The Middle East is experiencing rapid growth due to increased platform investments and rising consumer demand. In Africa, the online food delivery market is still in its early stages, with urbanization and the adoption of mobile payment systems driving expansion opportunities.

Competitive Landscape

The online food delivery market comprises both large international companies and strong regional players, resulting in a moderately fragmented landscape. Major platforms, such as DoorDash, Uber Eats, Meituan, and Delivery Hero, lead the online food delivery market due to their size, strong brand presence, and advanced technology. These companies are expanding their services beyond food delivery to include groceries, convenience items, and mobility-related offerings. By introducing loyalty programs and bundling services, they aim to attract more customers and encourage frequent usage, helping them maintain a competitive edge.

Technology is a major factor in driving success in the online food delivery market. Leading companies are investing heavily in tools such as artificial intelligence, machine learning, and data analytics to enhance their operations. These technologies help predict customer demand, optimize delivery routes, and enhance the overall user experience. Advancements in automation, such as smart kitchens and autonomous delivery systems, are enabling companies to reduce costs and enhance efficiency. These innovations are essential for staying competitive in a market where profit margins are often narrow.

Regional players in the online food delivery market are also making a strong impact by focusing on local needs and preferences. In areas like Latin America, Southeast Asia, and the Middle East, these companies build their presence through partnerships with local restaurants, super-app ecosystems, and cloud kitchens. They also gain an advantage by complying early with local regulations, which helps them establish trust with governments and customers. The combination of global companies leveraging their scale and regional players adapting to local markets is shaping the future of the online food delivery market.

Online Food Delivery Industry Leaders

-

Delivery Hero SE

-

Uber Technologies Inc.

-

Meituan Dianping

-

Just Eat Takeaway.com N.V.

-

DoorDash Inc.

- *Disclaimer: Major Players sorted in no particular order

Online Food Delivery Market Companies Covered in this Report

- Delivery Hero SE

- Meituan Dianping

- Uber Technologies Inc.

- DoorDash Inc.

- Just Eat Takeaway.com N.V.

- Grab Holdings Ltd.

- Delivery.com LLC

- Roofoods Ltd

- Bundl Technologies Pvt Ltd

- Eternal Limited

- Prosus

- Rappi Inc.

- DiDi Global Inc.

- Roppen Transportation Services Private Limited

- ChowNow Inc.

- GoPuff

- Domino’s Pizza Inc.

- Bolt Technology OÜ

- Wonder Group, Inc.

- Sea Limited

Recent Industry Developments in Online Food Delivery Market

- August 2025: Rapido expanded its operations into the food delivery market by introducing Ownly, a dedicated app aimed at offering customers budget-friendly meal options.

- April 2024: Zomato launched a "large order fleet" to handle orders for groups of people or events. This was claimed to be an all-electric fleet, explicitly designed to serve orders for gatherings of up to 50 people.

- April 2024: DoorDash Inc. enabled over 180,000 orders with reusable packaging globally across the countries DoorDash and Wolt operate. The company is working to grow that number in partnership with DeliverZero in the United States.

- May 2024: Instacart and Uber Technologies, Inc. announced a strategic partnership aimed at integrating Uber Eats restaurant delivery into Instacart's platform. This collaboration allowed Instacart users across the United States to order from a wide range of restaurants.

Global Online Food Delivery Market Report Scope

The online food delivery market comprises digital platforms and applications that enable consumers to order meals and beverages from restaurants, cafes, and foodservice outlets for delivery to their homes or workplaces. The online food delivery market is segmented by business model, service type, payment mode, platform, and geography. Based on the business model, the market is segmented into aggregator-to-restaurant and restaurant-to-customer. Based on the service type, the market is segmented into platform delivery and restaurant-managed delivery. Based on payment mode, the market is segmented into online payment mode and cash-on-delivery mode. Based on the platform, the market is segmented into mobile/tablet applications, desktop/web portals, and other categories. Based on geography, the market is segmented into North America, Europe, Asia-Pacific, South America, and the Middle East and Africa. The market forecasts are provided in terms of value (USD).

Segmentation Overview

| Aggregator to Restaurant |

| Restaurant to Consumer |

| Platform Delivery |

| Restaurant Managed Delivery |

| Online Payment Mode |

| Cash on Delivery Mode |

| Mobile/Tablet Applications |

| Desktop/Web Portals |

| Others |

| North America | United States |

| Canada | |

| Mexico | |

| Rest of North America | |

| South America | Brazil |

| Colombia | |

| Chile | |

| Peru | |

| Argentina | |

| Rest of South America | |

| Europe | United Kingdom |

| Germany | |

| France | |

| Italy | |

| Spain | |

| Poland | |

| Belgium | |

| Sweden | |

| Rest of Europe | |

| Asia-Pacific | China |

| Japan | |

| India | |

| Australia | |

| Indonesia | |

| South Korea | |

| Thailand | |

| Singapore | |

| Rest of Asia-Pacific | |

| Middle East and Africa | South Africa |

| Saudi Arabia | |

| United Arab Emirates | |

| Nigeria | |

| Egypt | |

| Morocco | |

| Turkey | |

| Rest of Middle East and Africa |

| By Business Model | Aggregator to Restaurant | |

| Restaurant to Consumer | ||

| By Service Type | Platform Delivery | |

| Restaurant Managed Delivery | ||

| By Payment Mode | Online Payment Mode | |

| Cash on Delivery Mode | ||

| By Platform | Mobile/Tablet Applications | |

| Desktop/Web Portals | ||

| Others | ||

| By Geography | North America | United States |

| Canada | ||

| Mexico | ||

| Rest of North America | ||

| South America | Brazil | |

| Colombia | ||

| Chile | ||

| Peru | ||

| Argentina | ||

| Rest of South America | ||

| Europe | United Kingdom | |

| Germany | ||

| France | ||

| Italy | ||

| Spain | ||

| Poland | ||

| Belgium | ||

| Sweden | ||

| Rest of Europe | ||

| Asia-Pacific | China | |

| Japan | ||

| India | ||

| Australia | ||

| Indonesia | ||

| South Korea | ||

| Thailand | ||

| Singapore | ||

| Rest of Asia-Pacific | ||

| Middle East and Africa | South Africa | |

| Saudi Arabia | ||

| United Arab Emirates | ||

| Nigeria | ||

| Egypt | ||

| Morocco | ||

| Turkey | ||

| Rest of Middle East and Africa | ||

Key Questions Answered in the Report

What is the 2026 value of the Global online food delivery market?

The sector is valued at USD 284.73 billion in 2026 and is set to reach USD 468.51 billion by 2031.

Which business model currently dominates online food delivery?

Restaurant-to-consumer channels lead with 68.75% share in 2025, reflecting large chains’ preference for proprietary apps and fleets.

Which region is growing fastest?

Asia-Pacific is expanding at a 12.53% CAGR through 2031, driven by players such as Meituan, Swiggy, and Grab.

How large is the mobile share of orders?

Mobile and tablet applications account for 82.76% of global transactions as of 2025.

Page last updated on: