Market Overview

| Study Period | 2021 - 2031 |

|---|---|

| Forecast Data Period | 2026 - 2031 |

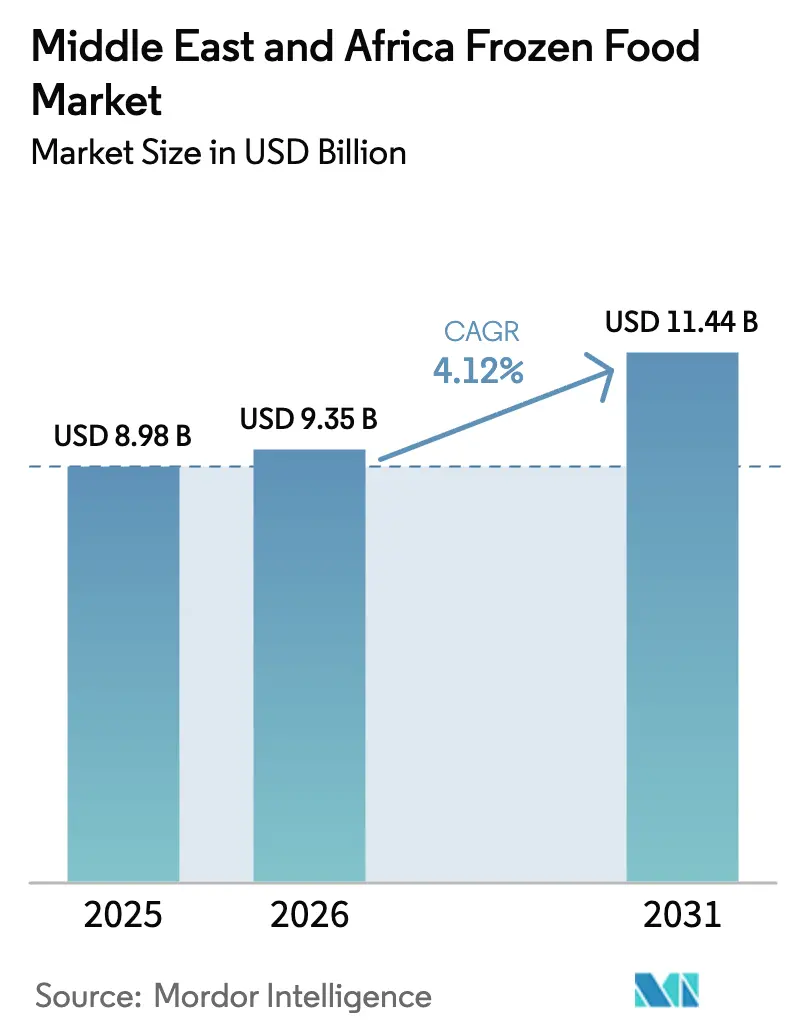

| Base Year Market Size (2025) | USD 8.98 Billion |

| Market Size (2026) | USD 9.35 Billion |

| Market Size (2031) | USD 11.44 Billion |

| Growth Rate (2026 - 2031) | 4.12% CAGR |

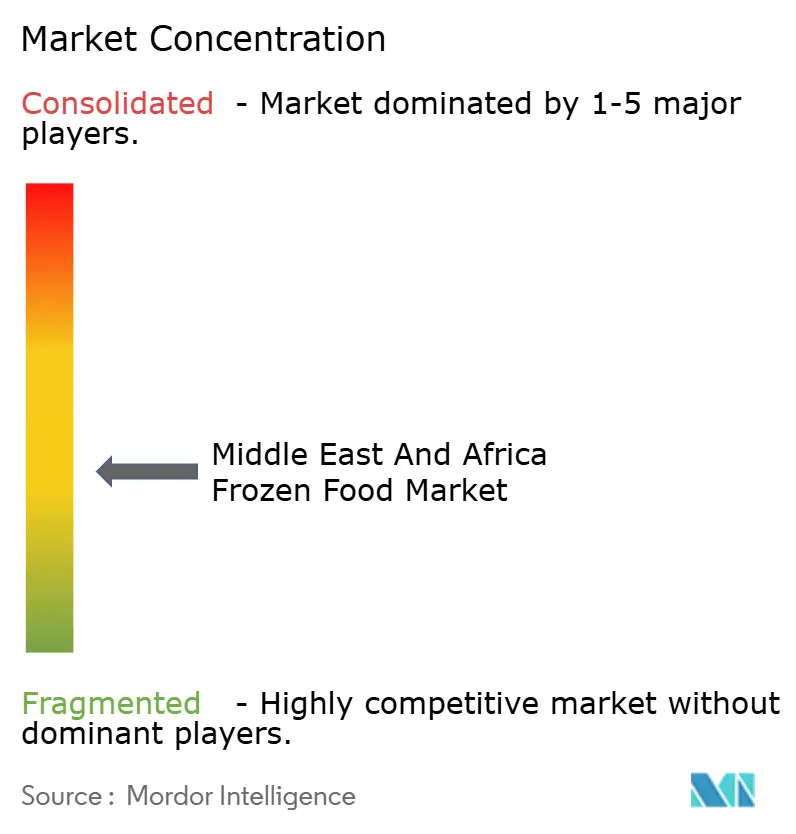

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

Middle East And Africa Frozen Food Market Analysis by Mordor Intelligence

The Middle East and Africa frozen food market size in 2026 is estimated at USD 9.35 billion, growing from 2025 value of USD 8.98 billion with 2031 projections showing USD 11.44 billion, growing at 4.12% CAGR over 2026-2031. This market development reflects a fundamental shift in consumer behavior and infrastructure advancement across the region. The transformation is driven by the convergence of urbanization, evolving dietary preferences, and investments in cold chain logistics, reshaping food consumption patterns from the Gulf states to sub-Saharan Africa. Despite the region's traditional inclination toward fresh foods, the market demonstrates a significant evolution in food retail and consumption habits. The growth is supported by increasing urbanization, the rise of dual-income households, and enhanced cold-chain infrastructure, leading to higher per-capita frozen food consumption across Gulf states and key African markets. Government initiatives focusing on food security, the establishment of regional manufacturing facilities, and the expansion of modern retail channels have improved product accessibility. The market benefits from regional climate conditions that promote stockpiling behavior and increasing consumer acceptance of frozen foods as viable alternatives to fresh products. The competitive environment remains moderately fragmented, featuring a mix of multinational companies and regional brands that capitalize on their local market understanding and sourcing advantages.

Key Report Takeaways

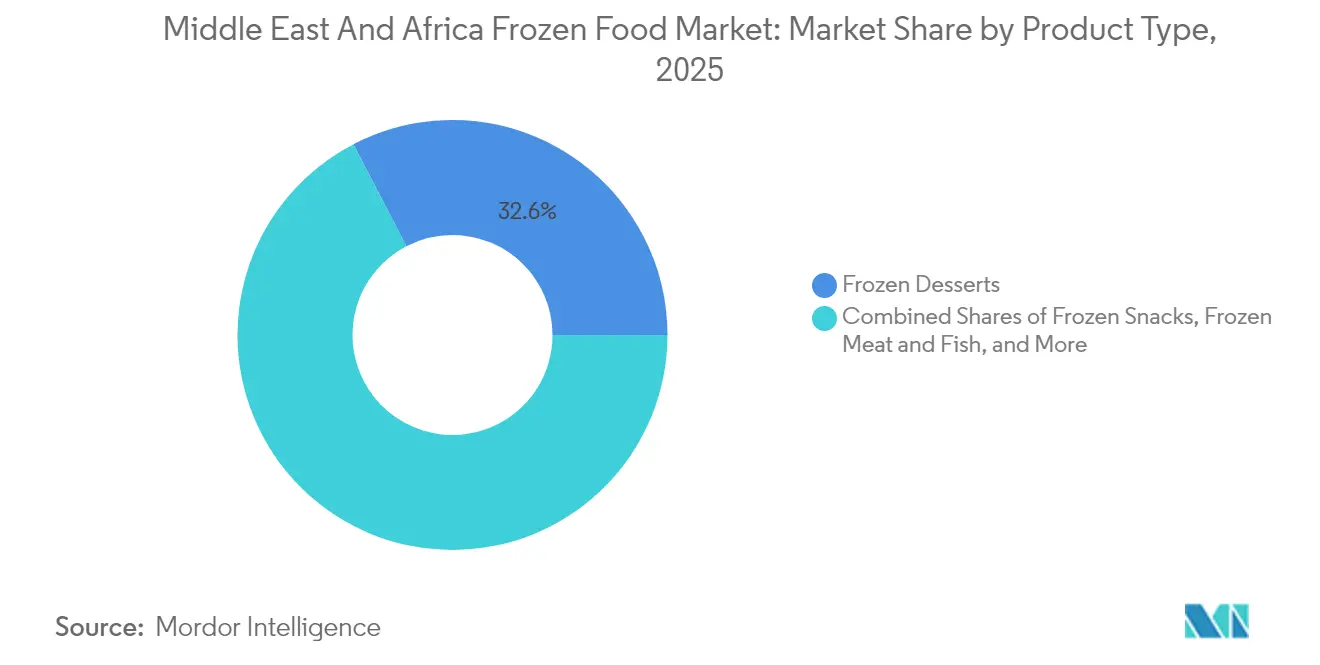

- By product type, frozen desserts led with 32.62% revenue share in 2025 while frozen meat & fish recorded the fastest momentum at a 5.16% CAGR for 2026-2031.

- By category, conventional items accounted for 75.86% of 2025 sales whereas organic variants are forecast to expand at a 5.62% CAGR through 2031.

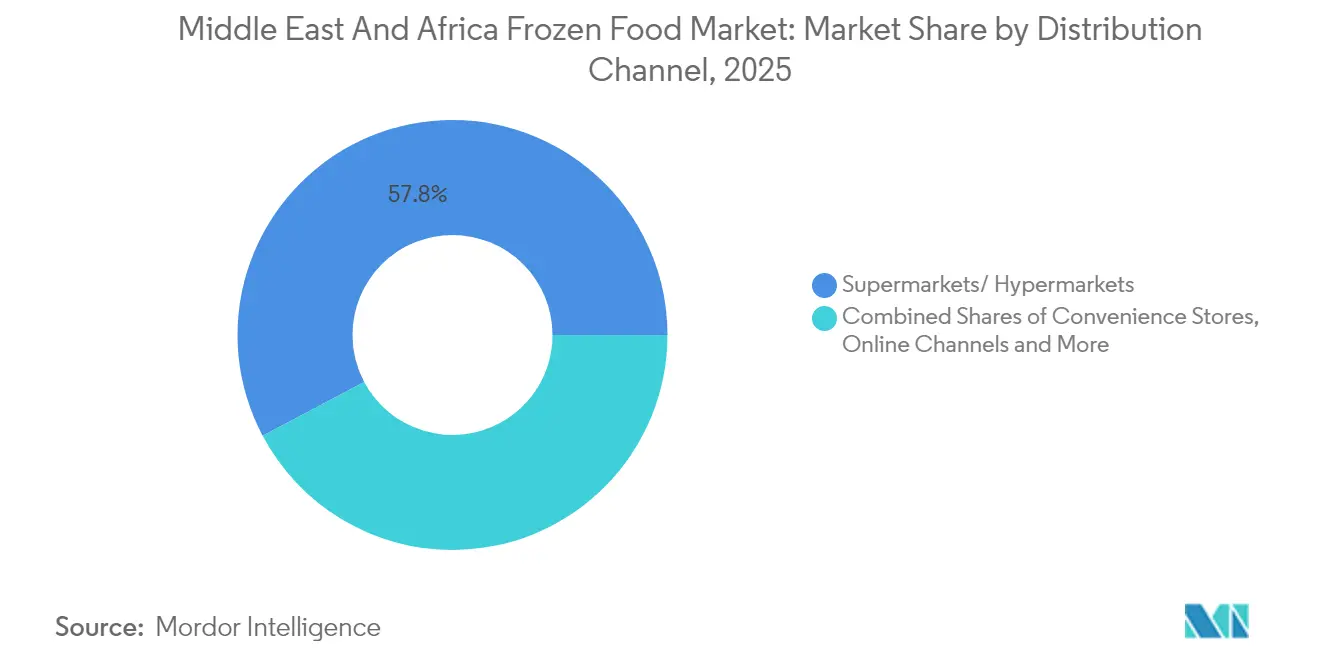

- By distribution channel, supermarkets and hypermarkets held 57.77% share in 2025, yet online channels are on track for a 4.86% CAGR to 2031.

- By geography, Saudi Arabia dominated with 37.77% share in 2025 and South Africa is positioned for a 4.95% CAGR over the outlook period.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of 2026.

Middle East And Africa Frozen Food Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Rising demand for ready-to-eat (RTE) and ready-to-cook (RTC) meals | +1.2% | Global, strongest in UAE and Saudi Arabia | Medium term (2-4 years) |

| Gaining popularity of westernized diets and global cuisines | +0.8% | Urban centers across MEA, led by Gulf states | Long term (≥ 4 years) |

| Improved cold chain infrastructure and logistics facilitating distribution | +1.1% | Saudi Arabia, UAE, South Africa with spillover effects | Medium term (2-4 years) |

| Expansion of modern retail outlets including supermarkets and hypermarkets | +0.9% | Regional, concentrated in major cities | Medium term (2-4 years) |

| Seasonal variations and climate adversity promoting stockpiling of frozen foods | +0.6% | Gulf states and North Africa | Short term (≤ 2 years) |

| Wider product availability, including ethnic and local frozen dishes | +0.4% | Regional with cultural adaptation needs | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

Rising demand for ready-to-eat (RTE) and ready-to-cook (RTC) meals

The consumption of ready-to-eat (RTE) and ready-to-cook (RTC) meals in the Middle East and Africa (MEA) region has experienced substantial growth, with Middle Eastern consumers increasingly purchasing prepared foods and ordering takeaway meals on a weekly basis. This transformation in consumer behavior stems from the growing prevalence of dual-income households and extended working hours in professional environments. Urban areas demonstrate robust demand for convenience-oriented frozen meals, driven by time constraints and evolving lifestyle patterns. Manufacturers are adapting their product offerings to local tastes, moving beyond traditional Western-style frozen meals, as demonstrated by Al Kabeer's introduction of limited-edition cheese samosas during Ramadan in the UAE and KSA. The market expansion is further supported by technological advancements in frozen food preparation, including products compatible with air fryers, which have become common kitchen appliances in MEA households. This trend is expected to continue as urbanization increases and disposable incomes grow across key markets, particularly benefiting the frozen cooked ready meals segment. The regulatory framework, including standards established by food safety authorities such as UAE's ESMA, ensures the quality and safety of convenience frozen foods, further supporting market development.

Gaining popularity of westernized diets and global cuisines

The MEA region is experiencing a shift toward Western dietary patterns, reflecting broader changes in lifestyle preferences and cultural integration. This transformation is evident in the frozen food market, where international cuisines, particularly Asian street food products, are showing significant growth. The market expansion is supported by increased international travel, growing expatriate communities, and widespread digital media exposure, which has familiarized consumers with diverse food options. For example, McCain Foods has expanded its vegetable-based product range through collaborations with Strong Roots to meet the increasing demand for diverse frozen food options. This trend is particularly prominent among younger consumers who consider international cuisine consumption as part of their cultural identity. Market success requires adaptation to local preferences and compliance with regional requirements, such as halal certification. Manufacturers are investing in research and development to develop products that combine international flavors with local taste preferences, indicating a long-term transformation in product offerings.

Improved cold chain infrastructure and logistics facilitating distribution

The development of cold chain infrastructure across the MEA region is transforming the frozen food market landscape by establishing robust distribution networks and unlocking new market opportunities. The UAE's cold chain logistics market continues to demonstrate substantial growth, reflecting the region's commitment to infrastructure advancement. A notable example is RSA Cold Chain's state-of-the-art Regional Distribution Centre in Dubai's Jebel Ali Free Zone, equipped with extensive pallet storage capacity and advanced temperature control systems, which strengthens supply chain operations throughout the Middle East market [1]Source: Free Trade Zone, “Meat, Poultry & Seafood Processing Industry in the UAE,” uaqftz.gov.ae. Infrastructure enhancement includes comprehensive last-mile delivery solutions, as demonstrated by BinDawood's investment in delivery hubs to optimize logistics performance. DP World's strategic investment initiative for African ports and logistics infrastructure in June 2024 will strengthen distribution capabilities, particularly benefiting South Africa's frozen food market. The infrastructure improvements incorporate artificial intelligence and machine learning systems to optimize capacity planning, improve forecast accuracy, and reduce product waste in temperature-controlled environments.

Expansion of modern retail outlets including supermarkets and hypermarkets

The expansion of modern retail formats across the MEA region is fundamentally transforming the landscape of frozen food distribution and accessibility, creating enhanced opportunities for consumer engagement and product discovery. The growth of modern trade channels in MENA markets, particularly in the United Arab Emirates and Saudi Arabia, is driving substantial growth in frozen food sales through improved product visibility and consumer education initiatives. The retail sector transformation in Saudi Arabia demonstrates remarkable progress, with the expansion of modern retail channels providing essential refrigeration infrastructure for frozen food merchandising [2]Source: Food Export Association of the Midwest USA and Food Export USA–Northeast “Saudi Arabia,” foodexport.org. Consumer shopping behaviors are evolving in response to this retail modernization, characterized by increased purchase frequency and greater willingness to explore new frozen food products in organized retail environments. Infrastructure development supporting this modern retail growth is evident through strategic warehouse capacity expansions in key locations like Abu Dhabi, benefiting various industries including food and beverages. The modern retail expansion facilitates optimized inventory management and minimizes product waste through enhanced cold chain management at the retail level, with this trend expected to strengthen as retail modernization extends to secondary cities and emerging markets within the MEA region, supported by foreign direct investment and local retail chain expansion initiatives.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Cultural preference for fresh food over frozen products among many consumers | -0.7% | Regional, strongest in traditional communities | Long term (≥ 4 years) |

| Limited refrigeration infrastructure in rural towns and emerging markets | -0.5% | Rural areas across Africa and secondary cities | Medium term (2-4 years) |

| Competition from ambient/shelf-stable convenience foods | -0.4% | Regional, price-sensitive segments | Short term (≤ 2 years) |

| Import dependency for some categories due to lack of regional production | -0.3% | Import-dependent markets, currency fluctuation exposure | Medium term (2-4 years) |

| Source: Mordor Intelligence | |||

Cultural preference for fresh food over frozen products among many consumers

The cultural preference for fresh foods in MEA markets presents a substantial business challenge, as consumers maintain strong emotional and practical connections to traditional food preparation methods. This preference is deeply woven into the fabric of daily life, where families engage in regular fresh food shopping as a social activity and cultural ritual. Market research indicates that consumers associate fresh ingredients with superior quality, better nutrition, and authentic cooking experiences, creating natural barriers to frozen food adoption. While traditional communities show particular resistance, market dynamics are evolving, especially in urban centers where younger consumers demonstrate increasing acceptance of frozen convenience foods. Product category performance varies significantly - frozen desserts and snacks have achieved better market penetration, while frozen vegetables and meats face stronger competition from fresh alternatives due to their central role in traditional cooking. In response, food manufacturers are implementing strategic initiatives, including product development focused on preserving authentic flavors and nutritional value, alongside comprehensive consumer education programs that address safety concerns and highlight the practical benefits of frozen food technology in modern lifestyles.

Limited refrigeration infrastructure in rural towns and emerging markets

The lack of infrastructure in rural and emerging markets across the MEA region creates barriers to frozen food market growth, particularly in distribution networks. This challenge is most evident in sub-Saharan Africa, where significant rural populations lack the electrical infrastructure and retail cold storage facilities needed for frozen food distribution. The issue affects the entire cold chain, from distribution centers to retail outlets, requiring comprehensive infrastructure improvements. In Nigeria, economic conditions, including high inflation rates, further compound these challenges by reducing both infrastructure investment and consumer purchasing power for frozen foods. However, government infrastructure programs and private sector investments in cold storage solutions are addressing these limitations. The impact of infrastructure constraints is expected to decrease as rural electrification expands and new cold storage technologies, including solar-powered refrigeration systems, become available across the region's emerging markets.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Product Type: Desserts Lead, Protein Pivots Growth

The frozen desserts segment commands a significant 32.62% of the MEA market share in 2025, demonstrating its robust presence in the region's food industry. This substantial market position is deeply rooted in regional consumer behavior, where ice cream and sweet treats play an integral role in social gatherings, religious festivals, and family celebrations. The segment's market strength received further validation when Unilever announced the strategic separation of its ice cream business in April 2024, including the well-established Kwality Wall's brand, signaling confidence in the growth trajectory and economic potential of the frozen desserts category.

The frozen meat and fish segment demonstrates promising market dynamics with a projected CAGR of 5.16% through 2031, indicating sustained expansion in this category. This growth trajectory is primarily influenced by the transformation in urban consumer lifestyles and an increasing preference for high-quality protein options that offer extended storage capabilities. The segment's positive performance aligns with broader shifts in regional dietary preferences, as households increasingly incorporate frozen meat and fish products into their regular consumption patterns. This trend is particularly evident among time-conscious consumers who value the convenience and reliability of frozen protein options while maintaining their busy professional and personal schedules.

By Category: Organic Momentum Builds Despite Conventional Dominance

The frozen food market demonstrates a clear consumer preference for conventional products, which command a substantial 75.86% market share in 2025. This dominance reflects deep-rooted consumer trust and established purchasing patterns in traditional frozen food categories. In parallel, the organic segment is experiencing notable expansion, projected to grow at a CAGR of 5.62% through 2031. This growth is primarily attributed to an increasing number of health-conscious consumers, particularly in affluent demographics, who are actively seeking premium frozen food options. The organic segment's expansion represents a significant evolution in consumer behavior, as individuals increasingly prioritize products they believe offer superior nutritional value and environmental benefits, despite the premium pricing associated with organic certification.

The MEA region is witnessing a transformative shift in consumer preferences, with a growing population demonstrating increased willingness to invest in products that align with their health and environmental values. Despite this emerging trend, conventional frozen foods maintain their strong market position, largely due to widespread price sensitivity among mass-market consumers and the current infrastructure limitations affecting organic frozen food distribution across various regional markets. The significance of this market development is further emphasized by the 22nd Middle East Organic and Natural Products Expo 2024 in Dubai, supported by the UAE Ministry of Climate Change and Environment (November 2024). This event not only showcases the robust regional demand for organic products but also highlights the Middle East's position as a key market for organic product expansion and international collaboration opportunities .

By Distribution Channel: Digital Disruption Challenges Traditional Retail

The frozen food distribution landscape in the MEA region is predominantly controlled by supermarkets and hypermarkets, which command a substantial 57.77% market share in 2025. These retail giants have established their market leadership through significant investments in cold storage facilities and by maintaining an extensive range of frozen food products. This infrastructure advantage allows them to meet diverse consumer demands while ensuring product quality and freshness throughout the supply chain.

While traditional retail channels maintain their stronghold, the market is witnessing a notable shift in consumer behavior with online channels emerging as the fastest-growing distribution method, achieving a 4.86% CAGR through 2031. The preference for physical retail remains deeply rooted in MEA consumer shopping habits, where customers value the ability to personally inspect frozen products. This traditional retail dominance is further strengthened by the continuous expansion of modern retail formats across Saudi Arabia and UAE, where improved store layouts and sophisticated frozen food merchandising strategies enhance the overall shopping experience.

Geography Analysis

The MEA frozen food market demonstrates robust regional dynamics, with Saudi Arabia maintaining a commanding 37.77% market share in 2025. This market leadership stems from the Kingdom's strong economic fundamentals, including substantial consumer purchasing power, well-developed retail infrastructure, and comprehensive government initiatives focused on food security. In parallel, South Africa has established itself as the region's growth engine, recording an impressive 4.95% CAGR through 2031, primarily attributed to its ongoing economic recovery and the expanding purchasing power of its middle-class population.

The Saudi Arabian market demonstrates remarkable expansion through its Vision 2030 framework, which has stimulated extensive investments in food processing infrastructure development. This growth trajectory has captured significant attention from international companies, particularly evident in major investments by industry leaders BRF and JBS in advanced meat processing facilities in Jeddah, with JBS planning facility expansion in April 2025. The United Arab Emirates has established itself as an essential regional distribution center, capitalizing on its strategic geographical position and advanced logistics capabilities. The UAE's frozen food manufacturing sector maintains consistent growth, bolstered by government-led food security initiatives and strategic partnerships with global logistics providers.The regional market landscape is enhanced by the varied market characteristics of Oman, Qatar, Bahrain, and Kuwait, each contributing distinct consumer behaviors and import requirements. Egypt and Nigeria demonstrate considerable market potential, though they continue to address infrastructure development needs. South Africa's market shows positive momentum, primarily driven by evolving meat consumption trends and ongoing economic stability measures, while managing infrastructure limitations and currency market challenges.

Competitive Landscape

The MEA frozen food market demonstrates moderate fragmentation, creating opportunities for multinational corporations and regional players to capture market share through strategic positioning, product innovation, and localized offerings. Market leaders implement various strategies, from capacity expansion and vertical integration to strategic partnerships and cultural adaptation. For instance, BRF plans to invest USD 160 million in April 2025 in Saudi Arabian production facilities, while regional players like Al Kabeer develop culturally relevant products, including limited-edition Ramadan offerings.

The competitive landscape features global food giants alongside established regional players with deep cultural understanding and distribution networks. This creates a dynamic environment where success requires both scale advantages and local market expertise. Technology adoption has emerged as a key differentiator, with companies investing in advanced cold chain management, AI-driven demand forecasting, and sustainable packaging solutions to improve operational efficiency and environmental performance. In June 2024, Nomad Foods' research into raising frozen storage temperatures from -18°C to -15°C demonstrated potential energy consumption reduction of over 10%, illustrating how technological innovation can generate competitive advantages while addressing sustainability concerns.

Market opportunities exist in organic frozen foods, culturally adapted convenience meals, and premium frozen desserts. Emerging companies are utilizing e-commerce platforms and direct-to-consumer models to bypass traditional distribution channels. The regulatory framework, overseen by standards bodies like UAE's ESMA and regional food safety authorities, establishes entry barriers while presenting opportunities for companies that effectively manage compliance requirements while maintaining product quality and safety standards.

Middle East And Africa Frozen Food Industry Leaders

Nestlé S.A.

McCain Foods Ltd.

General Mills Inc.

Kellanova

Al Islami Foods

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- April 2025: BRF announced a USD 160 million investment in a new meat processing facility in Jeddah, Saudi Arabia, expected to increase local production capacity from 17,000 to 57,000 tons annually by mid-2026, demonstrating significant commitment to regional market expansion

- September 2024: Al Islami Foods’ refreshed brand identity and innovative packaging directly support its strong presence and growth in the Middle East and Africa frozen food market, emphasizing premium halal quality and cultural values.

- March 2024: Al Kabeer partnered with Kiri to launch limited-edition cheese samosas for Ramadan in UAE and KSA, demonstrating successful cultural adaptation and seasonal product innovation strategies in the MEA frozen food market

Middle East And Africa Frozen Food Market Report Scope

Frozen food is defined as food products that are preserved under low temperatures and used over a long period. The frozen food market is segmented by product type, product category, distribution channel, and geography. By product type, the market is segmented into frozen fruits and vegetables, frozen snacks, frozen seafood, frozen meat and poultry, frozen desserts, and other product types. By product category, the market is classified as ready-to-eat, ready-to-cook, and others. By distribution channel, the market is segmented into supermarkets/hypermarkets, convenience stores, online retail channels, and other distribution channels. It provides an analysis of the frozen food market in the emerging and established markets across the region, including United Arab Emirates, Saudi Arabia, South Africa, and Rest of Middle East and Africa. The report offers market size and forecasts in value (USD million) for the above segments.

By Product Type

| Frozen Fruits and Vegetables |

| Frozen Meat and Fish |

| Frozen Cooked Ready Meals |

| Frozen Desserts |

| Frozen Snacks |

| Other Product Types |

By Category

| Organic |

| Conventional |

By Distribution Channel

| Supermarkets/ Hypermarkets |

| Convenience Stores |

| Online Channels |

| Other Distribution Channels |

By Geography

| United Arab Emirates |

| Saudi Arabia |

| Oman |

| Qatar |

| Bahrain |

| Kuwait |

| South Africa |

| Egypt |

| Nigeria |

| Iraq |

| Rest of Middle East and Africa |

| By Product Type | Frozen Fruits and Vegetables |

| Frozen Meat and Fish | |

| Frozen Cooked Ready Meals | |

| Frozen Desserts | |

| Frozen Snacks | |

| Other Product Types | |

| By Category | Organic |

| Conventional | |

| By Distribution Channel | Supermarkets/ Hypermarkets |

| Convenience Stores | |

| Online Channels | |

| Other Distribution Channels | |

| By Geography | United Arab Emirates |

| Saudi Arabia | |

| Oman | |

| Qatar | |

| Bahrain | |

| Kuwait | |

| South Africa | |

| Egypt | |

| Nigeria | |

| Iraq | |

| Rest of Middle East and Africa |

Key Questions Answered in the Report

How large is the MEA frozen food market in 2026?

The MEA frozen food market size is USD 9.35 billion in 2026, with a projected value of USD 11.44 billion by 2031.

Which product category leads sales across the region?

Frozen desserts hold the largest share at 32.62% in 2025, reflecting strong demand for ice cream and sweet snacks in hot climates.

What is the fastest-growing product segment?

Frozen meat and fish is forecast to expand at a 5.16% CAGR between 2026 and 2031 as urban consumers prioritize safe, long-shelf-life proteins.

Which country dominates regional revenue?

Saudi Arabia accounts for 37.77% of MEA frozen food market share in 2025 due to high incomes and sizable investments in processing capacity.

Page last updated on: