Market Overview

| Study Period | 2021 - 2031 |

|---|---|

| Forecast Data Period | 2026 - 2031 |

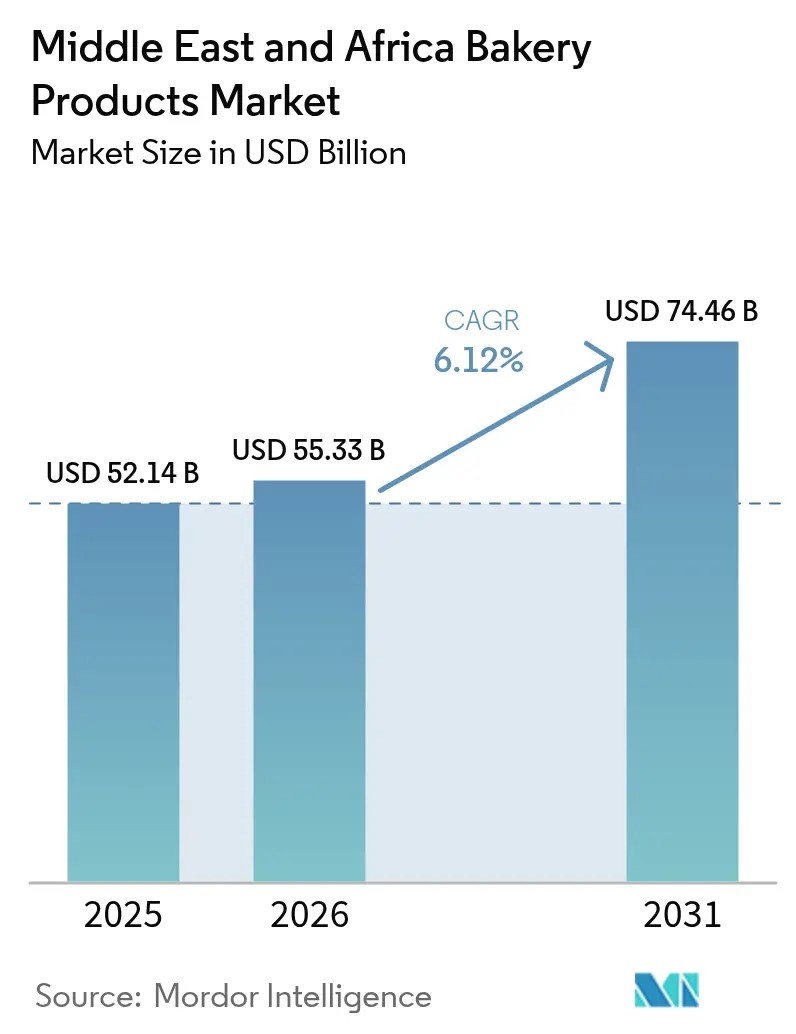

| Base Year Market Size (2025) | USD 52.14 Billion |

| Market Size (2026) | USD 55.33 Billion |

| Market Size (2031) | USD 74.46 Billion |

| Growth Rate (2026 - 2031) | 6.12% CAGR |

| Market Concentration | Medium |

Major Players

*Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. |

|

Middle East And Africa Bakery Products Market Analysis by Mordor Intelligence

The Middle East and Africa bakery products market size is expected to grow from USD 52.14 billion in 2025 to USD 55.33 billion in 2026 and is forecast to reach USD 74.46 billion by 2031 at 6.12% CAGR over 2026-2031. Urban migration is on the rise, and with the expansion of modern retail, bakery products are becoming an integral part of daily convenience eating in the Middle East and Africa. Saudi Arabia boasts a vast consumer base, South Africa's middle class is on the rise, and Turkey's milling sector is geared towards exports. Together, these dynamics bolster volume growth in the region by driving higher consumption and production levels. Meanwhile, trends like premiumization, a culture of gifting, and innovations catering to 'free-from' demands are driving up the market's value by appealing to evolving consumer preferences for quality and health-conscious products. Producers who automate their plants, diversify their grain inputs, and collaborate with e-commerce platforms are better positioned to safeguard their margins. This is crucial in an environment where energy volatility and currency fluctuations pose threats to supply continuity, as these strategies enhance operational efficiency and mitigate risks associated with supply chain disruptions.

Key Report Takeaways

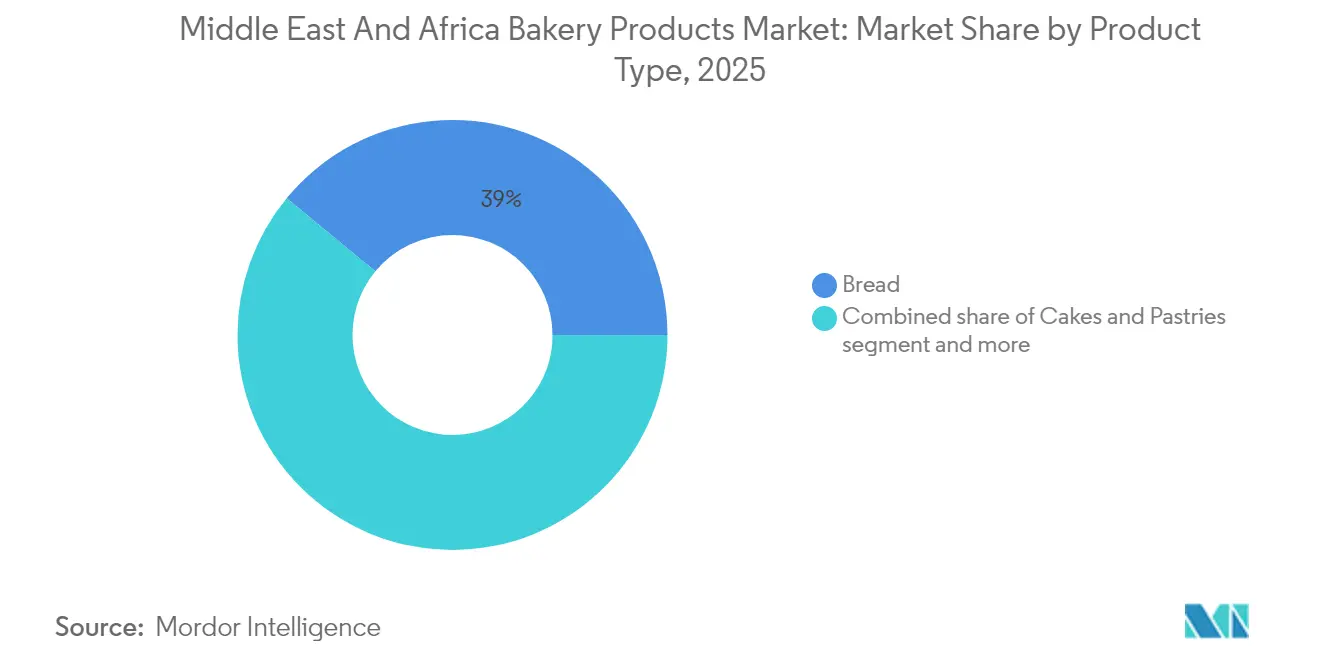

- By product type, bread led with a 39.02% share of the Middle East and Africa bakery products market in 2025, while cakes and pastries are forecast to grow at a 6.75% CAGR through 2031.

- By category, conventional lines accounted for 90.74% of 2025 revenue; free-from alternatives are set to expand at an 8.05% CAGR between 2026-2031.

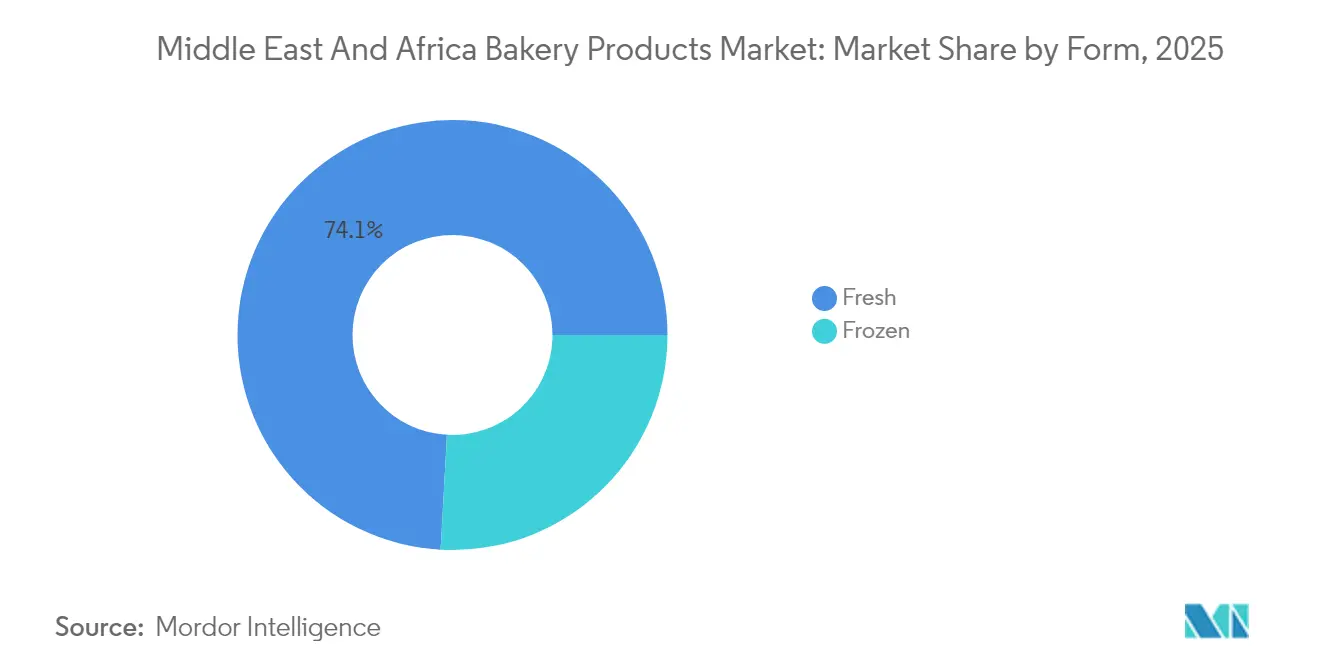

- By form, fresh items captured 74.12% of the Middle East and Africa bakery products market share in 2025, while frozen lines are poised to grow at 6.58% CAGR over the forecast period.

- By distribution channel, retail held an 81.96% revenue lead in 2025, and foodservice is projected to post a 7.16% CAGR to 2031 as foodservice recovers.

- By geography, Saudi Arabia contributed 19.05% of 2025 sales, whereas South Africa is forecast to post the fastest 7.78% CAGR through 2031.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of 2026.

Middle East And Africa Bakery Products Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~)% Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Rapid urbanization and modern retail expansion | +1.2% | Global, with strongest impact in Saudi Arabia, UAE, Nigeria, Turkey | Medium term (2-4 years) |

| Growing demand for healthier, fortified and "free-from" bakery lines | +0.9% | UAE, Saudi Arabia, Qatar core, spillover to South Africa | Long term (≥ 4 years) |

| E-commerce and last-mile delivery are unlocking new consumption occasions | +0.8% | Urban centers across all markets, led by UAE and Saudi Arabia | Short term (≤ 2 years) |

| Rising wheat import substitution policies driving composite flour innovation | +0.7% | Turkey, Nigeria, South Africa with regional supply chain benefits | Medium term (2-4 years) |

| Automation and Industry 4.0 are improving plant economics and capacity | +0.6% | Saudi Arabia, UAE, Turkey, South Africa manufacturing hubs | Long term (≥ 4 years) |

| Tourism-linked premiumization and gifting culture (Hajj, Expo, Expo 2025) | +0.5% | Saudi Arabia, UAE, Qatar with tourism spillover effects | Short term (≤ 2 years) |

| Source: Mordor Intelligence | |||

Rapid Urbanization and Modern Retail Expansion

Across urban food shopping corridors in Riyadh, Johannesburg, Lagos, and Dubai, modern grocery chains, hypermarkets, and convenience stores have taken center stage. These outlets are redefining the shopping experience by offering a wide range of products under one roof, catering to the evolving preferences of urban consumers. New outlets are now extending bakery aisles into the suburbs, offering 24-hour access to packaged loaves, snack cakes, and impulse pastries, ensuring convenience for customers with varying schedules. By adopting retail templates from Europe and North America, these outlets have set higher standards for hygienic packaging and ingredient disclosure, favoring branded lines over traditional unpackaged street bread. This shift not only enhances consumer trust but also aligns with global trends in food safety and transparency. Furthermore, the data-driven merchandising of modern trade is not only enhancing product development cycles but also enabling bakers to fine-tune stock-keeping units, catering to working consumers with longer commutes. Real-time sell-through data allows retailers to better understand consumer preferences, ensuring that shelves are stocked with products that resonate with their target audience. Government city-building programs, notably Saudi Vision 2030, funnel discretionary income into modern retail baskets where bakery staples top the convenience list[1]Source: Digital Government Authority, "Saudi Vision 2030", vision2030.gov.sa.

Growing Demand for Healthier, Fortified and “Free-From” Lines

As lifestyle-related disorders rise, there's a growing demand for products that are rich in fiber, boosted with protein, and low in sugar. Shoppers in the UAE are willing to pay a premium for items like chickpea-protein sandwich loaves, oat-fiber paninis, and gluten-free flatbreads. These products not only cater to traditional tastes but also align with health-conscious goals. In both Saudi Arabia and the UAE, tax penalties on sugar-sweetened beverages are pushing bakers to reformulate their sweet offerings, leaning towards naturally sweetened or reduced-sugar variants. Food technologists are turning to date paste, stevia, and apple-fiber blends, ensuring products maintain their moisture and softness without the usual sucrose spikes. Additionally, consumer apps that scan barcodes for ingredient alerts are pressuring bakers to simplify their labels and eliminate artificial improvers.

E-Commerce and Last-Mile Delivery Unlocking New Consumption Occasions

Quick-commerce platforms like Talabat and Instashop now deliver muffins, croissants, and birthday cakes in under 60 minutes. This rapid service enables bakers to sidestep physical shelf constraints, offering fresher and shorter-coded items, which cater to the growing consumer demand for convenience and quality. Collaborating with local influencers, social-commerce amplifies limited-edition launches, transforming Ramadan pastries and National Day cakes into viral, high-margin sensations that drive significant consumer engagement and brand visibility. Urban professionals are increasingly opting for subscription models, scheduling daily bread deliveries right in time for breakfast, which aligns with their busy lifestyles and need for consistency. Additionally, strategic cold-chain investments are expanding the market reach for frozen dough and par-baked items, which were previously limited to institutional buyers, enabling businesses to tap into new customer segments and geographic areas.

Rising Wheat Import Substitution Policies Driving Composite Flour Innovation

Turkey and Nigeria are taking significant steps to reduce their reliance on foreign currency by promoting the use of locally sourced grains through their milling and cassava-blend initiatives. In Turkey, the export-led milling industry focuses on incorporating local grains, while Nigeria emphasizes cassava blends to achieve similar goals. Bakers in these regions are actively experimenting with blends of sorghum-wheat and millet-wheat. These innovative blends not only maintain the loaf's volume and crust color but also contribute to reducing import costs, which is a critical factor for economies with high foreign-exchange exposure. To address the challenges posed by the weaker gluten matrices in composite flours, bakers are investing in advanced equipment. High-shear mixers and extended proofers are being installed to ensure the crumb structure remains intact and to extend the shelf life of the bread. Furthermore, successful formulations are gaining recognition and receiving procurement preferences in public-sector feeding programs, which play a pivotal role in scaling up their adoption and encouraging broader use of these blends.

Restraints Impact Analysis*

| Restraint | (~)% Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Volatile global wheat prices and logistics disruptions | -1.1% | Global, with highest impact on import-dependent markets like UAE, Qatar | Short term (≤ 2 years) |

| Energy and cooling costs squeezing bakery margins | -0.8% | Nigeria, South Africa, Turkey with high energy intensity | Medium term (2-4 years) |

| Stringent sugar-reduction / HFSS regulations | -0.4% | Saudi Arabia, UAE, Qatar with expanding regulatory frameworks | Long term (≥ 4 years) |

| Skilled-labor shortages accelerating wage inflation | -0.6% | Saudi Arabia, UAE, Qatar with nationalization policies | Medium term (2-4 years) |

| Source: Mordor Intelligence | |||

Volatile Global Wheat Prices and Logistics Disruptions

In recent seasons, global wheat benchmarks have fluctuated by over 30%, posing significant challenges for Gulf millers who rely heavily on U.S. dollar-priced imports to meet local demand. When the naira or Egyptian pound depreciates, it exacerbates spikes in landed costs, making wheat imports increasingly expensive. As a result, bakers are either reducing loaf sizes or substituting wheat with more affordable grains to manage costs. Furthermore, logistical issues such as port congestion and surcharges on Red Sea freight insurance are further eroding profit margins for millers. In response to these pressures, larger producers are adopting strategies to mitigate risks, including hedging with futures contracts to stabilize costs and diversifying their sourcing by turning to Black Sea and South American cargoes, which offer more competitive pricing and supply reliability.

Energy and Cooling Costs Squeezing Bakery Margins

Energy costs account for 20-40% of a bakery's operating expenses, with ovens alone consuming 70-80% of gas usage. This makes energy price volatility a crucial factor in determining profit margins across the region. Manufacturing firms in Ethiopia face an average monthly cost of ETB 51,777 (approximately USD 976) due to power interruptions. This cost highlights the challenges of energy reliability, which go beyond just pricing issues. In several developing countries, while petroleum subsidies are intended to support manufacturing, they often unintentionally hinder investments in reliable electricity infrastructure. This creates a paradox: the very subsidies meant to aid manufacturing can compromise its operational reliability. According to the ILO, the dual challenges of unreliable and costly energy are significant constraints for African food processors[2]Source: International Labour Organization, " Promotion of decent work and a just transition, including skills development and lifelong learning, in the food and beverage industry", ilo.org. These challenges hinder their ability to add value and compete effectively in regional markets. For bakeries, the need for cooling and refrigeration, be it for fresh products or frozen dough, intensifies energy demands. This is especially challenging in hotter climates, where elevated ambient temperatures amplify cooling needs. While the shift to renewable energy sources promises long-term cost stability, it demands a hefty capital investment, a hurdle many regional bakery manufacturers find hard to overcome.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Product Type: Premium Cakes Outpace Staple Bread

In 2025, bread commands a dominant 39.02% share of the Middle East and Africa's bakery products market. This stronghold underscores bread's status as a staple, cherished across all income brackets in the region. The segment's resilience is bolstered by bulk flour contracts and deep retail penetration, ensuring price stability even amidst wheat price fluctuations. Bread's ubiquitous presence in both urban and rural diets highlights its fundamental role. A robust supply chain management guarantees its availability, spanning from modern retail outlets to traditional distribution methods. Even in the face of economic shifts, bread's essential nature and affordability keep it firmly in consumers' daily baskets.

On the other hand, the cakes and pastries segment is on a rapid ascent, with projections indicating a CAGR of 6.75%. This surge is fueled by an uptick in gifting occasions and a burgeoning café culture in major urban hubs. Manufacturers in this category are innovating, offering everything from single-serve chiffon slices to grand multi-layer celebration cakes. This strategy caters to consumers seeking both weekday snacks and weekend treats. Flavor innovations often spotlight premium local ingredients, like date caramel and pistachio ganache, resonating with locals and international tourists in search of genuine souvenirs. The segment's growth is further propelled by a rising appetite for premium artisanal products and the burgeoning presence of boutique bakeries and specialty food outlets. Tapping into cultural trends tied to celebrations and social events, the cakes and pastries segment is broadening its appeal from daily treats to centerpiece offerings for special occasions.

By Category: Free-From Lines Scale But Remain Niche

In 2025, conventional bakery items dominated the Middle East and Africa market, capturing a substantial 90.74% of sales. This stronghold can be attributed to consumers' price sensitivity and deep-rooted culinary traditions. Typically crafted from wheat flour, sugar, and yeast, these items are not just staples but also cherished comfort foods across diverse income brackets. The bread and staple bakery segment, bolstered by bulk flour contracts and widespread retail presence, has managed to keep prices accessible, even when wheat prices fluctuate. Such stability has fortified conventional bakery goods against economic upheavals. Consumers are drawn to these products not only for their affordability and widespread availability but also for their cultural significance in daily meals. Major players, like Grupo Bimbo, adeptly utilize their established distribution networks to ensure the efficient supply of these conventional items, further cementing their dominant market presence and driving high sales volumes.

On the other hand, the free-from bakery category is emerging as the market's fastest-growing segment, projected to surge at an impressive 8.05% CAGR. This growth is largely fueled by heightened awareness of gluten intolerance among physicians and the clean-label lifestyle trends championed by influencers. Notably, gluten-free offerings, such as flatbreads crafted from rice-tapioca blends, are retailing at prices two to three times higher than their standard pita counterparts, ensuring robust margins for trailblazing brands. Meanwhile, sugar-free sandwich buns, sweetened with alternatives like monk fruit extract, are becoming increasingly favored by health-conscious and diabetic consumers. This trend underscores a rising demand for functional bakery items. To further penetrate this segment, larger baking groups are strategically placing free-from SKUs alongside mainstream products in retail spaces, effectively lowering the barriers for consumer trials. Moreover, the segment is witnessing innovations that cater to health concerns while satisfying the consumer's desire for indulgence. In essence, the free-from bakery category is not just growing; it's redefining the market with a focus on premiumization and wellness-centric consumption patterns.

By Form: Frozen Lines Gain Share Through Convenience

In 2025, fresh loaves and pastries command a dominant 74.12% share of the baked goods market. The enticing aroma of freshly baked bread and the delicate softness of pastries consistently signal quality to consumers, solidifying this segment's status as the go-to choice for daily purchases. Hypermarkets, local bakeries, and quick-service retailers leverage the unmatched sensory allure of fresh-baked goods to draw in foot traffic. The immediate availability of these items, coupled with an emotional connection to their freshness and authenticity, drives repeat purchases. Cultural traditions further bolster the demand for bread, especially in regions where daily bread shopping is customary. Despite technological advancements enhancing frozen products, the perception of freshness as the gold standard in the bakery industry remains unchallenged. This deep-rooted market leadership explains why producers emphasize freshness, artisanal craftsmanship, and in-store baking displays to sustain their dominance.

On the other hand, frozen bakery products are on a rapid ascent, with projections indicating a 6.58% CAGR. This surge is largely attributed to improvements in cold-chain logistics and the strategic placement of freezer endcaps in hypermarkets, amplifying product visibility. Innovations like flash-frozen croissant dough are a boon for hotels and foodservice establishments, allowing them to achieve top-notch lamination without the need for specialized pastry chefs. Households, too, are embracing convenience with par-baked baguettes that achieve an authentic French-style crust in just 10 minutes. Producers are channeling investments into advanced nitrogen-freezing tunnels, which not only preserve moisture and flavor but also bridge the sensory divide with fresh goods. This leap in product quality empowers manufacturers to extend their distribution beyond traditional daily delivery zones, reaping economies of scale. Collectively, these advancements are reshaping the perception of frozen bakery items, positioning them as serious contenders in the market.

By Distribution Channel: Foodservice Recovery Re-balances Mix

In 2025, retail channels took the lead in bakery distribution, clinching a notable 81.96% share of the revenue pie. Supermarket planograms, where category captains deftly position products at eye level, play a pivotal role in this dominance, boosting both visibility and sales. Meanwhile, neighborhood minimarkets are vital for fostering repeat purchases, providing easy access to daily bread and pastry essentials. Retailers often employ strategies like cross-category bundle deals, pairing bread with spreads, nudging households to buy in bulk rather than just individual items. The vast reach of supermarkets, combined with the concentration of local retail outlets, solidifies off-trade as the go-to for bakery purchases. Moreover, off-trade's supremacy is bolstered by consumers' inclination towards affordability and consistency, cementing its status as the revenue backbone of the bakery sector.

Conversely, the on-trade channel is swiftly gaining momentum, with projections pointing to a CAGR of 7.16% as dining out becomes more frequent. Establishments like cafés, quick-service restaurants, and hotels are turning to bakery items, not just to diversify their menus but also to elevate the dining experience. A key growth catalyst is the advent of frozen dough solutions, which cut down proofing time and streamline operations. This innovation empowers HORECA buyers to serve fresh, top-notch products without the need for specialized artisan staff. Furthermore, corporate canteens, campus dining services, and institutional caterers are venturing into subscription-based bakery programs, especially for croissants. This strategy ensures steady volume commitments from industrial bakers, smoothing out supply chains and guaranteeing foodservice operators consistent access to premium offerings. With an increasing number of hospitality and foodservice venues emphasizing both quality and operational efficiency, the on-trade channel is poised to seize a larger share of the bakery sector's value, outpacing other channels in growth.

Geography Analysis

In 2025, Saudi Arabia's sales reached 19.05%, driven by its vast population, rising disposable incomes, and a bold retail mall strategy that positions in-store bakeries as central attractions. Under the Vision 2030 initiative, Saudi Arabia is channeling international tourists into its airports and bustling high-street cafés, where premium date cakes and saffron buns are in high demand. Meanwhile, in the health-conscious expatriate neighborhoods of Riyadh, there's a growing appetite for 'free-from' bread lines.

The United Arab Emirates, capitalizing on its status as a trade hub, prominently features both imported artisanal brands and local labels. With a high per-capita income and a majority expatriate population, there's a robust demand for everything from sourdough boules to Asian-style chiffon cakes. In Dubai, where e-commerce penetration surpasses 90%, the surge in direct-to-consumer launches is evident, spotlighting the Middle East and Africa's expanding bakery products market amidst a backdrop of regional retail innovation.

South Africa, driven by a burgeoning middle class and robust cold-chain infrastructure, is at the forefront with an 7.78% CAGR. Retail behemoths, Shoprite and Pick n Pay, are rapidly rolling out private-label muffins and crusty rolls, expanding accessibility while keeping prices competitive. Nigeria, grappling with currency fluctuations, still holds a bright long-term promise, thanks to its vast 220-million population. Regional trade pacts, especially the African Continental Free Trade Area (AfCFTA), are set to lower tariff barriers and boost intra-regional trade. This shift stands to benefit bakery manufacturers adept in multi-country production and distribution. In the suburbs of Lagos, the growing trend of community bakeries and the shift towards composite flour are bolstering local supply chains. Turkey, celebrated for its pastry heritage and as a flour supplier to its neighbors, plays a crucial role, ensuring supply-chain resilience for the bakery products market spanning the Middle East and Africa.

Competitive Landscape

In the Middle East and Africa, the bakery products market showcases a moderate concentration, highlighting a competitive landscape where regional specialists vie with multinational giants eager to solidify or broaden their foothold. Companies boasting robust local market insights, streamlined distribution networks, and the agility to tailor products to diverse cultural tastes and price points are finding favor in the market dynamics. The region's diverse consumer base, spanning various income levels and cultural backgrounds, further intensifies the competition, requiring players to adopt highly localized strategies to succeed.

Strategic trends point towards vertical integration. Top players are channeling investments into flour milling, ingredient sourcing, and forging retail alliances. This strategy not only helps them manage costs but also bolsters supply chain reliability, especially in the face of unpredictable commodity markets and logistical challenges. Additionally, vertical integration allows companies to maintain greater control over product quality and ensure timely delivery, which are critical factors in building consumer trust. There's a burgeoning opportunity at the crossroads of health-centric formulations and traditional flavors. Manufacturers adept at crafting products that align with nutritional standards while retaining cultural essence stand to gain a premium market position. For instance, the growing demand for whole-grain and gluten-free options, combined with the preference for traditional recipes, presents a lucrative avenue for innovation.

Disruptors on the rise include e-commerce brands harnessing direct-to-consumer avenues and subscription services. These disruptors are capitalizing on the increasing internet penetration and changing consumer shopping habits in the region. Meanwhile, established entities like Grupo Bimbo are showcasing how technology can be a game-changer. Through clean-label reformulations, strategic acquisitions, and enhanced operational efficiencies, they're capturing significant market shares. Furthermore, digital initiatives, such as AI-driven quality checks and IoT-based production oversight, are emerging as key differentiators. These advancements not only ensure consistent quality and cost savings but also aid in navigating regulatory landscapes across various production sites and markets. The adoption of such technologies also enables companies to respond swiftly to market demands and maintain a competitive edge in an evolving industry.

Middle East And Africa Bakery Products Industry Leaders

-

Modern Bakery LLC

-

Almarai Group

-

Grupo Bimbo

-

Lantmännen Unibake

-

Agthia Group

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- August 2025: New SA debuted its latest offering, the Sasko snack bun, in South Africa. This product launch is part of the company's strategy to expand its portfolio of convenient and innovative bakery items, targeting the increasing consumer preference for on-the-go snack options

- June 2025: Delite Foods introduced a new line of creamy cheesecakes in South Africa. The launch reflects the company's focus on diversifying its dessert offerings to meet the rising demand for premium and indulgent sweet treats in the market.

- April 2025: Michelin-starred chef Askar unveiled his latest cafe in Istanbul, specializing in artisanal bread and a variety of baked goods. The cafe aims to cater to the growing demand for high-quality, handcrafted bakery products in the region, offering a unique culinary experience to its customers.

- February 2025: Halk Ekmek Inc, a Turkish company, rolled out its latest offerings, including Sourdough Bread, Gourmet Hamburgers, and a selection of baked goods, nationwide in Turkey. This product expansion aligns with the company's goal to strengthen its presence in the Turkish bakery market by providing a wider range of high-quality baked products to consumers.

Middle East And Africa Bakery Products Market Report Scope

Bakery products are prepared from flour or meal derived from some form of grains and are available in a wide range.The Middle East and African bakery products market is segmented by product type, distribution channel, and country. Based on product type, the market is segmented into cakes and pastries, biscuits and cookies, bread, morning goods, and other product types. Based on the distribution channel, the market is segmented into hypermarkets/supermarkets, convenience stores, specialty stores, online retailing, and other distribution channels. Also, the study analyzes the bakery products market in emerging and established markets across the Middle East and Africa, including South Africa, Saudi Arabia, and the Rest of the Middle East and Africa. For each segment, the market sizing and forecasts have been done based on value (in USD Million).

By Product Type

| Bread |

| Cakes and Pastries |

| Biscuits and Cookies |

| Morning Goods (Muffins, Doughnuts, Croissants) |

| Others |

Category

| Conventional |

| Free From |

Form

| Fresh |

| Frozen |

Distribution Channel

| Foodservice | |

| Retail | Supermarkets/Hypermarkets |

| Convenience Stores | |

| Specialist Bakeries | |

| Online Retail Stores | |

| Others |

By Geography

| Saudi Arabia |

| United Arab Emirates |

| Qatar |

| Kuwait |

| Oman |

| Bahrain |

| South Africa |

| Nigeria |

| Turkey |

| Rest of Middle East and Africa |

| By Product Type | Bread | |

| Cakes and Pastries | ||

| Biscuits and Cookies | ||

| Morning Goods (Muffins, Doughnuts, Croissants) | ||

| Others | ||

| Category | Conventional | |

| Free From | ||

| Form | Fresh | |

| Frozen | ||

| Distribution Channel | Foodservice | |

| Retail | Supermarkets/Hypermarkets | |

| Convenience Stores | ||

| Specialist Bakeries | ||

| Online Retail Stores | ||

| Others | ||

| By Geography | Saudi Arabia | |

| United Arab Emirates | ||

| Qatar | ||

| Kuwait | ||

| Oman | ||

| Bahrain | ||

| South Africa | ||

| Nigeria | ||

| Turkey | ||

| Rest of Middle East and Africa | ||

Key Questions Answered in the Report

How big is the Middle East and Africa bakery products market in 2026?

The market stands at USD 55.33 billion in 2026 and is forecast to reach USD 74.46 billion by 2031.

Which country generates the highest bakery revenue in the region?

Saudi Arabia leads with 19.05% of 2025 sales thanks to population scale and retail modernization.

What is the fastest-growing product category through 2031?

Cakes & pastries post the highest forecast growth, advancing at a 6.75% CAGR.

Why are frozen bakery items gaining traction?

Improved cold-chain logistics and on-demand foodservice needs boost frozen products at a 6.58% CAGR.

Page last updated on: