Middle East and Africa Data Center GPU Market Size and Share

Market Overview

| Study Period | 2021 - 2031 |

|---|---|

| Forecast Data Period | 2026 - 2031 |

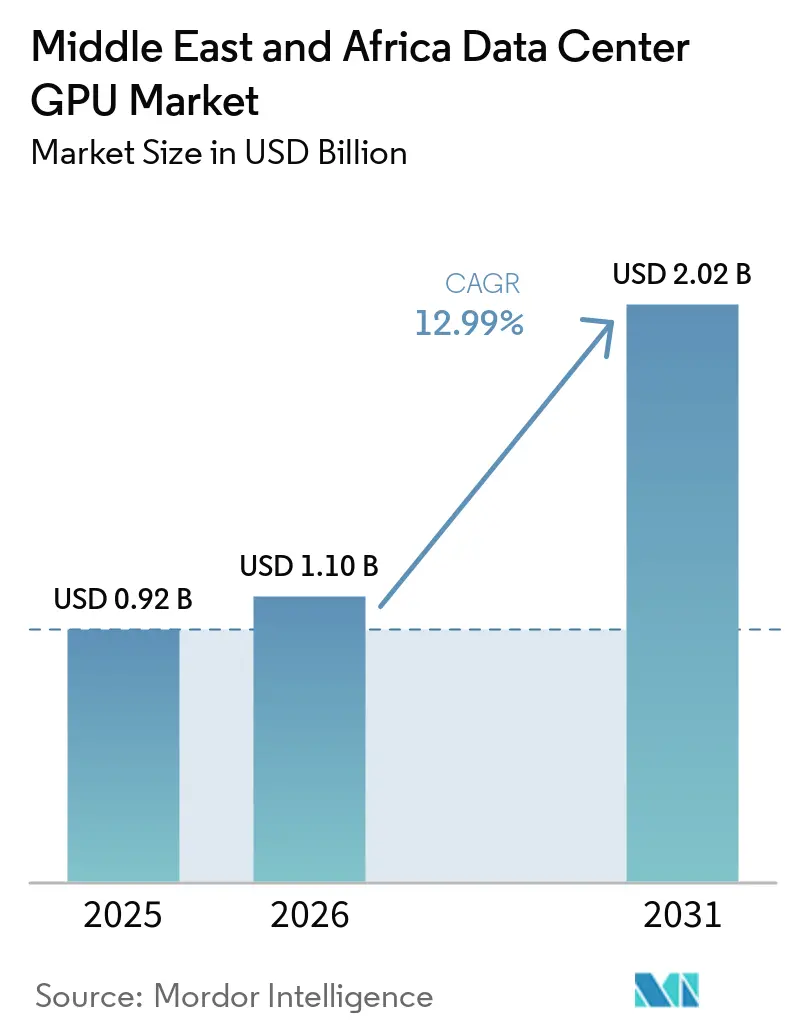

| Base Year Market Size (2025) | USD 0.92 Billion |

| Market Size (2026) | USD 1.10 Billion |

| Market Size (2031) | USD 2.02 Billion |

| Growth Rate (2026 - 2031) | 12.99% CAGR |

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

Middle East and Africa Data Center GPU Market Analysis by Mordor Intelligence

The Middle East and Africa data center GPU market size is projected to expand from USD 0.92 billion in 2025 and USD 1.10 billion in 2026 to USD 2.02 billion by 2031, registering a CAGR of 12.99% between 2026 and 2031. The pace of investment reflects a sharp shift in how AI infrastructure is funded across the region, with sovereign wealth funds moving faster than conventional enterprise budgets and shortening deployment schedules. Bilateral chip supply agreements also changed the region’s position in the global queue for advanced GPUs, which gave Gulf projects earlier access to high-end capacity than many enterprise buyers in other regions. Africa also moved into a stronger position as multi-country GPU commitments targeted South Africa, Nigeria, Kenya, Egypt, and Morocco for new AI-oriented data center capacity. Competitive conditions remain active rather than closed, because NVIDIA retained a strong lead in training shipments while AMD, Intel, hyperscalers, and regional operators increased their presence through joint ventures, campus builds, and open-ecosystem offerings. Growth opportunities remain strongest where operators can solve power, cooling, cable availability, and deployment speed at the same time, especially in projects tied to sovereign AI programs, industrial inference, and local data processing requirements.

Key Report Takeaways

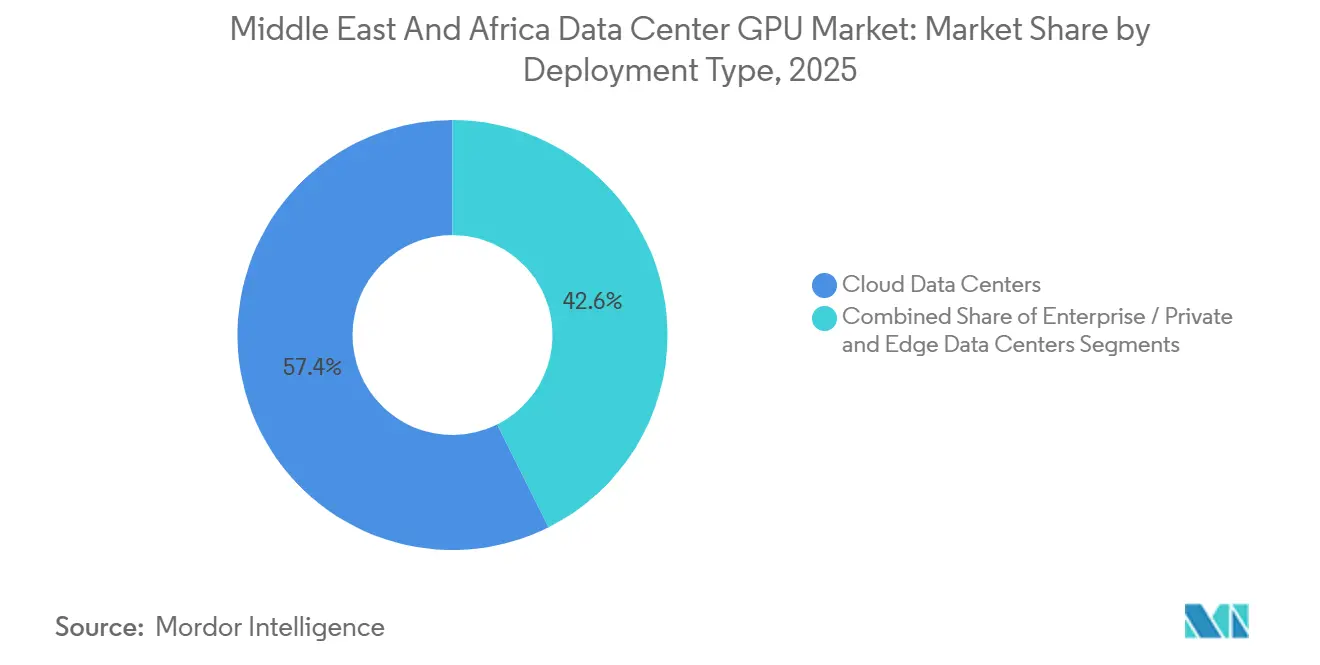

- By deployment type, cloud data centers held 57.39% of revenue in 2025, while edge data centers are projected to expand at 13.67% CGAR through 2031 as real-time inference moves closer to field locations and end users.

- By GPU type, inference GPUs accounted for 59.86% of revenue in 2025, and the same segment is expected to remain the fastest-growing at 13.89% CGAR category through 2031 as lower inference costs improve commercial adoption.

- By interconnect, PCIe-based GPUs captured 69.97% of revenue in 2025, while high-bandwidth interconnect GPUs are expected to expand faster at 14.67% CGAR through 2031 as large training clusters scale up.

- By workload type, artificial intelligence and machine learning workloads represented 58.44% of revenue in 2025, while data analytics is projected to record the fastest growth at 14.01% CGAR through 2031.

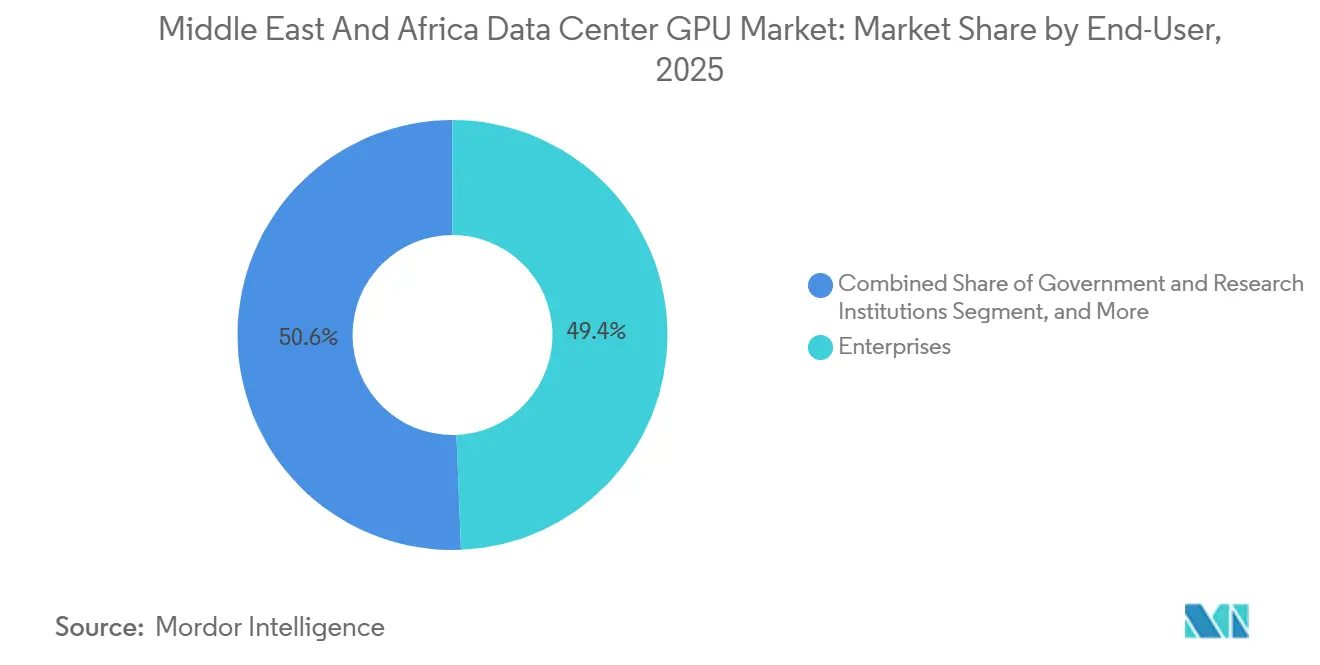

- By end user, hyperscalers and cloud service providers held 49.37% of the Middle East and Africa data center GPU market share in 2025, while enterprises are expected to at 14.37% CGAR grow the fastest through 2031 as on-premises infrastructure spending rises.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of January 2026.

Middle East and Africa Data Center GPU Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Accelerated Adoption of Generative AI and Large Language Models in Gulf Sovereign Initiatives | +3.2% | UAE, Saudi Arabia, Qatar, with spillover to Egypt and Morocco | Medium term (2-4 years) |

| Rapid Hyperscale Cloud Expansion Backed by Sovereign Wealth Funds | +2.8% | UAE, Saudi Arabia, Qatar, South Africa, Nigeria | Short term (≤ 2 years) |

| Hardware Innovation Cycle Toward High-Bandwidth Memory and Multi-Chip Module GPUs | +2.1% | Global, with early adoption in UAE and Saudi Arabia | Medium term (2-4 years) |

| Sovereign GPU Allocation Agreements Skewing Supply in Favor of MEA Projects | +1.9% | UAE, Saudi Arabia, Qatar | Short term (≤ 2 years) |

| Deployment of Waste-Gas-to-Power Data Centers in Middle East Oilfields | +0.8% | Saudi Arabia, UAE, Oman, Qatar | Long term (≥ 4 years) |

| Preferential Liquid-Cooling Infrastructure Grants in Desert Campuses | +0.7% | UAE, Saudi Arabia, Qatar | Medium term (2-4 years) |

| Source: Mordor Intelligence | |||

Accelerated Adoption of Generative AI and Large Language Models in Gulf Sovereign Initiatives

The Middle East and Africa data center GPU market is being pushed forward by sovereign AI programs that moved adoption windows from traditional multi-year cycles into much shorter deployment schedules. Saudi Arabia’s HUMAIN initiative partnered with xAI in January 2026 to deploy Grok-3 inference clusters across Riyadh and Jeddah, with a target of 50,000 concurrent Arabic-language queries by Q3 2026.[1]Reuters, “Saudi HUMAIN, xAI Announce Grok-3 Partnership,” Reuters, reuters.comIn the UAE, G42 operated a 200-megawatt AI campus in Masdar City that housed NVIDIA GB200 NVL72 racks designed for models with 1.8 trillion parameters, which placed the facility at a scale previously associated with U.S. hyperscalers. Morocco also moved into this pattern when the Nexus AI factory was announced with NVIDIA in November 2025, with a plan for 500 megawatts of GPU capacity by 2028 and a North African role in French and Arabic language model deployment. These projects matter because they absorb GPU supply faster than enterprise buyers that still move through quarterly budget approvals and compliance reviews. The result is a hardware mix that shifts toward training as well as inference, because localized language models require regional datasets, dialect support, and deployment under local legal and cultural frameworks.[2]Reuters, “US Approves 35,000 AI Chip Exports to Middle East,” Reuters, reuters.com

Rapid Hyperscale Cloud Expansion Backed by Sovereign Wealth Funds

The Middle East and Africa data center GPU market is also benefiting from sovereign wealth fund capital that lets hyperscalers secure land, power, and hardware earlier than peers in many other regions. Microsoft announced a USD 15.2 billion commitment to UAE AI infrastructure with G42 in March 2025, including a 200-megawatt expansion scheduled by the end of 2026. In Qatar, the Brookfield-Qai joint venture broke ground in February 2026 on a 100-megawatt compute center in Doha under a broader USD 20 billion commitment, with projected power costs of USD 0.06 per kilowatt-hour. Amazon Web Services expanded its Bahrain region with 3 additional availability zones in January 2026 and added GPU-optimized EC2 P5 instances based on NVIDIA H200 Tensor Core GPUs. This funding model removes the financing bottlenecks that often slow large cloud projects, which is why several MEA campuses moved toward operating status far faster than the longer timelines common in global builds. It also widened the addressable base of the Middle East and Africa data center GPU market, because capacity is being prepared not only for sovereign projects but also for enterprise tenants that need local hosting and AI acceleration.

Hardware Innovation Cycle Toward High-Bandwidth Memory and Multi-Chip Module GPUs

The Middle East and Africa data center GPU market is being shaped by a hardware cycle that makes premium deployments easier to justify despite high power and cooling costs. NVIDIA’s GB200 NVL72 rack combined 72 Blackwell GPUs with 1.44 terabytes of HBM3e memory and delivered 720 petaflops of FP4 throughput, while shipments to UAE and Saudi customers began in Q4 2025. AMD’s MI325X paired 288 gigabytes of HBM3e with a 6-nanometer compute die and a 5-nanometer I/O chiplet, which gave the platform 5.3 terabytes per second of memory bandwidth for large language model inference. Intel’s Gaudi 3 accelerator entered South African enterprise discussions through Dell PowerEdge XE9680 server shipments in early 2026, which gave customers another option when they wanted open software frameworks instead of full dependence on CUDA. Multi-chip approaches are especially relevant in hot climates because they spread thermal loads across smaller dies and help operators manage performance within tighter temperature limits. This innovation cycle is also shortening refresh expectations, since vendors can update compute or memory elements faster than in older monolithic designs, which keeps advanced campuses active buyers in the Middle East and Africa data center GPU market.[3]NVIDIA Investor Relations, “NVIDIA GB200 NVL72 Specifications,” NVIDIA, investor.nvidia.com

Sovereign GPU Allocation Agreements Skewing Supply in Favor of MEA Projects

The Middle East and Africa data center GPU market gained momentum from bilateral allocation agreements that gave Gulf projects access to advanced GPU shipments ahead of many competing regions. The U.S. Commerce Department approved exports of 35,000 Blackwell-equivalent GPUs to the UAE and Saudi Arabia in January 2025, which represented 12% of NVIDIA’s Q1 2025 data center GPU shipments. These volumes were tied to end-use monitoring agreements that limited re-export and required regular compliance checks, which effectively preserved supply for in-region deployment. Qatar secured a separate allocation of 8,000 H200 GPUs in March 2025, which helped pull forward the timeline for the Brookfield-Qai compute center by 6 months. Morocco also negotiated a 2026-2027 allocation of 15,000 GPUs through its Nexus AI factory arrangement with NVIDIA, subject to alignment with European Union-style data sovereignty principles. These agreements matter because chipmakers are clearly favoring customers that combine long-term geopolitical partnerships, infrastructure readiness, and regulatory certainty, and that directly improve execution visibility across the Middle East and Africa data center GPU market.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| High Power and Cooling OPEX in Desert Climates | -3.10% | Middle East | Medium term (2–4 years) |

| Semiconductor Export Restrictions Limiting High-End GPU Supply to Some African Countries | -2.40% | Africa | Short term (≤ 2 years) |

| Chronic DAC/AOC Fiber Lead-Time Bottlenecks for Large MEA GPU Clusters | -1.80% | Middle East, Africa | Medium term (2–4 years) |

| Scarcity of Local AI Infrastructure Talent Driving Deployment Delays | -1.30% | Middle East, Africa | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

High Power And Cooling OPEX In Desert Climates

The Middle East and Africa data center GPU market faces a direct cost challenge because desert facilities can operate at power and cooling costs above USD 0.12 per kilowatt-hour, while the global hyperscale average is near USD 0.06 per kilowatt-hour. A 10-megawatt GPU cluster running at 90% utilization in Riyadh or Abu Dhabi can incur annual electricity costs of USD 9.5 million, compared with USD 4.7 million for a comparable facility in Northern Europe. Extreme heat also forces operators to over-provision chillers by 30% to 40%, which pushes cooling capital expenditure to USD 1,200 per kilowatt against USD 800 per kilowatt in more temperate locations. Liquid-cooling systems can improve efficiency, but the HPE and Khazna partnership highlighted that these designs require specialized fluids and corrosion-resistant infrastructure that raise rack-level deployment costs. Waste-gas-to-power projects can help in selected oilfield locations, but they are not a region-wide answer because site selection, permitting, and construction are tightly constrained. This cost pressure is particularly severe for inference applications where revenue per query is very small, so operators need better power contracts, alternative energy arrangements, or higher-value workloads to protect margins in the Middle East and Africa data center GPU market.

Semiconductor Export Restrictions Limiting High-End GPU Supply to Some African Countries

The Middle East and Africa data center GPU market is also constrained by export controls that slow procurement in several African countries, even when local demand is in place. U.S. semiconductor export rules placed 14 African nations under case-by-case review, which delayed some GPU shipments by 90 to 120 days and created a more uneven regional supply picture. South Africa received Tier 1 status in March 2025, but Nigeria and Egypt remained subject to tighter review and quarterly volume limits. Cassava Technologies stated in its June 2025 investor update that export license processing added 14 to 16 weeks to procurement timelines and delayed the launch of its Johannesburg AI hub. Alternative China-origin GPUs were outside the U.S. control regime, but the software stack and third-party validation around those systems remained less developed for many enterprise buyers, which reduced their practical appeal. The result is a two-speed African market where South African operators can move faster on newer hardware while several peers in West and East Africa remain limited by licensing delays and lower visibility on delivery schedules.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Deployment Type: Edge Gains Ground as Inference Migrates to Field Sites

Cloud data centers held 57.39% of deployment-type revenue in 2025, which gave them the largest share of the Middle East and Africa data center GPU market size within this segment set. That position reflected hyperscaler strength in training workloads, centralized compute, and batch analytics across major Gulf campuses. Edge data centers are still expected to grow faster through 2026-2031 because field operations and urban service nodes are prioritizing local processing for response-sensitive use cases. Saudi Aramco deployed 12 edge GPU pods across the Ghawar and Safaniya oilfields in Q1 2026, and each pod contained 64 NVIDIA L40S inference GPUs for real-time seismic processing and drill-bit optimization. That example shows why edge deployments are becoming more practical in energy operations, where waiting for a centralized cloud response can reduce the value of the analysis. The Middle East and Africa data center GPU market is therefore widening beyond centralized campuses and into distributed environments that support industrial inference close to assets.

Enterprise and private data centers remained the second-largest deployment type because regulated industries still prefer direct control over data placement and compute resources. The UAE Central Bank issued guidance in August 2025 that required domestic banks to process customer transaction data within national borders, which pushed institutions such as Emirates NBD and First Abu Dhabi Bank toward private GPU systems. This type of regulatory push supports on-premise deployment even when cloud offerings are technically available. Edge sites also face higher per-rack capital costs, because rugged enclosures, redundant power, and remote connectivity requirements make these systems more complex to install. Even so, operators continue to fund them where real-time decision making in oil and gas fields, smart-city nodes, and transport corridors produces a clear operational return. That balance between centralized scale and local responsiveness is likely to keep all 3 deployment types relevant as the Middle East and Africa data center GPU market continues to expand.

By GPU Type: Inference Dominates as Cost-Per-Token Economics Unlock Commercial Scale

Inference GPUs held 59.86% of GPU-type revenue in 2025, which made them the leading product category in the Middle East and Africa data center GPU market. Their growth profile also remains the strongest through 2031 because lower inference costs changed the economics of deploying chatbots, voice systems, recommendation engines, and localized language services at commercial scale. The decline in per-token inference costs from USD 0.02 in early 2024 to USD 0.0008 by late 2025 was a major reason why real-time Arabic language applications became more viable across public and private deployments. G42 allocated 70% of its 200-megawatt Masdar City capacity to inference workloads in 2025, which shows that demand is now centered on serving users rather than only training frontier models. This demand pattern is especially visible in government portals, translation services, customer support, and enterprise AI tools, where scale depends on transaction cost, not only raw compute capability. The Middle East and Africa data center GPU market is therefore moving from a build-first phase into a serve-at-scale phase for many deployments.

Training GPUs remain essential even though they represent a smaller unit base, because sovereign AI programs still need local models trained on regional legal, medical, and language datasets. NVIDIA stated that H200 pricing sat well above inference-oriented L40S configurations, which keeps training systems concentrated in state-backed campuses and hyperscaler labs rather than broad enterprise rollouts. Saudi Arabia’s HUMAIN initiative used 10,000-plus H200 GPUs in a Riyadh facility that went live in January 2026 for Arabic legal and medical language models. This split between training and inference is important because it means revenue growth does not depend on one workload alone. Inference expands unit demand across more users and locations, while training supports a smaller number of very large projects with higher selling prices. That combination gives the Middle East and Africa data center GPU market both breadth and depth across the GPU-type mix.

By Interconnect: High-Bandwidth Fabrics Accelerate Despite PCIe Installed Base

PCIe-based GPUs accounted for 69.97% of interconnect revenue in 2025, which made them the largest installed option across the Middle East and Africa data center GPU market size for this category. Their lead came from the installed base of enterprise servers that already relied on PCIe Gen 5 slots and were well matched to inference, analytics, and modest-scale training workloads. These systems remain attractive where buyers want simpler integration, lower upfront networking cost, and a clear upgrade path from existing enterprise infrastructure. High-bandwidth interconnect GPUs are nonetheless expanding faster through 2031 because large sovereign and hyperscale campuses now require much stronger GPU-to-GPU communication for model training at scale. NVIDIA’s GB200 NVL72 rack delivered fifth-generation NVLink connectivity in the UAE and Saudi sovereign campuses in late 2025, which sharply reduced training time for very large model runs. The Middle East and Africa data center GPU market is therefore shifting toward a dual structure where PCIe remains broad, but high-bandwidth fabrics capture the most demanding AI projects.

AMD’s Infinity Fabric supported that shift by giving MI325X systems strong internal bandwidth and a more open software position for customers that wanted an alternative to NVIDIA’s ecosystem. At the large-cluster level, InfiniBand remained the preferred option for major training environments because Quantum-2 switches offered 400 gigabits per second per port and very low latency. The challenge is that this networking layer carries a meaningful cost premium over Ethernet, which limits adoption to projects with very large budgets and strong utilization expectations. That keeps high-bandwidth architectures concentrated in sovereign AI campuses, hyperscaler training centers, and a small number of premium enterprise deployments. PCIe-based environments will stay relevant in enterprise and edge settings where the application does not justify that higher capital and operational complexity. This balance between installed practicality and scaling performance is likely to remain central to the interconnect mix of the Middle East and Africa data center GPU market.

By Workload Type: Data Analytics Surges on Real-Time Processing Demand

Artificial intelligence and machine learning workloads captured 58.44% of revenue in 2025, which made them the largest workload group in the Middle East and Africa data center GPU market. That lead came from large language model inference, computer vision, recommendation systems, and public sector AI applications that were already active across Gulf cloud and sovereign campuses. Data analytics is still expected to grow faster through 2031 because financial institutions, energy companies, and digital commerce platforms increasingly need sub-second processing for operational decisions. Emirates NBD deployed NVIDIA A100 GPUs in August 2025 and reduced fraud screening time from 2.3 seconds to 180 milliseconds, which shows how GPU acceleration is moving into routine transaction analysis. Saudi Aramco also used GPU-accelerated seismic interpretation to process 40 terabytes of subsurface data per well in under 6 hours rather than 72 hours on CPU-only systems. These examples show that the Middle East and Africa data center GPU market is no longer tied only to generative AI narratives, because analytics workloads are producing direct value in banks, oilfields, and other real operating environments.

High-performance computing workloads remain more concentrated in government research institutions and universities, where scientific computing still justifies dedicated GPU clusters. Graphics and visualization use cases are also growing in architecture, engineering, and construction, but they remain smaller in revenue terms because utilization rates are lower than AI and analytics workloads. The workload mix matters because it broadens the customer base beyond a single buyer profile or a single compute pattern. AI and ML still anchor the largest share, but analytics is creating a second growth engine tied to everyday enterprise decision making. That shift supports more repeatable demand, because fraud detection, customer modeling, and seismic interpretation are recurring processes rather than occasional experiments. It also gives the Middle East and Africa data center GPU market a more balanced workload structure as new deployments move from proof of concept into production.

By End-User: Enterprises Close the Gap as Sovereign Mandates Lift On-Premise Demand

Hyperscalers and cloud service providers represented 49.37% of end-user spending in 2025, which made them the largest buyer group in the Middle East and Africa data center GPU market. Their position was supported by Microsoft’s UAE expansion, AWS capacity in Bahrain, and other large multi-tenant cloud investments that gave them scale in shared infrastructure. Even so, enterprises are expected to grow faster through 2031 because data residency rules and sovereign AI mandates are redirecting spending toward local and on-premise systems. First Abu Dhabi Bank installed a 128-GPU cluster in its Dubai data center in March 2026 and used AMD MI300X accelerators for credit risk and anti-money-laundering models. MTN Nigeria also partnered with Kasi Cloud in January 2026 to deploy a 200-GPU inference cluster in Lagos for network optimization and churn prediction. These moves show that the Middle East and Africa data center GPU market is seeing more direct enterprise ownership of AI infrastructure, where regulation, latency, or data sensitivity makes shared cloud less attractive.

Government and research institutions remained the third end-user group, but they are expanding steadily as national AI programs fund university clusters and applied research facilities. Saudi Arabia’s King Abdullah University of Science and Technology expanded its GPU cluster from 512 to 2,048 units in Q4 2025 to support desalination and renewable materials research. That type of deployment does not match hyperscaler scale, but it strengthens the local ecosystem for scientific computing and technical workforce development. It also aligns with sovereign efforts to keep model development, applied research, and advanced simulation work within national borders. As a result, end-user demand is broadening from a hyperscaler-led base into a more mixed structure that includes enterprises, government agencies, and research organizations. This wider demand pattern should make the Middle East and Africa data center GPU market less dependent on a single buyer class over the forecast period.

Geography Analysis

The Middle East held the largest share of regional revenue in 2025, and that leadership was built on sovereign AI commitments in the UAE and Saudi Arabia that exceeded USD 30 billion in announced capital. The Middle East and Africa data center GPU market share was therefore concentrated first in the Gulf, where policy alignment, capital access, and power planning moved faster than in most African markets. Saudi Arabia emerged as the largest single-country market in 2025, supported by the HUMAIN initiative’s 100-megawatt GPU deployment in Riyadh and the AMD-Cisco joint venture that targets 1 gigawatt by 2030. The UAE remained close behind through the G42-Microsoft partnership and Khazna’s 100-megawatt Ajman facility that went live in January 2026. Qatar also strengthened its role through the Brookfield-Qai program, which linked low-cost gas-backed power with a 100-megawatt compute center in Doha. Oman, Bahrain, and Kuwait remained smaller, but they benefited from spillover demand as hyperscalers and regional operators looked for additional sites that satisfied local data sovereignty requirements.

Africa is growing faster through 2026-2031, even though its base remained smaller than the Gulf in 2025. South Africa, Nigeria, and Egypt represented 70% of Africa’s 2025 revenue, which shows how concentrated early adoption still is within a handful of national markets. South Africa led the continent through its scale, stronger export status, and large campuses such as Teraco’s Johannesburg facility, which commissioned 3,000 GPUs in December 2025. Nigeria stood out as West Africa’s main growth center, supported by 86 megawatts of operational data center capacity, a larger development pipeline, and new projects such as Equinix LG3 and the MTN-Kasi Cloud deployment. Egypt continued to build its role as a North African gateway, especially for enterprise and government workloads that need regional reach and domestic processing controls. This means the Middle East and Africa data center GPU market is becoming more geographically balanced, but the lead African countries still dominate early-scale deployment.

Kenya and Morocco are the next markets to watch because both have clear positioning in broader multi-country AI infrastructure programs. Africa Data Centres used expansion capital to build out GPU-ready infrastructure in Nairobi and Mombasa, which improved Kenya’s role in East African enterprise and government demand. Morocco’s USD 1.2 billion Nexus AI factory with NVIDIA gave it a stronger bridge role between European and African AI workloads, especially for French and Arabic language model deployment. Ghana, Senegal, and Tanzania remained earlier-stage markets, where activity was still centered more on universities and public institutions than on large commercial campuses. Geographic expansion is therefore real, but it is unfolding in tiers based on capital access, regulatory status, export controls, and local infrastructure readiness. That tiered pattern will keep the Middle East as the revenue core in the near term, while Africa contributes more of the incremental growth in the Middle East and Africa data center GPU market over the forecast period.

Competitive Landscape

The Middle East and Africa data center GPU market showed moderate concentration in 2025, with NVIDIA holding an estimated 80% share of training GPU shipments while competition still widened across other parts of the value chain. AMD strengthened its position in February 2026 when it joined Cisco and Saudi Arabia’s HUMAIN initiative in a 100-megawatt Riyadh venture that aims for 1 gigawatt of MI-series capacity by 2030. Intel remained a smaller force, but Gaudi 3 gave enterprise buyers an open-ecosystem option in systems such as Dell’s PowerEdge XE9680 platform. Competition also extended beyond chip vendors, because liquid-cooling specialists, server makers, interconnect suppliers, and regional campus operators all shaped deployment outcomes. LiquidStack partnered with INNOVO and Castrol in November 2025 to deploy single-phase immersion cooling across UAE and Saudi sites, which directly addressed the thermal barrier that limits high-density AI racks in desert settings. This means vendor strength in the Middle East and Africa data center GPU market depends not only on GPU performance, but also on cooling, networking, delivery speed, and local execution support.

Regional operators have become more important because they often secure land, power, and government approvals faster than global entrants. Khazna targeted 1 gigawatt across Saudi Arabia, Egypt, Turkey, Kenya, France, and Italy, which showed how regional operators are scaling beyond a domestic footprint into a larger cross-border campus strategy. Africa Data Centres also planned 12,000 GPUs across 5 countries by late 2026, using local market knowledge and public-sector relationships to support multi-country rollout. Crusoe Energy added another layer of competition with its Oman waste-gas-to-power project, which tied GPU infrastructure to low-cost energy capture from oilfield operations. These examples show that the Middle East and Africa data center GPU market is not a simple vendor race between NVIDIA and AMD alone. It is a more complex contest where operators that solve infrastructure bottlenecks can capture value even when they do not produce the GPU itself.

Strategy has also split into 2 distinct paths, with hyperscalers building multi-tenant cloud environments and sovereign programs creating single-tenant campuses optimized for specific national workloads. NVIDIA’s Blackwell architecture set the performance benchmark for the highest-end training deployments, which helped the company protect its leadership in frontier model infrastructure. AMD’s MI455X roadmap pointed to a future offer centered on very high memory capacity and bandwidth, which could appeal to customers that place memory density ahead of peak compute AMD. Networking vendors also remained active, as Arista and Cisco pushed Ethernet fabrics that challenged InfiniBand in selected AI environments through lower-cost, low-latency switching options. As competition broadens across compute, memory, networking, cooling, and site development, the Middle East and Africa data center GPU market is likely to stay moderately concentrated at the chip level while becoming more contested across the rest of the infrastructure stack. That makes execution quality, local partnerships, and deployment speed just as important as raw silicon leadership in determining who wins the next wave of regional projects.

Middle East and Africa Data Center GPU Industry Leaders

NVIDIA Corporation

Amazon Web Services, Inc.

Advanced Micro Devices, Inc.

Microsoft Corporation

Google LLC

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- February 2026: AMD, Cisco, and Saudi Arabia's HUMAIN initiative announced a joint venture to deploy 100 megawatts of MI-series GPU capacity in Riyadh in 2026, scaling to 1 gigawatt by 2030, with an initial investment exceeding USD 500 million. The partnership positions AMD as the first non-NVIDIA vendor to secure a sovereign AI contract in the Gulf, leveraging MI325X and MI350 GPUs optimized for Arabic language model training.

- February 2026: Equinix opened its LG3 data center in Lagos, Nigeria, a 15-megawatt facility designed to support GPU-accelerated AI workloads for West African enterprises and hyperscalers. The facility is the company's first GPU-optimized deployment in sub-Saharan Africa and includes liquid-cooling infrastructure capable of supporting 100-kilowatt racks.

- February 2026: Qatar's Brookfield-Qai joint venture broke ground on a 100-megawatt compute center in Doha, anchored by a USD 20 billion capital commitment and targeting a 2027 launch. The facility will leverage Qatar's surplus liquefied natural gas to deliver power at USD 0.06 per kilowatt-hour, positioning the country as a cost-competitive alternative to the UAE and Saudi Arabia for hyperscale GPU deployments.

- January 2026: Khazna Data Centers commissioned its 100-megawatt AI-optimized facility in Ajman, UAE, the largest single-site GPU deployment in the Middle East as of Q1 2026. The campus houses NVIDIA GB200 NVL72 racks and employs single-phase immersion cooling to achieve a power usage effectiveness of 1.15, 30% below the regional average.

Middle East and Africa Data Center GPU Market Report Scope

Data Center GPU refers to a specialized graphics processing unit engineered for large-scale computing environments, such as enterprise data centers and cloud platforms, rather than for personal computers or gaming.

The Middle East and Africa Data Data Center GPU Market Report is Segmented by Deployment Type (Cloud Data Centers, Enterprise/Private Data Centers, and Edge Data Centers), GPU Type (Training GPUs, Inference GPUs), Interconnect (PCIe-Based GPUs, and High-Bandwidth Interconnect GPUs), Workload Type (Artificial Intelligence (AI) and Machine Learning (ML), High-Performance Computing (HPC) (non-AI scientific computing), Data Analytics (database acceleration, query processing), and Graphics and Visualization (VDI, rendering, digital twins)), and End-User (Hyperscalers/Cloud Service Providers, Enterprises, and Government and Research Institutions). The Market Forecasts are Provided in Terms of Value (USD).

| Cloud Data Centers |

| Enterprise / Private Data Centers |

| Edge Data Centers |

| Training GPUs |

| Inference GPUs |

| PCIe-Based GPUs |

| High-Bandwidth Interconnect GPUs |

| Artificial Intelligence and Machine Learning |

| High-Performance Computing (non-AI scientific computing) |

| Data Analytics (database acceleration, query processing) |

| Graphics and Visualization (VDI, rendering, digital twins) |

| Hyperscalers / Cloud Service Providers |

| Enterprises |

| Government and Research Institutions |

| Middle East | Saudi Arabia |

| United Arab Emirates | |

| Qatar | |

| Rest of Middle East | |

| Africa | South Africa |

| Nigeria | |

| Egypt | |

| Rest of Africa |

| By Deployment Type | Cloud Data Centers | |

| Enterprise / Private Data Centers | ||

| Edge Data Centers | ||

| By GPU Type | Training GPUs | |

| Inference GPUs | ||

| By Interconnect | PCIe-Based GPUs | |

| High-Bandwidth Interconnect GPUs | ||

| By Workload Type | Artificial Intelligence and Machine Learning | |

| High-Performance Computing (non-AI scientific computing) | ||

| Data Analytics (database acceleration, query processing) | ||

| Graphics and Visualization (VDI, rendering, digital twins) | ||

| By End-User | Hyperscalers / Cloud Service Providers | |

| Enterprises | ||

| Government and Research Institutions | ||

| By Geography | Middle East | Saudi Arabia |

| United Arab Emirates | ||

| Qatar | ||

| Rest of Middle East | ||

| Africa | South Africa | |

| Nigeria | ||

| Egypt | ||

| Rest of Africa | ||

Key Questions Answered in the Report

What is the 2026 size of the Middle East and Africa data center GPU space?

It stood at USD 1.10 billion in 2026 and is forecast to reach USD 2.02 billion by 2031 at a 12.99% CAGR.

What is driving demand for GPUs in Middle East and Africa data centers?

Sovereign AI programs, hyperscale cloud expansion, localized Arabic language model deployment, and faster enterprise adoption in banking, telecom, and energy are the main demand drivers.

Which deployment model leads regional revenue?

Cloud data centers led with 57.39% of deployment-type revenue in 2025, though edge data centers are expected to grow faster as field inference use cases expand.

Why are inference GPUs seeing stronger momentum than training GPUs?

Inference GPUs held 59.86% of GPU-type revenue in 2025, and lower per-token costs made chatbots, translation, and real-time AI services more commercially viable.

Which countries are shaping regional growth the most?

Saudi Arabia and the UAE led regional revenue in 2025, while South Africa, Nigeria, Egypt, Kenya, and Morocco are central to Africa’s next wave of expansion.

What are the main risks for operators and investors?

High desert power and cooling costs, export licensing delays in several African markets, cable lead-time bottlenecks, and local talent shortages can slow deployment and raise project costs.

Page last updated on: