United Kingdom Data Center GPU Market Size and Share

Market Overview

| Study Period | 2020 - 2031 |

|---|---|

| Forecast Data Period | 2026 - 2031 |

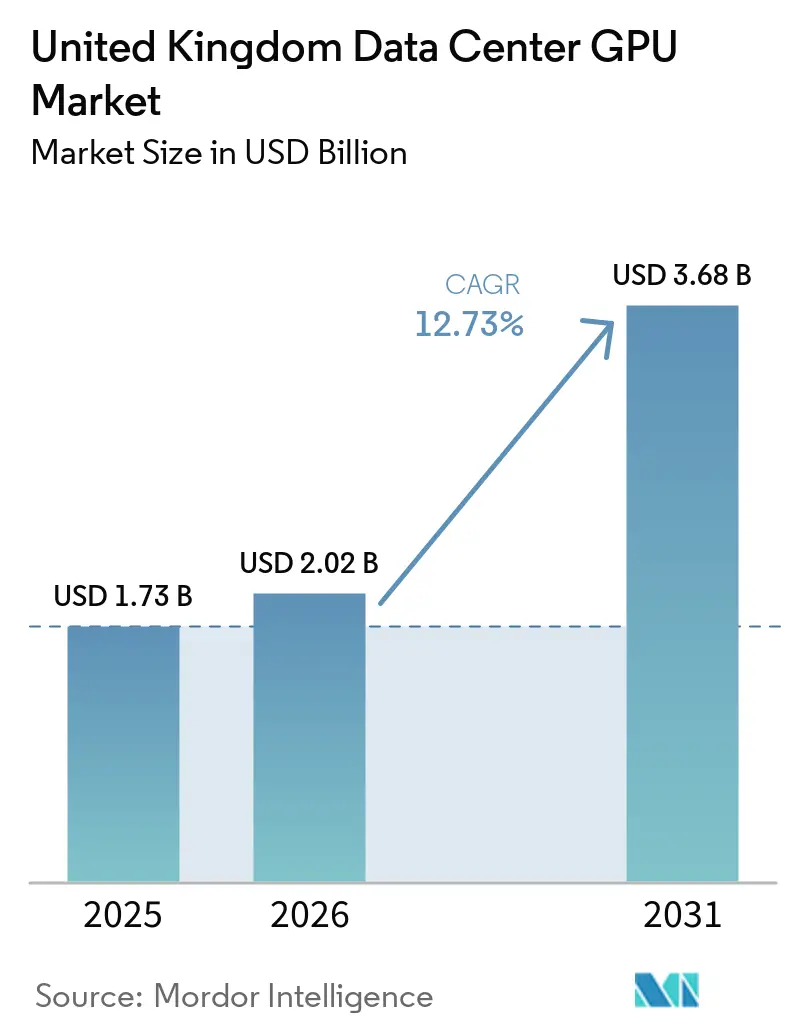

| Base Year Market Size (2025) | USD 1.73 Billion |

| Market Size (2026) | USD 2.02 Billion |

| Market Size (2031) | USD 3.68 Billion |

| Growth Rate (2026 - 2031) | 12.73% CAGR |

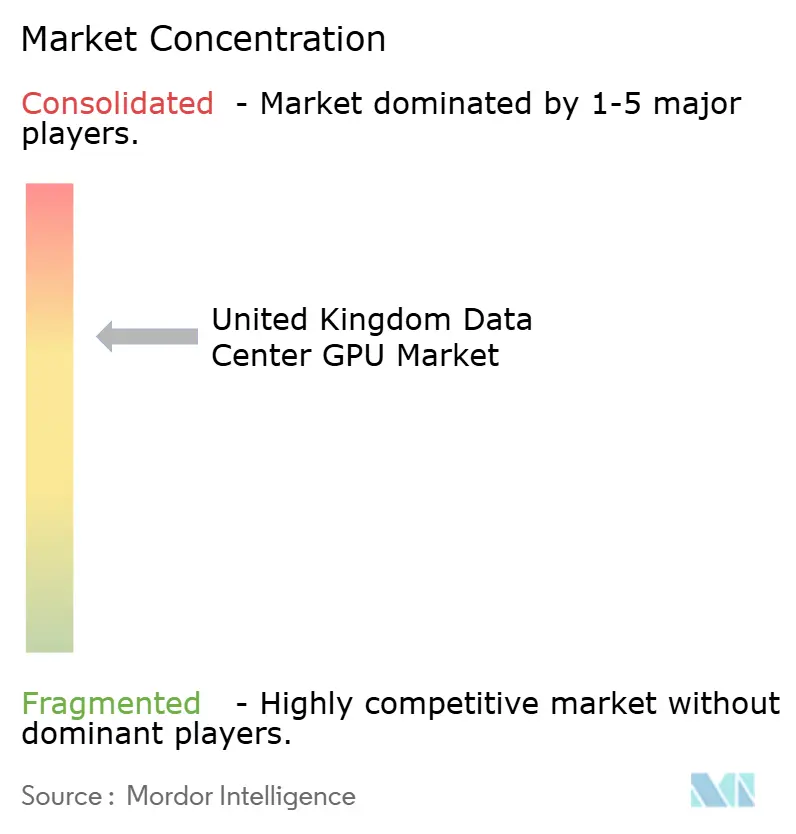

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

United Kingdom Data Center GPU Market Analysis by Mordor Intelligence

The United Kingdom data center GPU market size was valued at USD 1.73 billion in 2025 and is estimated to grow from USD 2.02 billion in 2026 to reach USD 3.68 billion by 2031, at a CAGR of 12.73% during the forecast period (2026-2031). The growth curve reflects a fundamental shift toward production AI, with inference workloads expanding far faster than model training, reshaping rack-level power density targets and prompting rapid adoption of liquid-cooled systems. Hyperscalers have already committed more than GBP 20 billion (USD 26.8 billion) in new capacity, while government-designated AI Growth Zones are steering fresh investment into Scotland, the North East, and Wales. Sovereign cloud providers are entering the field with vertically integrated offerings, responding to data-residency mandates and the surge of sensitive workloads from finance, healthcare, and defense. At the same time, supply-side friction ranging from constrained CoWoS packaging lines to steep U.K. electricity prices continues to pressure margins and accelerate interest in alternative accelerators and advanced cooling technologies.

Key Report Takeaways

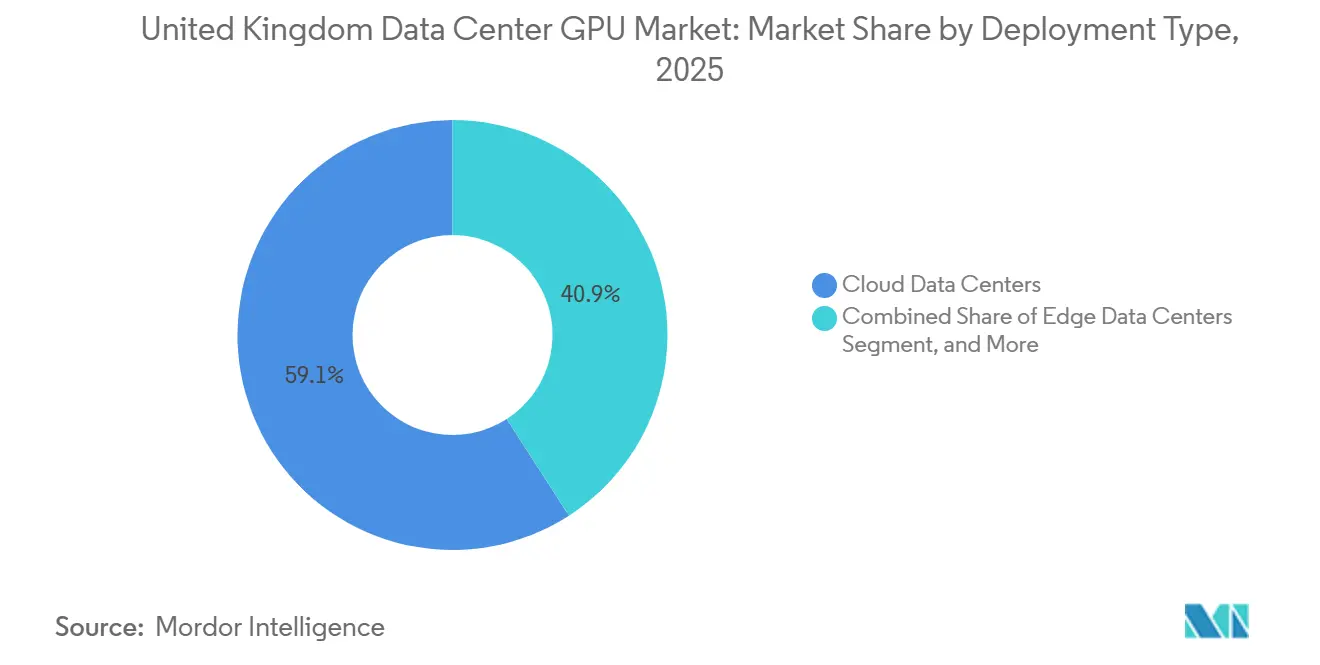

- By deployment type, cloud facilities led the United Kingdom data center GPU market with a 59.11% share in 2025, while edge data centers are projected to post the fastest growth at a 13.77% CAGR through 2031.

- By GPU type, inference devices commanded 55.66% of the United Kingdom data center GPU market share in 2025 and are pacing the field with a 14.11% CAGR through 2031.

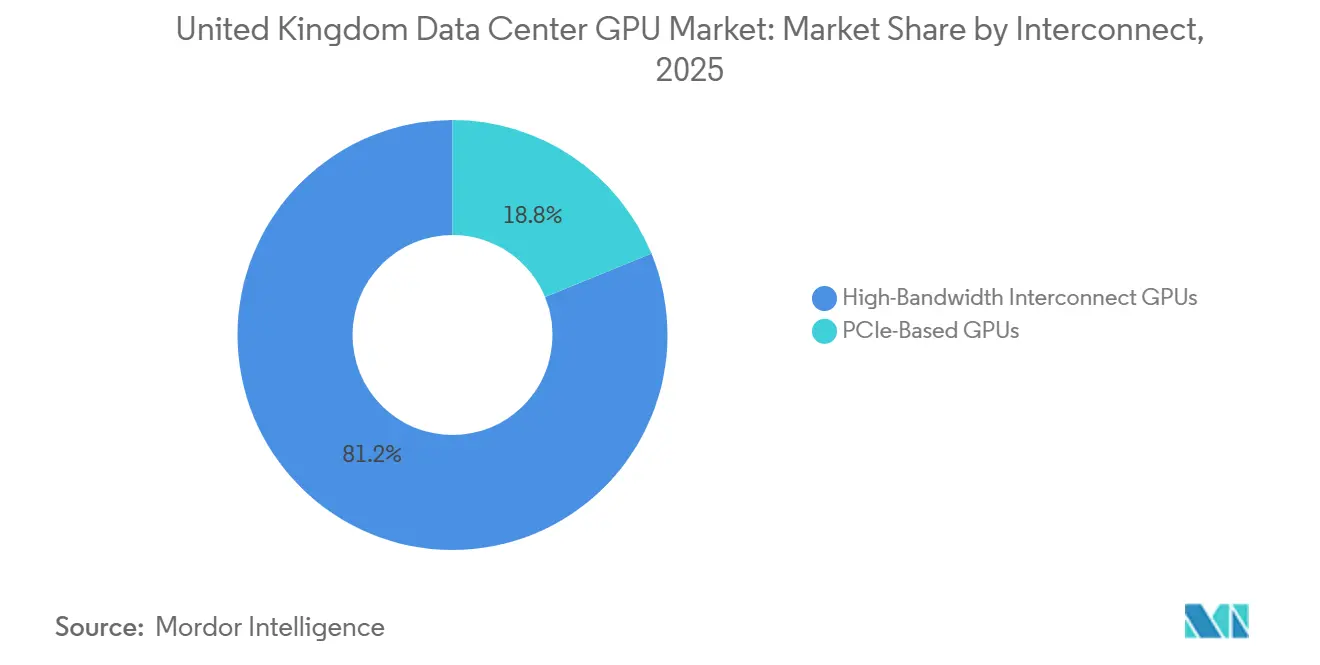

- By interconnect, PCIe-based boards accounted for 69.84% of the United Kingdom data center GPU market size in 2025, yet GPUs linked by high-bandwidth fabrics are advancing at a 13.45% CAGR to 2031.

- By workload, AI and machine learning accounted for 57.86% of the 2025 demand, while data analytics is expected to expand at a 14.61% CAGR through 2031.

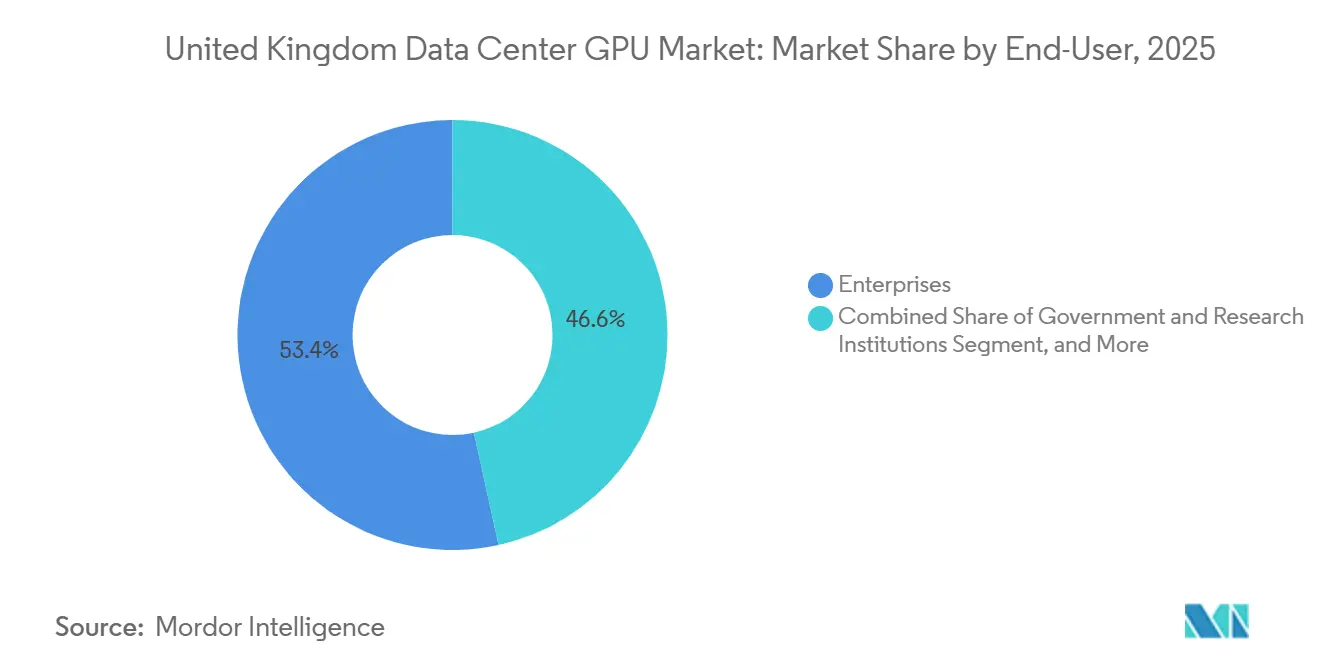

- By end user, enterprises held a 53.44% share of the United Kingdom data center GPU market in 2025, but government and research institutions are forecast to grow the fastest at a 14.36% CAGR through 2031.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of January 2026.

United Kingdom Data Center GPU Market Trends and Insights

Drivers Impact Analysis*

| DRIVER | (~) % IMPACT ON CAGR FORECAST | GEOGRAPHIC RELEVANCE | IMPACT TIMELINE |

|---|---|---|---|

| Accelerated Adoption of AI Workloads by United Kingdom Enterprises | +2.8% | London, Manchester, Edinburgh | Medium term (2-4 years) |

| Hyperscaler Expansion of United Kingdom Availability Zones | +2.5% | National, priority AI Growth Zones | Short term (≤ 2 years) |

| Government Incentives for Digital Infrastructure and AI Research | +2.2% | Scotland, Northeast, Cumbria, Wales | Long term (≥ 4 years) |

| Growing Demand for Sovereign Cloud GPU Instances | +1.8% | London and research institutions nationwide | Medium term (2-4 years) |

| Convergence of Edge Computing in Smart Manufacturing Corridors | +1.2% | Stockton-on-Tees, Teesside industrial belt | Long term (≥ 4 years) |

| Rise of Liquid-Cooled GPU Servers to Meet Sustainability Mandates | +1.0% | National, especially AI Growth Zones | Medium term (2-4 years) |

| Source: Mordor Intelligence | |||

Accelerated Adoption of AI Workloads by United Kingdom Enterprises

Enterprises are migrating live customer-facing applications from the public cloud to dedicated stacks that guarantee latency, compliance, and predictable costs. Private AI platforms offered by local integrators deliver turnkey clusters bundled with storage, networking, and managed software, compressing deployment cycles from months to weeks. Demand is especially strong in regulated verticals, banking, healthcare, and critical infrastructure, where on-premises control and auditability outweigh raw cloud elasticity. Hardware vendors respond with smaller, energy-efficient GPU SKUs that fit within existing power envelopes, enabling phased upgrades rather than greenfield builds.

Hyperscaler Expansion of United Kingdom Availability Zones

AWS, Microsoft, and Google are rolling out multi-year build programs that layer new availability zones on top of AI Growth Zone planning reforms. Construction lead times are shrinking because zoning approvals now take roughly 12 months, down from 18 previously. Hyperscalers gain priority grid connections, while local authorities retain all business rates for a quarter-century, creating a self-reinforcing loop of tax revenue and infrastructure expansion. Each of these hyperscale campuses reserves parcel space for renewable generation or private-wire import agreements, ensuring that incremental megawatts do not breach national carbon budgets. The hyperscaler land grabs, in turn, pull optical fiber backbones, data center housing, and tertiary suppliers into adjacent districts, raising the competitive bar for smaller colocations.[1]NVIDIA Corporation, “NVLink and High-Bandwidth GPU Interconnect,” nvidia.com

Government Incentives for Digital Infrastructure and AI Research

The AI Growth Zone framework offers electricity rebates of up to GBP 24/MWh (USD 32/MWh) and enables developers to self-build high-voltage substations, accelerating time-to-power by up to 5 years. A dedicated national planning task force is funded to standardize environmental assessments, removing the patchwork delays that have historically plagued large data projects. Parallel public funding lines UKRI’s GBP 2 billion (USD 2.68 billion) compute roadmap, and the National Wealth Fund co-financing window de-risks first-of-kind builds such as the 23-exaflop Isambard-AI supercomputer. These measures lower both CapEx and OpEx, tipping marginal projects in Scotland, Cumbria, and Wales into investable territory.[2]NVIDIA Corporation, “NVLink and High-Bandwidth GPU Interconnect,” nvidia.com

Growing Demand for Sovereign Cloud GPU Instances

Financial services, defense, and public sector buyers increasingly require locally domiciled compute that never leaves U.K. soil. Domestic cloud providers now bundle GPU capacity with contractual clauses for data residency, judicial oversight, and incident disclosure that hyperscalers refuse to offer. Series-C funding rounds topping USD 2 billion equip these challengers with the balance-sheet strength to lock in multi-year chip supply and energy hedges. The success of this segment is lifting utilization at regional campuses that would otherwise struggle against London’s network gravity.

Restraints Impact Analysis*

| RESTRAINT | (~) % IMPACT ON CAGR FORECAST | GEOGRAPHIC RELEVANCE | IMPACT TIMELINE |

|---|---|---|---|

| Supply Chain Constraints for Advanced GPUs | -1.5% | Global, with 50-week lead times, hitting U.K. buyers | Short term (≤ 2 years) |

| Rising Energy Costs and Carbon Targets | -1.3% | London and Southeast premium-price zones | Medium term (2-4 years) |

| Limited High-Bandwidth Interconnect Expertise Among Integrators | -0.8% | Nationwide outside major tech hubs | Medium term (2-4 years) |

| Competition from ASIC Accelerators for Inference Workloads | -0.7% | Global, alternatives under evaluation | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

Supply Chain Constraints for Advanced GPUs

CoWoS packaging bottlenecks and tight HBM3e supply push delivery windows beyond 50 weeks, relegating mid-tier enterprises to secondary allocation after hyperscalers. Spot pricing spikes force CFOs to weigh GPU rental at GBP 75-95 (USD 101.93 - 129.11) per hour against capital purchases that may not arrive for an entire budget cycle. The shortage is accelerating interest in ASICs and pushing software teams toward model compression to stretch existing hardware.

Rising Energy Costs and Carbon Targets

Electricity in the United Kingdom averages 35% above German rates, and quadruple U.S. prices, undermining price-sensitive AI training workloads that can execute anywhere fiber and cheap power coincide. Climate Change Agreement targets compel operators to cut energy intensity 14.5% by 2030, effectively capping total input MWh even as demand soars. Operators therefore race to deploy immersion and cold-plate cooling, which slash fan loads by up to 90%, though up-front retrofits can run USD 1 million per megawatt. Grid-parity renewable contracts and waste-heat reuse schemes are emerging as board-level KPIs, not optional extras.[3]UK Government, “Climate Change Agreements,” gov.uk

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Deployment Type: Edge Gains Ground as Latency Trumps Scale

Edge facilities captured a smaller share of the United Kingdom data center GPU market size in 2025, but are accelerating at a 13.77% CAGR through 2031 as manufacturers demand sub-10 millisecond inference. Stockton-on-Tees will host the first of 40 neural-edge sites, each optimized for compact 165 W RTX PRO GPUs, allowing factories to run visual inspection lines without shipping frames to London for processing.[4]Latos AI, “£100 Million Investment in Stockton-on-Tees AI Data Center,” latos.ai

Latency economics shape network topology. Hyperscalers respond by seeding micro-regions within carrier hotels and creating private transit rings to connect edge nodes back to their flagship campuses. For many mid-market enterprises, a hybrid approach dominates: bulk training jobs run in low-cost Scottish zones, while customer-facing inference runs on a metro-adjacent edge node. This choreography lets operators balance power-price arbitrage against compliance-driven data locality, sustaining cloud dominance for large-scale batch jobs while still rewarding edge expansion.

By GPU Type: Inference Overtakes Training as Production Workloads Scale

Inference silicon accounted for 55.66% of the United Kingdom data center GPU market share in 2025, outpacing training GPUs, which posted a 14.11% CAGR through 2031 as real-time customer interactions become the core workload.

Training remains mission-critical for foundation-model providers, but most enterprises now fine-tune rather than train from scratch, shrinking overall demand for top-bin HBM memory footprints. Vendors segment their catalog accordingly: dual-slot, 250 W inference boards proliferate, while ultra-dense NVLink trays cluster at hyperscale sites. This bifurcation allows operators to right-size deployments and diversify chip sourcing, a hedge against future supply disruptions.

By Interconnect: High-Bandwidth Fabrics Rise as Model Scale Demands Tighter Coupling

PCIe solutions still accounted for 69.84% of 2025 installations thanks to ubiquity and lower cost, yet GPUs tethered by NVLink 5 or 800 Gb/s InfiniBand are growing at a 13.45% CAGR through 2031. Model checkpoints with more than 100 billion parameters simply saturate PCIe, so forward-looking buyers bundle high-bandwidth networks with every rack, even if near-term workloads do not need them.[5]NVIDIA Corporation, “InfiniBand Networking Products,” nvidia.com

Skills scarcity slows adoption outside traditional tech clusters. To bridge the gap, OEMs ship reference architectures that integrate switches, cabling, and firmware state machines, reducing deployment time from months to weeks. Meanwhile, Ethernet-based RoCEv2 offers a middle path for operators unwilling to pay the full InfiniBand premium, though it sacrifices some determinism under congestion.

By Workload Type: Data Analytics Surges as Operational AI Displaces Experimentation

AI and machine learning still accounted for 57.86% of 2025 usage, but data analytics leads the growth chart with a 14.61% CAGR, mirroring the industry's migration from PoC sandboxes to revenue-generating decision engines. Vector search and semantic extraction pile more query traffic onto the same clusters, rewarding GPUs with high throughput over peak FLOPS.

High-performance computing retains its research niche, buoyed by sovereign initiatives such as Isambard-AI. Graphics and visualization, while smaller, unlock new use cases for digital twins and immersive training and help justify mixed-workload scheduling that maximizes GPU utilization. This diversification insulates operators from single-segment volatility and underpins steady demand across economic cycles.

By End-User: Government and Research Outpace Enterprises as Sovereignty Drives Procurement

Enterprises held 53.44% of the United Kingdom data center GPU market in 2025, yet public-sector buyers will notch the fastest gains at 14.36% CAGR through 2031. Government roadmaps fund supercomputers and carve out reserved cloud slices that smaller universities can tap without capital outlay, ensuring consistent baseline demand. AI Growth Zones further concentrate early projects at an Isambard-AI node here, a defense modeling cluster there, creating local ecosystems of contractors, students, and suppliers.

Enterprise budgets remain robust, but procurement teams lean on managed platforms to mitigate long inventory wait times. Subscription-based infrastructure bundles, where hardware, software, and support are billed monthly, flatten CapEx spikes and align spend with value capture. Together, these forces grow the addressable base while maintaining room for hyperscalers and sovereign innovators to differentiate.

Geography Analysis

London still hosts over four-fifths of installed capacity, yet grid constraints and soaring power tariffs compel new projects to fan outward. Scotland’s Lanarkshire AI Growth Zone secured GBP 1.5 billion (USD 2.01 billion) for a renewable-backed campus that will drive the growth of the United Kingdom data center GPU market in the region beginning in 2027. The Northeast follows with a targeted GBP 30 billion (USD 40.2 billion) pipeline anchored by Cobalt Park, while Teesside eyes one of Europe’s largest single-site builds.

Oxford’s Culham cluster benefits from fusion-related talent and existing nuclear grid nodes, positioning it as a scientific computing enclave. Wales leverages wind and tidal surplus, and Cumbria markets lake-water cooling potential, each sweetened by tailored electricity rebates kicking in from April 2027. Skills programs tie each zone to local universities, training thousands of technicians and dev-ops specialists to operate the next wave of liquid-cooled halls.

Legacy London operators respond by doubling down on efficiency: new West London builds a couple of district heating systems with 100% renewable PPAs to defend economics despite stubborn real-estate and power premiums. Over the forecast horizon, such adaptive strategies will converge, producing a two-tier geography where hyperscale AI clusters concentrate in rebate-rich zones while latency-sensitive enterprise nodes cling to metro fiber rings.

Competitive Landscape

Market concentration remains moderate. NVIDIA captures a significant share of the training board market today, but the share war is most intense in inference, where ASICs and rival GPUs erode its incumbency. AMD’s MI400 line, Intel-Lenovo bundles, and cloud-native silicon such as Trainium or TPU v7 collectively dilute NVIDIA’s grip, with projections showing the United Kingdom data center GPU leadership slipping by 2028. Hyperscalers use dual sourcing to hedge supply and pricing, while sovereign clouds offer data-residency guarantees that multinationals decline to offer.

OEMs pivot from box-shippers to solution providers, shipping pre-filled shipping racks with GPUs, storage, and AI frameworks, plus managed services. Liquid-cooling specialists Iceotope and Deep Green Energy insert themselves into value chains by proving 90% fan-load reductions that translate directly into PUE gains, a critical differentiator given the United Kingdom power costs. Vertical integration also rises as CoreWeave positions itself as a sovereign hyperscaler, controlling everything from renewable PPAs to Kubernetes control planes.

Taken together, these dynamics ensure a lively competitive theater where technology roadmaps, energy strategy, supply-chain resilience, and regulatory posture all influence buying decisions as much as raw chip performance.

United Kingdom Data Center GPU Industry Leaders

NVIDIA Corporation

Advanced Micro Devices, Inc.

Intel Corporation

Graphcore Ltd.

Imagination Technologies Ltd.

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- March 2026: Nscale closed a USD 2 billion Series C round to roll out 10,000 Blackwell GPUs across U.K. sites by Q1 2027.

- March 2026: Supermicro unveiled seven AI Data Platform solutions that integrate RTX PRO Blackwell Server Edition GPUs for turnkey enterprise deployments.

- March 2026: Dell Technologies expanded its AI Factory portfolio with Lightning File System and exascale storage optimized for Vera Rubin NVL72 clusters.

- March 2026: ARM launched the AGI CPU featuring 136 Neoverse V3 cores and liquid-cooled rack designs supporting 45,000 cores.

United Kingdom Data Center GPU Market Report Scope

The United Kingdom Data Center GPU Market Report is Segmented by Deployment Type (Cloud Data Centers, Enterprise/Private Data Centers, and Edge Data Centers), GPU Type (Training GPUs, and Inference GPUs), Interconnect (PCIe-Based GPUs and High-Bandwidth Interconnect GPUs), Workload Type (AI and ML, HPC, Data Analytics, and Graphics and Visualization), and End-User (Hyperscalers/CSPs, Enterprises, and Government and Research). The Market Forecasts are Provided in Value (USD).

| Cloud Data Centers |

| Enterprise / Private Data Centers |

| Edge Data Centers |

| Training GPUs |

| Inference GPUs |

| PCIe-Based GPUs |

| High-Bandwidth Interconnect GPUs |

| Artificial Intelligence (AI) and Machine Learning (ML) |

| High-Performance Computing (HPC) (non-AI scientific computing) |

| Data Analytics (database acceleration, query processing) |

| Graphics and Visualization (VDI, rendering, digital twins) |

| Hyperscalers / Cloud Service Providers |

| Enterprises |

| Government and Research Institutions |

| By Deployment Type | Cloud Data Centers |

| Enterprise / Private Data Centers | |

| Edge Data Centers | |

| By GPU Type | Training GPUs |

| Inference GPUs | |

| By Interconnect | PCIe-Based GPUs |

| High-Bandwidth Interconnect GPUs | |

| By Workload Type | Artificial Intelligence (AI) and Machine Learning (ML) |

| High-Performance Computing (HPC) (non-AI scientific computing) | |

| Data Analytics (database acceleration, query processing) | |

| Graphics and Visualization (VDI, rendering, digital twins) | |

| By End-User | Hyperscalers / Cloud Service Providers |

| Enterprises | |

| Government and Research Institutions |

Key Questions Answered in the Report

How big is the United Kingdom data center GPU market in 2026?

The market is valued at USD 2.02 billion in 2026.

Which GPU deployment type is expanding fastest in the United Kingdom?

Edge data centers are forecast to grow at a 13.77% CAGR through 2031, outpacing other deployment models.

Why are inference GPUs gaining share over training GPUs?

Enterprises are moving from model development to real-time AI services, making cost-efficient inference boards more attractive as token costs have fallen fifty-fold.

How are AI Growth Zones influencing regional GPU investment?

Electricity rebates and accelerated grid access in zones such as Lanarkshire and the Northeast are diverting new GPU capacity away from London toward renewable-rich regions.

Which workload category shows the fastest future expansion?

Data analytics workloads lead with a projected 14.61% CAGR as companies embed GPU-accelerated query and decision engines into daily operations.

Page last updated on: