GPU Orchestration Market Size and Share

Market Overview

| Study Period | 2020 - 2031 |

|---|---|

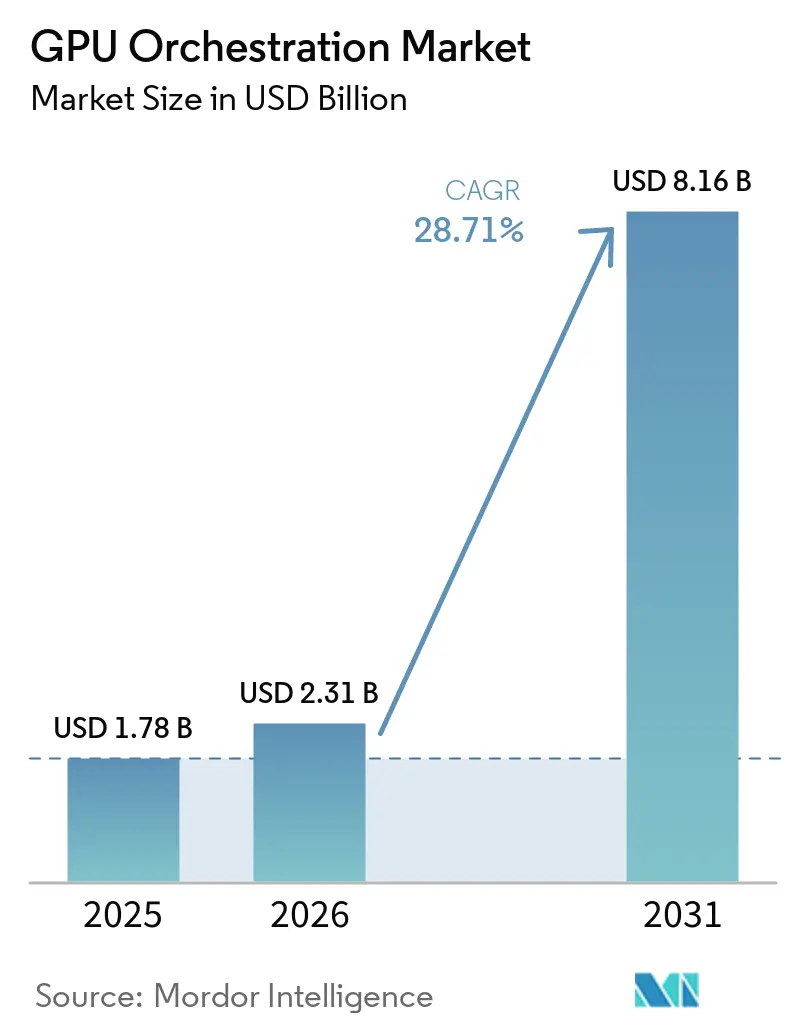

| Market Size (2026) | USD 2.31 Billion |

| Market Size (2031) | USD 8.16 Billion |

| Growth Rate (2026 - 2031) | 28.71% CAGR |

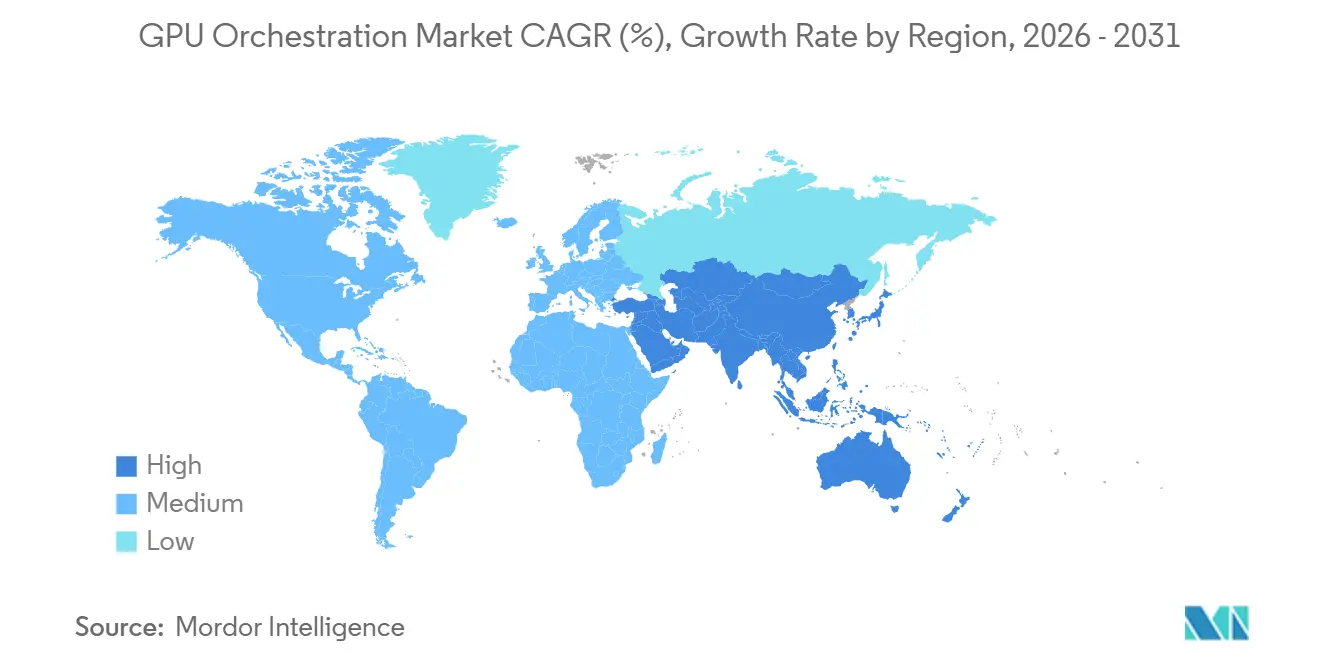

| Fastest Growing Market | Asia-Pacific |

| Largest Market | North America |

| Market Concentration | High |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

GPU Orchestration Market Analysis by Mordor Intelligence

The GPU orchestration market size is expected to increase from USD 1.78 billion in 2025 to USD 2.31 billion in 2026 and reach USD 8.16 billion by 2031, growing at a CAGR of 28.71% over 2026-2031. The GPU orchestration market is expanding because AI infrastructure spending has moved from one-time GPU procurement toward continuous workload management, where buyers now care as much about scheduling discipline, cluster visibility, and policy control as they do about raw compute access. The shift from static provisioning toward workload-aware orchestration is shaping vendor strategy across the GPU orchestration market, as cloud operators, platform software vendors, and chip ecosystem leaders all try to become the control layer that decides where AI workloads run and how shared capacity is used. Hybrid operating models are also widening demand in the GPU orchestration market, because enterprises now want one scheduling plane that can manage on-premises clusters, sovereign cloud environments, and burst capacity on public cloud without forcing teams to rebuild their operating model. Open-source scheduling primitives are lowering entry barriers, but they are also moving competition in the GPU orchestration market toward governance, cost attribution, observability, and energy-aware placement, where enterprise buyers still accept premium pricing for production-grade software. That combination, rising AI workload complexity, pressure to use costly GPU fleets better, and vendor moves toward integrated orchestration stacks, leaves the GPU orchestration market with room to grow across cloud platforms, enterprise software, and industrial AI deployments.

Key Report Takeaways

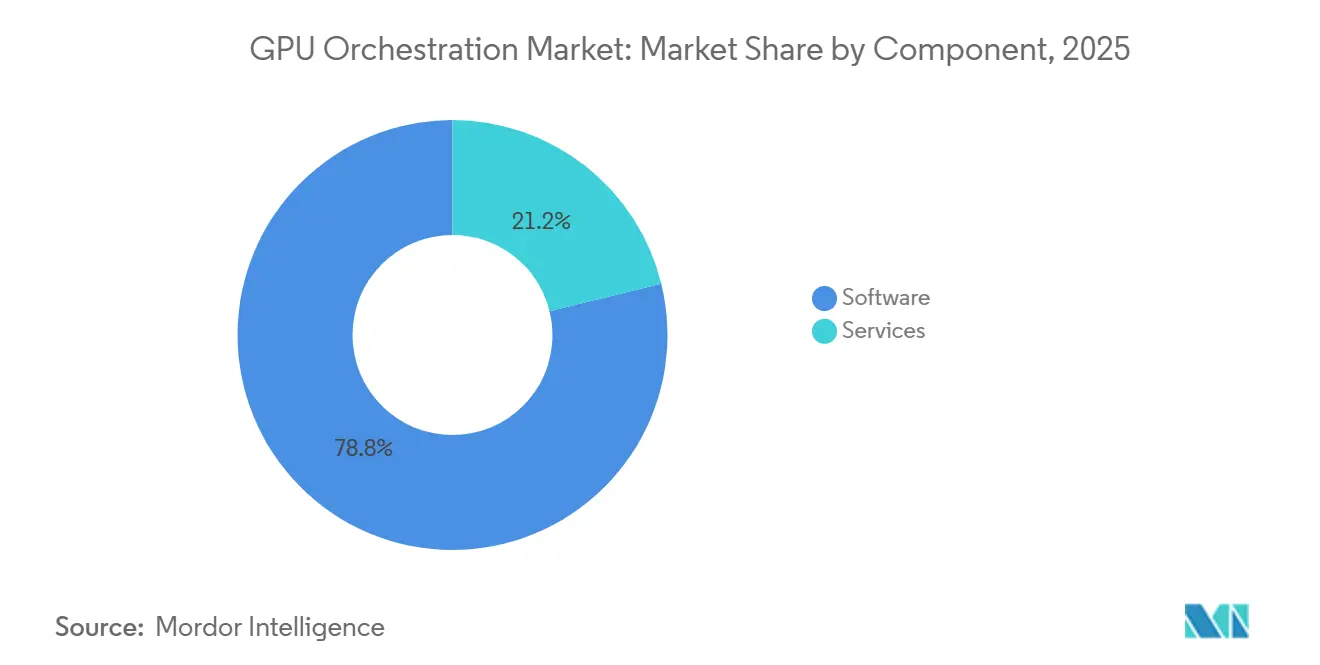

- By component, software held 78.83% of the GPU orchestration market share in 2025, while services are projected to expand at a 29.86% CAGR through 2031.

- By deployment model, cloud held 52.69% of the GPU orchestration market share in 2025, while hybrid is projected to expand at a 29.53% CAGR through 2031.

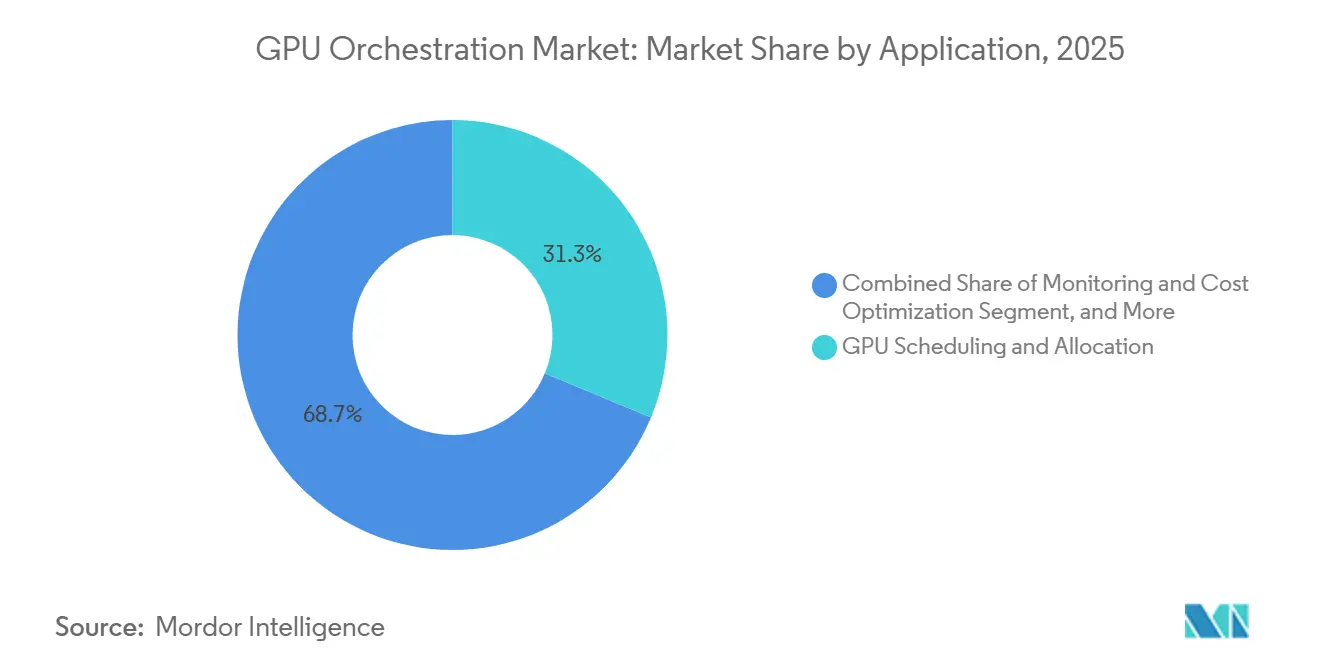

- By application, GPU scheduling and allocation accounted for 31.26% of the GPU orchestration market size in 2025, while monitoring and cost optimization are projected to expand at a 29.64% CAGR through 2031.

- By end user, cloud service providers and GPUaaS providers held 32.71% of revenue in 2025, while manufacturing and automotive are projected to grow at a 29.28% CAGR through 2031.

- By geography, North America held 47.52% of revenue in 2025, while Asia-Pacific is projected to expand at a 29.45% CAGR through 2031.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of January 2026.

Global GPU Orchestration Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Rising Demand for LLM Training and Inference Workloads | +8.5% | Global, early concentration in North America and the Asia-Pacific | Medium term (2-4 years) |

| Need To Maximize Expensive GPU Utilization | +7.0% | Global, North America, and Europe are the most cost-pressured | Short term (≤ 2 years) |

| Rapid Shift to Cloud-Native and Hybrid GPU Operations | +5.0% | North America and Europe leading, Asia-Pacific accelerating | Medium term (2-4 years) |

| Multi-Tenant GPU Sharing Across Enterprise AI Teams | +3.5% | Global, BFSI, and healthcare prioritizing tenant isolation | Short term (≤ 2 years) |

| Energy-Aware Scheduling to Reduce AI Compute Waste | +2.0% | Europe, North America data centers | Long term (≥ 4 years) |

| Edge-Integrated Real-Time AI Processing | +1.5% | Asia-Pacific, North America, and automotive corridors in Germany and Japan | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

Rising Demand for LLM Training and Inference Workloads

The GPU orchestration market is benefiting from the fact that large model training and production inference now place very different demands on the same pool of accelerators. Training jobs require long reservation windows, stable interconnect performance, and coordinated multi-node execution, while inference creates uneven demand that can rise or fall quickly over time and location. That mismatch makes static GPU allocation expensive and slow, which is why the GPU orchestration market is moving closer to the center of enterprise AI infrastructure design. NVIDIA described how its NeMo Framework uses adaptive resource orchestration to reduce long-haul bandwidth pressure during distributed training, demonstrating that orchestration is now tied directly to model performance rather than solely to cluster administration. As reasoning models, fine-tuning pipelines, and production inference all compete for the same infrastructure, the GPU orchestration market is gaining from software that can balance long-running jobs with burst workloads without locking capacity into rigid reservations. This is also pushing vendors in the GPU orchestration market to treat scheduling, queue policy, and cluster awareness as product differentiators rather than background infrastructure features that buyers can ignore.

Need To Maximize Expensive GPU Utilization

The GPU orchestration market is also being driven by the high cost of AI infrastructure and the growing pressure on operators to recover idle capacity within GPU clusters. Enterprises that bought or reserved large GPU fleets during the recent AI build cycle are now under pressure to demonstrate that these assets are being used in a disciplined, measurable way. That pressure is turning the GPU orchestration market into a practical cost-control category, because utilization improvements can change the effective cost of training, fine-tuning, and inference even when the hardware footprint stays the same. Anyscale stated in March 2026 that production deployments using NVIDIA H100 and H200 fleets were sustaining more than 80% GPU utilization through rack-aware scheduling and fractional allocation, providing the GPU orchestration market with a clear operational benchmark for what mature implementations can achieve. NVIDIA also moved core-scheduling software into the open with the KAI Scheduler and later placed a Dynamic Resource Allocation driver under community governance, which supports a broader ecosystem for higher-efficiency GPU use. As a result, the GPU orchestration market is no longer selling only operational convenience; it is selling measurable improvement in how costly GPU fleets are consumed and governed.

Rapid Shift to Cloud-Native and Hybrid GPU Operations

The GPU orchestration market is being shaped by a clear move toward cloud-native control planes that can also reach into on-premises GPU infrastructure. Many enterprises no longer want separate operating models for internal clusters and public cloud capacity, because this creates duplicate policies, fragmented observability, and inconsistent workload behavior. This is why the GPU orchestration market is seeing stronger demand for unified schedulers that can place jobs across environments based on cost, latency, data location, and service-level requirements. SoftBank introduced Infrinia AI Cloud OS in January 2026 as a software stack for multi-tenant GPU AI data centers, with Kubernetes-as-a-Service and Inference-as-a-Service, underscoring the growing value of orchestration software as the operating layer of AI cloud infrastructure. KDDI also launched a GPU cloud service in April 2026 around NVIDIA GB200 NVL72 infrastructure for use cases such as automotive AI model training, genomic research, and financial market modeling, which reinforces the role of orchestrated hybrid and sovereign deployments in the GPU orchestration market.[1]KDDI Corporation, “KDDI GPU Cloud Service Launch,” KDDI Newsroom, newsroom.kddi.com As this architecture becomes more common, the GPU orchestration market is likely to reward vendors that can present cloud and on-premises resources as one governed, policy-driven environment.

Multi-Tenant GPU Sharing Across Enterprise AI Teams

The GPU orchestration market is also growing because GPU fleets now need to be shared across business units, product teams, and user groups rather than assigned to a single project. That shift matters because internal contention over scarce accelerator capacity can delay production timelines even when total installed hardware is adequate. Buyers in the GPU orchestration market increasingly want fair-share policies, quota controls, preemption rules, and isolation options that let one team run high-priority work without blocking all other workloads. NVIDIA open-sourced the KAI Scheduler in November 2024, with support for capabilities such as fractional allocation and policy-based scheduling, underscoring how multi-tenant cluster control has become central to the software layer for GPU operations. SoftBank positioned Infrinia AI Cloud OS as a multi-tenant software stack for GPU AI data centers, reflecting how service providers now see tenant separation and operational automation as commercial requirements, not optional features. In practice, this keeps the GPU orchestration market tied closely to enterprise governance needs, especially in sectors where auditability, internal chargeback, and workload prioritization matter as much as compute throughput.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Interoperability Gaps Across Heterogeneous GPU Stacks | -2.5% | Global, Asia-Pacific most affected with mixed NVIDIA, AMD, and Huawei Ascend deployments | Medium term (2-4 years) |

| Limited Availability of GPU-Cluster Orchestration Talent | -2.0% | Global, most acute in Europe and South America | Medium term (2-4 years) |

| Security and Privacy Risks in Multi-Tenant Environments | -1.5% | Global, BFSI, and healthcare verticals are most affected | Short term (≤ 2 years) |

| High Integration Complexity with Legacy Data Center Tooling | -1.0% | North America and Europe, on-premises-heavy enterprises | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

Interoperability Gaps Across Heterogeneous GPU Stacks

The GPU orchestration market still faces a real adoption barrier when enterprises need a single software layer to manage hardware, drivers, and scheduling logic across mixed-accelerator environments. Many orchestration stacks were initially built around NVIDIA-heavy environments, so support for other hardware ecosystems remains uneven across plugins, observability tools, topology handling, and policy frameworks. That creates longer integration cycles and higher maintenance overhead for buyers who do not want to standardize their entire AI stack on one vendor. NVIDIA’s decision to donate its GPU Dynamic Resource Allocation driver to the CNCF in March 2026 points to an effort to widen interoperability through community-led scheduling standards, but it also highlights that cross-vendor consistency is still a work in progress. The GPU orchestration market is therefore advancing in an environment where multi-vendor support is becoming increasingly important, even as the tooling landscape remains fragmented. Until interoperability improves further, some buyers will keep deployments smaller, rely more heavily on managed service partners, or choose vendor-specific stacks instead of broader orchestration layers.

Limited Availability of GPU-Cluster Orchestration Talent

The GPU orchestration market is also constrained by the shortage of engineers who can work across Kubernetes internals, distributed systems behavior, AI workload characteristics, and hardware-aware cluster design. This is not a routine infrastructure skill set, and it is especially hard to build inside enterprises where GPU operations are still a new function rather than a long-standing platform team responsibility. Organizations often understand why orchestration matters, but they do not always have the staff needed to tune policies, align queue rules with business priority, or manage production-grade hybrid clusters. The need to combine scheduler policy, workload isolation, topology awareness, and cost attribution raises the implementation burden across the GPU orchestration market, especially outside core technology sectors. That gap favors vendors that package orchestration with managed services, implementation support, and repeatable deployment frameworks. It also means the GPU orchestration market may grow fastest where buyers can access experienced platform partners or where cloud providers reduce the amount of custom operational work needed for production use.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Component: Software-Led Spending Shapes Value Capture

Software accounted for 78.83% of revenue in 2025, indicating that buyers in the GPU orchestration market have placed the highest value on the control layer rather than attached services. The software-heavy mix reflects the fact that enterprises want direct command over scheduling policy, observability, governance, multi-tenant access, and utilization management as they move AI workloads into production. In the GPU orchestration market, software is often the part that determines how efficiently the same hardware base can be shared across teams, priorities, and environments. That is why software captured the largest share even as the broader infrastructure stack continued to expand around managed cloud and integration services. Buyers also tend to prefer software platforms that shorten deployment time and provide a single administrative plane for resource allocation, queue policy, and performance monitoring.

Services are projected to grow at a 29.86% CAGR through 2031, making it the fastest-growing component of the GPU orchestration market, even though it started from a smaller base. That growth signals that enterprise adoption still involves heavy design and operational work, especially when buyers need to connect schedulers with storage, observability, compliance, and legacy internal tooling. Anyscale’s March 2026 release pointed to production deployments that used rack-aware scheduling and fractional allocation to sustain high utilization on NVIDIA H100 and H200 fleets, which supports the view that well-implemented orchestration depends on deep operational tuning and not only software purchase.[2]Anyscale, “Anyscale Cuts Multimodal AI Data Processing Costs With NVIDIA RTX PRO 4500 Blackwell Server Edition,” Anyscale Press Release, anyscale.com NVIDIA’s open-source moves around KAI Scheduler and the DRA driver may lower barriers at the basic scheduling layer, but they also push value in the GPU orchestration market toward integration, governance, and optimization services that help enterprises move from pilots to scaled operations. Over time, the component mix suggests that the GPU orchestration market will keep monetizing both platform control software and the services required to make that software work reliably inside complex enterprise environments.

By Deployment Model: Hybrid Architecture Gains Ground

Cloud accounted for 52.69% of the GPU orchestration market size in 2025, which confirms that managed cloud environments remained the easiest starting point for AI teams that wanted fast access to shared GPU capacity. The cloud lead came from the operational simplicity of managed Kubernetes environments, faster provisioning, and the ability to begin orchestration without first building large internal platform teams. For many buyers in the GPU orchestration market, cloud deployment also reduced the time needed to test queue policies, monitoring models, and team-level access controls under real production workloads. That made cloud the largest deployment model at a time when many organizations were still establishing their first production AI operations pattern. It also helped hyperscalers keep orchestration closer to their own ecosystems, strengthening the link between managed compute consumption and embedded scheduling software.

Hybrid is projected to expand at a 29.53% CAGR through 2031, indicating that the GPU orchestration market is moving toward a more distributed operating model across both owned and rented infrastructure. Enterprises that invested in on-premises GPU hardware now want the flexibility to burst into cloud when demand spikes, while still keeping sensitive workloads or regulated data in controlled environments. SoftBank’s Infrinia AI Cloud OS was introduced as a software stack for GPU AI data centers that automates Kubernetes-as-a-Service and Inference-as-a-Service, which reflects the increasing importance of orchestration software in managing multi-environment operations. KDDI’s GPU Cloud service launch in April 2026 also supports this direction, because it was positioned for secure and data-sovereign use cases such as automotive AI training, genomics, and financial modeling. The deployment mix therefore suggests that the GPU orchestration market is shifting from simple cloud scheduling toward broader control planes that can manage cost, compliance, and workload placement across several infrastructure boundaries.

By Application: Core Scheduling Leads While Cost Control Accelerates

GPU scheduling and allocation accounted for 31.26% of the GPU orchestration market in 2025, confirming that basic resource placement remained the central value proposition in this category. The largest share at this layer is logical, because the first problem most buyers try to solve is how to decide which workload gets which accelerator, when, and under which queue policy. In the GPU orchestration market, scheduling and allocation also determine whether capacity can be shared effectively across clusters, teams, and job types without forcing manual intervention. That foundational role keeps the segment large even as adjacent applications, such as cost control and governance, become more important in enterprise buying decisions. It also means vendors that perform well on core scheduling usually gain the first opportunity to cross-sell broader orchestration functions.

Monitoring and cost optimization are projected to grow at a 29.64% CAGR through 2031, indicating that the GPU orchestration market is increasingly judged by financial control and visibility, not just by cluster uptime. Buyers now want to know which team used capacity, whether allocation matched priority, and how infrastructure efficiency changed over time under production traffic. NVIDIA’s 2026 discussion of token production per GPU, per rack, and per watt reflects a wider move toward operational metrics that connect infrastructure use with output and efficiency, which supports the growing role of monitoring and optimization inside the GPU orchestration market. NVIDIA’s March 2026 Grove release for disaggregated inference management also points to how orchestration is expanding beyond static scheduling into more dynamic control of production AI serving. This application pattern shows that the GPU orchestration market is moving from pure allocation software toward broader systems that connect scheduling, cost observability, and workload performance in one platform.

By End User: Providers Lead While Industrial Buyers Scale Faster

Cloud service providers and GPUaaS providers accounted for 32.71% of revenue in 2025, making them the largest end-user group in the GPU orchestration market. Their lead reflects the simple fact that these operators manage large, shared fleets and must match diverse workloads to finite accelerator pools while preserving service quality for many customers simultaneously. In the GPU orchestration market, this makes them early adopters of advanced queue policy, capacity partitioning, tenant controls, and cluster-level observability. They also have a direct commercial reason to improve scheduling efficiency, because even small gains in usable capacity can affect margin, service availability, and expansion planning. The provider segment, therefore, remains central to how the GPU orchestration market develops, tests, and commercializes new scheduling and governance features.

Manufacturing and automotive are projected to expand at a 29.28% CAGR through 2031, making them the fastest-growing end-user segments in the GPU orchestration market. Growth here reflects the need to coordinate cloud training with inference and decision workloads closer to factories, vehicles, and industrial systems. Visteon’s March 2026 launch of an edge-to-cloud AI arbitration architecture for software-defined vehicles demonstrated how automotive-oriented deployments are beginning to dynamically distribute AI workloads between vehicle hardware and cloud infrastructure. Visteon reinforced that direction in June 2026 with D6Sigma for industrial automation, extending GPU-accelerated AI use into production lines and strengthening the case for orchestrated edge-to-cloud architectures across the GPU orchestration market. As industrial AI programs mature, the GPU orchestration market is likely to benefit from buyers that need one control layer for factory analytics, automotive development, robotics, and production inference.

Geography Analysis

North America held 47.52% of the GPU orchestration market share in 2025, keeping the region in the lead, as it combines hyperscaler presence, enterprise AI demand, and a dense ecosystem of cloud-native software teams. The United States remains the core growth engine in the GPU orchestration market because many managed GPU services, orchestration software vendors, and AI platform specialists are either headquartered there or closely tied to its cloud ecosystem. That concentration has made North America the region where orchestration features move fastest from engineering problem to commercial product. It has also kept the GPU orchestration market closely linked to managed Kubernetes adoption, enterprise inference rollout, and the push to treat GPU governance as a board-level infrastructure issue. Anyscale’s June 2026 launch of a native Azure integration built on Azure Kubernetes Service and Azure Resource Manager highlights how the North American ecosystem continues to turn orchestration into a directly consumable enterprise software layer.

Europe remained the second-largest regional market for GPU orchestration, with demand driven by regulated enterprise workloads, sovereign compute priorities, and the need for auditable infrastructure control. Germany and the United Kingdom stand out because automotive AI, financial services, and life sciences all depend on production environments where scheduling policy and workload traceability matter. The region also gives the GPU orchestration market a governance-heavy demand profile, because buyers often need software that can document resource access, workload placement, and operational consistency. NVIDIA’s March 2026 move to place its GPU DRA driver under CNCF governance at KubeCon Europe in Amsterdam supports a broader European preference for open standards and community-led infrastructure components. Europe therefore remains an important region for enterprise-grade orchestration, even when it is not the fastest-growing part of the GPU orchestration market.

Asia-Pacific is projected to expand at a 29.45% CAGR through 2031, which makes it the fastest-growing region in the GPU orchestration market. Japan is a major source of that momentum, with KDDI launching GPU Cloud in April 2026 and SoftBank introducing Infrinia AI Cloud OS as a domestically developed software stack for multi-tenant GPU AI data centers.[3]SoftBank Corp., “AI Data Center Software Stack ‘Infrinia AI Cloud OS’ Announced,” SoftBank Corporate News, softbank.jp GMO Internet also introduced NVIDIA HGX B300 on its managed Slurm GPU cloud service in March 2026, which strengthens the region’s access to advanced managed compute infrastructure. South America and the Middle East and Africa remain smaller in the GPU orchestration market, but both regions are becoming more relevant where sovereign AI capacity, domestic data handling, and industry-specific cloud demand are beginning to support early deployments.

Competitive Landscape

The GPU orchestration market is highly consolidated, with NVIDIA occupying a structurally strong position because its software footprint now extends from hardware management to scheduling, workload governance, and influence in the open-source ecosystem. The company’s control of foundational GPU technologies gives it an advantage in shaping how orchestration features are exposed, standardized, and integrated into production AI environments. NVIDIA strengthened that position by open-sourcing the KAI Scheduler in November 2024 and by donating its GPU DRA driver to the CNCF in March 2026, moves that help its preferred scheduling model spread through the broader infrastructure ecosystem. At the same time, hyperscalers remain powerful participants in the GPU orchestration market because they can embed resource management directly into managed Kubernetes and GPU cloud services. That dynamic keeps the top of the GPU orchestration market competitive, but it does not fully close the field, because large buyers still need neutral orchestration across several clouds and on-premises estates.

Specialist vendors are competing by offering deeper workload logic, stronger cost visibility, and better support for cross-cloud operations than hyperscaler-native tools usually provide. Anyscale’s June 2026 Azure integration is a good example, because it brought its orchestration model into a native Azure operating pattern while preserving customer tenancy, security, and billing structure. Databricks also introduced AI Runtime in 2026 to provide scalable serverless NVIDIA GPU access for training and fine-tuning inside its own software environment, which shows how orchestration is being absorbed into wider data and AI platforms.[4]Databricks, “Introducing AI Runtime, Scalable, Serverless NVIDIA GPUs On Databricks For Training And Finetuning,” Databricks Blog, databricks.com These moves matter because they shift the GPU orchestration market away from being a narrow scheduling niche and toward becoming a broader platform capability that shapes developer workflow, infrastructure policy, and operational cost control. Vendors that can connect orchestration with ML workflow, enterprise governance, and managed cloud consumption are likely to hold stronger positions as the category matures.

The GPU orchestration market also has open space for newer entrants, especially in multi-cloud brokerage, verticalized orchestration, and energy-aware cluster management. Research published in MRS Energy and Sustainability in 2025 showed that federated carbon intelligence frameworks can combine hardware telemetry with grid data for real-time optimization across heterogeneous fleets, which suggests a longer-term path for scheduling software beyond pure utilization improvement. This matters because future competition in the GPU orchestration market may depend less on basic queueing logic and more on whether a platform can optimize for governance, operating cost, and sustainability at the same time. The field therefore remains active, with leadership visible at the top but meaningful room still open for specialists that solve complex multi-environment or high-compliance workload problems.

GPU Orchestration Industry Leaders

NVIDIA Corporation

Amazon.com, Inc.

Microsoft Corporation

Google LLC

IBM Corporation

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- June 2026: Anyscale launched the public preview of Anyscale on Azure, a native integration built on Azure Kubernetes Service and Azure Resource Manager, enabling enterprises to build and operate production-scale AI workloads entirely within their own Azure tenancy. The offering draws down from existing Microsoft Azure Consumption Commitments and positions compute-governed sovereign AI as an alternative to external model API cost structures.

- June 2026: Visteon Corporation introduced D6Sigma, a new edge AI product line for industrial automation developed in collaboration with Qualcomm Technologies. Built on the CognitoAI-IoT platform and Qualcomm Dragonwing IQ9 Series processors, D6Sigma brings GPU-accelerated real-time computer vision and AI inference to automotive and electronics manufacturing production lines, extending the automotive GPU orchestration use case from training clusters to factory floor edge AI.

- April 2026: KDDI Corporation began accepting service applications for KDDI GPU Cloud, a commercial GPU compute service built on NVIDIA GB200 NVL72 at the Osaka Sakai Data Center, Japan. The service specifically targets automotive AI model training, genomic research, and financial market modeling in a secure, carrier-grade network environment addressing Japan's data sovereignty priorities.

- March 2026: NVIDIA donated its Dynamic Resource Allocation (DRA) driver for GPUs to the CNCF at KubeCon Europe in Amsterdam, transitioning a key GPU scheduling primitive to community governance. At the same event, NVIDIA released Grove, an open-source Kubernetes API for managing disaggregated LLM inference workloads across GPU clusters, and announced integration with the llm-d inference stack.

Global GPU Orchestration Market Report Scope

The GPU orchestration market covers solutions and services that automate, manage, and optimize the allocation, scheduling, scaling, and monitoring of GPU resources across on-premises, cloud, and hybrid environments. The scope of the report includes the analysis of GPU orchestration platforms used to support workloads such as artificial intelligence, machine learning, high-performance computing, data analytics, and graphics-intensive applications across end-user industries.

The GPU Orchestration Market Report is Segmented by Component (Software, and Services), Deployment Model (Cloud, On-Premises, and Hybrid), Application (GPU Scheduling and Allocation, Workload Orchestration, Cluster Management, Governance and Multi-Tenancy, and Monitoring and Cost Optimization), End User (Cloud Service Providers and GPU-as-a-Service Providers, IT and Technology Companies, BFSI, Healthcare and Life Sciences, Manufacturing and Automotive, and Other End Users), and Geography (North America, Europe, Asia-Pacific, South America, and Middle East and Africa). The Market Forecasts are Provided in Terms of Value (USD).

| Software |

| Services |

| Cloud |

| On-Premises |

| Hybrid |

| GPU Scheduling and Allocation |

| Workload Orchestration |

| Cluster Management |

| Governance and Multi-Tenancy |

| Monitoring and Cost Optimization |

| Cloud Service Providers and GPU-as-a-Service Providers |

| IT and Technology Companies |

| BFSI |

| Healthcare and Life Sciences |

| Manufacturing and Automotive |

| Other End Users |

| North America | United States |

| Canada | |

| Mexico | |

| Europe | Germany |

| United Kingdom | |

| France | |

| Italy | |

| Rest of Europe | |

| Asia-Pacific | China |

| Japan | |

| South Korea | |

| India | |

| Southeast Asia | |

| Rest of Asia-Pacific | |

| South America | |

| Middle East and Africa |

| By Component | Software | |

| Services | ||

| By Deployment Model | Cloud | |

| On-Premises | ||

| Hybrid | ||

| By Application | GPU Scheduling and Allocation | |

| Workload Orchestration | ||

| Cluster Management | ||

| Governance and Multi-Tenancy | ||

| Monitoring and Cost Optimization | ||

| By End User | Cloud Service Providers and GPU-as-a-Service Providers | |

| IT and Technology Companies | ||

| BFSI | ||

| Healthcare and Life Sciences | ||

| Manufacturing and Automotive | ||

| Other End Users | ||

| By Geography | North America | United States |

| Canada | ||

| Mexico | ||

| Europe | Germany | |

| United Kingdom | ||

| France | ||

| Italy | ||

| Rest of Europe | ||

| Asia-Pacific | China | |

| Japan | ||

| South Korea | ||

| India | ||

| Southeast Asia | ||

| Rest of Asia-Pacific | ||

| South America | ||

| Middle East and Africa | ||

Key Questions Answered in the Report

What is the 2026 size of GPU orchestration?

The GPU orchestration market stands at USD 2.31 billion in 2026 and is projected to reach USD 8.16 billion by 2031 at a CAGR of 28.71% over 2026-2031.

What is driving adoption of GPU orchestration platforms?

Demand is being driven by large model training, rising inference complexity, pressure to improve GPU utilization, and the shift toward hybrid GPU operations across cloud and on-premises environments.

Which deployment model is expanding the fastest?

Hybrid is the fastest-growing deployment model, with a projected CAGR of 29.53% through 2031, as enterprises combine owned GPU clusters with cloud burst capacity.

Which application area leads revenue today?

GPU scheduling and allocation leads with 31.26% of revenue in 2025, showing that core resource placement remains the main use case for orchestration software.

Which end-user group is growing the quickest?

Manufacturing and automotive is the fastest-growing end-user segment, with a projected CAGR of 29.28% through 2031, supported by edge-to-cloud AI and software-defined vehicle programs.

Which region offers the strongest growth outlook?

Asia-Pacific has the strongest growth outlook at 29.45% CAGR through 2031, supported by new GPU cloud launches and domestic orchestration initiatives in markets such as Japan.

Page last updated on: