North America Data Center GPU Market Size and Share

Market Overview

| Study Period | 2020 - 2031 |

|---|---|

| Forecast Data Period | 2026 - 2031 |

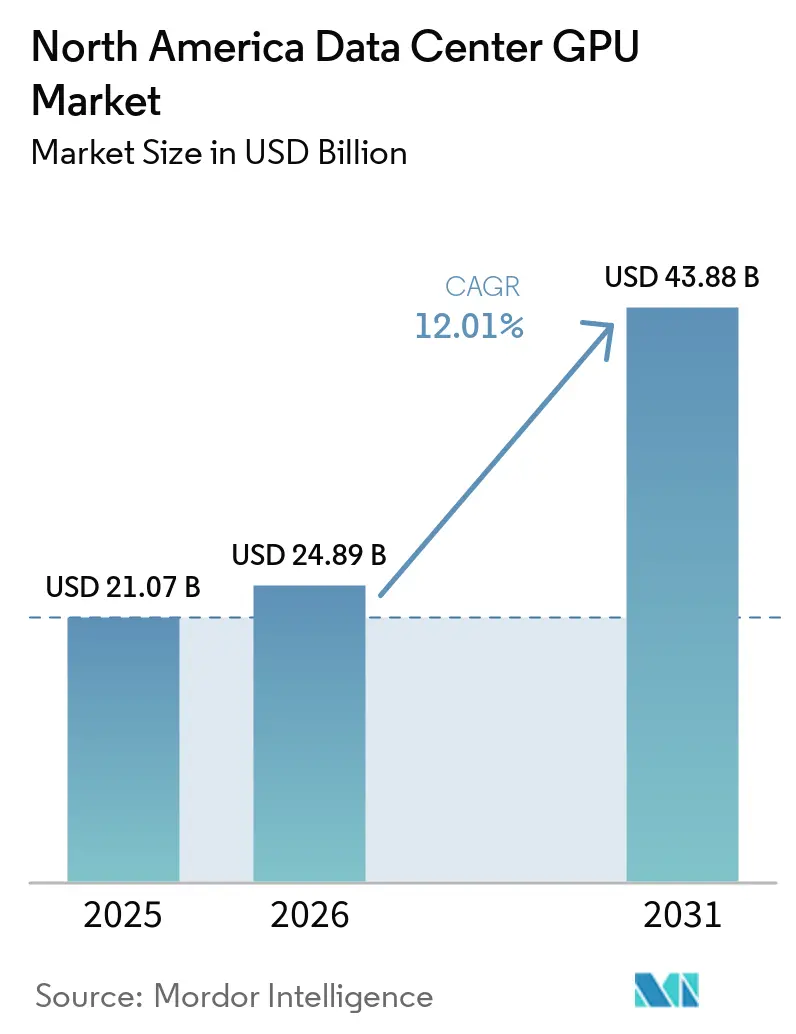

| Base Year Market Size (2025) | USD 21.07 Billion |

| Market Size (2026) | USD 24.89 Billion |

| Market Size (2031) | USD 43.88 Billion |

| Growth Rate (2026 - 2031) | 12.01% CAGR |

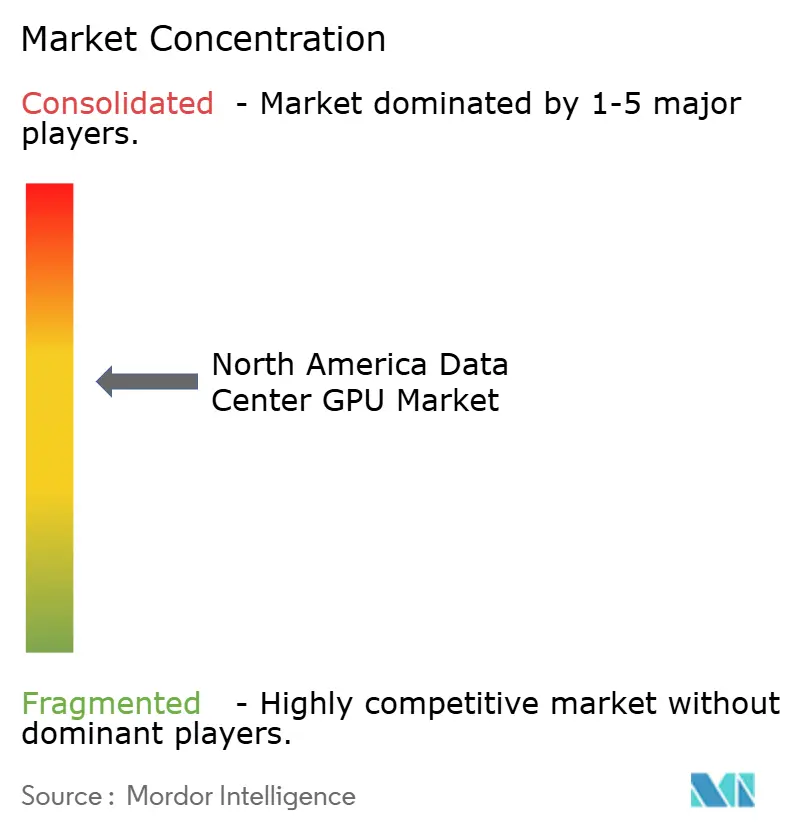

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

North America Data Center GPU Market Analysis by Mordor Intelligence

The North America data center GPU market size is expected to increase from USD 24.89 billion in 2026 to USD 43.88 billion by 2031, growing at a CAGR of 12.01% over 2026-2031. Generative AI deployments, sovereign-cloud mandates, and liquid-cooled rack architectures are reshaping compute strategies as hyperscalers and enterprises migrate from CPU-centric to GPU-accelerated workloads. Rapid adoption of rack-scale NVLink fabrics is lowering inter-GPU latency, while rising electricity tariffs are pushing operators toward energy-efficient, immersion- and cold-plate-cooled GPU servers. The North America data center GPU market is also benefiting from provincial incentives in Canada that favor on-premises AI infrastructure and from U.S. federal spending on exascale research clusters. Finally, a robust venture pipeline of composable infrastructure start-ups offers new procurement options for enterprises seeking to avoid vendor lock-in.

Key Report Takeaways

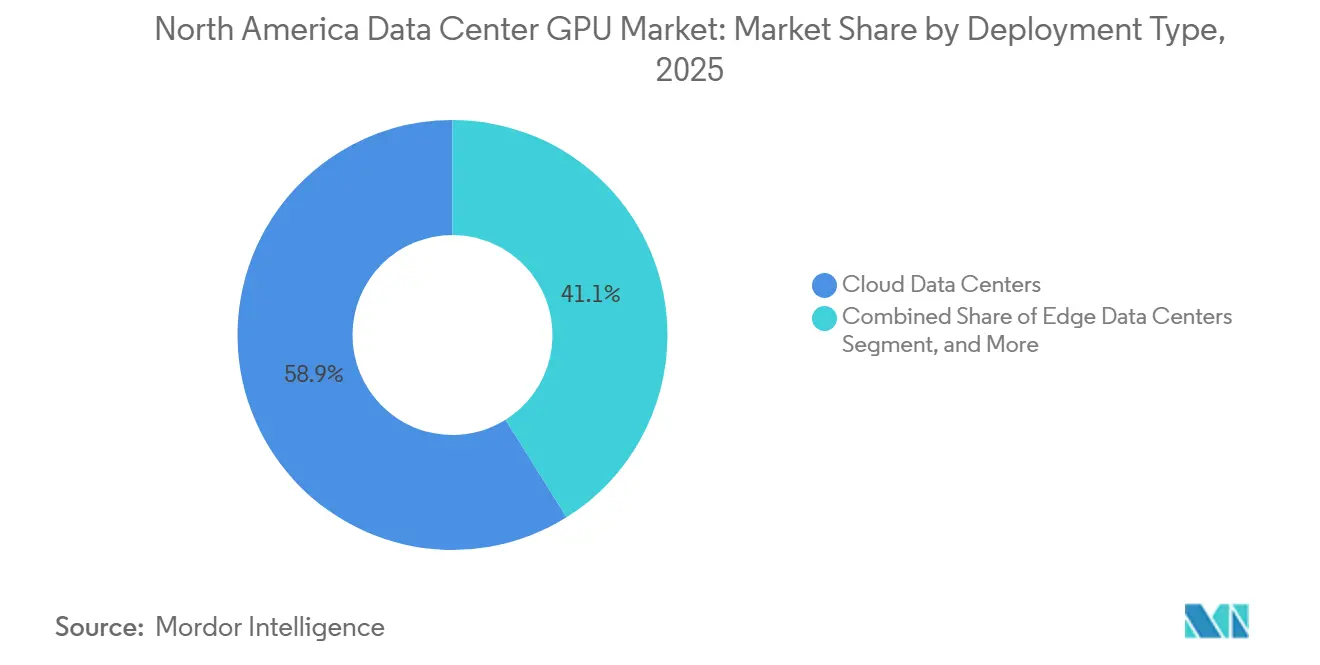

- By deployment type, cloud data centers led with 58.90% of the North America data center GPU market share in 2025, while edge data centers are projected to expand at a 13.89% CAGR through 2031.

- By GPU type, training GPUs captured 57.82% share of the North America data center GPU market size in 2025; inference GPUs are forecast to grow at a 13.45% CAGR.

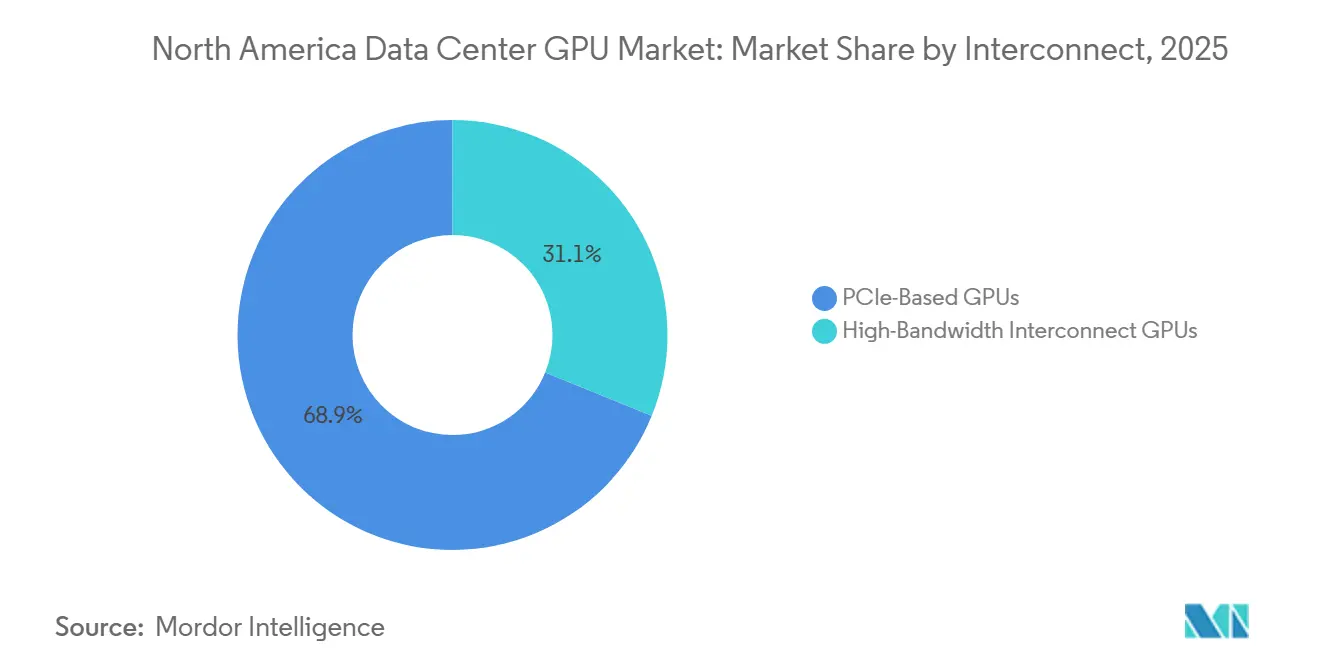

- By interconnect, PCIe-based GPUs accounted for 68.87% of the market share in 2025, whereas high-bandwidth interconnect GPUs is expected to grow at a 14.21% CAGR.

- By workload, AI and ML accounted for 67.99% of revenue share in 2025, and GPU-accelerated analytics is poised for a 14.66% CAGR.

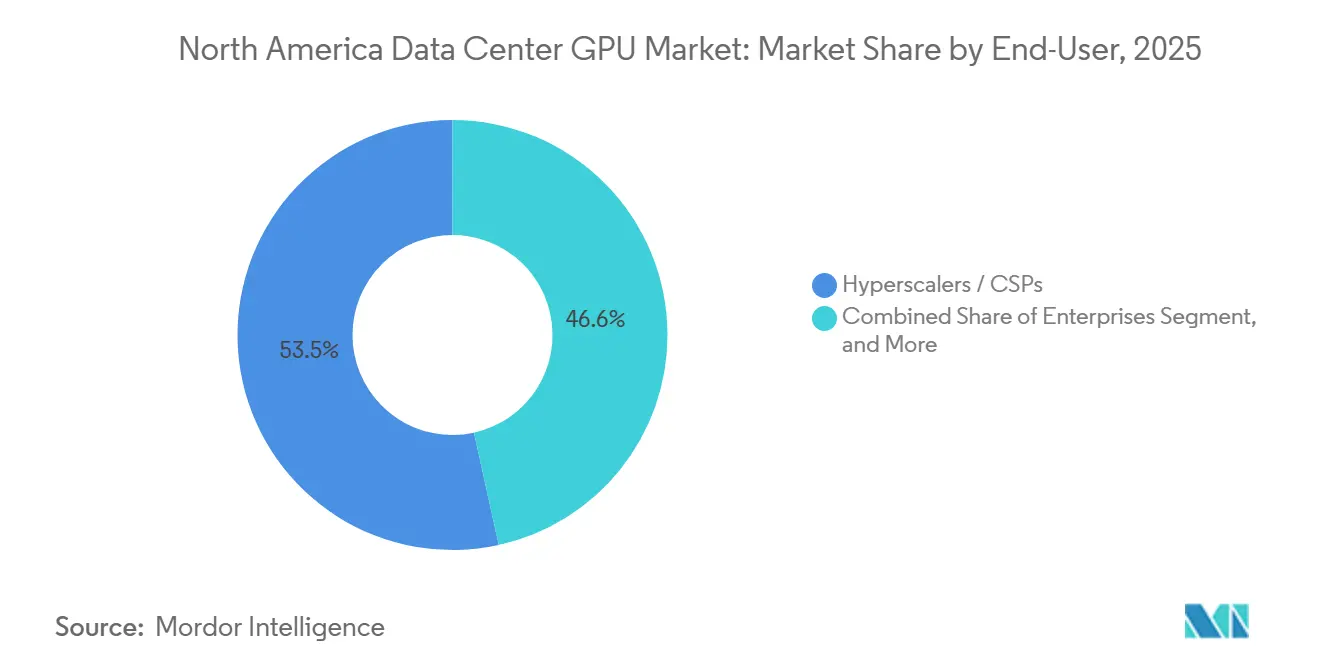

- By end user, hyperscalers held 53.45% share in 2025, and the government and research institutions segment is expected to register the fastest 14.84% CAGR.

- By geography, the United States commanded 83.45% share in 2025, while Canada is set to register a 13.77% CAGR.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of January 2026.

North America Data Center GPU Market Trends and Insights

Drivers Impact Analysis*

| DRIVER | (~) % IMPACT ON CAGR FORECAST | GEOGRAPHIC RELEVANCE | IMPACT TIMELINE |

|---|---|---|---|

| Surging AI and ML training workloads in hyperscale data centers | +3.2% | United States (Oregon, Virginia, Texas); Canada (Quebec) | Medium term (2–4 years) |

| Growing adoption of hybrid cloud strategies among Fortune 500 enterprises | +2.8% | United States (nationwide); Canada (Ontario, British Columbia) | Medium term (2–4 years) |

| Accelerated deployment of generative-AI-optimized GPU instances by CSPs | +2.5% | United States (AWS, Azure, Google Cloud regions); Canada (emerging) | Short term (≤ 2 years) |

| Expansion of sovereign cloud regions demanding on-prem GPU capacity | +1.9% | Canada (Quebec, Saskatchewan); United States (federal agencies) | Long term (≥ 4 years) |

| Rapid emergence of GPU disaggregation and composable infrastructure | +1.1% | United States (hyperscaler R&D hubs); early pilots in Canada | Long term (≥ 4 years) |

| Availability of energy-efficient liquid-cooled GPU servers lowering TCO | +0.9% | United States (Texas, Arizona); Canada (British Columbia hydro corridors) | Medium term (2–4 years) |

| Source: Mordor Intelligence | |||

Surging AI and ML Training Workloads in Hyperscale Data Centers

Hyperscalers are now training trillion-parameter frontier models on clusters with more than 100,000 GPUs, a scale unlocked by NVLink fabrics that reduce all-reduce latency from minutes to seconds.[1]NVIDIA Corporation, “Form 10-K Annual Report,” U.S. Securities and Exchange Commission, sec.govRecord revenue at a leading GPU vendor in 2025 underscored a demand cycle fueled by model budgets surpassing USD 100 million per run. Public-sector projects such as Solstice and Equinox are adopting 10,000-plus GPU clusters for climate models, reinforcing long-term visibility for suppliers. Operators increasingly factor test-time compute into capacity planning, effectively doubling life-cycle GPU requirements as inference budgets grow to parity with training allocations. The resulting pull-through effect keeps advanced-node fabs fully allocated and intensifies competition for HBM capacity.

Growing Adoption of Hybrid Cloud Strategies Among Fortune 500 Enterprises

Enterprises are repatriating AI workloads to on-premises GPU stacks to control proprietary data and avoid cloud egress fees that can top 30% of total spend. Turnkey private-cloud-AI appliances with 4-64 GPUs and SaaS-like management are enabling firms in pharmaceuticals, automotive, and media to fine-tune LLMs behind their firewalls.[2]Hewlett Packard Enterprise, “HPE Private Cloud AI QuickSpecs,” hpe.com The hybrid model is underpinned by mature virtualization, with vGPU 19.0 supporting 48 virtual machines per Blackwell GPU and slicing accelerators for multiple business units. During seasonal peaks, overflow jobs burst into CSP capacity, preserving agility without long-term public-cloud lock-in. This fluidity in workload is expanding the addressable market for mid-sized data centers and fueling demand for GPU leasing.

Accelerated Deployment of Generative-AI-Optimized GPU Instances by CSPs

Cloud providers released Blackwell-based instances in 2025 and are scaling capacity through 2026. AWS P6-B200 and P6-B300 deliver 1.8 TB-per-second-per-GPU NVLink bandwidth, while Google’s Flex-start VM queuing offers discounted idle GPUs to lower inference costs.[3]Amazon Web Services, “Amazon EC2 P6 Instances,” aws.amazon.com Microsoft is building Rubin-ready campuses in Wisconsin and Georgia, aiming for hundreds of thousands of GPUs by late 2026. Competing architectures, such as Gaudi 3 on IBM Cloud, offer cost-optimized alternatives, promising 50% better inference performance per dollar. These offerings reflect a pivot to inference-centric economics as model deployment costs now eclipse training outlays for high-traffic AI services.

Expansion of Sovereign Cloud Regions Demanding On-Prem GPU Capacity

Canada committed CAD 250 million (USD 178 million) to the LaSalle sovereign AI hub, while Saskatchewan’s Prairie2Cloud is seeding provincial GPU clusters. IREN ordered more than 50,000 NVIDIA B300 GPUs for second-half 2026 deployment, projecting USD 3.7 billion-plus annualized revenue. The 5C Group announced a 2 GW road map with 100,000-GPU deployment capability across North America.[4]5C Group, “5C Group Corporate Website,” 5cgroup.comThese initiatives create a procurement channel outside traditional hyperscalers, diversifying regional demand for accelerators.

Restraints Impact Analysis*

| RESTRAINT | (~) % IMPACT ON CAGR FORECAST | GEOGRAPHIC RELEVANCE | IMPACT TIMELINE |

|---|---|---|---|

| Persistent semiconductor supply-chain constraints for advanced nodes | -2.1% | United States (TSMC Arizona delays); Canada (HBM import dependencies) | Short term (≤ 2 years) |

| Rising data center electricity tariffs and carbon-emission regulations | -1.6% | United States (California, New York); Canada (carbon pricing CAD 65–170/tonne) | Medium term (2–4 years) |

| Capital-expenditure freeze among SMBs owing to macro uncertainty | -0.8% | United States (regional SMBs); Canada (mid-market enterprises) | Short term (≤ 2 years) |

| Vendor lock-in risks tied to proprietary GPU software ecosystems | -0.5% | United States (enterprise IT); Canada (public-sector procurement) | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

Persistent Semiconductor Supply-Chain Constraints for Advanced Nodes

Lead times for Blackwell and Rubin GPUs now exceed 50 weeks as advanced packaging remains supply-constrained. CoWoS capacity is short of demand, and HBM3E supply is trailing orders through 2026. Vendors are responding with United States fab expansions, but ramp timelines limit near-term relief, forcing hyperscalers into multi-billion-dollar pre-purchase agreements and equity-linked deals. Meta’s 6 GW Instinct commitment secured warrants for AMD shares, illustrating how customers leverage balance-sheet capacity to lock in allocation. Start-ups without similar negotiating leverage face prolonged qualification cycles and postponed revenue.

Rising Data Center Electricity Tariffs and Carbon-Emission Regulations

The Environmental Protection Agency’s Clean Air Act guidance and Department of Energy interconnection rules require operators to demonstrate that new loads will not inflate residential bills, thereby delaying permits in congested grids.[5]U.S. Department of Energy, “Department of Energy,” energy.govCanada’s carbon price will reach CAD 170 per tonne (USD 121 per tonne) by 2030, directly increasing OPEX for air-cooled GPU halls. Liquid-cooled HGX racks cut power per teraFLOP by 30-40%, but the USD 0.5-1 million-per-rack capital hit slows payback for smaller operators. Consequently, adoption is fastest in hydropower-rich British Columbia and low-cost-electricity Texas, widening the regional cost gap for hosting AI workloads.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Deployment Type: Edge Gains as Latency Trumps Scale

Cloud facilities dominated the North America data center GPU market in 2025, accounting for 58.90% share, yet edge nodes will compound at a 13.89% CAGR to 2031 as conversational AI, AR, and autonomous-vehicle inference shift closer to users. The North America data center GPU market size for edge deployments is climbing as telecom carriers deploy 10-50 GPU pods in central offices, shaving latency by double-digit milliseconds. Liquid-cooled micro-modules help meet noise and heat limits in retail and campus environments, while improved orchestration lets operators partition GPUs for bursty multi-tenant traffic.

Edge expansion reflects both economics and physics. Backhauling terabytes of sensor and video data to centralized clusters costs more than placing GPU capacity on-site, especially in Canada, where long-haul bandwidth pricing remains high. Multi-tenant vGPU slicing enables fractional consumption models that attract SMB developers. Meanwhile, hyperscaler outposts such as AWS Local Zones and Azure Edge Zones extend cloud management to regional POPs, blending cloud tools with edge sovereignty. Together, these factors propel edge nodes from pilot to production scale throughout the forecast window.

By GPU Type: Inference Narrows the Training Lead

Training GPUs accounted for 57.82% of 2025 revenue, but inference accelerators will outpace it at a 13.45% CAGR as post-training compute budgets rise. The North America data center GPU market share for inference hardware is widening thanks to FP4 engines in Blackwell, 288 GB HBM3E on MI355X, and Gaudi 3’s price-performance profile. Enterprises favor inference GPUs that cut watt-hours per generated token by half, improving TCO under carbon caps.

Architectural convergence blurs boundaries between training and serving. Unified GPU clusters now reconfigure on demand, with Kubernetes scheduling HBM-rich nodes for few-shot fine-tuning by day and high-throughput inference overnight. Test-time compute, chain-of-thought prompting, and RLHF loops increase inference cycles per user query, driving demand parity with training within three years. Consequently, vendors are optimizing memory bandwidth and scheduler microcode for real-time serving, redefining performance metrics around tokens per joule rather than pure FLOPs.

By Interconnect: NVLink Fabrics Redefine Rack-Scale Compute

PCIe configurations accounted for 68.87% of deployments in 2025, yet high-bandwidth fabrics will grow at a 14.21% CAGR as training clusters scale beyond 16-GPU boxes. The North America data center GPU market for GPUs linked via NVLink or CXL is expanding because hyperscalers view lost opportunity in minutes of wall-clock time. NVLink 5 bonds 72 GPUs into a logical super-accelerator, delivering 130 TB-per-second fabric bandwidth that cuts communication overhead from 30% to under 5%.

Economic calculus favors NVLink for multi-billion-parameter models, but PCIe Gen5 remains adequate for single-server fine-tunes and edge inference. Liquid-cooling prerequisites still slow NVLink adoption in older colocation halls that lack chilled-water loops. Nevertheless, operators in Texas and Arizona retrofit facilities to capture tax incentives tied to energy-efficient gear, and renewable-powered campuses in Quebec are ordering NVL72 racks that pair hydroelectricity with 95%-plus water-side economizers.

By Workload Type: Analytics Emerges as GPU’s Next Frontier

AI and ML workloads accounted for 67.99% of demand in 2025, yet analytics will register a 14.66% CAGR as GPU-accelerated data warehouses mature. The North America data center GPU industry is seeing SQL engines on DuckDB, Presto, and Photon delivering 6-7x price-performance gains, motivating banks and telecoms to migrate risk and churn models to GPUs.

The shift hinges on software democratization. RAPIDS plug-ins eliminate CUDA code, enabling data engineers to port ETL pipelines with minimal refactoring. Financial-services firms that once tolerated overnight batch reports now push for intraday insights, and GPU clusters satisfy compliance windows without multiplying server footprints. As data gravity rises, downstream AI pipelines benefit from co-located analytics, reinforcing GPU penetration beyond pure model training.

By End User: Government Labs Lead the Next Wave

Hyperscalers held 53.45% market share in 2025, but government and research institutions will grow at 14.84% CAGR as U.S. and Canadian agencies fund exascale AI. The North America data center GPU market size allocated to federal labs is expanding through programs such as Horizon and Doudna, which aggregate more than 14 exaflops of AI compute.

Public-sector appetite shapes the vendor road map. Labs act as first adopters of Blackwell and Rubin platforms, de-risking architectures before enterprise rollout. Procurement rules stipulate domestic manufacturing and open-stack compatibility, driving investment in U.S. fabs and ROCm porting. Once stabilized, configurations cascade to Fortune 500 adopters seeking validated blueprints, shortening their proof-of-concept cycles and reinforcing the learning curve for non-hyperscale buyers.

Geography Analysis

The United States anchored 83.45% of 2025 revenue and continues to dominate the North America data center GPU market thanks to multi-gigawatt campuses in Oregon’s Chehalis Corridor, Virginia’s Data Center Alley, and Texas’s Renewable Triangle. Property-tax abatements, 230 kV substation permits, and ready fiber backbones accelerate ground-up builds that house hundreds of thousands of GPUs. Yet stricter interconnection studies now add 12-24 months of lead time, prompting private-equity-backed roll-ups of shovel-ready sites to hedge regulatory risk. A USD 40 billion consortium's acquisition of a 5 GW operator underscores how control of infrastructure has become strategic for AI investors.

Canada is projected to outgrow the region at a 13.77% CAGR, buoyed by sovereign cloud mandates, abundant hydroelectricity, and CAD-denominated carbon levies that reward energy-efficient liquid cooling. Quebec and British Columbia host clusters of 50,000-plus GPUs serviced by 99% renewable grids, enabling cloud-adjacent AI factories with credible green-compute claims. Provincial co-investment, exemplified by the LaSalle AI hub and Prairie2Cloud, reduces financing hurdles for domestically-owned data centers and keeps sensitive workloads north of the border.

Mexico remains embryonic but is gaining traction as a nearshoring substitute for congested U.S. markets. A 10 MW, 5,000-GPU build in Querétaro targets Latin American enterprises and U.S. overflow demand. Competitive power tariffs and favorable depreciation schedules shorten ROI, although limited long-haul fiber outside core metros tempers immediate scale. Over the forecast period, the North America data center GPU market expects Mexico to absorb spillover demand that cannot be sited in carbon-constrained U.S. grids.

Competitive Landscape

Market concentration is moderate. One incumbent controls a majority of training and inference revenue, leveraging a mature CUDA stack and the NVLink ecosystem. Nonetheless, AMD secured a multi-generation, 6 GW deal with a leading social media platform, tying shipment milestones to a sizable warrant. Intel’s Gaudi 3, sold via IBM Cloud, offers 50% better inference throughput per dollar, appealing to cost-sensitive enterprises seeking an ecosystem hedge.

Specialized vendors are carving niches. Cerebras deploys wafer-scale engines in regional data centers for latency-critical edge inference. Tenstorrent raised nearly USD 1 billion to commercialize Blackhole p100/p150 cards with composable interconnects, signing USD 150 million in contracts. Graphcore pivots toward sovereign-AI buyers that prize open software. While these challengers face integration costs and limited developer mindshare, they introduce pricing pressure and broaden architectural choices for buyers wary of single-vendor reliance.

Strategically, vertical integration is accelerating. A multibillion-dollar optics pact between a top GPU vendor and a photonics supplier secures on-shore capacity for next-gen interconnects. CoreWeave locked in a USD 6.3 billion unsold-capacity guarantee, funding rapid GPU-as-a-service expansion and signaling a new financing model that pairs acceleration inventory with cloud-native orchestration. Private-equity consortia are amassing data-center portfolios, betting that controlling megawatts is as critical as owning silicon.

North America Data Center GPU Industry Leaders

NVIDIA Corporation

Advanced Micro Devices Inc.

Intel Corporation

Graphcore Ltd.

Cerebras Systems Inc.

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- April 2026: NVIDIA released vGPU 19.0, enabling up to 48 virtual machines per RTX PRO 6000 Blackwell GPU across regulated sectors.

- March 2026: NVIDIA and Coherent entered a multi-year optics partnership, backed by a USD 2 billion equity investment, to scale next-gen photonic interconnects.

- February 2026: AMD and Meta signed a multi-generation pact for up to 6 GW of Instinct GPUs, with shipments starting 2H 2026 and a performance-based warrant for up to 160 million AMD shares.

- October 2025: A USD 40 billion consortium acquisition of Aligned Data Centers added roughly 5 GW of capacity to a new AI-focused portfolio.

North America Data Center GPU Market Report Scope

The North America Data Center GPU Market Report is Segmented by Deployment Type (Cloud Data Centers, Enterprise/Private Data Centers, and Edge Data Centers), GPU Type (Training GPUs, and Inference GPUs), Interconnect (PCIe-Based GPUs and High-Bandwidth Interconnect GPUs), Workload Type (AI and ML, HPC, Data Analytics, and Graphics and Visualization), End-User (Hyperscalers/CSPs, Enterprises, and Government and Research), and Geography (United States, Canada, and Mexico). The Market Forecasts are Provided in Value (USD).

| Cloud Data Centers |

| Enterprise / Private Data Centers |

| Edge Data Centers |

| Training GPUs |

| Inference GPUs |

| PCIe-Based GPUs |

| High-Bandwidth Interconnect GPUs |

| Artificial Intelligence (AI) and Machine Learning (ML) |

| High-Performance Computing (HPC) (non-AI scientific computing) |

| Data Analytics (database acceleration, query processing) |

| Graphics and Visualization (VDI, rendering, digital twins) |

| Hyperscalers / Cloud Service Providers |

| Enterprises |

| Government and Research Institutions |

| United States |

| Canada |

| Mexico |

| By Deployment Type | Cloud Data Centers |

| Enterprise / Private Data Centers | |

| Edge Data Centers | |

| By GPU Type | Training GPUs |

| Inference GPUs | |

| By Interconnect | PCIe-Based GPUs |

| High-Bandwidth Interconnect GPUs | |

| By Workload Type | Artificial Intelligence (AI) and Machine Learning (ML) |

| High-Performance Computing (HPC) (non-AI scientific computing) | |

| Data Analytics (database acceleration, query processing) | |

| Graphics and Visualization (VDI, rendering, digital twins) | |

| By End-User | Hyperscalers / Cloud Service Providers |

| Enterprises | |

| Government and Research Institutions | |

| By Country | United States |

| Canada | |

| Mexico |

Key Questions Answered in the Report

What is the 2026 value of the North America data center GPU market?

The North America data center GPU market size is valued at USD 24.89 billion in 2026.

Which deployment segment is growing fastest?

Edge data centers are projected to expand at a 13.89% CAGR through 2031 as latency-sensitive inference moves closer to users.

Who holds the largest share among GPU vendors?

NVIDIA maintains the leading market position, driven by its CUDA software stack and NVLink interconnect ecosystem.

Why are government laboratories increasing GPU purchases?

U.S. and Canadian research agencies are funding exascale AI clusters to advance climate modeling, materials science, and national security applications.

How are electricity tariffs influencing data center design?

Rising tariffs and carbon pricing are accelerating the adoption of liquid-cooled GPU servers that reduce power consumption per teraFLOP by up to 40%.

What role does high-bandwidth memory play in supply constraints?

Shortages of HBM3E and packaging capacity extend GPU lead times beyond 50 weeks, prompting multi-year purchase agreements and equity-linked supply deals.

Page last updated on: