Germany Data Center GPU Market Size and Share

Market Overview

| Study Period | 2020 - 2031 |

|---|---|

| Forecast Data Period | 2026 - 2031 |

| Base Year Market Size (2025) | USD 3.38 Billion |

| Market Size (2026) | USD 3.91 Billion |

| Market Size (2031) | USD 6.89 Billion |

| Growth Rate (2026 - 2031) | 11.96% CAGR |

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

Germany Data Center GPU Market Analysis by Mordor Intelligence

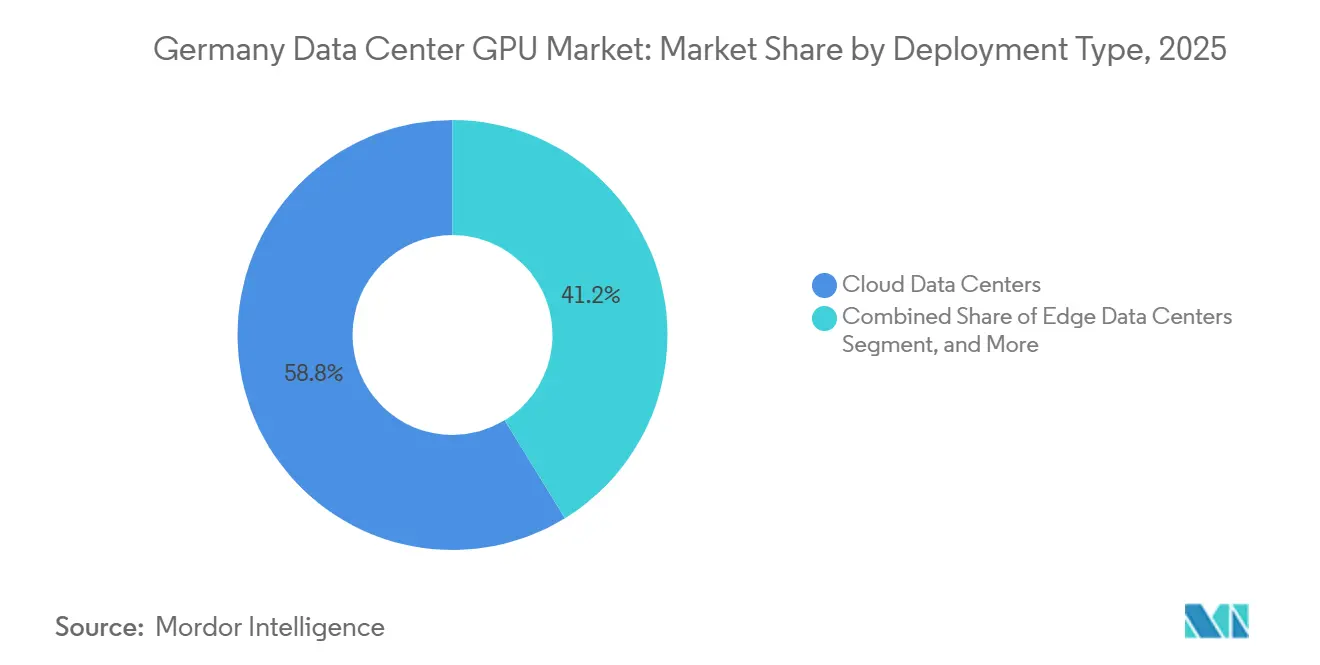

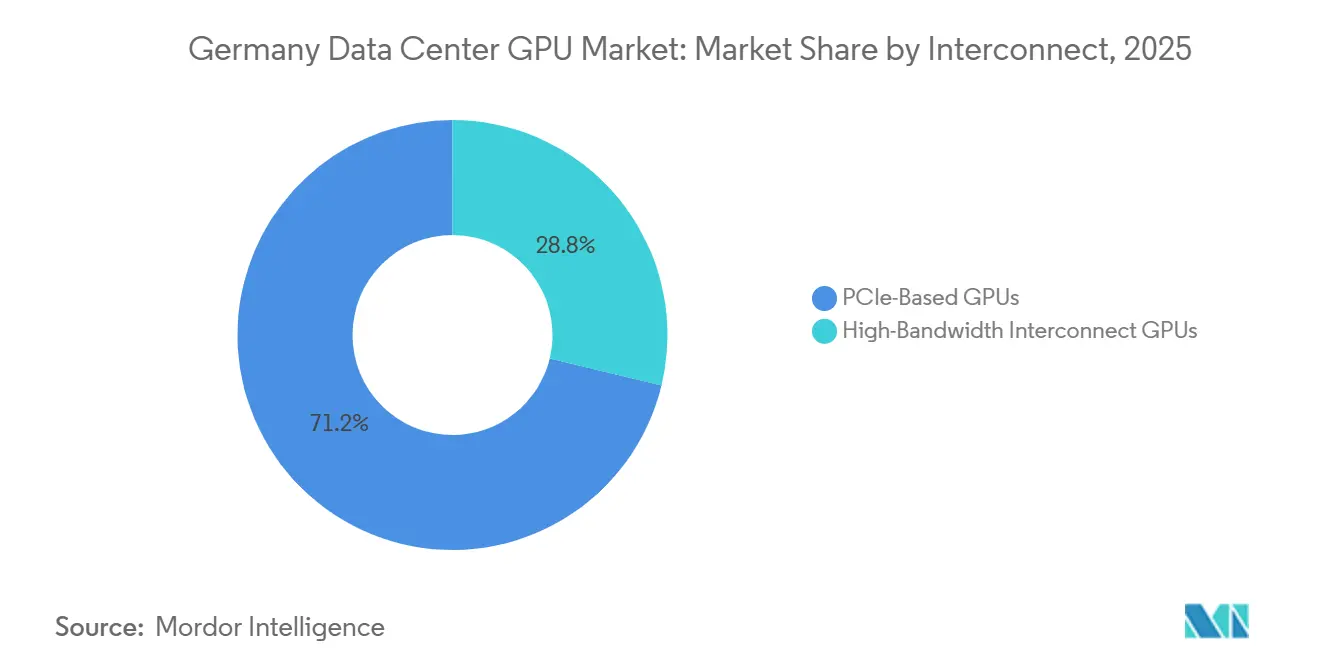

The Germany data center GPU market size is expected to increase from USD 3.38 billion in 2025 to USD 3.91 billion in 2026 and reach USD 6.89 billion by 2031, growing at a CAGR of 11.96% over 2026-2031. Cloud data centers led with 58.76% of deployment share in 2025, but grid bottlenecks in Frankfurt and Berlin are diverting new builds toward sovereign and edge facilities. Edge deployments are expanding fastest because automotive and industrial automation workloads need sub-10-millisecond inference latency. PCIe-based GPUs retained a 71.22% share in 2025, although NVLink and InfiniBand fabrics are climbing at double-digit rates to support foundation-model training. The Energy Efficiency Act drives liquid-cooled racks, while the EU AI Act steers sensitive workloads onto sovereign clouds.

Key Report Takeaways

- By deployment type, cloud data centers held 58.76% of the Germany data center GPU market share in 2025, and edge facilities are expected to advance at a 12.78% CAGR through 2031.

- By GPU type, training accelerators commanded 55.72% of the Germany data center GPU market in 2025, and inference accelerators are projected to grow at a 12.88% CAGR between 2026-2031.

- By interconnect, PCIe solutions accounted for 71.22% revenue share in 2025, while graphics and visualization are expanding at a 13.11% CAGR to 2031.

- By workload type, AI and ML accounted for 57.77% revenue share in 2025, while high-bandwidth fabrics are expected to expand at a 13.11% CAGR to 2031.

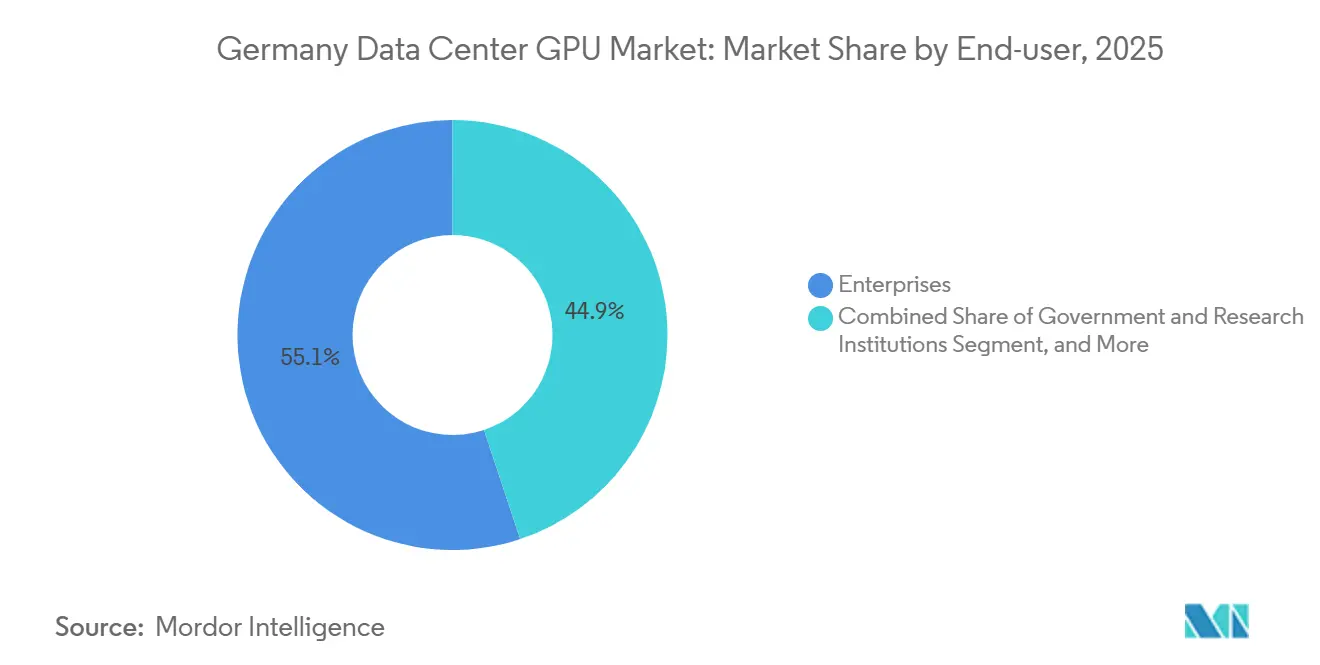

- By end-user enterprises represented 55.10% of end-user demand in 2025, whereas government and research institutions are expected to be the fastest-growing end users at a 13.65% CAGR through 2031.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of January 2026.

Germany Data Center GPU Market Trends and Insights

Drivers Impact Analysis*

| DRIVER | (~) % IMPACT ON CAGR FORECAST | GEOGRAPHIC RELEVANCE | IMPACT TIMELINE |

|---|---|---|---|

| Growing Adoption of AI Workloads in German Enterprises | +3.2% | Bavaria, Baden-Württemberg, Hesse | Medium term (2–4 years) |

| Expansion of Hyperscaler Cloud Regions in Frankfurt and Berlin | +2.8% | Frankfurt Rhine-Main, Berlin-Brandenburg | Short term (≤ 2 years) |

| Emergence of Sovereign Cloud Initiatives Driving Local GPU Capacity | +2.1% | National, federal procurement priority | Long term (≥ 4 years) |

| Rising Demand for Energy-Efficient GPU Servers Amid ESG Regulations | +1.6% | National, stricter in urban hubs | Medium term (2–4 years) |

| Government Funding for HPC and Quantum Research Facilities | +1.3% | Baden-Württemberg, Bavaria | Long term (≥ 4 years) |

| Increasing Edge Computing Needs for Autonomous Manufacturing | +1.0% | Bavaria, Baden-Württemberg, North-Rhine-Westphalia | Medium term (2–4 years) |

| Source: Mordor Intelligence | |||

Growing Adoption of AI Workloads in German Enterprises

SAP’s Industrial AI Cloud signed over 100 manufacturers in 2025, shifting mid-market buyers from capital purchases toward consumption-based GPU contracts.[1]SAP SE, “Industrial AI Cloud – Customer Commitments,” sap.com By Q4 2025, Northern Data revealed that its H100 and H200 GPUs were secured under reserved or on-demand agreements, highlighting a shift from speculative interest to firm enterprise commitments. BMW harnessed DGX Hopper clusters to produce synthetic driving images, slashing the training time for perception models. While financial services continue to test fraud-detection models, the rollout is delayed by transparency requirements under the EU AI Act.

Expansion of Hyperscaler Cloud Regions in Frankfurt and Berlin

AWS spent EUR 8.8 billion (USD 9.9 billion) expanding Frankfurt zones, yet new entrants must now fund 100% of substation upgrades under revised grid rules. Google countered with a EUR 5.5 billion (USD 6.2 billion) Dietzenbach campus that bypasses inner-city transformer congestion. AWS’s EUR 7.8 billion (USD 8.8 billion) Brandenburg sovereign cloud, targeting federal workloads, shows operators are geographically splitting latency-sensitive inference and batch training.

Emergence of Sovereign Cloud Initiatives Driving Local GPU Capacity

Deutsche Telekom’s EUR 1 billion (USD 1.13 billion) Munich AI Factory contracts guarantee data never leaves EU jurisdiction, meeting defense and pharma compliance needs. SAP partnered with OpenAI on a 4,000-GPU sovereign instance slated for 2026, providing public agencies with GPT-class tools without cross-border exposure. Schwarz Group plans a 100,000-GPU campus in Lübbenau by 2027, providing wholesale capacity to firms that lack direct access to NVIDIA or AMD supply.

Rising Demand for Energy-Efficient GPU Servers Amid ESG Regulations

The Energy Efficiency Act enforces a PUE < 1.3 by 2030 and 10-20% waste-heat reuse, prompting liquid-cooled rack adoption.[2]German Federal Ministry for Economic Affairs and Climate Action, “Energy Efficiency Act,” bmwk.de Dell’s PowerEdge XE9680L recovers heat at 60-70 °C, fitting municipal district-heating ranges. Retrofitting older halls costs ~EUR 500 (USD 565) per kW and needs coordination with local utilities that often lack pipe capacity, favoring deep-pocket hyperscalers.

Restraints Impact Analysis*

| RESTRAINT | (~) % IMPACT ON CAGR FORECAST | GEOGRAPHIC RELEVANCE | IMPACT TIMELINE |

|---|---|---|---|

| High Electricity Costs and Grid Constraints in Major German Data Center Hubs | -2.4% | Frankfurt Rhine-Main, Berlin, Munich | Short term (≤ 2 years) |

| Supply Chain Dependence on Non-EU GPU Manufacturers | -1.8% | National, Europe-wide spillover | Medium term (2–4 years) |

| Stringent Data Protection and Residency Regulations Limiting Cross-Border Workloads | -0.9% | National, heightened in public sector | Long term (≥ 4 years) |

| Skilled GPU Programming Talent Shortage | -0.7% | Bavaria, Baden-Württemberg | Medium term (2–4 years) |

| Source: Mordor Intelligence | |||

High Electricity Costs and Grid Constraints in Major German Data Center Hubs

In 2024, medium-voltage users in Frankfurt faced network fees. With pending grid requests in Berlin totaling 2.8 GW, operators are now tasked with financing comprehensive substation upgrades. These upgrades extend the construction timeline by 18 to 36 months.

Supply Chain Dependence on Non-EU GPU Manufacturers

The EU Chips Act funds mature-node fabs, not 3 nm lines needed for Blackwell or MI450 GPUs. SK Hynix controlled up to 80% of HBM3E supply in 2025, granting hyperscalers first rights and forcing mid-market buyers to pay a 30% premium.[3]SK Hynix, “HBM3E Supply and Market Share,” skhynix.com HLRS mitigated single-vendor risk by selecting AMD MI300A APUs for its Hunter system, yet software teams must now straddle ROCm and CUDA.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Deployment Type: Edge Outpaces Cloud in Growth Velocity

Edge facilities are forecast to record a 12.78% CAGR through 2031, underpinned by automotive OEMs that install local GPU clusters to keep perception latency below 10 ms. BMW’s Munich research hub used DGX Hopper nodes to achieve an 8-fold increase in synthetic-image generation, underscoring why private edge racks are proliferating.[4]BMW Group, “SORDI Dataset with NVIDIA DGX Hopper,” bmwgroup.com

Cloud data centers still accounted for 58.76% of revenue in 2025, but Frankfurt’s grid caps and Baukostenzuschüsse now slow further construction. SAP’s sovereign AI Cloud straddles private and public models, letting manufacturers retain data locality while offloading operations.

By GPU Type: Inference Accelerators Close the Gap

Training GPUs accounted for 55.72% of 2025 spending, as hyperscalers snapped up H100 and H200 inventory for foundation-model runs. Intel’s Gaudi 3, offered in IBM Cloud’s Frankfurt region, claims 50% lower inference costs than the H100, promoting Ethernet fabrics over InfiniBand.

Inference demand is rising most sharply at the edge, where slot power and form-factor efficiency matter more than peak FLOPS. AMD’s MI300 roadmap doubles HBM per GPU, appealing to memory-bound inference tasks in sovereign clouds.[5]Advanced Micro Devices, “Data Center Segment Q4 FY2025 Results,” amd.com

By Interconnect: Bandwidth Demands Reshape Topology

High-bandwidth fabrics should post a 13.11% CAGR through 2031, driven by NVLink and InfiniBand clusters such as Deutsche Telekom’s 10,000-GPU Munich AI Factory. PCIe still anchors 71.22% of 2025 installs because it fits existing x86 racks.

Intel’s Ethernet-based RoCE design reduces switch cost for scale-out inference farms. Smaller enterprises embrace PCIe cards because many inference jobs remain single-GPU and capital budgets remain tight.

By Workload Type: Graphics Gains Momentum

Graphics and visualization workloads are projected to expand at 12.64% CAGR as firms adopt digital twins for factory layouts and CAD rendering for remote teams. AI and ML jobs accounted for 57.77% of jobs in 2025, but are now trending toward cost-optimized production deployments.

HPC stays anchored in research labs such as HLRS’s Hunter supercomputer, which delivers 48.1 petaflops on MI300A APUs. HP’s Z8 Fury G6i puts four RTX PRO 6000 Blackwell Max-Q GPUs into a single tower for on-site media rendering.

By End-User: Government Accelerates Fastest

Government and research bodies will advance GPU spend at 13.65% CAGR through 2031, supported by Germany’s goal to quadruple AI and HPC resources by 2030. AWS’s Brandenburg sovereign cloud pledges GPU capacity solely for federal clients, meeting strict data-residency demands.

Enterprises held a 55.10% share in 2025, led by the automotive and chemical verticals, which are integrating GPUs into product engineering. Schwarz Group’s 100,000-GPU campus will wholesale capacity to mid-tier buyers that cannot secure direct allocation from NVIDIA or AMD.

Geography Analysis

Frankfurt remains the primary interconnect hub but faces pending grid requests, so operators fund complete substation builds, adding EUR 10-50 million (USD 1.17 - 58.45 million) to budgets. Google’s Dietzenbach campus, 25 km outside Frankfurt, uses surplus transformer capacity for AI training clusters.

Munich-Bavaria emerges as a sovereign AI cluster: Deutsche Telekom’s Munich AI Factory offers 10,000 Blackwell GPUs with data-residency guarantees. Siemens’ Erlangen digital twin hub anchors manufacturing-edge pilots. HLRS in nearby Stuttgart operates the Hunter MI300A system and has ordered the Herder exascale supercomputer for 2027.

Berlin-Brandenburg is evolving into a public-sector cloud center, led by AWS’s sovereign region and Schwarz Group’s Lübbenau mega-campus. Secondary cities like Nuremberg host Hetzner’s GPU instances, appealing to cost-sensitive SMEs priced out of Frankfurt.

Competitive Landscape

NVIDIA secured a significant share of 2025 training GPU shipments, leveraging its CUDA software and ecosystem tooling. Deutsche Telekom deployed 10,000 Blackwell GPUs in Munich, bundling them with managed MLOps for German enterprises that prefer sovereign infrastructure. Siemens, in partnership with NVIDIA and utilizing its BlueField DPUs, has positioned itself as an industrial-edge integrator, extending NVIDIA IP into factories where hyperscalers face challenges.

AMD is making inroads into the market through high-bandwidth memory. Meta's roadmap for the 6-GW MI450 and HLRS's selection of the MI300A and the upcoming MI430X GPUs indicate a shift towards diversifying procurement, moving away from reliance on a single vendor. AMD's data-center growth is putting pressure on NVIDIA to ramp up capacity, especially given U.S. export-control quotas that limit shipments to China.

Intel is focusing on inference deployments with Gaudi 3's Ethernet-first topology. In the Frankfurt region, IBM Cloud is offering Gaudi 3 instances that use 1.2 Tbps RoCE links instead of NVLink. This strategy aligns with the preferences of European enterprises, which prefer standards-based interconnects and open-source frameworks. Northern Data is carving a niche in high-frequency trading and cryptocurrency by reselling reserved H100/H200 nodes at premium spot tariffs. Meanwhile, Schwarz Group is channeling its retail cash flows to fund a 100,000-GPU campus, positioning itself as a nationwide wholesale capacity marketplace.

Germany Data Center GPU Industry Leaders

NVIDIA Corporation

Advanced Micro Devices Inc.

Intel Corporation

Dell Technologies Inc.

Hewlett Packard Enterprise Company

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- April 2026: Siemens launched the Industrial Automation DataCenter, integrating NVIDIA GPUs and BlueField DPUs for sub-10 ms edge inference.

- April 2026: HP unveiled the Z8 Fury G6i workstation with four RTX PRO 6000 Blackwell Max-Q GPUs.

- March 2026: The Federal Ministry for Digital and Transport released the National Data Center Strategy, aiming to increase AI and HPC capacity by 4x by 2030.

- January 2026: Siemens and NVIDIA introduced the Industrial AI Operating System for GPU-accelerated digital twins.

Germany Data Center GPU Market Report Scope

The Germany Data Center GPU Market Report is Segmented by Deployment Type (Cloud Data Centers, Enterprise/Private Data Centers, and Edge Data Centers), GPU Type (Training GPUs, and Inference GPUs), Interconnect (PCIe-Based GPUs and High-Bandwidth Interconnect GPUs), Workload Type (AI and ML, HPC, Data Analytics, and Graphics and Visualization), and End-User (Hyperscalers/CSPs, Enterprises, and Government and Research). The Market Forecasts are Provided in Value (USD).

| Cloud Data Centers |

| Enterprise / Private Data Centers |

| Edge Data Centers |

| Training GPUs |

| Inference GPUs |

| PCIe-Based GPUs |

| High-Bandwidth Interconnect GPUs |

| Artificial Intelligence (AI) and Machine Learning (ML) |

| High-Performance Computing (HPC) (non-AI scientific computing) |

| Data Analytics (database acceleration, query processing) |

| Graphics and Visualization (VDI, rendering, digital twins) |

| Hyperscalers / Cloud Service Providers |

| Enterprises |

| Government and Research Institutions |

| By Deployment Type | Cloud Data Centers |

| Enterprise / Private Data Centers | |

| Edge Data Centers | |

| By GPU Type | Training GPUs |

| Inference GPUs | |

| By Interconnect | PCIe-Based GPUs |

| High-Bandwidth Interconnect GPUs | |

| By Workload Type | Artificial Intelligence (AI) and Machine Learning (ML) |

| High-Performance Computing (HPC) (non-AI scientific computing) | |

| Data Analytics (database acceleration, query processing) | |

| Graphics and Visualization (VDI, rendering, digital twins) | |

| By End-User | Hyperscalers / Cloud Service Providers |

| Enterprises | |

| Government and Research Institutions |

Key Questions Answered in the Report

What is the forecast size of Germany’s data center GPU spending by 2031?

The Germany data center GPU market size is projected to reach USD 6.89 billion by 2031, expanding at an 11.96% CAGR.

Which deployment model is expanding fastest?

Edge facilities are set to grow at a 12.78% CAGR through 2031, driven by sub-10 ms latency demands in automotive and industrial plants.

What share did training GPUs capture in 2025?

Training accelerators held 55.72% of 2025 revenue, though inference GPUs are closing the gap.

Why is sovereign cloud capacity critical in Germany?

GDPR and the EU AI Act require sensitive data to remain in national jurisdictions, prompting Deutsche Telekom, SAP, and AWS to build domestic GPU regions.

What regulatory rule is changing data-center cooling?

The Energy Efficiency Act mandates a PUE below 1.3 by 2030 and 10-20% waste-heat reuse, pushing operators toward liquid-cooled GPU racks.

Which end-user group will record the highest growth rate?

Government and research institutions are forecast to expand GPU demand at a 13.65% CAGR, buoyed by federal HPC funding.

Page last updated on: