Europe Data Center GPU Market Size and Share

Market Overview

| Study Period | 2020 - 2031 |

|---|---|

| Forecast Data Period | 2026 - 2031 |

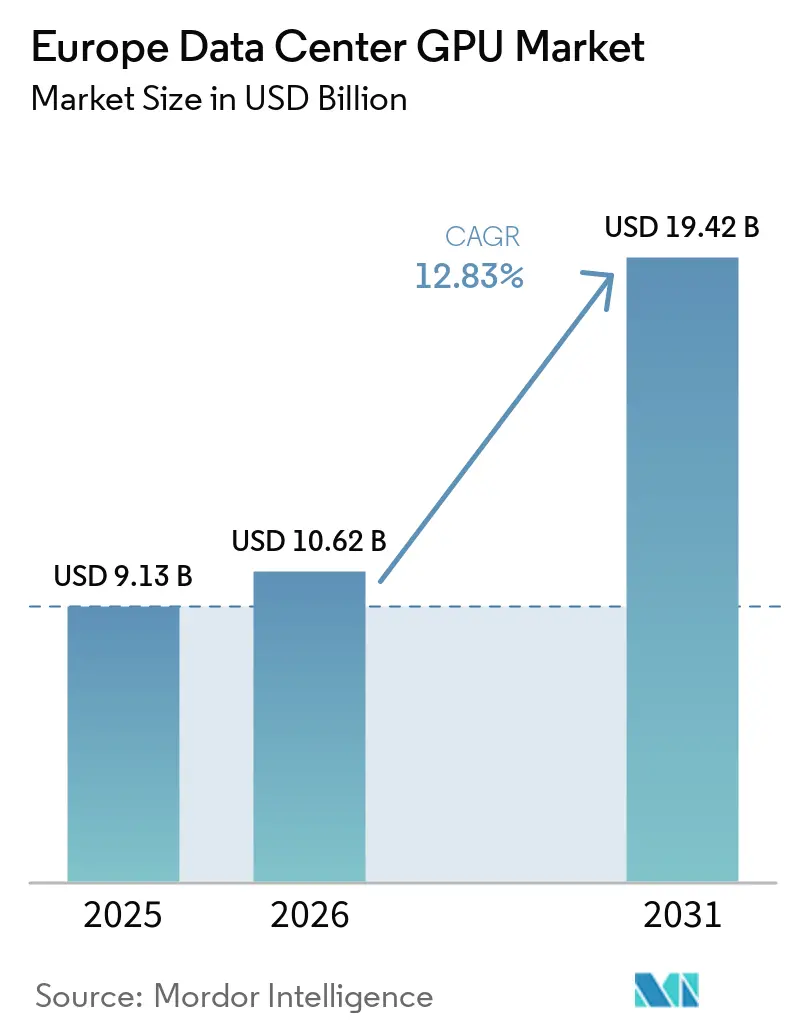

| Base Year Market Size (2025) | USD 9.13 Billion |

| Market Size (2026) | USD 10.62 Billion |

| Market Size (2031) | USD 19.42 Billion |

| Growth Rate (2026 - 2031) | 12.83% CAGR |

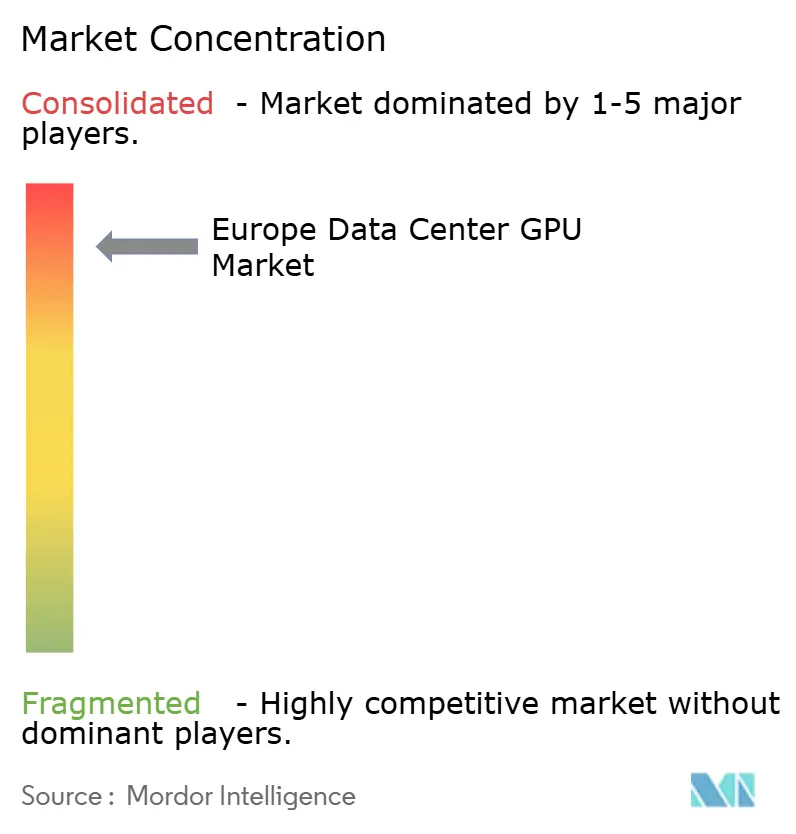

| Market Concentration | High |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

Europe Data Center GPU Market Analysis by Mordor Intelligence

The Europe data center GPU market is expected to grow from USD 10.62 billion in 2026 to USD 19.42 billion by 2031, at a 12.83% CAGR over 2026-2031. Edge data centers are scaling faster than cloud campuses as latency-sensitive inference moves closer to end users, while sovereign-cloud mandates steer capital toward on-premises GPU fleets. Enterprises continue to anchor demand, yet EuroHPC procurements and national AI strategies are accelerating public-sector adoption. Persistent supply-chain tightness in advanced packaging keeps lead times elevated, encouraging operators to diversify accelerator vendors and geographic sourcing. Liquid-cooling retrofits and green-bond incentives underpin energy-efficient upgrades, tempering the cost pressures created by high European electricity prices.

Key Report Takeaways

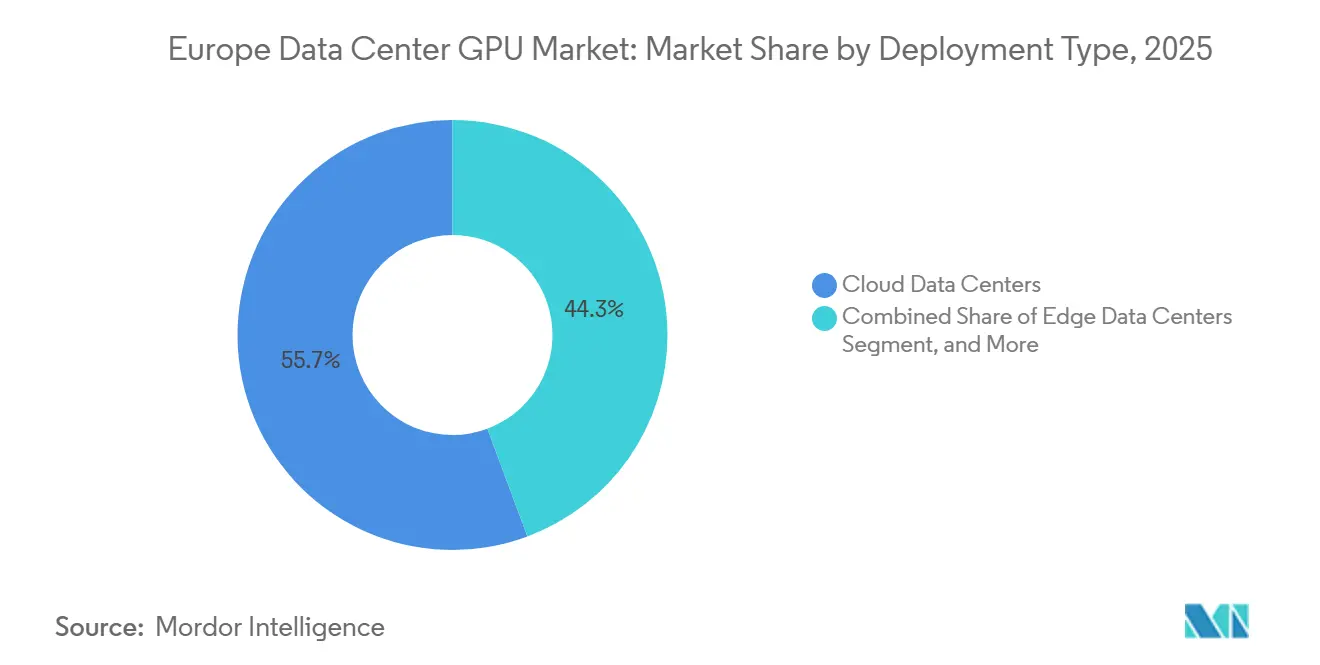

- By deployment type, cloud data centers led with 55.67% revenue share in 2025, while edge facilities are projected to expand at a 14.66% CAGR through 2031.

- By GPU type, training accelerators held 59.87% of the Europe data center GPU market share in 2025, whereas inference devices are forecast to post a 14.78% CAGR to 2031.

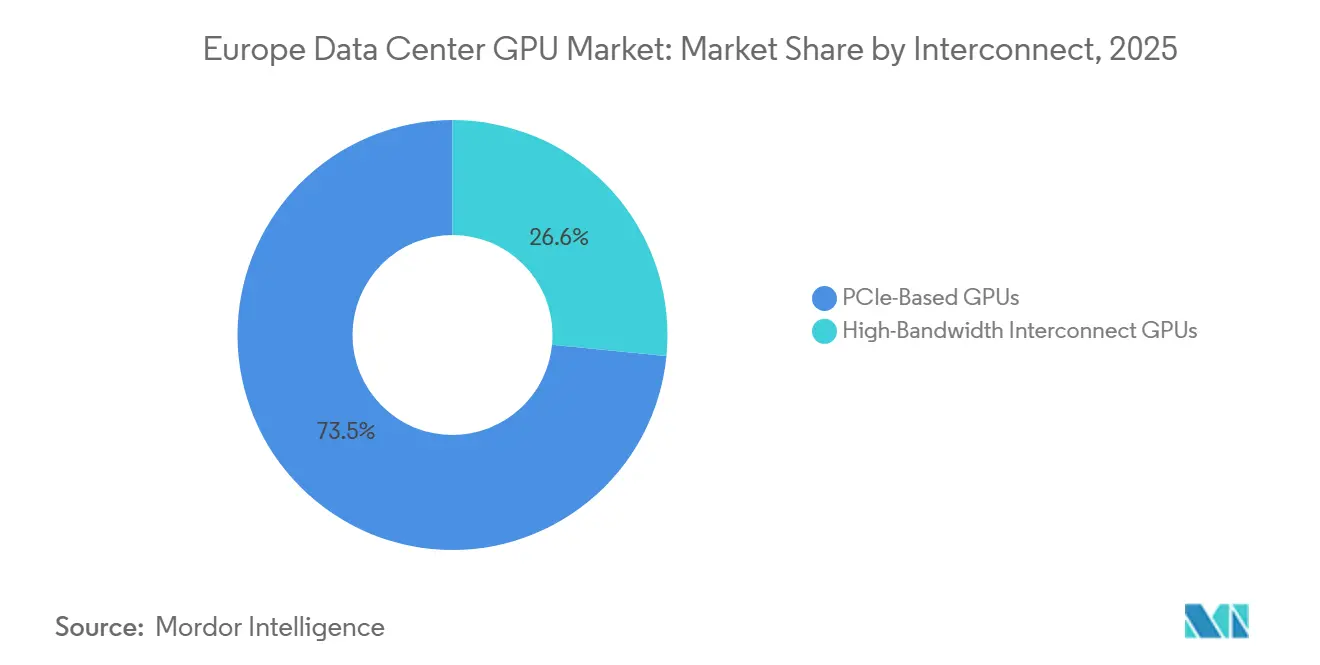

- By interconnect, PCIe solutions accounted for 73.45% of the Europe data center GPU market size in 2025, yet high-bandwidth fabrics are expected to grow at a 15.21% CAGR between 2026-2031.

- By workload, AI and machine-learning applications captured 57.89% of the revenue share in 2025, while graphics and visualization workloads are set to rise at a 14.23% CAGR through 2031.

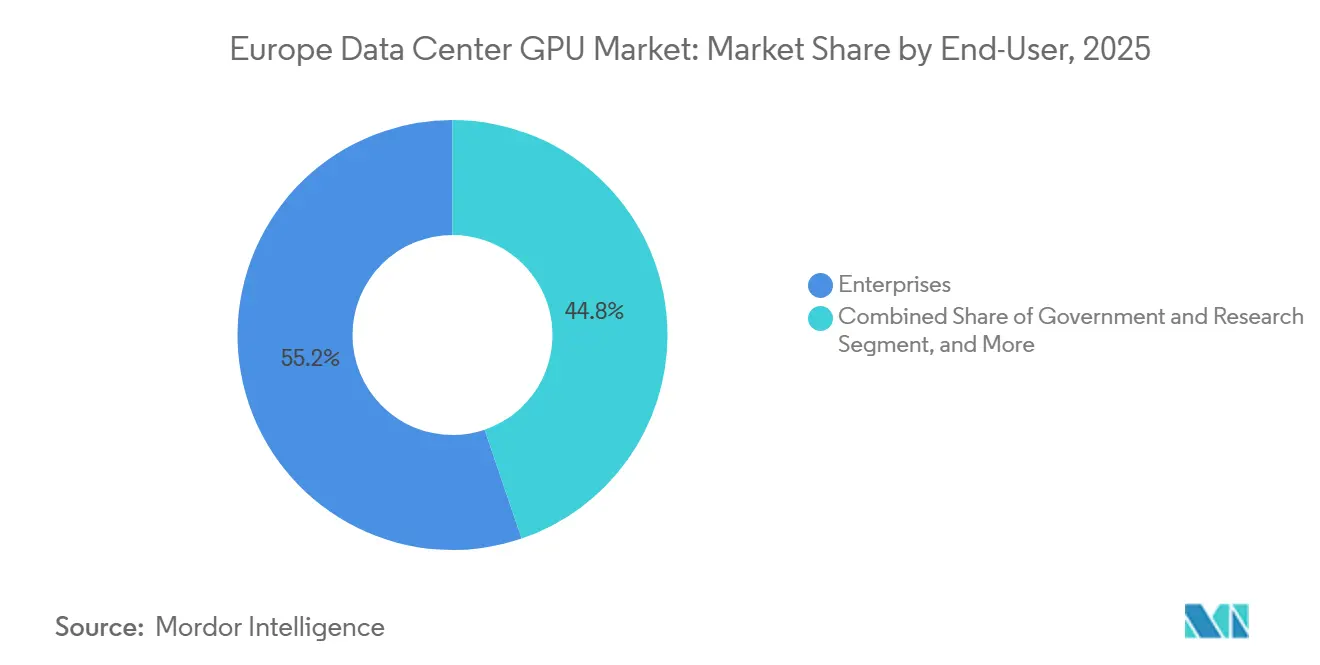

- By end user, enterprises generated 55.21% of 2025 revenue, whereas government and research institutions are anticipated to register a 15.55% CAGR through 2031.

- By geography, Germany accounted for 34.33% of revenue in 2025; France is projected to be the fastest-growing country at a 15.77% CAGR over 2026-2031.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of January 2026.

Europe Data Center GPU Market Trends and Insights

Drivers Impact Analysis*

| DRIVER | (~) % IMPACT ON CAGR FORECAST | GEOGRAPHIC RELEVANCE | IMPACT TIMELINE |

|---|---|---|---|

| Accelerating demand for AI model training capacity across European hyperscale campuses | +3.2% | Germany, France, the Nordic region | Medium term (2-4 years) |

| Growing adoption of GPU-powered analytics platforms in the financial services and telecom sectors | +2.8% | Germany, the United Kingdom, and France | Short term (≤ 2 years) |

| EU Green Deal incentives are pushing energy-efficient GPU upgrades in data centers | +2.1% | European Union-wide, strongest in Germany and the Netherlands | Long term (≥ 4 years) |

| Rising uptake of sovereign cloud initiatives requiring on-prem GPU clusters | +1.9% | France, Germany, Italy | Medium term (2-4 years) |

| Emergence of liquid-cooling retrofits enabling higher GPU rack densities | +1.5% | Germany, the United Kingdom, Nordic region | Short term (≤ 2 years) |

| Proliferation of synthetic data generation startups is driving a burst of GPU leasing | +1.2% | Austria, Netherlands, France | Short term (≤ 2 years) |

| Source: Mordor Intelligence | |||

Accelerating Demand for AI Model Training Capacity Across European Hyperscale Campuses

Hyperscale operators are commissioning GPU clusters with more than 10,000 accelerators to meet the compute intensity of foundation-model training, with deployments in Munich, Paris, and the Nordic states pushing regional exascale thresholds. Flexible power contracts and low-carbon grids attract capital to Northern Europe, while sovereign-cloud rules in Germany and France ensure that a sizeable share of this capacity remains domestically controlled. The scale of these clusters necessitates high-bandwidth fabrics such as NVLink 6, which reduces all-reduce latency and keeps GPU utilization above 90%. Collectively, these investments expand the addressable market for complementary interconnects, cooling systems, and on-premises AI services, boosting the European data center GPU market. However, they also magnify exposure to advanced packaging bottlenecks, compelling operators to secure multi-vendor contracts to hedge supply risk.

Growing Adoption of GPU-Powered Analytics Platforms in Financial Services and Telecom Sectors

Banks and carriers are embedding GPUs into fraud-detection, risk-modeling, and network-optimization pipelines, trimming inference times from minutes to milliseconds. Deutsche Bank, ING, Vodafone, and Orange each reported double-digit latency improvements after migrating analytical workloads to GPU clusters, validating the return on investment for accelerator upgrades. The surge of transactional and telemetry data streaming through European networks necessitates real-time processing, which CPU-only platforms cannot sustain cost-effectively. As a result, the Europe data center GPU market benefits from recurring hardware refresh cycles, software stack integrations, and managed service offerings tailored to regulated industries. Vendor support for open-source frameworks further lowers adoption barriers, allowing smaller institutions to harness GPU acceleration without proprietary lock-in.

EU Green Deal Incentives Pushing Energy-Efficient GPU Upgrades in Data Centers

The Energy Efficiency Directive obliges data centers above 500 kW to disclose power-usage effectiveness and renewable-energy metrics, creating a compliance imperative that favors liquid-cooled GPU racks capable of sub-1.20 PUE.[1]EuroHPC Joint Undertaking, “JUPITER Supercomputer,” eurohpc-ju.europa.euOperators adopting direct-to-chip or immersion solutions have documented electricity savings near 20% per rack, reducing annual energy bills. Access to green-bond financing under the EU Taxonomy further lowers the weighted-average cost of capital for facilities that retrofit legacy halls with efficient GPUs, thereby reinforcing hardware demand. These incentives expand the Europe data center GPU market by accelerating replacement cycles and motivating first-time buyers who previously delayed investments due to power constraints.

Rising Uptake of Sovereign Cloud Initiatives Requiring On-Prem GPU Clusters

National regulations in France, Germany, and Italy compel critical AI workloads to reside within domestic borders, spurring on-premises GPU build-outs inside certified facilities. Public-sector contracts specify European ownership, localized data processing, and adherence to GDPR criteria, which favor regional colocation providers and server makers. Partnerships such as Deutsche Telekom’s EURO-3C alliance and OVH’s 100,000-GPU roadmap illustrate how sovereignty clauses redirect spending from non-EU hyperscalers to local infrastructure. The Europe data center GPU market thus captures incremental revenue from government tenders, consulting services, and specialized security features integrated into accelerator deployments.

Restraints Impact Analysis*

| RESTRAINT | (~) % IMPACT ON CAGR FORECAST | GEOGRAPHIC RELEVANCE | IMPACT TIMELINE |

|---|---|---|---|

| Supply chain concentration risk around advanced packaging in Taiwan and South Korea | -2.1% | European Union-wide | Medium term (2-4 years) |

| High electricity prices in key European colocation hubs are denting TCO economics | -1.8% | Germany, Netherlands, United Kingdom | Short term (≤ 2 years) |

| Emerging EU chip-sovereignty rules are complicating cross-border GPU fleet sharing | -0.9% | European Union-wide, strongest in France and Germany | Long term (≥ 4 years) |

| Growing scrutiny over water usage for liquid-cooled GPU farms in drought-prone regions | -0.7% | Netherlands, Spain, Italy | Medium term (2-4 years) |

| Source: Mordor Intelligence | |||

Supply Chain Concentration Risk Around Advanced Packaging in Taiwan and South Korea

CoWoS and HBM3e capacity constraints extend delivery lead times for flagship GPUs beyond 50 weeks, disrupting rollout schedules for European cloud and research projects. Samsung and SK hynix prioritize larger North American contracts, compelling EU operators to consider alternative vendors or older GPU SKUs. The shortage inflates spot-market pricing, narrowing project margins and delaying revenue recognition across the Europe data center GPU market. Contingency actions, such as dual-sourcing strategies and inventory buffers, partially mitigate risk but add working-capital burdens.

High Electricity Prices in Key European Colocation Hubs Denting TCO Economics

Tariffs in Germany and the Netherlands surpass EUR 0.28 per kWh, elevating annual operating costs for 1 MW GPU clusters by millions of euros relative to Nordic sites.[2]European Commission, “Energy Efficiency Directive,” energy.ec.europa.eu These price differentials encourage capacity shifts toward Sweden, Finland, and Spain, where renewable supply is abundant and regulated rates are lower.[3]Dutch Government, “Water Restrictions for Data Centers,” government.nl Operators remaining in high-cost markets must deploy energy-efficient GPUs and aggressive heat-reuse systems to sustain competitiveness, putting pressure on the Europe data center GPU market to deliver performance gains without proportional power increases.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Deployment Type: Edge Acceleration Gains Traction

Edge facilities contributed a modest slice of 2025 revenue, yet are projected to outpace the Europe data center GPU market average with a 14.66% CAGR. Rapid adoption stems from autonomous-vehicle telemetry, industrial IoT sensor fusion, and augmented-reality streaming, all of which require under 10 ms round-trip latency. Cloud campuses retained 55.67% of turnover in 2025, reflecting hyperscale training clusters and multi-tenant inference farms anchored in Germany and France. Enterprises and private clouds fill the remainder, driven by compliance mandates favoring on-prem GPUs for sensitive financial and healthcare data.

Edge deployments benefit from micro-modular designs, fanless liquid cooling, and real-time orchestration stacks that push inference closer to subscribers. Telcos deploy GPU-enabled nodes at 5G base stations to dynamically slice bandwidth, while retail chains pilot in-store computer vision systems to enhance shopper analytics. Cloud providers respond by offering distributed inference services, creating hybrid architectures that span central campuses and regional aggregation points. This decentralized pattern expands the addressable market for Europe data center GPU markets beyond metropolitan hubs, unlocking opportunities for specialized integrators and carrier-neutral exchanges.

By GPU Type: Inference Accelerators Erode Training Dominance

Training GPUs accounted for 59.87% of 2025 sales because multi-rack clusters powered foundation-model development, but inference accelerators are forecast to post a 14.78% CAGR as enterprises shift budgets toward production deployment. NVIDIA’s L40S and L4 attract edge and enterprise buyers seeking high performance per watt for chatbots and fraud detection.[4]NVIDIA, “H100, H200, GB300, NVLink 6 Specifications,” nvidia.com AMD’s MI300X provides a lower-cost path for both training and inference at CoreWeave and Lambda Labs sites in Frankfurt and Paris.[5]AMD, “MI300X, MI325X, Infinity Fabric,” amd.com

Banks now channel most incremental capex toward inference, allocating memory-rich GPUs that handle millions of transactions per second without network round-trips to cloud campuses. Telecom operators prioritize latency and energy efficiency, selecting accelerators with on-package networking to minimize PCIe overhead. Training remains mission-critical for hyperscalers and research institutes, but its proportional share declines as mature models age into inference-heavy life-cycle phases.

By Interconnect: High-Bandwidth Fabrics Scale Out

PCIe-attached accelerators accounted for 73.45% of 2025 interconnect revenue, supported by broad server compatibility and lower entry costs. High-bandwidth fabrics such as NVLink and Infinity Fabric are expected to record a 15.21% CAGR through 2031, in lockstep with the need to synchronize thousands of GPUs inside exascale clusters. The Europe data center GPU market size for these premium fabrics grows when operators pursue trillion-parameter models or real-time physics simulations that cannot tolerate PCIe bottlenecks.

NVLink 6 ships with 3.6 TB s-1 per GPU, enabling pod-level all-reduce latencies under 3 µs. Infinity Fabric eases heterogeneous x86-GPU coherence, streamlining data-prep stages. Lenovo and Dell integrate PCIe Gen5 backplanes to keep cost-sensitive inference workloads competitive until high-bandwidth fabrics cascade into mid-range price points. Meanwhile, startups explore photonic interposers to extend link reach across aisles without degrading bandwidth, a potential inflection point that could reshape the Europe data center GPU market-share battle between incumbent and emerging interconnect technologies.

By Workload Type: Visualization Catches Up

AI-centric tasks accounted for 57.89% of 2025 revenue, yet visualization and graphics workloads are projected to grow at a 14.23% CAGR as digital twin adoption widens. Automotive and aerospace firms shift from CPU-bound rendering to GPU-driven real-time simulations, shortening design cycles and reducing physical prototyping costs. Virtual desktop infrastructure surged following the normalization of hybrid work, prompting enterprises to provision GPU blades that deliver workstation-class experiences to remote staff. These trends diversify the Europe data center GPU market beyond headline AI demand, cushioning cyclicality tied to model-training waves.

High-performance computing retains a sizable footprint, with EuroHPC deploying exascale systems for climate and materials science. Data analytics acceleration flourishes in financial services, where GPU-optimized SQL engines shrink reporting windows from hours to minutes. The incremental capacity carved out for graphics and analytics deepens utilization rates, enabling operators to monetize idle training GPUs during off-peak periods through time-sliced inference and rendering jobs.

By End User: Public-Sector Momentum Builds

Enterprises captured 55.21% of 2025 turnover, but government and research buyers are expected to post the fastest growth at 15.55% CAGR through 2031. EuroHPC procurements, national AI labs, and defense programs allocate multi-billion-euro budgets to sovereign GPU capacity. These initiatives strengthen domestic innovation ecosystems, foster open-source model development, and widen talent pipelines. The Europe data center GPU market thus becomes an instrument of industrial policy, with local content rules favoring European integrators and contract manufacturers.

Cloud service providers continue to anchor hyperscale capex, yet face share donations to on-prem sovereign clouds in sectors handling classified or strategic data. Energy firms, hospitals, and utilities are emerging as new adopters, attracted by proven case studies in predictive maintenance, medical imaging, and grid optimization. This broadening user mix stabilizes demand across economic cycles and diminishes over-reliance on a handful of hyperscale customers.

Geography Analysis

Germany remained the linchpin of the Europe data center GPU market in 2025, accounting for 34.33% of revenue thanks to hyperscale investments in Frankfurt, Hanau, and Munich. National telcos and automotive giants co-locate GPU clusters near fiber crossroads, leveraging dense peering to distribute global model. Elevated electricity costs, exceeding EUR 0.30 per kWh, are pressuring operator margins, but investments in liquid-cooling and heat reuse mitigate some expense headwinds. EuroHPC’s JUPITER supercomputer cements Germany’s role as a public-sector AI hub, anchoring research collaborations that radiate demand for ancillary accelerator services.

France is projected to be the fastest-growing locale, posting a 15.77% CAGR through 2031 as sovereign-cloud statutes and GPU-dense builds in Paris and Nordic interconnect sites gain momentum. Mistral AI’s multibillion-euro clusters showcase the country’s intent to retain training sovereignty while tapping low-carbon Nordic energy. Regulatory clarity under the 8ra initiative prompts ministries to shift workloads off non-EU clouds, boosting domestic demand for GPU colocation and managed services. Consistent nuclear baseload tempers wholesale price volatility, strengthening the value proposition relative to neighbors grappling with fossil-supply shocks.

The United Kingdom, Italy, Spain, and the broader Nordic corridor round out regional dynamics. London and Manchester cater to latency-critical finance and media tenants, relying on dense metro fiber grids to deliver sub-10 ms packet times. Italy leverages ISO-certified colocation to court public agencies, while ENI’s GPU supercomputer underscores industrial AI use cases spanning seismic imaging to carbon-capture modeling. Spain attracts hyperscalers with competitive solar and wind tariffs below EUR 0.20 per kWh, though water-usage caps in the Netherlands and Catalonia temper expansion plans for immersion-cooled halls. Nordic sites benefit from abundant hydroelectric power, reinforcing their allure for sustainably minded operators and underpinning diversification of the European data center GPU market footprint.

Competitive Landscape

NVIDIA dominates the Europe data center GPU market, leveraging its CUDA software moat alongside NVLink fabrics to entrench share. Blackwell-generation roadmaps promise industry-leading perf-per-watt, but sustained capacity constraints at TSMC invite buyers to hedge with AMD and Intel alternatives. AMD gains traction via MI300X deployments at CoreWeave and Lambda Labs, offering favorable cost-per-gigaflop metrics for inference and certain training tiers. Intel’s Gaudi 3 appeals to sovereign-cloud providers seeking diversification and open-standard software stacks.

Regional vendors carve niches by pairing accelerators with bespoke cooling, security, and orchestration services. Graphcore focuses on energy-efficient sparse inference, landing research contracts despite constrained scale. Submer, Atos, and local system integrators bundle immersion tanks, BullSequana chassis, and compliance wrappers to capture public-sector tenders. Colocation specialists such as Equinix and Digital Realty embed turnkey GPU pods into carrier-neutral campuses, shortening customer time-to-AI while spreading infrastructure risk across multi-tenant footprints.

Forward-looking competition centers on rack-level reference designs that integrate CPUs, GPUs, DPUs, and optical fabrics into modular blocks. Vendors tout power-reuse, waste-heat districting, and sovereign-cloud certifications as differentiators in bids. Market concentration remains high yet shows early signs of dilution as alternative accelerators mature, toolchains diversify, and buyers prioritize price-performance amid macroeconomic uncertainty. These dynamics keep the Europe data center GPU market vibrant, with incumbents innovating to protect share and challengers exploiting every supply-chain hiccup to gain footholds.

Europe Data Center GPU Industry Leaders

NVIDIA Corporation

Advanced Micro Devices Inc.

Intel Corporation

Samsung Electronics Co. Ltd. (HBM supply)

Graphcore Ltd.

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- March 2026: NVIDIA unveiled the GB300 Grace Blackwell Superchip, delivering 30 petaflops per rack for European hyperscale training fleets.

- February 2026: Amazon Web Services committed EUR 33.7 billion (USD 35.7 billion) to expand GPU capacity in Spain through 2033.

- January 2026: AMD introduced the MI325X inference accelerator with 288 GB HBM3e; first European installations occurred in France and Germany.

- December 2025: Google announced a EUR 5.5 billion (USD 5.83 billion) GPU and TPU build-out in Hanau and Frankfurt.

Europe Data Center GPU Market Report Scope

The Europe Data Center GPU Market Report is Segmented by Deployment Type (Cloud Data Centers, Enterprise/Private Data Centers, and Edge Data Centers), GPU Type (Training GPUs, and Inference GPUs), Interconnect (PCIe-Based GPUs and High-Bandwidth Interconnect GPUs), Workload Type (AI and ML, HPC, Data Analytics, and Graphics and Visualization), End-User (Hyperscalers/CSPs, Enterprises, and Government and Research), and Geography (Germany, United Kingdom, France, Italy, and Rest of Europe). The Market Forecasts are Provided in Value (USD).

| Cloud Data Centers |

| Enterprise / Private Data Centers |

| Edge Data Centers |

| Training GPUs |

| Inference GPUs |

| PCIe-Based GPUs |

| High-Bandwidth Interconnect GPUs |

| Artificial Intelligence (AI) and Machine Learning (ML) |

| High-Performance Computing (HPC) (non-AI scientific computing) |

| Data Analytics (database acceleration, query processing) |

| Graphics and Visualization (VDI, rendering, digital twins) |

| Hyperscalers / Cloud Service Providers |

| Enterprises |

| Government and Research Institutions |

| Germany |

| United Kingdom |

| France |

| Italy |

| Rest of Europe |

| By Deployment Type | Cloud Data Centers |

| Enterprise / Private Data Centers | |

| Edge Data Centers | |

| By GPU Type | Training GPUs |

| Inference GPUs | |

| By Interconnect | PCIe-Based GPUs |

| High-Bandwidth Interconnect GPUs | |

| By Workload Type | Artificial Intelligence (AI) and Machine Learning (ML) |

| High-Performance Computing (HPC) (non-AI scientific computing) | |

| Data Analytics (database acceleration, query processing) | |

| Graphics and Visualization (VDI, rendering, digital twins) | |

| By End-User | Hyperscalers / Cloud Service Providers |

| Enterprises | |

| Government and Research Institutions | |

| By Country | Germany |

| United Kingdom | |

| France | |

| Italy | |

| Rest of Europe |

Key Questions Answered in the Report

What is the current size of the Europe data center GPU market, and how fast is it growing?

The Europe data center GPU market size is projected at USD 10.62 billion in 2026 and is forecast to reach USD 19.42 billion by 2031, advancing at a 12.83% CAGR over 2026-2031.

Which deployment type is expanding the quickest across Europe?

Edge data centers are expected to outpace other deployment types with a 14.66% CAGR through 2031 as real-time inference shifts compute closer to users.

How are sovereign-cloud rules influencing GPU demand?

National data-residency mandates are propelling on-premises GPU investments by governments and regulated industries, lifting the public-sector segment at a 15.55% CAGR.

Which interconnect technology is gaining share in large training clusters?

High-bandwidth fabrics such as NVLink and Infinity Fabric are forecast to grow at a 15.21% CAGR, driven by their ability to efficiently synchronize thousands of GPUs.

Why are electricity prices a restraint for GPU expansion in some hubs?

Tariffs above EUR 0.28 per kWh in markets like Germany and the Netherlands inflate the total cost of ownership, prompting operators to add liquid-cooling and consider relocations to lower-cost Nordic regions.

Page last updated on: