France Data Center GPU Market Size and Share

Market Overview

| Study Period | 2021 - 2031 |

|---|---|

| Forecast Data Period | 2026 - 2031 |

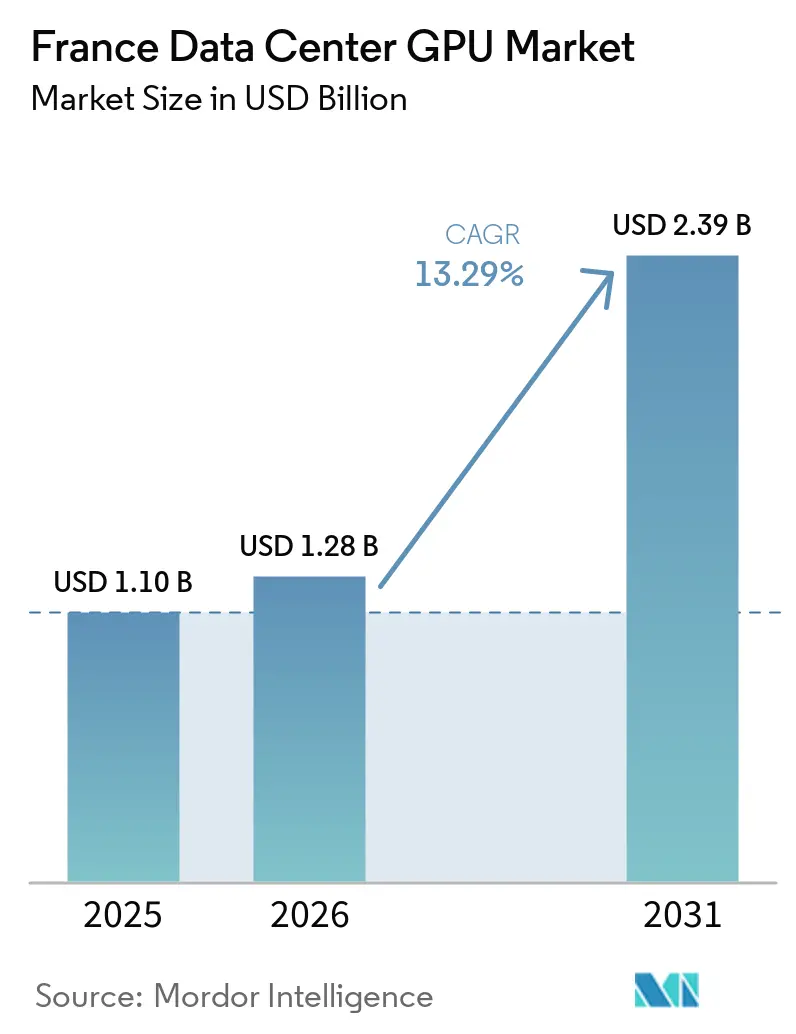

| Base Year Market Size (2025) | USD 1.10 Billion |

| Market Size (2026) | USD 1.28 Billion |

| Market Size (2031) | USD 2.39 Billion |

| Growth Rate (2026 - 2031) | 13.29% CAGR |

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

France Data Center GPU Market Analysis by Mordor Intelligence

The France Data Center GPU Market size is expected to increase from USD 1.10 billion in 2025 to USD 1.28 billion in 2026 and reach USD 2.39 billion by 2031, growing at a CAGR of 13.29% over 2026-2031. The expansion reflects a clear shift toward sovereign AI infrastructure in France, supported by large private investment commitments announced in early 2025 and by a power system that relies heavily on nuclear generation, which supports lower-carbon compute growth. Demand is broadening from a small base of training-heavy deployments toward a wider mix of production inference, graphics rendering, simulation, and analytics workloads, which is making capacity planning more diverse across the France Data Center GPU Market. Compliance needs are also shaping buyer decisions, because French and wider European rules on data residency, resilience, and cybersecurity make local hosting more attractive for regulated users. Competition is becoming sharper as domestic providers widen accelerator options, hyperscalers add capacity, and edge operators target low-latency deployments in secondary cities. Growth still depends on how quickly operators can manage electricity volatility, cooling retrofits for higher-wattage accelerators, and dependence on external advanced packaging supply chains.

Key Report Takeaways

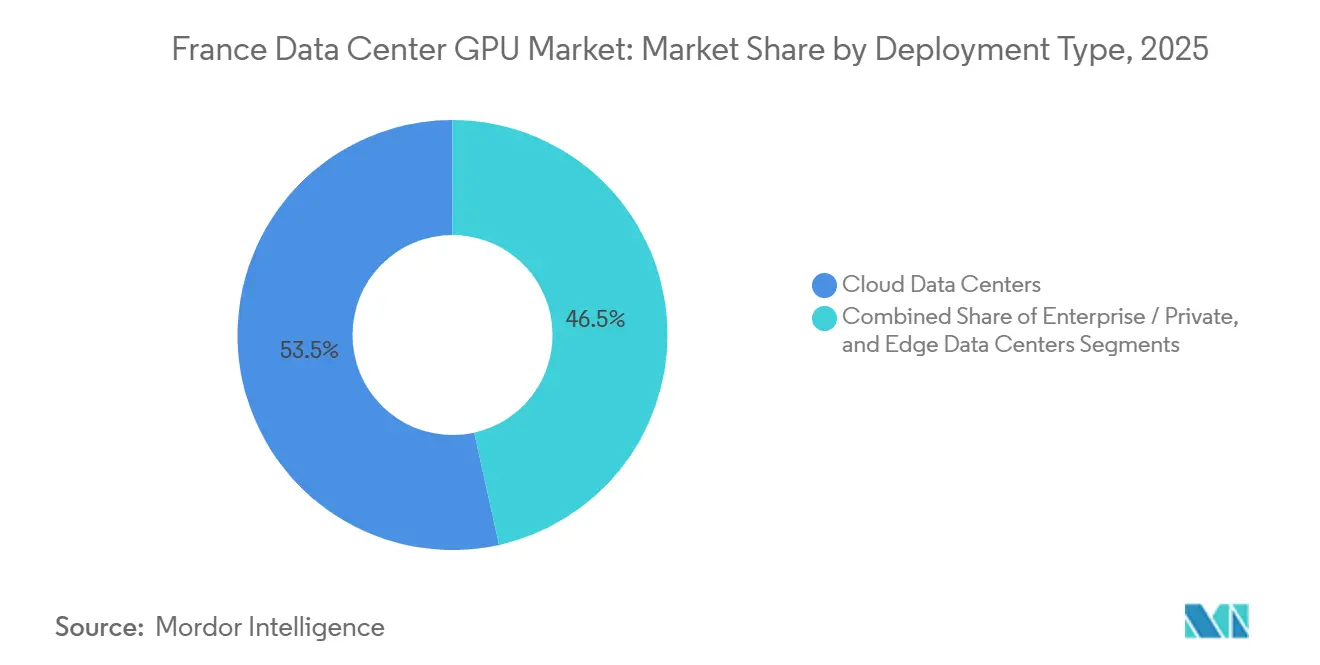

- By deployment type, cloud data centers held 53.47% of deployment-type revenue in 2025, while edge data centers are projected to expand at 14.90% CAGR through 2031.

- By GPU type, training GPUs accounted for 57.83% of segment revenue in 2025, while inference GPUs are expected to record the strongest growth at 14.04% CAGR through 2031.

- By interconnect, PCIe-based GPUs captured 71.29% of interconnect revenue in 2025, while high-bandwidth interconnect GPUs are projected to grow fastest at 15.90% CAGR through 2031.

- By workload type, AI and ML represented 54.62% of segment revenue in 2025, while graphics and visualization applications are expected to expand fastest at 15.46% CAGR through 2031.

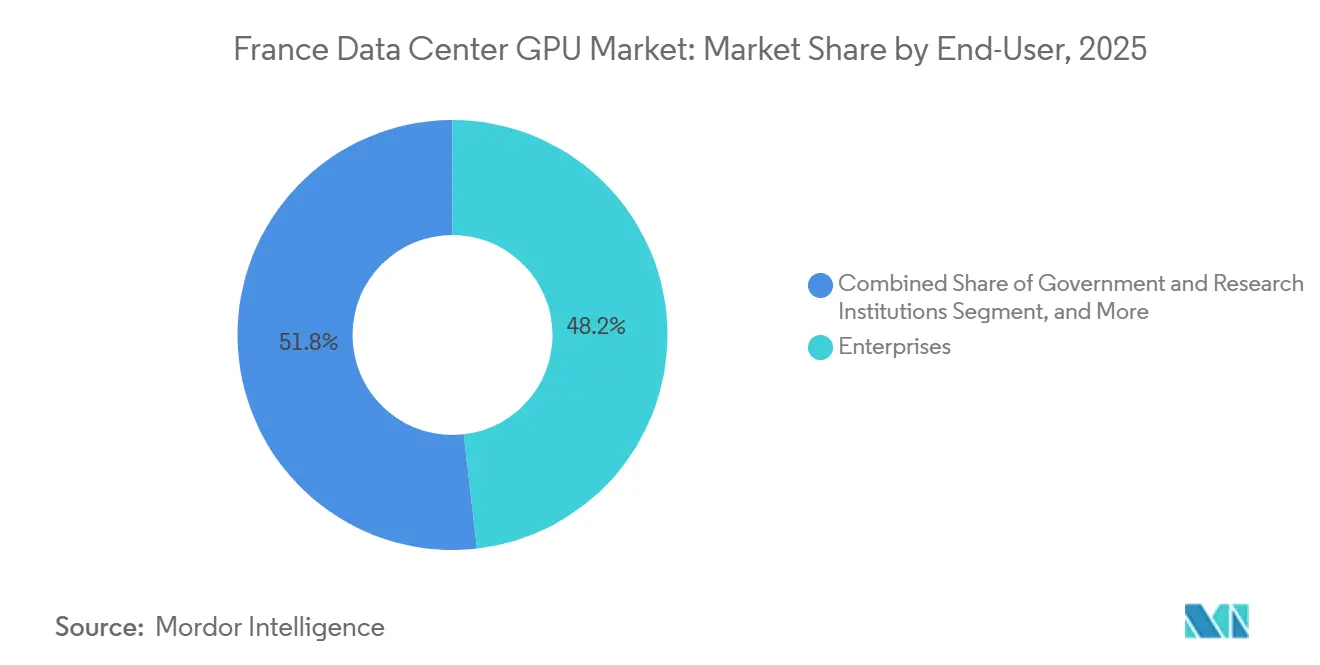

- By end-user, enterprises held 48.19% of spending in 2025 in the France Data Center GPU Market, while hyperscalers and cloud service providers are expected to add the largest absolute capacity at 15.92% CAGR through 2031.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of January 2026.

France Data Center GPU Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Surging Adoption of Generative AI Workloads | +4.2% | National, concentrated in Paris, Grenoble, Lyon, Marseille | Short term (≤ 2 years) |

| Rapid Expansion of France-Based Hyperscale Facilities | +3.8% | National, with major deployments in Île-de-France, Auvergne-Rhône-Alpes, Provence-Alpes-Côte d'Azur | Medium term (2-4 years) |

| Government Tax Incentives for Green Data Centers | +2.1% | National, early gains in regions meeting PUE and heat-recovery thresholds | Medium term (2-4 years) |

| Falling Total Cost of Ownership of GPU-Accelerated Servers | +1.9% | National, benefiting cloud providers and large enterprises | Long term (≥ 4 years) |

| Growth of Sovereign-Cloud Compliance Mandates | +1.3% | National, with spillover to EU member states adopting SecNumCloud-equivalent frameworks | Medium term (2-4 years) |

| Emergence of Small-Scale Modular Edge Data Centers | +1.1% | National, regional deployments in Bordeaux, Lyon, Strasbourg, Lille, Nantes | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

Surging Adoption of Generative AI Workloads

Generative AI is moving GPU procurement in France from pilot projects into sustained infrastructure planning, because enterprises and research organizations now need dense compute for both model development and production serving. The strongest demand comes from regulated use cases in banking, insurance, healthcare, defense, and telecommunications, where data locality and auditable processing matter as much as raw benchmark speed. This is pushing the France Data Center GPU Market toward a premium sovereign tier in which operators can charge more for local control, tighter service, and clearer compliance support. The demand profile is also widening because many organizations now deploy a larger number of smaller models in production instead of relying only on a few large training runs. SITEC’s AI hosting platform in Corsica shows how local infrastructure is being positioned for regional experimentation, flexible GPU profiles, and direct technical support under public digital-innovation programs.[1]SITEC, “Une Infrastructure D'hébergement Dédiée À L'intelligence Artificielle,” SITEC, sitec.corsica As these workloads move closer to operations teams and business units, the France Data Center GPU Market benefits from steadier utilization, more repeat buying, and stronger interest in regional inference capacity.

Rapid Expansion of France-Based Hyperscale Facilities

The build-out of large campuses is increasing the physical base on which the France Data Center GPU Market can grow over the rest of the decade. Data4 raised planned investment in its PAR03 campus in Nozay from EUR 1 billion (USD 2.26 billion) to EUR 2 billion (USD 2.26 billion), lifted the site to 250 MW, and designed it to host around 200,000 GPUs, which signals how large planned clusters are becoming in France. The company also plans to interconnect PAR03 with its existing Marcoussis campus, creating a larger digital corridor that strengthens the Paris-Saclay area as a gravity center for AI capacity. Outside the capital region, Iliad and OpCore committed EUR 2.5 billion (USD 2.83 billion) to a 700 MW site in Montereau with EDF, while other operators are planning large projects in Bordeaux and other secondary locations. More capacity at this scale improves equipment allocation, shortens wait times for large customers, and helps the France Data Center GPU Market support both sovereign AI projects and commercial cloud demand at the same time. It also creates room for more specialized services, because once core power and networking are available, operators can differentiate on cooling design, certification, and managed AI tooling rather than on land access alone.

Government Tax Incentives for Green Data Centers

Energy and environmental rules are becoming a direct growth factor because France is rewarding facilities that combine high density with better thermal and reporting performance. France’s DDADUE framework, which implemented the EU Energy Efficiency Directive, requires energy reporting for data centers above 500 kW and heat-recovery obligations for sites above 1 MW, which favors newer GPU-oriented sites that plan efficiency measures from the start. These rules encourage liquid cooling, heat reuse, and tighter operational monitoring, which lowers the risk that new GPU capacity will face expensive redesigns later. Data4’s PAR03 campus includes waste-heat reuse for a nearby eco-district, which shows how compliance, local approvals, and community acceptance can reinforce each other when projects are designed early for environmental performance. Sesterce’s Valence facility follows a similar direction with closed-loop water cooling and planned waste-heat recovery for adjacent industrial users, which aligns the project with regional development goals. Public support for upgrades such as Jean Zay also shows that the France Data Center GPU Market is being shaped not only by more servers, but by a policy preference for efficient high-density infrastructure with measurable reuse of energy.

Falling Total Cost of Ownership of GPU-Accelerated Servers

Lower hourly cloud pricing, more product choice, and flexible consumption models are reducing the entry barrier for users who could not justify GPU capacity a few years ago. Scaleway priced H100 PCIe instances at EUR 2.73 (USD 3.09) per hour by mid-2025, while L40S and L4 instances reached EUR 1.40 (USD 1.58) and EUR 0.75 (USD 0.85) per hour, which made on-demand inference and burst capacity more practical for startups and mid-sized enterprises.[2]Scaleway, “Scaleway and Lepton AI DGX Cloud,” Scaleway, scaleway.comOVHcloud also widened the price ladder with L4 instances starting at GBP 834 (USD 1,043) per month and L40S at GBP 2,555 (USD 3,197), which helped local buyers compare more cost-focused domestic options against global clouds. Dell France’s listed pricing for L4, L40S, and H100 accelerators in early 2026 suggests that acquisition costs have become more transparent and more stable after the earlier supply squeeze. AMD’s June 2025 positioning of the Instinct MI350 Series around stronger tokens-per-dollar economics, together with Lenovo’s TruScale model that shifts spending from capital to operating expense, is widening the addressable customer base for the France Data Center GPU Market.[3] Lenovo, “TruScale,” Lenovo, lenovo.com As cost discipline improves, buyers who once treated accelerators as exceptional purchases are beginning to view them as a normal part of IT and data-center planning.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Persistently High Electricity Prices in France | -1.8% | National, acute in regions without direct nuclear or renewable contracts | Short term (≤ 2 years) |

| Limited Domestic Supply Chain for Advanced Packaging | -1.5% | National, with dependency on Taiwan, South Korea, Japan for HBM and CoWoS | Long term (≥ 4 years) |

| Data-Localization Rules Slowing Cross-Border Cloud Growth | -0.9% | National, affecting multinational enterprises with pan-European operations | Medium term (2-4 years) |

| Cooling Infrastructure Bottlenecks for >700 W GPUs | -0.7% | National, concentrated in legacy facilities lacking liquid-cooling retrofits | Medium term (2-4 years) |

| Source: Mordor Intelligence | |||

Persistently High Electricity Prices in France

Electricity remains a real constraint for the France Data Center GPU Market because GPU clusters convert high utilization directly into large recurring energy bills. The end of the ARENH regulated-access mechanism in 2025 reduced price certainty for operators that do not have long-term contracts or strong negotiating leverage, which makes financial planning harder for new projects. This pressure is strongest for independent colocation providers, private enterprise sites, and regional facilities that cannot spread risk across very large estates. Higher rack densities also compound the issue, because power costs rise together with cooling requirements once operators move into the newest accelerator generations. Large campuses and sovereign projects are better placed to negotiate favorable terms or absorb temporary volatility, which creates a gap between very large buyers and smaller participants in the France Data Center GPU Market. If power pricing remains unstable, some capacity will still be built, but more buyers will favor hybrid use models and staged deployments rather than large immediate rollouts.

Limited Domestic Supply Chain for Advanced Packaging

France has meaningful research capability in advanced semiconductor integration, but it still lacks high-volume local capacity for the packaging technologies that matter most to high-end GPUs. CEA-Leti’s FAMES platform in Grenoble supports fan-out wafer-level packaging and chiplet integration, and the institute is also involved in the APECS pilot line for advanced assembly, but both efforts remain oriented toward process development rather than mass production. That means French operators still depend on overseas ecosystems for high-bandwidth memory stacking and other complex package steps that determine performance, power efficiency, and delivery schedules. The Alice Recoque system illustrates this dependence because it relies on AMD Instinct MI430X accelerators with 432 GB HBM4 and 19.6 TB/s bandwidth, yet the packaging base behind such products is not onshore in France. This slows the sovereign ambition of the France Data Center GPU Market, because system integration can be French while the most constrained parts of the bill of materials remain external. Until pilot programs become industrial production, French buyers will continue to face longer lead times, allocation risk, and weaker bargaining power during global supply tightness.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Deployment Type: Edge Expands Alongside Cloud Scale

Cloud data centers commanded 53.47% of deployment-type revenue in 2025, and they remain the main commercial base of the France Data Center GPU Market because multi-tenant utilization supports better hardware absorption, stronger pricing flexibility, and faster refresh cycles, while edge data centers are projected to expand at 14.90% CAGR through 2031. Large campuses can combine dense power, liquid cooling, and managed software layers in ways that enterprise sites often struggle to replicate at the same speed. Data4’s PAR03 project shows the scale advantage clearly, because the company designed the Nozay campus for 250 MW and around 200,000 GPUs after doubling its investment plan to EUR 2 billion (USD 2.26 billion). Scaleway’s managed H100 offering and OVHcloud’s widening portfolio of L4, L40S, and H100 instances also show why cloud operators can serve a broad buyer base that ranges from startups to regulated enterprises with variable demand. This model keeps the France Data Center GPU Market anchored in large shared facilities even as workload diversity increases.

Edge data centers are projected to grow fastest through 2031 because inference, industrial analytics, and graphics-heavy use cases often need proximity that centralized campuses cannot always deliver at acceptable latency. UltraEdge’s Datapoles program committed EUR 400 million (USD 452 million) and 51 MW across 9 regional sites, including Bordeaux, Lyon, Strasbourg, Lille, and Nantes, to support sub-10-millisecond processing for automotive, industrial IoT, and real-time video workloads. Standardized modular builds also shorten delivery times, which makes regional supply more responsive to actual demand. Enterprise and private data centers still matter where users want direct control, stable utilization, and no cloud egress costs, and server vendors such as Dell and Lenovo now support both owned and consumption-based GPU estates for that reason. The result is a France data center GPU industry that is not moving toward a single deployment model, but toward a layered structure in which cloud scale, edge responsiveness, and private sovereignty each solve a different operating problem.

By GPU Type: Inference Demand Broadens the Installed Base

Training GPUs accounted for 57.83% share of the France Data Center GPU Market size in 2025 because large model development and scientific simulation still require expensive, high-memory accelerators deployed in dense clusters, while inference GPUs are expected to record the strongest growth at 14.04% CAGR through 2031. That spending pattern is reinforced by sovereign AI ambitions, because organizations that want domestic control over model training must commit upfront capital to powerful hardware and supporting infrastructure. Training clusters also tend to pull in higher networking and cooling spend, which raises their revenue weight relative to smaller inference deployments. At the same time, the demand profile is widening because cloud providers now offer a broader set of lower-power accelerators for production use. Scaleway’s pricing for H100, L40S, and L4 instances, along with OVHcloud’s portfolio of monthly GPU options, shows how buyers can now match accelerator choice more closely to serving, fine-tuning, and mixed enterprise workloads.

Inference GPUs are projected to grow fastest through 2031 because enterprises are shifting from isolated experimentation toward live deployment across customer service, fraud detection, recommendation, and document automation. This part of the France Data Center GPU Market benefits from better power efficiency, lower hourly pricing, and the fact that many production models do not need the most expensive training silicon. AMD’s June 2025 positioning of the Instinct MI350 Series around stronger tokens-per-dollar economics adds more pressure to inference pricing and widens the available supplier set. Training GPUs still remain essential for national compute capability, as shown by Alice Recoque and the Jean Zay upgrade, which both support advanced research and high-end AI workloads at sovereign sites. The France data center GPU industry is therefore entering a phase in which training keeps technical prestige and high ticket sizes, while inference delivers the broader and steadier deployment curve.

By Interconnect: High-Bandwidth Fabrics Gain Strategic Importance

PCIe-based GPUs held 71.29% of the France Data Center GPU Market share within interconnect revenue in 2025 because they remain the most practical choice for enterprise servers, many cloud instances, and distributed edge nodes where inter-accelerator traffic is limited, while high-bandwidth interconnect GPUs are projected to grow fastest at 15.90% CAGR through 2031. They are easier to deploy, easier to replace, and better aligned with the familiar server formats that a large part of the installed base already uses. Dell and other server vendors continue to support broad PCIe deployment paths, which keep this segment commercially relevant across private infrastructure and general cloud offerings. Scaleway’s H100 PCIe instances also show that strong performance can still be delivered in formats that do not require the full complexity of tightly coupled fabrics for every workload. This keeps PCIe as the volume base of the France Data Center GPU Market, even while more advanced cluster architectures expand.

High-bandwidth interconnect GPUs are projected to grow fastest through 2031 because large-scale training and multi-node inference need low-latency communication that PCIe alone cannot provide at the same level. GENCI’s Dalia system, which brought Europe’s first GB200 NVL72 configuration to IDRIS, illustrates how tightly integrated GPU-CPU memory and networking are becoming central to frontier AI and HPC deployments. Eviden’s Alice Recoque platform also highlights this shift through its BullSequana XH3500 design, BXI v3 interconnect, and direct liquid cooling, all of which are meant to improve cluster density and efficiency together. The challenge is cost, because high-bandwidth fabrics increase switching, adapter, and integration expenses, which limits them to buyers with very large budgets or strategic national backing. AMD’s support for more open interconnect development suggests that the cost barrier could ease over time, but the France Data Center GPU Market still operates as a two-tier structure in which PCIe serves general deployment while premium fabrics support frontier clusters.

By Workload Type: AI Stays Largest While Graphics Rises Fast

AI and ML captured 54.62% share of the France Data Center GPU Market size in 2025 because the strongest buying interest still comes from foundation-model training, fine-tuning, and production inference across regulated and data-rich sectors, while graphics and visualization applications are expected to expand fastest at 15.46% CAGR through 2031. Cloud providers and regional operators are both serving this demand, which means the installed base is no longer limited to one type of site or one class of customer. SITEC’s regional AI platform, together with managed H100 environments from Scaleway and broader GPU access from OVHcloud, shows how AI workloads now span local experimentation, commercial deployment, and national-scale research. HPC for non-AI research remains important, especially where numerical precision and memory bandwidth matter more than serving efficiency, which is why Alice Recoque still stands out as a strategic public investment. Data analytics also benefits from GPU parallelism, but its spending footprint remains smaller than the AI-led category at this stage.

Graphics and visualization applications are projected to expand fastest through 2031 because digital twins, virtual workstations, media rendering, and simulation are moving into more routine enterprise use. This demand is especially relevant in France, where aerospace, automotive, industrial engineering, and design-intensive sectors already use advanced simulation and visualization in core workflows. NVIDIA’s L4 platform is well positioned for virtual desktop and video-rich environments because it combines low idle power with video acceleration and practical deployment characteristics for shared infrastructure. Cloud access matters here as well, because providers can supply burst rendering and visualization capacity during project peaks without forcing users into permanent high capital spending. As AI-generated content and neural rendering become more common, the boundary between graphics and AI will keep narrowing, which supports broader accelerator demand across the France Data Center GPU Market.

By End-User: Enterprises Lead Spending While Public Projects Shape Capability

Enterprises represented 48.19% of end-user spending in 2025, which shows that the France Data Center GPU Market is not driven only by hyperscalers or public labs, but also by commercial buyers that want direct control over mission-critical compute, while hyperscalers and cloud service providers are expected to add the largest absolute capacity at 15.92% CAGR through 2031.. Manufacturers, pharmaceutical companies, banks, insurers, and telecom operators often prefer owned or tightly governed environments because these reduce latency, simplify data handling, and avoid repeated transfer charges. Dell’s PowerEdge XE9680 and related enterprise systems show how server vendors are packaging dense GPU capacity for buyers who want on-premises or hybrid deployment paths. Lenovo’s TruScale model adds another route by allowing organizations to scale GPU use without large upfront hardware purchases, which is particularly useful for mid-market users with uneven demand. This combination of ownership and flexible consumption keeps enterprises at the center of demand in the France Data Center GPU Market.

Hyperscalers and cloud service providers are expected to add the largest absolute capacity through 2031 because they can absorb bigger clusters, spread utilization across many customers, and package hardware with managed AI services. Scaleway’s DGX Cloud partnership with Lepton AI is one example of how cloud platforms are moving beyond raw instance sales toward model deployment, monitoring, and operational simplification. Government and research institutions remain smaller in revenue share, but they shape technical standards and national capability through projects such as Dalia, Jean Zay, and Alice Recoque, which anchor frontier AI and HPC capacity on French soil. The end-user mix therefore remains balanced, with enterprises driving immediate commercial demand, hyperscalers supplying scale, and public institutions securing long-term sovereign capability for the France Data Center GPU Market.

Geography Analysis

Paris-region projects held the dominant position in announced high-density investment in 2025 and 2026, which makes Île-de-France the operational core of the France Data Center GPU Market. This lead comes from a dense concentration of cloud nodes, enterprise customers, public institutions, and network interconnection points that simplify large AI campus development. Data4’s PAR03 project in Nozay is central to that lead, because the site was designed for 250 MW and around 200,000 GPUs after the company doubled its planned investment to EUR 2 billion (USD 2.26 billion). The planned link between Nozay and Marcoussis also gives the Paris-Saclay corridor an unusual scale for a national AI hub. This concentration keeps Paris attractive for the largest clusters, even as land, cooling, and connection constraints encourage some expansion elsewhere.

Auvergne-Rhône-Alpes is emerging as the strongest secondary zone in the France Data Center GPU Market because it combines semiconductor research, HPC assets, and new commercial capacity. Grenoble strengthens the region through CEA-Leti’s advanced packaging platform, while Valence adds commercial momentum through Sesterce’s planned EUR 450 million (USD 509 million) AI data center with 40,000 GPUs. France 3 Régions also highlighted the project’s closed-loop cooling and heat-recovery orientation, which supports the region’s appeal for efficient high-density sites. Provence-Alpes-Côte d'Azur and western secondary cities are also gaining relevance as connectivity, land availability, and regional compute demand support new deployments.

Regional diversification is now a defining feature of the France Data Center GPU Market because not every AI workload needs to sit near the capital if latency, data residence, or power access are better elsewhere. UltraEdge’s Datapoles program spread 51 MW across 9 sites in Bordeaux, Lyon, Strasbourg, Lille, and Nantes, which shows that edge and regional inference demand is becoming commercially meaningful. Corsica also entered the picture through SITEC’s NVIDIA H100 NVL infrastructure under the EDIH Corsica.ai initiative, which proves that even peripheral regions can attract advanced AI capacity when public programs and local support align. As projects spread, the competitive map is shifting from a single-center model to a network model in which Paris dominates frontier scale and other regions capture specialized or latency-sensitive growth.

Competitive Landscape

The France Data Center GPU Market remains moderately concentrated because a limited number of large cloud platforms and NVIDIA-based hardware stacks influence the biggest deployments, yet domestic providers still hold meaningful strategic ground in sovereign and compliance-led use cases. NVIDIA hardware continues to anchor much of the deployed ecosystem through H100, L40S, L4, and newer Blackwell-related platforms, which keeps software compatibility and ecosystem maturity on its side. At the same time, AMD has secured visible strategic ground through Alice Recoque, where its Instinct MI430X accelerators were selected for France’s first exascale supercomputer. This matters because it gives public-sector buyers a credible alternative at the top end of the performance spectrum. The state’s April 2026 acquisition of Atos’s Advanced Computing assets, rebranded Bull, also shows that France wants domestic systems integration and supercomputer manufacturing capability to remain part of the national stack.

Strategic partnerships are becoming one of the clearest ways companies are differentiating themselves in the France Data Center GPU Market. OVHcloud partnered with SambaNova Systems in early 2025 to offer RDU accelerators alongside NVIDIA L4, L40S, and H100 instances, which broadened customer choice beyond a pure GPU portfolio. Scaleway then expanded its managed offer in June 2025 through a DGX Cloud partnership with Lepton AI, combining H100 clusters with deployment and monitoring tools that are attractive to AI-native startups and fast-growing application teams. Cerebras also expanded in Europe in late 2025 and positioned wafer-scale systems as an alternative path for inference-heavy applications, which adds more architectural variety to a field still dominated by GPU thinking. These moves show that competition is no longer only about hardware volume, but also about who can package the right operating model around it.

There is still significant room for challengers in edge inference, sovereign hosting, and specialized cluster integration. UltraEdge is pursuing that opening with regional deployments, while local providers such as OVHcloud, Scaleway, and Orange Business Services can compete where certification, French support, and residency requirements matter more than pure global scale. Technology differentiation is also becoming sharper, because Eviden’s BXI v3 interconnect and AMD’s push for more open fabric approaches both address cost and efficiency concerns that large buyers now treat as strategic. That leaves the France Data Center GPU Market in a competitive position where scale still matters, but where regulation, architecture choice, and service design continue to create room for more than a handful of winners.

France Data Center GPU Industry Leaders

Nvidia Corporation

Advanced Micro Devices, Inc.

Intel Corporation

Graphcore Limited

Huawei Technologies Co., Ltd.

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- April 2026: France completed the acquisition of Atos's Advanced Computing assets, rebranded Bull, for up to EUR 404 million (USD 468 million), preserving the Angers supercomputer manufacturing plant as Europe's sole production facility and ensuring domestic systems-integration expertise for exascale and AI-factory projects. The transaction excludes zData and Vision AI units, focusing on high-performance computing, quantum, and business-computing divisions that generated approximately EUR 700 million (USD 810 million) revenue in FY2025.

- February 2026: Nebius announced plans to expand its France site, with B300, GB300, and Vera Rubin NVL72 deployments planned for 2026, positioning the company to serve European sovereign-cloud demand with next-generation NVIDIA architectures.

- November 2025: GENCI and NVIDIA announced Dalia, Europe's first GB200 NVL72 system, pairing 72 NVIDIA Blackwell GPUs with 36 Grace CPUs in a rack-scale architecture, operational at IDRIS and demonstrating tightly coupled GPU-CPU memory coherence for AI and HPC workloads.

France Data Center GPU Market Report Scope

Data Center GPU refers to a specialized graphics processing unit engineered for large-scale computing environments, such as enterprise data centers and cloud platforms, rather than for personal computers or gaming.

The France Data Center GPU Market Report is Segmented by Deployment Type (Cloud Data Centers, Enterprise/Private Data Centers, and Edge Data Centers), GPU Type (Training GPUs, Inference GPUs), Interconnect (PCIe-Based GPUs, and High-Bandwidth Interconnect GPUs), Workload Type (Artificial Intelligence (AI) and Machine Learning (ML), High-Performance Computing (HPC) (non-AI scientific computing), Data Analytics (database acceleration, query processing), and Graphics and Visualization (VDI, rendering, digital twins)), and End-User (Hyperscalers/Cloud Service Providers, Enterprises, and Government and Research Institutions). The Market Forecasts are Provided in Terms of Value (USD).

| Cloud Data Centers |

| Enterprise / Private Data Centers |

| Edge Data Centers |

| Training GPUs |

| Inference GPUs |

| PCIe-Based GPUs |

| High-Bandwidth Interconnect GPUs |

| Artificial Intelligence (AI) and Machine Learning (ML) |

| High-Performance Computing (HPC) (non-AI scientific computing) |

| Data Analytics (database acceleration, query processing) |

| Graphics and Visualization (VDI, rendering, digital twins) |

| Hyperscalers / Cloud Service Providers |

| Enterprises |

| Government and Research Institutions |

| By Deployment Type | Cloud Data Centers |

| Enterprise / Private Data Centers | |

| Edge Data Centers | |

| By GPU Type | Training GPUs |

| Inference GPUs | |

| By Interconnect | PCIe-Based GPUs |

| High-Bandwidth Interconnect GPUs | |

| By Workload Type | Artificial Intelligence (AI) and Machine Learning (ML) |

| High-Performance Computing (HPC) (non-AI scientific computing) | |

| Data Analytics (database acceleration, query processing) | |

| Graphics and Visualization (VDI, rendering, digital twins) | |

| By End-User | Hyperscalers / Cloud Service Providers |

| Enterprises | |

| Government and Research Institutions |

Key Questions Answered in the Report

What is the current size of the France data center GPU market?

The France Data Center GPU Market stood at USD 1.28 billion in 2026 and is forecast to reach USD 2.39 billion by 2031, growing at a 13.29% CAGR over 2026-2031.

What is driving GPU demand in French data centers?

The main drivers are sovereign AI infrastructure build-out, wider generative AI adoption, hyperscale campus expansion, and lower operating barriers from better pricing and service models.

Which deployment model leads spending in France?

Cloud data centers led deployment revenue with 53.47% in 2025, supported by scale, multi-tenant utilization, and stronger managed service capability.

Why are edge facilities gaining traction across France?

Edge sites are growing faster because inference, industrial analytics, and real-time graphics workloads often need local processing, lower latency, and stronger regional data control.

Which workload category is the largest in French GPU data centers?

AI and ML was the largest workload group in 2025 with 54.62% of segment revenue, reflecting strong demand for model training, fine-tuning, and production inference.

Who are the main buyers of GPU capacity in France?

Enterprises led end-user spending with 48.19% in 2025, while hyperscalers and cloud providers are expected to add the largest absolute capacity over the forecast period.

Page last updated on: