India Data Center GPU Market Size and Share

Market Overview

| Study Period | 2021 - 2031 |

|---|---|

| Forecast Data Period | 2026 - 2031 |

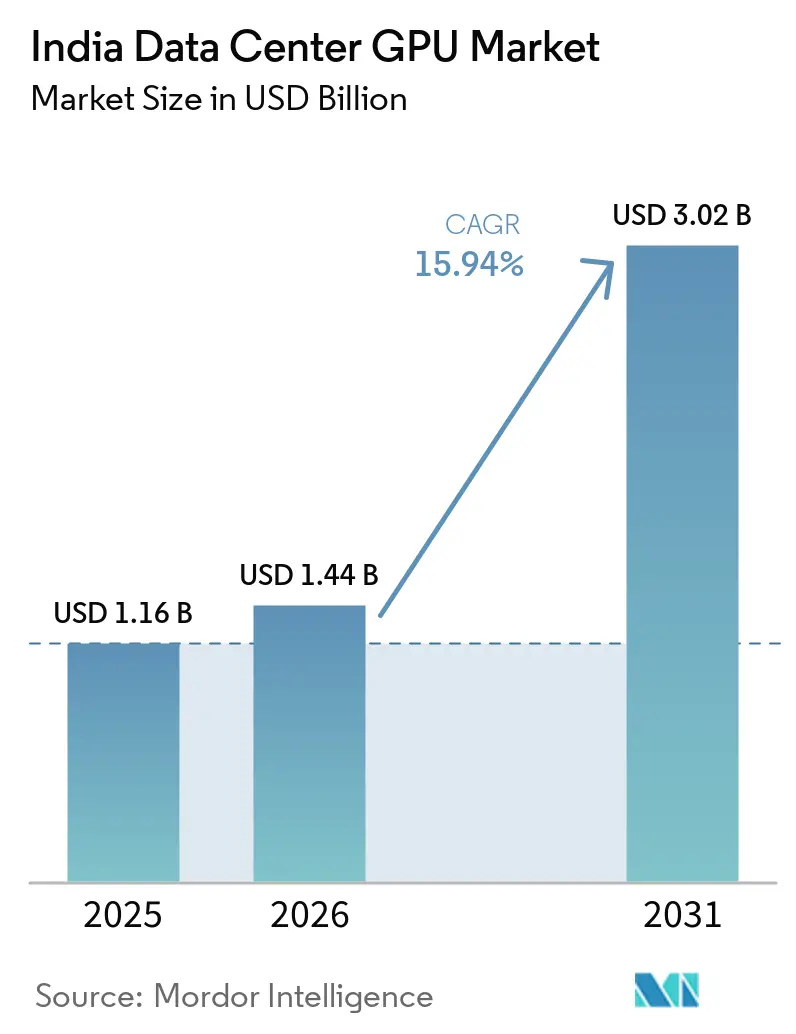

| Base Year Market Size (2025) | USD 1.16 Billion |

| Market Size (2026) | USD 1.44 Billion |

| Market Size (2031) | USD 3.02 Billion |

| Growth Rate (2026 - 2031) | 15.94% CAGR |

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

India Data Center GPU Market Analysis by Mordor Intelligence

The India data center GPU market size is expected to increase from USD 1.16 billion in 2025 to USD 1.44 billion in 2026 and reach USD 3.02 billion by 2031, growing at a CAGR of 15.94% over 2026-2031. Sovereign AI mandates, heavy hyperscale capital outlays, and fast-spreading 5G edge nodes collectively place India on the short list of global destinations where demand for accelerated computing outstrips worldwide supply. Government subsidies that cut hourly GPU pricing by nearly 70%, together with data-localization rules that block offshore processing of regulated workloads, have turned on-premise and colocation clusters into strategic assets rather than cost centers. The growing pool of AI-native startups, already topping 1,700 firms, is reinforcing utilization rates above 80% across facilities in Mumbai, Bangalore, and Hyderabad. Meanwhile, supply-chain constraints on advanced packaging and high-bandwidth memory remain the single biggest operational risk for operators planning to triple their installed GPU base before 2031.

Key Report Takeaways

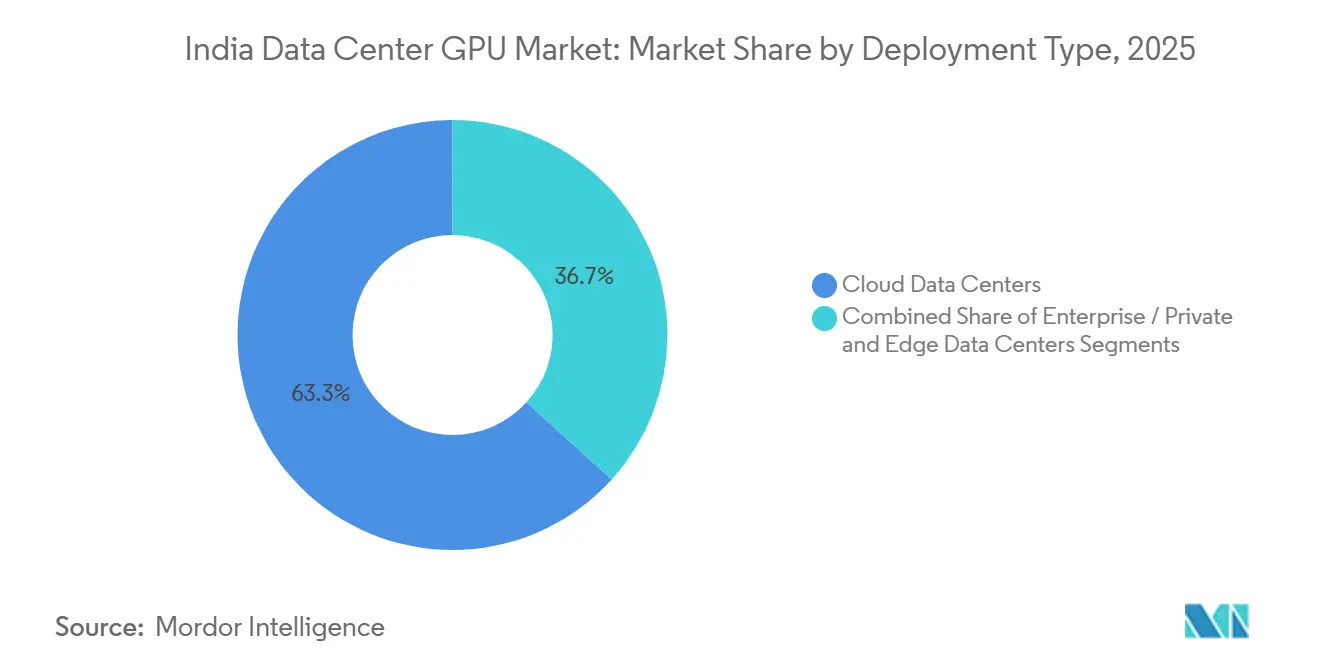

- By deployment type, cloud data centers led with 63.28% of the India data center GPU market share in 2025, while edge data centers were identified as the fastest-growing segment through at 16.94% CAGR through 2031.

- By GPU type, inference accelerators commanded 58.37% of the India data center GPU market size in 2025, whereas training GPUs are registering the highest growth at 17.45% CAGR through 2031 momentum across the forecast window.

- By interconnect, PCIe-based devices accounted for 74.63% of the India data center GPU market size in 2025, and high-bandwidth interconnect GPUs are expected to post the quickest expansion as larger language models become commonplace at 16.89% CAGR through 2031.

- By workload, AI and machine learning workloads captured 67.94% of the India data center GPU market share in 2025, with data analytics overtaking all other use cases as the fastest climber at 17.58% CAGR through 2031.

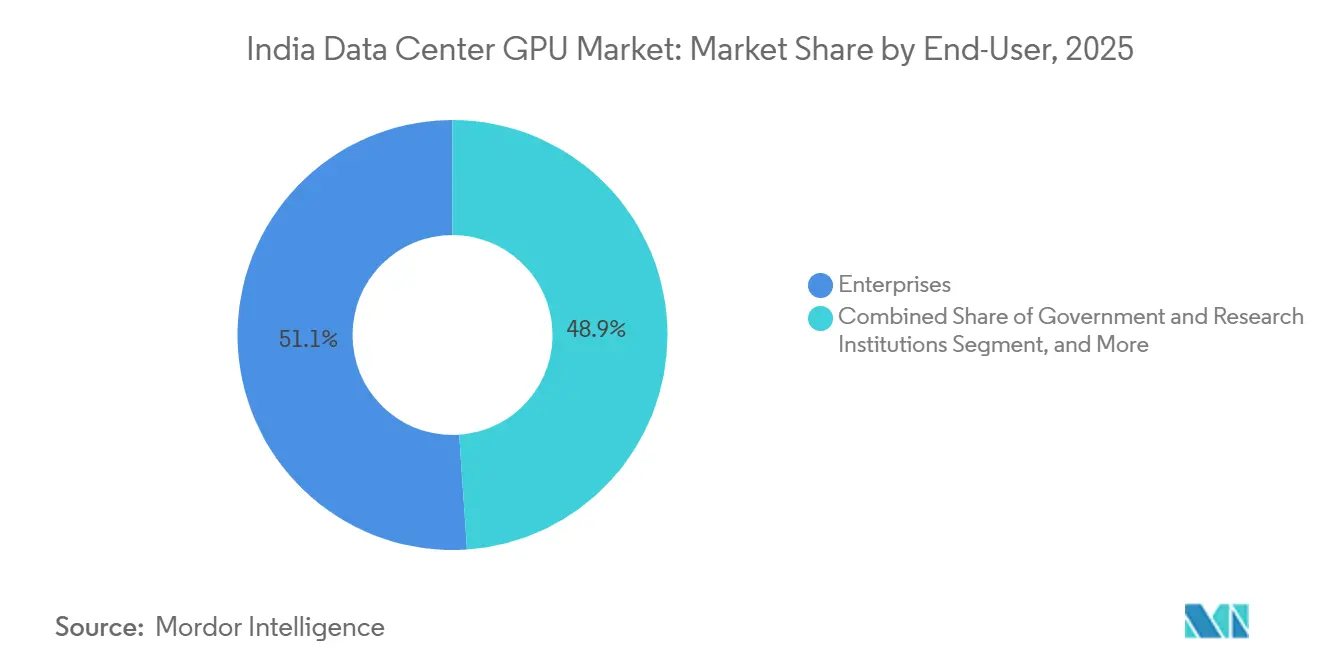

- By end-user, enterprises represented 51.08% of spending in 2025, while hyperscalers remain the fastest-expanding customer group at 17.02% CAGR through 2031.as they continue multibillion-dollar build-outs across India.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of January 2026.

India Data Center GPU Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Rapid Expansion of Hyperscale Cloud Regions | +4.2% | National, concentrated in West India (Mumbai, Pune) and South India (Bangalore, Chennai, Hyderabad) | Medium term (2-4 years) |

| Government Incentives Under Digital India and Data Localization Norms | +3.8% | National, with early adoption in government and BFSI sectors | Short term (≤ 2 years) |

| Rising AI Startup Ecosystem Demand for GPU-Accelerated Compute | +2.9% | National, concentrated in Bangalore, Hyderabad, Delhi-NCR startup hubs | Medium term (2-4 years) |

| Surge in Video Streaming, Gaming and AR/VR Requiring GPU-Based Transcoding and Rendering | +1.7% | National, with higher penetration in urban centers | Long term (≥ 4 years) |

| Deployment of 5G and Edge Computing Driving Micro Data Centers With GPUs | +1.5% | National, led by telecom operators in metro and Tier-1 cities | Medium term (2-4 years) |

| Declining Cost per TFLOP of Data Center GPUs Enabling Broader Adoption | +1.3% | National, benefiting SMEs and mid-market enterprises | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

Rapid Expansion of Hyperscale Cloud Regions in India

Unprecedented capital expenditure by Amazon Web Services, Google Cloud, Microsoft, and Oracle is compressing build cycles for new capacity to under 24 months, ensuring that aggregate GPU inventory in the India data center GPU market will more than double before 2028.[3]Yotta Infrastructure, “H100 Supercomputing Cluster Fact Sheet,” yottainfra.com AWS alone earmarked USD 7 billion for Hyderabad, while Google’s USD 15 billion Visakhapatnam region is pairing subsea cable landings with H100 clusters to serve multilingual inference workloads. This wave of investment shortens round-trip latency for Indian SaaS providers from 200-300 milliseconds to sub-50 milliseconds, a gain that directly raises customer conversion rates for recommendation engines. Job creation programs attached to these investments aim to certify 100,000 AI developers, reinforcing a virtuous cycle where a larger talent pool drives higher GPU utilization. Hyperscalers’ purchasing scale also secures early allocations from NVIDIA and AMD, shielding the domestic supply stack from global shortages.

Government Incentives Under Digital India and Data Localization Norms

The INR 10,372 crore (USD 1.24 billion) IndiaAI Mission reserves 38,000 GPUs for subsidized usage at INR 65 per hour, lowering the economic barrier for prototype training runs by 70% relative to retail cloud pricing.[1]Microsoft, “Microsoft Announces USD 17.5 Billion Investment in India Cloud and AI Infrastructure,” microsoft.com Parallel data-localization statutes compel banks, insurers, and hospitals to retain regulated data inside India, a mandate that steers fresh capex toward both captive and colocation GPU clusters. Production-linked incentives covering 4-6% of incremental sales reduce total system costs for local integrators, letting them undercut branded OEMs by 15-20%. When combined with Bureau of Indian Standards certification, the scheme removes quality concerns traditionally associated with white-box hardware. Early adoption in government and BFSI workloads has already produced a 40% year-over-year jump in enterprise GPU rack leases, signaling durable demand.

Rising AI Startup Ecosystem Demand for GPU-Accelerated Compute

More than 1,700 AI-focused startups had collectively raised USD 5.5 billion by 2025, and recent rounds are explicitly ring-fencing compute budgets alongside cash. Sarvam AI’s allocation of 4,096 H100 GPUs plus INR 99 crore subsidy demonstrates how sovereign-compute goals channel resources toward Indic language models, a content niche underserved by global players. GPU-as-a-service vendors such as Neysa AI let founders scale from 16 to 512 GPUs within hours, converting capital requirements into variable operating expenses and broadening participation beyond heavily funded ventures.[2]National Payments Corporation of India, “GPU-Accelerated Fraud Analytics Deployment,” npci.org.in Venture investors now treat guaranteed GPU access as a diligence item on par with revenue traction, effectively baking infrastructure readiness into every term sheet. The result is a reinforcement loop where fresh equity raises accelerate GPU procurement, in turn swelling the total addressable market for managed services.

Surge in Video Streaming, Gaming and AR/VR Requiring GPU-Based Transcoding and Rendering

India’s OTT subscriber base is on track to surpass 1 billion by 2027, and platforms have already switched to GPU-accelerated transcoders that shrink bitrate conversion costs by up to 40%. Cloud gaming pilots from NVIDIA GeForce Now and Xbox Cloud Gaming hinge on edge deployments capable of sub-20 millisecond responsiveness, a target achievable only with GPU-equipped micro data centers positioned inside telco points of presence. Retail and real-estate customers in Mumbai and Delhi now account for 60% of domestic AR rendering revenues, using photorealistic digital twins to drive buyer engagement. Volumetric video capture during the 2025 Indian Premier League proved the viability of 8K, multi-camera pipelines that feed GPU clusters and generate broadcast-ready replays inside 90 seconds. Such latency-sensitive workloads ensure that demand persists even when general enterprise spending tightens, giving operators a hedge against macro-cyclical dips.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| High Capital Expenditure for GPU-Equipped Data Centers | -2.1% | National, acute in Tier-2 and Tier-3 cities with limited financing options | Short term (≤ 2 years) |

| Limited Domestic Manufacturing Capacity Leading to Import Dependency | -1.6% | National, with supply chain concentrated in Taiwan, South Korea, and China | Medium term (2-4 years) |

| Power and Cooling Infrastructure Constraints in Tier-2/3 Indian Cities | -1.4% | Regional, affecting cities like Ahmedabad, Jaipur, Indore, Coimbatore | Medium term (2-4 years) |

| Supply-Chain Volatility in Advanced Packaging Components | -1.2% | National, dependent on TSMC and SK Hynix production schedules | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

High Capital Expenditure for GPU-Equipped Data Centers

A single rack populated with eight H100 GPUs costs USD 400,000-500,000, excluding real estate and power provisioning, which forces mid-market operators to allocate 40-50% equity in project finance deals versus the 25-30% norms observed in mature economies. Liquid cooling retrofits, now indispensable for dense AI clusters, add another USD 50,000-80,000 per rack and push energy footprints higher at a time when carbon disclosure mandates are tightening. Lenders remain wary of residual-value risk on specialized hardware, making interest spreads up to 250 basis points wider than for traditional data-center projects. In Tier-2 locations, the absence of 99.99% utility uptime obliges developers to oversize diesel gensets and battery strings, lifting all-in build costs by an additional 20-25%. Without targeted green-financing instruments that reward improved power usage effectiveness, new entrants outside the metro clusters face a prohibitive cost curve.

Limited Domestic Manufacturing Capacity Leading to Import Dependency

India imported USD 2.8 billion of GPUs and accelerator cards in 2025, 85% of which originated from Taiwan, China, and Malaysia, leaving local operators exposed to tariff swings and geopolitical flashpoints. The national semiconductor incentive prioritizes memory and analog devices, so sub-7-nanometer GPU fabrication remains out of scope until at least 2028. Import duties of 10-15% on finished cards inflate landed costs just as Southeast Asian free-trade competitors enjoy zero-tariff regimes, eroding India’s regional price competitiveness. HBM3 packaging, exclusively handled by TSMC’s CoWoS lines that already run at full capacity, imposes 6-9 month lead times, delaying cluster launch schedules and stranding capital in unfinished shells. Until indigenous assembly lines achieve volume scale and ecosystem depth, operators must navigate fluctuating availability that can derail multi-year expansion roadmaps.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Deployment Type: Cloud Anchors, Edge Accelerates

Cloud data centers accounted for 63.28% of the India data center GPU market share in 2025, underscoring hyperscalers’ ability to aggregate workloads and monetize GPUs via granular usage tiers, while edge data centers were identified as the fastest-growing segment through at 16.94% CAGR through 2031. The India data center GPU market now sees AWS, Microsoft Azure, and Google Cloud touting region-locked H100 instances that comply with data-residency statutes, a pivot that resonates with banks and life-sciences firms. Enterprises piggyback on these footprints, spinning up short-lived training jobs without committing capex and thereby shifting balance-sheet exposure to opex. Edge facilities, often 100-kilowatt pods attached to 5G base stations, are the fastest-growing node category because they reduce inference latency to sub-10 milliseconds for autonomous mobile robots and smart-city cameras.

The shift is powered by India’s 5G rollout across 400 cities, which is widening the addressable edge radius and establishing deterministic latency guarantees. Telecom operators such as Bharti Airtel leverage partnerships with NVIDIA to pre-install inference-optimized GPUs, creating an asset base that can be upsold to over-the-top media, logistics, and retail clients. Private data centers remain relevant for regulated verticals: pharmaceutical exporters subject to FDA audit trails and defense contractors bound by classified-data handling rules continue to procure isolated GPU clusters. The result is a hybrid topology in which the India data center GPU market size gets distributed across cloud, colocation, and edge rather than gravitating toward a single archetype.

By GPU Type: Inference Leads, Training Gains Momentum

Inference GPUs secured 58.37% of the India data center GPU market size in 2025, driven by commercial chatbots, product-recommendation engines, and real-time fraud-detection models that require high-throughput yet power-efficient silicon. NVIDIA’s L4 and L40S modules dominate because they deliver superior queries-per-watt, an attribute that dovetails with tightening power-availability caps in urban colocation campuses, whereas training GPUs are registering the highest growth at 17.45% CAGR through 2031 momentum across the forecast window. Training GPUs, while smaller in volume, command higher average selling prices and are expanding quickly as sovereign models for Indic languages and multimodal content gain policy backing.

Sarvam AI’s 4,096-H100 deployment illustrates how macro-level policy ambitions funnel capital into dense, training-only clusters. Concurrently, cloud vendors have launched on-demand eight-GPU slices that democratize access for teams looking to fine-tune open-weights models instead of building from scratch. Enterprises often pair H100 clusters for periodic retraining with L40S fleets for day-to-day inference, striking an internal equilibrium between capex constraints and latency targets. This mixed-fleet strategy underlines a nuanced demand curve: the India data center GPU market must accommodate both high-bandwidth, tightly coupled fabrics for training and PCIe-centric, power-sipping cards for inference.

By Interconnect: PCIe Dominates, HBM Interconnects Gain Share

Standard PCIe retained 74.63% of the India data center GPU market share in 2025 because it meshes with legacy x86 servers and leverages commodity networking gear, and high-bandwidth interconnect GPUs are expected to post the quickest expansion as larger language models become commonplace at 16.89% CAGR through 2031. Rapid adoption of PCIe Gen5 doubled bandwidth headroom without forcing a full stack overhaul, which appealed to enterprises upgrading five-year-old clusters. Yet projects that target trillion-parameter language models cannot escape all-to-all communication overhead; hence, hyperscalers are moving toward NVLink, NVSwitch, and InfiniBand fabrics capable of 900 GB/s node-to-node throughput.

Yotta Infrastructure’s 20,736-GPU Blackwell Ultra cluster harnesses NVSwitch to slice training time for 175-billion-parameter models from weeks to mere days. AMD’s Infinity Fabric and Intel’s Xe Link enter the conversation by bundling low-level software integrations that help customers avoid single-vendor lock-in. Cost differentials remain steep, with high-bandwidth fabrics adding 30-40% to bill-of-materials, but amortization across multi-year AI roadmaps increasingly justifies the outlay. Therefore, while PCIe continues to dominate routine inference jobs, the fastest-growth pocket within the India data center GPU market lies in high-bandwidth silicon interconnects.

By Workload Type: AI and ML Dominate, Analytics Surges

AI and machine learning workloads represented 67.94% of the India data center GPU market size in 2025, covering NLP, computer vision, and generative content services, with data analytics overtaking all other use cases as the fastest climber at 17.58% CAGR through 2031. Enterprises with moderate data-science talent now lean on pre-built model libraries, slashing integration lead times from quarters to weeks. Data analytics is the breakout category, propelled by GPU-accelerated SQL engines that cut batch windows from eight hours to under an hour for e-commerce clickstream analysis.

Flipkart’s migration to RAPIDS-powered clusters in 2025 reduced nightly ETL cycles to 45 minutes, a win that unlocked same-day pricing optimizations and trimmed excess inventory. High-performance computing for non-AI simulations remains a niche but strategically valuable slice, particularly for pharma molecules and aerospace digital twins. Graphics and visualization applications—spanning CAD, digital twins, and broadcast rendering- capture premium revenue because they rely on specialized GPUs that command higher rates per rack. Collectively, these patterns show that the India data center GPU market has broadened beyond early AI pioneers and now services an array of data-intensive, latency-sensitive workloads.

By End-User: Enterprises Lead, Hyperscalers Invest Aggressively

Enterprises owned 51.08% of spending in 2025, a testament to India’s sizable cohort of mid-market manufacturers, banks, and healthcare providers that cannot export regulated data, while hyperscalers remain the fastest-expanding customer group at 17.02% CAGR through 2031, as they continue multibillion-dollar build-outs across India. Adoption accelerated in banking, where GPU-based fraud detection scans millions of card transactions in real time and flags anomalies within 150 milliseconds. In pharmaceuticals, GPU-accelerated docking simulations are shaving months off drug-discovery pipelines and lowering early-stage R&D burn rates.

Hyperscalers, despite rapid capex deployment, remained second in market share because many corporations prefer single-tenant environments for sensitive workloads. Yet AWS, Azure, and Google Cloud are growing faster than any other customer group by packaging managed AI services that abstract away cluster orchestration hassles. Government and research deployments, anchored by the 38,000-GPU IndiaAI Mission and Indian Space Research Organization clusters, form a smaller but strategically vital share because they set data-governance precedents that private sector players must later follow. Taken together, these dynamics confirm that the India data center GPU market will stay multi-tenant yet sovereignty-driven for the foreseeable future.

Geography Analysis

West and South India together commanded more than 75% of installed GPU capacity in 2025, making Mumbai-Pune and Bangalore-Hyderabad the epicenters of India data center GPU market growth. Navi Mumbai’s clustering of AWS, Microsoft, and Oracle regions benefits from direct submarine-cable connectivity to the Middle East and Europe, shaving tens of milliseconds off round-trip latency for transcontinental inference catalogs. Bangalore’s Electronics City continues to pair GPU-rich colocation sites with India’s largest talent pool of AI engineers, creating an ecosystem where startups, system integrators, and hyperscalers coexist in symbiosis.

Hyderabad’s rise is anchored in a USD 15 billion commitment from Google Cloud and a USD 7 billion build by AWS, which jointly transform the corridor into the eastern gateway for Southeast Asian traffic. Chennai and Pune capture overflow demand from automotive and manufacturing clients that prioritize proximity to Tier-1 suppliers using GPU-powered predictive-maintenance dashboards. North India, centered on Delhi-NCR and Noida, holds roughly 18% of capacity and leans heavily on government workloads, including the Noida sovereign compute hub that opened in late 2024.

East, Central, and Northeast India remain nascent but show edge-deployment potential as BharatNet fiber expansion reaches rural clusters, opening the door for GPU-enabled telemedicine and precision agriculture inference. Tier-2 cities in established corridors, such as Coimbatore and Nashik, are emerging as cost-effective spillover locations where land runs 40% cheaper than in metros, keeping the India data center GPU market distributed rather than overly centralized. Smart Cities Mission infrastructure packages that bundle dedicated power substations and dark-fiber rings will likely accelerate this geographic diffusion by 2028-2030.

Competitive Landscape

The India data center GPU market is moderately concentrated, with NVIDIA controlling roughly 75-80% of silicon shipments, followed by AMD’s MI300 series and Intel’s Gaudi line pressing for share in high-volume inference skews. Hyperscalers employ vertical-integration tactics, reserving entire fabrication slots to guarantee uninterrupted supply, while colocation providers adopt asset-light leasing models that hedge capex risk. Local white-box integrators, buoyed by production-linked incentives, now sell GPU servers at 15-20% lower total cost of ownership, capturing mid-market demand that prizes affordability over tier-one branding.

Licensing barriers remain high, as NVIDIA’s CUDA ecosystem counts over 11,000 active patents and a decade of software tooling that binds customers to its hardware roadmaps. AMD counters with an open-source ROCm stack, and Intel offers oneAPI, both aimed at undercutting CUDA lock-in and appealing to public-sector entities that favor open standards. Emerging disruptors such as Neysa AI and E2E Networks bypass brick-and-mortar constraints by offering GPU-as-a-service models with minute-level billing granularity, lowering switching costs for developers.

Strategic differentiation also appears in cooling innovations: NxtGen’s liquid-immersion deployments hit a 1.15 power usage effectiveness ratio, granting them a 10-15% operating-cost edge. Certification against ISO 27001 and conformance with Bureau of Indian Standards guidelines now function as table stakes for enterprise contracts, culling less mature operators from shortlists. As demand outpaces global supply of HBM3 modules, buyers explore second-source agreements with Korean and Japanese suppliers to sidestep potential chokepoints, adding a new axis of competition centered on resilience rather than pure cost.

India Data Center GPU Industry Leaders

NVIDIA Corporation

Advanced Micro Devices, Inc.

Intel Corporation

Super Micro Computer, Inc.

Dell Technologies Inc.

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- January 2026: Yotta Infrastructure completed the deployment of 20,736 NVIDIA Blackwell Ultra GPUs in Navi Mumbai, creating India’s largest private AI training cluster.

- December 2025: E2E Networks commissioned 1,024 NVIDIA B200 GPUs in Noida, launching bare-metal instances priced 30% below hyperscale equivalents.

- November 2025: NxtGen Datacenter and Cloud Technologies installed 4,096 NVIDIA B200 GPUs across Mumbai and Bangalore, integrating liquid cooling that pushed PUE to 1.15.

India Data Center GPU Market Report Scope

Data Center GPU refers to a specialized graphics processing unit engineered for large-scale computing environments, such as enterprise data centers and cloud platforms, rather than for personal computers or gaming.

The India Data Center GPU Market Report is Segmented by Deployment Type (Cloud Data Centers, Enterprise/Private Data Centers, and Edge Data Centers), GPU Type (Training GPUs, Inference GPUs), Interconnect (PCIe-Based GPUs, and High-Bandwidth Interconnect GPUs), Workload Type (Artificial Intelligence (AI) and Machine Learning (ML), High-Performance Computing (HPC) (non-AI scientific computing), Data Analytics (database acceleration, query processing), and Graphics and Visualization (VDI, rendering, digital twins)), and End-User (Hyperscalers/Cloud Service Providers, Enterprises, and Government and Research Institutions). The Market Forecasts are Provided in Terms of Value (USD).

Key Questions Answered in the Report

What is the current size of the India data center GPU market and its forecast growth?

The market was valued at USD 1.16 billion in 2025, is projected at USD 1.44 billion in 2026, and is expected to reach USD 3.02 billion by 2031, reflecting a CAGR of 15.94% over 2026-2031.

Which deployment model leads GPU adoption within India?

Cloud data centers lead with 63.28% market share, while edge sites attached to 5G base stations are expanding at the quickest rate.

How are government policies influencing GPU demand?

Data-localization rules and the IndiaAI Mission together subsidize GPU access and require regulated workloads to remain onshore, directly stimulating domestic capacity additions.

Which GPU type is most widely deployed today?

Inference-optimized GPUs dominate, holding 58.37% of spending in 2025 because production workloads such as chatbots and recommendation engines are scaling faster than new model training projects.

Page last updated on: