South Korea Data Center GPU Market Size and Share

Market Overview

| Study Period | 2021 - 2031 |

|---|---|

| Forecast Data Period | 2026 - 2031 |

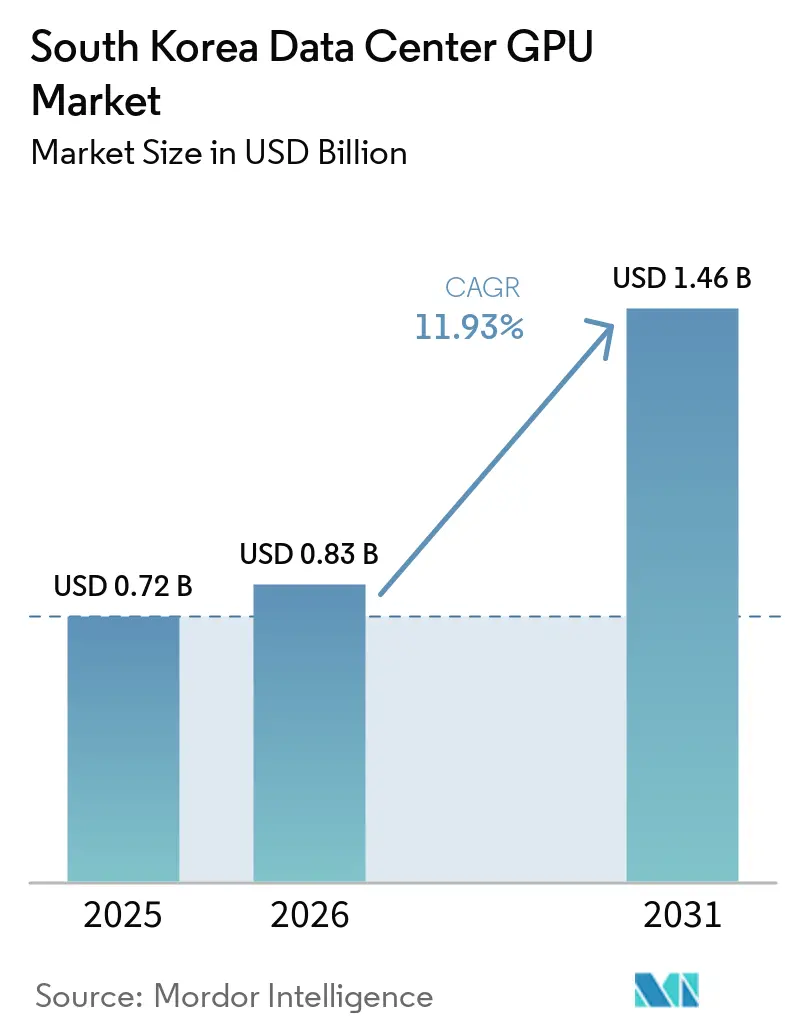

| Base Year Market Size (2025) | USD 0.72 Billion |

| Market Size (2026) | USD 0.83 Billion |

| Market Size (2031) | USD 1.46 Billion |

| Growth Rate (2026 - 2031) | 11.93% CAGR |

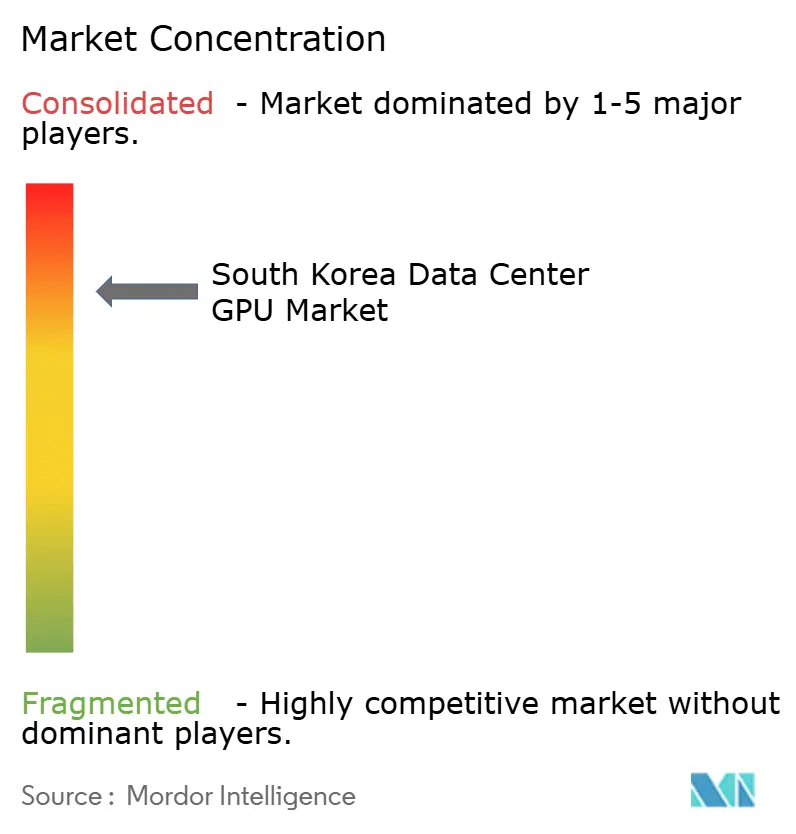

| Market Concentration | High |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

South Korea Data Center GPU Market Analysis by Mordor Intelligence

The South Korea Data Center GPU Market size is expected to grow from USD 0.72 billion in 2025 to USD 0.83 billion in 2026 and is forecast to reach USD 1.46 billion by 2031 at 11.93% CAGR over 2026-2031.

Robust sovereign-AI programs, accelerated 5G edge roll-outs, and government subsidies that cut financing costs on large GPU orders are jointly widening capital inflows. Local hyperscalers now commit to multiyear capacity contracts that guarantee volume discounts, while device makers SK hynix and Samsung Electronics compress supply-chain lead times by colocating HBM4 packaging plants with hyperscale campuses. A widening preference for inference-optimized accelerators is lifting token-generation throughput per watt, enabling providers to recoup hardware outlays within 30 months despite a 12% year-on-year rise in industrial power tariffs. Vendor roadmaps for liquid-cooling and rack densities above 100 kW further offset rising energy prices.

Key Report Takeaways

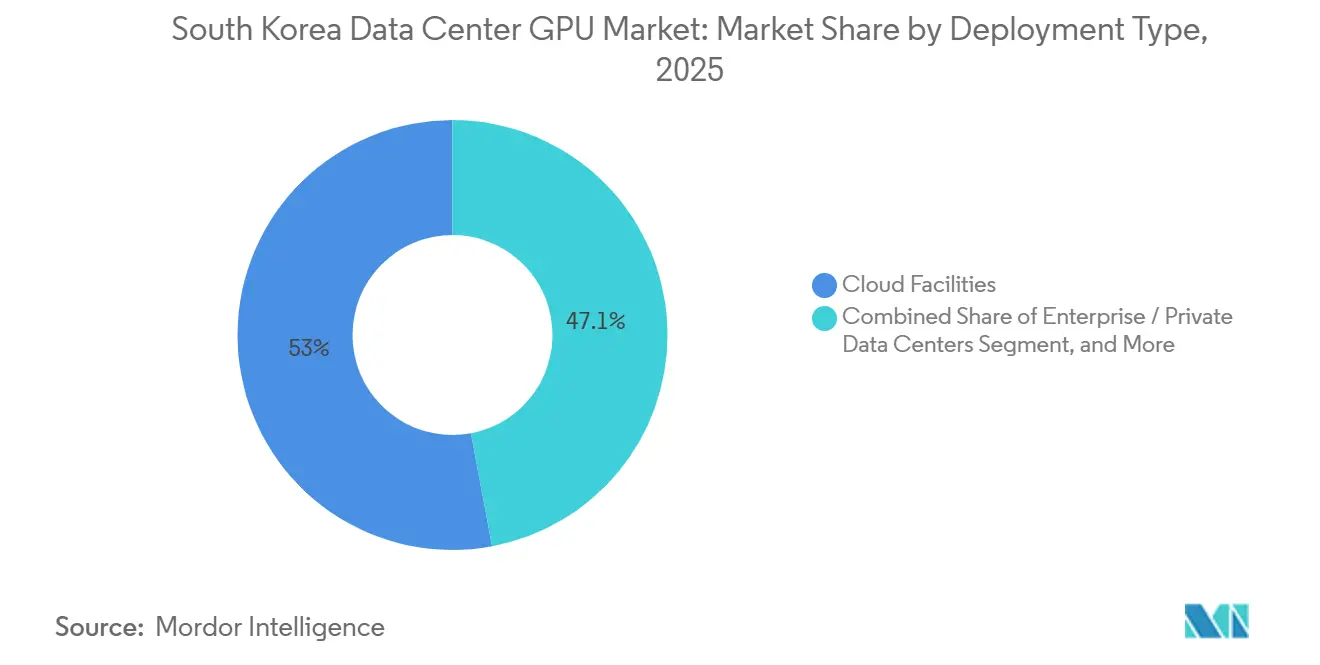

- By deployment type, cloud data centers held 52.95% of the South Korea data center GPU market share in 2025, whereas edge nodes are advancing at the fastest 11.93% CAGR through 2031.

- By GPU type, inference accelerators led with 59.44% revenue share in 2025, and this class continues to expand at a double-digit CAGR to 2031.

- By interconnect, PCIe devices captured 65.81% share of the South Korea data center GPU market size in 2025, but NVLink-class high-bandwidth parts record the highest forecast CAGR.

- By workload, artificial intelligence and machine learning workloads commanded 62.17% of the South Korea data center GPU market size in 2025, while data analytics is projected to post the most rapid growth through 2031.

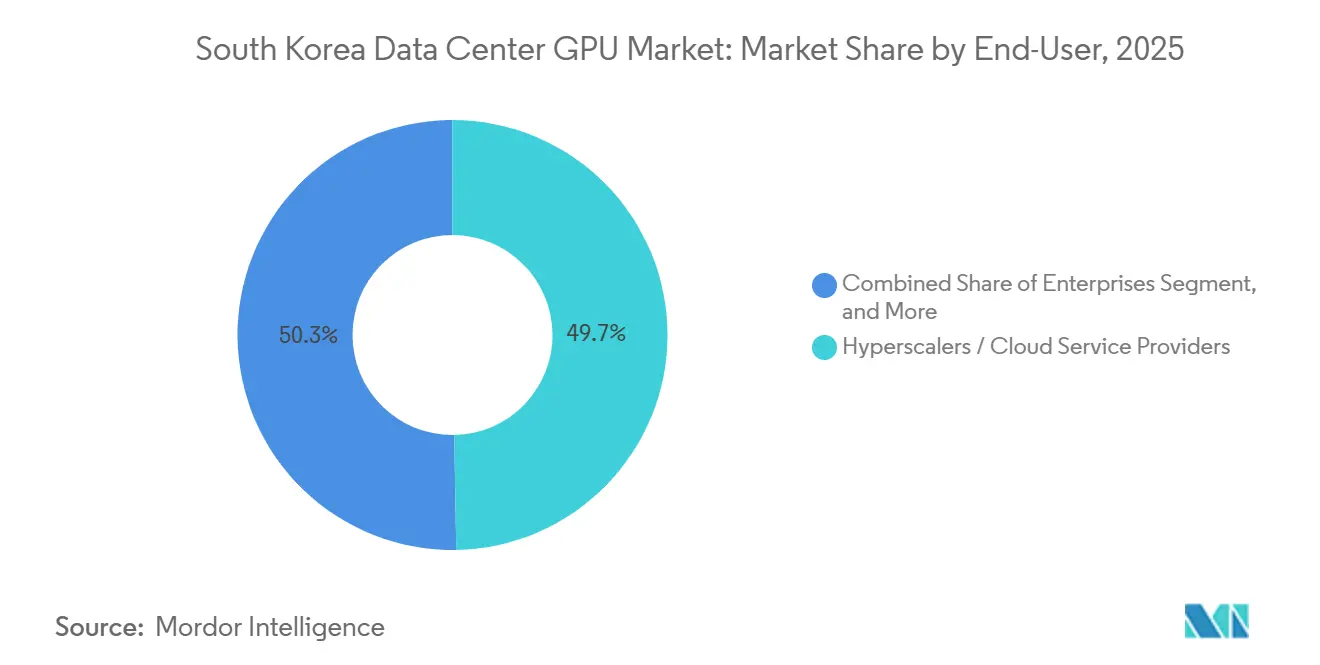

- By end-user, hyperscalers and cloud service providers accounted for 49.72% share in 2025, but enterprises exhibit the fastest CAGR as conglomerates internalize compute.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of January 2026.

South Korea Data Center GPU Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Surging Adoption of Generative AI Workloads in Korean Hyperscale Data Centers | +3.2% | National, concentrated in Seoul, Gyeonggi, Busan | Medium term (2-4 years) |

| Rapid Expansion of 5G and Edge Computing Infrastructure | +2.8% | National, early gains in Seoul, Incheon, Ulsan | Short term (≤ 2 years) |

| Government Incentives for High-Tech Manufacturing and Semiconductor Self-Reliance | +2.5% | National, K-Semiconductor Belt focus | Long term (≥ 4 years) |

| Increasing Demand for High-Performance Computing in Biomedical Research | +1.4% | National, led by Seoul, Daejeon | Medium term (2-4 years) |

| Localization of Large Language Models for Korean Language Services | +1.1% | Seoul metro area | Short term (≤ 2 years) |

| Carbon Emission Trading Pressure Driving GPU Consolidation and Liquid Cooling Adoption | +0.9% | Seoul and Incheon industrial zones | Medium term (2-4 years) |

| Source: Mordor Intelligence | |||

Surging Adoption of Generative AI Workloads

Korean hyperscalers are scaling multimodal language models that serve tens of millions of domestic users, which keeps utilization rates above 80% and locks in predictable demand. Naver’s KRW 400 billion (USD 307.7 million) debt facility earmarked for HyperCLOVA X OMNI adds thousands of GPUs, and SK Group alone targets 50,000 units by 2027.[1]Naver Corp., “Naver Expands HyperCLOVA X OMNI With KRW 400 Billion Investment,” navercorp.comMulti-year contracts coupled with vendor rebates lower per-GPU acquisition cost and lift the South Korea data center GPU market profitability.

Rapid Expansion of 5G and Edge Computing Infrastructure

Standalone 5G coverage exceeding 97% of households reduces round-trip latency requirements and sparks micro-modular edge builds around Seoul’s manufacturing corridors. KT’s Gasan AI Data Center reaches 1.15 PUE using direct-to-chip liquid cooling, delivering 35% energy savings.[2]KT Corp., “KT Launches Gasan AI Data Center With Liquid Cooling Technology,” kt.comEdge operators prioritize inference-tuned L4 and MI210 cards that fit 28 kW racks, broadening the South Korea data center GPU market footprint outside legacy hyperscale campuses.

Government Incentives for Semiconductor Self-Reliance

Tax credits worth KRW 1.2 trillion (USD 923.1 million) back local GPU design and chip-on-wafer packaging, encouraging Samsung and SK hynix to shorten domestic supply-chain loops. Faster HBM4 availability halves inventory cycles, improving capital efficiency for cloud buyers and sustaining a steady ramp in the South Korea data center GPU market.

Increasing Demand for Biomedical High-Performance Computing

KAIST’s K-Fold cluster and Samsung Biologics’ fluid-dynamics simulations underline how double-precision workloads accelerate drug discovery timelines, raising specialized GPU demand. Hospitals and research outfits gain government-funded access to 2,000 new accelerators in 2026, widening the non-hyperscale segment of the South Korea data center GPU market.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Supply Chain Volatility in Advanced GPU Packaging | -1.8% | National, acute for Samsung and SK hynix | Short term (≤ 2 years) |

| Rising Energy Prices and Grid Constraints in Metropolitan Seoul | -1.5% | Seoul, Incheon, Gyeonggi | Medium term (2-4 years) |

| Technological Dependence on Foreign GPU Vendors Amid Trade Tensions | -0.9% | National, export-oriented firms | Long term (≥ 4 years) |

| Talent Shortage in GPU Programming and Data Center Operations | -0.7% | Seoul and Daejeon tech hubs | Medium term (2-4 years) |

| Source: Mordor Intelligence | |||

Supply Chain Volatility in Advanced GPU Packaging

Yield dips for early HBM4 runs and calibration delays at new package lines restrict near-term volumes, forcing domestic buyers to extend order lead times and maintain 90-day inventories.[3]SK hynix, “SK hynix Begins Mass Production of HBM4,” skhynix.comImport licenses on H200 and MI325X units add further uncertainty, shaving 1.8 percentage points off the baseline CAGR forecast for the South Korea data center GPU market.

Rising Energy Prices and Grid Constraints

A 38% jump in data center electricity consumption clashes with slower grid reinforcements, while industrial tariffs rose 12% in 2026, wiping an estimated USD 15 million from annual cash flow per 10,000-GPU campus.[4]Korea Electric Power Corp., “Data Centers Consume 4.2 TWh in 2025,” kepco.co.kr Carbon trading costs at KRW 45,000 per tCO₂ (USD 34.6) press operators to adopt liquid cooling and shift training clusters to coastal Ulsan, tempering short-term growth in the South Korea data center GPU market.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Deployment Type: Edge Nodes Outpace Centralized Cloud Builds

Cloud facilities captured 52.95% of South Korea data center GPU market revenue in 2025, anchored by multi-tenant halls in Seoul’s Pangyo and Gasan districts. Higher rack utilization, bulk power procurement, and interconnect-rich fiber links keep per-GPU opex 30% below enterprise norms. Demand nevertheless tilts toward edge nodes that shorten latency to sub-10 milliseconds for autonomous mobility and augmented reality applications. KT’s liquid-cooled Gasan site runs 120 kW racks, marrying cloud-grade density with metro-edge proximity.

Enterprises such as Hyundai Motor Group deploy private clusters exceeding 50,000 accelerators to safeguard proprietary simulation data, demonstrating how conglomerates now fragment GPU demand across self-owned halls. Regulatory mandates that public services keep personal data onshore further lift edge uptake, fostering hundreds of micro-sites connected via 5G backhaul. This pivot diversifies revenue streams and cements the South Korea data center GPU market as a highly distributed ecosystem.

By Workload Type: Data Analytics Registers the Swiftest Upswing

AI and ML pipelines accounted for 62.17% of 2025 spending, underpinned by recommendation engines, search ranking, and conversational agents. These always-on inference flows optimize tokens-per-watt economics, sustaining 24-hour utilization cycles. GPU-accelerated SQL engines tripled fraud-detection query speeds at a Seoul National University pilot, signaling a fresh wave of database offloads.

High-performance computing retains a niche yet lucrative share due to double-precision needs in genomics, CFD, and weather modeling. Graphics virtualization for digital twins attracts automotive and electronics OEMs keen on shrinking prototype cycles, further diversifying the South Korean data center GPU market workload mix.

By Interconnect: NVLink and Infinity Fabric Narrow PCIe Dominance

PCIe devices held 65.81% market share in 2025 because enterprise buyers and inference clusters seldom require cross-node synchronization. Yet NVLink-5.0 and AMD Infinity Fabric now post the fastest shipment growth, propelled by foundation-model training groups that need 1.8 TBps of peer bandwidth.

Leaf-spine fabrics carrying 400 Gb Ethernet add USD 2 million in switch cost per rack, concentrating adoption among hyperscalers able to amortize capex over massive batch workloads. PCIe remains attractive for data analytics clusters and edge cabinets that chase cost efficiency, ensuring the South Korean data center GPU market retains a mix of high-bandwidth and mainstream interconnect offerings.

By GPU Type: Inference Hardware Leads Owing to Korean-Language LLM Traffic

Inference devices secured 59.44% of South Korea data center GPU market revenue in 2025 because consumer platforms like HyperCLOVA X OMNI serve millions of token requests each second. NVIDIA L40S and AMD MI300X cards, tuned for transformer inference, deliver fourfold higher revenue per watt than training counterparts, justifying more frequent refresh cycles NAVER.CORP.

Training GPUs still attract premium pricing thanks to high-bandwidth NVLink clusters that cut epoch time for 100 billion-parameter models. AWS’s underwater Ulsan hall will host 60,000 Blackwell units when it opens in 2027, emphasizing that large-scale training shifts to energy-cheaper coastal cities. The dichotomy sustains a two-tier supply structure that broadens the South Korea data center GPU market portfolio.

By End-User: Enterprises Gain Ground on Traditional Hyperscalers

Hyperscalers absorbed 49.72% of unit volumes in 2025, pooling customer demand to drive 80% utilization. Conglomerates such as Shinsegae and LG CNS increasingly favor on-premises deployments for data sovereignty and predictable total cost of ownership.

Government labs and universities procure specialized clusters under a USD 1.6 billion public budget line, advancing pandemic preparedness and precision medicine. The resulting fragmentation lowers the top-three buyer share to 62%, intensifying competition and reshaping sales tactics across the South Korea data center GPU market.

Geography Analysis

Seoul and its adjoining Gyeonggi and Incheon regions hosted 68% of operational GPUs in 2025, benefiting from dense fiber, talent pools, and proximity to 25 million consumers. Cloud operators cluster halls in Pangyo Techno Valley for sub-5 ms latency to e-commerce and fintech platforms. However, grid congestion and rising land prices prompt hyperscalers to place training farms in Ulsan and Busan, where seawater cooling trims PUE to 1.2 and land costs run 25% lower, enlarging the coastal slice of the South Korea data center GPU market.

Daejeon emerges as a biomedical computing hot spot, hosting KAIST’s K-Fold exaflop system and several federally funded biotech labs. Incheon Free Economic Zone attracts foreign colocation specialists such as Equinix and Digital Realty, adding edge nodes that serve autonomous port logistics and semiconductor R&D partners.

The Yongin-Pyeongtaek semiconductor corridor completes a self-contained value chain from HBM4 assembly to hyperscale deployment within 100 km, providing logistical advantages unmatched by rival markets. Intel and AMD each opened AI design centers in Seoul, joining Korean startups Rebellions and Sapeon to localize firmware and compiler stacks, further multiplying innovation nodes across the South Korea data center GPU market.

Competitive Landscape

NVIDIA retained roughly 85% of training-GPU shipments in 2025 thanks to CUDA lock-in and first-mover access to HBM4 memory. The Blackwell series pushes 2.5× performance gains, letting Korean hyperscalers downsize cluster counts by 40% while holding throughput steady. Chipped away at inference share, landing 18% of shipments on the strength of MI300X’s 192 GB VRAM and 60% lower sticker price versus H100 equivalents. Intel’s Gaudi 3 appeals to price-sensitive enterprises that can tolerate limited software ecosystems, selling at a 40% TCO discount for sub-30 billion-parameter models.

Local challengers Rebellions and Sapeon promise domain-specific inference chips offering 50% lower watt draw, though commercial volumes remain small. Samsung’s planned B300 accelerator aims for a 2027 debut to capture government-backed demand tied to semiconductor self-reliance targets. AWS, Google, and Microsoft extend the competitive field by rolling out proprietary Trainium, TPU, and MI300X-backed instances, respectively, reducing external GPU requirements.

Supplier power eases as customers adopt heterogeneous fleets, forcing vendors to bargain on bundled software, service credits, and memory-bandwidth guarantees. Margins thin for non-CUDA providers battling to seed ecosystems, while white-label ODMs gain relevance by integrating mixed-vendor pods for edge and enterprise buyers, reinforcing multipolar competition throughout the South Korea data center GPU market.

South Korea Data Center GPU Industry Leaders

NVIDIA Corporation

Advanced Micro Devices Inc.

Intel Corporation

Samsung Electronics Co. Ltd.

FuriosaAI Inc.

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- July 2026: NHN Cloud partners with Krafton to install 1,000 NVIDIA Blackwell Ultra GPUs, accelerating game-development asset generation by 40%.

- March 2026: KT launches the Gasan AI Data Center, featuring direct-to-chip liquid cooling for B200 GPUs, achieving a 1.15 PUE.

- February 2026: The government distributes 13,000 GPUs to Naver, Kakao, and NHN Cloud under a KRW 2.08 trillion (USD 1.6 billion) subsidy scheme.

South Korea Data Center GPU Market Report Scope

A data center GPU is an enterprise-grade, server-optimized parallel processor designed for 24/7 operation in rack-based infrastructure, featuring thousands of compute cores, high-bandwidth ECC memory, and specialized tensor/matrix units to accelerate data-parallel workloads such as AI training and inference, high-performance computing, data analytics, and graphics virtualization.

The South Korea Data Center GPU Market Report is Segmented by Deployment Type (Cloud Data Centers, Enterprise/Private Data Centers, and Edge Data Centers), GPU Type (Training GPUs and Inference GPUs), Interconnect (PCIe-Based GPUs and High-Bandwidth Interconnect GPUs), Workload Type (Artificial Intelligence (AI) and Machine Learning (ML), High-Performance Computing (HPC) [non-AI scientific computing], Data Analytics [database acceleration, query processing], and Graphics and Visualization [VDI, rendering, digital twins]), and End-User (Hyperscalers / Cloud Service Providers, Enterprises, and Government and Research Institutions). The Market Forecasts are Provided in Terms of Value (USD).

| Cloud Data Centers |

| Enterprise / Private Data Centers |

| Edge Data Centers |

| Training GPUs |

| Inference GPUs |

| PCIe-Based GPUs |

| High-Bandwidth Interconnect GPUs |

| Artificial Intelligence (AI) and Machine Learning (ML) |

| High-Performance Computing (HPC) (non-AI scientific computing) |

| Data Analytics (database acceleration, query processing) |

| Graphics and Visualization (VDI, rendering, digital twins) |

| Hyperscalers / Cloud Service Providers |

| Enterprises |

| Government and Research Institutions |

| By Deployment Type | Cloud Data Centers |

| Enterprise / Private Data Centers | |

| Edge Data Centers | |

| By GPU Type | Training GPUs |

| Inference GPUs | |

| By Interconnect | PCIe-Based GPUs |

| High-Bandwidth Interconnect GPUs | |

| By Workload Type | Artificial Intelligence (AI) and Machine Learning (ML) |

| High-Performance Computing (HPC) (non-AI scientific computing) | |

| Data Analytics (database acceleration, query processing) | |

| Graphics and Visualization (VDI, rendering, digital twins) | |

| By End-User | Hyperscalers / Cloud Service Providers |

| Enterprises | |

| Government and Research Institutions |

Key Questions Answered in the Report

What is the 2026 value of the South Korea data center GPU market?

The market is expected to reach USD 0.83 billion in 2026.

Which deployment model is growing fastest?

Edge data centers record the highest CAGR due to 5G latency requirements and onshore data rules.

Why do Korean hyperscalers favor inference GPUs?

Continuous serving of Korean-language LLMs yields higher revenue per watt, making inference accelerators more cost-effective than training devices.

How are energy constraints being addressed?

Operators deploy liquid cooling, relocate training clusters to coastal cities, and invest in high-efficiency racks to reduce grid load and carbon costs.

Page last updated on: