Southeast Asia Data Center GPU Market Size and Share

Market Overview

| Study Period | 2021 - 2031 |

|---|---|

| Forecast Data Period | 2026 - 2031 |

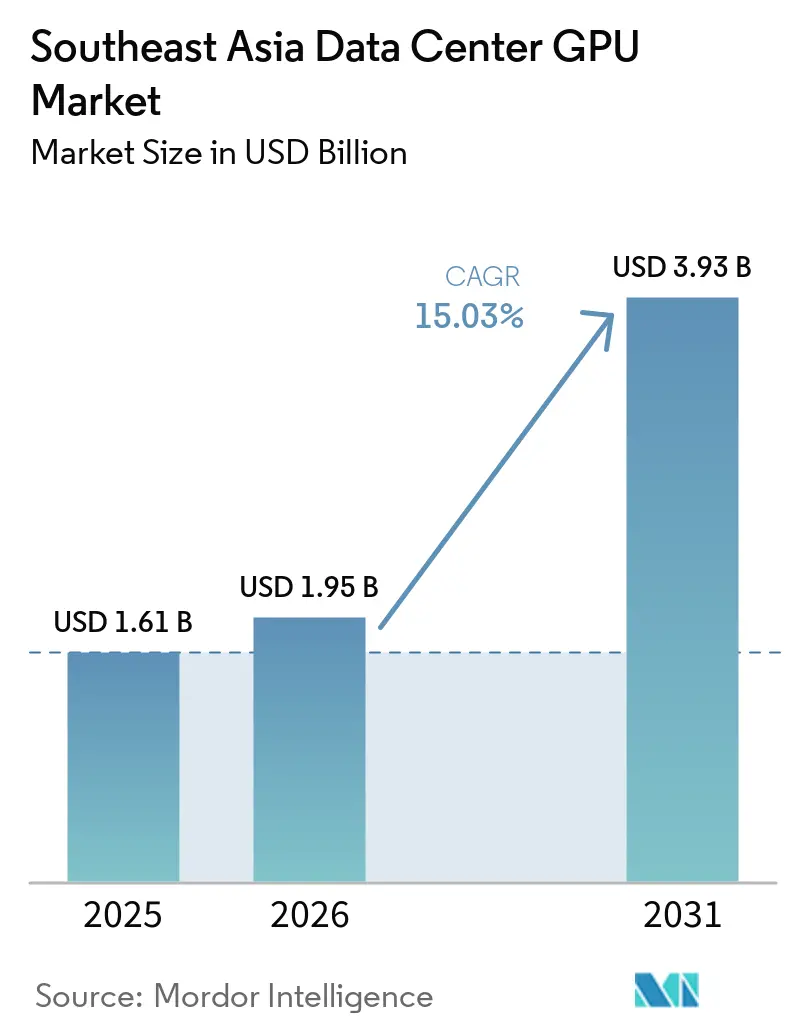

| Base Year Market Size (2025) | USD 1.61 Billion |

| Market Size (2026) | USD 1.95 Billion |

| Market Size (2031) | USD 3.93 Billion |

| Growth Rate (2026 - 2030) | 15.03% CAGR |

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

Southeast Asia Data Center GPU Market Analysis by Mordor Intelligence

The Southeast Asia data center GPU market size is projected to be USD 1.61 billion in 2025, USD 1.95 billion in 2026, and reach USD 3.93 billion by 2031, growing at a CAGR of 15.03% from 2026 to 2031. Strong hyperscaler commitments worth more than USD 13 billion over the last fifteen months are accelerating the pivot from CPU-centric infrastructure toward accelerated computing, which lifts rack densities to 120 kilowatts and drives incremental demand for liquid-cooling systems. Cloud facilities still anchor close to three-fifths of regional deployments, yet rapid 5G rollout is shifting part of the spend toward thousands of edge nodes that require inference-optimized accelerators. High-bandwidth memory shortages and import tariffs add price pressure, making mid-range GPUs attractive to enterprises that need predictable total cost of ownership. The competitive field remains moderately concentrated as NVIDIA’s CUDA ecosystem anchors the bulk of large language model training, though AMD’s price-performance gains and Intel’s Gaudi 3 launches are widening buyer choice.

Key Report Takeaways

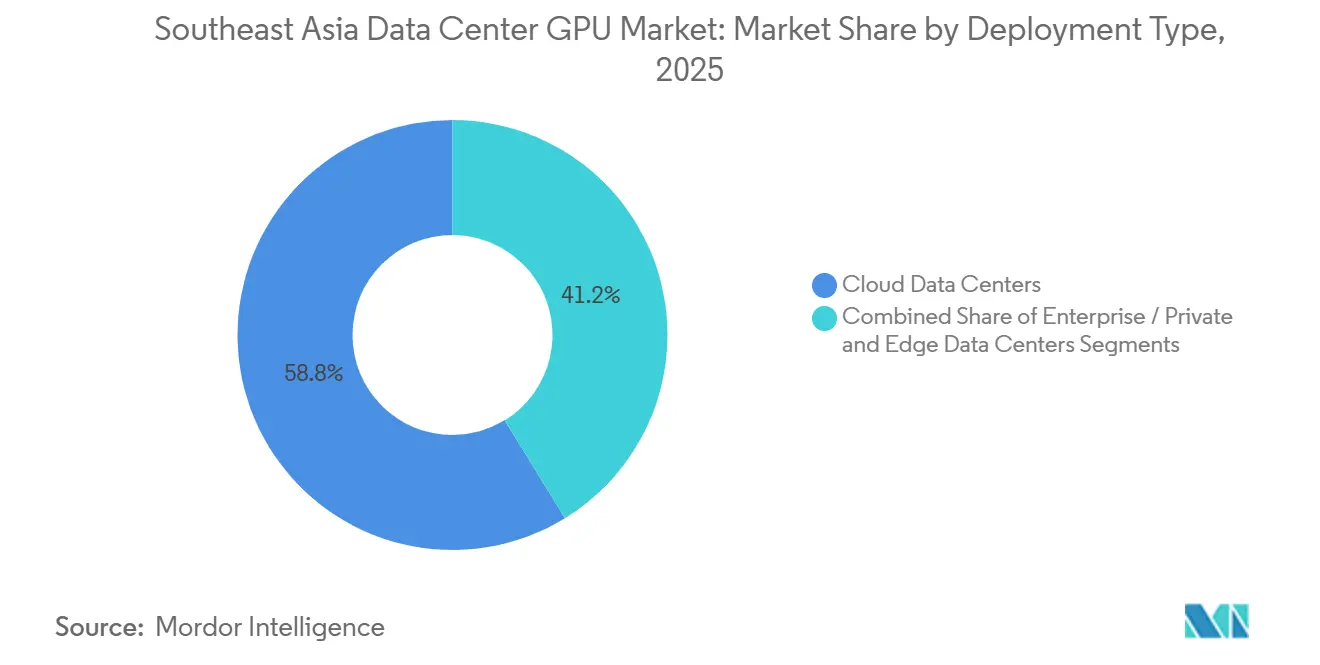

- By deployment type, cloud data centers led with 58.76% share in 2025 while edge sites are forecast to record the fastest CAGR at 22.4% through 2031.

- By GPU type, inference accelerators accounted for 57.52% of the data center GPU market share in 2025 and the segment is projected to expand at 17.9% CAGR to 2031.

- By interconnect, PCIe-based cards held 66.19% of 2025 shipments and high-bandwidth fabrics are set to grow at 19.2% CAGR between 2026 and 2031.

- By workload, AI and machine learning captured 60.35% revenue in 2025, while data analytics is forecast to advance at a 20.1% CAGR during 2026-2031.

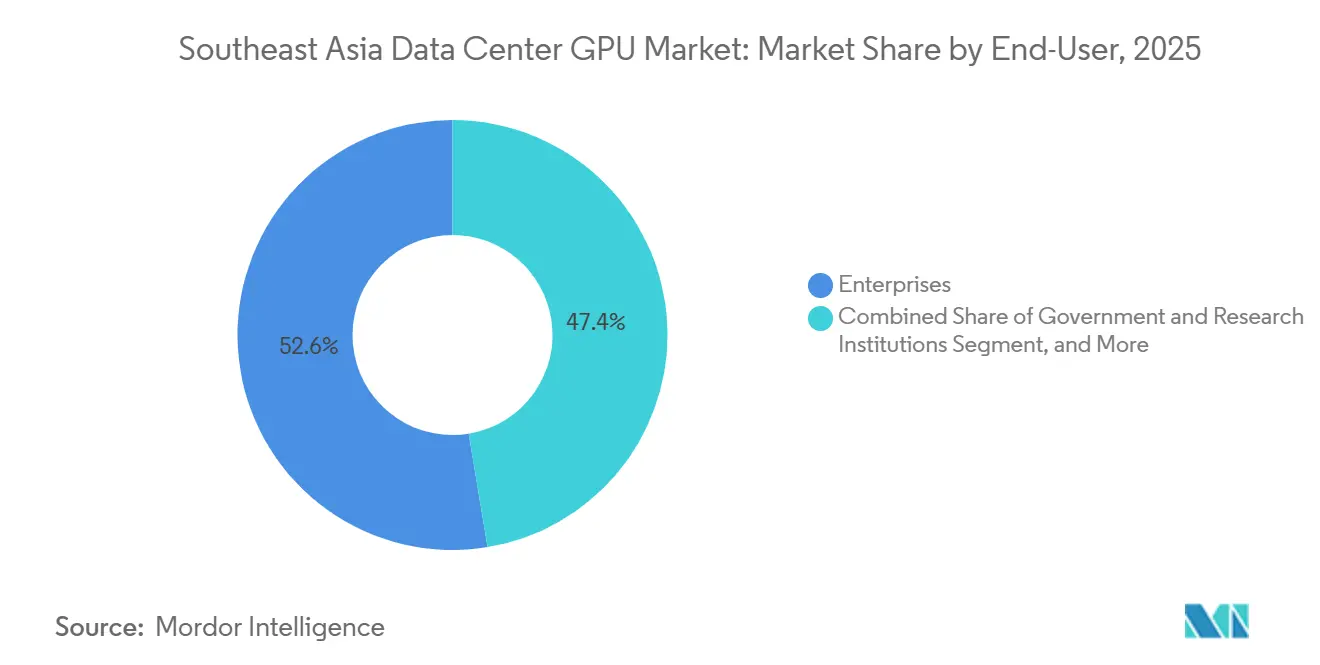

- By end-user, hyperscalers and cloud service providers commanded 52.61% demand in 2025; enterprises are expected to post the highest CAGR of 18.5% over the forecast horizon.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of January 2026.

Southeast Asia Data Center GPU Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Rapid Build-Out of AI-Optimized Hyperscale Facilities | 3.60% | Southeast Asia | Medium term (2–4 years) |

| Rising Adoption of GPU-Accelerated Databases for Fintech | 2.40% | Singapore, Indonesia, Malaysia, Thailand | Short term (≤ 2 years) |

| Government Incentives for Green Data Centers and Carbon Credits | 2.10% | Singapore, Malaysia, Indonesia | Medium term (2–4 years) |

| Growing Demand for Real-Time Digital Twin Platforms in Smart Cities | 2.00% | Singapore, Thailand, Vietnam | Medium term (2–4 years) |

| Proliferation of 5G-Enabled Edge Nodes for Low-Latency AI Inference | 2.80% | Southeast Asia | Short term (≤ 2 years) |

| Expansion of Cloud Gaming Services Across Southeast Asia | 1.90% | Southeast Asia | Short term (≤ 2 years) |

| Source: Mordor Intelligence | |||

Rapid Build-Out of AI-Optimized Hyperscale Facilities

Hyperscaler capital commitments topped USD 13 billion between January 2025 and March 2026, highlighted by Microsoft’s USD 5.5 billion plan for Singapore and USD 1.1 billion for Thailand. New campuses in Batam and Johor are designed around GPU-dense racks that exceed 80 kilowatts, a configuration that pushes liquid-cooling adoption and shapes vendor roadmaps toward chassis-level heat reuse.[1]Digital Edge, “Digital Edge Commits USD 4.5 Billion to Indonesia Batam Campus,” Financial Times, ft.comProximity to subsea cable landings improves latency to major Asian metros, which keeps workloads such as large language model serving anchored in the same availability zones. However, clustering of megawatt-scale projects inside a few corridors exposes operators to grid caps that can slow additional build-outs. Overall, sustained multiyear capex pipelines provide a clear demand signal that underpins the next wave of GPU volume orders.

Proliferation of 5G-Enabled Edge Nodes for Low-Latency AI Inference

More than 15,000 5G base stations installed during 2025 embedded micro data centers that host 4- to 8-GPU appliances for video analytics, autonomous vehicle telemetry, and industrial IoT workloads. Singtel’s Paragon platform showed sub-10-millisecond performance, proving that inference can shift away from centralized cloud while meeting quality-of-service targets.[2]Singtel Newsroom, “Singtel and Telkomsel Launch Paragon Edge Platform,” Reuters, reuters.comTelecommunications operators are now bundling infrastructure-as-a-service contracts that spread GPU capex across multiyear leases, which shortens sales cycles for entry-level accelerators. Yet fragmented site footprints create operational complexity because each edge location demands on-site maintenance skills, hardened enclosures, and remote orchestration stacks.

Rising Adoption of GPU-Accelerated Databases for Fintech

Transaction volumes doubled for leading payment networks in 2025, forcing banks and payment processors to migrate core risk engines to GPU-accelerated databases. VNPAY cut fraud detection latency from 200 milliseconds to 8 milliseconds after installing DGX A100 systems, while Indonesian wallet provider DANA saw a tenfold lift in analytic queries.[3]Nguyen Thi Bich, “Vietnam’s VNPAY Deploys NVIDIA DGX A100 for Real-Time Payments,” Reuters, reuters.comPerformance gains convert directly into lower chargeback losses and faster customer onboarding, which turns what a pilot workload was into a board-level agenda. Integration skills around CUDA kernels and data-lake ingestion remain scarce, slowing penetration into tier-2 banks, but early movers report payback periods under twelve months on infrastructure outlays.

Government Incentives for Green Data Centers and Carbon Credits

Malaysia, Thailand, and Singapore introduced tiered incentives that link tax breaks and carbon credits to renewable energy sourcing and power usage effectiveness benchmarks. Malaysia’s Digital Economy program offers MYR 1.2 billion (USD 270 million) in offsets for facilities achieving 80% renewable supply by 2027, anchoring long-term solar power purchase agreements. Singapore’s carbon tax at SGD 80 (USD 59) per ton applies financial pressure that accelerates adoption of liquid-cooling loops able to trim chiller loads by 30% to 40%. Such frameworks favor well-capitalized hyperscalers with the balance sheet capacity to prepay renewable infrastructure, while smaller colocation firms face margin compression if they cannot access similar financing terms.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Chronic Grid Instability and Power-Supply Constraints | -2.5% | Malaysia, Indonesia, Philippines, Vietnam | Short term (≤ 2 years) |

| Escalating Geopolitical Risk to Global GPU Supply Chains | -2.0% | Singapore, Malaysia, Thailand import channels | Medium term (2-4 years) |

| Limited Availability of Tier IV Data-Center Real Estate in Metro Hubs | -1.2% | Singapore, Kuala Lumpur, Jakarta, Bangkok | Medium term (2-4 years) |

| High Import Tariffs on Advanced Semiconductor Components | -0.8% | Indonesia, Vietnam, Philippines, Thailand | Short term (≤ 2 years) |

| Source: Mordor Intelligence | |||

Chronic Grid Instability and Power-Supply Constraints

Johor regulators rejected nearly one-third of data center applications in 2025 because substations could not meet megawatt-scale loads, placing operators in multiyear queues for capacity upgrades. Indonesia’s coal-dependent grid delivers only 99.7% uptime, short of the 99.995% needed for Tier III certification, leading to voltage swings that trip GPU thermal throttling safeguards. Power demand across the region is set to jump from 9 terawatt-hours in 2024 to 68 terawatt-hours by 2030, far outpacing confirmed generation projects. Enterprises are forced to lease diesel generators, which lift operating expenditure by up to 20% and undermine net-zero pledges, creating a wedge between sustainability rhetoric and day-to-day resiliency planning.

Escalating Geopolitical Risk to Global GPU Supply Chains

Effective January 2026, 25% United States tariffs added USD 7,500-10,000 to the landed cost of each H200 or MI325X GPU imported into Southeast Asia, eroding already thin cloud EBITDA margins. High-bandwidth memory shortages restricted NVIDIA to 700,000 H200 units per quarter, less than half of disclosed demand, stretching delivery lead times to nine months for some hyperscalers. Limited CoWoS advanced packaging capacity at subcontractors is fully booked until mid-2027, meaning price spikes and allocation battles will likely persist. Operators without multiyear offtake contracts must compete on secondary markets that command 40% premiums, which strains enterprise budgets and could delay AI adoption roadmaps.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Deployment Type: Edge Acceleration Outpaces Cloud Consolidation

Cloud installations delivered 58.76% of regional shipments in 2025, anchored in Singapore and Johor campuses that string tens of thousands of GPUs behind NVLink and InfiniBand fabrics to train and serve trillion-parameter models. Hyperscalers benefit from renewable power contracts that assure sub-1.3 power usage effectiveness as well as tax abatements linked to export revenue. Edge facilities, though smaller individually, are multiplying quickly because 5G densification demands inference at the radio access network; each micro site carries 4-8 NVIDIA T4 or A2 cards to guarantee sub-10-millisecond response for video analytics. The data center GPU market size tied to edge nodes is projected to surge at more than 22% CAGR, driven by telecom partnerships that spread capex across monthly subscriptions. Enterprise and private data centers round out the picture, mainly serving regulated industries that must retain certain records on-premises and burst excess loads to the public cloud when seasonal peaks hit.

Smaller footprints at the edge shift infrastructure design toward modular blades with single-phase immersion cooling and remote orchestration, a contrast to the monolithic chillers deployed in 120-kilowatt cloud racks. Telecommunication operators now negotiate joint procurement pools to unlock volume discounts, but heterogeneous deployment standards still inflate integration overhead. Meanwhile, colocation landlords in Jakarta and Bangkok bundle dedicated dark fiber into leases to capture hybrid workloads that pin sensitive data on premises while leaning on hyperscaler GPU bursts for peak analytics. This distributed topology diversifies revenue for the data center GPU market and hedges location risk, yet also fragments vendor relationships, complicating firmware management at scale.

By GPU Type: Inference Dominance Reflects Production Deployment Maturity

Inference accelerators captured 57.52% share in 2025 as enterprises prioritized monetizable services like chatbots, recommendation engines, and fraud screening over pure research training. The data center GPU market share tied to inference is expected to widen as transformer quantization reduces memory requirements and allows four inference GPUs to serve workloads previously needing eight. NVIDIA H100 NVL and L40S boards headline deployments in hyperscaler inference farms, while AMD MI300X competes on cost per token processed, especially in subscription tiers engineered for small-to-mid-size enterprises. Training GPUs such as H200 and MI325X remain vital for new foundation model development, but their share is bound by high memory premiums and longer lead times.

National supercomputing centers in Singapore and Thailand anchor most training clusters, which are now exploring partitioned scheduling that leases idle cycles to universities and startups. Inference boards, by contrast, surface everywhere from media studios rendering photorealistic scenes to fintech start-ups that refresh risk scores in milliseconds. The pivot toward inference shrinks average card power from 700 watts to 300 watts, easing rack integration and enabling incremental adoption of liquid-cooling retrofits rather than wholesale mechanical overhauls. Vendors that bridge software portability across FP16, FP8, and upcoming FP4 precisions can capture outsized share as model compression techniques proliferate.

By Interconnect: High-Bandwidth Fabrics Gain Share in AI Clusters

PCIe solutions still held 66.19% of shipments in 2025 because enterprise refresh cycles favor standards-based cards that slide into existing x86 servers without bespoke backplanes. The data center GPU market size for high-bandwidth fabrics nonetheless is rising fast, driven by clusters above 10,000 GPUs where all-reduce operations saturate PCIe even at Gen5 speeds. NVIDIA’s NVLink and InfiniBand topologies now ship with 900 gigabytes per second lane bandwidth, while AMD is pairing MI300X with Infinity Fabric over Ethernet to court price-sensitive operators. Microsoft’s Singapore region adopted HGX H200 trays linked via fifth-generation NVSwitch, and Alibaba Cloud’s Malaysia site uses InfiniBand HDR200 to knit 5,000 MI300X cards into one logical pool.

Enterprises that anchor data marts and visualization tasks on GPUs can stretch PCIe architecture through oversubscription without visible user impact, but machine-learning practitioners that chase larger parameter counts are budgeting for NVLink clusters despite 30-40% higher bill of materials. Future proofing is also swaying decisions because PCIe Gen6 will not reach commercialization until late decade, whereas NVLink roadmaps already cite 1.8 terabytes per second duplex bandwidth. Over the forecast horizon, incremental share gain for high-bandwidth fabrics will be capped by fabrication cost and supply constraints at advanced substrate plants, placing a premium on integrators that optimize mixed-interconnect topologies.

By Workload Type: Data Analytics Emerges as Growth Vector

AI and machine learning continued to dominate with 60.35% revenue in 2025, powered by continuous growth in large language model tokens and computer vision frame counts. However, explosive adoption of GPU-accelerated databases in fintech and telecom is turning data analytics into the fastest-expanding slice, outpacing AI by a full three percentage points in 2026. The data center GPU market size for analytics workloads benefits from regulatory pushes toward real-time payments, which mandate millisecond-level anti-fraud checkpoints. Graphics and visualization workloads, such as digital twin renderings for smart-city dashboards, are moving from high-end workstations into enterprise clusters, filling overnight idle cycles. High-performance computing stays niche but strategically important for regional climate modeling and genomic research.

Forward demand for data analytics aligns tightly with 5G subscriber growth because network telemetry furnishes terabytes of log data ripe for GPU acceleration. Banks in Jakarta, Ho Chi Minh City, and Manila are already layering GPU engines under columnar data stores to meet near-instant ledger reconciliation. Conversely, if open-source vector databases achieve effective CPU offload, a moderation of GPU attach rates could follow, underlining a dependency risk for vendors that lean on database-led expansion.

By End-User: Hyperscalers Command Procurement but Enterprises Diversify

Hyperscalers and cloud service providers purchased 52.61% of units in 2025, securing multi-year allocation agreements that shield them from supply shocks. This buying power allowed Azure, AWS, Google Cloud, Alibaba Cloud, and Tencent Cloud to lock in H100, H200, and MI325X deliveries months ahead of production runs. Enterprises, particularly fintech, media, and manufacturing firms, now regard reserved-instance offerings as insurance against tariff-driven price spikes, yet many still complete on-premise pilots to protect sensitive data. Government and research institutions remain volume-light but wield influence through early validation of novel architectures like Gaudi 3 or wafer-scale processors.

Enterprise boards are commonly present in two-rack pods inside existing data halls to sidestep major electrical upgrades. In contrast, hyperscalers can aggregate tens of thousands of cards into single-tenant halls with 120-kilowatt racks because they underwrite new high-voltage feeders. Governments fund national clusters that run mixed workloads and offer grant-subsidized cycles to startups, which helps local ecosystems but also distorts spot pricing when excess capacity is sub-leased on commercial terms.

Geography Analysis

Singapore retained the largest share of the data center GPU market in 2025 on the back of 1.4 gigawatts of installed capacity spread across more than 70 Tier IV facilities. The government’s post-moratorium green corridor permits only sites with power usage effectiveness below 1.3 and 80% renewable energy, steering demand into efficient liquid-cooled halls connected to subsea cables that deliver sub-5-millisecond latency to Hong Kong and Tokyo. Johor, Malaysia, emerges as the preferred scale-out zone for operators priced out of Singapore land auctions, but 30% of applications were rejected in 2025 because grid upgrades lag project timelines, limiting near-term offtake.

Indonesia posts the steepest growth trajectory as Digital Edge invests USD 4.5 billion in a 500-megawatt Batam campus and sovereign-AI projects anchor workloads in Jakarta and Surabaya. Although the grid still derives 68% of power from coal, demand for localized compute overrides efficiency concerns and motivates colocations to pre-install utility-scale battery farms. Vietnam draws growing attention, buoyed by Ho Chi Minh City campus builds and fintech poster child VNPAY’s DGX footprint, while Thailand leverages a USD 500 million multilateral loan to green its data-center power mix. The Philippines and the rest of Southeast Asia trail due to patchy power and limited submarine cable routes, but 5G investments are laying the groundwork for distributed edge inference nodes that will gradually add to regional volumes.

Competitive Landscape

NVIDIA continued to hold roughly 75-80% of training shipments and 65-70% of inference units in 2025, a dominance rooted in its CUDA developer moat and supply allocation rights struck long before pandemic shortages. AMD lifted its stake to the low-teens percentage range by positioning MI300-series parts at a 20-30% acquisition discount, which resonates with cloud tiers engineered for small-to-medium enterprises that tolerate slightly lower FLOPS. Intel’s Gaudi 3 earned pilot wins among enterprises seeking diversification strategies, though immature software tooling hampered broader adoption. Chinese accelerator alternatives remain largely inaccessible to Southeast Asian operators due to export controls and a tightening reliance on Western vendors.

Server original equipment manufacturers differentiate on thermal engineering; Supermicro shipped more than 100,000 GPU racks worldwide in fiscal 2025 and aims for Southeast Asia to supply 18% of incremental revenue. Dell Technologies and Hewlett-Packard Enterprise rely on embedded enterprise relationships and financial leasing arms to smooth purchase cycles, especially for CAPEX-averse customers. White-space disruption potential sits with mid-range inference accelerators, software abstraction layers that neutralize vendor lock-in, and emerging interconnect options that challenge NVLink economics. Despite modest entry from newcomers like Graphcore and Qualcomm, their penetration remains marginal because hyperscalers rarely risk production workloads on architectures lacking mass-market tooling.

Southeast Asia Data Center GPU Industry Leaders

NVIDIA Corporation

Advanced Micro Devices, Inc.

Intel Corporation

Huawei Technologies Co., Ltd.

Qualcomm Technologies, Inc.

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- March 2026: NVIDIA launched the Blackwell B200 GPU for Southeast Asian hyperscalers, promising 2.5x inference uplift over the H200 and 1.8 terabytes per second of NVLink bandwidth.

- February 2026: Microsoft committed USD 1.1 billion to GPU-rich data centers in Bangkok and Chonburi, with completion targeted for late 2027.

- January 2026: The United States enacted 25% tariffs on H200 and MI325X imports, adding about USD 10,000 per accelerator to Southeast Asian landed costs.

Southeast Asia Data Center GPU Market Report Scope

Data Center GPU refers to a specialized graphics processing unit engineered for large-scale computing environments, such as enterprise data centers and cloud platforms, rather than for personal computers or gaming.

The Southeast Asia GPU Market Report is Segmented by Deployment Type (Cloud Data Centers, Enterprise/Private Data Centers, and Edge Data Centers), GPU Type (Training GPUs, Inference GPUs), Interconnect (PCIe-Based GPUs, and High-Bandwidth Interconnect GPUs), Workload Type (Artificial Intelligence (AI) and Machine Learning (ML), High-Performance Computing (HPC) (non-AI scientific computing), Data Analytics (database acceleration, query processing), and Graphics and Visualization (VDI, rendering, digital twins)), and End-User (Hyperscalers/Cloud Service Providers, Enterprises, and Government and Research Institutions). The Market Forecasts are Provided in Terms of Value (USD).

| Cloud Data Centers |

| Enterprise / Private Data Centers |

| Edge Data Centers |

| Training GPUs |

| Inference GPUs |

| PCIe-Based GPUs |

| High-Bandwidth Interconnect GPUs |

| Artificial Intelligence (AI) and Machine Learning (ML) |

| High-Performance Computing (HPC) (non-AI scientific computing) |

| Data Analytics (database acceleration, query processing) |

| Graphics and Visualization (VDI, rendering, digital twins) |

| Hyperscalers / Cloud Service Providers |

| Enterprises |

| Government and Research Institutions |

| Indonesia |

| Malaysia |

| Philippines |

| Singapore |

| Thailand |

| Vietnam |

| Rest of Southeast Asia |

| By Deployment Type | Cloud Data Centers |

| Enterprise / Private Data Centers | |

| Edge Data Centers | |

| By GPU Type | Training GPUs |

| Inference GPUs | |

| By Interconnect | PCIe-Based GPUs |

| High-Bandwidth Interconnect GPUs | |

| By Workload Type | Artificial Intelligence (AI) and Machine Learning (ML) |

| High-Performance Computing (HPC) (non-AI scientific computing) | |

| Data Analytics (database acceleration, query processing) | |

| Graphics and Visualization (VDI, rendering, digital twins) | |

| By End-User | Hyperscalers / Cloud Service Providers |

| Enterprises | |

| Government and Research Institutions | |

| By Geography | Indonesia |

| Malaysia | |

| Philippines | |

| Singapore | |

| Thailand | |

| Vietnam | |

| Rest of Southeast Asia |

Key Questions Answered in the Report

What is the projected value of the Southeast Asia data center GPU market in 2031?

The data center GPU market is forecast to reach USD 3.93 billion by 2031.

Which deployment type is growing fastest across Southeast Asia?

Edge data centers are projected to expand at about 22% CAGR through 2031 because 5G rollouts require low-latency inference close to users.

How will import tariffs affect GPU pricing in the region?

A 25% United States tariff adds roughly USD 7,500-10,000 per high-end GPU, which compresses cloud margins and can delay enterprise purchases.

Why are inference GPUs gaining share over training GPUs?

Enterprises now prioritize production inference workloads like chatbots and fraud detection, making mid-power accelerators more cost-effective than flagship training boards.

Page last updated on: