Microwave-Safe Paperboard Trays Market Size and Share

Market Overview

| Study Period | 2019 - 2030 |

|---|---|

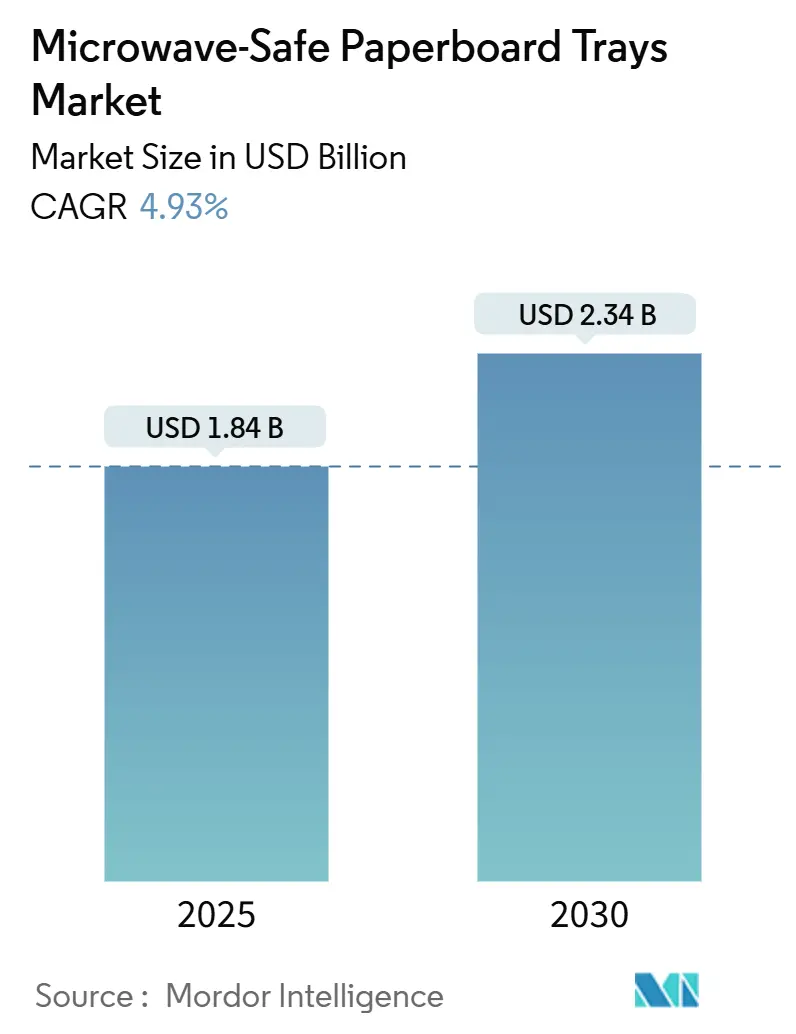

| Market Size (2025) | USD 1.84 Billion |

| Market Size (2030) | USD 2.34 Billion |

| Growth Rate (2025 - 2030) | 4.93% CAGR |

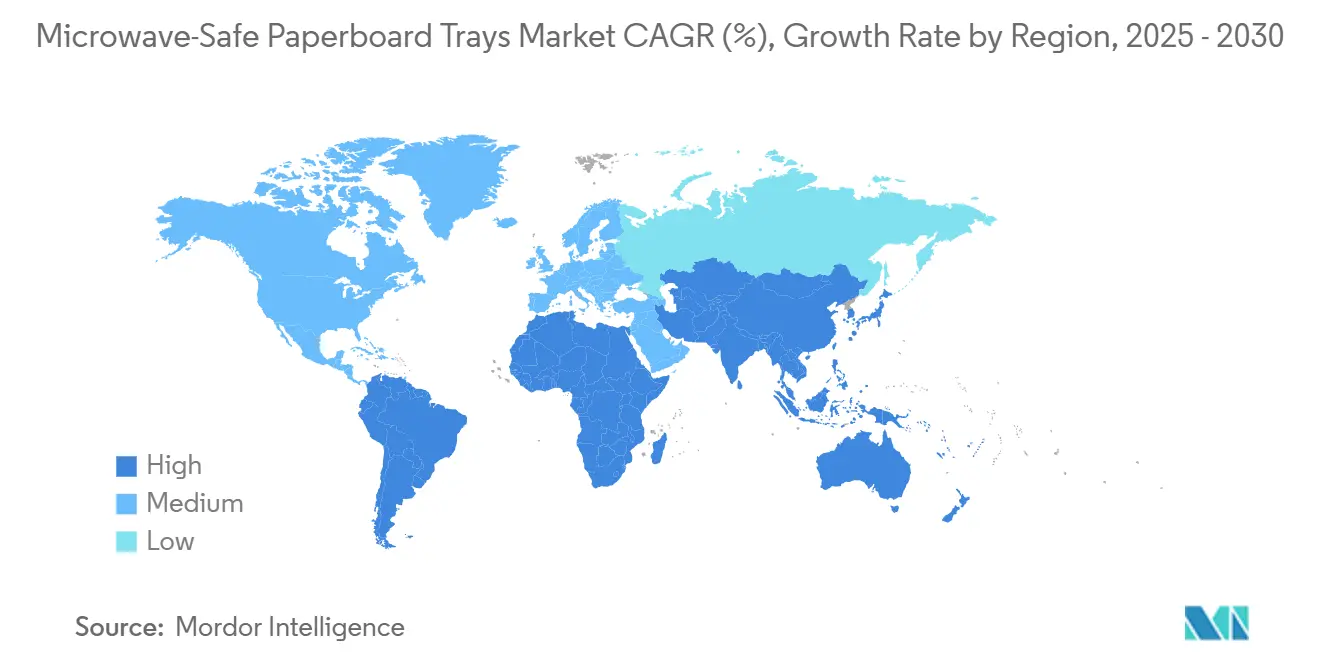

| Fastest Growing Market | Asia Pacific |

| Largest Market | Europe |

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

Microwave-Safe Paperboard Trays Market Analysis by Mordor Intelligence

The microwave-safe paperboard trays market size stood at USD 1.84 billion in 2025 and is forecast to rise to USD 2.34 billion by 2030, reflecting a 4.93% CAGR over the period. Rising regulatory bans on problematic plastics, brand-owner sustainability mandates, and technical advances in PFAS-free barrier coatings are widening the addressable universe for paper-based dual-ovenable formats. Momentum is strongest in premium ready-meal and meat applications where conventional-oven browning, microwave convenience, and recyclability requirements converge. Leading suppliers are scaling proprietary aqueous-coating lines, while converters without in-house formulation expertise confront higher compliance costs. Geographically, Europe’s circular-economy framework cements its leadership position, whereas urbanization and convenience-food uptake propel Asia-Pacific growth.

Key Report Takeaways

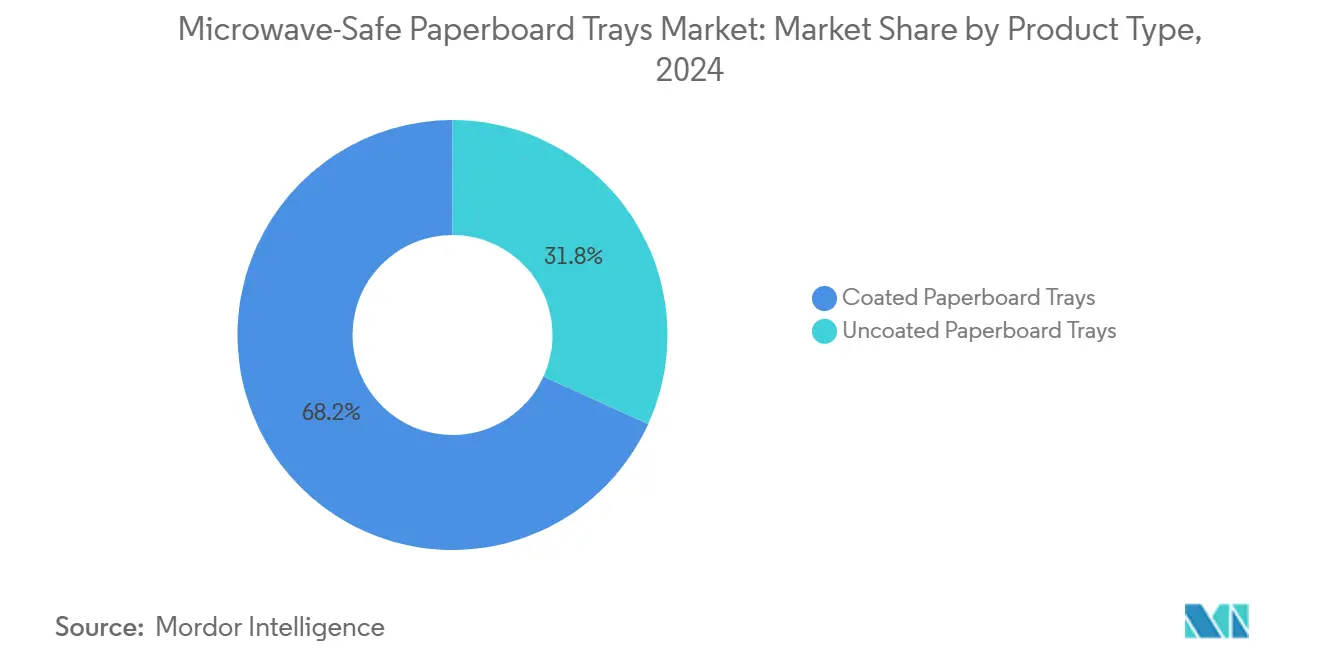

- By product type, coated paperboard trays led with 68.21% of the microwave-safe paperboard trays market share in 2024.

- By coating technology, microwave-safe paperboard trays market size for PFAS-free water-based barriers is projected to grow at a 5.37% CAGR between 2025- 2030.

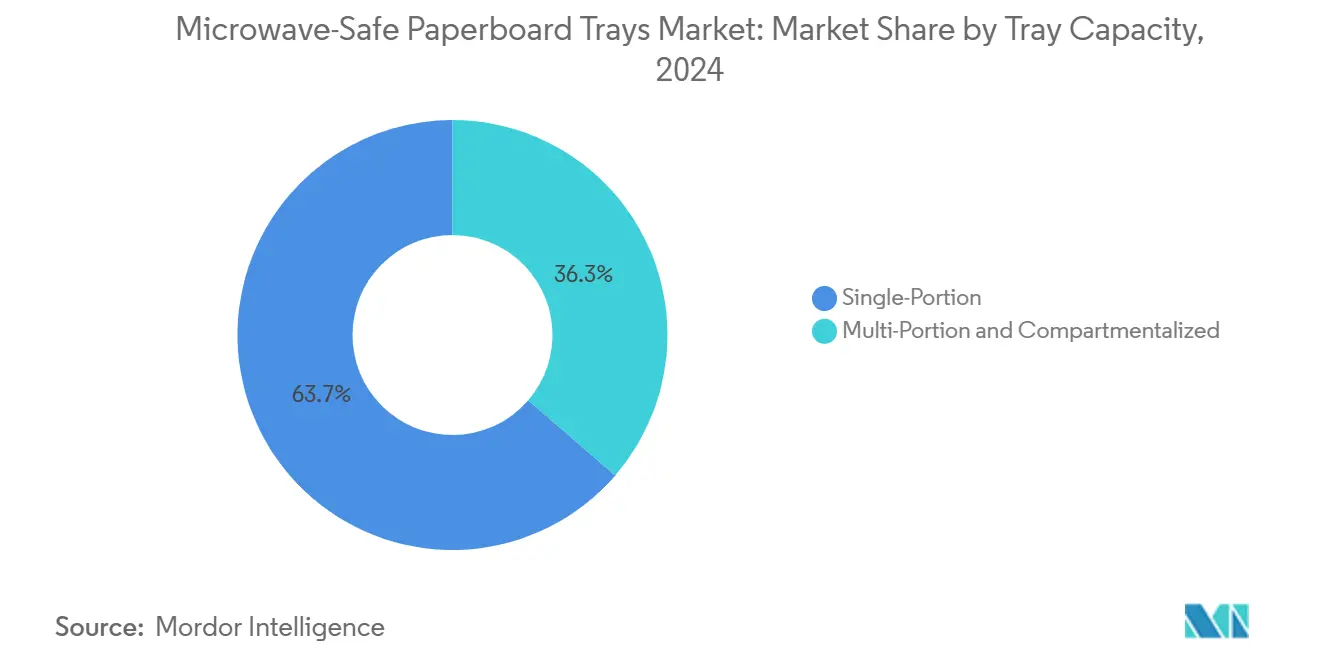

- By tray capacity, single-portion formats accounted for 63.67% of the microwave-safe paperboard trays market share in 2024.

- By end-use application, microwave-safe paperboard trays market size for meat and poultry packaging is projected to grow at a 6.21% CAGR between 2025 -2030.

- By geography, Europe dominated with 32.17% of the microwave-safe paperboard trays market share in 2024.

Global Microwave-Safe Paperboard Trays Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Regulatory bans on single-use plastics | +1.2% | Global, with EU and California leading | Medium term (2-4 years) |

| Retailer sustainability commitments | +0.8% | North America and EU, expanding to APAC | Long term (≥ 4 years) |

| Premium ready-meal demand for dual-ovenable packaging | +1.1% | Global, concentrated in urban markets | Short term (≤ 2 years) |

| Advances in barrier-coating technology | +0.9% | Global, R&D centered in North America and EU | Long term (≥ 4 years) |

| High-power convenience-store microwave adoption | +0.6% | APAC core, spill-over to urban MEA | Medium term (2-4 years) |

| Scope-3 carbon accounting pressure on brands | +0.7% | Global, multinational corporations first | Medium term (2-4 years) |

| Source: Mordor Intelligence | |||

Regulatory Bans on Single-Use Plastics

Sweeping legislation accelerated in 2024, most notably the EU Regulation 2025/40 that stipulates fully recyclable packaging by 2030 and restricts PFAS to 25 ppb in direct-food-contact formats [1]European Commission, “New rules for more sustainable and competitive packaging economy,” europa.eu. California’s SB 54 adds a 25% plastic-reduction target by 2032, pushing U.S. supply chains toward compliant fiber-based trays. Similar statutes emerged in South Australia, signaling how early-mover rules cascade across regions. For incumbents with PFAS-free technologies, the compressed compliance window converts regulation into a margin-defending moat. New entrants lacking formulation depth face capital-intensive retrofits, delaying time-to-market.

Retailer Sustainability Commitments

By 2025 McDonald’s aims for 100% renewable or recycled guest packaging, having already cleared 99.5% of fluorinated compounds. [2]McDonald’s Corporation, “Social Responsibility, Sustainability & ESG Reporting,” mcdonalds.com Wendy’s pursues the same goal by 2026, while Sysco pushes a 3,500-item sustainable catalog that diffuses requirements across fragmented food-away-from-home channels. Because these mandates run longer than statutory deadlines, suppliers obtain stable order visibility that justifies barrier-coating investments and regional capacity expansion. Winner-take-all dynamics emerge as selection criteria bundle recyclability, renewable content, and chain-of-custody proof.

Premium Ready-Meal Demand for Dual-Ovenable Packaging

Consumers trading up for chef-crafted chilled entrées value both microwave speed and oven browning, enabling coated paperboard trays to command 20-30% premiums over plastic. The ready-meal segment’s 46.48% share underscores this pricing power. Technical advances keep structure intact at 400 °F, widening use beyond microwave-only formats. Urban retailers exploit premium packaging to lift average selling prices, and foodservice operators specify dual-ovenable trays for takeaway menus that travel well yet crisp in-home ovens.

Advances in Barrier-Coating Technology

Commercial PFAS-free dispersion coatings from Kemira and paper-printer integrations from Solenis-Heidelberg hit scale in 2024 [3]Kemira, “Dispersion Barrier Coatings Are the Future of Recyclable Food Packaging,” kemira.com. Water-based chemistries match grease resistance of legacy PFAS systems while preserving recyclability. Mondi’s agricultural-by-product coatings point to bio-derived polymers that elevate barrier performance and biodegradability concurrently. R&D interest clusters around cellulose-nanofibril matrices and polysaccharide complexes, shifting the competition from raw-material access to application expertise

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Higher cost versus CPET/APET trays | -1.4% | Global, most acute in price-sensitive segments | Short term (≤ 2 years) |

| Moisture and grease-resistance limits at long hold times | -0.9% | Global, critical for extended foodservice applications | Medium term (2-4 years) |

| Limited recycling for hybrid paper-plastic formats | -0.7% | North America and EU, infrastructure-dependent regions | Long term (≥ 4 years) |

| Impending PFAS-coating prohibitions | -0.5% | Global, EU and California leading implementation | Short term (≤ 2 years) |

| Source: Mordor Intelligence | |||

Higher Cost Versus CPET/APET Trays

Specialty barrier coatings, food-grade pulp, and dedicated ovens for in-line drying raise unit costs 15-25% above CPET. The gap widens when virgin-resin prices fall. Price-sensitive programs in institutional catering thus prolong plastic tenure. Manufacturers respond with throughput gains from single-pass coaters and total-cost-of-ownership messaging that factors landfill fees and brand equity.

Moisture and Grease-Resistance Limits at Long Hold Times

Under heat lamps, water migration softens board and lets grease breach coatings, risking food safety and presentation. USDA advisories flag material choice for multi-hour holds. Protein-rich meat trays are most exposed. Research into hybrid multilayer chemistries is ongoing yet commercial adoption lags due to cost and regulatory validation cycles.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Product Type: Coated Solutions Drive Market Leadership

Coated paperboard held 68.21% of 2024 revenue, underscoring broad acceptance of aqueous and polymer-dispersion barriers that comply with the latest PFAS thresholds. The microwave-safe paperboard trays market size for coated variants is projected to advance at 4.62% CAGR as converters retrofit lines for in-line drying and flexographic integration. Uncoated grades linger in dry-food corners but lack grease resistance for mainstream foodservice. Innovation skews toward proprietary formulas such as Cascades Sonoco’s FlexSHIELD, which extend oven tolerance to 400 °F while preserving curbside recyclability. Suppliers with captive formulation teams thus secure predictable demand from global QSR chains.

Demand concentration around coated solutions positions material science as a brand-differentiating lever. Patent filings in 2024 covered cellulose-nanofibril reinforcement and cross-linked starch dispersions that boost water vapor transmission rates. As trial orders scale, the microwave-safe paperboard trays market begins consolidating around a smaller group of barrier-technology owners, discouraging price-only competition and supporting mid-single-digit margin expansion.

By Coating Technology: PFAS-Free Innovation Accelerates

Plastic lamination still represents 47.36% of global sales, yet water-based PFAS-free coatings record the sharpest rise at 5.37% CAGR. In absolute terms, the microwave-safe paperboard trays market size linked to lamination remains sizeable but faces legislative expiry dates in tier-one markets. Water-based chemistries leverage existing offset presses, trimming capex for converters and smoothing pathway to European recyclability logos. Bio-polymers derived from agricultural residues such as Mondi’s traceless solution move from pilot to pre-commercial scale, targeting full compostability by 2027.

The competitive narrative pivots on application know-how rather than raw-material access. Integrated paper groups exploit in-house lab analytics to iterate grease-kit scores quickly, outpacing toll-coating peers. Systems thinking covering pulp sourcing, dispersion preparation, line-speed calibration, and end-of-life pathways defines winning propositions.

By Tray Capacity: Single-Portion Dominance Faces Multi-Portion Challenge

Single-serve formats controlled 63.67% of shipments in 2024, reflecting entrenched consumption of individual frozen entrées and lunch kits. Nonetheless, meal kits, family dishes, and catering platters boost multi-portion demand, which outpaces the headline market at 5.03% CAGR. Innovative ribbed designs mitigate flex during heating, while compartmented variants separate proteins, starches, and sauces for even microwave energy distribution. The microwave-safe paperboard trays market share for multi-portion units is therefore set to widen as foodservice chains adopt portion-control menus for groups.

Cost-per-gram remains higher than single-serve equivalents, but menu premiums offset packaging upcharges. Converters with larger press formats and reinforced crease technology are best positioned, as conventional die cutters struggle with depth-of-draw required for family-size dishes.

By End-Use Application: Ready Meals Lead While Meat Segments Surge

Ready meals held 46.48% of global turnover in 2024, consolidating microwave-safe paperboard trays as the default for premium chilled and frozen dishes. Meat and poultry units, however, deliver a 6.21% CAGR through 2030 the fastest among tracked end uses. Retailers exploit dual-ovenable paperboard to showcase artisanal cuts and oven-finish convenience, positioning packs at higher price tiers. USDA’s endorsement of “ovenable board” for microwave meat further validates the shift. Suppliers now develop grease-lock formulations that maintain integrity during protein drip, meeting stringent retailer shelf-life tests.

Diversification into produce, bakery, and confectionery proceeds steadily, leveraging printability and natural aesthetics for branding. Because each food category demands distinct barrier combinations, multiline converters gain share by offering modular coating stacks tuned to moisture, fat, and oxygen profiles.

Geography Analysis

Europe retained 32.17% of global sales in 2024 underpinned by Regulation 2025/40, which mandates recyclable formats by 2030 and caps PFAS at trace levels. Green-public-procurement clauses further cement demand, as municipal cafeterias and transport concessions pivot to fiber trays. Nordic suppliers exploit abundant certified forestry to anchor supply security, while Mediterranean processors accelerate adoption to satisfy tourism-sector sustainability ratings. Energy-price volatility pressures pulp margins, yet scale economics from large mill clusters offset part of the squeeze.

Asia-Pacific delivers the highest growth at 7.02% CAGR to 2030, riding rapid urban migration, convenience-store chains, and rising microwave penetration. China’s pulp integration provides a cost base, though quality variances demand tight process control for export-grade orders. India’s ready-meal aisle expands alongside e-grocery, with microwave ovens exceeding 41 million units in use by 2025. Japan remains the reference market for high-power microwave compatibility, spurring suppliers to design trays that withstand sudden thermal load. Government directives in South Korea and Taiwan on food-contact fluorine thresholds mirror EU rules, smoothing regulatory alignment.

North America benefits from California’s SB 54, which forces a 25% plastic reduction by 2032 and applies nationwide through brand-spec standardization. U.S. quick-service leaders lock in multi-year fiber-tray contracts, providing volume certainty for coating-line retrofits in the Midwest and Southeast. Canada advances in parallel via provincial EPR rules, while Mexican processors capitalize on USMCA tariff exemptions to export PFAS-free trays northbound. Curbside recycling infrastructure remains a bottleneck for PE-lined board, but installation of dispersion-barrier pulpers expands, especially in Pacific-Northwest mills.

Competitive Landscape

The market shows moderate concentration: the top five suppliers control roughly 55% of revenue, balancing economies of scale with space for regional challengers. Huhtamaki, Graphic Packaging International, and Pactiv Evergreen leverage vertically integrated coating, molding, and printing lines across three continents. Huhtamaki’s 2024 fiber-lid capacity addition in Northern Ireland illustrates geography-diversification that cushions Brexit-linked trade frictions. Graphic Packaging extends European presence through PaperSeal™ Shape trays, blending premium aesthetics with recyclability. Pactiv Evergreen banks on domestic U.S. distribution to service national restaurant chains under just-in-time protocols.

Technology partnerships intensify: Solenis teams with Heidelberg to embed barrier dispersion directly in flexo presses, trimming process stages and licensing fees. Amcor’s AmFiber patent underscores cross-industry convergence between flexible packaging and molded fiber, signaling future licensing possibilities. Midsized players pursue niche strategies pecialty tray formats for institutional catering or bio-coated ranges for organic retailers to avoid head-to-head fights with giants.

M&A remains selective; buyers prioritize coating know-how, regulatory approvals, and blue-chip customer rosters over mere tonnage. Private-equity owners monitor exit windows tied to regulatory triggers that could unlock valuation uplifts as plastic substitution accelerates.

Microwave-Safe Paperboard Trays Industry Leaders

Huhtamaki Oyj

Graphic Packaging International LLC

Pactiv Evergreen Inc.

Sabert Corporation

Stora Enso Oyj

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- January 2025: Mondi and Traceless unveiled pilot trials of agricultural-residue-based water-borne coatings aimed at full industrial rollout in 2026.

- December 2024: Graphic Packaging and Elaborados Naturales commercialized the PaperSeal Shape Tray in Spain, adding styling flexibility to microwave-safe formats.

- October 2024: UPM Specialty Papers and Eastman launched a biopolymer-coated grease-barrier paper compatible with standard LDPE extruders, lowering adopter capex.

- September 2024: Solenis and Heidelberg announced joint flexographic barrier-coating systems, promising 15% cost savings versus off-line lamination.

Global Microwave-Safe Paperboard Trays Market Report Scope

| Coated Paperboard Trays |

| Uncoated Paperboard Trays |

| PFAS-Free Water-Based Barrier |

| Bio-Based Polymer Barrier |

| Plastic Lamination (PE, PP) |

| Single-Portion |

| Multi-Portion and Compartmentalized |

| Ready Meals |

| Meat and Poultry |

| Produce and Fresh-Cut |

| Bakery and Confectionery |

| Food-service Take-away |

| North America | United States | |

| Canada | ||

| Mexico | ||

| South America | Brazil | |

| Argentina | ||

| Rest of South America | ||

| Europe | Germany | |

| United Kingdom | ||

| France | ||

| Italy | ||

| Spain | ||

| Russia | ||

| Rest of Europe | ||

| Asia-Pacific | China | |

| Japan | ||

| India | ||

| South Korea | ||

| Australia | ||

| Rest of Asia-Pacific | ||

| Middle East and Africa | Middle East | Saudi Arabia |

| United Arab Emirates | ||

| Turkey | ||

| Rest of Middle East | ||

| Africa | South Africa | |

| Nigeria | ||

| Rest of Africa | ||

| By Product Type | Coated Paperboard Trays | ||

| Uncoated Paperboard Trays | |||

| By Coating Technology | PFAS-Free Water-Based Barrier | ||

| Bio-Based Polymer Barrier | |||

| Plastic Lamination (PE, PP) | |||

| By Tray Capacity | Single-Portion | ||

| Multi-Portion and Compartmentalized | |||

| By End-Use Application | Ready Meals | ||

| Meat and Poultry | |||

| Produce and Fresh-Cut | |||

| Bakery and Confectionery | |||

| Food-service Take-away | |||

| By Geography | North America | United States | |

| Canada | |||

| Mexico | |||

| South America | Brazil | ||

| Argentina | |||

| Rest of South America | |||

| Europe | Germany | ||

| United Kingdom | |||

| France | |||

| Italy | |||

| Spain | |||

| Russia | |||

| Rest of Europe | |||

| Asia-Pacific | China | ||

| Japan | |||

| India | |||

| South Korea | |||

| Australia | |||

| Rest of Asia-Pacific | |||

| Middle East and Africa | Middle East | Saudi Arabia | |

| United Arab Emirates | |||

| Turkey | |||

| Rest of Middle East | |||

| Africa | South Africa | ||

| Nigeria | |||

| Rest of Africa | |||

Key Questions Answered in the Report

What was the global value of microwave-safe paperboard trays in 2025?

The market was valued at USD 1.84 billion in 2025.

Which region leads in adoption?

Europe commanded 32.17% of worldwide revenue in 2024 due to stringent circular-economy rules.

Which end-use category dominates demand?

Ready meals represent 46.48% of sales, leveraging dual-ovenable features for premium positioning.

Which segment will grow the fastest to 2030?

Meat and poultry packaging is projected to rise at a 6.21% CAGR as brands seek dual-ovenable, grease-resistant solutions.

How are brands meeting PFAS regulations?

Suppliers are shifting to water-based and bio-derived barrier coatings that meet FDA and EU PFAS limits.

What hampers wider uptake in foodservice?

Higher costs versus CPET and performance limits under prolonged heat-lamp dwell times remain key restraints.

Page last updated on: