Silicone-Coated Paperboard Packaging Market Size and Share

Market Overview

| Study Period | 2019 - 2030 |

|---|---|

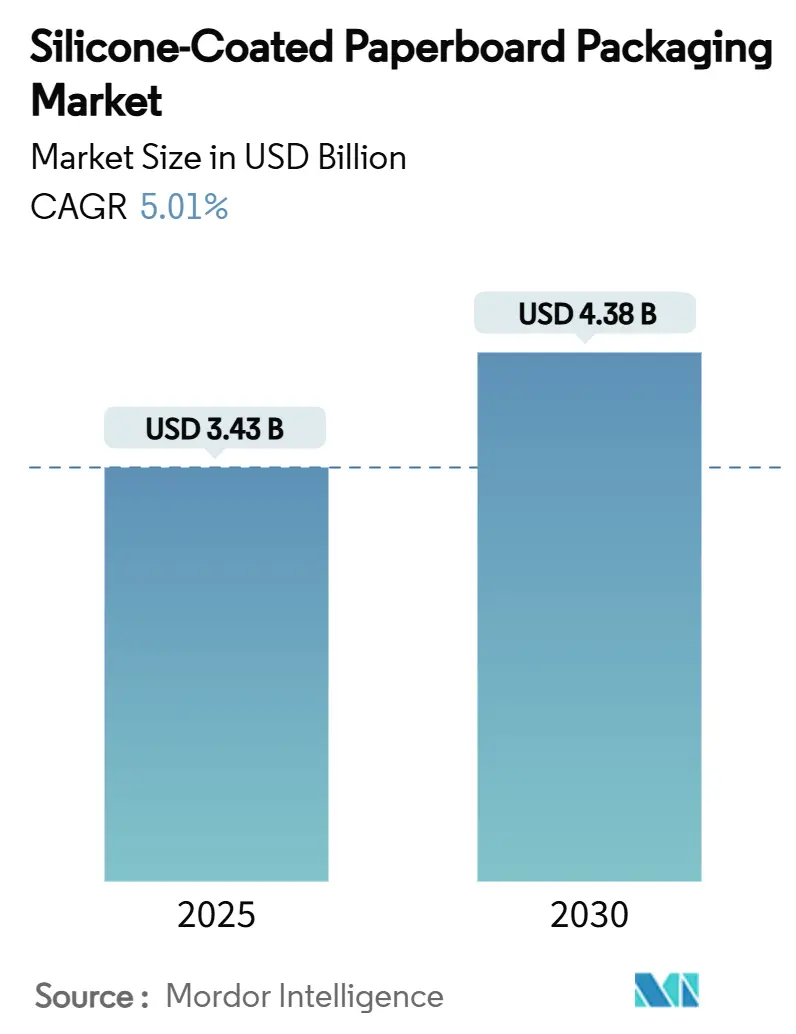

| Market Size (2025) | USD 3.43 Billion |

| Market Size (2030) | USD 4.38 Billion |

| Growth Rate (2025 - 2030) | 5.01% CAGR |

| Fastest Growing Market | South America |

| Largest Market | Asia Pacific |

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

Silicone-Coated Paperboard Packaging Market Analysis by Mordor Intelligence

The silicone-coated paperboard packaging market size stands at USD 3.43 billion in 2025 and is forecast to reach USD 4.38 billion by 2030, advancing at a 5.01% CAGR. Moderate but steady expansion reflects the push-and-pull between regulatory mandates favoring fiber substrates and operational realities that still demand high-performance barrier coatings. Brand owners seeking to decarbonize portfolios, quick-service chains racing to streamline fulfillment, and e-commerce platforms looking for friction-free automation collectively underpin demand for silicone liners. On the supply side, solventless processes safeguard air-quality compliance, while water-based emulsions gain traction as capital investment channels into lower-VOC assets. Capacity additions across Asia and South America balance regional demand, tempering risk of tight supply even as feedstock volatility looms. Competitive positioning hinges less on raw fiber cost and more on vertically integrated value chains that synchronize pulp, coating, and converting operations to meet aggressive lead-time expectations.

Key Report Takeaways

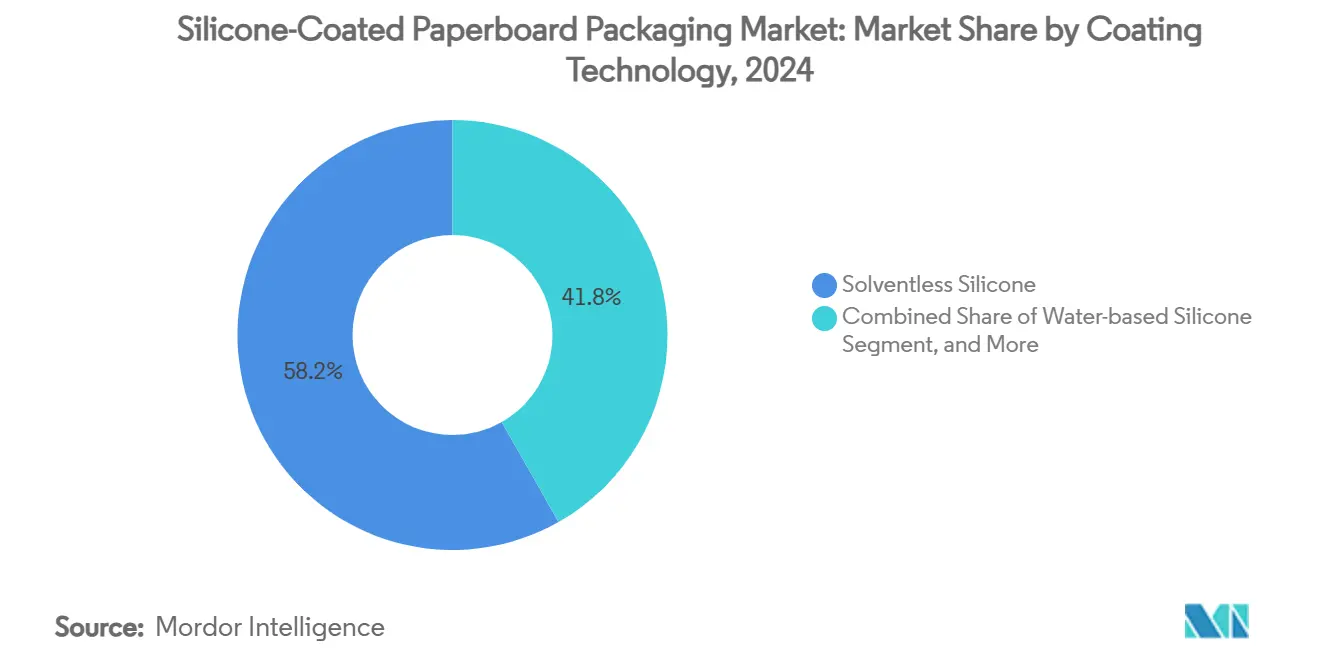

- By coating technology, solventless silicone captured a 58.21% of the silicone-coated paperboard packaging market share in 2024.

- By end-use industry, silicone-coated paperboard packaging market size for meal-kit and take-away formats segment projected to grow at 6.90% CAGR between 2025-2030.

- By geography, Asia-Pacific region captured 41.21% of the silicone-coated paperboard packaging market share in 2024.

Global Silicone-Coated Paperboard Packaging Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Plastics-ban legislation accelerating paperboard substitution | +1.2% | Global, with EU and North America leading | Medium term (2-4 years) |

| Surge in quick-service and meal-kit formats needing grease-resistant board | +0.8% | Global, concentrated in urban markets | Short term (≤ 2 years) |

| E-commerce ready-to-ship designs demanding high-slip release liners | +0.6% | APAC core, spill-over to North America | Medium term (2-4 years) |

| CAPEX wave in APAC SBS/FBB mills adding silicone-coating capacity | +0.4% | APAC, with secondary effects in MEA | Long term (≥ 4 years) |

| Roll-to-roll plasma pretreatments lowering silicone coat weight | +0.3% | Global, with early adoption in Europe | Medium term (2-4 years) |

| PFAS-exit policies favouring silicone over fluorochemicals | +0.9% | North America and EU, expanding to APAC | Short term (≤ 2 years) |

| Source: Mordor Intelligence | |||

Plastics-Ban Legislation Accelerating Paperboard Substitution

Lawmakers on both sides of the Atlantic now codify aggressive recyclability and PFAS-elimination thresholds, creating a compliance premium for barrier solutions that remain recyclable at the mill. The EU Packaging and Packaging Waste Regulation requires 70% recyclability by 2030 and virtually bars PFAS in food contact by 2026. California’s AB 347 mirrors that stance with a 100 ppm PFAS ceiling and phased enforcement starting 2024.[1]California AB 347 Analysis Team, “California Enacts Enforcement Scheme for PFAS Ban,” Keller and Heckman, packaginglaw.com Australia’s pending producer-responsibility scheme strengthens the same trajectory. Brand owners view silicone coatings as an immediately commercialized path to satisfy these overlapping rules while maintaining oil- and grease-resistance. As converters reposition assets, order lead-times for solventless systems have tightened, signaling heightened demand velocity across both multinational and regional plants.

Surge in Quick-Service and Meal-Kit Formats Needing Grease-Resistant Board

Urban consumers gravitate toward meals that travel well and reheat quickly, fueling a worldwide uptick in meal-kit and takeaway packaging. Silicone-coated folding boxboard handles prolonged contact with hot oils without delaminating, an attribute that uncoated fiber grades cannot match. U.S. FDA Food Code (2022) underscores safety prerequisites, nudging chain restaurants toward proven chemistries. State-level food-service manuals such as Georgia’s technical guide further codify material integrity, indirectly steering operators toward silicone-lined formats. Performance certainty keeps replacement cycles short, ensuring recurring liner demand even when menu volumes fluctuate. Coupled with growing ghost-kitchen models, the silicone-coated paperboard packaging market sees new addressable tonnage in single-use clamshells, bowls, and sleeves.

E-Commerce Ready-to-Ship Designs Demanding High-Slip Release Liners

Fulfillment centers aim to ship more orders per labor hour, which makes surface friction a cost variable. Papers treated with thin silicone layers exhibit consistent release forces below 1.5 N/cm after atmospheric plasma pretreatment, reducing line jams in automated pack stations. Roll-to-roll plasma rigs, validated on nanocellulose substrates, align with high-volume conveyance speeds used in apparel and cosmetics mail-order hubs. Global integrators now bundle release-liner performance specs into procurement RFQs, opening a channel for coated board grades that double as retail-ready outer cartons. The cumulative pull from millions of parcels drives incremental square-meter demand that complements traditional food-contact tonnage, allowing mills to run broader width configurations for better asset utilization.

CAPEX Wave in APAC SBS/FBB Mills Adding Silicone-Coating Capacity

Asian mills are re-tooling to secure higher margins by integrating on-line silicone coaters. Recent marquee projects—such as the 750,000 tpa consumer board line at Stora Enso’s Oulu site and Billerud’s North American refit—mirror similar expansion in South Korea and Vietnam, where SBS capacity is climbing.[2]Stora Enso Press Office, “Oulu Board Line Starts Up,” storaenso.com Investments often couple solventless heads with inline plasma units to future-proof VOC compliance. Regional governments provide energy-efficiency grants, cushioning operating costs for new curing ovens. As converted tonnage climbs, the silicone-coated paperboard packaging market benefits from shorter logistics chains that cut transit time for fast-turn food sectors.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Volatile silicone-polymer feedstock prices | -0.7% | Global, with APAC manufacturing concentration | Short term (≤ 2 years) |

| Energy-intensive curing ovens inflating Scope-1 emissions | -0.5% | EU and North America with carbon pricing | Medium term (2-4 years) |

| Narrow repulpability window for high-coat-weight grades | -0.4% | Global, with EU circular economy focus | Long term (≥ 4 years) |

| Competing bio-barrier (starch, PVOH) technologies maturing | -0.6% | Global, with faster adoption in Europe | Medium term (2-4 years) |

| Source: Mordor Intelligence | |||

Volatile Silicone-Polymer Feedstock Prices

Dimethylsiloxane monomer trades remain vulnerable to outages at specialty plants that cluster in China, South Korea, and Germany. Wacker Chemie notes margin compression whenever upstream energy spikes raise chlorosilane input costs, prompting quarterly price surcharges that ripple through the coating supply chain. Bio-based silicone additives derived from corn ethanol offer diversification but still carry cost premiums of 15%–18%, limiting their buffer role. Converters often hedge with multi-month inventory, yet rising working-capital requirements strain smaller coaters and may deter new entrants from scaling capacity.

Energy-Intensive Curing Ovens Inflating Scope-1 Emissions

Solventless and solvent-based systems demand thermal curing at 150 °C–200 °C to cross-link silicone, drawing heavily on natural-gas or steam grids. Mills pursuing 2030 science-based targets must therefore offset these emissions via boiler upgrades or renewable energy PPAs. Billerud’s recovery-boiler retrofit illustrates the scale of capital outlay required to shave megawatts from energy profiles. Carbon-pricing regimes in the EU add a direct cost overlay, shrinking margin windows for high-coat-weight SKUs.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Coating Technology: Solventless Dominance Drives Environmental Compliance

Solventless formulations commanded 58.21% of the silicone-coated paperboard packaging market share in 2024 and continue to anchor mill production planning because they emit almost no VOCs during curing. Water-based emulsions, however, are pacing fastest at an 8.60% CAGR as converters in densely populated zones pivot to meet occupational exposure limits tied to solvent vapors. The silicone-coated paperboard packaging market size linked to water-based lines is expected to rise from USD 0.82 billion in 2025 to USD 1.24 billion by 2030, underscoring a tangible shift in capital allocation toward low-emission assets. Innovations such as inline plasma activation enable coat-weight reductions that cushion feedstock cost swings while preserving release force benchmarks below 2 N/cm.

Despite regulatory advantages, water-based systems sometimes underperform in high-temperature bakery uses, maintaining a niche for solvent-based variants where oven-bake reheat cycles exceed 200 °C. Mills hedge risk by installing dual-station coaters capable of switching between solventless and solvent-based chemistries with minimal downtime. Stora Enso and Felix Schoeller each commissioned such hybrid lines in 2024, citing customer preference for supply-chain flexibility. Through 2030, R&D labs are likely to converge on silane-modified aqueous dispersions that close the heat-seal gap, potentially accelerating the water-based share even further.

By End-Use Industry: Food Service Evolution Reshapes Demand Patterns

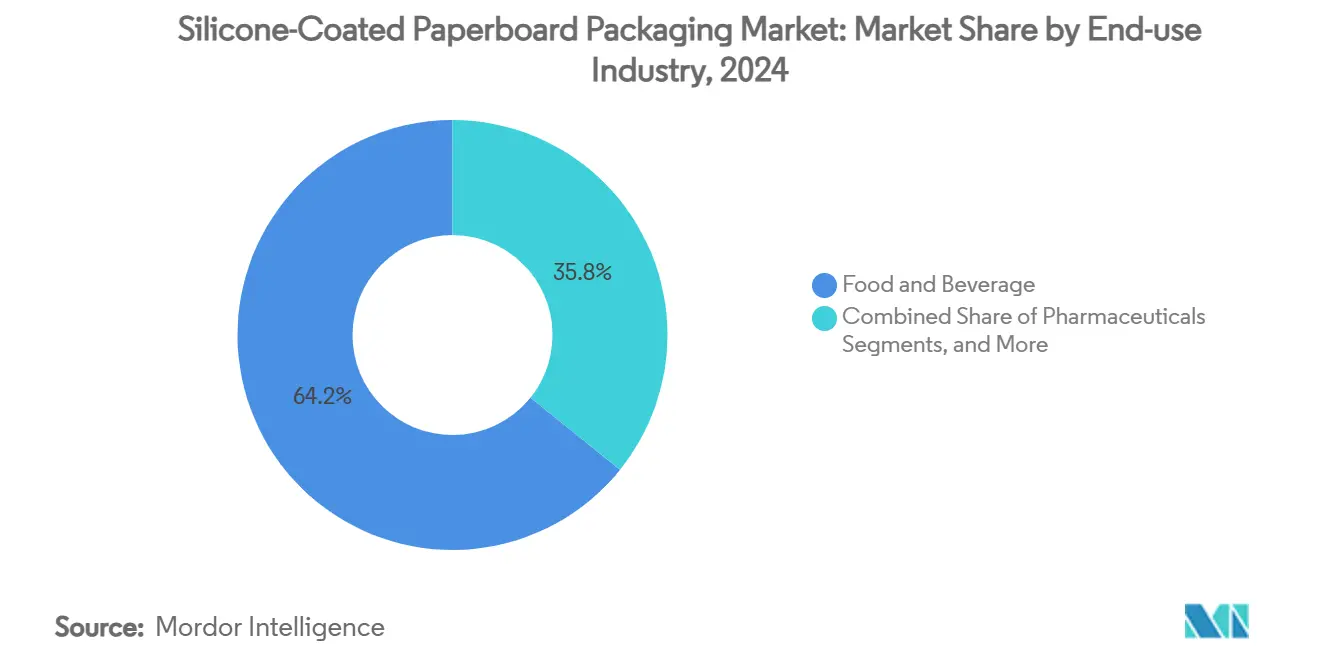

Food and beverage converters consumed 64.21% of total coated board tonnage in 2024, translating to a silicone-coated paperboard packaging market size of USD 2.20 billion at the mill gate. Meal-kit and take-away segments, though smaller, are charting the highest trajectory at 6.90% CAGR on expanding urban density and shift-work lifestyles. These formats prioritize microwave resilience, leading brand owners to specify board that can endure 1000 W heating without blistering.

Pharmaceutical inserts and personal-care unit cartons adopt silicone release liners for tamper-evidence but grow more modestly at 2%–3% annually. Industrial sectors like self-adhesive graphics add incremental demand for high-slip liners compatible with UV-cured inks. E-commerce folding boxboard incorporating silicone spot-coating for tear-strip functionality emerged in late 2024 and already secures pilot volumes with multinational apparel labels. Collectively, these use-cases diversify the silicone-coated paperboard packaging industry revenue base, buffering cyclical swings tied to single markets.

Geography Analysis

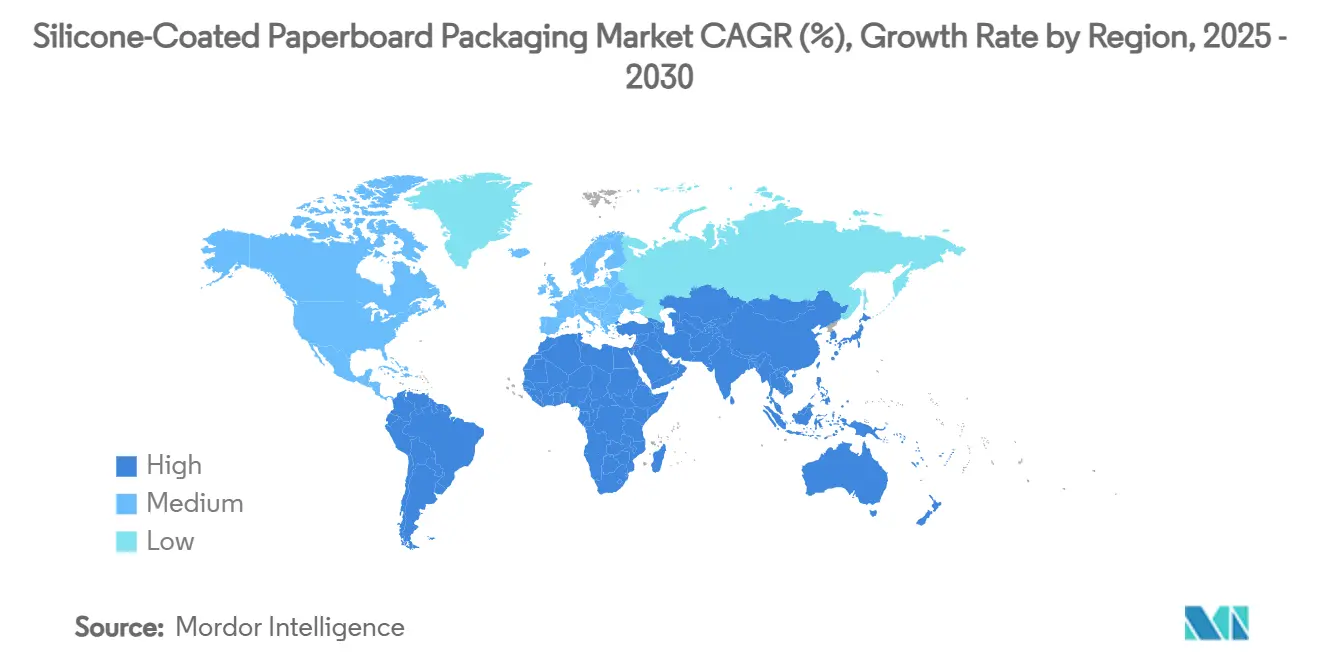

Asia-Pacific generated 41.21% of global revenue in 2024, roughly USD 1.41 billion, benefiting from integrated supply networks stretching from chlorosilane feedstock to finished folding cartons. China, Japan, and South Korea anchor demand, aided by robust food-delivery ecosystems and favorable utility costs that keep curing expenses manageable.

South America, led by Brazil and Chile, records the fastest trajectory at 6.70% CAGR as pulp-rich economies leverage competitive fiber costs and pro-recycling legislation. Government investment grants aimed at bio-based industries streamline permitting for new silicone-coating assets, enabling regional mills to capture export orders from North America during capacity crunches.

Asia-Pacific maintains leadership through 2025 thanks to combined advantages in raw fiber, silicone feedstock, and a booming quick-service sector that values grease-proof performance. Startup volumes from new Chinese solventless lines find immediate offtake in domestic meal-delivery channels that dispatch more than 70 million orders daily. Governments in India and Indonesia relax foreign-ownership caps in paperboard to spur inward investment, a policy that accelerates technology transfer for state-of-the-art coaters.

Europe experiences steady progress anchored by regulatory certainty. The silicone-coated paperboard packaging market size for the region was USD 0.97 billion in 2025 and is forecast to cross USD 1.18 billion by 2030, reflecting a 4.0% CAGR as recyclability mandates solidify purchasing criteria. Germany and France top consumption owing to sophisticated grocery networks that adopt PFAS-free solutions ahead of statutory deadlines. Carbon pricing, however, keeps pressure on mills to reduce energy intensity, accelerating adoption of plasma curing pilots.

North America sees mid-single-digit growth as e-commerce automation heightens demand for slip-coated papers. California’s regulatory enforcement catalyzes early adoption across U.S. West Coast converters, while Canada aligns barrier performance specifications with FDA norms, facilitating continental supply-chain planning. Mexico’s rising middle class and proximity to U.S. quick-service chains open an additional vector, prompting global brands to localize folding boxboard production south of the border.

Competitive Landscape

The silicone-coated paperboard packaging market comprises a dozen global producers alongside regional specialists, yielding moderate concentration. International Paper, WestRock, and Graphic Packaging integrate pulp mills with multiple silicone coating lines, enabling cost synergies and rapid scale-up when legislation triggers demand spikes. Their combined footprint exceeds 45% of the world's coated board tonnage, giving them leverage in long-term supply contracts.

European players such as Stora Enso, Billerud, and Mondi invest heavily in solventless technology and post-curing energy recovery. Stora Enso’s EUR 1 billion (USD 1.08 billion) Oulu conversion brings 750,000 tpa of new capacity that targets PFAS-free food packaging in both EU and U.S. markets. Mondi’s TrayWrap kraft substrate, launched mid-2024, demonstrates how fiber substitution strategies blend with silicone spot-coating to replace polyolefin shrink film.[3]Mondi Investor Relations, “Half-Year Results 2024,” mondigroup.com

Innovation ecosystems center on plasma surface engineering, with equipment providers partnering directly with mills to co-develop low-grammage coatings. Start-ups focusing on digital-print compatible release liners enter joint-ventures with Asian SBS manufacturers, securing market access while de-risking scale-up. Feedstock giants like Wacker Chemie and Dow Silicones reinforce position through forward-integrated technical service that assists converters in navigating food-contact migration testing. Taken together, these dynamics suggest rising but manageable competitive intensity framed around regulatory conformity rather than price wars.

Silicone-Coated Paperboard Packaging Industry Leaders

Graphic Packaging Holding Company

International Paper Company

Metsä Board Corporation

Stora Enso Oyj

Smurfit Westrock PLC

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- March 2025: Stora Enso commenced operations of a new consumer packaging board line at Oulu, Finland; the EUR 1 billion (USD 1.08 billion) facility adds 750,000 tpa of folding box board and coated unbleached kraft capacity.

- February 2025: The European Union enacted Regulation EU 2025/40 to tighten recyclability and PFAS restrictions across all packaging classes.

- December 2024: Billerud unveiled new financial targets and SEK 1.4 billion (USD 0.13 billion) North American mill upgrades to accelerate paperboard transition

- September 2024: California approved AB 347, establishing a phased PFAS enforcement scheme for plant-based food packaging.

Global Silicone-Coated Paperboard Packaging Market Report Scope

| Solventless Silicone |

| Solvent-based Silicone |

| Water-based Silicone Emulsion |

| Food and Beverage |

| Pharmaceuticals |

| Personal Care and Cosmetics |

| Industrial and Others |

| North America | United States | |

| Canada | ||

| Mexico | ||

| South America | Brazil | |

| Argentina | ||

| Rest of South America | ||

| Europe | Germany | |

| United Kingdom | ||

| France | ||

| Italy | ||

| Spain | ||

| Russia | ||

| Rest of Europe | ||

| Asia-Pacific | China | |

| Japan | ||

| India | ||

| South Korea | ||

| Australia | ||

| Rest of Asia-Pacific | ||

| Middle East and Africa | Middle East | Saudi Arabia |

| United Arab Emirates | ||

| Turkey | ||

| Rest of Middle East | ||

| Africa | South Africa | |

| Nigeria | ||

| Rest of Africa | ||

| By Coating Technology | Solventless Silicone | ||

| Solvent-based Silicone | |||

| Water-based Silicone Emulsion | |||

| By End-use Industry | Food and Beverage | ||

| Pharmaceuticals | |||

| Personal Care and Cosmetics | |||

| Industrial and Others | |||

| By Geography | North America | United States | |

| Canada | |||

| Mexico | |||

| South America | Brazil | ||

| Argentina | |||

| Rest of South America | |||

| Europe | Germany | ||

| United Kingdom | |||

| France | |||

| Italy | |||

| Spain | |||

| Russia | |||

| Rest of Europe | |||

| Asia-Pacific | China | ||

| Japan | |||

| India | |||

| South Korea | |||

| Australia | |||

| Rest of Asia-Pacific | |||

| Middle East and Africa | Middle East | Saudi Arabia | |

| United Arab Emirates | |||

| Turkey | |||

| Rest of Middle East | |||

| Africa | South Africa | ||

| Nigeria | |||

| Rest of Africa | |||

Key Questions Answered in the Report

What is the current size of the silicone-coated paperboard packaging market?

The market is valued at USD 3.43 billion in 2025 and is projected to reach USD 4.38 billion by 2030.

Which coating technology dominates the market today?

Solventless silicone leads with 58.21% 2024 market share thanks to its low-VOC profile and strong food-contact performance.

Which end-use segment is growing fastest?

Meal-kit and take-away formats are advancing at a 6.90% CAGR due to rising urban demand for convenient, grease-resistant packaging.

Why are regulators pushing brands toward silicone-coated paperboard?

EU and U.S. laws are phasing out PFAS and demanding higher recyclability; silicone coatings deliver barrier performance while keeping fiber recoverable.

Which region is expanding quickest?

South America is forecast to grow at 6.70% CAGR through 2030, benefiting from new mill investments and supportive recycling policies.

Page last updated on: