Ovenable And Microwaveable Ready-Meal Packaging Market Size and Share

Market Overview

| Study Period | 2019 - 2030 |

|---|---|

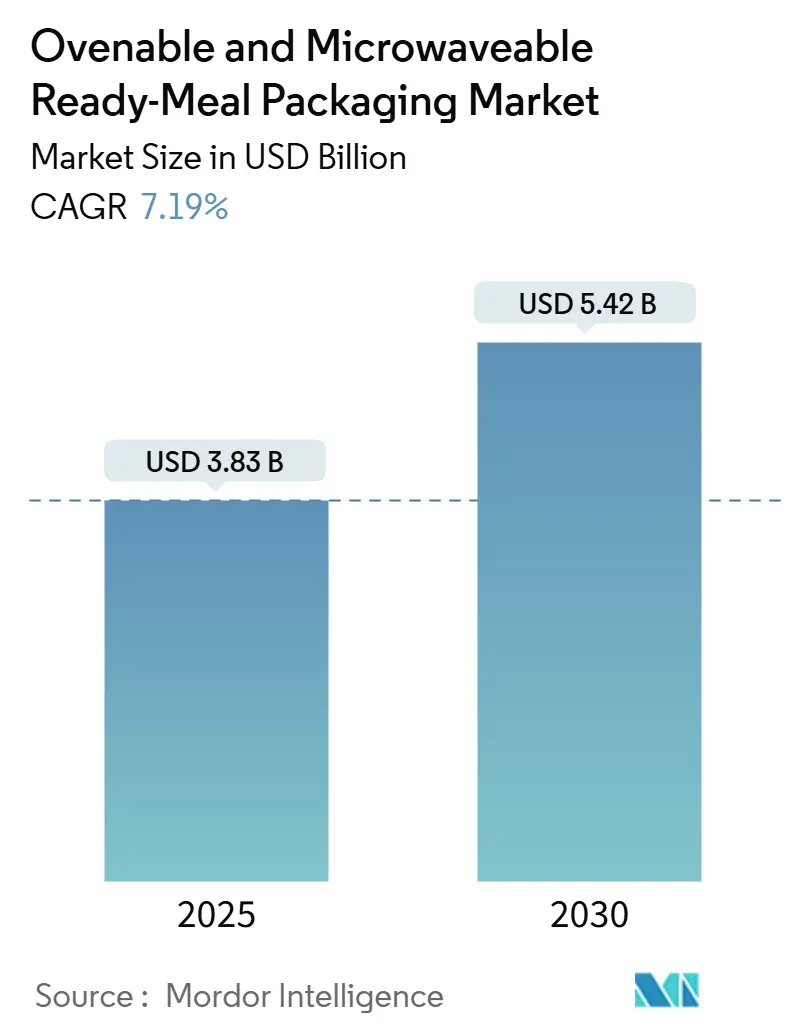

| Market Size (2025) | USD 3.83 Billion |

| Market Size (2030) | USD 5.42 Billion |

| Growth Rate (2025 - 2030) | 7.19% CAGR |

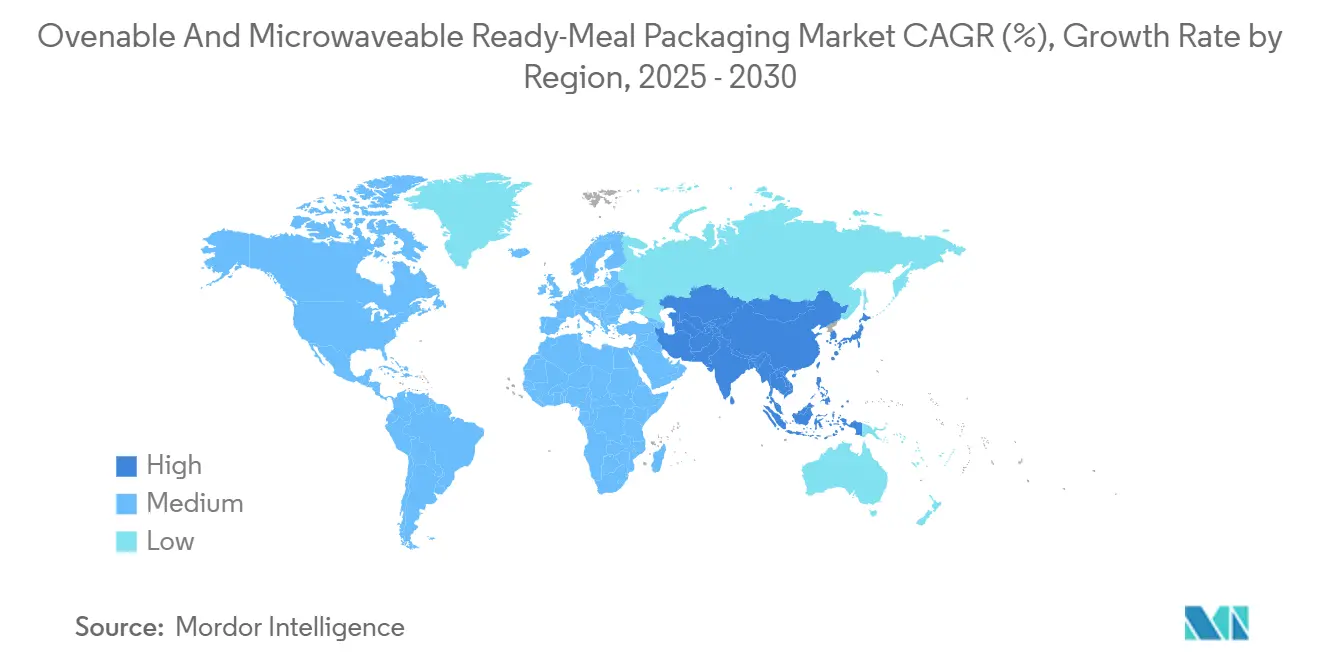

| Fastest Growing Market | Asia Pacific |

| Largest Market | North America |

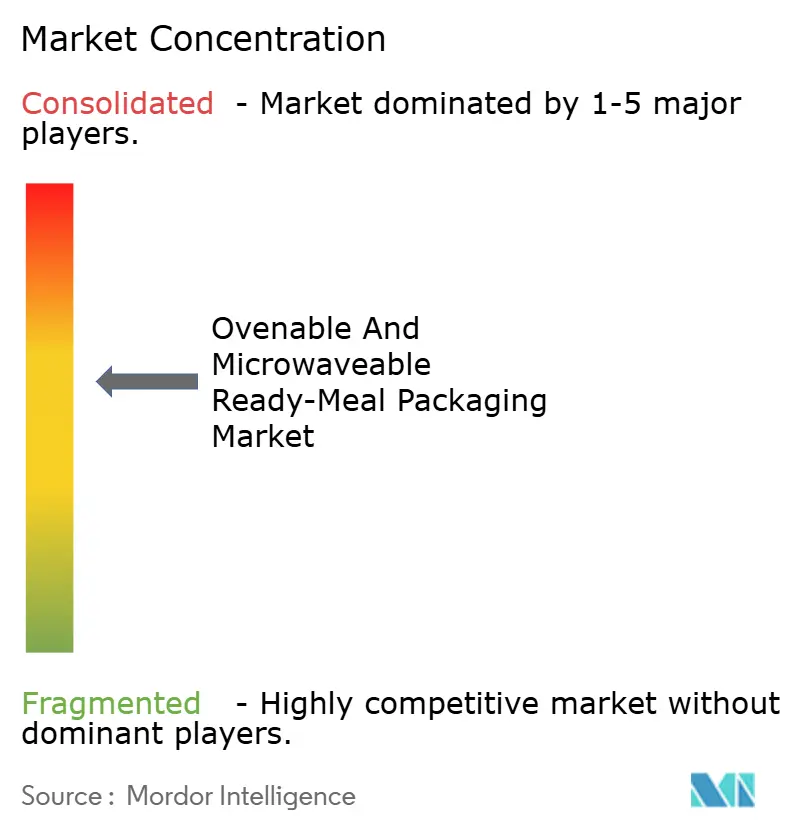

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

Ovenable And Microwaveable Ready-Meal Packaging Market Analysis by Mordor Intelligence

The ovenable and microwaveable ready-meal packaging market size is valued at USD 3.83 billion in 2025 and is forecast to reach USD 5.42 billion by 2030, expanding at a 7.19% CAGR. Consistent uptake of dual-ovenable CPET trays, retailers’ recycled-content requirements, and fast-rising meal-kit delivery volumes form the backbone of this growth path. Manufacturers benefit from higher‐margin chilled ready-meal formats that rely on advanced barrier films, while consumers reward packaging that accommodates both microwave and conventional ovens without compromising food safety. Regulatory initiatives in North America, Europe, and the Asia-Pacific region are accelerating the transition toward mono-material solutions, spurring R&D budgets and capital spending on new thermoforming lines. At the same time, virgin polymer price volatility and PFAS restrictions continue to test supply-chain agility, motivating converters to diversify raw-material portfolios and pursue chemical recycling partnerships.

Key Report Takeaways

- By packaging technology, dual-ovenable solutions commanded 52.44% revenue share in 2024, and the segment is projected to post the fastest 13.82% CAGR through 2030.

- By geography, North America led with 32.82% of the ovenable and microwaveable ready-meal packaging market share in 2024, whereas Asia-Pacific is set to clock the highest 10.61% CAGR to 2030.

- By packaging material, CPET held 38.03% of the ovenable and microwaveable ready-meal packaging market size in 2024, while paper-based mono-materials are slated to grow at an 11.23% CAGR during the outlook period.

- By packaging format, trays contributed 46.23% of 2024 revenue, yet pouches and bags are forecast to accelerate at a 12.92% CAGR owing to meal-kit logistics advantages.

- By end-user channel, retail outlets took 57.03% share in 2024, and online meal-kit platforms are expected to expand at a brisk 15.71% CAGR through 2030.

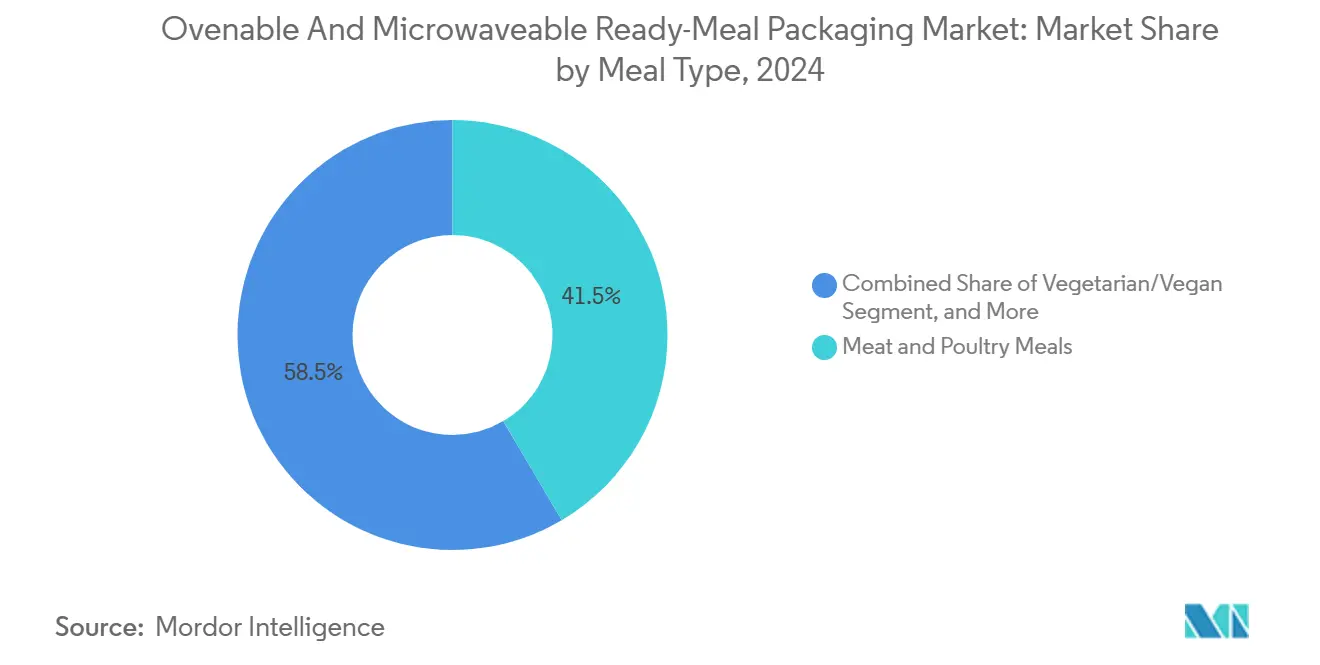

- By meal type, meat and poultry retained 41.51% share in 2024, while vegetarian and vegan offerings are on track for a 14.32% CAGR, reshaping protein packaging requirements.

Global Ovenable And Microwaveable Ready-Meal Packaging Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Shift From Frozen to Chilled Ready-Meals | +1.2% | Global, early adoption in North America and Europe | Medium term (2-4 years) |

| Surge in Dual-Ovenable CPET Tray Adoption | +1.8% | North America and Europe, expanding to Asia-Pacific | Short term (≤ 2 years) |

| Retailers’ Recyclable-Content Mandates | +0.9% | Europe and North America, spillover to Asia-Pacific | Long term (≥ 4 years) |

| Rapid Growth of Meal-Kit Delivery Services | +1.5% | Global, concentrated in urban centers | Medium term (2-4 years) |

| Food Safety Regulations Favouring Hermetic Seals | +0.7% | Global, stricter in developed markets | Long term (≥ 4 years) |

| Emerging “Heat-and-Eat” Demand in SE-Asia | +1.1% | Asia-Pacific core, especially Southeast Asia | Medium term (2-4 years) |

| Source: Mordor Intelligence | |||

Shift From Frozen to Chilled Ready-Meals

Retailers are replacing frozen entrées with chilled variants that deliver fresher sensory cues and lower energy intensity across the cold chain. Chilled meals require oxygen-scavenging films, modified-atmosphere sealing, and dual-ovenable tray geometry that maintains product integrity during store-to-home transit. Large U.S. grocers have already shifted shelf facings toward chilled SKUs, prompting converters to scale multilayer high-barrier lines that achieve up to 30-day unopened shelf life SEA.[1]Sealed Air, “SEE and Ossid Create Strategic Partnership to Offer New Sustainable Tray Overwrapping Total Solution,” sealedair.com The trend raises tray volumes because chilled meals rely on rigid formats for leak protection, and it magnifies demand for liner-less paperboard sleeves that enhance shelf appeal while remaining recyclable. Converter service models now integrate in-line vision systems to guarantee hermetic seals that comply with HACCP standards, reducing recall risk and supporting brand reputation.

Surge in Dual-Ovenable CPET Tray Adoption

CPET’s crystalline structure resists warping at 220 °C, enabling consumers to brown lasagna in an oven one night and reheat leftovers in a microwave the next day. European thermoformers added more than 50,000 tons of CPET capacity between 2024 and 2025, and comparable expansions are underway in the United States to meet private-label ready-meal contracts.[2]Faerch Group, “Faerch expands CPET capacity to meet growing dual-ovenable demand,” faerch.com CPET’s inherent recyclability in PET streams aligns with Extended Producer Responsibility fees that penalize non-sortable multilayers, driving brand conversions even in price-sensitive SKUs. Visual clarity improvements and dark-food recycling logos printed on the base have further strengthened shopper confidence, pushing premium meal producers to accept modest packaging cost uplifts in exchange for fewer customer complaints.

Retailers’ Recyclable-Content Mandates

European supermarkets now specify a minimum 30% post-consumer resin in own-label packaging from 2026, compelling suppliers to qualify food-grade rPET in CPET and explore high-heat paperboard alternatives that resist delamination when exposed to steam. U.S. retailers have adopted parallel policies through voluntary associations, pressuring converters to secure supply contracts with PET recyclers and to invest in de-inking systems for dark trays. Packaging R&D has shifted toward mono-PET lidding films that weld to CPET without tie layers, simplifying end-of-life separation.[3]Greenyard, “Shelf revolution: Greenyard and Tetra Pak partner for more sustainable packaging,” greenyard.group Compliance costs favor larger players with vertically integrated recycling assets, widening the gap between global majors and smaller regional thermoformers.

Rapid Growth of Meal-Kit Delivery Services

Meal-kit shipments topped 1 billion boxes globally in 2024, and urban consumers now expect portion-controlled ingredients delivered in packaging that doubles as a cooking vessel. Providers specify lightweight dual-ovenable trays that nest efficiently in corrugated outers, reducing dimensional-weight charges while withstanding chilled gel packs. Recipe cards highlight “oven-ready” convenience, making straightforward heating the most cited service benefit among subscribers. As courier networks pursue net-zero targets, meal-kit firms prioritize mono-material solutions that are curbside recyclable, creating growth avenues for paper-based trays with plant-derived coatings. Packaging line OEMs have responded with robotic pick-and-place cells that automate variable SKU packing, cutting changeover times to under 8 minutes.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Recycling Infrastructure Gaps for Multilayer Films | -1.3% | Global, acute in developing markets | Long term (≥ 4 years) |

| Volatility in Virgin Polymer Prices | -0.8% | Global, cost-sensitive segments most affected | Short term (≤ 2 years) |

| Consumer Concerns Over PFAS and Microwave Toxins | -0.6% | North America and Europe, rising in Asia-Pacific | Medium term (2-4 years) |

| High Capital Cost of CPET Thermo-forming Lines | -0.4% | Global, impacts small and mid-size converters | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

Recycling Infrastructure Gaps for Multilayer Films

Chemical recycling pilots have achieved 99% polymer purity, yet throughput remains below 20,000 tons annually, a fraction of multilayer waste generated each year.[4]Bavarian Research Alliance, “EU Project CIRCULAR FoodPack shows ways to make flexible food packaging circular,” bayfor.org Developing markets lack collection and sorting capacity, forcing brand owners to incur export taxes on non-recyclable waste or redesign structures for mechanical workflows. Funding shortfalls delay industrial-scale delamination plants and postpone circularity targets announced by FMCG companies. The infrastructure deficit curtails multilayer flexible adoption in meal-kits and undermines converter margin recovery plans.

Volatility in Virgin Polymer Prices

Spot PET and PP prices swung more than 35% during 2024, inflating packaging costs and triggering emergency surcharges from mid-tier converters. Ready-meal producers renegotiated supply contracts quarterly, disrupting production planning and elevating working-capital needs. Smaller converters without futures hedges accepted lower utilization rates to avoid overpricing trays that compete with store-brand canned meals. This volatility fuels demand for recycled inputs, yet food-grade rPET trades at a 10-15% premium, limiting substitution in value-oriented SKUs.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Packaging Material: CPET Leads as Paper Accelerates

CPET retained 38.03% of 2024 revenue thanks to dependable dual-ovenable performance and compatibility with high-speed fill-seal lines. Within this premium bracket, CPET products accounted for USD 1.46 billion of the ovenable and microwaveable ready-meal packaging market size. Ongoing line expansions and proprietary color-change indicators that signal full reheat maturity will reinforce CPET’s dominance through 2030.

Paper-based mono-materials posted the fastest 11.23% CAGR, supported by fiber-barrier R&D that meets 200 °C oven thresholds, plus retailer mandates that grade suppliers on recyclability scores. Cost differentials have narrowed to less than 8 cents per unit for medium portions, enabling private-label adoption in Germany, the United Kingdom, and selected U.S. grocers. The emerging paper tier challenges aluminum trays in bake-at-home pastry kits and competes directly with PP bowls in microwave snacks. Supplier competition now pivots on heat-seal varnish innovations that do not hinder curbside recycling, an area where Scandinavian mills hold patent-protected edge coatings.

By Packaging Format: Trays Hold Ground While Flexibles Gain

Rigid trays represented 46.23% of 2024 demand equal to USD 1.78 billion within the ovenable and microwaveable ready-meal packaging market. Form-fill-seal compatibility, portion control, and merchandizing aesthetics underpin their longevity. Value engineering has shaved tray gram weights by 7-9% without compromising stiffness, enabling producers to align with carbon disclosures.

Pouches and bags, although only 13.6% of today’s volume, deliver a 12.92% CAGR as meal-kit platforms favor flexibles for spice blends, sauces, and sous-vide components. Stand-up pouches integrate laser-sintered valves that vent steam, letting consumers microwave contents without separate plates. Their lower cube improves last-mile economics, explaining why meal-kit operators push suppliers toward mono-PE laminations. Investments in pouch filling lines that run 140 packs per minute have therefore escalated in Spain, the United States, and South Korea.

By End-User Channel: Retail Still Rules Amid Digital Disruption

Traditional supermarkets controlled 57.03% of global volume in 2024, or USD 2.19 billion, leveraging chilled cabinets and strong private-label propositions. Category resets place chilled meals adjacent to fresh deli, enhancing impulse conversion. Packaging vendor scorecards increasingly tie tray performance to in-store shrink targets, leading to anti-fog lid specifications and leak-proof crimp profiles.

Online meal-kit services, expanding at a 15.71% CAGR, reshape pack geometry to balance fridge fit and courier weight limits. Their rigid quality protocols favor ISO-certified suppliers that prove temperature hold within three-day transit. Converters bundle carbon calculators to help platforms publish box-level footprint metrics, satisfying eco-conscious subscribers.

By Meal Type: Plant-Based Boom Redefines Specs

Meat and poultry entrées dominated with 41.51% share, approximately USD 1.60 billion of the ovenable and microwaveable ready-meal packaging market size. These products demand high-oxygen barriers to retard lipid oxidation and odor ingress, sustaining multilayer EVOH structures.

Vegetarian and vegan SKUs are projected to grow at 14.32% CAGR, intensifying the call for plant-oil-resistant coatings within paper trays. Texture variability across soy, pea, and mushroom proteins necessitates wider sealing windows during retort, prompting trials of bio-based adhesive layers that withstand temperature spikes. Packaging briefs for plant-based lines also specify transparent lids that showcase colorful grains and vegetables, countering consumer skepticism about processed analogs.

By Packaging Technology: Dual-Ovenable Sets the Pace

Dual-ovenable formats captured 52.44% share in 2024, translating to USD 2.02 billion, underscoring their centrality to the ovenable and microwaveable ready-meal packaging market. Suppliers have optimized crystallinity to shorten CPET cooling cycles, boosting line throughput by 15% and trimming unit costs. Microwave-only packs maintain relevance in single-serve lunches, yet brands increasingly transition hero SKUs to dual-ovenable to simplify inventory and enhance consumer flexibility.

Conventional-oven-only solutions cling to niche gourmet offerings requiring browning effects that microwaves cannot replicate. However, R&D is exploring laminate-free coated paper trays that achieve crispiness in combi-ovens while tolerating brief microwave reheats, blurring historical distinctions between technology silos.

Geography Analysis

North America contributed 32.82% of global revenue in 2024 thanks to widespread microwave saturation, sophisticated cold chains, and a culture that values convenience without sacrificing perceived freshness. The region’s regulatory frameworks, including FDA migration limits and state-level PFAS bans, push suppliers toward compliant high-heat resins and recyclable mono-structures. Recent retail mandates for 30% recycled content in private-label packaging are accelerating CPET-rPET blend qualification, while meal-kit subscriptions maintain double-digit growth in urban corridors. Investments by U.S. thermoformers in vision-guided trim systems aim to shrink labor costs and hit landfill-diversion scorecards.

Asia-Pacific will deliver the fastest 10.61% CAGR through 2030 as rising urban incomes and smaller households fuel take-up of heat-and-eat meals. China leads absolute volume, yet Southeast Asian markets such as Thailand and Indonesia register the steepest adoption curves, aided by convenience-store chains rolling out chilled-meal sections. Packaging localization is critical; for example, Korean kimchi rice bowls demand odor-barrier lids and steam-vented films that survive 800-watt microwaves without blistering. Regulatory clarity is emerging on recycled inputs, with Japan piloting food-grade rPET loops that may soon serve regional CPET lines.

Europe, a mature but innovation-driven arena, accounts for roughly 28% of global spend. Stringent Packaging and Packaging Waste Regulation proposals spur rapid material redesign, while consumers exhibit low tolerance for non-recyclable trays. Germany and the United Kingdom mandate on-pack recycling labels that guide curbside sorting, compressing the timeline for mono-material conversions. CPF (conventional plastic fees) across Benelux markets penalize multilayers, tipping cost arithmetic toward CPET and coated fiber. Retailers experiment with digital watermarking to enhance PET stream accuracy, and early results report 99% detection rates under near-infrared sorting lines.

Middle East and Africa and South America remain emerging frontiers, contributing smaller shares yet presenting long-run upside as cold-chain logistics improve. Gulf retailers introduce ready-meal aisles in hypermarkets frequented by expatriate workforces, while Brazilian frozen-food majors pilot chilled lasagna in recyclable PET trays to capture premium margins.

Competitive Landscape

The ovenable and microwaveable ready-meal packaging market is moderately concentrated. The top five converters, including Amcor, Sealed Air, Mondi, Faerch, and Sabert, collectively command about 55-60% revenue, while regional specialists serve niche protein or cuisine categories. Scale advantages manifest in lower resin procurement costs and faster regulatory compliance approvals. Integrated players bundle design, tray production, and lidding films, anchoring multiyear supply contracts with global ready-meal brands.

Strategic differentiation now hinges on sustainability metrics. Amcor’s Recycle-Ready CPET program leverages internal PCR sourcing, cutting Scope 3 emissions for customer SKUs. Sealed Air’s partnership with Ossid introduces compostable overwrap coupled with leak-proof machinery, offering protein processors a turnkey line retrofit without throughput loss. Mondi’s launch of paper-based dual-ovenable trays extends its fiber expertise into high-heat niches, winning pilot orders from Scandinavian salmon brands.

Start-ups exploit white spaces such as bio-based coatings and advanced solvated recycling that recovers barrier polymers for tray-to-tray loops. Venture funding flows into artificial-intelligence inspection systems that detect seal contamination and foreign objects at 400 ppm resolution, reducing recalls. Patent publications covering solvent-less adhesive lamination and crystalline nucleating agents indicate sustained R&D activity despite margin pressures from polymer volatility.

Brand owners increasingly co-locate R&D centers with converter pilot lines to fast-track concept-to-commercial cycles, often within 12 months. This proximity enables iterative tests on oven-browning, microwave transparency, and shelf-life targets, shortening time-to-market for limited-edition recipes tied to streaming-platform promotions. Market entrants must navigate complex food-contact approval pathways that favor incumbents with established compliance portfolios.

Ovenable And Microwaveable Ready-Meal Packaging Industry Leaders

Amcor Plc

Sealed Air Corporation

Mondi Group

Huhtamaki Oyj

Graphic Packaging Holding Company

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- May 2025: Amcor won the UK Packaging Awards for its PrimeSeal Ovenable Flow Pack for meat, fish, and seafood products. The pack offers 100% hermetic sealing and self-venting technology, reduces labor and packaging components, and improves leak protection. It supports lightweighting and runs on high-speed VFFS lines

- April 2025: Sealed Air announced its CRYOVAC sustainable packaging solutions at IFFA 2025, focusing on packaging that integrates protection and ready recyclability. The company highlighted innovations targeted at meat processors and retailers, combining performance with sustainability-driven automation improvements.

- January 2025: Amcor introduced its OvenRite ovenable packaging, designed for convenience meals that go from refrigerator or freezer directly to oven. It features self-venting lids, microwave and oven safety up to 425°F, and printed films to eliminate labeling. The packaging aims to reduce cross-contamination risk and save prep and cleanup time for consumers and processors.

- November 2024: Amcor announced the completion of its USD 8.4 billion acquisition of Berry Global, creating a packaging powerhouse with expanded rigid and flexible capabilities.

Global Ovenable And Microwaveable Ready-Meal Packaging Market Report Scope

The Ovenable and Microwaveable Ready-Meal Packaging Market Report is Segmented by Packaging Material (CPET, Polypropylene, Paper and Board, Aluminum, Other Materials), Packaging Format (Trays, Bowls and Cups, Pouches and Bags, Lidding Films, Cartons and Sleeves), Meal Type (Meat and Poultry, Seafood, Vegetarian/Vegan, Bakery and Confectionery, Other), End-User Channel (Retail, Convenience Stores, Food-service, Online Meal-Kit), Packaging Technology (Microwave-Only, Conventional-Oven-Only, Dual-Ovenable), and Geography. The Market Forecasts are Provided in Terms of Value (USD).

| CPET (Crystalline PET) |

| Polypropylene (PP) |

| Paper and Board |

| Aluminum |

| Other Packaging Materials (PLA, PE, etc.) |

| Trays |

| Bowls and Cups |

| Pouches and Bags |

| Lidding Films |

| Cartons and Sleeves |

| Retail (Super / Hypermarkets) |

| Convenience and Forecourt Stores |

| Food-service (QSR, FSR, Cafés) |

| Online Meal-Kit and eGrocery |

| Meat and Poultry Ready-Meals |

| Seafood Ready-Meals |

| Vegetarian / Vegan Ready-Meals |

| Bakery and Confectionery |

| Other Meal Type |

| Microwave-Only |

| Conventional-Oven-Only |

| Dual-Ovenable |

| North America | United States | |

| Canada | ||

| Mexico | ||

| South America | Brazil | |

| Argentina | ||

| Rest of South America | ||

| Europe | Germany | |

| United Kingdom | ||

| France | ||

| Italy | ||

| Spain | ||

| Russia | ||

| Rest of Europe | ||

| Asia-Pacific | China | |

| Japan | ||

| India | ||

| South Korea | ||

| South-East Asia | ||

| Rest of Asia-Pacific | ||

| Middle East and Africa | Middle East | Saudi Arabia |

| United Arab Emirates | ||

| Turkey | ||

| Rest of Middle East | ||

| Africa | South Africa | |

| Nigeria | ||

| Rest of Africa | ||

| By Packaging Material | CPET (Crystalline PET) | ||

| Polypropylene (PP) | |||

| Paper and Board | |||

| Aluminum | |||

| Other Packaging Materials (PLA, PE, etc.) | |||

| By Packaging Format | Trays | ||

| Bowls and Cups | |||

| Pouches and Bags | |||

| Lidding Films | |||

| Cartons and Sleeves | |||

| By End-User Channel | Retail (Super / Hypermarkets) | ||

| Convenience and Forecourt Stores | |||

| Food-service (QSR, FSR, Cafés) | |||

| Online Meal-Kit and eGrocery | |||

| By Meal Type | Meat and Poultry Ready-Meals | ||

| Seafood Ready-Meals | |||

| Vegetarian / Vegan Ready-Meals | |||

| Bakery and Confectionery | |||

| Other Meal Type | |||

| By Packaging Technology | Microwave-Only | ||

| Conventional-Oven-Only | |||

| Dual-Ovenable | |||

| By Geography | North America | United States | |

| Canada | |||

| Mexico | |||

| South America | Brazil | ||

| Argentina | |||

| Rest of South America | |||

| Europe | Germany | ||

| United Kingdom | |||

| France | |||

| Italy | |||

| Spain | |||

| Russia | |||

| Rest of Europe | |||

| Asia-Pacific | China | ||

| Japan | |||

| India | |||

| South Korea | |||

| South-East Asia | |||

| Rest of Asia-Pacific | |||

| Middle East and Africa | Middle East | Saudi Arabia | |

| United Arab Emirates | |||

| Turkey | |||

| Rest of Middle East | |||

| Africa | South Africa | ||

| Nigeria | |||

| Rest of Africa | |||

Key Questions Answered in the Report

What is the projected value of ovenable and microwaveable ready-meal packaging in 2030?

The market is forecast to reach USD 5.42 billion by 2030, expanding at a 7.19% CAGR.

Which region will grow the fastest through 2030?

Asia-Pacific is set to record a 10.61% CAGR, the highest among all regions.

Why are dual-ovenable packages gaining popularity?

They let consumers heat meals in either microwaves or conventional ovens, enhancing convenience while meeting retailer mandates for versatile, recyclable formats.

How are retailer recycled-content rules affecting materials?

Supermarkets now require up to 30% post-consumer resin, steering converters toward CPET-rPET blends and paper-based mono-materials that are easily sorted and curbside recyclable.

What role do meal-kit services play in packaging demand?

Meal-kit providers, expanding at 15.71% CAGR, favor lightweight dual-ovenable trays and pouches that withstand chilled distribution and simplify home cooking.

Which packaging material is growing fastest?

Paper-based mono-materials are advancing at an 11.23% CAGR as fiber-barrier innovations achieve oven compatibility without sacrificing recyclability.

Page last updated on: