Automated Tray Packing Machinery Market Size and Share

Market Overview

| Study Period | 2019 - 2030 |

|---|---|

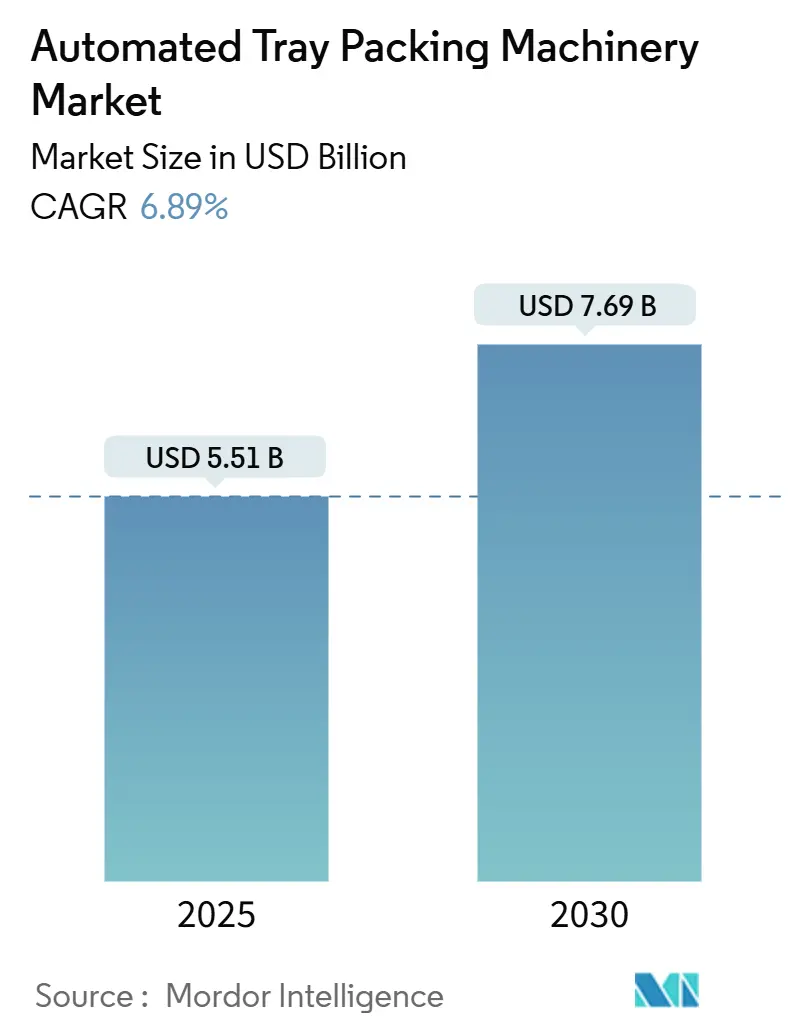

| Market Size (2025) | USD 5.51 Billion |

| Market Size (2030) | USD 7.69 Billion |

| Growth Rate (2025 - 2030) | 6.89% CAGR |

| Fastest Growing Market | Asia Pacific |

| Largest Market | Europe |

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

Automated Tray Packing Machinery Market Analysis by Mordor Intelligence

The automated tray packing machinery market size reached USD 5.51 billion in 2025 and is projected to increase to USD 7.69 billion by 2030, growing at a 6.89% CAGR. Labor scarcity, rising adoption of bio-based trays, and tightening global food-safety mandates are converging to accelerate capital spending on automated lines. Equipment suppliers capable of sealing paper, mono-plastic, and renewable polymer trays without throughput loss are gaining orders from both food and pharmaceutical clients. Modified-atmosphere and vacuum-skin formats are scaling rapidly as retailers seek longer shelf life, while AI-enabled condition monitoring reduces unplanned downtime and aligns with Industry 4.0 initiatives. A 15-25% increase in steel and aluminum prices since October 2024 continues to pressure end-user budgets, while also strengthening regional manufacturing plays designed to sidestep tariff exposure.

Key Report Takeaways

- By automation level, fully automatic equipment captured 48.01% of the automated tray packing machinery market share in 2024.

- By end-use industry, the automated tray packing machinery market size for the pharmaceutical segment is projected to grow at an 8.28% CAGR between 2025-2030.

- By tray material, bio-based substrates accounted for 8.98% of the automated tray packing machinery market size in 2025.

- By sealing technology, the automated tray packing machinery market size for modified-atmosphere and vacuum-skin systems is projected to grow at an 8.10% CAGR between 2025-2030.

- By geography, Europe captured 30.41% of the automated tray packing machinery market share in 2024.

Global Automated Tray Packing Machinery Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Labor-shortage led automation demand | +1.0% | Global, with acute impact in North America and Europe | Medium term (2-4 years) |

| Sustainability-driven shift to paper and mono-plastics | +0.8% | Europe and North America leading, Asia-Pacific following | Long term (≥ 4 years) |

| Stricter global food-safety regulations | +0.6% | Global, with regional compliance variations | Medium term (2-4 years) |

| Rise of ready-to-eat meals and grocery e-commerce | +0.5% | Asia-Pacific core, spill-over to global markets | Short term (≤ 2 years) |

| AI-enabled predictive maintenance boosting OEE | +0.4% | North America and Europe early adoption, Asia-Pacific scaling | Medium term (2-4 years) |

| Trade-bloc incentives for localized packaging machinery production | +0.3% | Regional focus on EU, USMCA, and ASEAN markets | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

Labor-Shortage Led Automation Demand

Manufacturers in Europe and North America reported that up to 73% of new packaging budgets in 2024 were channeled toward automation, as vacant operator positions remained unfilled for an average of six consecutive months.[1]PMMI, “Guide to Global Markets 2024,” PMMI, pmmi.org The automated tray packing machinery market, therefore, captures investment from processors seeking to maintain output without adding headcount. Mid-tier food companies are opting for semi-automatic tray sealers that can be manned by two workers instead of six, yet still achieve 25 cycles per minute. Larger plants with shift-length production runs are transitioning to fully automatic robotic loaders integrated with AI vision, which eliminates an additional 18% of manual touchpoints. As baby-boomer retirements accelerate, analysts expect labor-driven automation budgets to persist well beyond 2030, locking in a durable tailwind for the automated tray packing machinery market.

Sustainability-Driven Material Shifts to Paper and Mono-Plastics

Retailers, including Carrefour and Walmart, have issued supplier scorecards that reward trays made with single-polymer PET or fiber blends that achieve a recyclability rate of 90% or higher. Sealed Air and Eastman co-developed a compostable tray that can operate on existing sealing stations at 140 °C while maintaining gas-barrier performance. Such innovation compels machinery manufacturers to re-engineer heaters, anvils, and tooling to accommodate lower melt points and thicker flange tolerances. European packers piloting molded-fiber trays report that an ultrasonic seal head reduces energy consumption by 12% and prevents scorch marks that previously necessitated quality rework. The automated tray packing machinery market thus benefits from a dual mandate: raising sustainability scores while maintaining throughput.

Stricter Global Food-Safety Regulations

The EU Machine Regulation 2023/1230 introduces mandatory cybersecurity and AI-safety firmware audits starting January 2027. At the same time, China’s SAMR has ordered more frequent hygienic-design inspections at frozen food plants. Compliance complexity elevates the value proposition of line-level data capture, stainless-steel hygienic welds, and CIP-ready conveyors, which are integrated in every next-generation tray packer. FSMA rules in the United States now require cold chain data logs with a two-year retention window, a task far easier to automate than to perform manually. Collectively, these converging regulations amplify demand for equipment that can verify seal integrity, ensure product traceability, and prevent contamination, further advancing the automated tray packing machinery market.

Rise of Ready-to-Eat Meals and Grocery E-Commerce

Meal-kit operators and dark-store grocers in the Asia-Pacific region posted 21% order growth in 2024, adding pressure for single-serve MAP trays that can survive next-day courier networks. Automated lines offer the consistency and speed needed to deliver ninety thousand portions per shift without labor fatigue-related seal failures. Vacuum-skin trays packed with roasted proteins now command a 15% price premium in online channels, providing retailers with sufficient margin to justify higher capital expenditures on shelf-life-extending pack formats. As same-day delivery windows shrink to under four hours in tier-one Chinese cities, demand for leak-proof, presentation-grade trays produced on high-cycle equipment propels the automated tray packing machinery market well past legacy manual alternatives.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| High upfront CAPEX for fully automated lines | -0.9% | Global, SME impact acute | Short term (≤ 2 years) |

| Tariff-driven steel and aluminum cost volatility | -0.7% | Global | Medium term (2-4 years) |

| Shortage of skilled maintenance technicians | -0.5% | North America and Europe | Medium term (2-4 years) |

| Competition from flexible-pack alternatives | -0.4% | Global | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

High Upfront CAPEX for Fully-Automated Lines

Investment thresholds of USD 500,000 to USD 2 million for a turn-key robotic tray-sealing cell present a formidable hurdle for bakeries and regional meat processors that operate on thin margins. Although leasing programs and as-a-service models are emerging, equipment ownership still dominates, leaving SMEs exposed to interest rates that remain above 6% in most industrialized economies. The automated tray packing machinery market thus sees many processors upgrading via semi-automatic modules first before migrating to full robotics once payback is demonstrated. Suppliers offering modular tool sets and quick-swap magazines shorten changeover times and lower initial entry costs, helping temper but not remove CAPEX concerns.

Tariff-Driven Steel and Aluminum Cost Volatility

Since 2024, 25% tariffs on imported stainless-steel grades into the United States and 20% duties into the EU have added an average of USD 32,000 to a mid-range tray sealer bill of materials. Some buyers delayed purchase orders for two quarters until prices stabilized, shaving off near-term revenue for the automated tray packing machinery market. Manufacturers such as MULTIVAC responded by localizing frame fabrication at their Kansas and Wolfertschwenden plants, while their Asian rivals secured alternative supplies from Indonesia to bypass surcharges. The ability to quote stable delivery timelines and hedge raw material risk is quickly becoming a competitive differentiator in capex-sensitive bids.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Automation Level: Mid-Tier Processors Balance Flexibility with Throughput

In 2024, fully automatic lines commanded 48.01% of automated tray packing machinery market share, driven by high-volume frozen meal and pet-food plants that run three shifts per day. Yet semi-automatic systems recorded a faster 7.49% CAGR, illustrating how mid-sized dairies and ready-meal startups value tool-less changeovers that cut downtime from 45 minutes to 10 minutes. The automated tray packing machinery market size, attributed to semi-automatic equipment, is on track to exceed USD 2.6 billion by 2030 as operators deploy collaborative robots and AI vision as incremental upgrades rather than investing in monolithic lines. Footprint constraints in brownfield facilities also encourage step-wise automation strategies that fit existing floor plans.

The distinction between automation levels is blurring as servo-driven infeed belts and cloud-connected HMIs become standard even on entry models. Balluff-enabled condition monitoring demonstrated a 90% reduction in analytical labor at a U.S. confectionery plant, showing that smart-sensor suites are no longer exclusive to fully robotic cells.[2]Balluff, “Condition Monitoring for Packaging Machinery 2024,” Balluff, balluff.com As a result, procurement decisions increasingly rest on projected yearly volume rather than on technology availability. The automated tray packing machinery market will see higher specification overlap, with price-tier segmentation replacing binary automation labels.

By End-Use Industry: Pharmaceutical Compliance Drives Premium Features

The pharmaceutical sector is growing at an 8.28% CAGR through 2030, outpacing food processors, which nonetheless hold 42.60% of the revenue. Serialization mandates effective in the United States and EU require data-matrix printing and inline vision inspection, prompting drug-contract packagers to select high-precision servo sealers with ±0.2 mm positional accuracy. The automated tray packing machinery market size for pharma applications is anticipated to surpass USD 1.3 billion by 2030, driven by vaccine vial kitting and cell-therapy cold-chain formats.

Cross-industry adoption is evident as cosmetics brands demand pharmaceutical-grade cleanroom finishes to support sensitive skin formulations, while plant-based meat startups apply aseptic techniques originally developed for injectables. This cross-pollination supports equipment suppliers with portfolios that straddle both food and pharma regulations. The automated tray packing machinery industry benefits because premium compliance features built for medicines can be repurposed for high-margin consumer packaged goods without extensive redesign.

By Tray Material: Renewable Polymers and Fiber Blends Accelerate

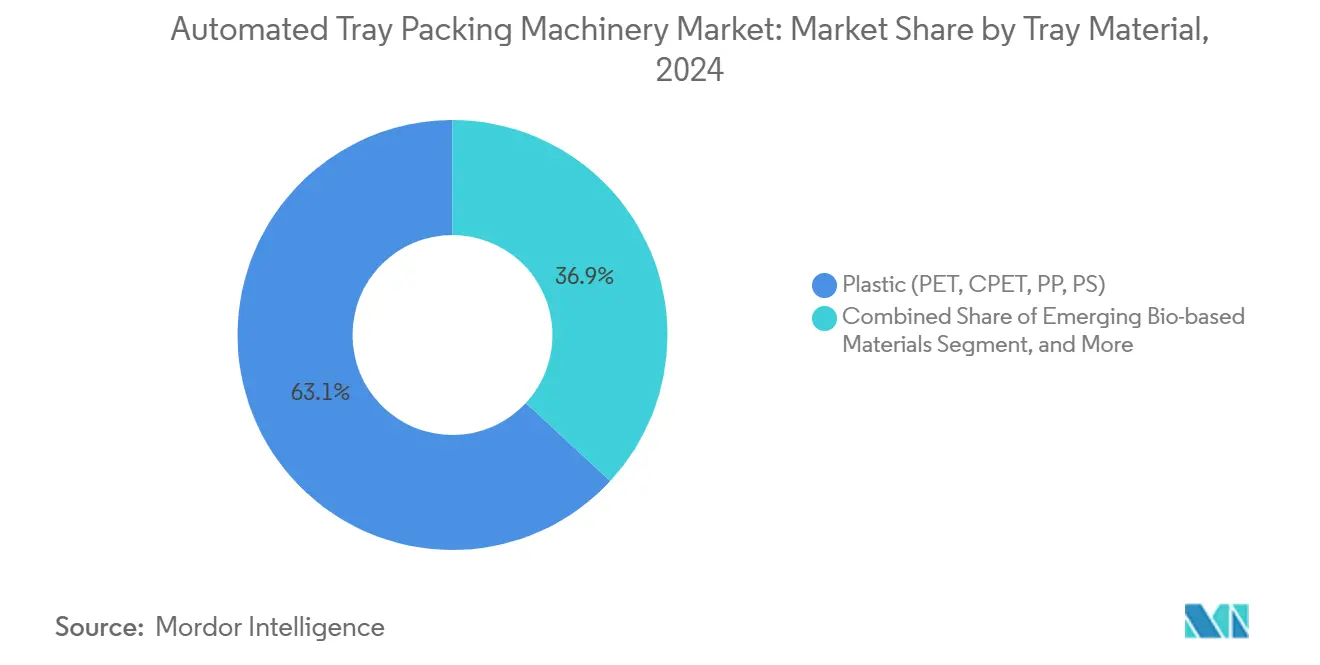

Plastic substrates still account for 63.12% of the automated tray packing machinery market share, but bio-based variants are scaling at an 8.98% CAGR as carbon-footprint scorecards become part of retailer listing contracts. Line trials with BASF ecovio trays required seal-jaw dwell times 22% longer than PET, pushing engineers to add predictive thermal balancing to avoid bottlenecks.

Fiber and mono-paperboard solutions gained acceptance after large UK retailers approved microwave-safe barrier lacquers that extend chilled shelf life to nine days. The automated tray packing machinery market size dedicated to fiber trays is expected to exceed USD 850 million by 2030. Aluminum remains the material of choice for premium pet food and airline catering packs where oxygen sensitivity and stack strength outweigh cost premiums, reinforcing the need for multi-substrate machinery platforms.

By Sealing Technology: MAP and Vacuum-Skin Secure Shelf Life Advantage

Heat sealing retains 53.01% of the automated tray packing machinery market share because of its simplicity and consistent cycle times. Yet modified-atmosphere packaging and vacuum-skin formats are expanding at 8.10% CAGR, particularly in seafood and red meat. Processors adopting vacuum-skin technology report a 3-day shelf life extension and a 1.4% shrink reduction, benefits that offset the 12% higher film costs.

The automated tray packing machinery market size aligned with MAP platforms is projected to exceed USD 2.1 billion by 2030, driven by high CO₂ emissions in poultry applications. ISO 22002-1:2025 introduces tighter seal validation rules, favoring ultrasonic and induction methods that deliver real-time seal-integrity data and enable automatic reject sorting. Consequently, the sealing-technology race is shifting from mechanical throughput to data-rich process control that satisfies auditors.

Geography Analysis

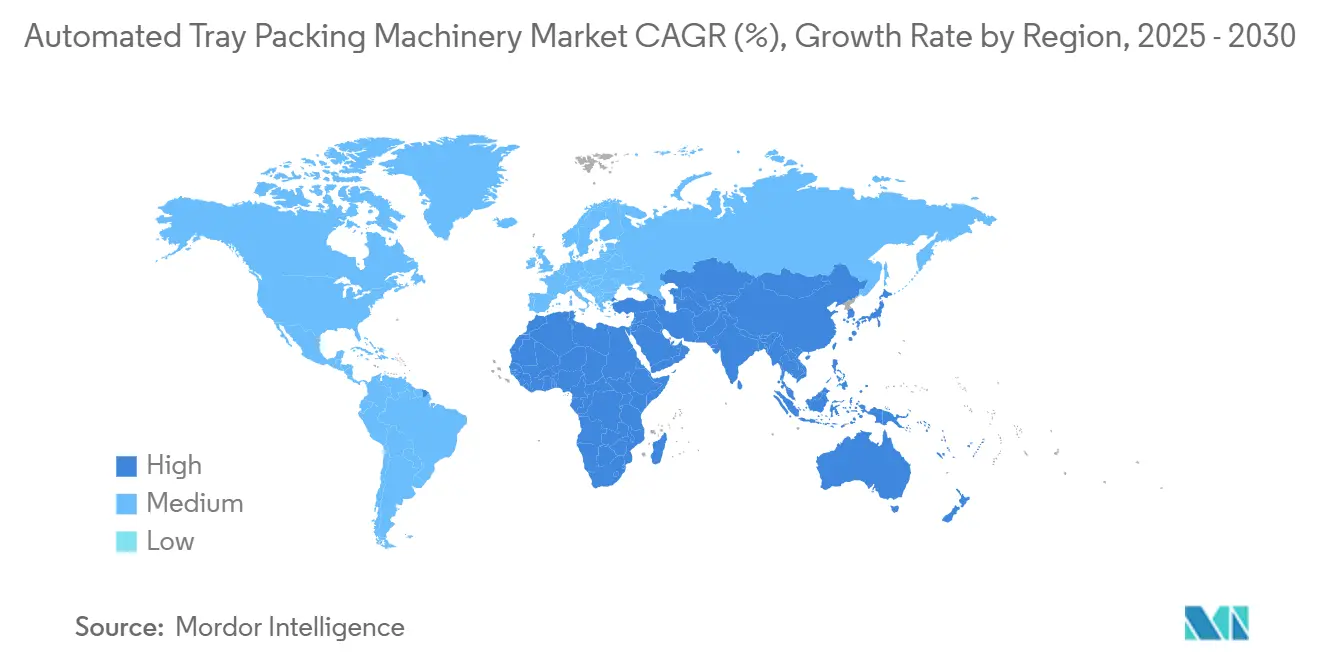

Europe maintained a 30.41% revenue share in 2024 as German, Italian, and Dutch machine builders leveraged Industry 4.0 design leadership. Italy posted EUR 9.2 billion (USD 10.1 billion) in packaging machinery turnover, with domestic clients alone accounting for an 8% increase in spending.[3]Italian Packaging Machinery Association, “Italian Packaging Machinery Market 2024 Growth,” UCIMA, ucima.it EU-wide sustainability directives accelerated demand for mono-material tray compatibility, giving European OEMs a technical edge in tailored tooling and low-energy seal systems. Machine Regulation 2023/1230 comes into force in 2027, likely triggering a replacement cycle for legacy servo drives and contributing to the momentum of the automated tray packing machinery market.

The Asia-Pacific region is the fastest-growing, with a 7.76% CAGR, driven by e-commerce food sales that surpassed USD 350 billion in 2025. MULTIVAC’s EUR 9 million (USD 9.9 million) plant in Ghiloth, India, offers three-week lead times for localized frames, helping processors avoid 25% import duties. China’s SAMR hygiene audits now require data-logged seal strength results, encouraging chilled-ready-meal factories to adopt automated tray packing machinery market solutions over manual heat guns. Southeast Asian shifts of electronics and textile supply chains also expand cold-chain infrastructure for factory canteens, producing new demand nodes for entry-level tray sealers.

North America remains steady as replacement cycles address aging fleets installed in 2011-2014. USMCA rules prompt near-shoring of protein processing to Mexico, boosting orders for 8-lane MAP sealers rated at 120 trays per minute. Yet import tariffs raised stainless-steel chassis costs, driving some buyers to negotiate dual sourcing with Canadian fabricators. Nevertheless, FSMA compliance remains a powerful tailwind, ensuring the automated tray packing machinery market stays essential for processors seeking audit readiness on demand.

Competitive Landscape

The automated tray packing machinery market features moderate concentration. The top five suppliers control approximately 58% of the global revenue, with MULTIVAC, Ishida, and Proseal occupying the premium tiers. Their moat is derived from integrated MAP gas analytics, turnkey robotics, and a global service footprint. European leaders deepen regional penetration through M&A; MULTIVAC acquired an 80% stake in Italianpack to secure price-competitive segments while safeguarding its proprietary high-vacuum fieldbus protocols.

Asian challengers, notably from China and South Korea, deliver cost-competitive stainless frames priced 18% below EU peers, albeit with narrower validation tool sets. Strategic partnerships with sensor specialists such as Balluff add IIoT features that close the functional gap, intensifying competition. In the United States, Duravant’s pending integration of Pattyn brings bag-in-box expertise into its portfolio, expanding cross-selling opportunities into protein packers.

Customers are increasingly evaluating suppliers based on predictive-maintenance dashboards and cloud-licensing terms, rather than mechanical speed alone. Those offering embedded OPC-UA and MQTT connectivity, along with cybersecurity compliance documents, achieve higher win rates in pharmaceutical and pet food bids. Vendors slow to adopt data standards risk relegation to lower-margin aftermarket tooling. Consequently, the automated tray packing machinery industry continues to pivot toward software-rich value propositions.

Automated Tray Packing Machinery Industry Leaders

MULTIVAC SE and Co. KG

Ishida Co., Ltd.

Proseal UK Limited (JBT)

G. Mondini SpA

SEALPAC GmbH

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- February 2025: Duravant agreed to acquire Pattyn Group BV, adding six European manufacturing sites and 550 employees to its Packaging Solutions Group.

- January 2025: SMIPACK launched BP TRAY + FILM servo-driven models with modular end-of-arm tooling for multi-depth trays.

- December 2024: ULMA Packaging bought PackDesign AB, strengthening its Nordic market reach and sustainable design capabilities.

- October 2024: Mpac Group completed the USD 57.8 million purchase of CSi Palletising, broadening its secondary-packaging lineup.

Global Automated Tray Packing Machinery Market Report Scope

| Fully Automatic |

| Semi-Automatic |

| Manual |

| Food |

| Beverage |

| Pharmaceutical |

| Cosmetics and Personal Care |

| Other End-Use Industries |

| Plastic (PET, CPET, PP, PS) |

| Fiber/Paperboard |

| Aluminium |

| Emerging Bio-based Materials |

| Heat-Seal |

| MAP/Vacuum-Skin |

| Ultrasonic |

| Induction/Other Niche Sealing Technologies |

| North America | United States | |

| Canada | ||

| Mexico | ||

| South America | Brazil | |

| Argentina | ||

| Rest of South America | ||

| Europe | Germany | |

| United Kingdom | ||

| France | ||

| Italy | ||

| Spain | ||

| Russia | ||

| Rest of Europe | ||

| Asia-Pacific | China | |

| Japan | ||

| India | ||

| South Korea | ||

| South-East Asia | ||

| Rest of Asia-Pacific | ||

| Middle East and Africa | Middle East | Saudi Arabia |

| United Arab Emirates | ||

| Turkey | ||

| Rest of Middle East | ||

| Africa | South Africa | |

| Nigeria | ||

| Rest of Africa | ||

| By Automation Level | Fully Automatic | ||

| Semi-Automatic | |||

| Manual | |||

| By End-Use Industry | Food | ||

| Beverage | |||

| Pharmaceutical | |||

| Cosmetics and Personal Care | |||

| Other End-Use Industries | |||

| By Tray Material | Plastic (PET, CPET, PP, PS) | ||

| Fiber/Paperboard | |||

| Aluminium | |||

| Emerging Bio-based Materials | |||

| By Sealing Technology | Heat-Seal | ||

| MAP/Vacuum-Skin | |||

| Ultrasonic | |||

| Induction/Other Niche Sealing Technologies | |||

| By Geography | North America | United States | |

| Canada | |||

| Mexico | |||

| South America | Brazil | ||

| Argentina | |||

| Rest of South America | |||

| Europe | Germany | ||

| United Kingdom | |||

| France | |||

| Italy | |||

| Spain | |||

| Russia | |||

| Rest of Europe | |||

| Asia-Pacific | China | ||

| Japan | |||

| India | |||

| South Korea | |||

| South-East Asia | |||

| Rest of Asia-Pacific | |||

| Middle East and Africa | Middle East | Saudi Arabia | |

| United Arab Emirates | |||

| Turkey | |||

| Rest of Middle East | |||

| Africa | South Africa | ||

| Nigeria | |||

| Rest of Africa | |||

Key Questions Answered in the Report

How large is the automated tray packing machinery market in 2025?

The automated tray packing machinery market size stands at USD 5.51 billion in 2025 and is projected to grow steadily through 2030.

What CAGR is forecast for automated tray packing machinery to 2030?

Industry forecasts place the CAGR at 6.89% between 2025 and 2030, reflecting strong adoption drivers.

Which segment shows the fastest growth within automated tray packing equipment?

Pharmaceutical packaging lines are advancing at an 8.28% CAGR due to serialization and aseptic requirements.

Why are semi-automatic tray packers gaining traction?

Mid-tier processors favor semi-automatic lines for flexible changeovers and lower CAPEX while still easing labor constraints.

Which region is expected to lead future demand?

Asia-Pacific is on track for a 7.76% CAGR through 2030, driven by e-commerce and manufacturing expansion.

How do sustainability trends affect tray packing machinery choices?

Demand for paper, mono-plastic, and bio-based trays requires machinery able to handle varied substrates without compromising speed, spurring new tooling designs.

Page last updated on: