Bamboo Paper Packaging Market Size and Share

Market Overview

| Study Period | 2019 - 2030 |

|---|---|

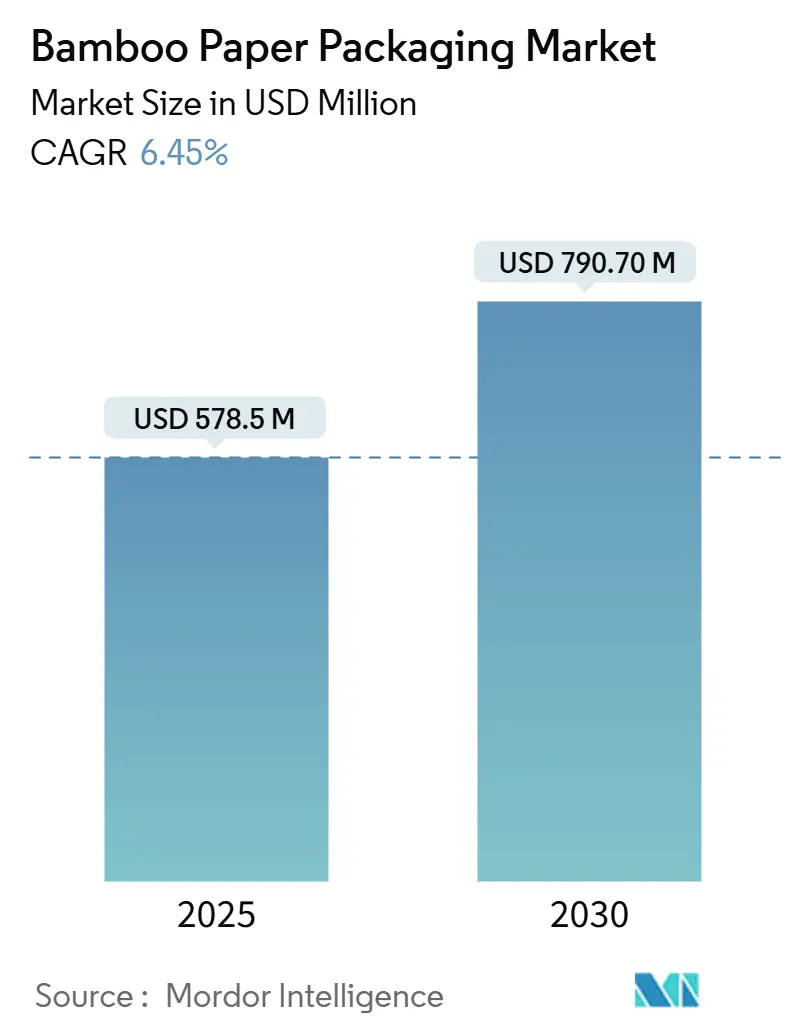

| Market Size (2025) | USD 578.5 Million |

| Market Size (2030) | USD 790.70 Million |

| Growth Rate (2025 - 2030) | 6.45% CAGR |

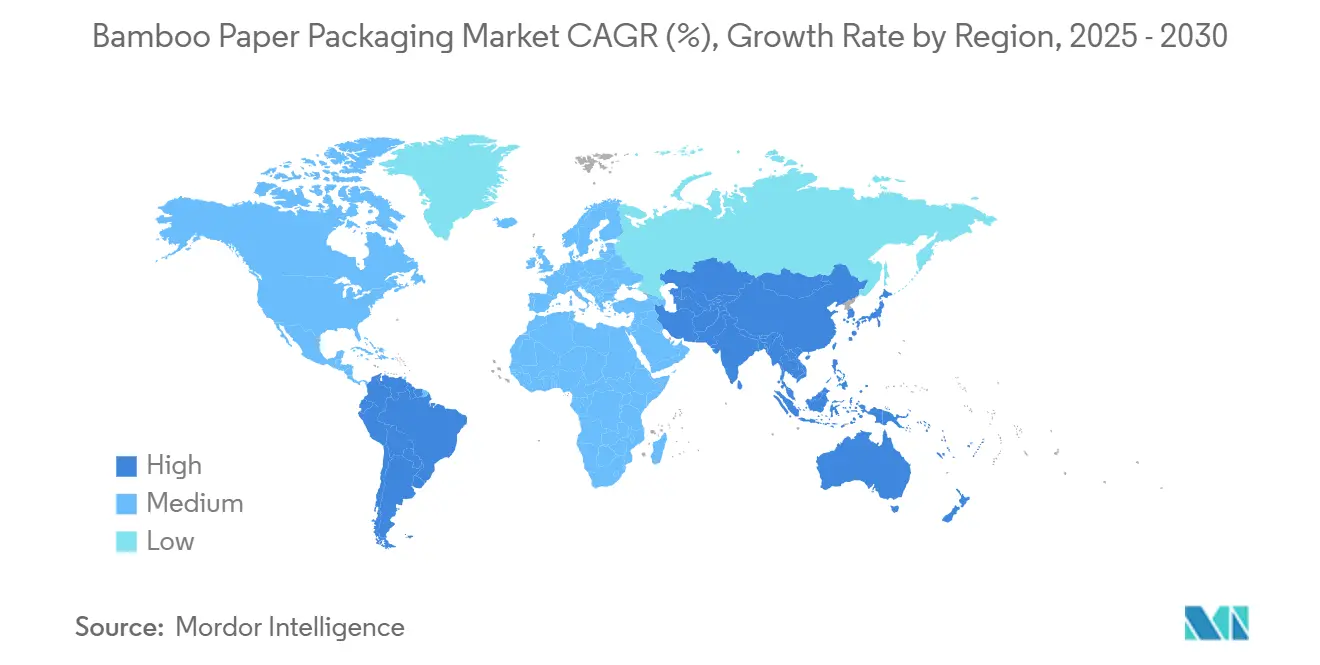

| Fastest Growing Market | South America |

| Largest Market | Asia Pacific |

| Market Concentration | Low |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

Bamboo Paper Packaging Market Analysis by Mordor Intelligence

The bamboo paper packaging market size stood at USD 578.5 million in 2025 and is forecast to reach USD 790.7 million by 2030, registering a 6.45% CAGR over the period. This healthy expansion reflects global policies phasing out single-use plastics, the arrival of cost-competitive thermo-formable bamboo pulp and large brand-owner commitments to tree-free fibres, all of which merge to accelerate demand for curb-side-recyclable solutions. Strong manufacturing roots in East Asia give the bamboo paper packaging market early-stage scale advantages, while developing regions now leverage abundant lignocellulosic biomass to carve out alternative supply routes. Breakthroughs in steam-assisted pulping have narrowed the cost gap with conventional paper substrates, opening new pockets of opportunity in both food service and e-commerce fulfilment. At the same time, certification irregularities in parts of the Asian supply chain prompt downstream buyers to reward producers that can guarantee traceability, pushing the industry toward stricter governance frameworks.

Key Report Takeaways

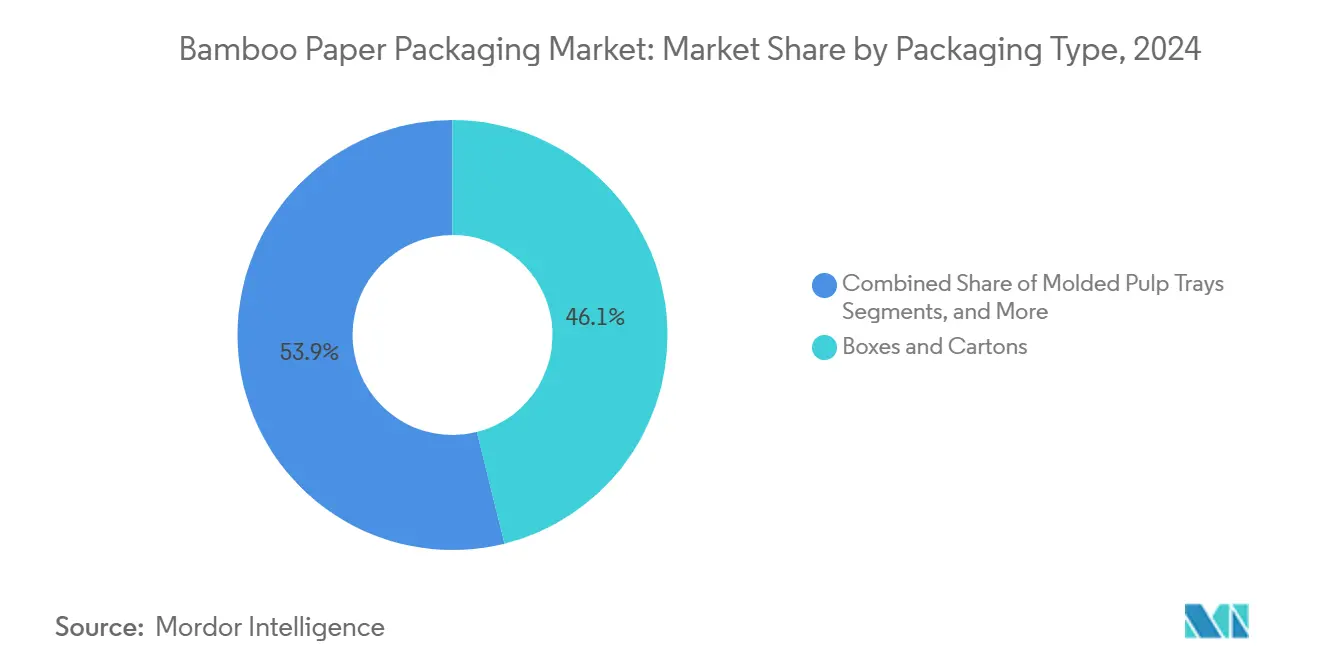

- By packaging type, boxes and cartons captured 46.12% of the bamboo paper packaging market share in 2024.

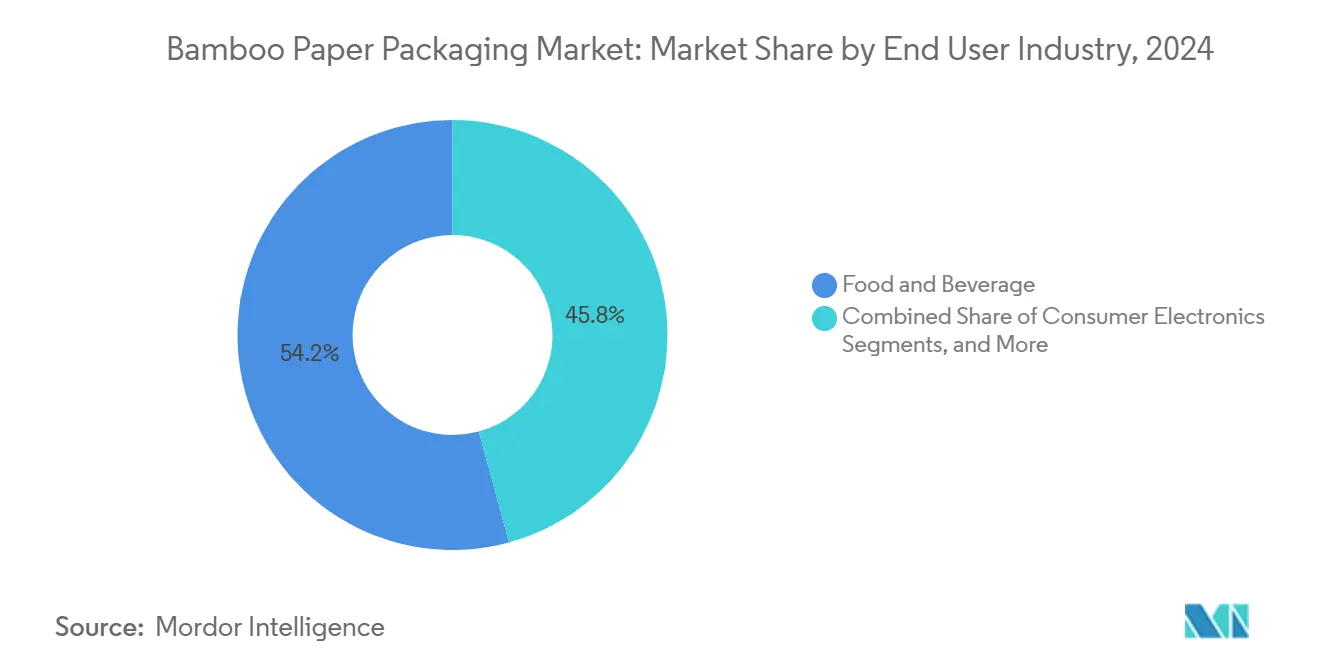

- By end-use industry, bamboo paper packaging market size for consumer electronics segment projected to grow at 16.41% CAGR between 2025-2030.

- By geography, Asia-Pacific captured 47.56% of the bamboo paper packaging market share in 2024.

Global Bamboo Paper Packaging Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Rapid bans on single-use plastics in food service and retail | +1.8% | Global, with early adoption in EU, APAC core markets | Short term (≤ 2 years) |

| Brand-owner pledges for tree-free fibre adoption | +1.2% | North America and EU, expanding to APAC | Medium term (2-4 years) |

| Cost-down breakthroughs in thermo-formable bamboo pulp | +1.5% | Global, manufacturing concentrated in China, Vietnam | Medium term (2-4 years) |

| E-commerce shift to curb-side-recyclable mailers | +0.9% | Global, with highest impact in North America, EU | Short term (≤ 2 years) |

| Carbon-credit monetisation for bamboo agro-forestry (under-the-radar) | +0.7% | APAC core, expanding to South America | Long term (≥ 4 years) |

| Corporate procurement of biodiversity-positive packaging (under-the-radar) | +0.6% | North America and EU, premium segments | Medium term (2-4 years) |

| Source: Mordor Intelligence | |||

Rapid bans on single-use plastics drive immediate market expansion

Hong Kong’s 2024 prohibition of disposable cutlery and the European Union’s Regulation 2025/40 mandating 65% recycled content in plastic packaging by 2040 are accelerating the bamboo paper packaging market.[1]Diana Dominguez, “Hong Kong's single-use plastic ban to curb F&B waste with green alternatives,” Hong Kong Business, hongkongbusiness.hk Restaurants, retailers and quick-service chains have shifted purchasing toward bamboo trays and liners because these degrade quickly and do not incur extended producer responsibility fees. Short-term spikes in demand are already evident, yet manufacturers must still clear food-contact migration tests before entering certain categories. Australia’s 2024 consultation on end-of-life obligations signals wider adoption of similar curbs, tightening compliance windows for petroleum-based formats. The legislative domino effect therefore adds measurable uplift to order volumes during the next two years.

Brand-owner sustainability pledges accelerate tree-free fibre adoption

Consumer-facing multinationals increasingly publish timetables for eliminating virgin plastic in secondary packaging. Sony’s Original Blended Material, which blends bamboo, sugarcane bagasse and post-consumer fibre, features across flagship gadgets and trims plastic usage by over 90%, proving bamboo’s suitability for premium configurations. Similar commitments from personal-care labels are spreading from Europe to North America, creating reliable offtake that justifies mill upgrades. While these programmes initially target higher-margin SKUs, volume growth will cascade into mainstream categories once process costs fall further. Downstream, marketing teams exploit bamboo’s biodiversity credentials to differentiate, reinforcing the demand loop.

Cost-down breakthroughs in thermo-formable bamboo pulp manufacturing

Research into high-pressure steam treatment and precise thermal modification has delivered compressive strength gains without chemical additives, allowing thinner gauge boards that match hardwood pulp performance. Scalable micro-cellulose extraction protocols now reach 77.2% crystallinity, opening paths to lightweight yet strong molded items. Because Asia-Pacific mills can retrofit existing digesters for bamboo feedstock, capex per tonne is falling and the bamboo paper packaging market is converging toward parity with bleached kraft. These savings most benefit molded pulp trays where complex geometries had previously required cost-prohibitive tooling modifications. Investors consequently prioritise plants near bamboo plantations to capture raw-material logistics savings.

E-commerce growth drives demand for curb-side-recyclable mailers

Online merchants prefer mailers that shoppers can flatten and drop into household recycling bins. Ranpak’s honeycomb-structured naturemailer replaced foam cushioning without sacrificing protection, illustrating performance parity that satisfies fulfilment centres. Where municipalities upgrade composting capacity, bamboo fibre mailers can enter organics streams, aligning with zero-waste pledges. Nevertheless, uneven infrastructure in dense urban areas curbs penetration rates, pushing converters to design dual-path solutions compatible with both recycling and composting. Shipment surges during peak shopping seasons amplify this driver, locking in volumes for paper-based alternatives.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Higher cap-ex for dedicated bamboo pulp lines | -0.8% | Global, most acute in North America, EU | Medium term (2-4 years) |

| Supply-chain concentration in China and Vietnam | -1.1% | Global, with highest impact on North America, EU importers | Short term (≤ 2 years) |

| Allergens and food-contact regulatory uncertainty (under-the-radar) | -0.5% | Global, most restrictive in EU, North America | Medium term (2-4 years) |

| Limited composting infrastructure in urban markets (under-the-radar) | -0.4% | Global, acute in high-density urban areas | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

Higher capital expenditure requirements for dedicated bamboo pulp lines

Bamboo fibres need extra washing, delignification and sugar removal steps, so mills must add separate digesters and effluent treatment units that elevate project budgets beyond wood-pulp benchmarks. North American and European operators face stricter emissions and worker-safety mandates, lengthening payback periods. This barrier deters small converters, maintaining reliance on imports and reinforcing geographic imbalance in the bamboo paper packaging market. Financial incentives in China and Vietnam offset some costs, yet investors elsewhere require long-term offtake contracts to secure funding. As a result, new entrants adopt asset-light strategies such as toll-pulping until domestic fibre supply matures.

Supply-chain concentration risks in China and Vietnam create vulnerability

More than half of global bamboo pulp capacity clusters in two countries; certification lapses uncovered by the Forest Stewardship Council exposed false claims and unverified origins, prompting downstream buyers to escalate audits. Trade frictions compound vulnerability, illustrated by United States countervailing duties on bamboo-based paper bags that reshuffled order flows in 2024. European importers now trial South American supply chains to mitigate geopolitical exposure, yet lack of processing infrastructure still limits available tonnage. Until diversified sourcing scales, price volatility and shipment delays will dampen the bamboo paper packaging market’s near-term upside.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Packaging Type: Molded pulp innovation unlocks new applications

Boxes and cartons retained 46.12% of the bamboo paper packaging market in 2024, leveraging existing corrugating equipment that adapts easily to bamboo liner and medium grades. Molded pulp trays and clamshells, aided by cost-down steam-treatment techniques, are forecast to post an 18.32% CAGR, raising their slice of the bamboo paper packaging market size significantly by 2030. Their openness to bespoke shapes gives food-service brands the freedom to replace foam or PET clamshells without redesigning fill-and-seal lines. Research into precision thermal energy control during deep drawing lets converters hold wall stability at 25% moisture, expanding viable SKU ranges.[2]Leonard Vogt and Marek Hauptmann, “Tailoring Thermal Energy Supply Towards the Advanced Control of Deformation Mechanisms in 3D Forming of Paper and Board,” MDPI, mdpi.com

Pouches, sachets and bags form a mature sub-segment that benefits from anti-litter regulations targeting flexible plastics, yet ongoing moisture-barrier challenges keep growth moderate. Labels and sleeves serve niche personal-care and beverage applications where bamboo fibres deliver premium tactile finishes. As molded products unlock three-dimensional geometries, converters can enter electronics accessory packs that once relied on thermoformed rPET, creating high-margin opportunities within the bamboo paper packaging market share.

By End-Use Industry: Electronics set the growth pace

Food and beverage applications absorbed 54.23% of revenues in 2024, valuing quick biodegradation and natural antimicrobial properties that align with evolving food-contact rules. Consumer electronics, however, posts a 16.41% CAGR to 2030, raising its contribution to the bamboo paper packaging market size on the back of eco-branding and high retail margins. Sony’s adoption of bamboo-sugarcane blends in headphone boxes underscores how premium devices now treat packaging as an extension of sustainability storytelling.

Personal-care manufacturers follow suit, integrating laser-engraved bamboo sleeves that convey natural positioning, while healthcare and OTC remain cautious due to barrier-property requirements. Industrial and e-commerce shippers adopt bamboo-based void fill to meet corporate decarbonisation targets; enzyme-aided fibre matrices trim thermal-drying energy by double digits, lowering total cost of ownership. Collectively, segment momentum demonstrates how stable supply and proven performance move bamboo from boutique to mainstream adoption across verticals.

Geography Analysis

Asia-Pacific held 47.56% of the bamboo paper packaging market in 2024, underpinned by dense bamboo plantations and well-established pulp networks in China and Vietnam. National programmes such as China’s “bamboo as a substitute for plastic” blueprint incentivise downstream converters through tax breaks and fast-track permitting. Yet FSC integrity probes have compelled exporters to overhaul chain-of-custody protocols, raising compliance costs and nudging brands toward alternative regions.

South America, led by Brazil, Colombia and Ecuador, records the highest regional CAGR at 15.27% as investors retrofit sugarcane bagasse mills for bamboo fibre streams, capitalising on plentiful lignocellulosic feedstock.[3]Gustavo P. Romanelli, “Valorization of residual lignocellulosic biomass in South America,” conicet.gov.ar Pilot agro-forestry projects also monetise carbon credits, improving project returns and encouraging local landowners to cultivate native Guadua species. Proximity to North American buyers adds logistical advantages that offset early-stage scale limitations.

Europe and North America are mature but opportunity-rich. EU Regulation 2025/40 obliges converters to design recyclable formats and phase in recycled content thresholds, stimulating imports of semi-finished bamboo paper while local processors evaluate dedicated lines. However, divergent food-contact rulings, including specific bans on bamboo-melamine composites, complicate product qualification pathways. In the United States, countervailing measures against Chinese paper bags encourage regional converters to explore Latin American fibre sources, accelerating supply-chain diversification.

Competitive Landscape

The bamboo paper packaging market is structurally fragmented because raw-material cultivation, pulping and converting often occur in separate jurisdictions. Few players exceed single-digit global shares; instead, many regional specialists integrate plantation management with pulp and molded-pulp operations to control fibre quality and mitigate logistics costs. Certification has become the key competitive lever, with buyers rewarding Forest Stewardship Council compliance amid rising traceability scrutiny.

Technology investments focus on thermo-formable board lines and enzyme-assisted refining that upgrade fibre bonding while trimming energy use. Early adopters of thermal-modification chambers now supply high-strength flattened bamboo sheets that unlock laptop sleeve and phone-case inserts, carving out premium niches. Cross-border joint ventures, such as Vietnamese mills partnering with Japanese converters, spread risk and pool process know-how.

Recent capital raises reflect growing investor appetite. Enrission India Capital’s July 2025 funding round for Bambrew finances reinforced-paper commercialisation, expanding production of bamboo-agri-waste blends aimed at local brands facing imminent plastic-phase-out mandates. Nordic leaders Stora Enso and Billerud accelerate board-line conversions to address customer trials for bleach-white kraft liners free of fossil-based coatings. Market share therefore remains fluid, with certified, vertically integrated players best positioned to capture brand-owner contracts tied to science-based climate targets.

Bamboo Paper Packaging Industry Leaders

ITC Ltd.

Huhtamaki Oyj

Better Packaging Co.

Bambrew India

Chengdu Qingya Paper Industries

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- July 2025: ENRISSION INDIA CAPITAL announced investment in Bambrew Plant Fiber Technology Pvt. Ltd., backing bamboo-based “Reinforced Paper” scale-up.

- April 2025: Stora Enso reported 9% Q1 sales growth to EUR 2,362 million after starting a new consumer board line focused on renewable packaging.

- April 2025: Billerud completed the first sale of US-produced containerboard, marking progress toward localised renewable packaging supply.

- April 2025: Ranpak launched climaliner Plus and naturemailer, both 100% curb-side-recyclable paper formats.

Global Bamboo Paper Packaging Market Report Scope

| Boxes and Cartons |

| Pouches, Sachets and Bags |

| Molded Pulp Trays and Clamshells |

| Labels and Sleeves |

| Food and Beverage |

| Personal Care and Cosmetics |

| Consumer Electronics |

| Healthcare and OTC |

| Industrial and E-commerce |

| North America | United States | |

| Canada | ||

| Mexico | ||

| South America | Brazil | |

| Argentina | ||

| Rest of South America | ||

| Europe | Germany | |

| France | ||

| United Kingdom | ||

| Italy | ||

| Spain | ||

| Russia | ||

| Rest of Europe | ||

| Asia-Pacific | China | |

| Japan | ||

| South Korea | ||

| India | ||

| Australia | ||

| Thailand | ||

| Rest of Asia-Pacific | ||

| Middle East and Africa | Middle East | GCC |

| Turkey | ||

| Rest of Middle East | ||

| Africa | South Africa | |

| Nigeria | ||

| Rest of Africa | ||

| By Packaging Type | Boxes and Cartons | ||

| Pouches, Sachets and Bags | |||

| Molded Pulp Trays and Clamshells | |||

| Labels and Sleeves | |||

| By End-Use Industry | Food and Beverage | ||

| Personal Care and Cosmetics | |||

| Consumer Electronics | |||

| Healthcare and OTC | |||

| Industrial and E-commerce | |||

| By Geography | North America | United States | |

| Canada | |||

| Mexico | |||

| South America | Brazil | ||

| Argentina | |||

| Rest of South America | |||

| Europe | Germany | ||

| France | |||

| United Kingdom | |||

| Italy | |||

| Spain | |||

| Russia | |||

| Rest of Europe | |||

| Asia-Pacific | China | ||

| Japan | |||

| South Korea | |||

| India | |||

| Australia | |||

| Thailand | |||

| Rest of Asia-Pacific | |||

| Middle East and Africa | Middle East | GCC | |

| Turkey | |||

| Rest of Middle East | |||

| Africa | South Africa | ||

| Nigeria | |||

| Rest of Africa | |||

Key Questions Answered in the Report

What is the current value of the bamboo paper packaging market?

The bamboo paper packaging market size reached USD 578.5 million in 2025 and is set to grow to USD 790.7 million by 2030.

Which region leads the bamboo paper packaging market?

Asia-Pacific holds leadership with 47.56% share in 2024, driven by mature bamboo cultivation and processing infrastructure.

Which segment shows the fastest growth?

Molded pulp trays and clamshells are the fastest-growing packaging type, advancing at an 18.32% CAGR through 2030.

Why are electronics brands adopting bamboo packaging?

Premium electronics makers adopt bamboo packaging to cut plastic content by over 90% and to strengthen sustainability positioning, supporting a 16.41% CAGR in that segment.

What risks could slow market growth?

High capital costs for dedicated bamboo pulp lines and supply-chain concentration in China and Vietnam pose significant restraints that may temper near-term expansion.

Page last updated on: