Aromatic Paperboard Packaging Market Size and Share

Market Overview

| Study Period | 2019 - 2030 |

|---|---|

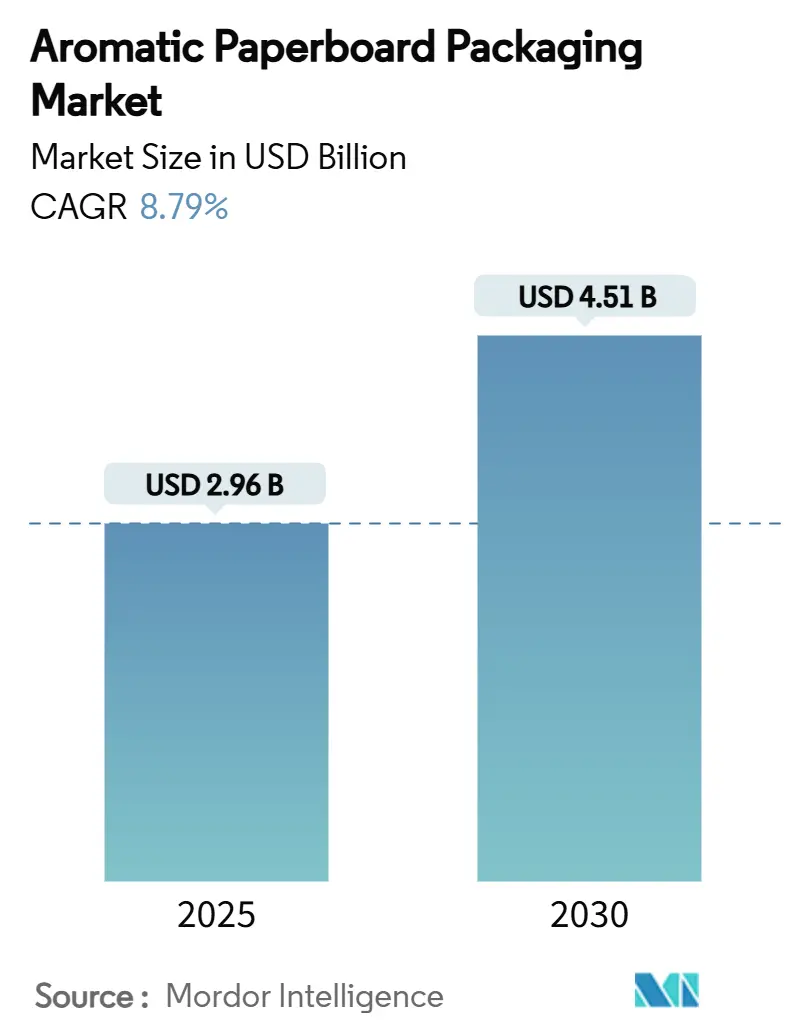

| Market Size (2025) | USD 2.96 Billion |

| Market Size (2030) | USD 4.51 Billion |

| Growth Rate (2025 - 2030) | 8.79% CAGR |

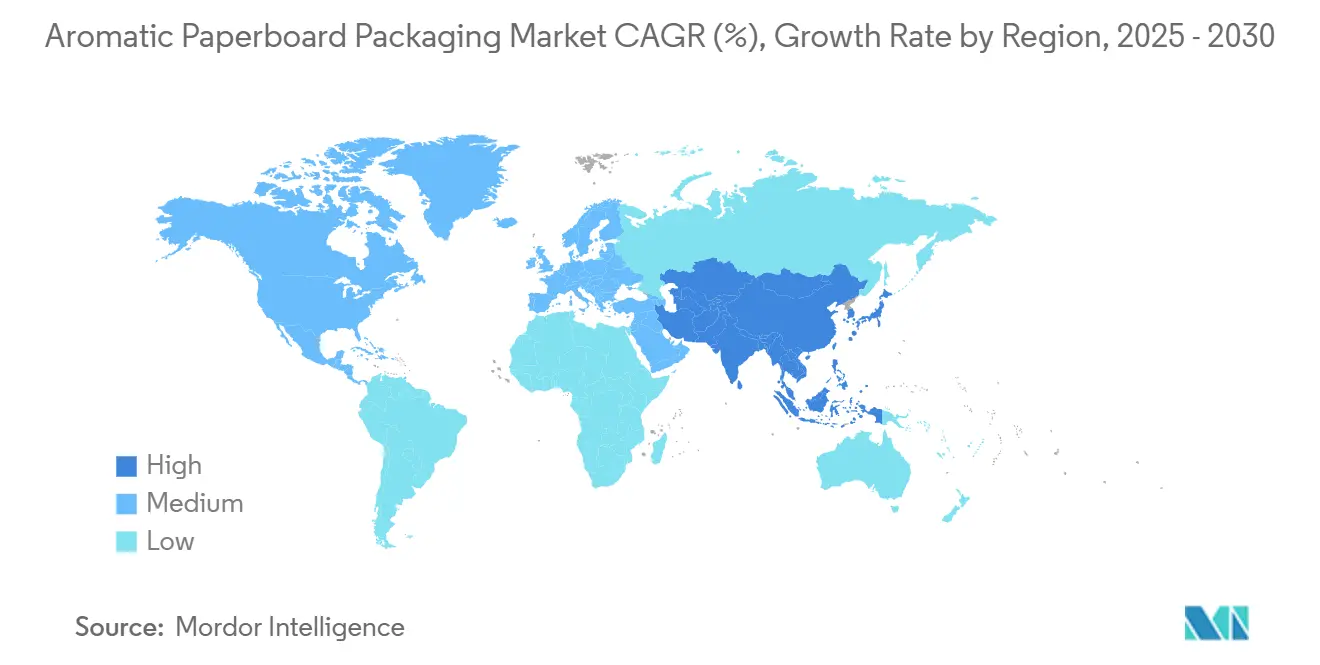

| Fastest Growing Market | Asia Pacific |

| Largest Market | North America |

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

Aromatic Paperboard Packaging Market Analysis by Mordor Intelligence

The aromatic paperboard packaging market size stood at USD 2.96 billion in 2025 and is forecast to reach USD 4.51 billion in 2030, expanding at a CAGR of 8.79%. This growth trajectory is propelled by sustainability-driven regulations, premium brand demand for multi-sensory experiences, and rapid diffusion of fragrance-delivery technologies. Folding cartons and rigid boxes continue to dominate shipments, while micro-encapsulation coatings underpin consistent scent performance across global supply chains. Luxury goods and cosmetics brands are deepening investments as they link unboxing rituals with distinct olfactory cues that reinforce brand equity. Concurrently, North American converters leverage established fragrance partners to commercialize recyclable, aroma-enabled fiber solutions, while Asia-Pacific participants accelerate capacity additions to meet e-commerce-driven demand.

Key Report Takeaways

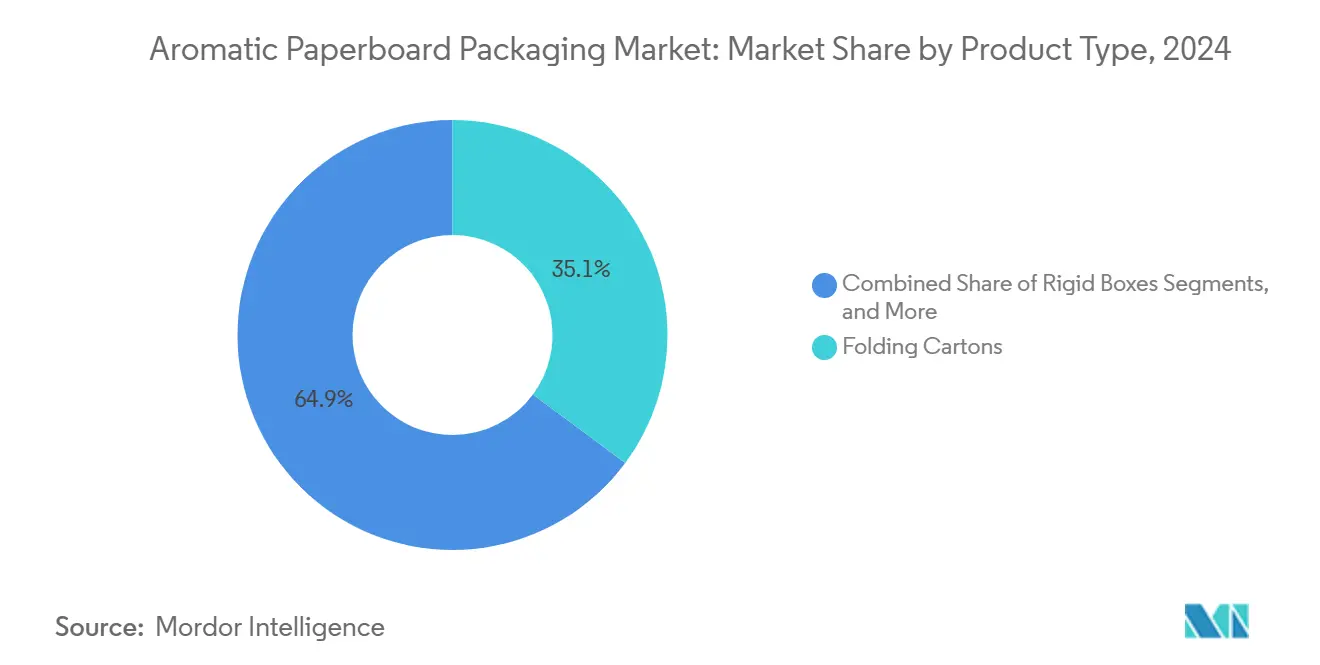

- By product type, folding cartons led with 35.14% revenue share of the aromatic paperboard packaging market size in 2024.

- By aroma release mechanism, micro-encapsulated coatings accounted for 37.79% of the aromatic paperboard packaging market share in 2024

- By paperboard grade, the aromatic paperboard packaging market size for the recycled grades segment is projected to grow at a 9.78% CAGR between 2025-2030.

- By end-use industry, cosmetics and personal care accounted for 41.58% of the aromatic paperboard packaging market share in 2024.

- By geography, the aromatic paperboard packaging market size for the Asia-Pacific region is projected to grow at a 10.02% CAGR between 2025-2030.

Global Aromatic Paperboard Packaging Market Trends and Insights

Drivers Impact Analysis*

| Driver | % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Sustainability-driven shift from plastic to paperboard | 2.1% | Global, with strongest impact in EU & North America | Medium term (2-4 years) |

| Demand for sensory/experiential packaging in premium goods | 1.8% | North America & EU luxury markets, expanding to APAC | Long term (≥ 4 years) |

| Regulatory curbs on single-use plastics and VOCs | 1.5% | EU primary, with spillover to North America & APAC | Short term (≤ 2 years) |

| Advances in micro-encapsulation extending fragrance life | 1.3% | Global, with R&D concentrated in North America & EU | Long term (≥ 4 years) |

| E-commerce "unboxing" pushing scented brand experiences | 1.1% | Global, led by North America & APAC e-commerce growth | Medium term (2-4 years) |

| Digital-scent marketing integrations with smart packaging | 0.9% | North America & EU early adoption, APAC following | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

Sustainability-Driven Regulatory Momentum Accelerates Fiber-Based Adoption

Mandates requiring fully recyclable packaging stimulate conversion away from plastic toward fiber substrates that can host fragrances without undermining recyclability. The EU’s Regulation 2025/40, in force since February 2025, obliges all primary and secondary packs to be recyclable by 2030 and imposes minimum recycled-content thresholds. Parallel frameworks in China and India likewise tighten heavy-metal and food-contact rules, steering converters toward aroma-enabled paperboard formats that comply with material bans yet elevate consumer experience. WestRock reports that 96% of its portfolio is already recyclable, compostable, or reusable, underscoring its readiness to capture incremental volume. Brands now view compliant aroma-ready paperboard as a dual-advantage platform that addresses both environmental audits and experiential marketing goals.

Premium Brand Experience Economy Drives Sensory Packaging Innovation

Luxury houses and prestige cosmetics players amplify investment in packaging that appeals to sight, touch, and now scent. L’Oréal’s roadmap to exclusive use of FSC-certified fiber boxes demonstrates how upscale categories meld sustainability with sensory storytelling. Europe’s fragrance ecosystem contributes EUR 30 billion in gross value added, ensuring deep technical expertise for cross-over packaging applications. [1]International Fragrance Association, “The Socio-Economic Impact of Fragrance Technologies in Europe,” ifrafragrance.org Givaudan’s Fragrance & Beauty division grew 14.1%, mirroring surging demand for novel scent-delivery formats beyond traditional perfumery. As a result, premium-price segments allocate larger budgets to aroma-enhanced paperboard that elevates unboxing rituals and nurtures social-media shareability.

Micro-Encapsulation Technology Breakthroughs Extend Fragrance Durability

Next-generation microcapsules fabricated from melamine resins retain volatile compounds for 2,400 hours, delivering consistent aroma from factory line to consumer doorstep.R&D now focuses on biodegradable shells to satisfy forthcoming bans on intentionally added microplastics, with polymeric matrices enabling controlled diffusion while decomposing after disposal. Patent filings reveal polymer-matrix entrapment systems engineered for humidity resistance, essential for tropical logistics corridors. These breakthroughs permit the aromatic paperboard packaging market to penetrate categories previously deterred by scent fade or migration concerns.

E-Commerce Unboxing Culture Transforms Packaging Into Marketing Medium

B2C parcel volumes soared during the pandemic, permanently raising consumer expectations for memorable unboxing. OECD analysis confirms that e-commerce sales acceleration recast packaging from a protect-and-ship utility to a front-line brand asset. International Paper targets a USD 50 billion addressable opportunity in fiber-based e-commerce packs, noting that scent cues magnify emotional engagement during at-home delivery moments. Smart-packaging patents integrating IoT sensors and NFC tags foreshadow hybrid formats where fragrance emission synchronizes with digital content, pushing the aromatic paperboard packaging market toward interactive storytelling platforms.

Restraints Impact Analysis*

| Restraint | % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| High cost of aroma-enabled converting processes | -1.4% | Global, with higher impact in cost-sensitive APAC markets | Short term (≤ 2 years) |

| Production-scale consistency of scent intensity | -0.9% | Global manufacturing locations | Medium term (2-4 years) |

| IFRA/allergen compliance limiting fragrance palette | -0.7% | EU & North America regulatory markets | Long term (≥ 4 years) |

| Humidity-driven scent fade in tropical supply chains | -0.6% | APAC, Latin America, MEA tropical regions | Medium term (2-4 years) |

| Source: Mordor Intelligence | |||

Production Cost Premiums Challenge Mass Market Adoption

Aroma-enabled coating and insert lines add 25-40% to conversion cost due to specialized curing ovens, clean-room controls, and additional quality checks. Smaller converters also shoulder incremental VOC-compliance expenses linked to solvent-based fragrance carriers, as outlined by United States EPA guidelines on ink and paint manufacturing. [2]U.S. Environmental Protection Agency, “Control of VOC Emissions from Ink and Paint Manufacturing Processes,” epa.gov Research into in-situ calcium-carbonate fillers for eucalyptus pulp illustrates ongoing attempts to offset raw-material costs, but the payback horizon remains prohibitive for high-volume, low-margin SKUs. Until scale economies accrue, adoption will concentrate in premium tiers where brand owners tolerate the surcharge.

IFRA Compliance Framework Restricts Fragrance Innovation Scope

The IFRA–RIFM Quantitative Risk Assessment caps consumer exposure to known allergens, narrowing the fragrance palette suitable for direct-contact packs. Recycled paperboard introduces additional volatile traces from legacy inks, complicating compliance validation. Migration testing extends development timelines, requiring larger capital outlays for analytical instrumentation. Consequently, niche formulators must collaborate with established fragrance houses to secure compliant scent profiles, reinforcing barriers for start-ups in the aromatic paperboard packaging industry.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Product Type: Folding Cartons Consolidate Versatility Benefit

Folding cartons accounted for 35.14% of 2024 shipments, capitalizing on die-cut flexibility and established supply lines that accept fragrance coatings with minimal retooling. The aromatic paperboard packaging market size for folding cartons is forecast to surpass USD 1.7 billion by 2030 as brand owners exploit cost-efficient formats that preserve scent integrity during global distribution. Rigid boxes, while representing a smaller tonnage base, are poised for 9.82% CAGR on the strength of luxury goods’ emphasis on tactile and olfactory storytelling. Sleeve packs and blister cards retain niche functions direct mail sampling and pharma where scratch-and-sniff windows or tamper-evident layers provide situational advantages.

Complementary patent activity on flexible printed electronics hints at future cartons embedded with humidity sensors that trigger fragrance diffusion upon threshold breach, suggesting new revenue layers for converters capable of electronics integration.

By Aroma Release Mechanism: Micro-Encapsulation Retains Lead

Micro-encapsulated coatings delivered 37.79% of 2024 revenue owing to proven shelf-life performance that withstands ocean freight, air cargo, and long-term retail display. The aromatic paperboard packaging market share for active aroma-releasing inserts, however, will surge as CPG brands pursue post-production aromatization to tailor regional scent preferences. Scratch-and-sniff varnishes remain event-driven tools for promotional mailers, whereas scented inks face thermal stability hurdles that impede broad adoption. Emerging Metal-Organic Framework reservoirs promise higher payload capacity and moisture-responsive release, positioning them as potential disruptors over the next decade.

By Paperboard Grade: Recycled Fiber Gains Regulatory Tailwinds

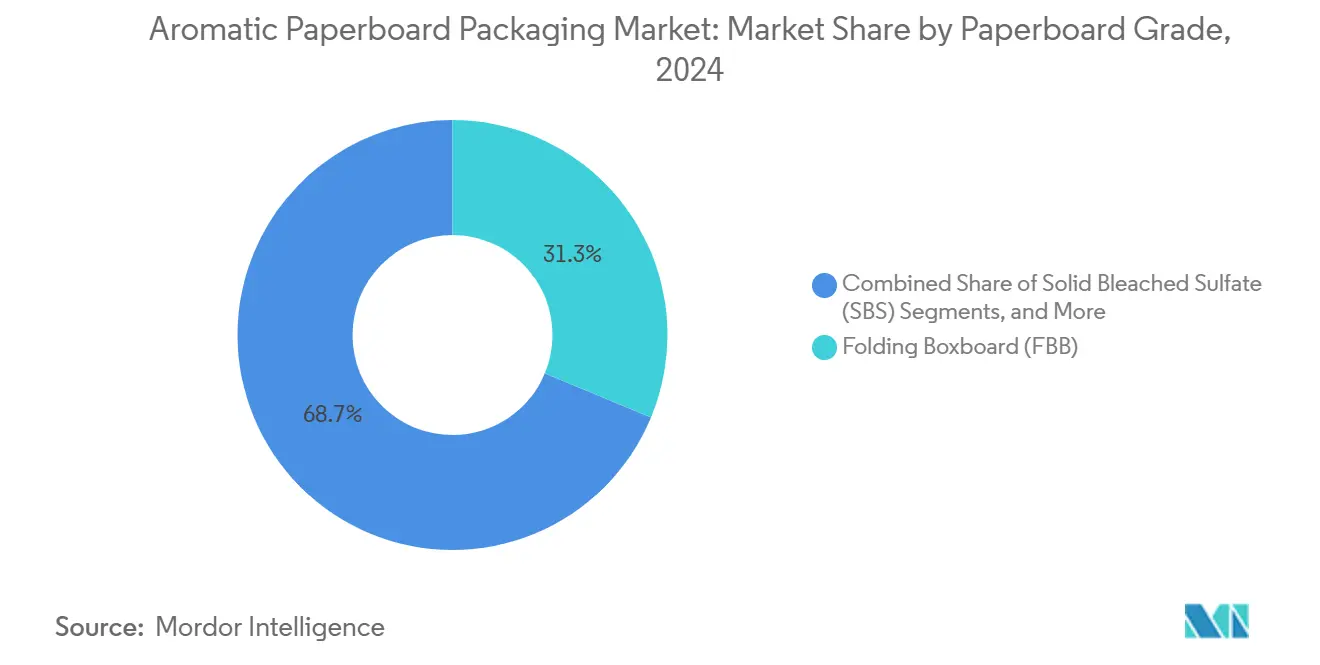

Folding boxboard (FBB) held 31.25% of shipments in 2024, buoyed by food-safe coatings and smooth caliper conducive to consistent fragrance layer thickness. Yet recycled paperboard will post the fastest 9.78% CAGR as EPR schemes reward post-consumer content. The aromatic paperboard packaging market size for recycled grades is expanding as converters deploy advanced de-inking and odor-neutralization steps to match sensory purity benchmarks of virgin fiber. Solid Bleached Sulfate continues to serve prestige skincare and fragrance coffrets where brilliant whiteness pairs with high-fidelity print graphics.

By End-Use Industry: Cosmetics Remain Early-Adopter Stronghold

Cosmetics and personal care contributed 41.58% of 2024 demand, propelled by alignment between product function and scented pack narratives. Luxury gifts will accelerate at 9.67% CAGR as high-end spirits, jewelry, and designer accessories court consumers with immersive unboxing. Within food and beverage, aroma-enabled fiber formats focus on premium chocolates and specialty teas where subtle fragrance complements flavor cues without regulatory friction. Household care brands leverage scent to signal efficacy, albeit under stricter IFRA limits for allergen exposure.

Geography Analysis

North America commanded 31.67% of global value in 2024, supported by robust fragrance-ingredient supply chains and mature luxury markets. Givaudan’s CHF 7,412 million Fragrance & Beauty turnover underscores the deep R&D ecosystem that underpins aroma-ready pack launches.[3]Givaudan, “2024 Integrated Report,” givaudan.com The United States also hosts leading converters that bundle design, printing, and fragrance micro-encapsulation under one roof, reinforcing regional leadership in the aromatic paperboard packaging market.

Europe’s footprint leverages stringent recyclability statutes and dense clusters of luxury brands. The bloc’s Regulation 2025/40 sets firm end-of-life criteria, incentivizing converters to pivot toward mono-material fiber structures that integrate biodegradable scent systems. Mondi’s position as the largest kraft-paper supplier and its 85% sustainable revenue mix spotlight Europe’s technology leadership and policy-driven demand.

Asia-Pacific, registering a blazing 10.02% CAGR to 2030, benefits from population-scale e-commerce, rising middle-class purchasing power, and stepped-up environmental rules like China’s GB 43352-2023. Local contract packers are investing in aroma-capable coaters to serve multinational brand houses seeking regional agility. Over the forecast window, APAC will contribute the lion’s share of incremental tonnage to the aromatic paperboard packaging market, gradually narrowing the gap with incumbent western regions.

Competitive Landscape

The arena remains moderately fragmented. International Paper, WestRock, and Smurfit Kappa jointly captured 28% of 2024 turnover, integrating aroma functions through partnerships with fragrance experts such as Givaudan’s Active Beauty unit. ScentSational Technologies and other pure-plays carve niches by offering proprietary polymer matrix systems enabling customized release profiles. Patent analysis reveals two competitive thrusts: global fiber majors embedding scent layers into mainstream grades, and specialty fragrance houses developing pack-ready delivery modules.

Strategic alliances dominate recent moves. International Paper’s merger with DS Smith expands design laboratories capable of pilot-scale aroma trials, while Stora Enso’s EUR 1 billion rebuild at Oulu earmarks capacity for coated consumer board optimized for fragrance adhesion.Market participants also eye smart-packaging convergence, filing IP that links temperature sensors to programmable fragrance bursts an avenue poised to differentiate offerings once IoT costs recede.

Aromatic Paperboard Packaging Industry Leaders

International Paper Company

Smurfit Westrock plc

Graphic Packaging International

Mondi Plc

Stora Enso Oyj

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- March 2025: Stora Enso posted a 9% sales rise to EUR 2,362 million and advanced its Oulu consumer-board line toward full aroma-grade output.

- February 2025: EU Regulation 2025/40 entered force, mandating 100% recyclable packaging by 2030.

- January 2025: Givaudan recorded CHF 7,412 million 2024 sales, buoyed by 14.1% growth in Fragrance & Beauty.

- September 2024: L’Oréal confirmed 97% FSC-certified paper usage for instructions leaflets and 100% for outer boxes.

Global Aromatic Paperboard Packaging Market Report Scope

| Folding Cartons |

| Rigid Boxes |

| Sleeve Packaging |

| Blister Cards |

| Micro-encapsulated Coatings |

| Scratch-and-Sniff Varnish |

| Embedded Scented Inks |

| Fragrance-Infused Adhesive Labels |

| Active Aroma-Releasing Inserts |

| Folding Boxboard (FBB) |

| Solid Bleached Sulfate (SBS) |

| Coated Unbleached Kraft (CUK) |

| White Lined Chipboard (WLC) |

| Recycled Paperboard |

| Cosmetics and Personal Care |

| Food and Beverages |

| Household and Home Care |

| Luxury Goods and Gifts |

| Promotional and Direct Mail |

| North America | United States | |

| Canada | ||

| Mexico | ||

| South America | Brazil | |

| Argentina | ||

| Rest of South America | ||

| Europe | Germany | |

| France | ||

| United Kingdom | ||

| Italy | ||

| Spain | ||

| Russia | ||

| Rest of Europe | ||

| Asia-Pacific | China | |

| India | ||

| Japan | ||

| South Korea | ||

| Australia | ||

| Thailand | ||

| Indonesia | ||

| Rest of Asia-Pacific | ||

| Middle East and Africa | Middle East | GCC |

| Turkey | ||

| Rest of Middle East | ||

| Africa | South Africa | |

| Nigeria | ||

| Rest of Africa | ||

| By Product Type | Folding Cartons | ||

| Rigid Boxes | |||

| Sleeve Packaging | |||

| Blister Cards | |||

| By Aroma Release Mechanism | Micro-encapsulated Coatings | ||

| Scratch-and-Sniff Varnish | |||

| Embedded Scented Inks | |||

| Fragrance-Infused Adhesive Labels | |||

| Active Aroma-Releasing Inserts | |||

| By Paperboard Grade | Folding Boxboard (FBB) | ||

| Solid Bleached Sulfate (SBS) | |||

| Coated Unbleached Kraft (CUK) | |||

| White Lined Chipboard (WLC) | |||

| Recycled Paperboard | |||

| By End-use Industry | Cosmetics and Personal Care | ||

| Food and Beverages | |||

| Household and Home Care | |||

| Luxury Goods and Gifts | |||

| Promotional and Direct Mail | |||

| By Geography | North America | United States | |

| Canada | |||

| Mexico | |||

| South America | Brazil | ||

| Argentina | |||

| Rest of South America | |||

| Europe | Germany | ||

| France | |||

| United Kingdom | |||

| Italy | |||

| Spain | |||

| Russia | |||

| Rest of Europe | |||

| Asia-Pacific | China | ||

| India | |||

| Japan | |||

| South Korea | |||

| Australia | |||

| Thailand | |||

| Indonesia | |||

| Rest of Asia-Pacific | |||

| Middle East and Africa | Middle East | GCC | |

| Turkey | |||

| Rest of Middle East | |||

| Africa | South Africa | ||

| Nigeria | |||

| Rest of Africa | |||

Key Questions Answered in the Report

What is the current value of the aromatic paperboard packaging market?

The aromatic paperboard packaging market size reached USD 2.96 billion in 2025 and is projected to hit USD 4.51 billion by 2030 at an 8.79% CAGR.

Which product type leads global adoption?

Folding cartons hold the largest 2024 share at 35.14% thanks to structural versatility and low conversion barriers for fragrance integration.

Why is Asia-Pacific the fastest-growing region?

Rapid e-commerce expansion, rising middle-class spending, and converging sustainability regulations drive a 10.02% CAGR in Asia-Pacific demand.

How do micro-encapsulated coatings outperform other aroma release mechanisms?

They protect scent molecules for up to 2,400 hours and provide controlled diffusion that withstands varied logistics climates.

What main restraint limits mass-market penetration?

Aroma-enabled converting adds 25-40% to production cost, making the technology economical mainly for premium or luxury product lines.

Which regulations most influence material selection?

EU Regulation 2025/40 mandates universal recyclability by 2030, accelerating the shift from plastic to fiber-based aromatic solutions.

Page last updated on: