Microalgae In Fertilizers Market Size and Share

Market Overview

| Study Period | 2020 - 2030 |

|---|---|

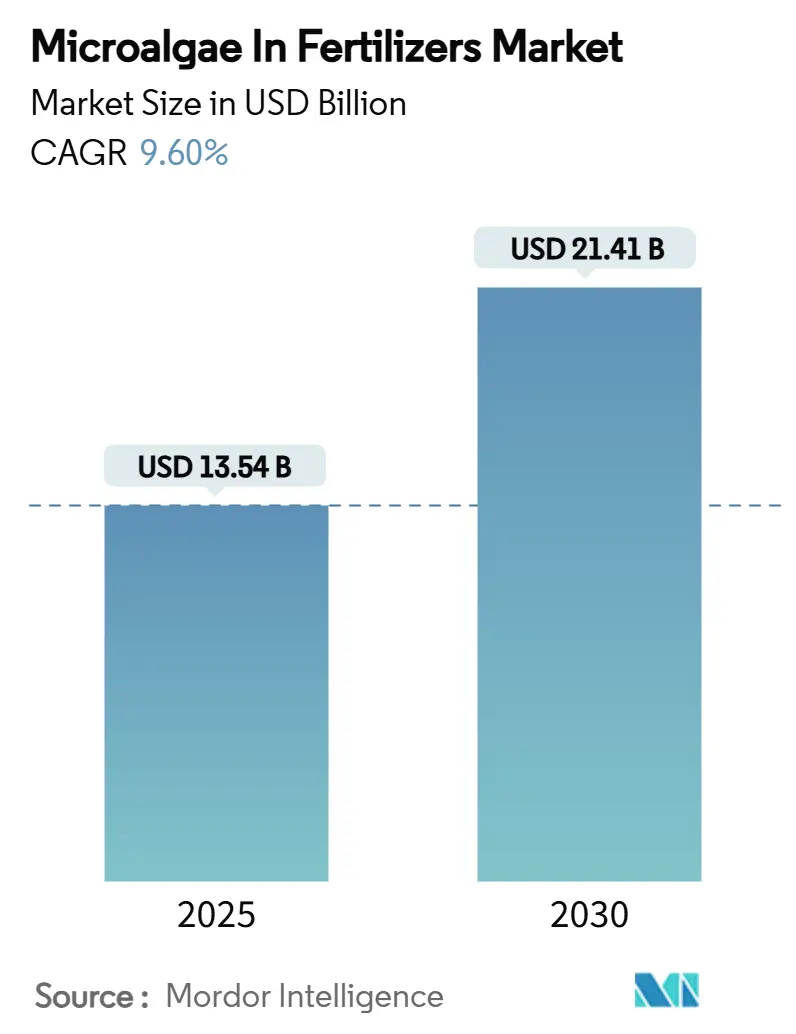

| Market Size (2025) | USD 13.54 Billion |

| Market Size (2030) | USD 21.41 Billion |

| Growth Rate (2025 - 2030) | 9.60% CAGR |

| Fastest Growing Market | Asia Pacific |

| Largest Market | Europe |

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

Microalgae In Fertilizers Market Analysis by Mordor Intelligence

The microalgae in fertilizers market size stands at USD 13.54 billion in 2025 and is forecast to reach USD 21.41 billion by 2030, expanding at a 9.6% CAGR. Regulatory moves that favor biological inputs, steady advances in high-throughput photobioreactors, and mounting investor interest in circular business models keep demand on an upward trajectory. Europe’s fast-tracked approval of twenty algal species for agricultural use removed a USD 10.8 million compliance burden and signaled a clear policy tailwind for residue-free solutions. The swift implementation of controlled-environment agriculture in the Asia-Pacific region, along with strong subsidy initiatives in China and India, has created an energetic momentum for growth in the area. Product differentiation increasingly rests on species selection, nutrient-release profile, and compatibility with precision deployment tools, factors that together shape supplier competitiveness.

Key Report Takeaways

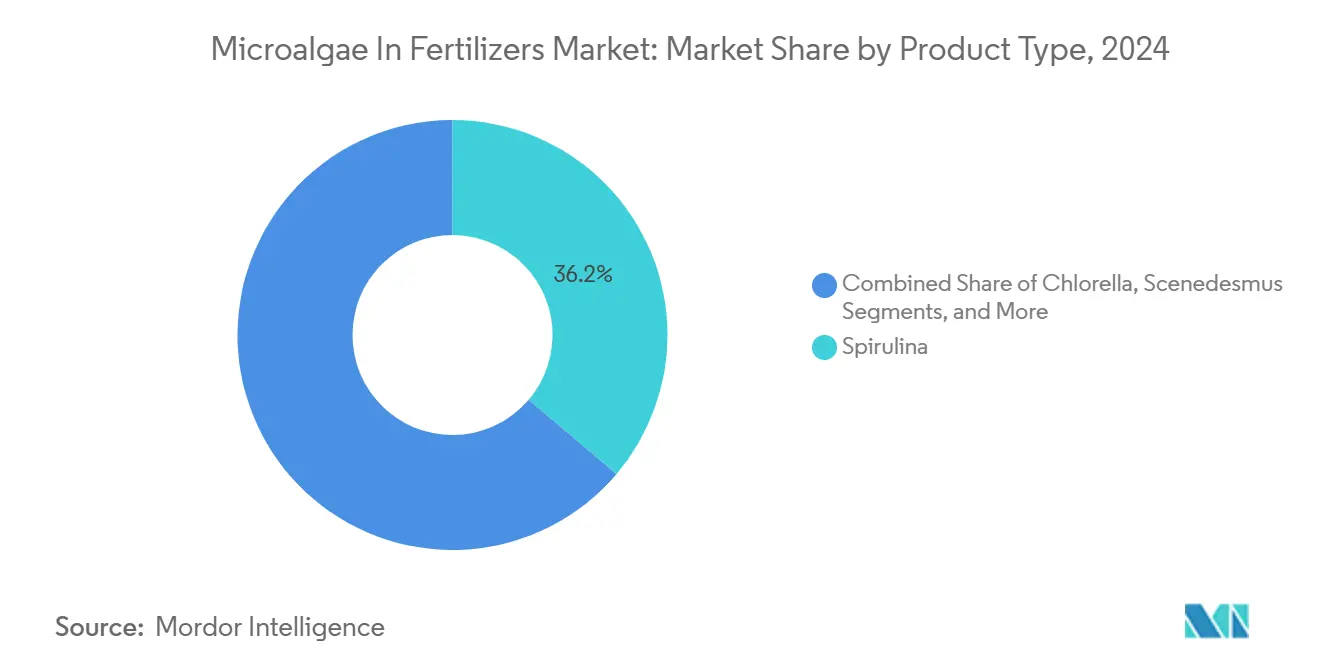

- By product type, spirulina led with 36.2% of microalgae in fertilizers market share in 2024, while Nannochloropsis is projected to advance at a 12.8% CAGR through 2030.

- By form, liquid formulations accounted for a 40.5% share of the microalgae in fertilizers market size in 2024 and are forecast to grow at an 11.6% CAGR to 2030.

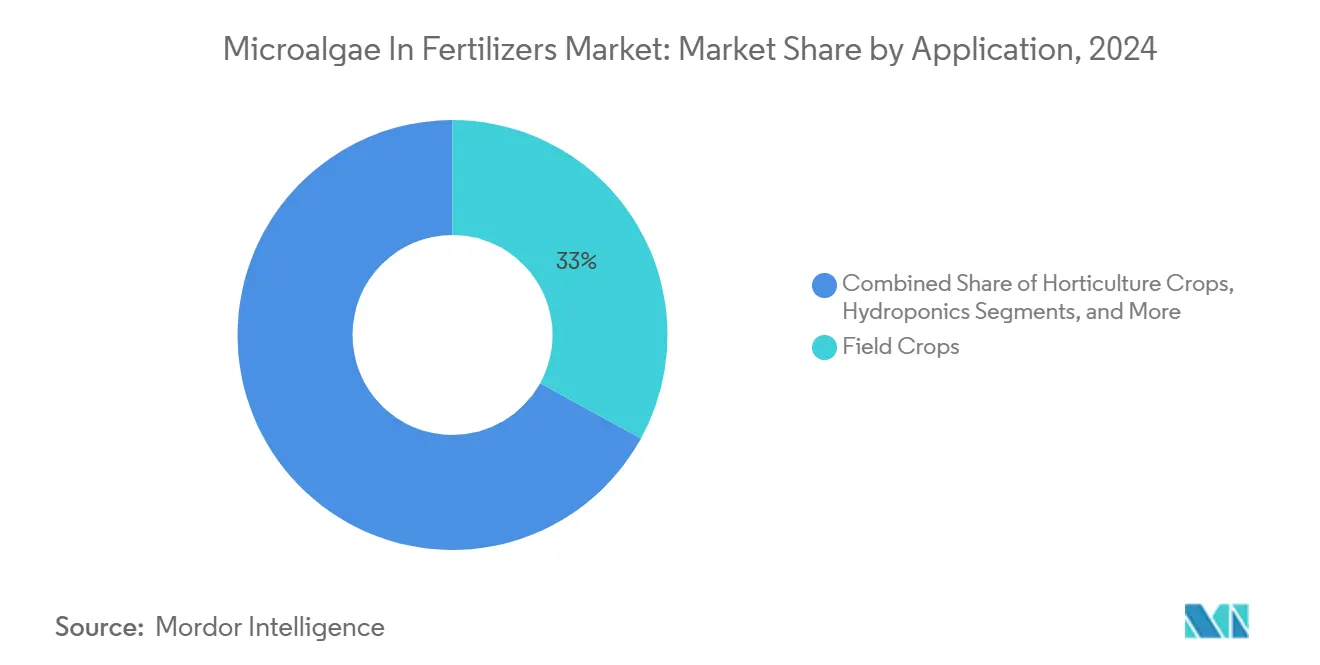

- By application, field crops captured a 33% share of the microalgae in fertilizers market size in 2024, while hydroponics is set to expand at a 10.4% CAGR through 2030.

- By mode of application, soil treatment held a 55% share of the microalgae in fertilizers market in 2024, while foliar spray methods posted the fastest 12.6% CAGR to 2030.

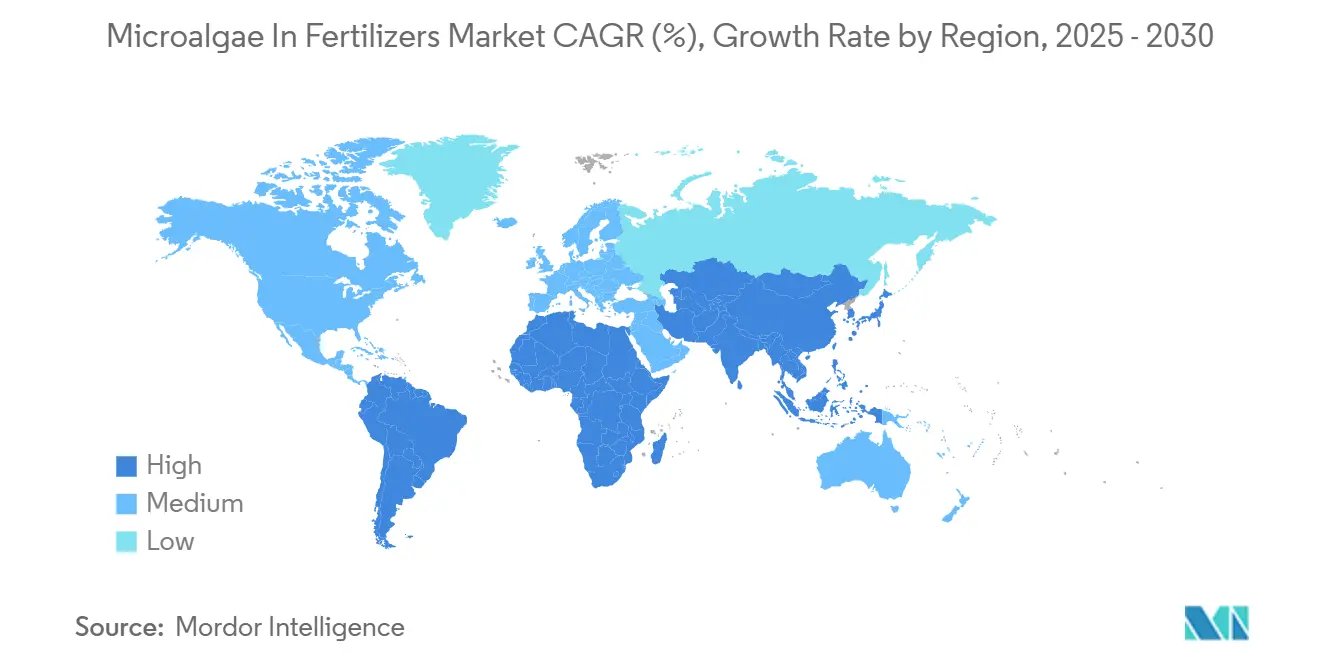

- By geography, Europe commanded a 35% revenue share in 2024, and Asia-Pacific shows the highest 10.4% forecast CAGR to 2030.

Global Microalgae In Fertilizers Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Shift toward organic farming and tighter residue regulations | +1.8% | Global with European Union and North America leading | Medium term (2-4 years) |

| Government subsidy and carbon-credit incentives for algal biofertilizers | +1.5% | Europe, North America, select Asia-Pacific markets | Short term (≤ 2 years) |

| Growth of high-value horticulture crops needing residue-free inputs | +1.2% | Global, concentrated in premium crop regions | Medium term (2-4 years) |

| Decentralized on-farm photobioreactors powered by agri-voltaics | +0.9% | Asia-Pacific core, spill-over to Middle East and Africa and South America | Long term (≥ 4 years) |

| Wastewater co-cultivation unlocking dual revenue streams | +0.8% | Global with early uptake in water-stressed regions | Medium term (2-4 years) |

| Gene-edited microalgae with enhanced nutrient-release profiles | +0.7% | North America and European Union pending regulatory clearance | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

Shift Toward Organic Farming and Tighter Residue Regulations

Policy pressure that caps chemical residues has amplified demand for biological inputs. FDA fast-tracked approvals for algae-derived additives in 2025, and the EPA eased registration rules on several microalgal strains.[1]Source: U.S. Food and Drug Administration, “Food Additive Approvals,” FDA, fda.gov Certified organic farmland in Europe grew 8.1% a year between 2023 and 2024, creating a premium buyer pool ready to absorb higher input costs for compliance. Liquid microalgae blends integrate smoothly into existing organic protocols and therefore meet the most stringent export standards. As retailers place QR codes on produce to display traceability data, residue-free fertilizers move from optional premium to baseline requirement in key export markets.

Government Subsidy and Carbon-Credit Incentives for Algal Biofertilizers

Carbon-credit programs now assign USD 15-25 per metric ton of CO₂ captured via microalgae cultivation, effectively discounting biofertilizer costs for adopters. The European Union Green Deal dedicates EUR 1 billion (USD 1.08 billion) each year to sustainable farming transitions, with a carve-out for biological inputs.[2]Source: European Food Safety Authority, “Novel Food Status Catalogue Updates,” EFSA, efsa.europa.eu India reimburses up to 50% of farmers’ biofertilizer spend, shrinking the cost gap with synthetics. These incentives guarantee baseline demand, boost bankability of new facilities, and accelerate payback on cultivation infrastructure. As credit markets mature, firms that bundle fertilizer sales with verified sequestration units gain revenue diversification and stronger balance sheets.

Growth of High-Value Horticulture Crops Needing Residue-Free Inputs

Organic vegetables, berries, and specialty herbs fetch 40-200% price premiums over conventional produce. Microalgae fertilizers supply micronutrients and natural growth hormones that lift sugar content, antioxidant load, and shelf life attributes that resonate in high-margin retail segments. Controlled-environment farms specify residue-free inputs in contracts with grocery chains, aiming for differentiated product lines. Traceability apps now let consumers view the entire input list for premium greens, bolstering the business case for algae-based solutions. As high-value horticulture acreage rises, so does the pull-through on advanced biofertilizers.

Gene-Edited Microalgae with Enhanced Nutrient-Release Profiles

CRISPR/Cas9 editing has raised the internal production of plant growth compounds such as astaxanthin by up to 60%.[3]Source: Rajesh Kumar and Anjali Sharma, “Microalgal-Fungal Pellets for Hydroponics,” PMC, pmc.ncbi.nlm.nih.gov Tailored nutrient-release curves now align more closely with crop uptake, trimming leaching losses and input waste. Regulatory uncertainty remains the European Union classifies most gene-edited organisms as genetically modified, while the United States follows a trait-based approach, creating dual compliance tracks. Intellectual property frameworks are still evolving, yet early patents hint at competitive moats for firms that master strain-specific enhancements. Successful approvals could set a new high bar for product performance in the microalgae in fertilizers market.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| High production cost versus conventional fertilizers | -2.1% | Global with strongest effect in price-sensitive regions | Short term (≤ 2 years) |

| Inconsistent field performance and lack of standards | -1.3% | Global, especially developing markets | Medium term (2-4 years) |

| Risk of heavy-metal uptake from industrial effluents | -0.8% | Industrial regions worldwide | Medium term (2-4 years) |

| Limited shelf life of live-cell liquid formulations | -0.6% | Global with logistics challenges | Short term (≤ 2 years) |

| Source: Mordor Intelligence | |||

High Production Cost Versus Conventional Fertilizers

Commercial microalgae fertilizer runs USD 315-500 per kilogram, dwarfing the USD 0.50-1.20 per kilogram cost of bulk nitrogen products. Capital-heavy photobioreactors and energy-intensive harvesting steps keep unit economics stubbornly above parity. The benefits of scale economies are limited since actual yields only reach 10-15% of what is achieved in laboratory conditions. For commodity crops, the price premium eliminates margin gains from organic certification. While financial support and carbon credits provide temporary relief, achieving long-term sustainability requires innovations in crop productivity and energy-efficient dewatering methods.

Limited Shelf Life of Live-Cell Liquid Formulations

Live-cell suspensions lose vigor after 30-90 days unless kept below 8 degrees Celsius, pushing distributors into cold-chain logistics. Small retailers in emerging markets often lack dependable refrigeration, shortening sell-through windows and hiking return rates. Preservation fixes, including acidification and vacuum packaging, extend life but can diminish biological activity. Seasonal crop calendars compound the problem, inventory produced in the off-season may expire before peak demand. Without formulation advances, liquid products may cede ground to dried powder alternatives despite their lower bioavailability.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Product Type: Spirulina Leads as Nannochloropsis Accelerates

Spirulina held 36.2% of the microalgae in fertilizers market share in 2024, benefiting from mature cultivation know-how and broad regulatory clearance. Its robust protein matrix delivers consistent nitrogen release across multiple crop types, anchoring supplier revenue streams. Nannochloropsis grows at a 12.8% CAGR due to its 37% lipid content that enhances nutrient absorption in precision systems. Producers are investing in Nannochloropsis photobioreactors to meet rising demand from horticulture players seeking higher crop-quality metrics. Chlorella and Scenedesmus play niche roles in organic soil regeneration and wastewater valorization projects.

Across the forecast, Spirulina’s entrenched supply chain keeps it central to blended formulations, yet Nannochloropsis may chip away at dominance in high-tech farms. Specialty strains such as Porphyridium gain traction where growers aim for added plant-growth compounds, even at premium prices. Gene-edited variants could shift cost curves if regulatory hurdles are cleared, injecting another layer of competition. Overall, the microalgae in fertilizers market will likely support a multi-species portfolio that balances cost, nutrient profile, and processing ease.

By Form: Liquid Bioavailability Outruns Powder Stability

Liquid products captured 40.5% of the microalgae in fertilizers market size in 2024 and remain the fastest-moving format, expanding at 11.6% CAGR. High solubility boosts nutrient uptake in drip lines and foliar rigs, aligning with precision practices. Yet shelf-life hurdles and cold-chain costs keep powder and granule formats relevant. Powders hold steady demand where growers favor extended storage and lower freight weight, while granules address slow-release needs in rain-fed field crops.

Innovation blurs classic form lines. Encapsulated liquids promise the bioavailability of suspensions with the stability of powders. Spray-dried microalgae blended with biochar unlock ancillary soil-conditioning income streams. While liquid solutions currently lead in growth, the microalgae market for fertilizers will continue to offer a diverse mix tailored to specific crops, climate conditions, and logistical needs.

By Application: Volume Comes from Field Crops, Growth from Hydroponics

Field crops provided 33% of 2024 demand, cementing the microalgae in fertilizers market’s foundation in staple agriculture. Adoption leans on organic certification premiums and soil-health gains such as better water retention. Meanwhile, hydroponics logs a 10.4% CAGR as vertical and rooftop farms proliferate near megacities. In nutrient film systems, microalgae replace synthetic chelates and align with residue-free brand promises.

Horticulture crops maintain mid-single-digit growth because premium retail pricing cushions higher input costs. Turf and ornamentals serve as a stable, non-seasonal outlet, especially for maintenance contracts at sports venues. Over the forecast, success rests on tailoring formulations to each application’s nutrient timing and delivery method.

By Mode of Application: Soil Treatment Still Dominant but Foliar Gains Speed

Soil treatments controlled 55% of 2024 revenue, supported by existing farm machinery and broad compatibility with crop rotations. Soil contact also lets microalgae improve microbial diversity, a selling point for regenerative farming programs. Foliar spray shows a 12.6% CAGR on the back of drone-enabled precision delivery that slices waste and addresses mid-season nutrient gaps. Seed treatment remains nascent but interesting for organic growers who cannot use synthetic coatings.

Long-term growth hinges on digital agronomy platforms that recommend mode and dosage per field zone, raising both efficacy and farmer confidence. As sensor-driven feedback loops mature, they will likely push microalgae usage deeper into foliar and seed channels, balancing the traditional soil segment.

Geography Analysis

Europe’s 35% share in 2024 reflects tight residue limits that penalize synthetic fertilizers and favor biological substitutes. The EU’s 2024 inclusion of twenty algae species in its Novel Food Status Catalogue removed EUR 10 million (USD 10.8 million) in red tape and opened a projected EUR 9 billion (USD 9.7 billion) demand corridor by 2030. Germany and France award carbon income of USD 15-25 per metric ton CO₂ for verified algal sequestration, enhancing project returns. Well-developed organic supply chains allow manufacturers to secure better margins than in commodity-driven regions.

Asia-Pacific is on track for a 10.4% CAGR, buoyed by government cost-sharing schemes that cover 30-50% of biofertilizer expenses. China’s green-agriculture mandates and India’s push for residue-free exports add structural pull. Urbanized markets such as Singapore adopt high-density vertical farms that specify microalgae inputs for premium salad lines. Water-scarcity programs across Australia and Southeast Asia promote algae soil amendments that lift moisture retention, further supporting adoption.

North America grows steadily, supported by clear EPA guidance on biologicals and strong consumer demand for organic produce. Precision agriculture tools make variable-rate microalgae application viable across vast acreages. South American regions are trialing wastewater-powered algae projects that simultaneously meet tightening discharge norms. Middle East and African countries explore solar-driven decentralized units aiming to cut fertilizer imports and combat desertification.

Competitive Landscape

The microalgae in fertilizers market shows moderate concentration, with the top five suppliers accounting for around 47.6% of global revenue. Scale advantages come from controlling the entire chain of strain development, photobioreactor assets, downstream processing, and last-mile distribution. Incumbents focus on proprietary cultivation hardware and formulation know-how that raise switching costs for buyers. At the same time, many regional specialists operate single-species farms or wastewater-linked units, keeping price competition lively and preventing any one firm from dominating.

Capital inflows signal that investors view the sector as ready for accelerated scale-up. In April 2025, Brevel raised USD 5 million to expand closed-loop cultivation lines and refine lipid-rich Nannochloropsis blends for indoor farms. Algiecel followed in October 2024 with EUR 6.5 million (USD 7.0 million) to build containerized photobioreactor systems that attach directly to industrial exhaust streams, offering carbon capture plus fertilizer output. Large fertilizer incumbents are also moving. ICL entered the space by acquiring Nitro 1000 in October 2024, gaining an immediate microalgae portfolio and establishing distribution in North America. These transactions illustrate a dual track where start-ups secure growth capital while multinationals buy capabilities to shorten learning curves.

Technology partnerships increasingly dictate competitive edge. Leading firms co-develop gene-edited strains with university labs to sharpen nutrient-release timing and reduce heavy-metal uptake risks, creating intellectual property walls around high-performance seeds. Several suppliers have aligned with drone and sensor companies so that their liquid formulations integrate smoothly into variable-rate spray programs, tightening the link between product and precision-agriculture software. As carbon-credit protocols mature, alliances with verification agencies help monetize sequestration services and sweeten buyer economics. Together, these moves point to a market where sustained leadership will hinge on ecosystem integration rather than commodity price alone.

Microalgae In Fertilizers Industry Leaders

AlgaEnergy International Limited (DE SANGOSSE)

Algatech LTD (Solabia Group)

Kemin Industries, Inc.

PhycoTerra (Heliae Agriculture LLC)

DIC Corporation (DIC Group)

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- May 2025: AlgaEnergy received European Union certification as the first company to produce microalgae biomass without cyanobacteria, allowing its use in CE-marked biostimulants and soil amendments. This certification enhances the regulatory acceptance of algae-based agricultural inputs in Europe, supporting the sustainability objectives of the European Union Green Deal.

- March 2025: HyveGeo transforms desert landscapes by combining biochar, microalgae-derived biostimulants, and beneficial microbes to create fertile soil and improve crop growth in high-temperature conditions. The company's innovative approach strengthens the microalgae fertilizer market by demonstrating successful applications in extreme environmental conditions.

- March 2024: Probelte introduced Spirunol, a biostimulant and fertilizer derived from enzymatically hydrolyzed Spirulina (strain AGNOVA-001). The product contains polyphenols, amino acids, antioxidants, and prebiotic proteins. Certified for organic farming under European Union Regulation 2018/848, Spirunol enhances flowering, root development, and soil microbiota balance, establishing the company's presence in the microalgae fertilizer market.

- July 2023: DE SANGOSSE acquired AlgaEnergy's agricultural division and established AE Agribiologicals, which specializes in microalgae-based biosolutions for crop sustainability worldwide. This acquisition combines research and development capabilities and extends biosolution products to more than 4 million farmers across over 60 countries.

Global Microalgae In Fertilizers Market Report Scope

| Spirulina |

| Chlorella |

| Scenedesmus |

| Nannochloropsis |

| Porphyridium |

| Others |

| Liquid |

| Powder |

| Granules |

| Field Crops |

| Horticulture Crops |

| Turf and Ornamentals |

| Hydroponics |

| Soil Amendment |

| Foliar Spray |

| Seed Treatment |

| North America | United States |

| Canada | |

| Mexico | |

| Rest of North America | |

| South America | Brazil |

| Argentina | |

| Rest of South America | |

| Europe | Germany |

| France | |

| United Kingdom | |

| Italy | |

| Spain | |

| Russia | |

| Rest of Europe | |

| Asia-Pacific | China |

| India | |

| Japan | |

| South Korea | |

| Australia | |

| New Zealand | |

| Rest of Asia-Pacific | |

| Middle East | Saudi Arabia |

| United Arab Emirates | |

| Turkey | |

| Rest of Middle East | |

| Africa | South Africa |

| Egypt | |

| Rest of Africa |

| By Product Type | Spirulina | |

| Chlorella | ||

| Scenedesmus | ||

| Nannochloropsis | ||

| Porphyridium | ||

| Others | ||

| By Form | Liquid | |

| Powder | ||

| Granules | ||

| By Application | Field Crops | |

| Horticulture Crops | ||

| Turf and Ornamentals | ||

| Hydroponics | ||

| By Mode of Application | Soil Amendment | |

| Foliar Spray | ||

| Seed Treatment | ||

| By Geography | North America | United States |

| Canada | ||

| Mexico | ||

| Rest of North America | ||

| South America | Brazil | |

| Argentina | ||

| Rest of South America | ||

| Europe | Germany | |

| France | ||

| United Kingdom | ||

| Italy | ||

| Spain | ||

| Russia | ||

| Rest of Europe | ||

| Asia-Pacific | China | |

| India | ||

| Japan | ||

| South Korea | ||

| Australia | ||

| New Zealand | ||

| Rest of Asia-Pacific | ||

| Middle East | Saudi Arabia | |

| United Arab Emirates | ||

| Turkey | ||

| Rest of Middle East | ||

| Africa | South Africa | |

| Egypt | ||

| Rest of Africa | ||

Key Questions Answered in the Report

What is the current value of the microalgae in fertilizers marketand forecasted market size?

The microalgae in fertilizers market size is USD 13.54 billion in 2025 and is projected to reach USD 21.41 billion by 2030.

Which product type holds the largest share?

Spirulina led the market with 36.2% share in 2024.

Which region grows the fastest over the forecast?

Asia-Pacific posts the highest forecast CAGR of 10.4% through 2030.

Why are liquid formulations expanding so quickly?

Liquids offer superior bioavailability for precision irrigation systems, driving an 11.6% CAGR despite cold-chain challenges.

How do carbon credits affect adoption?

Payments of USD 15-25 per ton CO2 captured lower effective fertilizer costs and improve project payback.

What is the biggest cost restraint?

Production costs of USD 315-500 per kilogram make microalgae fertilizers far more expensive than conventional nitrogen inputs.

Page last updated on: