Bioenzyme Fertilizer Market Size and Share

Market Overview

| Study Period | 2020 - 2030 |

|---|---|

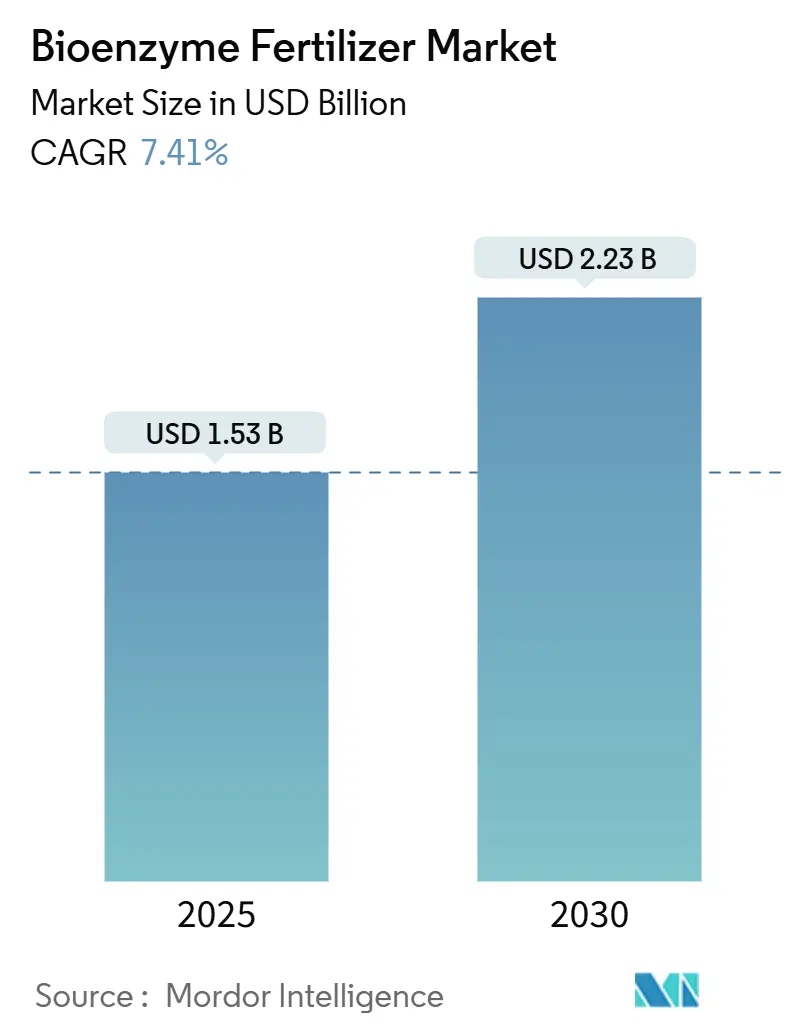

| Market Size (2025) | USD 1.53 Billion |

| Market Size (2030) | USD 2.23 Billion |

| Growth Rate (2025 - 2030) | 7.41% CAGR |

| Fastest Growing Market | Asia Pacific |

| Largest Market | Europe |

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

Bioenzyme Fertilizer Market Analysis by Mordor Intelligence

The bioenzyme fertilizer market size is valued at USD 1.53 billion in 2025 and is forecast to advance at a 7.41% CAGR, reaching USD 2.23 billion by 2030. Current expansion is propelled by regulatory incentives for residue-free production, premium pricing opportunities in specialty crops, and steady gains in carbon-credit programs that reward growers for biological inputs. Precision nutrient delivery lowers overall nutrient costs while improving soil health, prompting large farm operators to trial multi-enzyme blends on marginal soils where synthetic fertilizers no longer deliver dependable returns. Liquid formulations continue to dominate distribution channels because they integrate smoothly with fertigation and drone-spray systems, while new microencapsulation techniques extend shelf life and preserve activity across wider temperature ranges. Consolidation among global enzyme producers has improved quality control, yet moderate concentration ensures room for niche innovators that target specific crop stresses or regional soil chemistries. These combined factors are poised to make the bioenzyme fertilizer market a key driver of sustainable intensification strategies over the coming years.

Key Report Takeaways

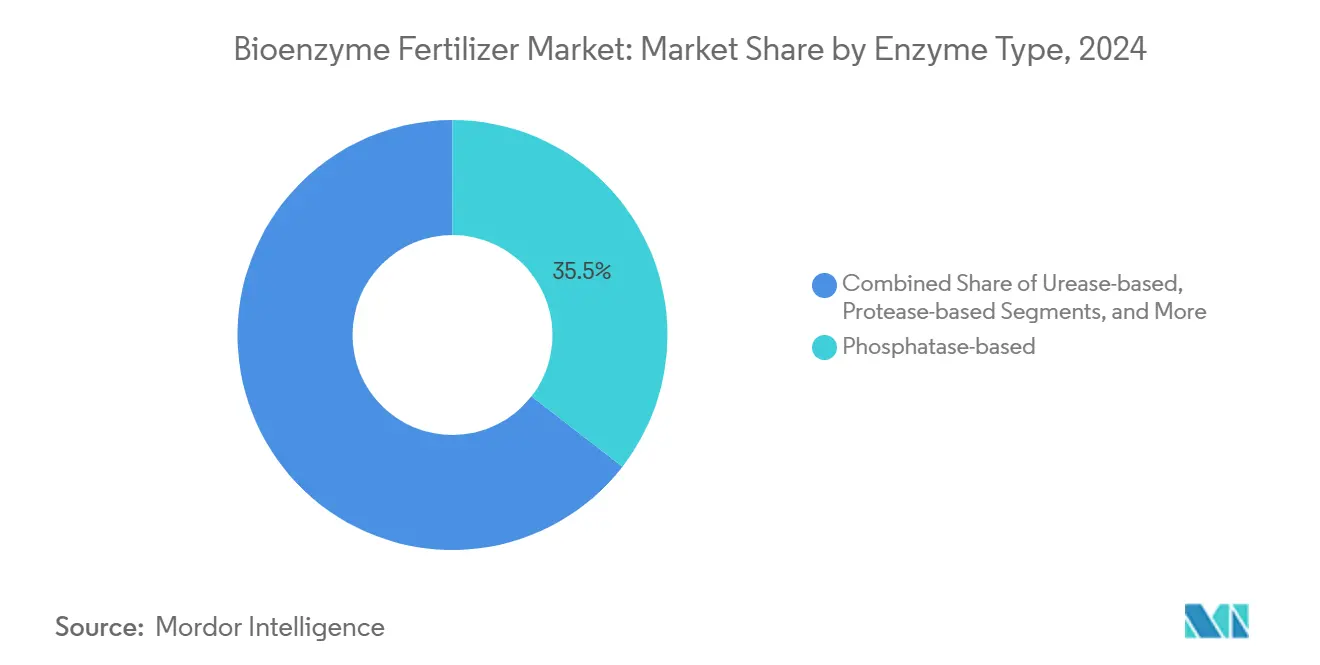

- By enzyme type, phosphatase formulations held 35.5% of the bioenzyme fertilizer market share in 2024, while urease products are forecast to expand at a 6.8% CAGR through 2030.

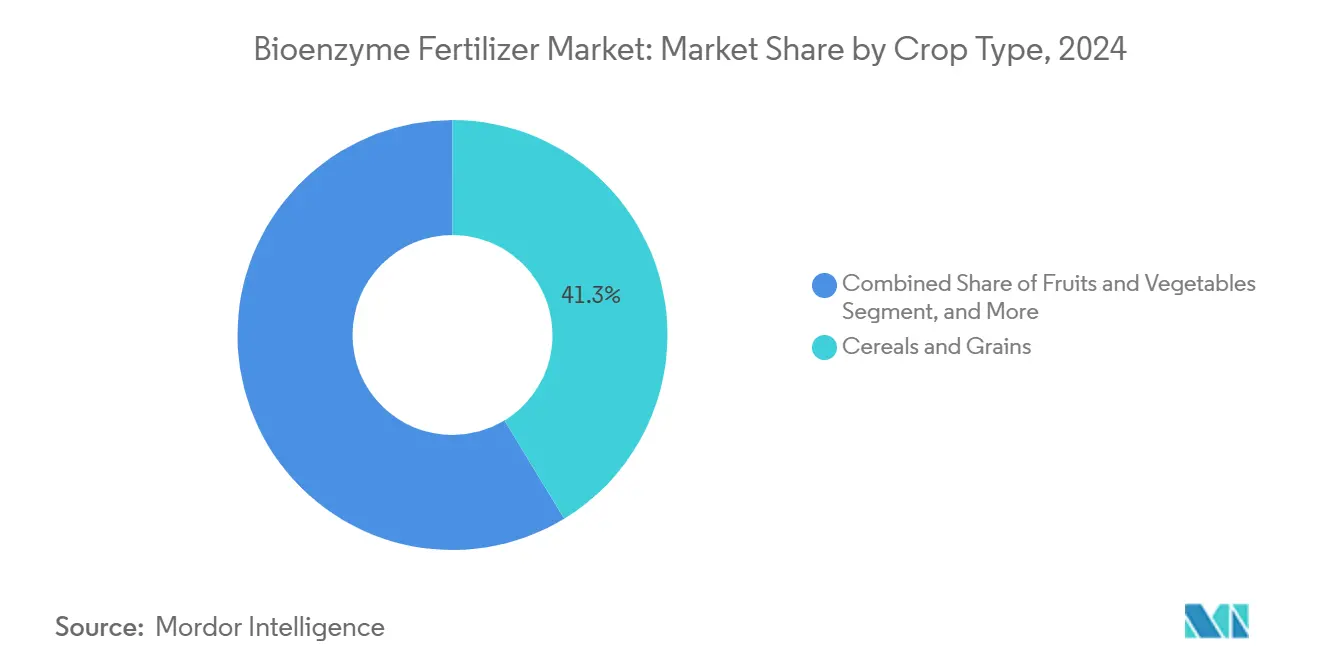

- By crop type, cereals and grains accounted for 41.3% of the bioenzyme fertilizer market size in 2024, whereas fruits and vegetables are projected to post the fastest growth at a 7.2% CAGR to 2030.

- By form, liquid products commanded 63.4% revenue share in 2024 and are projected to maintain a 7.6% CAGR on account of superior enzyme stability.

- By application method, soil treatments led with 52.1% share in 2024, but foliar sprays are rising at an 8.4% CAGR driven by precision delivery gains in protected cultivation.

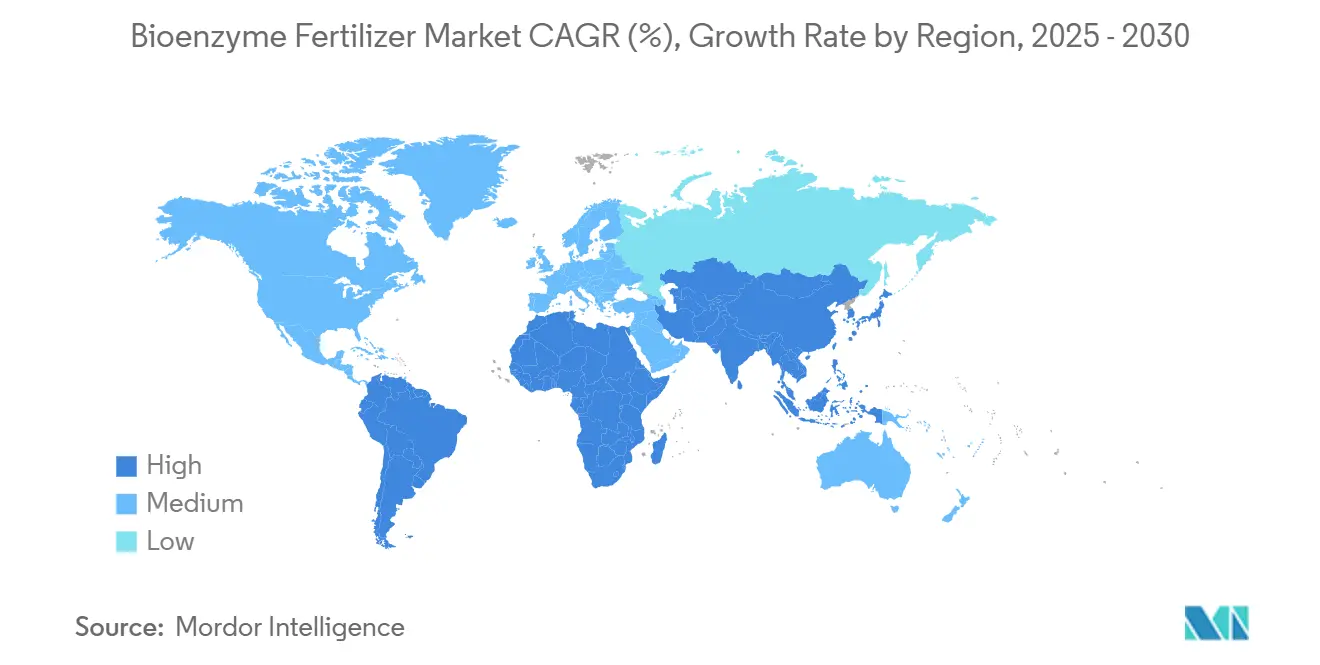

- By geography, Europe accounted for a 32.3% share in 2024, while Asia‑Pacific is projected to grow at a CAGR of 7.9% between 2025 and 2030, making it the fastest‑expanding region.

- Novonesis A/S, Corteva Agriscience, Syngenta Group, UPL Limited, and Koppert B.V. are key market players, jointly nearly half of the share of the market.

Global Bioenzyme Fertilizer Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Growing Demand for Residue-free Food | +2.1% | Global, with early gains in Europe and North America | Medium term (2-4 years) |

| Regulatory Push for Sustainable Inputs | +1.8% | Europe and North America, expanding to Asia-Pacific | Long term (≥ 4 years) |

| Cost-effective Yield Enhancement vs. Synthetic Fertilizers | +2.3% | Global, particularly in emerging markets | Short term (≤ 2 years) |

| Rapid Adoption in Protected Cultivation | +1.4% | Asia-Pacific core, spill-over to Europe and North America | Medium term (2-4 years) |

| Enzyme-enabled Nutrient Unlocking in Marginal Soils | +1.9% | Global, with focus on arid and semi-arid regions | Long term (≥ 4 years) |

| Carbon-credit Monetization for Bio-fertilizer Users | +1.2% | North America and Europe, expanding globally | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

Growing Demand for Residue-free Food

European retail chains now require zero-residue certification for various fresh produce categories, leading greenhouse tomato and cucumber producers to adopt enzyme bio-fertilizers that meet these standards while maintaining yield levels.[1]United States Department of Agriculture Natural Resources Conservation Service, “Soil Quality Physical Indicator Information Sheet Series,” nrcs.usda.gov The United States Food and Drug Administration's GRAS (Generally Recognized as Safe) status for specific Bacillus strains in enzyme production has reduced regulatory barriers and enabled faster product launches.[2]United States Food and Drug Administration, “GRAS Notices Inventory,” fda.gov European supermarkets maintain higher prices for enzyme-treated produce, offsetting the increased costs of biological formulations. This price advantage is significant in controlled environment agriculture, where accurate input management increases the profitability of enzyme-based products. The application of enzyme treatments has expanded from specialty crops to premium rice and berry production, creating additional revenue opportunities for suppliers who meet consumer demand for sustainable food products.

Regulatory Push for Sustainable Inputs

The European Union Farm to Fork strategy requires a 50% reduction in chemical pesticides by 2030, supported by Regulation 2019/1009, which standardizes bio-fertilizer regulations across member states.[3]European Parliament and Council, “Regulation (EU) 2019/1009,” eur-lex.europa.eu This regulatory framework facilitates enzyme product trade between countries and reduces approval times. The United States Environmental Protection Agency's tolerance exemptions for enzyme-producing microbes simplify the registration process, lowering development costs. China's fertilizer efficiency initiative aims for a 40% improvement by 2025, making enzymes essential for row-crop farmers to meet compliance requirements. The inclusion of enzyme-mediated soil carbon improvements in national greenhouse-gas accounting systems strengthens regulatory incentives and establishes bioenzyme fertilizer as an integral element in sustainability reporting.

Cost-effective Yield Enhancement vs. Synthetic Fertilizers

Rising energy costs increased global urea prices significantly in 2024, reducing the price difference between chemical and biological fertilizers. Research demonstrates that using phosphatase enzymes while decreasing synthetic phosphorus by 25% maintains crop yields and reduces nutrient expenses by 12-15%. Improved precision fermentation techniques have reduced microbial enzyme production costs, allowing manufacturers to offer competitive prices in emerging markets while maintaining profitability. Farmers working with nutrient-poor soils benefit additionally, as enzymes unlock previously unavailable soil phosphorus and nitrogen, decreasing fertilizer requirements. This has led to the expansion of the bioenzyme fertilizer market from organic farming segments into conventional agriculture, with agricultural cooperatives securing volume-based agreements to control input costs.

Rapid Adoption in Protected Cultivation

Controlled environment agriculture enhances biological activity through precise regulation of temperature, pH, and moisture levels, which optimize enzyme performance. Foliar enzyme applications in greenhouse conditions improve nutrient uptake efficiency compared to open-field applications. Hydroponic lettuce production shows reduced nutrient solution waste when using enzyme combinations in recirculating systems, resulting in lower water-treatment costs. The compatibility of liquid enzyme formulations with drip irrigation and fogging systems facilitates implementation. These combined benefits drive growth in the protected cultivation segment at a rate exceeding the overall bioenzyme fertilizer market. High-value crops, particularly strawberries and bell peppers, are at the forefront of this trend due to their premium retail pricing based on visual quality.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Short shelf life and cold-chain dependency | -1.7% | Global with greatest impact in developing markets | Short term (≤2 years) |

| Batch-to-batch efficacy variability | -1.3% | Global across all segments | Medium term (2-4 years) |

| Limited farmer awareness in large-acreage row crops | -1.1% | North America and South America | Medium term (2-4 years) |

| Regulatory ambiguity on enzyme vs. bio-stimulant labels | -0.8% | Global with regional differences | Long term (≥4 years) |

| Source: Mordor Intelligence | |||

Short Shelf Life and Cold-chain Dependency

Commercial liquid enzymes typically lose 50% of their activity after 18 months at ambient temperatures, requiring refrigerated distribution that increases landed product costs by 15-20% in tropical markets. Temperature variations during transport diminish field performance and reduce farmer confidence, particularly when crop responses are not immediately visible. While Evonik's silica-carrier technology extends shelf life beyond 540 days, packaging costs remain prohibitive for price-sensitive growers. Companies are testing powder and microbe-encapsulated alternatives that withstand temperature fluctuations, though these solutions have not reached commercial scale. Cold-chain constraints continue to restrict demand in remote regions, limiting the overall growth of the bioenzyme fertilizer market.

Batch-to-batch Efficacy Variability

Enzyme activity varies based on fermentation pH, nutrient feed rates, and post-processing conditions, resulting in production lot variations. These inconsistencies in field performance make it difficult to provide accurate agronomic recommendations, leading dealers to prefer established brands despite higher prices. While industry associations develop standardized bioassays and genetic markers for performance prediction, smaller manufacturers show varied adoption rates. Regulatory requirements for stability data increase compliance costs but help eliminate substandard suppliers. The gradual improvement in product uniformity is anticipated to reduce this constraint, supporting sustained growth in the bioenzyme fertilizer market.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Enzyme Type: Phosphatase Dominance Faces Urease Disruption

Phosphatase products accounted for 35.5% of the bioenzyme fertilizers market share in 2024, primarily due to their effectiveness in releasing bound phosphorus in alkaline and calcareous soils. These products demonstrate the highest adoption rates in wheat, rice, and maize cultivation systems where phosphorus fixation reduces fertilizer efficiency. The combination of increasing input costs and environmental regulations limiting nutrient runoff continues to drive farmer demand for phosphorus-releasing enzymes, maintaining steady single-digit growth in this segment.

Urease solutions are projected to grow at a CAGR of 6.8% through 2030, representing the highest growth rate among enzyme categories. Rising urea costs and the increasing focus on nitrogen use efficiency drive this growth. These enzymes reduce ammonia volatilization and extend nitrogen availability in the root zone, resulting in improved protein content in cereals and enhanced leaf chlorophyll in horticultural crops. The development of integrated products that combine urease, nitrification inhibitors, and micronutrient chelators indicates a market shift toward comprehensive nutrient management solutions. This trend toward multi-enzyme formulations is anticipated to influence market dynamics and increase revenue from premium products in the bioenzyme fertilizers market.

By Form: Liquid Formulations Drive Innovation

Liquid bioenzyme fertilizers led the market in 2024, capturing 63.4% of total revenue, and are projected to maintain a strong 7.6% CAGR through 2030. Their dominance is attributed to superior enzyme stability in carrier fluids that remain effective across broad pH ranges. Liquids blend seamlessly with fertigation systems and UAV tanks, enabling frequent, low-dose applications that reduce enzyme degradation in soil. Encapsulation technologies now protect enzymes from UV radiation and mechanical stress during pumping, expanding geographic reach, and enhancing performance in high-value crops.

Granular and powder forms retain niche relevance in cost-sensitive and remote regions where cold-chain logistics are impractical. Priced 20–30% lower than liquids, they appeal to large-scale row-crop operations, though challenges like uneven dissolution and wind-driven distribution persist. Manufacturers are experimenting with clay-based carriers that swell upon moisture contact to release enzymes gradually, but commercialization remains limited. Liquid‑based innovations are emerging as the primary force propelling growth in the bioenzyme fertilizer market, while dry formats continue to play more targeted roles. Their advantages make liquid solutions especially influential in precision agriculture and protected cultivation systems, where efficiency and rapid nutrient delivery are essential.

By Crop Type: Cereals Leadership Challenged by Specialty Segments

Cereals and grains accounted for 41.3% of the bioenzyme fertilizers market size in 2024, driven by extensive treated acreage and established cooperative distribution networks. Large-scale farms benefit from the compatibility of enzyme liquid formulations with existing sprayer equipment, enabling broad field applications without significant infrastructure investments. The presence of established crop insurance programs reduces adoption risks in temperate regions, ensuring consistent demand levels.

The fruits and vegetables segment is projected to grow at a 7.2% CAGR, supported by organic and premium produce markets that command higher prices for residue-free products. Greenhouse tomato and cucumber production demonstrates increased adoption rates due to controlled environments enhancing enzyme effectiveness. Berry producers utilize foliar applications to improve anthocyanin development and extend shelf life. The higher returns in these specialty crops enable growers to implement subscription-based procurement models for consistent enzyme supply throughout growing seasons. This growth in specialty crops is reducing the market share gap with cereals and will significantly influence the bioenzyme fertilizer market through 2030.

By Application Method: Soil Treatment Leads While Foliar Gains

Soil treatments accounted for 52.1% of the revenue share in 2024, as growers primarily incorporate biologicals during planting or side-dressing operations for operational efficiency. The extended soil contact period optimizes phosphatase interaction with mineral complexes, enabling phosphorus release throughout the plant growth cycle. The adoption of drip irrigation systems enables precise, frequent enzyme application in the rhizosphere, improving nutrient uptake efficiency.

Foliar spray applications are experiencing an 8.4% CAGR, driven by the adoption of drone technology and electrostatic sprayers that enhance canopy coverage and reduce application costs. The rapid nutrient absorption through leaf stomata produces visible plant responses within days, increasing farmer adoption rates. Seed treatment applications represent a smaller market segment but show significant growth potential, as polymer coatings preserve enzyme stability during storage while ensuring activation during germination. Products such as BioWake demonstrate enhanced root development and nutrient uptake efficiency in early growth stages. These developments in application methods are diversifying the bioenzyme fertilizer market revenue streams.

Geography Analysis

Europe held a 32.3% of the bioenzyme fertilizer market share in 2024, supported by comprehensive policy frameworks and standardized regulations that facilitate cross-border trade. Germany and France's agricultural sectors support extensive demonstration programs showcasing enzyme effectiveness across various soil conditions, while Spain's greenhouse industry drives adoption of foliar applications in vegetable production. Government incentives for sustainable farming practices reduce implementation costs, while established cold-chain infrastructure ensures product quality during transport. These factors contribute to high customer retention rates and establish operational benchmarks for other regions.

Asia-Pacific is projected to achieve a 7.9% CAGR from 2025 to 2030, driven by China's policies to reduce fertilizer intensity and India's BioE3 program that provides incentives for biotechnology inputs. Southeast Asian small-scale farmers implement micro-dosing strategies to optimize limited resources while improving productivity, and Japanese horticultural companies target premium fruit exports requiring chemical-free certification. Australia's agricultural sector benefits from collaboration between academic institutions and farming cooperatives in enzyme testing for wheat-sheep farming systems. While rural infrastructure remains underdeveloped in certain areas, widespread mobile technology enables digital platforms to share implementation guidelines and improve adoption rates.

North America represents an established market where clear regulations and carbon trading programs encourage innovation. United States farmers adopt complex enzyme formulations compatible with precision agriculture systems, while Canada's expansion of organic farming increases demand for certified products. Mexico's greenhouse operations, supplying vegetables to the United States, benefit from established cold-chain transportation networks that also serve the flower industry. In South America, Brazil and Argentina are demonstrating increasing interest in enzymes for phosphorus mobilization in weathered soils, although implementation varies due to differences in agricultural support services. Agricultural input companies are creating integrated financing and product packages, indicating significant growth potential for the bioenzyme fertilizer market.

Competitive Landscape

The bioenzyme fertilizer market is moderately concentrated, with the top five players accounting for 50% of the bioenzyme fertilizer market share. Novonesis A/S maintains a significant market share through its extensive microbial strain libraries and fermentation infrastructure, enabling the development of region-specific formulations for local soil conditions. Koppert B.V. expanded its operations with a EUR 140 million (USD 152.6 million) investment from HAL Investments in February 2024, to increase production capacity and expand sales operations in Asia-Pacific markets. American Vanguard Corporation integrates enzyme products into its crop-protection portfolio through its GreenSolutions platform, creating cross-selling opportunities to strengthen dealer loyalty and market reach.

Partnerships between enzyme developers and irrigation technology companies enhance field-level performance through synchronized delivery systems. Smaller companies enter the market through licensing agreements for encapsulation technologies, bypassing the need for internal formulation capabilities. While microbial strain patents present significant entry barriers, open-innovation programs facilitate collaborative development of enzymes for saline and acidic soils, contributing to the bioenzyme fertilizer market size in regions where traditional fertilizers are less effective.

Global companies pursue scale advantages while regional firms succeed in niche markets such as protected cultivation and specialty crops, where agronomic services take precedence over price considerations. The market emphasizes product efficacy and shelf-life improvements rather than price competition, maintaining strong gross margins. This approach, combined with increasing demand for sustainable agriculture, government support, and advances in enzyme delivery and formulation, drives steady market growth.

Bioenzyme Fertilizer Industry Leaders

Novonesis A/S

Corteva Agriscience

Syngenta Group

UPL Limited

Koppert B.V.

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- January 2025: American Vanguard expanded its bioenzyme fertilizer portfolio through a partnership with DPH Biologicals. The agreement incorporated TerraTrove SP-1 Classic and AmplAphex into its GreenSolutions product line, strengthening its soil health offerings and supporting sustainable agriculture through enzyme-based nutrient solutions in regional markets.

- January 2025: Koppert deepened its bioenzyme fertilizer market reach by expanding its partnership with Acadian Plant Health. The collaboration targets Europe, the Middle East, and Africa, combining microbial and biostimulant technologies to deliver sustainable, enzyme-driven crop solutions tailored to diverse agronomic conditions and regional farming needs.

- September 2024: Elemental Enzymes partnered with AgIdea to enhance field screening of enzyme-based technologies for row crops. This collaboration advances bioenzyme biofertilizer development, with emphasis on nutrient efficiency, stress tolerance, and specialized fertility trials. These factors drive sustainable agriculture practices and microbial input adoption throughout the Americas.

- June 2024: BASF SE completed the sale of its bioenergy bioenzymes business to Lallemand, which included the transfer of Spartec technologies. This acquisition enhanced Lallemand's enzyme capabilities and supports bioenzyme biofertilizer innovation through combined R&D efforts, microbial expertise, and fermentation platforms focused on sustainable agriculture and soil health solutions.

Global Bioenzyme Fertilizer Market Report Scope

| Protease-based |

| Phosphatase-based |

| Urease-based |

| Others (Cellulase, Lipase, etc.) |

| Cereals and Grains |

| Fruits and Vegetables |

| Oilseeds and Pulses |

| Turf and Ornamentals |

| Liquid |

| Granular/Powder |

| Soil Treatment |

| Seed Treatment |

| Foliar Spray |

| North America | United States |

| Canada | |

| Mexico | |

| Rest of North America | |

| Europe | Germany |

| France | |

| Spain | |

| Russia | |

| Rest of Europe | |

| Asia-Pacific | China |

| India | |

| Japan | |

| Australia | |

| Rest of Asia-Pacific | |

| South America | Brazil |

| Argentina | |

| Chile | |

| Rest of South America | |

| Middle East | United Arab Emirates |

| Saudi Arabia | |

| Turkey | |

| Rest of Middle East | |

| Africa | South Africa |

| Rest of Africa |

| By Enzyme Type | Protease-based | |

| Phosphatase-based | ||

| Urease-based | ||

| Others (Cellulase, Lipase, etc.) | ||

| By Crop Type | Cereals and Grains | |

| Fruits and Vegetables | ||

| Oilseeds and Pulses | ||

| Turf and Ornamentals | ||

| By Form | Liquid | |

| Granular/Powder | ||

| By Application Method | Soil Treatment | |

| Seed Treatment | ||

| Foliar Spray | ||

| By Geography | North America | United States |

| Canada | ||

| Mexico | ||

| Rest of North America | ||

| Europe | Germany | |

| France | ||

| Spain | ||

| Russia | ||

| Rest of Europe | ||

| Asia-Pacific | China | |

| India | ||

| Japan | ||

| Australia | ||

| Rest of Asia-Pacific | ||

| South America | Brazil | |

| Argentina | ||

| Chile | ||

| Rest of South America | ||

| Middle East | United Arab Emirates | |

| Saudi Arabia | ||

| Turkey | ||

| Rest of Middle East | ||

| Africa | South Africa | |

| Rest of Africa | ||

Key Questions Answered in the Report

What is the forecast size of the bioenzyme fertilizer market by 2030?

The bioenzyme fertilizer market is projected to reach USD 2.23 billion by 2030, reflecting a 7.41% CAGR from 2025.

Which enzyme type is growing the fastest in commercial agriculture?

Urease formulations are expanding at a 6.8% CAGR because they improve nitrogen use efficiency amid rising urea prices.

How do bioenzyme fertilizers generate additional farm revenue?

Verified carbon-credit programs pay growers USD 50-100 per hectare annually for soil-carbon gains linked to enzyme applications.

Why are liquid enzyme formulations preferred over granular alternatives?

Liquids blend easily with fertigation and drone sprayers, offer superior enzyme stability, and support precise low-volume dosing.

Which region is anticipated to grow the quickest in bioenzyme fertilizer adoption?

Asia-Pacific is forecast to post a 7.9% CAGR through 2030, driven by policy incentives in China and India.

How concentrated is the supplier landscape for bioenzyme fertilizers?

The top five companies control nearly half of global revenue, indicating moderate concentration with ample room for specialists.

Page last updated on: