Market Overview

| Study Period | 2021 - 2031 |

|---|---|

| Forecast Data Period | 2026 - 2031 |

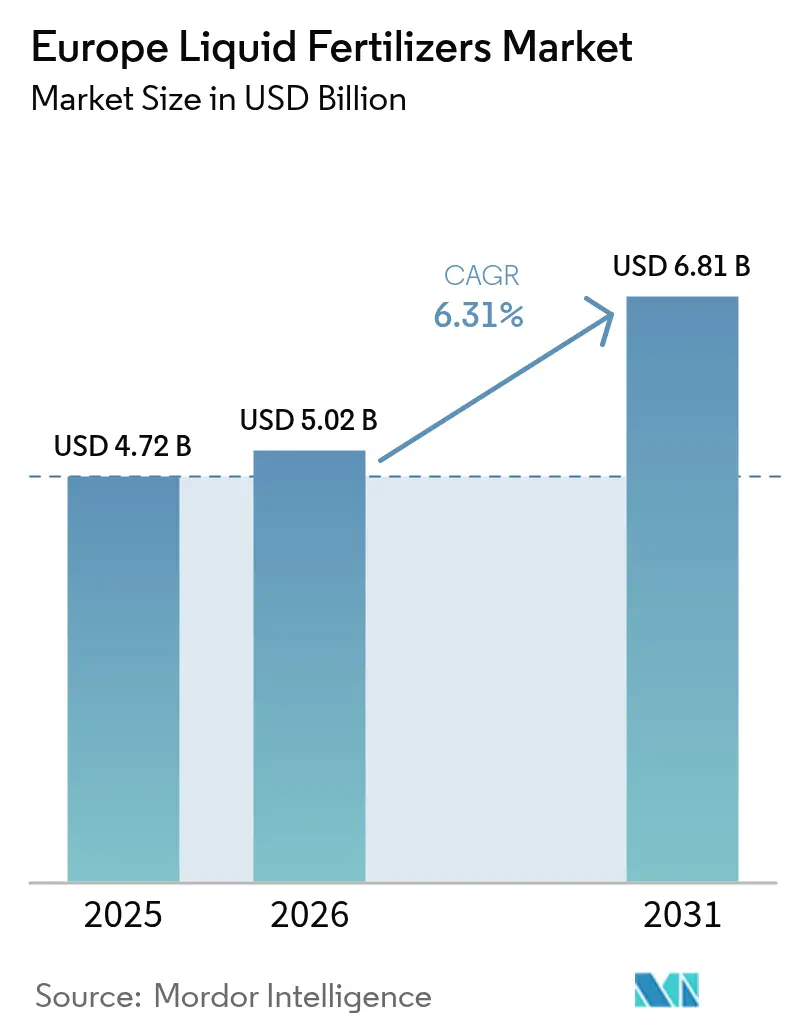

| Base Year Market Size (2025) | USD 4.72 Billion |

| Market Size (2026) | USD 5.02 Billion |

| Market Size (2031) | USD 6.81 Billion |

| Growth Rate (2026 - 2031) | 6.31% CAGR |

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

Europe Liquid Fertilizers Market Analysis by Mordor Intelligence

Europe liquid fertilizers market size in 2026 is estimated at USD 5.02 billion, growing from 2025 value of USD 4.72 billion with 2031 projections showing USD 6.81 billion, growing at 6.31% CAGR over 2026-2031. Rising adoption of precision-farming tools, mounting pressure to curb nutrient losses, and common agricultural policy (CAP) linked eco schemes have aligned policy and profitability objectives, accelerating demand for high-efficiency liquid formulations. Contracting arable land per capita in core Western economies, combined with strict water-quality limits, pushes growers toward fertigation systems that maximize nutrient-use efficiency. Technology-driven innovations, such as in-line micro-dosing valves, cloud-connected flow meters, and GPS-guided sprayers, are achieving double-digit adoption growth in greenhouse hubs where the common agricultural policy (CAP) accounts for an outsized share of discretionary spending on crop inputs. Parallel investment in low-carbon ammonia and nitrate production positions domestic manufacturers to offset the cost impact of the incoming Carbon Border Adjustment Mechanism, safeguarding long-term supply for the Europe liquid fertilizers market.

Key Report Takeaways

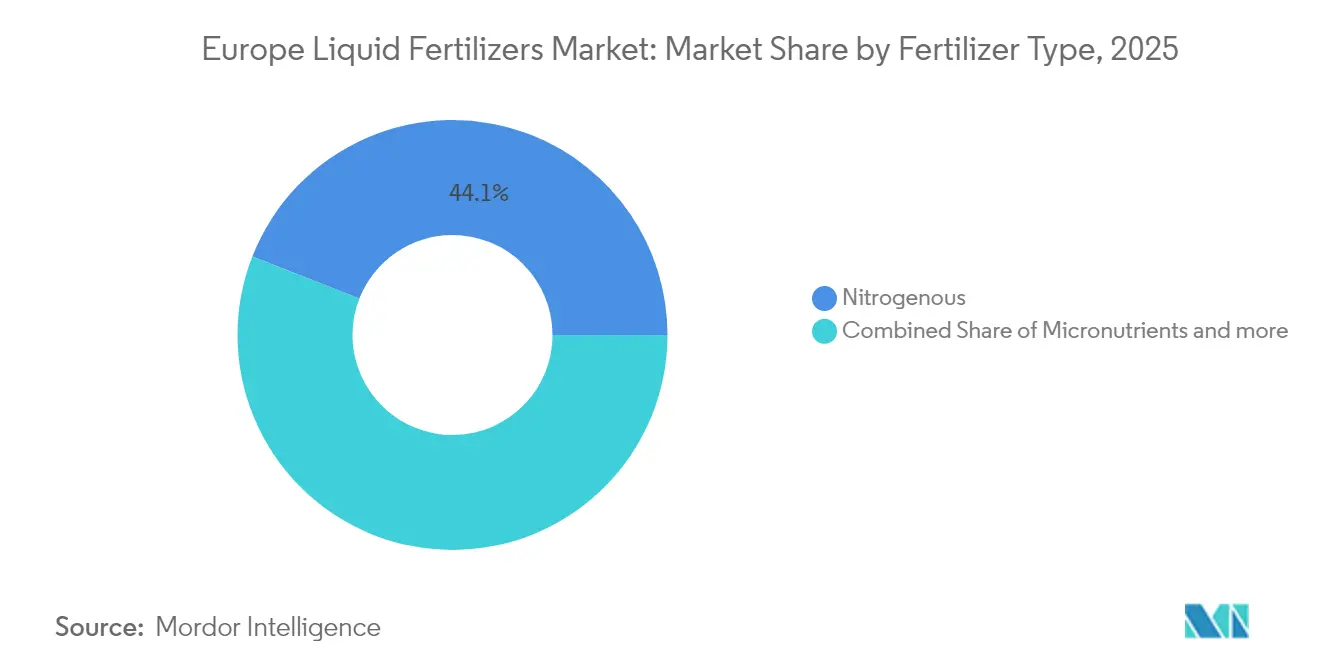

- By fertilizer type, nitrogenous products captured 44.05% of the Europe liquid fertilizers market share in 2025, while micronutrients are advancing at an 8.22% CAGR through 2031.

- By mode of application, fertigation commanded 50.62% of the market size in 2025, with foliar application expanding at a 8.86% CAGR to 2031.

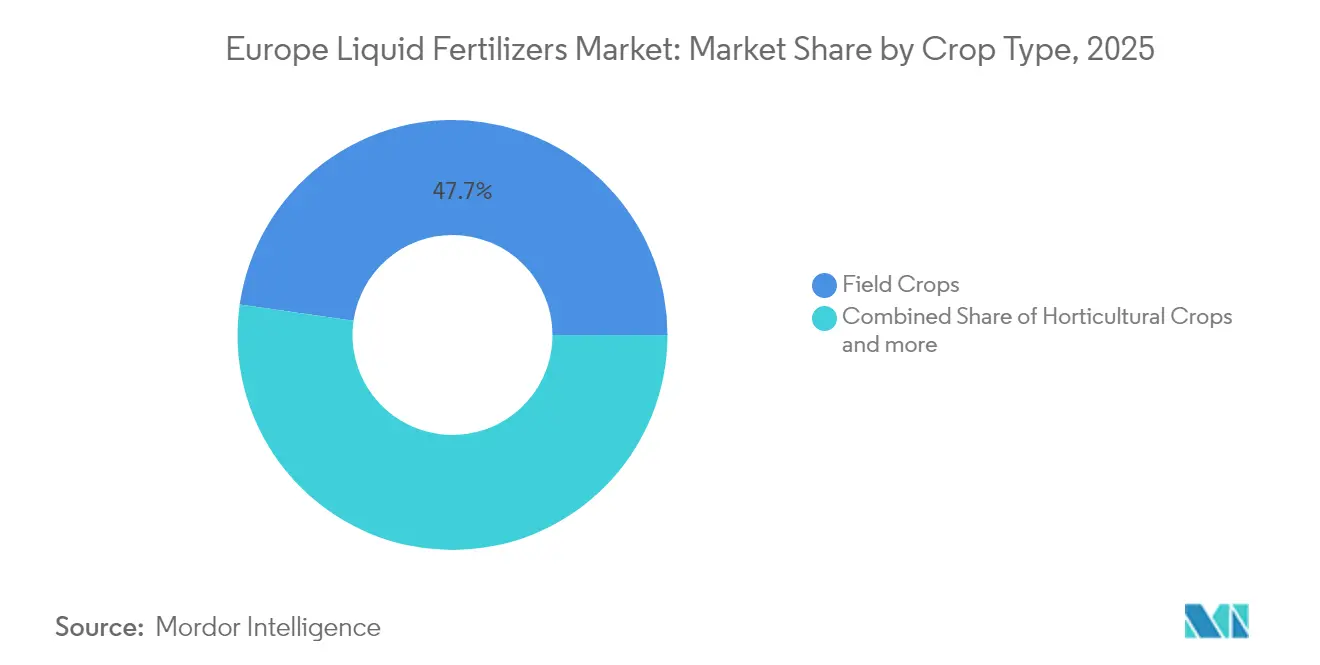

- By crop type, field crops held 47.74% of the Europe liquid fertilizers market size in 2025, while horticultural crops are progressing at a 7.46% CAGR to 2031.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of 2026.

Europe Liquid Fertilizers Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Precision-farming yield optimization | +1.8% | Netherlands, Germany, and France | Medium term (2-4 years) |

| Shrinking arable land per capita | +1.2% | Western Europe, notably Netherlands and Belgium | Long term (≥ 4 years) |

| Government Common Agricultural Policy (CAP) reform incentives | +1.5% | All EU member states, led by France and Germany | Short term (≤ 2 years) |

| Surge in controlled-release micro-dosing systems | +0.9% | Netherlands, Spain, Germany greenhouse regions | Medium term (2-4 years) |

| Pivot to low-salt greenhouse nutrition | +0.7% | Netherlands, Spain, and Belgium | Medium term (2-4 years) |

| Corporate net-zero fertilizer road-maps | +0.6% | EU-wide, strongest in Germany and France | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

Precision-Farming Yield Optimization

Variable-rate liquid fertilizer application systems are transforming European precision agriculture, delivering nitrogen use efficiency improvements of 15-20% compared to broadcast solid applications. The combination of GPS-guided sprayers with real-time soil sensing technology enables field-specific nutrient application that aligns with crop uptake patterns, minimizing over-application in low-productivity zones while maintaining optimal nutrition in high-yield areas. The Netherlands leads in precision farming adoption, with over 60% of commercial growers implementing these technologies due to land constraints and strict environmental regulations on nutrient losses. The European Commission's Digital Europe Programme has allocated EUR 1.3 billion (USD 1.4 billion) for digital transformation initiatives in 2024, with substantial funding directed toward agricultural digitalization projects supporting precision fertilizer management[1]Source: European Commission, “Digital Europe Programme,” digital-strategy.ec.europa.eu .

Shrinking Arable Land Per Capita

The European agricultural land base is declining by 0.3% annually due to urbanization and climate-related productivity losses, increasing the demand for high-analysis liquid fertilizers to maximize nutrient delivery per hectare. In Spain, arable land per capita decreased from 0.24 hectares in 2020 to 0.25 hectares in 2024, compelling farmers to optimize productivity through intensive liquid fertilization programs. These land constraints drive the adoption of concentrated liquid formulations containing over 400 kg N+P2O5+K2O per cubic meter, which reduces storage needs while maintaining application flexibility. In 2024, Belgium's protected horticulture sector increased its liquid fertilizer consumption by 18% as growers transitioned to soilless production systems that depend on liquid nutrient solutions[2]Source: OECD/FAO, “OECD-FAO Agricultural Outlook 2024-2033,” doi.org . The need to maximize returns per unit area continues to generate demand for high-performance liquid formulations that support intensive cropping systems and year-round production.

Government Common Agriculture Practices (CAP) Reform Incentives

The 2023-2027 Common Agricultural Policy (CAP) eco-schemes mark a significant change in European agricultural subsidies by incentivizing environmentally sustainable farming practices, including precision liquid fertilizer application. The programs offer direct payments ranging from EUR 50-150 per hectare (USD 55-165 per hectare) to farmers who implement nutrient management plans that reduce runoff and improve soil health. France has allocated EUR 2.1 billion (USD 2.3 billion) to CAP eco-schemes in 2024. Liquid fertigation systems qualify for higher payment rates due to their precise nutrient placement and lower volatilization losses. In sensitive watersheds, the policy framework prioritizes liquid formulations over granular alternatives, creating regulatory-driven demand. German farmers participating in eco-schemes demonstrated this trend with 23% higher adoption rates of liquid fertilizer systems in 2024, indicating the impact of policy incentives on market adoption[3]Source: European Commission, “CAP 2023-27,” agriculture.ec.europa.eu.

Surge In Controlled-Release Micro-Dosing Systems

In-line dosing valves and controlled-release injection systems improve liquid fertilizer application by enabling precise nutrient delivery that aligns with plant uptake patterns during the growing season. The Netherlands focuses on reducing fertilizer losses using micro-dosing systems compared to conventional fertigation schedules, resulting in better crop uniformity and yield quality. These systems connect to existing irrigation infrastructure to provide automated nutrient delivery based on plant growth stage, environmental conditions, and soil moisture levels, which reduces labor costs and optimizes fertilizer efficiency. The technology adoption is increasing in Spain's intensive horticulture regions, where water scarcity and environmental regulations necessitate precision application methods that reduce waste and environmental impact.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Organic-farming acreage targets | -1.4% | Austria, Sweden, and Denmark | Long term (≥ 4 years) |

| High logistics costs for bulk liquids | -0.8% | Eastern Europe and island territories | Short term (≤ 2 years) |

| European Union carbon-border adjustment levy risk | -0.6% | Import-reliant Eastern markets | Medium term (2-4 years) |

| Emerging biologic foliar alternatives | -0.5% | Western Europe premium segments | Medium term (2-4 years) |

| Source: Mordor Intelligence | |||

Organic-Farming Acreage Targets

Under the European Union's Farm to Fork Strategy, the target for organic farmland has been set to rise from 10.5% in 2022 to 25% by 2030. This shift poses challenges for the demand for synthetic liquid fertilizers, as organic producers turn to biological and mineral-based nutrition sources. Austria leads this transition with 26.5% organic acreage in 2024, followed by Sweden at 20.8%, demonstrating the feasibility of large-scale organic conversion that reduces synthetic fertilizer consumption. The organic transition process typically involves a 3-year conversion period during which farmers gradually reduce synthetic inputs while building soil biological activity, creating temporary demand destruction for liquid fertilizers in converting regions. The net market impact varies by region, with intensive agricultural areas like Spain, France, Germany, Italy, and the United Kingdom maintaining strong liquid fertilizer demand despite organic expansion, while extensive farming regions experience more pronounced demand reduction.

High Logistics Costs for Bulk Liquids

Transportation costs for liquid fertilizers have increased 12% annually since 2022, driven by fuel price volatility and specialized handling requirements that limit shipping flexibility compared to solid fertilizers. Bulk liquid transport requires dedicated tank trucks and rail cars that cannot be easily repurposed for other cargo, creating capacity constraints during peak application seasons that drive up freight rates. The Bertschi Group's specialized liquid chemical transport network demonstrates the infrastructure requirements for efficient liquid fertilizer distribution, but capacity limitations during spring application periods create bottlenecks that constrain market growth. Regional storage and blending facilities are emerging as strategic assets to reduce transport costs and improve supply chain flexibility, though the capital requirements limit investment to larger players with sufficient scale economies.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Fertilizer Type: Nitrogenous Products Sustain Dominance

The nitrogenous category retained 44.05% of the 2025 market share within the Europe liquid fertilizers market, underscoring the centrality of nitrogen management to cereal and rapeseed output. Extensive compatibility with variable-rate controllers assures ongoing share stability even as CAP (Common Agricultural Policy) revisions tighten ammonia-emission caps. Complex liquids appeal to mixed farms looking for one-pass nutrient delivery, while straight micronutrient blends tackle localized trace-element gaps.

As soil tests increasingly reveal zinc and boron deficiencies threatening grain quality, the micronutrient niche, growing at an 8.22% CAGR, stands to gain. Producers are rolling out chelated iron and Ethylenediaminetetraacetic acid (EDTA)-zinc liquids that command 15-20% price premiums over commodity grades, buoying value growth within the Europe liquid fertilizers market size. Specialty potassium phosphite lines are similarly targeting root-disease suppression, adding functional agronomy benefits that extend market reach beyond nutrition alone. Collectively, these advances cement the fertilizer-type segment as a prime arena for premiumization strategies that enlarge the Europe liquid fertilizers market.

By Mode of Application: Fertigation Leads, Foliar Rises Quickly

Fertigation systems delivered 50.62% of the 2025 market size as greenhouses and irrigated orchards integrate nutrient and water control into a single platform. Micro-sprinkler and drip lines blend liquid concentrates on the fly, achieving 20–30% savings against broadcast methods and curbing leaching in nitrate-vulnerable zones. Government water-efficiency grants further accelerate uptake, anchoring fertigation’s hold on the Europe liquid fertilizers market share.

Foliar application, while smaller nowadays, posts a 8.86% CAGR to 2031, fueled by specialty growers chasing rapid deficiency correction and fruit-finish quality enhancements. Advanced surfactant packages boost leaf-adhesion and cut evaporation loss, expanding foliar scope from micronutrient rescue to macronutrient supplementation during grain-fill stages. Equipment vendors now bundle variable-rate sprayers with handheld chlorophyll meters, tightening feedback loops that ensure precise timing. The dual-path growth of fertigation and foliar channels diversifies revenue and cushions the Europe liquid fertilizers market from input-price volatility.

By Crop Type: Horticulture Fastest, Field Crops Largest

Field crops represented 47.74% of the Europe liquid fertilizers market size in 2025, reflecting the region’s vast wheat, barley, and rapeseed acreage. Task-specific agronomy drives adoption, where in split N-applications tailored to phenology sustain yields while keeping nitrate-runoff penalties at bay. In a bid to strengthen loyalty in this high-volume channel, service providers are now offering comprehensive nutrient-mapping packages. These packages seamlessly integrate soil scanning, advanced recommendation algorithms, and tailored nutrient blends. Field crop applications are evolving toward variable-rate systems that optimize nitrogen application based on soil variability and yield potential mapping, reducing input costs while maintaining productivity.

Horticultural crops represent the fastest-growing segment at 7.46% CAGR through 2031, driven by expanding greenhouse production, specialty vegetable cultivation, and fruit production systems that demand precise nutrient management and premium crop quality. The horticultural segment's rapid expansion reflects consumer demand for year-round fresh produce and the economic advantages of controlled-environment agriculture in European markets with high land costs and environmental constraints.

Geography Analysis

Germany and France together contribute about 34% of regional consumption as large farms pursue yield insurance in the face of tightening nitrate-directive thresholds. State subsidies for variable-rate technology and low-carbon fertilizer procurement create a robust pull-through effect that anchors the Europe liquid fertilizers market. The Netherlands, despite limited land, wields outsized influence on technology trends. Its greenhouse complexes average nutrient-use efficiencies 40% above the EU mean, setting benchmarks widely emulated from Denmark to Poland. Dutch R&D clusters channel EUR 5.2 billion (USD 5.7 billion) into controlled-environment agriculture, amplifying upstream orders for precision fertigation concentrates.

Spain and Italy represent high-growth markets driven by expanding irrigated agriculture and specialty crop production that demands precise nutrient management. Spain's Mediterranean climate and water scarcity issues favor liquid fertilizer systems that integrate with efficient irrigation technologies, while Italy's diverse agricultural landscape, from intensive Po Valley operations to specialized southern fruit production, creates varied demand patterns. Eastern European markets, including Poland and the Czech Republic, show accelerating adoption as EU accession benefits and Common Agricultural Policy (CAP) subsidies support agricultural modernization and precision farming technology investments. The region's lower labor costs and expanding agricultural exports create economic incentives for productivity-enhancing liquid fertilizer adoption.

The United Kingdom maintains stable growth post-Brexit by mirroring European Union nitrate rules while experimenting with carbon-contracting schemes that favor low-emission liquid formulations. Nordic countries prioritize organic acreage expansion, tempering volume growth yet supporting niche demand for certified liquid nutrient solutions. Collectively, geographic diversity cushions cyclicality and stabilizes revenue streams for participants in the Europe liquid fertilizers market.

Competitive Landscape

The European liquid fertilizers market exhibits moderate fragmentation, with players including Yara International ASA, EuroChem Group AG, ICL Group Ltd, CF Industries Holdings Inc., and Grupa Azoty S.A. Market leaders leverage vertical integration strategies that span raw material production, formulation, and distribution networks, while smaller players capture value through specialized products and localized service capabilities. Technology adoption serves as a key competitive differentiator, with companies investing in precision application systems, controlled-release formulations, and digital agriculture platforms that enhance customer relationships and command premium pricing.

Strategic alliances redefine competitive lines. FertigHy’s green-ammonia complex, backed by InVivo, positions French agriculture for a ten-percent domestic supply of low-carbon nitrogen by 2030, shifting purchasing power toward players that secure early offtake contracts. Anglo American deepened distribution rights with Cefetra for POLY4, injecting a multi-nutrient polyhalite contender into a market historically dominated by NPK solutions. Patent filings around micro-encapsulation and controlled-release processes surged 18% in 2024 at the European Patent Office, signaling continued R&D intensity.

With the ISO 14064 greenhouse-gas certificate and REACH compliance in hand, businesses can navigate cross-border trade effortlessly. In contrast, smaller importers face the threat of margin erosion as Carbon Border Adjustment Mechanism (CBAM) tariffs come into play. Digital agronomy platforms act as sticky customer interfaces; firms bundling soil sensors, remote scouting, and tailored liquid blends record higher renewal rates. The competitive field remains dynamic, with Mergers &Acquisitons watchlists focusing on regional blenders that add last-mile logistics capacity to serve the fast-evolving Europe liquid fertilizers market.

Europe Liquid Fertilizers Industry Leaders

Yara International ASA

EuroChem Group AG

ICL Group Ltd

CF Industries Holdings Inc.

Grupa Azoty S.A.

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- September 2024: Grupa Azoty S.A. launched an improved version of its RSM (urea-ammonium nitrate solution), a widely used urea-ammonium nitrate solution. This new formulation, called RSM OPTIMA, is enriched with copper, boron, and molybdenum.

- April 2024: Yara International ASA launched YaraVita B-Phos, a novel foliar liquid fertilizer for legumes, in Germany. This product contains phosphorus and boron nutrients along with bioactive compounds, including alkanolamine salts and algae extracts rich in phytohormones.

- April 2024: Grupa Azoty S.A. has finalized contracts in the Agro segment for the 2024/2025 season. The company has signed 66 agreements with its authorized distribution network for the domestic fertilizer market. Through this partnership, the company aims to increase the supply of liquid fertilizers in the European and global markets.

Europe Liquid Fertilizers Market Report Scope

Liquid fertilizers are concentrates or water-soluble powders of synthetic chemicals of nitrogen, phosphorus, potassium, secondary macronutrients, and other micronutrient. The European liquid fertilizer market is segmented by Complex, Straight (Micronutrients, Nitrogenous, Phosphatic, Potassic, and Secondary Macronutrients), Mode of Application (Fertigation and Foliar application, Crop Type (Field crops, Horticultural crops, and Turf and Ornamental crops), and Geography (France, Italy, Germany, Netherlands, Russia, Spain, Ukraine, United Kingdom, and Rest of Europe). For each segment, the market sizing and forecasts have been done based on value (USD).

By Fertilizer Type

| Complex | |

| Straight | Micronutrients |

| Nitrogenous | |

| Phosphatic | |

| Potassic | |

| Secondary Macronutrients |

By Mode of Application

| Fertigation |

| Foliar Application |

By Crop Type

| Field Crops |

| Horticultural Crops |

| Turf and Ornamental Crops |

By Geography

| France |

| Germany |

| Italy |

| Netherlands |

| Russia |

| Spain |

| United Kingdom |

| Ukraine |

| Rest of Europe |

| By Fertilizer Type | Complex | |

| Straight | Micronutrients | |

| Nitrogenous | ||

| Phosphatic | ||

| Potassic | ||

| Secondary Macronutrients | ||

| By Mode of Application | Fertigation | |

| Foliar Application | ||

| By Crop Type | Field Crops | |

| Horticultural Crops | ||

| Turf and Ornamental Crops | ||

| By Geography | France | |

| Germany | ||

| Italy | ||

| Netherlands | ||

| Russia | ||

| Spain | ||

| United Kingdom | ||

| Ukraine | ||

| Rest of Europe | ||

Key Questions Answered in the Report

How large is the Europe liquid fertilizers market in 2026?

The market is valued at USD 5.02 billion in 2026.

What is the projected CAGR for Europe liquid fertilizers through 2031?

31% CAGR is forecast for 2026-2031.

Which fertilizer type leads European liquid sales?

Nitrogenous solutions hold 44.05% of 2025 revenue.

Why is fertigation preferred over broadcast application?

Fertigation pairs nutrients with irrigation, cutting runoff by up to 30% and enhancing crop response.

How will the Carbon Border Adjustment Mechanism influence supply?

CBAM raises costs on high-carbon imports, benefiting domestic producers investing in low-carbon ammonia lines.

Which segment shows the fastest growth?

Foliar application is advancing at 8.86% CAGR due to specialty crop adoption.

Page last updated on: