United States Seaweed Fertilizers Market Size and Share

Market Overview

| Study Period | 2020 - 2030 |

|---|---|

| Forecast Data Period | 2025 - 2030 |

| Historical Data Period | 2020 - 2023 |

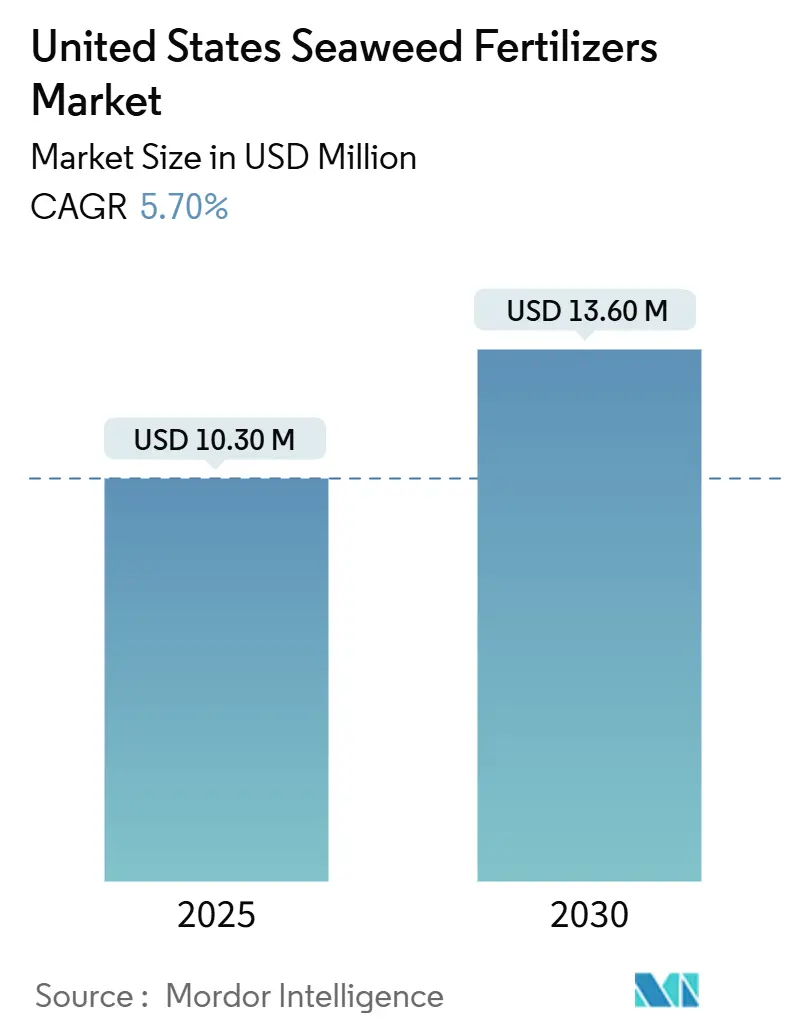

| Market Size (2025) | USD 10.30 Million |

| Market Size (2030) | USD 13.60 Million |

| Growth Rate (2025 - 2030) | 5.70% CAGR |

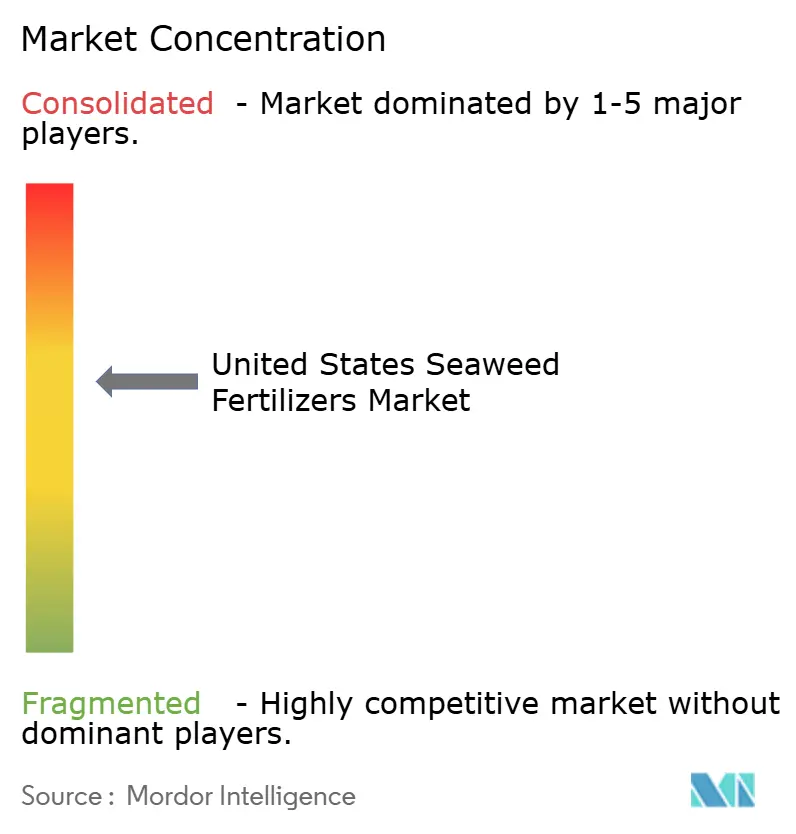

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

United States Seaweed Fertilizers Market Analysis by Mordor Intelligence

The United States seaweed fertilizers market size reached USD 10.3 million in 2025 and is projected to increase to USD 13.6 million by 2030, registering a steady 5.7% CAGR during the forecast period. This positive trajectory reflects the segment’s alignment with the broader fertilizer sector, as organic agriculture sales rose to USD 69.7 billion in 2023, even as certified acreage fell by 10.9% prior to 2023. Liquid formulations currently dominate the seaweed fertilizers market due to widespread retail and on-farm familiarity; however, powder and granule innovations are closing the gap, driven by lower freight costs and compatibility with fertigation. Brown seaweed supply chains underpin incumbents’ product lines, while green seaweed breakthroughs promise new performance attributes that resonate with specialty-crop growers seeking quality premiums. Federal incentives, rising synthetic fertilizer costs, and mounting climate stress in row-crop regions are combining to strengthen the business case for seaweed-based inputs across both high-value and broad-acre agriculture.

Key Report Takeaways

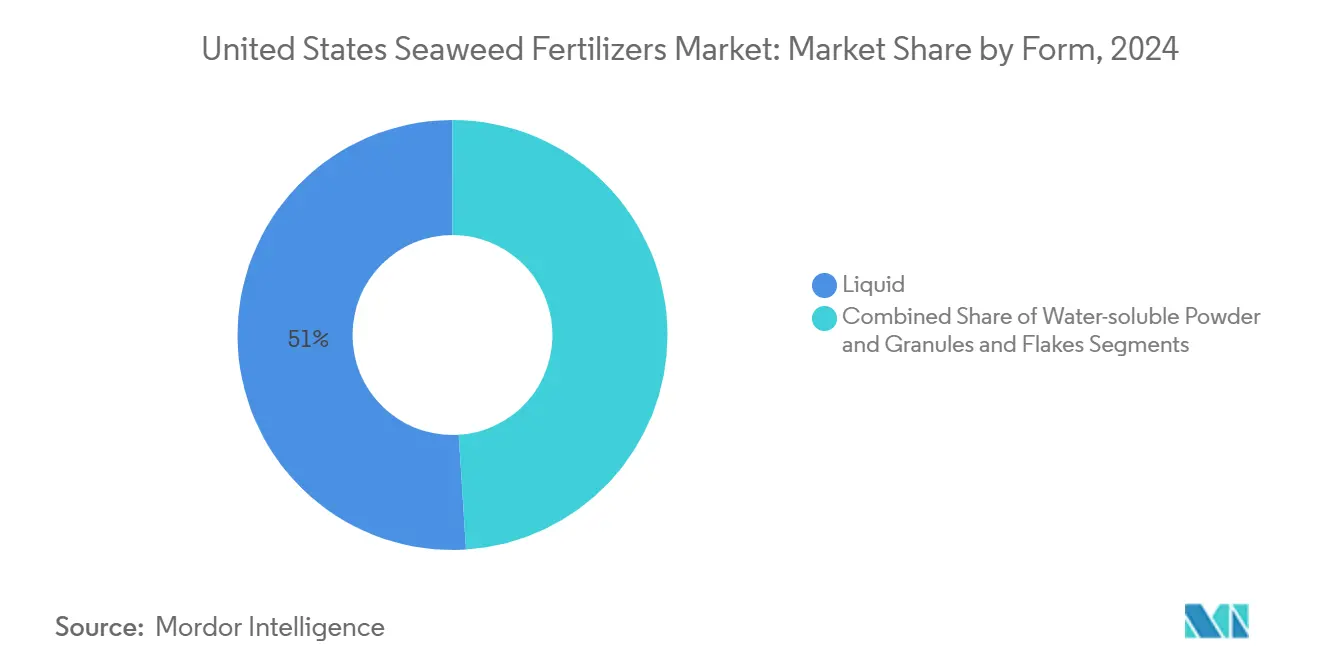

- By form, liquid products held 51% of the United States seaweed fertilizers market share in 2024, whereas the water-soluble powder and granule segment is projected to advance at a 12.2% CAGR through 2030.

- By source species, brown seaweeds led with 45% revenue contribution in 2024, while green seaweeds represent the fastest-growing source at a 13.5% CAGR to 2030.

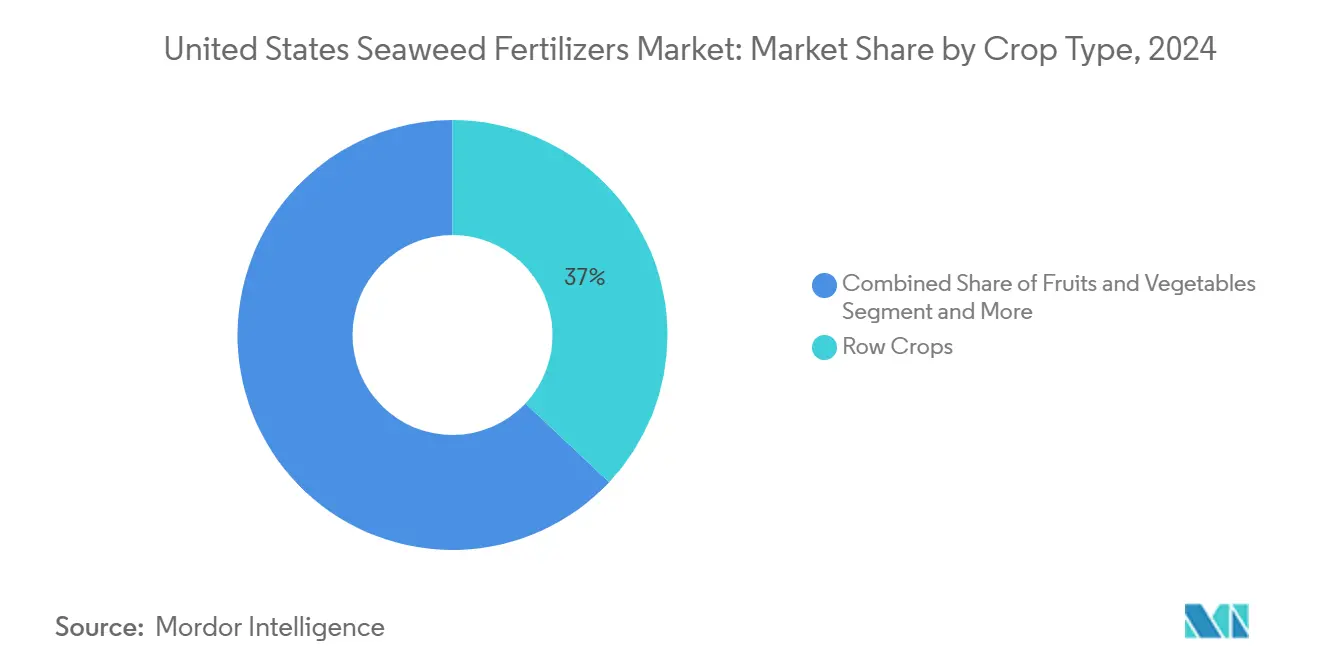

- By crop type, row crops accounted for a 37% share of the United States seaweed fertilizers market size in 2024, while fruits and vegetables are set to grow at a 10.9% CAGR through 2030.

- By application method, foliar spray dominated with 56% share in 2024, while fertigation is expanding at an 11.4% CAGR, propelled by precision-irrigation adoption.

United States Seaweed Fertilizers Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Shift Toward Certified Organic Acreage | +1.2% | California, Washington, and Oregon | Medium term (2-4 years) |

| Federal and State Incentives for Bio-Based Inputs | +0.8% | Nationwide, stronger in rural development zones | Short term (≤ 2 years) |

| Proven Abiotic-Stress Mitigation in Row Crops | +1.0% | Corn Belt and Cotton Belt | Medium term (2-4 years) |

| Rising Cost Spread Between Synthetic and Organic Fertilizers | +0.9% | Nationwide, pronounced in specialty-crop regions | Short term (≤ 2 years) |

| Carbon-Credit Monetization for Kelp Cultivation | +0.6% | Coastal states with kelp farms | Long term (≥ 4 years) |

| Kelp Biorefinery Co-Products Lowering Fertilizer Cost Base | +0.7% | Maine, Alaska, and California | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

Shift Toward Certified Organic Acreage

Organic farming is shifting from acreage expansion to value density, rewarding inputs that enhance quality and increase price realization. Even after a 10.9% decline in acreage, organic sales reached USD 69.7 billion in 2023, underscoring the effectiveness of the premium-crop strategy.[1]USDA National Institute of Food and Agriculture, “Organic Certification Cost Share Program,” nifa.usda.gov The United States Department of Agriculture (USDA) Organic Certification Cost Share Program offsets up to USD 750 of compliance expenses per operation, directing demand toward inputs such as seaweed extracts that meet organic standards. Controlled studies report 23% yield gains in strawberries treated with liquid kelp, reinforcing growers’ willingness to invest where added value is visible. Regenerative practices amplify this pull because seaweed products boost soil microbiology and carbon sequestration, crucial metrics in emerging eco-label programs. As retailers tighten sustainability requirements, growers view seaweed fertilizers as a credible route to differentiation rather than a cost burden.

Federal and State Incentives for Bio-Based Inputs

Washington’s Healthy Soils Program, California’s direct-payment scheme, and the USD 300 million Organic Transition Initiative create a policy tailwind that cuts payback times for seaweed-based solutions. The Environmental Quality Incentives Program (EQIP) classifies seaweed fertilizers under multiple conservation practices, encouraging adoption on acreage that would otherwise rely on synthetics. Environmental Protection Agency (EPA) exemptions for laminarin and chitosan polyphosphate (CPPA) remove costly data-package requirements, lowering the regulatory barrier to entry.[2]United States Environmental Protection Agency, “Plant Incorporated Protectants Exemptions,” epa.gov With additional carve-outs in rural development grants, processors can site dehydration and extraction plants closer to farms, slashing freight costs. Collectively, these measures institutionalize a competitive advantage for seaweed products long before carbon-credit revenue fully matures.

Proven Abiotic-Stress Mitigation in Row Crops

Field trials across drought-prone Midwest counties show 10% seaweed sap applications lifting maize yields by up to 26% under water stress conditions. Natural auxins and cytokinins in extracts expedite root growth, improving water capture during heat spikes that are increasing in frequency. Growers are shifting their perspective on seaweed fertilizers from simply boosting yields to managing risk, a view reinforced as insurance companies increasingly acknowledge their use as a risk-mitigation strategy. Cotton producers likewise report improved fiber strength when kelp-based foliar sprays are applied during flowering. Such cross-crop versatility supports volume scaling for manufacturers and underpins robust demand despite price premiums over conventional fertilizers.

Rising Cost Spread Between Synthetic and Organic Fertilizers

Urea prices averaged USD 492 per metric ton in early 2025, 8% higher than in 2024, while diammonium phosphate hit USD 739 per metric ton amid logistical bottlenecks. In contrast, seaweed fertilizer production costs remain in the USD 200-300 per dry metric ton range and could fall below USD 100 as biorefineries monetize protein and alginate co-products. Tariffs on Canadian potash accentuate the price divergence, giving seaweed alternatives a clear cost narrative, especially for specialty-crop growers who apply small quantities at critical phenological stages. Precision fertigation further enhances cost-effectiveness by delivering micro-doses exactly when crops need them. The widening price gap strengthens supplier bargaining power and supports higher margins without sacrificing grower economics.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Limited Domestic Kelp Biomass Supply | -1.4% | Coastal processors and inland importers | Medium term (2-4 years) |

| Biofertilizer Labeling and EPA Compliance Ambiguity | -0.8% | Nationwide | Short term (≤ 2 years) |

| Seasonal Variability in Ascophyllum Nodosum Bioactives | -0.6% | North Atlantic harvest zones | Short term (≤ 2 years) |

| Up-Cycling of Kelp into Foods and Bioplastics Inflating Feedstock Cost | -1.1% | Processing hubs across applications | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

Seasonal Variability in Ascophyllum Nodosum Bioactives

Bioactive levels in Ascophyllum nodosum fluctuate by up to 40% across harvest months, forcing processors to blend lots and run extra assays to meet label guarantees, raising costs and causing variable field performance. Growers who experience inconsistent results can revert to familiar synthetics, risking churn. Brown-seaweed dependent suppliers feel margin pressure because alternative species need re-engineered extraction lines. Until year-round cultivation stabilizes supply profiles, variability remains a hidden cost across the value chain.

Up-Cycling of Kelp into Foods and Bioplastics Inflating Feedstock Cost

Investments in seaweed-based packaging and alternative proteins surged after multiple consumer-goods giants signed offtake agreements, diverting biomass away from fertilizer channels. Bio-polymer converters pay premiums for pristine kelp, prompting farmers to prioritize contracts that offer higher margins than fertilizer feedstock. Fertilizer processors counter by adopting whole-biomass refineries, but capital outlays delay price relief. As new applications proliferate, competition for raw kelp will remain a structural cost headwind.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Form: Liquid Dominance Faces Powder Innovation

Liquid products captured 51% of 2024 revenues, giving them the largest United States seaweed fertilizers market share within the form segment. Immediate plant response through foliar sprays validates efficacy for growers, supporting repeat purchase rates. Retail garden channels stock mainly liquid SKUs, reinforcing consumer familiarity. Yet the segment’s growth pace lags emerging powders as freight and storage costs favor higher concentration formats. Water-soluble powders and granules are advancing at a 12.2% CAGR, aided by adoption in greenhouse fertigation systems where dose precision matters.

Powder formulations also suit inland states because transport involves less volume per unit of active ingredient, lowering carbon footprints. Innovators employ spray-drying that preserves kelp phytohormones, narrowing the performance gap with liquid extracts. The United States seaweed fertilizers market size for powders in row-crop fertigation is poised to swell as soil-moisture sensors cue automated nutrient delivery. Over the forecast horizon, liquid offerings will retain a loyal customer base, yet powders will command a growing share of commercial acreage.

By Source Species: Brown Seaweed Supremacy Challenged by Green Innovation

Brown seaweeds held 45% of the 2024 segment revenues, securing the largest United States seaweed fertilizers market share among source species, driven by well-established Ascophyllum nodosum harvests and robust auxin profiles. Producers rely on long-term North Atlantic supply agreements that underpin capacity planning. Green seaweeds top the growth leaderboard at a 13.5% CAGR, fueled by extraction methods that triple protein recovery and enhance stress-mitigation properties.

Species such as Ulva compressa thrive in land-based aquaculture without fertilizers, providing scalable biomass without marine-use conflicts. Red seaweeds play niche roles where carrageenan-rich residues improve soil aggregation, but higher cultivation costs cap volume growth. Feedstock competition from food and polymer sectors favors green seaweed farms capable of biorefinery co-outputs, spreading capital across multiple revenue streams. As domestic cultivation expands, green species will chip away at brown dominance, especially in specialty-crop belts seeking differentiated functional effects.

By Crop Type: Specialty Crops Drive Premium Growth

Row crops, including corn, soybeans, and cotton, remained the single largest application, accounting for 37% of 2024 revenues within the United States seaweed fertilizers market size. Growers value kelp extracts for drought resilience rather than headline yield gains, enhancing acreage penetration when weather volatility rises. Fruits and vegetables lead the growth trajectory at a 10.9% CAGR, supported by consumer willingness to pay premiums for organic-label produce.

Controlled trials showed 23% strawberry yield lifts and improved bell-pepper architecture, outcomes that easily justify higher per-acre input spends. Turf and ornamentals offer steady demand where aesthetics drive purchasing decisions. Golf course superintendents deploy liquid kelp to maintain vibrant greens during summer stress. Emerging cash crops such as hops and hemp round out the segment portfolio, with seaweed fertilizers aligning well with organic certification requirements. As regenerative labels proliferate, specialty crops will increasingly steer product development priorities.

By Application Method: Foliar Spray Leadership Faces Fertigation Challenge

Foliar sprays dominated the market with a 56% share in 2024, the largest among application methods in the United States seaweed fertilizers market. The technique bypasses soil pH constraints and delivers visible improvements within days, reinforcing grower confidence. Adoption barriers are minimal because existing sprayers require no major adaptations. Fertigation shows the fastest expansion at an 11.4% CAGR as sensor-driven irrigation automates nutrient delivery directly to the rhizosphere.

Greenhouse vegetable operators appreciate the labor savings and tighter nutrient-use efficiency, factors that strengthen margins in competitive fresh-produce markets. Innovations in foliar adjuvants extend spray uptake windows, while fertigation advances integrate weather data to refine scheduling. Over the forecast, foliar will stay on top for acreage, but fertigation will capture incremental value in technology-forward operations.

Geography Analysis

California anchors demand on the West Coast through its sizable specialty-crop economy and highest organic adoption rates nationwide. The state’s Healthy Soils Program reimburses growers for sustainable inputs, cementing loyalty to seaweed products.[3]USDA National Institute of Food and Agriculture, “Healthy Soils Program,” nifa.usda.gov Coastal proximity to kelp processors also minimizes freight, keeping landed costs competitive. The Midwest commands volume through corn and soybean acreage, where climate stress boosts interest in abiotic-stress solutions. Seaweed-based products are positioned as risk-management tools rather than yield maximizers. Freight differentials favor concentrated powders for inland users, a factor guiding new product development.

Maine, Rhode Island, and Alaska lead domestic cultivation with Atlantic Sea Farms' 2024 harvest of 589 metric tons, which paid USD 1 million to 40 fishing families. Yet these volumes satisfy only a fraction of coastal processors’ appetite, keeping supply chains tethered to imports. Alaska’s colder waters offer year-round farm permits but limited processing infrastructure, prompting investors to explore modular dehydration units that ship semi-processed flakes to mainland extractors.

Southern states from Texas to Georgia exhibit growing interest as cotton producers trial seaweed formulations to stabilize fiber quality under heat stress. Distribution hubs in Memphis and Atlanta facilitate two-day delivery to farm gates, bridging the coastal-inland logistics gap. Policy heterogeneity across states creates fragmented demand patterns nevertheless, sustained federal incentives help narrow adoption disparities.

Competitive Landscape

The market is moderately concentrated, with the five largest suppliers controlling a majority of 2024 revenues. Vertically integrated models that combine cultivation, extraction, and formulation offer scale economies and de-risk feedstock exposure. Atlantic Sea Farms exemplifies a partnership approach that secures raw kelp via long-term contracts with coastal fishers, ensuring a predictable supply while promoting community livelihoods. Leading extractors invest heavily in low-temperature and enzymatic processes that maintain bioactive integrity, translating into higher field performance and pricing power.

Mid-tier entrants differentiate through species specialization, especially in green seaweed lines where proprietary extraction yields protein-rich inputs that double as animal-feed additives. Start-ups leverage precision-fermentation know-how to create tailored formulation blends, appealing to greenhouse operators that demand consistency. Partnerships with fertigation-equipment vendors embed seaweed products into irrigation subscriptions, locking in recurring sales.

Competitive pressure comes from adjacent bio-based sectors vying for the same biomass. Suppliers address this through biorefinery strategies that monetize multiple fractions, thereby subsidizing fertilizer costs and improving margins. Intellectual-property positions center on extraction methods and proprietary blends rather than raw-material access alone, signaling a move toward technology-driven differentiation rather than volume leadership.

United States Seaweed Fertilizers Industry Leaders

Acadian Seaplants Limited

FMC Corporation

Ocean Organics

Kelpak

Maxicrop USA, Inc. (Syngenta Group)

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- February 2025: Acadian Plant Health introduced its Abiotic Stress Management (ASM) portfolio, which uses biofertilizer technologies to help crops reduce yield losses caused by extreme weather conditions. The ASM portfolio incorporates Ascophyllum nodosum seaweed extracts as its primary component. This seaweed-based product contributes to the U.S. seaweed fertilizer market by improving crop resilience and supporting sustainable agricultural practices in North America.

- December 2024: Dramm Corporation started constructing a solar-powered expansion at its Fish Fertilizer Facility in Algoma, Wisconsin, with funding from a grant under the United States Department of Agriculture’s Fertilizer Production Expansion Program (FPEP). This expansion enhances the sustainability of its DRAMMATIC Liquid Fish Fertilizer, which incorporates seaweed components and serves both organic and conventional farming markets in the United States.

- November 2023: Kelpak obtained CE Mark certification for its seaweed-based fertilizer under EU Fertilizer Regulation, confirming the product's safety, effectiveness, and regulatory compliance for European markets. This certification strengthens the company's international reputation and aligns with sustainable agriculture practices.

United States Seaweed Fertilizers Market Report Scope

| Liquid |

| Water-soluble Powder and Granules |

| Flakes |

| Brown Seaweeds |

| Red Seaweeds |

| Green Seaweeds |

| Row Crops |

| Fruits and Vegetables |

| Turf and Ornamentals |

| Other Specialty Crops |

| Foliar |

| Soil |

| Fertigation |

| By Form | Liquid |

| Water-soluble Powder and Granules | |

| Flakes | |

| By Source Species | Brown Seaweeds |

| Red Seaweeds | |

| Green Seaweeds | |

| By Crop Type | Row Crops |

| Fruits and Vegetables | |

| Turf and Ornamentals | |

| Other Specialty Crops | |

| By Application Method | Foliar |

| Soil | |

| Fertigation |

Key Questions Answered in the Report

What is the current value of the United States seaweed fertilizers market?

The seaweed fertilizers market size reached USD 10.3 million in 2025 and is forecast to rise to USD 13.6 million by 2030.

Which formulation dominates sales?

Liquid seaweed fertilizers hold 51% revenue share because of ease of application and retail familiarity.

Which crop segment is expanding fastest?

Fruits and vegetables lead growth at a 10.9% CAGR as specialty growers pay for quality improvements.

What policy supports adoption?

The USDA Organic Certification Cost Share Program reimburses 75% of certification costs up to USD 750, effectively subsidizing compliant inputs.

What threat could raise feedstock costs?

Rising demand from seaweed-based bioplastics and food applications is increasing competition for raw kelp, pressuring fertilizer input prices.

Page last updated on: