Asia-Pacific Semiconductor Device Market Size and Share

Market Overview

| Study Period | 2020 - 2031 |

|---|---|

| Forecast Data Period | 2026 - 2031 |

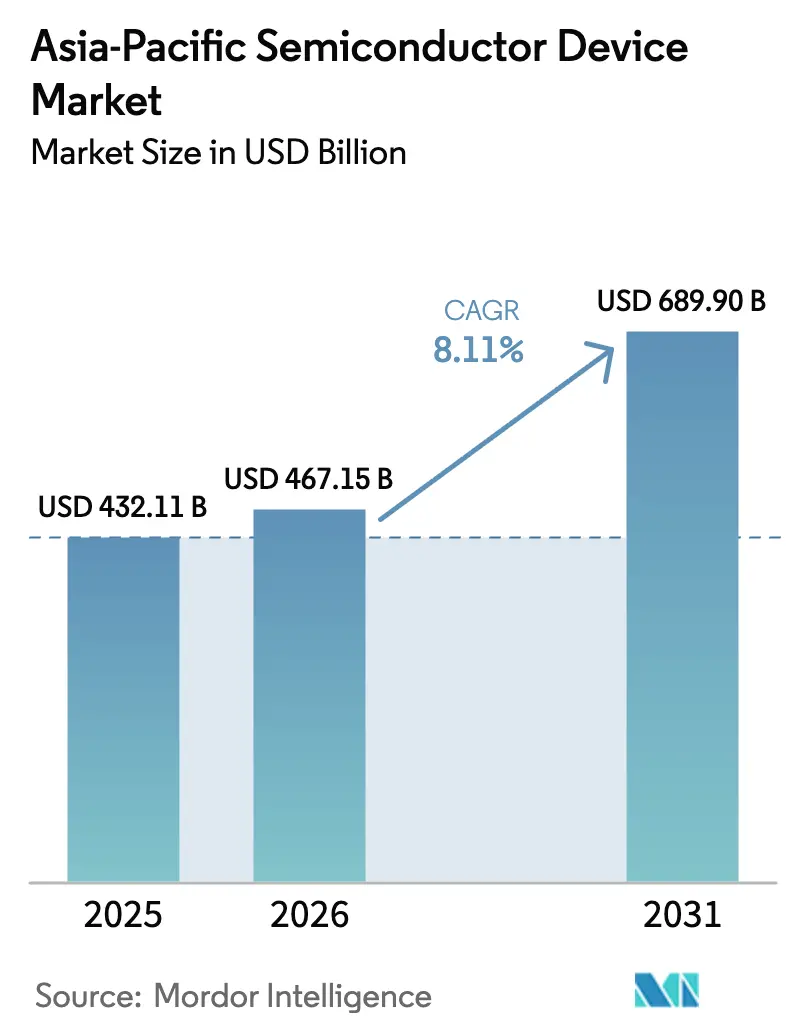

| Base Year Market Size (2025) | USD 432.11 Billion |

| Market Size (2026) | USD 467.15 Billion |

| Market Size (2031) | USD 689.9 Billion |

| Growth Rate (2026 - 2031) | 8.11% CAGR |

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

Asia-Pacific Semiconductor Device Market Analysis by Mordor Intelligence

Asia-Pacific semiconductor device market size in 2026 is estimated at USD 467.15 billion, growing from 2025 value of USD 432.11 billion with 2031 projections showing USD 689.9 billion, growing at 8.11% CAGR over 2026-2031. Robust demand for advanced logic, memory, and power devices, combined with expanding regional capacity, underpins this trajectory. Momentum is reinforced by government subsidies for sub-7 nm manufacturing, the rollout of 5G and emerging 6G networks, and accelerating electrification across transportation and renewable energy systems. Tight node migration schedules at leading foundries and sustained capital spending by memory producers keep utilization rates high even as macroeconomic volatility persists. Intensifying competition for skilled talent and utilities places additional emphasis on productivity improvements, advanced packaging, and sustainability-aligned process upgrades. Nonetheless, the Asia-Pacific semiconductor device market remains the principal hub for global wafer output, ecosystem depth, and technology leadership.

Key Report Takeaways

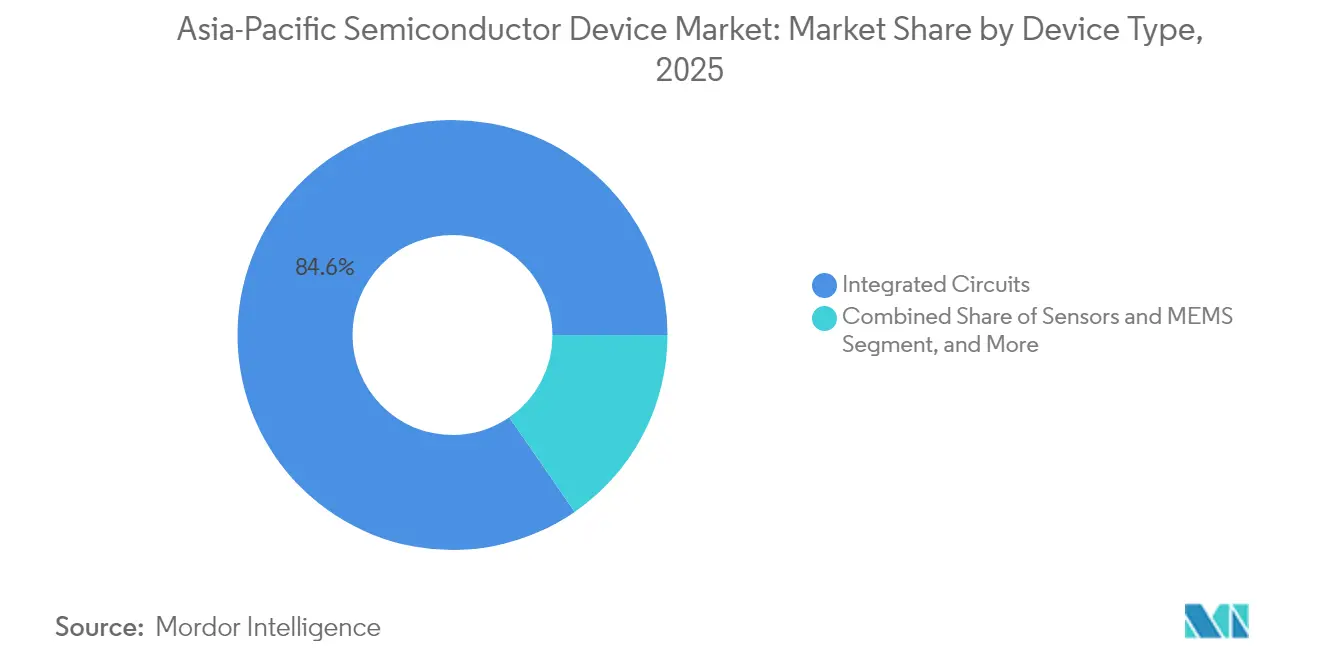

- By device type, integrated circuits captured 84.62% of the Asia-Pacific semiconductor device market share in 2025, while sensors and MEMS are projected to expand at a 9.54% CAGR through 2031.

- By business model, the IDM segment held 67.05% of the Asia-Pacific semiconductor device market share in 2025; fabless design vendors record the highest projected CAGR at 8.76% during 2026-2031.

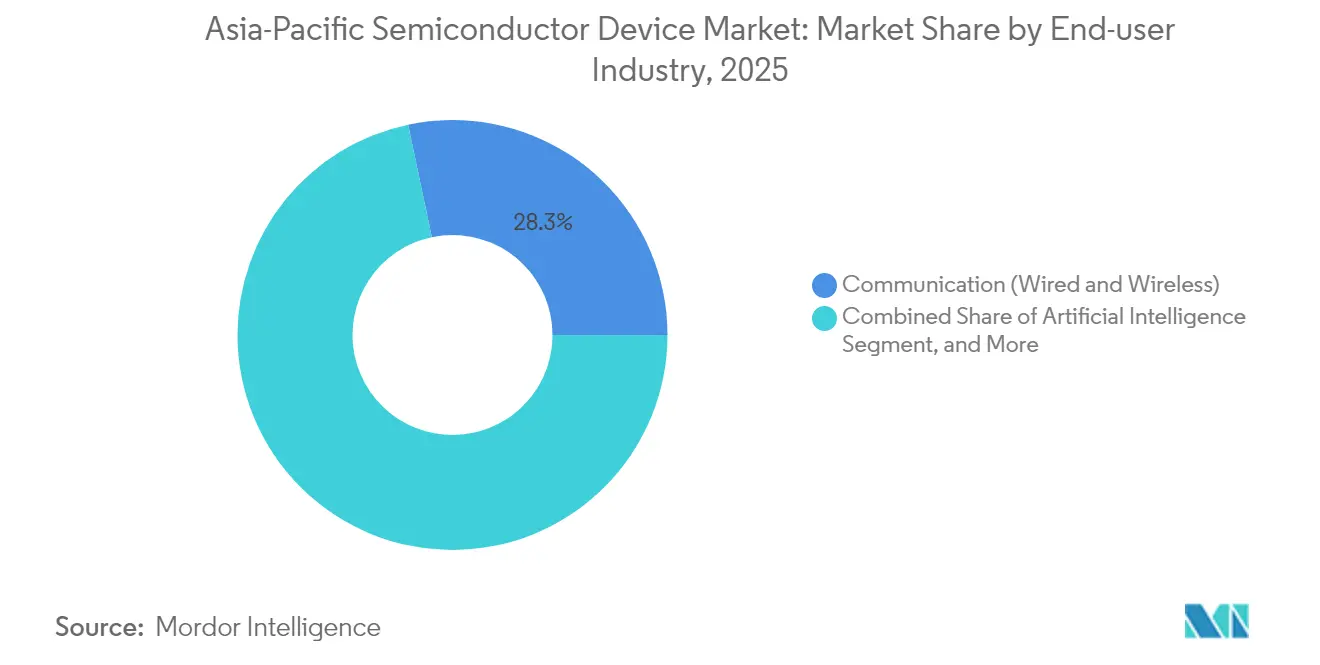

- By end-user industry, communication applications accounted for a 28.31% of the Asia-Pacific semiconductor device market share in 2025, whereas artificial intelligence workloads are advancing at a 9.72% CAGR to 2031.

- By country, China led with 51.62% of the Asia-Pacific semiconductor device market share in 2025, yet India is forecast to grow fastest at 9.29% CAGR through 2031.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of 2026.

Global valuation is built by aggregating outputs from multiple regions, with Asia forming one of the important contributors. Mordor Intelligence's global semiconductor device market size report represents that cumulative total.

Asia-Pacific Semiconductor Device Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| AI-centric compute demand surge | +2.8% | Taiwan, South Korea, China | Medium term (2-4 years) |

| Electrification and ADAS in vehicles | +1.9% | China, Japan, South Korea | Long term (≥ 4 years) |

| 5G/6G network roll-outs | +1.5% | China, South Korea, Japan, ASEAN | Medium term (2-4 years) |

| Regional subsidies for sub-7 nm fabs | +1.2% | Japan, South Korea, Taiwan, India | Long term (≥ 4 years) |

| PV/ESS boom boosting wide-band-gap power devices | +0.8% | China, Japan, South Korea | Medium term (2-4 years) |

| In-house silicon by hyperscale cloud providers | +0.6% | Global demand, Asia-Pacific production | Short term (≤ 2 years) |

| Source: Mordor Intelligence | |||

AI-centric compute demand surge

AI accelerators for generative and edge inference workloads continue to strain foundry capacity, with TSMC’s advanced nodes (7 nm and finer) representing 74% of the company's wafer revenue in 2024. SK hynix lifted quarterly operating profit to a record KRW 8.08 trillion on high-bandwidth memory (HBM) sales that quadrupled year over year.[1]“SK hynix Announces Q1 25 Financial Results,” SKHYNIX.COM Samsung has earmarked KRW 47.5 trillion for memory expansion focused on HBM3E and 3-nm gate-all-around logic to meet AI server demand. Foundries are scaling 2.5-D and 3-D chiplet packaging lines, yet substrate constraints keep lead times elevated into 2026. Continuous optimization of neural network architectures, including sparse computation and in-memory processing, is expected to reduce die size per TOPS but raise total wafer starts as AI permeates PCs, smartphones, and industrial edge nodes.

Electrification and ADAS in vehicles

China established domestic standards for more than 30 critical automotive semiconductors by 2025 to curb import dependence, accelerating local SiC and MCU sourcing. Regional EV adoption fuels incremental silicon content, with Southeast Asian vehicle output shifting toward battery electric platforms that require up to 2.5 times more power devices per unit than internal-combustion equivalents. Samsung Electro-Mechanics forecasts 11% annual growth in automotive MLCC shipments and plans production of the first LiDAR-grade capacitors in 2025. STMicroelectronics retains 32.6% share of the global SiC power market and is adding capacity in Catania and Wuxi to support double-digit CAGR through 2030. Mandatory functional-safety standards such as ISO 26262 continue to drive demand for high-reliability, automotive-grade ICs across propulsion, sensing, and zonal control domains.

5G/6G network roll-outs

China closed 2023 with 90% 5G penetration, operating 1.7 million base stations, and is targeting 1.6 billion 5G subscribers by 2030. South Korea pioneered 5G standalone deployments and now leads early-phase 6G trials leveraging 3GPP Release 20 features. India’s spectrum auctions and infrastructure build-out support a USD 1 trillion digital economy vision by 2025, with tower and small-cell installations rising 5.1% year on year to 5.79 million sites across Asia-Pacific. Higher-band carrier aggregation, integrated sensing, and sub-THz links for 6G will increase RF-front-end complexity, raising die demand for gallium nitrogen-on-silicon switches and power amplifiers. Network densification underpins ongoing investment in fronthaul optical transceivers, base-band ASICs, and timing ICs produced primarily in Taiwan and Japan.

Regional subsidies for sub-7 nm fabs

Japan awarded an additional JPY 590 billion (USD 3.9 billion) to Rapidus, lifting public funding to JPY 920 billion for a 2 nm process ramp in Hokkaido. South Korea’s KRW 471 trillion semiconductor super-cluster plan envisions 16 new fabs and 7.7 million wafer starts per month by 2030. India’s Semiconductor Mission offers 50% capital support to greenfield fabs, supplemented by state incentives that lift overall subsidies to 75% of the eligible outlay. Taiwan maintains a preferential tax rate of 5% on reinvested profits for semiconductor R&D and equipment purchases, sustaining domestic foundry dominance. Such measures strengthen regional competitiveness yet risk oversupply if global demand downshifts in late-decade cycles.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Export controls on advanced lithography and EDA | −1.8% | China, Taiwan, South Korea | Medium term (2-4 years) |

| Acute design-engineering talent shortage | −1.4% | Taiwan, Japan, South Korea, India | Long term (≥ 4 years) |

| Water-energy sustainability constraints on fabs | −0.9% | Taiwan, Japan, China | Medium term (2-4 years) |

| Memory down-cycles throttling CAPEX | −0.7% | South Korea, Taiwan, China | Short term (≤ 2 years) |

| Source: Mordor Intelligence | |||

Export controls on advanced lithography and EDA

Successive U.S. Bureau of Industry and Security rulings since 2022 restrict EUV scanners, direct-write e-beam tools, and advanced EDA software sales to Chinese fabs. The Netherlands and Japan aligned policies in 2024, extending licensing to deep-UV multipatterning and PECVD equipment.[2]Willie Shih, “Export Controls on Chipmaking Equipment,” CSIS.ORG China retaliated by excluding certain U.S. processors from government procurement and boosting domestic fab approvals worth USD 46 billion. Multinational IDMs must navigate divergent compliance frameworks, elevating legal and logistical expenses. Yet, provincial subsidies and tier-two EDA vendors support ongoing 28 nm and mature-node expansions, tempering the near-term drag on the broader Asia-Pacific semiconductor device market.

Acute design-engineering talent shortage

Asia-Pacific requires up to 1 million additional skilled workers by 2030 as wafer volumes climb and design cycles shorten. Taiwan alone projects a 34,000-person gap, prompting universities to double graduate program intake and industry to fund fast-track certificate courses. India courts overseas engineers with tax holidays and expedited visas, whereas Japan eases language requirements for foreign PhDs. Rising salary demands, reaching 20% premiums for FinFET design roles, and squeezed margins, especially at smaller fabless firms. Companies respond by automating verification, adopting AI-assisted layout tools, and expanding remote design centers in Vietnam and Malaysia.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Device Type: Continued IC Dominance with Sensor Upside

Integrated circuits generated 84.62% of the Asia-Pacific semiconductor device market revenue in 2025 and are projected to retain leadership through 2031 as leading-edge logic, HBM, and LPDDR6 volumes scale. Node transitions to 3 nm and the planned 2 nm pilot line at Rapidus reinforce the high value density of logic die produced in the region. Memory’s cyclical rebound, anchored by AI server demand, lifts blended wafer ASPs, while automotive-grade MCUs call for embedded MRAM features on 28 nm processes in Japan and China.

The sensors and MEMS category is forecast to outpace the broader Asia-Pacific semiconductor device market at a 9.54% CAGR on rising automotive radar, lidar, and environmental sensing adoption in smart factories. The Asia-Pacific semiconductor device market size for MEMS motion sensors used in AR/VR headsets could exceed USD 4.32 billion by 2031. Optical and discrete power devices register mid-single-digit growth, buoyed by LED micro-display demand and SiC powertrain rollouts.

By Business Model: IDM Scale Meets Fabless Agility

IDMs held 67.05% of the Asia-Pacific semiconductor device market share in 2025, benefiting from capital depth, tight process control, and co-optimization of design with manufacturing. Samsung’s dual focus on memory and foundry amplifies economies of scope, while SK Hynix leverages vertical integration to dominate HBM supply. Automotive customers favor IDMs for longevity guarantees of up to 15 years.

Fabless firms, however, are growing faster at 8.76% CAGR owing to specialization in AI inference, custom network silicon, and RF front-end designs. MediaTek’s Dimensity series, RISC-V server SOCs from Chinese start-ups, and India’s new edge-AI MCU players exemplify this dynamism. Supply-chain resilience remains a concern as leading-edge capacity tightens, prompting multi-foundry tape-out strategies and collaborative design-technology-co-optimization (DTCO) programs with TSMC and UMC.

By End-user Industry: Communication Scale Versus AI Velocity

Communication infrastructure absorbed 28.31% of the Asia-Pacific semiconductor device market revenue in 2025, led by China Mobile’s 1.7 million 5G base stations and Japan’s first 5G-Advanced demonstrations. Massive MIMO radios and fronthaul optical modules depend on high-performance FPGAs and network processors built on 5 nm platforms.

Artificial intelligence workloads represent the fastest-growing application, advancing at a 9.72% CAGR as hyperscale, automotive, and industrial inference proliferate. Asia-Pacific semiconductor device market size for AI data-center silicon is projected to exceed USD 86.37 billion by 2031, supported by multi-layer HBM stacks exceeding 12 GB per package. Automotive electrification, industrial automation, and consumer electronics with on-device AI sustain diversified demand profiles across the region.

Geography Analysis

China commanded 51.62% of the Asia-Pacific semiconductor device market revenue in 2025, shipping 245.99 billion units despite export controls, and expanding capacity to 10.1 million wafers per month in 2025. Government backing, deep supply chains, and endemic electronics consumption underpin expansion across logic, memory, and discrete sectors. China’s unrivaled domestic scale sustains investment across mature and advanced nodes, even as export restrictions complicate equipment procurement. Local champions SMIC and YMTC adapt by deepening 28 nm capacity and innovating 3D NAND architectures. Taiwan’s “Silicon Shield” status is reinforced by TSMC’s 68.8% global foundry share and the company’s ongoing 1.4 nm pilot line in Taichung slated for 2028 volume.

India, with a 9.29% CAGR, emerges as the region’s growth engine. The USD 11 billion Tata-Powerchip fab and Micron’s USD 2.7 billion ATMP in Gujarat anchor the nascent ecosystem, while the Production-Linked Incentive scheme offsets up to 50% capex. South Korea doubles down on memory leadership through the Yongin mega-cluster, targeting first wafer starts in 2027 and integrating AI-driven fab automation for yield uplift. Japan leverages materials expertise and state subsidies to re-enter logic leadership with Rapidus’s 2 nm effort and a TSMC consortium fab in Kumamoto. India’s ambition to capture USD 100 billion in semiconductor output by 2030 hinges on streamlined environmental clearances and a deepening local design base.

Southeast Asian nations, notably Singapore and Malaysia, expand backend and specialty-analog clusters. Singapore’s 300 mm NXP-VIS joint venture targets 55,000 wafers per month by 2029, strengthening the city-state’s role as an advanced mixed-signal hub. Regional free-trade accords and favorable tax regimes continue to attract outsourced assembly and test service (OSAT) investments.

Coverage of the semiconductor device market by Mordor Intelligence spans a wide geographic footprint, with regional analysis available for Europe, alongside detailed country-level intelligence for South Korea, China, and Japan, each shaped by local operating conditions.

Competitive Landscape

The Asia-Pacific semiconductor device market exhibits moderate concentration: the top five players command roughly 55-60% combined revenue, led by TSMC, Samsung, SK hynix, Micron, and SMIC. TSMC’s USD 165 billion global expansion includes three U.S. fabs and additional advanced packaging, safeguarding access for fabless customers while easing geopolitical supply-chain tensions.[4]“TSMC to Invest USD 165 Billion in U.S.,” PR.TSMC.COM Samsung balances foundry share gains against memory profitability by accelerating gate-all-around adoption at 3 nm. SK hynix strengthens its AI memory moat via 12-high HBM3E volumes shipped to Nvidia.

Rising challengers include Rapidus, backed by JPY 920 billion in subsidies, and India’s Tata Electronics. Chinese IDMs, buoyed by domestic demand, focus on specific niches like power discretes and NOR Flash. Strategic moves emphasize vertical integration, sustainability commitments, and co-development agreements: Denso-Rohm aligns on automotive SiC, Tenstorrent partners with Japan’s LSTC on 2 nm RISC-V accelerators, and 3M joins the US-JOINT materials consortium to expedite packaging innovation.

Supply-side risks remain concentrated in advanced lithography, specialty gases, and ABF substrates; firms mitigate exposure through multi-sourcing and long-term offtake contracts. Sustainability differentiation grows as TSMC, Samsung, and UMC pledge renewable energy targets exceeding 60% by 2030, aligning with customer ESG scorecard requirements.

Asia-Pacific Semiconductor Device Industry Leaders

Taiwan Semiconductor Manufacturing Company Limited (TSMC)

Samsung Electronics Co., Ltd.

SK hynix Inc.

Semiconductor Manufacturing International Corporation

United Microelectronics Corporation

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- August 2025: GlobalWafers America and Apple entered a partnership to boost advanced wafer supply for U.S. fabs, reinforcing resilient local sourcing.

- July 2025: TSMC began construction on four 1.4 nm plants in Central Taiwan Science Park, with first-phase output slated at 50,000 wafers per month.

- July 2025: Samsung increased HBM investment 2.5 times, setting a KRW 47.5 trillion chip capex plan for 2025.

- May 2025: TSMC confirmed nine new fabs and one packaging plant in response to AI demand, forecasting a 12-fold rise in AI chip shipments versus 2021.

- April 2025: SK hynix posted Q1 2025 revenue of KRW 17.64 trillion and an operating margin of 42% on surging HBM3E sales.

- March 2025: Tata Electronics, Himax, and Powerchip allied to grow India’s display and ultralow-power AI sensing supply chain.

- February 2025: 3M joined the US-JOINT consortium to speed advanced packaging R&D with a new Silicon Valley pilot line.

Asia-Pacific Semiconductor Device Market Report Scope

A semiconductor device is an electronic component that relies on the electronic properties of semiconductor material for its function.

The Asia-Pacific semiconductor device market is segmented by device type (discrete semiconductors, optoelectronics, sensors, integrated circuits [analog, logic, memory, micro [microprocessors, microcontrollers, and digital signal processors]]), by end-user vertical (automotive, communication [wired and wireless], consumer, industrial, and computing/data storage), and by country (Japan, China, Korea, Taiwan, and Rest of Asia-Pacific). The report offers market forecasts and size in value (USD) for all the above segments.

| Discrete Semiconductors | Diodes | ||

| Transistors | |||

| Power Transistors | |||

| Rectifier and Thyristor | |||

| Other Device Type | |||

| Optoelectronics | Light-Emitting Diodes (LEDs) | ||

| Laser Diodes | |||

| Image Sensors | |||

| Optocouplers | |||

| Other Optoelectronics | |||

| Sensors and MEMS | Pressure | ||

| Magnetic Field | |||

| Actuators | |||

| Acceleration and Yaw Rate | |||

| Temperature and Other Sensors and MEMS | |||

| Integrated Circuits | By IC Type | Analog | |

| Micro | Microprocessors (MPU) | ||

| Microcontrollers (MCU) | |||

| Digital Signal Processors | |||

| Logic | |||

| Memory | |||

| By Technology Node | less than 3 nm | ||

| 3 nm | |||

| 5 nm | |||

| 7 nm | |||

| 16 nm | |||

| 28 nm | |||

| Above 28 nm | |||

| IDM |

| Design/Fabless Vendor |

| Automotive |

| Communication (Wired and Wireless) |

| Consumer |

| Industrial |

| Computing/Data Storage |

| Data Centre |

| Artificial Intelligence |

| Government (Aerospace and Defence) |

| Other End-user Industry |

| China |

| Japan |

| South Korea |

| Taiwan |

| India |

| Singapore |

| Malaysia |

| Australia |

| Indonesia |

| Rest of Asia-Pacific |

| By Device Type | Discrete Semiconductors | Diodes | ||

| Transistors | ||||

| Power Transistors | ||||

| Rectifier and Thyristor | ||||

| Other Device Type | ||||

| Optoelectronics | Light-Emitting Diodes (LEDs) | |||

| Laser Diodes | ||||

| Image Sensors | ||||

| Optocouplers | ||||

| Other Optoelectronics | ||||

| Sensors and MEMS | Pressure | |||

| Magnetic Field | ||||

| Actuators | ||||

| Acceleration and Yaw Rate | ||||

| Temperature and Other Sensors and MEMS | ||||

| Integrated Circuits | By IC Type | Analog | ||

| Micro | Microprocessors (MPU) | |||

| Microcontrollers (MCU) | ||||

| Digital Signal Processors | ||||

| Logic | ||||

| Memory | ||||

| By Technology Node | less than 3 nm | |||

| 3 nm | ||||

| 5 nm | ||||

| 7 nm | ||||

| 16 nm | ||||

| 28 nm | ||||

| Above 28 nm | ||||

| By Business Model | IDM | |||

| Design/Fabless Vendor | ||||

| By End-user Industry | Automotive | |||

| Communication (Wired and Wireless) | ||||

| Consumer | ||||

| Industrial | ||||

| Computing/Data Storage | ||||

| Data Centre | ||||

| Artificial Intelligence | ||||

| Government (Aerospace and Defence) | ||||

| Other End-user Industry | ||||

| By Country | China | |||

| Japan | ||||

| South Korea | ||||

| Taiwan | ||||

| India | ||||

| Singapore | ||||

| Malaysia | ||||

| Australia | ||||

| Indonesia | ||||

| Rest of Asia-Pacific | ||||

Key Questions Answered in the Report

How large is the Asia-Pacific semiconductor market in 2026?

The Asia-Pacific semiconductor device market size reached USD 467.15 billion in 2026 and is forecast to grow at an 8.11% CAGR to USD 689.9 billion by 2031.

Which device type holds the largest revenue share?

Integrated circuits led with 84.62% of Asia-Pacific semiconductor market share in 2025, reflecting their central role across consumer, industrial, and AI applications.

What is driving the fastest growth in end-user demand?

Artificial intelligence workloads represent the fastest-growing segment, advancing at a 9.72% CAGR as data-center and edge inference expand.

Which country is growing quickest in the region?

India records the highest country-level CAGR at 9.29% through 2031, supported by significant government incentives and greenfield fab investments.

How are governments supporting advanced manufacturing?

Japan, South Korea, Taiwan, and India offer subsidies covering up to 75% of eligible fab costs, tax credits, and long-term power contracts to attract sub-7 nm capacity.

What risks could dampen Asia-Pacific semiconductor growth?

Export-control restrictions, skilled-labor shortages, and water-energy constraints pose the greatest headwinds, collectively trimming the forecast CAGR by an estimated 4.8 percentage points.

Page last updated on: