Philippines Semiconductor Market Size and Share

Market Overview

| Study Period | 2020 - 2031 |

|---|---|

| Forecast Data Period | 2026 - 2031 |

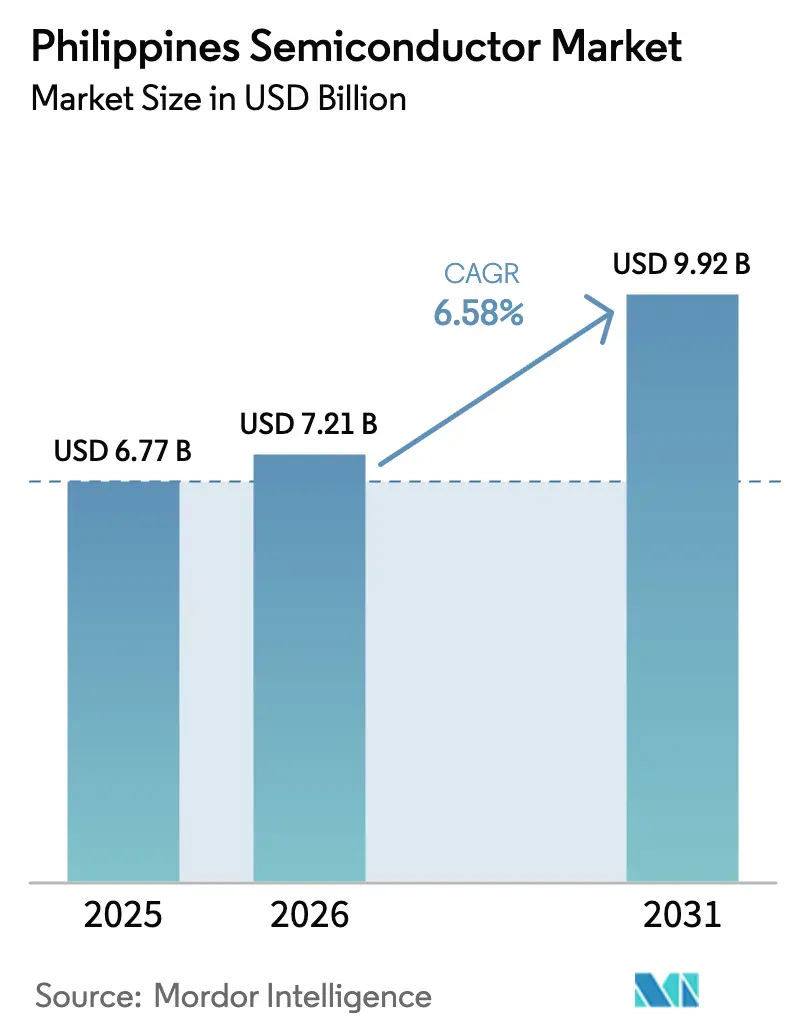

| Base Year Market Size (2025) | USD 6.77 Billion |

| Market Size (2026) | USD 7.21 Billion |

| Market Size (2031) | USD 9.92 Billion |

| Growth Rate (2026 - 2031) | 6.58% CAGR |

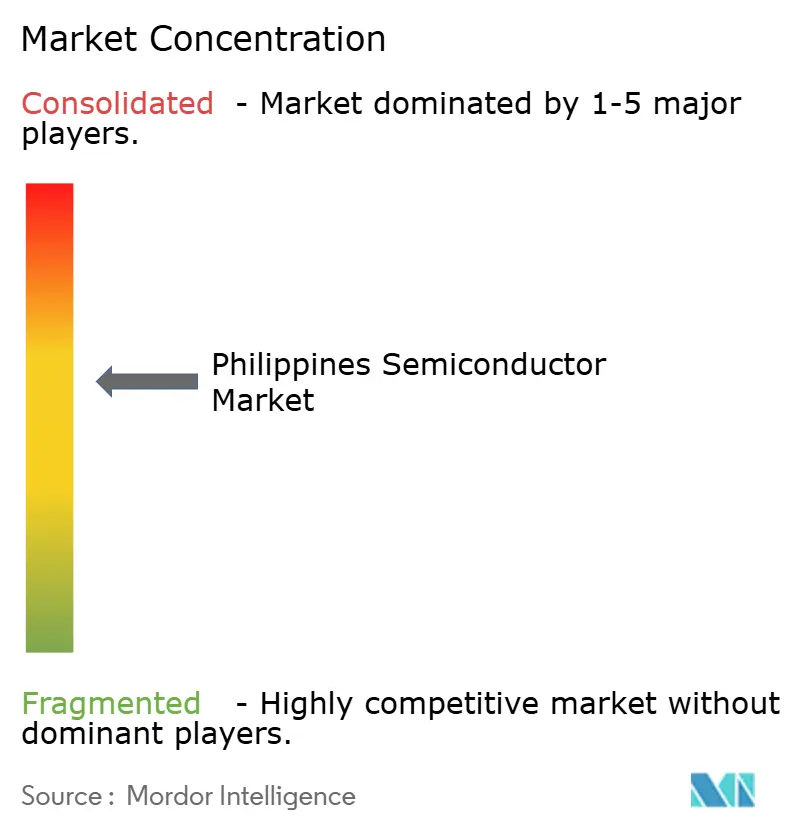

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

Philippines Semiconductor Market Analysis by Mordor Intelligence

The Philippines semiconductor market size is expected to grow from USD 6.77 billion in 2025 to USD 7.21 billion in 2026 and is forecast to reach USD 9.92 billion by 2031 at 6.58% CAGR over 2026-2031. This solid trajectory reflects rising global demand for alternative supply chains as firms deploy China + 1 strategies, intensified investment incentives under the CREATE MORE Act, and a decisive move into higher-value integrated-circuit design and advanced packaging. Fiscal incentives now cover expanded power-cost deductions, narrowing the nation’s historical electricity-price gap. U.S. government support through the CHIPS and Science Act is strengthening bilateral technology partnerships, while the archipelago’s English-proficient workforce and preferential trade agreements continue to draw new projects. The Philippines semiconductor market is also benefiting from rapid 5G rollout, automotive electrification, and AI-enabled data-center growth, each creating incremental demand for power, RF, and high-performance logic devices. Multinational incumbents are deepening footprints in Luzon’s economic zones, and local champions are pivoting toward medical and industrial niches to diversify revenue streams.[1]Philippine News Agency, “CREATE MORE Act attracts PHP 50.65-B Samsung capacitor plant,” pna.gov.ph

Key Report Takeaways

- By device type, Integrated Circuits led with 62.74% of Philippines semiconductor market share in 2025. Sensors and MEMS are advancing at a 9.68% CAGR, the fastest rate among device categories.

- By business model, Integrated Device Manufacturers accounted for 63.95% share of the Philippines semiconductor market size in 2025. Fabless vendors are growing at a 9.06% CAGR to 2031 as local design capability deepens.

- By end-user industry, Automotive controlled 27.18% of the Philippines semiconductor market size in 2025. Artificial Intelligence applications are registering the highest segment CAGR at 10.34% through 2031.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of 2026.

Philippines Semiconductor Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Government incentives under CREATE law | 1.20% | National, concentrated in CALABARZON and Metro Manila | Medium term (2-4 years) |

| Rising demand for automotive-grade electronics exports | 1.80% | Luzon economic zones, spill-over to Visayas | Long term (≥ 4 years) |

| China + 1 supply-chain diversification push | 2.10% | National, with priority in established industrial parks | Short term (≤ 2 years) |

| Nationwide 5G roll-out boosting RF and power IC demand | 0.90% | Metro Manila, Cebu, Davao with rural expansion | Medium term (2-4 years) |

| Government-funded pilot wafer-fab projects (DOST-ADMATEL) | 0.60% | National RandD centers, technology transfer hubs | Long term (≥ 4 years) |

| Metro-Manila AI data-center build-out driving advanced packaging | 0.40% | Metro Manila, extending to nearby provinces | Medium term (2-4 years) |

| Source: Mordor Intelligence | |||

Government Incentives Under CREATE Law

Lowering the corporate income-tax rate from 25% to 20% for registered enterprises and allowing larger deductions on power expenses have re-ranked the Philippines among the most incentive-rich semiconductor destinations in Southeast Asia. Samsung Electro-Mechanics allocated PHP 50.65 billion to a Calamba plant for automotive multilayer capacitors after the revised framework guaranteed predictable VAT refunds and clarified local-levy rules. Murata Manufacturing followed by pledging PHP 4.4 billion to expand multilayer ceramic-capacitor lines, citing the new deduction regime. Japanese investors such as MinebeaMitsumi accelerated project approvals because CREATE MORE eliminates regulatory ambiguity and shortens approval cycles, positioning the Philippines competitively against Malaysia and Vietnam. Expanded incentives specifically address power-intensive segments, a long-standing hurdle for wafer-fabrication prospects. The measure’s success is visible in rising PEZA approvals that topped PHP 123.76 billion between January and October 2024.

Rising Demand for Automotive-Grade Electronics Exports

Global electric-vehicle adoption, together with tighter safety rules, is lifting automotive semiconductor content per car and steering fresh orders toward Philippine plants certified to ISO/TS 16949. EMS Group secured USD 1.6 billion in capital from three multinational firms to produce power ICs targeting EV platforms, with output slated for 2026.[2]Manila Standard, “Foreign firms invest $1.6B in EMS Group,” manilastandard.net The Department of Trade and Industry aims to manufacture 4 million e-vehicles and major components locally, which will further embed semiconductor demand inside national value chains. Amkor Technology Philippines operates a center of excellence for automotive packages that have passed rigorous audits by tier-1 suppliers. As global OEMs push for geographic diversification, Philippine capacity aligned with automotive reliability standards is absorbing a growing share of new programs. Continuous content growth in advanced driver-assistance systems and power management ensures that the Philippines semiconductor market will keep supplying larger, higher-margin automotive chips.

Nationwide 5G Roll-Out Boosting RF and Power IC Demand

Globe and Smart invested more than PHP 170 billion in network upgrades, commissioning 256 new 5G sites during 2025 and achieving outdoor coverage that approaches 99% in Metro Manila.[3]RCR Wireless News, “Globe boosts 5G coverage across the Philippines,” rcrwireless.com As subscriptions surpassed 7 million users, demand for power-management and RF-front-end chips surged. Nokia’s modular Interleaved Passive Active Antenna deployment underscores the advanced RF content now embedded in Philippine infrastructure. Smart’s plan to allocate up to PHP 85 billion in 5G capital outlay translates into sustained call-off orders to local OSATs for power-amplifier modules and baseband processors. Ericsson estimates 5G will represent 40% of national mobile subscriptions by 2030, anchoring long-run semiconductor demand.

Government-Funded Pilot Wafer-Fab Projects (DOST-ADMATEL)

The Advanced Device and Materials Testing Laboratory (ADMATEL) under DOST is backing laboratory-scale wafer-fab pilots that give Philippine fabless startups access to prototype silicon without incurring high foreign shuttle-run costs. The initiative reduces lead times for proof-of-concept devices and encourages local IP creation essential for high-margin design export revenue. Whereas commercial fabs remain absent, the pilot plants lower entry barriers for MEMS and power-discrete innovators and help build engineering depth required to attract full-scale foundry partners in the long term. The Department of Trade and Industry expects these pilots to trigger clustering effects by 2028, including specialty gas suppliers and photomask houses.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| High industrial electricity tariffs | -1.40% | National, particularly affecting energy-intensive fabs | Short term (≤ 2 years) |

| Thin local upstream materials ecosystem | -0.80% | National, with acute impact on advanced packaging | Medium term (2-4 years) |

| Engineering-talent migration to Taiwan and Singapore | -0.70% | National, concentrated in Metro Manila and CALABARZON | Long term (≥ 4 years) |

| Typhoon and earthquake-related supply-chain disruption risk | -0.30% | Luzon and Visayas, seasonal impact patterns | Short term (≤ 2 years) |

| Source: Mordor Intelligence | |||

High Industrial Electricity Tariffs

Average industrial power rates remain among the highest in ASEAN, eroding cost competitiveness for energy-heavy wafer processes. SEIPI has ranked electricity pricing as the primary deterrent for attracting front-end fabs, with operators benchmarking against Vietnam and Thailand where targeted industrial rates fall 20% lower. Although the CREATE MORE Act lets registered firms deduct a bigger portion of electricity costs, the underlying tariff regime still relies heavily on imported fuel, exposing manufacturers to volatility. OSATs consuming large, stable baseloads often resort to captive solar rooftops and private-grid connections, yet implementation hurdles persist in both permitting and grid interconnection timelines. Unless structural reforms widen access to low-cost renewables, advanced-node wafer projects may continue to choose alternative ASEAN sites.

Thin Local Upstream Materials Ecosystem

While testing and packaging nodes are mature, local supply of photomasks, specialty gases, and high-purity chemicals remains thin, forcing import dependence and elongating lead times. Advanced packaging lines now being installed for AI devices require ultra-clean capillary underfills, copper pillars, and fine-pitch substrates. Most of these materials are still shipped from Japan or Taiwan, inflating inventories and working capital. The government is courting chemical suppliers to set up Philippines-based blending facilities; however, land-use permitting and port congestion issues have slowed commitments. The gap becomes more pronounced as devices move toward sub-10 µm bump pitches where material tolerances tighten.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Device Type: Integrated Circuits Retain Scale Advantage

Integrated Circuits accounted for 62.74% of Philippines semiconductor market size in 2025, anchored by decades-old assembly and test complexes run by Texas Instruments in Clark and STMicroelectronics in Calamba. Analog and power ICs enjoy resilient automotive demand, whereas logic and memory volumes shadow global handset and PC cycles. Philippine plants specialize in QFN, BGA, and advanced SiP layouts, and recent capital injections target copper-clip and wafer-level packages to lift value capture. Over the forecast horizon, integrated-circuit volumes are projected to expand at the overall market CAGR, supported by content growth in EV powertrains and 5G base stations.

Sensors and MEMS, though a smaller base, will post the quickest expansion at a 9.68% CAGR as ADAS mandates and industrial IoT adoption intensify. Vehicle safety law updates require pressure and inertial sensors, while smart-factory rollouts use MEMS microphones and environmental monitors. Philippine OSATs are adopting wafer-level vacuum encapsulation techniques that cut unit cost and widen export appeal to European Tier-1s. Discrete devices such as power MOSFETs and IGBTs benefit from renewable-energy inverters and EV chargers, whereas Optoelectronics maintains steady LED demand despite broader LCD shift toward OLED. Collectively, device diversification balances cyclical swings in consumer logic chips, reinforcing long-term growth resilience for the Philippines semiconductor market.

By Business Model: IDM Scale Versus Fabless Agility

IDMs commanded 63.95% of Philippines semiconductor market share in 2025, leveraging co-located assembly and test to control yield and reliability for automotive and industrial sectors. Their capital heft underwrites transitions toward system-in-package and heterogenous integration. Yet rising depreciation costs and quicker product cycles favour an asset-light model. Fabless enterprises, expanding at 9.06% CAGR, rely on growing domestic design clusters near university technology parks. DTI’s proposed government-backed wafer-lab will shorten prototype cycles and reduce dependence on Taiwan foundries. Local firms such as Integrated Micro-Electronics pivot to mixed-signal design IP that layers on auto-qualified packages manufactured by local IDMs, creating a virtuous supply loop. Over time, fabless agility combined with incentive-backed R&D could lift their revenue contribution toward one-third of the Philippines semiconductor market by 2031.

By End-User Industry: Automotive Foundation, AI Upsurge

Automotive captured 27.18% of Philippines semiconductor market size in 2025, sustained by ISO/TS-compliant lines producing power-management ICs, pressure sensors, and multilayer capacitors. Samsung Electro-Mechanics’ PHP 50.65 billion greenfield plant will add 100 billion auto-grade capacitors annually starting 2027, reinforcing long-term customer. EV battery-management systems, inverter modules, and radar sensors all elevate chip value per vehicle, cushioning revenue against cyclical light-vehicle volumes.

Artificial Intelligence, at a 10.34% CAGR, is transforming demand dynamics as hyperscale data-center tenants procure packaged GPUs and AI accelerators. The Philippine Institute for Development Studies expects the national AI economy to reach USD 1.025 billion by 2025, and each installed megawatt of compute draws hundreds of high-bandwidth memory stacks and advanced substrates. Segment growth extends to edge AI in smart appliances and surveillance devices, further widening the application base for domestic OSAT lines. Communication infrastructure chips benefit from 5G densification, while industrial automation raises MCU and sensor pulls. Consumer electronics remain cyclical, yet rising disposable income supports mid-tier smartphone and wearables production that feeds assembly orders.

Geography Analysis

Luzon houses more than 70% of operating semiconductor floor space, led by clusters in Clark, Calamba, and Cavite that enjoy close proximity to the Port of Manila, NAIA air gateways, and a deep engineering talent pool. Texas Instruments’ Clark site alone ships several billion analog units annually, while STMicroelectronics’ Calamba campus employs more than 4,000 workers on multi-line assembly. The Luzon Economic Corridor initiative promises further logistics and customs harmonization, a boon for just-in-time semiconductor flows.

Visayas is emerging as the secondary pole of the Philippines semiconductor market. Globe achieved 97.97% 5G coverage across key Visayas cities, enhancing connectivity for electronics exporters in Cebu and Iloilo. Several Tier-2 OSATs have begun pilot lines in Mactan and Leyte to hedge natural-disaster risk and tap competitively priced labour. Government plans for new PEZA parks in the region are supported by port upgrades aimed at shaving transit times to Japanese and U.S. customers.

Mindanao remains a nascent participant but shows promise in specialized R&D and design services. Mindanao State University’s DOST-funded project produced a low-power microchip for data-logger devices, proving the viability of high-value research outside traditional. Infrastructure gaps persist, yet progressive 5G rollouts and power-grid interconnection projects are unlocking feasibility for small-volume assembly and prototype validation sites. Over the forecast horizon, Mindanao could specialize in ruggedized chipsets for agritech and renewable-energy applications.

Competitive Landscape

The Philippines semiconductor market features moderate fragmentation, with the top five companies collectively holding an estimated 55% revenue share. Texas Instruments anchors analog and power IC assembly; Amkor Technology leads outsourced packaging for handset and automotive SoCs; STMicroelectronics focuses on mixed-signal and MEMS; ASE recently expanded via its 2024 acquisition of Infineon’s Cavite backend line, adding scale in automotive packages; and Integrated Micro-Electronics builds EMS-plus-design services for industrial clients. Competitive intensity is rising around 2.5D/3D packaging for AI accelerators, where OSATs race to install thermal-interface and under-bump metallization lines.

Strategic moves highlight consolidation and specialization. ASE’s asset purchase strengthens its bargaining power with foundry partners and unlocks new vehicle radar-module programs. Analog Devices’ USD 200 million R&D campus in Cavite is set to prototype 300 mm wafers for industrial power devices, signalling a climb up the value chain. Cirtek closed a multi-year contract to supply 5G transceiver modules for an American fibber-optic OEM, leveraging its licensed GaAs MMIC technology. Meanwhile, EMS Group’s capital raise positions it as a local champion for EV power modules, enhancing supply security for regional automakers.

Collaboration with upstream suppliers is intensifying. Entegris’ long-term agreement with on semi assures high-purity chemicals, mitigating one major restraint linked to thin materials ecosystems. Local substrate vendors are scaling ABF-class materials to serve AI GPU packages, and shipping tests have commenced with Japanese tier-one device makers. The competitive field now hinges on acquiring scarce technical talent and integrating vertically with substrate, mold-compound, and test-handler suppliers to shorten time-to-market.

Philippines Semiconductor Industry Leaders

Texas Instruments (Philippines), Inc.

Amkor Technology Philippines, Inc.

Integrated Micro-Electronics, Inc.

ROHM Electronics Philippines, Inc.

ON Semiconductor Philippines, Inc.

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- May 2025: Samsung Electro-Mechanics Philippines announced a PHP 50.65 billion plant in Calamba City to build 100 billion automotive multilayer capacitors annually, creating 3,000 jobs.

- May 2025: The United States designated the Philippines as a CHIPS Act partner country, unlocking USD 500 million for ecosystem strengthening over five years.

- April 2025: Analog Devices committed USD 200 million to a new R&D facility at Gateway Business Park, Cavite, focusing on 300 mm power-device prototypes.

- March 2025: EMS Group secured USD 1.6 billion from three foreign investors to manufacture automotive power ICs in Luzon, with production slated for 2026.

Philippines Semiconductor Market Report Scope

| Discrete Semiconductors | Diodes | ||

| Transistors | |||

| Power Transistors | |||

| Rectifier and Thyristor | |||

| Other Discrete Devices | |||

| Optoelectronics | Light-Emitting Diodes (LEDs) | ||

| Laser Diodes | |||

| Image Sensors | |||

| Optocouplers | |||

| Other Device Types | |||

| Sensors and MEMS | Pressure | ||

| Magnetic Field | |||

| Actuators | |||

| Acceleration and Yaw Rate | |||

| Temperature and Others | |||

| Integrated Circuits | By Integrated Circuit Type | Analog | |

| Micro | Microprocessors (MPU) | ||

| Microcontrollers (MCU) | |||

| Digital Signal Processors | |||

| Logic | |||

| Memory | |||

| By Technology Node (Shipment Volume Not Applicable) | Less than 3nm | ||

| 3nm | |||

| 5nm | |||

| 7nm | |||

| 16nm | |||

| 28nm | |||

| 28nm | |||

| Integrated Device Manufacturer (IDM) |

| Design / Fabless Vendor |

| Automotive |

| Communication (Wired and Wireless) |

| Consumer |

| Industrial |

| Computing / Data Storage |

| Data Center |

| Artificial Intelligence |

| Government (Aerospace and Defense) |

| By Device Type (Shipment Volume for Device Type is Complementary) | Discrete Semiconductors | Diodes | ||

| Transistors | ||||

| Power Transistors | ||||

| Rectifier and Thyristor | ||||

| Other Discrete Devices | ||||

| Optoelectronics | Light-Emitting Diodes (LEDs) | |||

| Laser Diodes | ||||

| Image Sensors | ||||

| Optocouplers | ||||

| Other Device Types | ||||

| Sensors and MEMS | Pressure | |||

| Magnetic Field | ||||

| Actuators | ||||

| Acceleration and Yaw Rate | ||||

| Temperature and Others | ||||

| Integrated Circuits | By Integrated Circuit Type | Analog | ||

| Micro | Microprocessors (MPU) | |||

| Microcontrollers (MCU) | ||||

| Digital Signal Processors | ||||

| Logic | ||||

| Memory | ||||

| By Technology Node (Shipment Volume Not Applicable) | Less than 3nm | |||

| 3nm | ||||

| 5nm | ||||

| 7nm | ||||

| 16nm | ||||

| 28nm | ||||

| 28nm | ||||

| By Business Model | Integrated Device Manufacturer (IDM) | |||

| Design / Fabless Vendor | ||||

| By End-user Industry | Automotive | |||

| Communication (Wired and Wireless) | ||||

| Consumer | ||||

| Industrial | ||||

| Computing / Data Storage | ||||

| Data Center | ||||

| Artificial Intelligence | ||||

| Government (Aerospace and Defense) | ||||

Key Questions Answered in the Report

How large is the Philippines semiconductor market in 2026?

The market is valued at USD 7.21 billion in 2026 and is projected to reach USD 9.92 billion by 2031.

What is the forecast CAGR for Philippines semiconductor market revenue?

Revenue is expected to rise at a 6.58% CAGR from 2026 to 2031.

Which device category leads sales in the Philippines?

Integrated Circuits dominate with 62.74% market share in 2025.

Which segment is growing fastest?

Sensors and MEMS are expanding at a 9.68% CAGR through 2031.

How significant is automotive demand?

Automotive applications hold 27.18% of sales and benefit from rising EV semiconductor content.

What incentives support new semiconductor investment?

The CREATE MORE Act lowers the corporate tax rate to 20% for registered firms and offers enhanced power-cost deductions.

Page last updated on: