Israel Semiconductor Market Size and Share

Market Overview

| Study Period | 2019 - 2030 |

|---|---|

| Forecast Data Period | 2025 - 2030 |

| Historical Data Period | 2019 - 2023 |

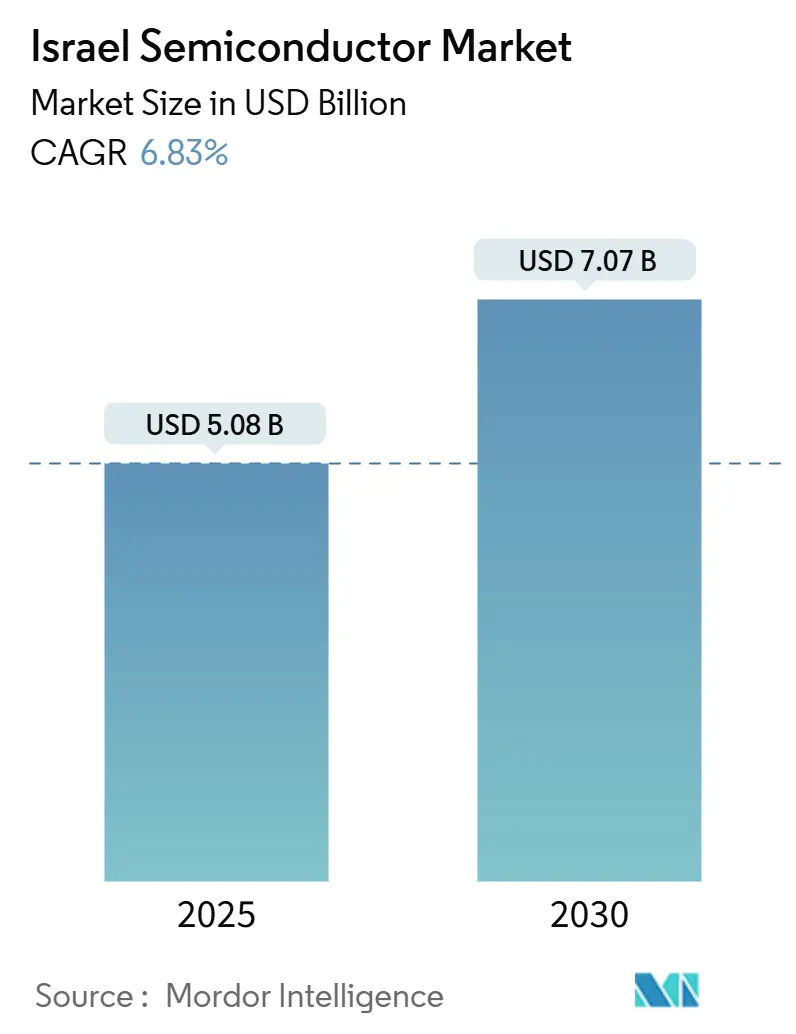

| Market Size (2025) | USD 5.08 Billion |

| Market Size (2030) | USD 7.07 Billion |

| Growth Rate (2025 - 2030) | 6.83% CAGR |

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

Israel Semiconductor Market Analysis by Mordor Intelligence

The Israel semiconductor market size stands at USD 5.08 billion in 2025 and is forecast to reach USD 7.07 billion by 2030, advancing at a 6.83% CAGR. Israel’s combination of generous fabrication incentives, a thriving AI-accelerator startup scene, and enduring defense-electronics demand continues to anchor steady expansion. Start-ups such as Hailo, Innoviz, and Valens keep funnelling venture capital into advanced node design, while global foundry bottlenecks push specialty analog and RF orders to local fabs. At the same time, skilled-labour shortages, water-supply constraints in the Negev, and energy-cost differentials versus Asia temper longer-term competitiveness, although ongoing defense procurements cushion cyclical swings.[1]Charlotte Trueman, “Intel Suspends Planned Expansion of Its Israeli Semiconductor Manufacturing Plant,” datacenterdynamics.com

Key Report Takeaways

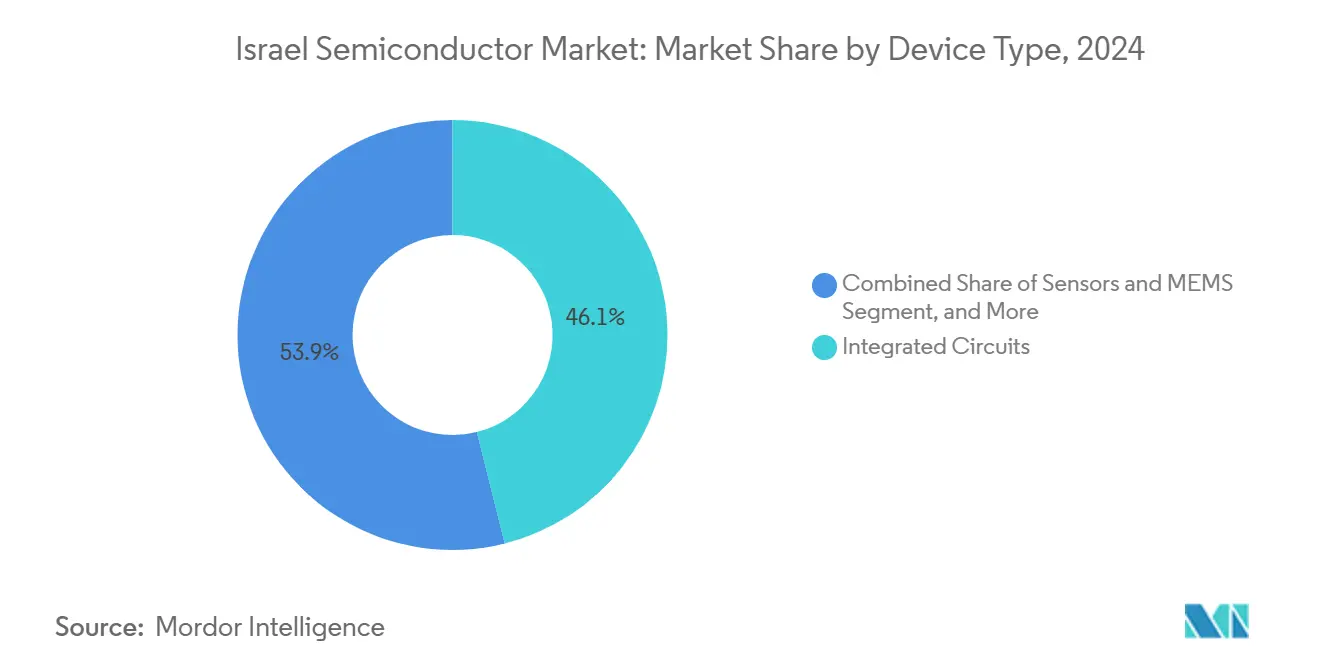

- By device type, Integrated Circuits led with 46% of Israel semiconductor market share in 2024; the segment is forecast to grow at a 10.22% CAGR through 2030.

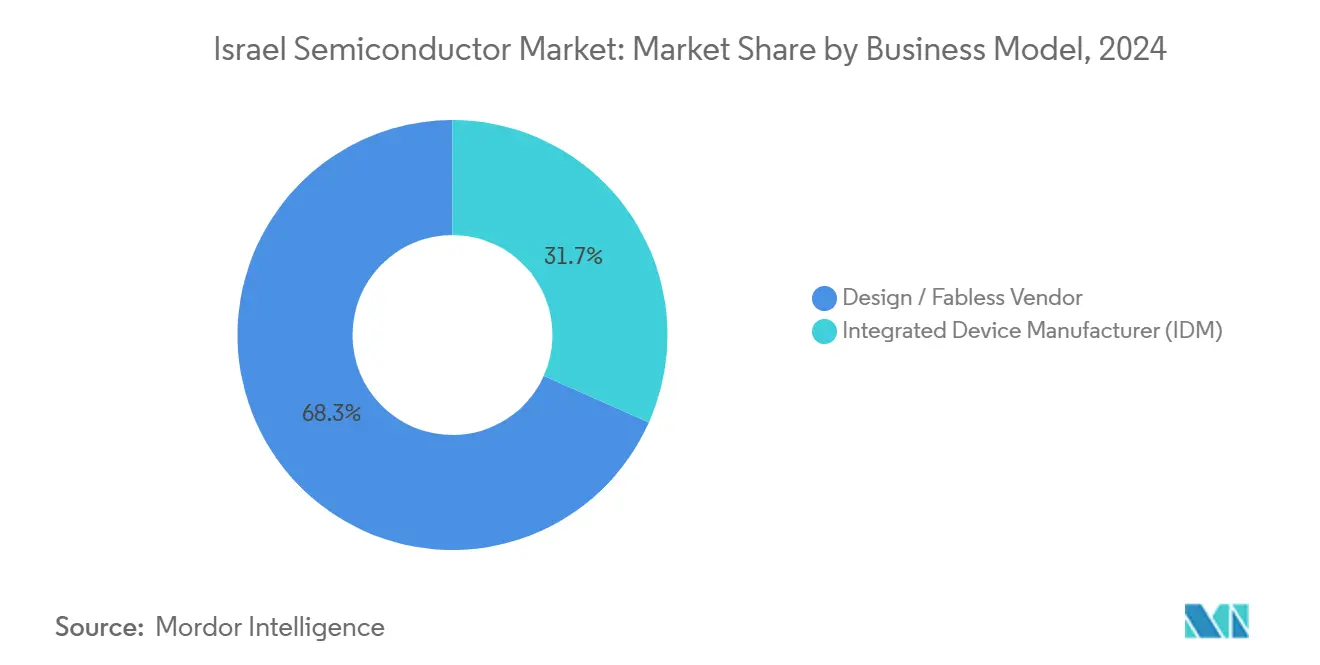

- By business model, the Design/Fabless segment held 68.33% of the Israel semiconductor market size in 2024 and is projected to expand at a 10.98% CAGR through 2030.

- By end-user, Communication captured 24% revenue share in 2024, while Automotive applications are expected to register the highest 9.85% CAGR to 2030.

Israel Semiconductor Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Government-backed fabrication incentives and tax breaks | +2.10% | National, concentrated in development zones | Long term (≥ 4 years) |

| Surge in AI accelerator start-ups driving advanced node tape-outs | +1.80% | Global, with Tel Aviv-Haifa corridor epicenter | Medium term (2-4 years) |

| Defense-grade semiconductor demand amid heightened regional security needs | +1.20% | National, with spillover to allied markets | Short term (≤ 2 years) |

| Global foundry capacity constraints redirecting orders to Israeli fabs | +0.90% | Global, particularly Asia-Pacific overflow | Medium term (2-4 years) |

| Rapid growth of local automotive-grade LiDAR and radar module ecosystem | +1.10% | Global automotive markets, EU focus | Long term (≥ 4 years) |

| Expansion of on-shore data-center build-outs requiring high-speed connectivity ICs | +0.70% | National, with regional data hub aspirations | Medium term (2-4 years) |

| Source: Mordor Intelligence | |||

Government-backed Fabrication Incentives and Tax Breaks

Israel’s Preferred Enterprise and Special Preferred Enterprise regimes slash corporate tax to 7.5% and 5% respectively, significantly improving fab economics.[2]PwC Israel Tax Team, “Israel – Corporate Tax Credits and Incentives,” pwc.com Intel’s USD 3.2 billion grant demonstrates policy resolve even after brief construction pauses in 2024 when personnel were mobilized for national service. The Preferred Technology Enterprise track further reduces levies for R&D-heavy firms, helping maintain Israel’s 6% contribution to high-tech GDP despite limited global capacity share. Secondary projects, including Tower Semiconductor’s planned USD 8 billion overseas fab, still locate R&D leadership in Israel, reinforcing its status as an innovation hub. Incentive certainty continues to attract foreign direct investment, insulating the Israel semiconductor market from cyclical capex cuts.

Surge in AI Accelerator Start-ups Driving Advanced Node Tape-outs

Hailo’s USD 136 million Series C round and unicorn valuation spotlight Tel Aviv’s edge-AI cluster.[3]Shoshanna Solomon, “Israeli AI Chip Maker Hailo Becomes Newest Unicorn,” timesofisrael.com Nvidia’s USD 1.1 billion purchase of Run:ai and Deci validates local expertise in GPU scheduling and automated model compression. Dozens of tape-outs below 7 nm now originate from Israeli design houses targeting inference acceleration, with photonic-computing pioneer CogniFiber touting 1,000× speed gains over GPUs. Military-electronics alumni and close proximity to Nvidia’s 5,000-person Israel campus form a self-reinforcing talent magnet that broadens the Israel semiconductor market opportunity set.

Defense-grade Semiconductor Demand Amid Heightened Regional Security Needs

Heightened threat perceptions accelerate procurement of radiation-hardened processors, secure FPGAs, and wide-temperature-range ICs. Domestic suppliers enjoy preferential contracts, ensuring predictable revenue while funding next-generation R&D. Export opportunities to allies looking for combat-tested electronics widen addressable demand. Requirements for on-chip security, anti-tamper features, and AI-enabled situational awareness align well with Israel’s specialty-IC competencies, supporting near-term cash flows that stabilize the Israel semiconductor market during macro volatility.

Global Foundry Capacity Constraints Redirecting Orders to Israeli Fabs

Persistent shortages in analog, RF, and advanced-packaging lines at Asian foundries have shifted overflow volumes toward Israeli facilities. Tower Semiconductor logged USD 1.44 billion 2024 revenue on the back of diversification demand for RF power and image-sensor processes. Intel Foundry Services leverages its Kiryat Gat assets to offer Western supply-chain security versus geopolitical flashpoints in East Asia. Proximity to European automotive OEMs shortens lead times, adding to Israel’s competitive edge.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Chronic skilled-labor shortages despite immigration programs | -1.40% | National, acute in engineering roles | Long term (≥ 4 years) |

| Water-usage limitations impacting fab scaling in the Negev region | -0.80% | Southern Israel, Negev development zones | Medium term (2-4 years) |

| Energy-cost volatility versus Asian fabrication hubs | -0.60% | National, particularly energy-intensive fabs | Medium term (2-4 years) |

| Geopolitical risk premium inflating insurance and logistics costs | -0.50% | National, with spillover to supply chain partners | Short term (≤ 2 years) |

| Source: Mordor Intelligence | |||

Chronic Skilled-labour Shortages Despite Immigration Programs

Global semiconductor hiring gaps translate into acute local scarcities, with projected 67,000 unfilled roles worldwide by 2030. Intel’s Israel payroll fell below 9,000 in 2025 despite capacity additions, the lowest in a decade. Reserve-duty mobilizations disrupted design schedules during 2024 conflicts. While immigration schemes exist, specialized process-engineering skills take years to cultivate, driving wage inflation that narrows foundry cost advantages. Nvidia’s aggressive recruitment, aiming for 5,000 employees, intensifies the talent tug-of-war.

Water-usage Limitations Impacting Fab Scaling in the Negev Region

Advanced logic fabs consume up to 10 million gallons daily, and Negev desalination capacity trails forecast demand. Industry water use could double by 2035, forcing Israeli fabs to achieve 90% recycling rates comparable with TSMC’s benchmarks. Climate-induced drought risk threatens production continuity and raises capex for reclamation systems, complicating large-scale node-migration projects. Water scarcity therefore caps the upper bound on Israel semiconductor market volume growth, even as value creation remains intact.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Device Type: Integrated Circuits Drive Innovation Leadership

Integrated Circuits generated 46.1% of Israel semiconductor market size in 2024 and are forecast to deliver the fastest 10.22% CAGR through 2030. Analog IC momentum stems from Tower Semiconductor’s BCD platform, which supports automotive LiDAR power rails and AI server voltage regulation. Logic ASICs aimed at edge-AI inference underpin design-service revenues, while specialty memories for mission-critical defense systems lift niche volumes. Sub-7 nm tape-outs underscore a pivot to bleeding-edge nodes yet mature 65 nm BCD lines still underpin automotive reliability. Discrete, optoelectronics, and MEMS categories complement IC performance by supplying power switches, silicon-photonics links, and inertial sensors, but remain secondary in absolute value. The Israel semiconductor industry continues to parlay its deep communication-DSP heritage into next-generation 5G and 6G baseband SoCs, extending design leadership beyond traditional analog strongholds.

Second-order growth levers include heterogeneous integration and on-substrate photonics, which allow local designers to stack RF, logic, and optical layers within a single package. This evolution reduces system latency and energy draw performance attributes prized in autonomous vehicles and defense ISR platforms. Local venture funding prioritizes IC teams that marry software-defined architectures with purpose-built silicon accelerators. Consequently, Israel semiconductor market share held by integrated circuits is likely to edge higher as software-centric workloads pursue hardware offload strategies that Favor ASIC and ASSP proliferation.

By Business Model: Design/Fabless Dominance Reflects IP Strength

Design/Fabless vendors accounted for 68.33% Israel semiconductor market share in 2024 and will likely widen reach at a 10.98% CAGR through 2030. The capital-light model lets firms deploy resources toward IP creation rather than wafer-fab depreciation, mitigating macro demand shocks. CEVA’s royalty stream 90% derived from Asia-Pacific licensing exemplifies scalable earnings without added fixed assets. Start-ups adopt a similar playbook, taping out at TSMC, GlobalFoundries, or Intel, then reinvesting margin into next-gen architectures.

IDM operators remain crucial for sovereign capacity. Intel’s Kiryat Gat delivers leading-edge output and process knowledge spillovers, though headcount reductions and construction pause underscore operational risk. Tower Semiconductor straddles foundry services and proprietary technology, catering to RF and power IC clients seeking bespoke process tweaks. Collectively, hybrid and pure-fabless approaches ensure Israel semiconductor market resilience across technology nodes and end-market cycles.

By End-user Industry: Communication Leads Multi-Sector Expansion

Communication captured 24% Israel semiconductor market size in 2024, buoyed by 5G backhaul, optical transceivers, and Wi-Fi 6 chipsets. Tower Semiconductor’s 1.6 Tbps silicon-photonics modules help hyperscale’s meet exploding AI-training bandwidth targets. Valens’ A-PHY agreements with Intel Foundry Services unlock automotive and industrial ethernet extensions to 15 m links.

Automotive electronics constitute the fastest-rising vertical at 9.85% CAGR, catalysed by Innoviz LiDAR wins and Autotalks V2X safety solutions acquired by Qualcomm in 2025. AI inference workloads, managed by edge accelerators from Hailo and Deci, create a parallel high-growth vector within data-center and embedded markets. Defense, industrial automation, and consumer segments round out demand, each leveraging specialized Israeli chips to differentiate on performance, reliability, or security rather than volume pricing.

Geography Analysis

Israel’s semiconductor activities cluster along the Tel Aviv–Haifa coastal corridor, where universities and defense R&D agencies form a dense innovation lattice. This region accounts for the majority of fabless design houses and serves as Intel’s global AI center. Government development zones in the Negev provide land grants and tax abatements, luring high-volume plants despite water-security caveats. Domestic demand alone cannot absorb capacity, so more than 80% of output targets export markets, predominantly Europe for automotive and Asia-Pacific for wireless and consumer SoCs.

Israel’s geographic positioning offers time-zone overlap with both Europe and the U.S. while remaining a short haul from Asian foundry hubs, enabling efficient design-production-validation loops. Ongoing geopolitical tensions raise insurance premiums and logistics costs, yet they simultaneously boost demand for locally produced, secure chips. Intel and Nvidia cite supply-chain diversification and cyber-resilience as chief reasons to enlarge Israeli footprints. European automakers prefer Israeli RF and LiDAR parts to offset Asia dependence and mitigate sanctions risk.

International expansion strategies rely on technology licensing and joint ventures rather than greenfield fabs abroad. Tower Semiconductor’s proposed USD 8 billion Indian facility illustrates how Israeli know-how migrates globally while higher-margin R&D stays home. Likewise, CEVA’s DSP cores power Chinese and Korean smartphones without necessitating local wafer output. Regional data-center builds reinforce domestic connectivity IC demand and buoy the Israel semiconductor market during downturns in consumer electronics cycles.[4]Soumyarendra Barik, “Tower Closes in on USD 8 Billion India Plant,” indianexpress.com

Competitive Landscape

Israel’s semiconductor arena shows moderate concentration, with the top five players controlling roughly 45% of revenue. Intel dominates advanced logic, while Tower holds sway in specialty analog foundry. CEVA and Valens lead IP licensing and high-speed serial interfaces, respectively. This division of labour lessens direct price wars, allowing firms to coexist across complementary niches. Barriers such as process know-how, military-grade certifications, and longstanding OEM relationships discourage new entrants.

Strategic moves emphasize technology differentiation. Nvidia’s USD 1.1 billion spree for Run:ai and Deci augments its orchestration and model-compression stack, integrating Israeli IP into global GPU roadmaps. Tower’s 65 nm BCD rollout positions it for automotive power-train electrification. CEVA’s 6G DSP launch aligns with carriers planning millimetre-wave densification. Consolidation remains selective; large conglomerates cherry-pick start-ups that fill architecture gaps rather than pursue scale-centric mergers.

Skilled-talent scarcity shapes competition as much as capital. Companies court engineers through equity incentives and hybrid work options, while government retraining grants aim to repatriate expat professionals. Although water and energy costs weigh on Negev site economics, subsidies and security considerations sustain continued, if measured, capacity growth. Overall, technology depth over cost benchmarking defines rivalry within the Israel semiconductor market.

Israel Semiconductor Industry Leaders

Tower Semiconductor Ltd.

Nova Ltd.

Camtek Ltd.

CEVA, Inc.

Valens Semiconductor Ltd.

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- July 2025: Sony announced plans to divest its Israeli IoT-chip unit amid portfolio reshuffles.

- June 2025: Qualcomm bought Autotalks for up to USD 400 million to bolster V2X offerings.

- May 2025: Tower Semiconductor reported USD 358.2 million Q1 revenue, up 9% year-over-year.

- February 2025: Camtek named Lior Aviram Executive Chairman, signalling a stronger M&A focus.

Israel Semiconductor Market Report Scope

| Discrete Semiconductors | Diodes | ||

| Transistors | |||

| Power Transistors | |||

| Rectifier and Thyristor | |||

| Other Discrete Devices | |||

| Optoelectronics | Light-Emitting Diodes (LEDs) | ||

| Laser Diodes | |||

| Image Sensors | |||

| Optocouplers | |||

| Other Device Types | |||

| Sensors and MEMS | Pressure | ||

| Magnetic Field | |||

| Actuators | |||

| Acceleration and Yaw Rate | |||

| Temperature and Others | |||

| Integrated Circuits | By Integrated Circuit Type | Analog | |

| Micro | Microprocessors (MPU) | ||

| Microcontrollers (MCU) | |||

| Digital Signal Processors | |||

| Logic | |||

| Memory | |||

| By Technology Node (Shipment Volume Not Applicable) | Less than 3nm | ||

| 3nm | |||

| 5nm | |||

| 7nm | |||

| 16nm | |||

| 28nm | |||

| 28nm | |||

| Integrated Device Manufacturer (IDM) |

| Design / Fabless Vendor |

| Automotive |

| Communication (Wired and Wireless) |

| Consumer |

| Industrial |

| Computing / Data Storage |

| Data Center |

| AI |

| Government (Aerospace and Defense) |

| By Device Type (Shipment Volume for Device Type is Complementary) | Discrete Semiconductors | Diodes | ||

| Transistors | ||||

| Power Transistors | ||||

| Rectifier and Thyristor | ||||

| Other Discrete Devices | ||||

| Optoelectronics | Light-Emitting Diodes (LEDs) | |||

| Laser Diodes | ||||

| Image Sensors | ||||

| Optocouplers | ||||

| Other Device Types | ||||

| Sensors and MEMS | Pressure | |||

| Magnetic Field | ||||

| Actuators | ||||

| Acceleration and Yaw Rate | ||||

| Temperature and Others | ||||

| Integrated Circuits | By Integrated Circuit Type | Analog | ||

| Micro | Microprocessors (MPU) | |||

| Microcontrollers (MCU) | ||||

| Digital Signal Processors | ||||

| Logic | ||||

| Memory | ||||

| By Technology Node (Shipment Volume Not Applicable) | Less than 3nm | |||

| 3nm | ||||

| 5nm | ||||

| 7nm | ||||

| 16nm | ||||

| 28nm | ||||

| 28nm | ||||

| By Business Model | Integrated Device Manufacturer (IDM) | |||

| Design / Fabless Vendor | ||||

| By End-user Industry | Automotive | |||

| Communication (Wired and Wireless) | ||||

| Consumer | ||||

| Industrial | ||||

| Computing / Data Storage | ||||

| Data Center | ||||

| AI | ||||

| Government (Aerospace and Defense) | ||||

Key Questions Answered in the Report

How large is the Israel semiconductor market in 2025?

The sector is valued at USD 5.08 billion in 2025 and is projected to reach USD 7.07 billion by 2030.

What compound annual growth rate is forecast for Israel’s chip sector through 2030?

A 6.83% CAGR is expected for the 2025–2030 period.

Which device type currently brings in the most revenue?

Integrated Circuits hold 46% of 2024 revenue and are set to rise at a 10.22% CAGR through 2030.

Why do fabless design houses dominate the country’s chip landscape?

Preferential tax regimes and a strong R&D talent base let companies focus on intellectual property while using global foundries for production.

How is Israel tackling the skilled-labor shortage in semiconductor engineering?

Government immigration programs, retraining grants, and competitive equity packages aim to attract and retain engineers, though hiring gaps remain.

What role do defense applications play in the local chip ecosystem?

Military demand for ruggedized, secure processors supplies steady revenue and funds R&D for next-generation, high-reliability components.

Page last updated on: