Americas Semiconductor Device Market Size and Share

Market Overview

| Study Period | 2020 - 2031 |

|---|---|

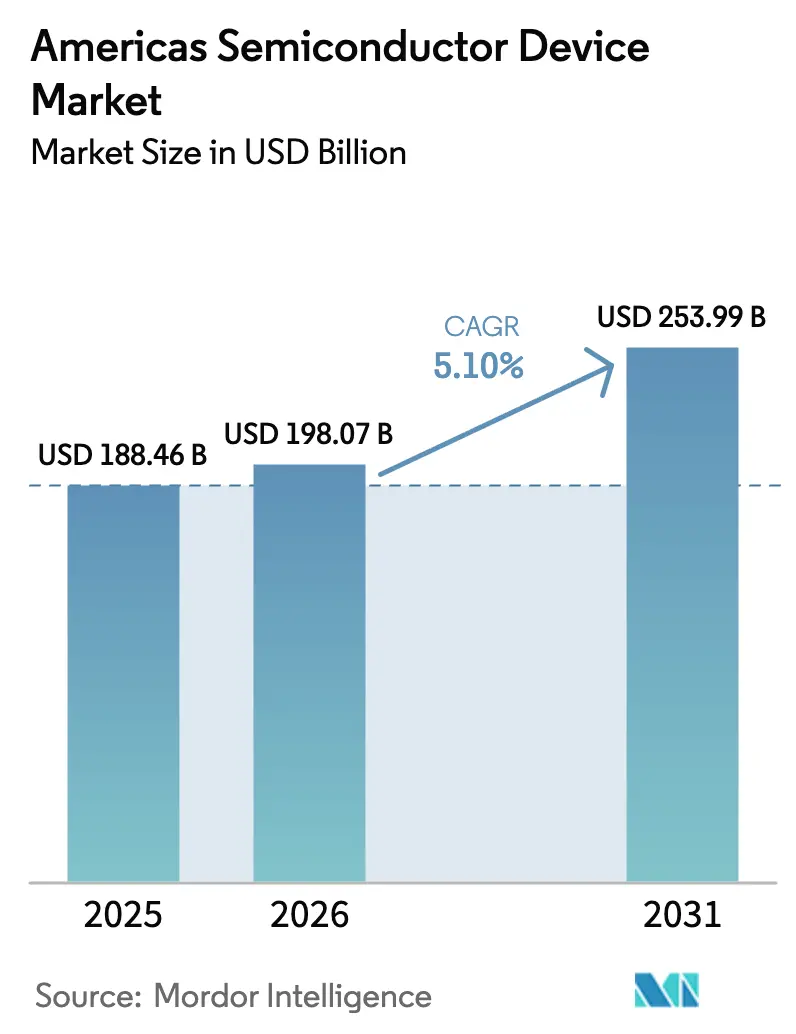

| Base Year Market Size (2025) | USD 188.46 Billion |

| Market Size (2026) | USD 198.07 Billion |

| Market Size (2031) | USD 253.99 Billion |

| Growth Rate (2026 - 2031) | 5.10% CAGR |

| Fastest Growing Market | South America |

| Largest Market | North America |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

Americas Semiconductor Device Market Analysis by Mordor Intelligence

The Americas semiconductor device market size is expected to grow from USD 188.46 billion in 2025 to USD 198.07 billion in 2026 and is forecast to reach USD 253.99 billion by 2031 at 5.1% CAGR over 2026-2031. Recent investment pledges under the CHIPS Act, the race for artificial-intelligence (AI) leadership, and a re-shoring policy push redefined competitive priorities across the supply chain. North America held an overwhelming 94.5% Americas semiconductor device market share in 2024, yet South America displayed the fastest regional expansion with an 8.1% CAGR for 2025-2030 as Mexican and Brazilian fabs scaled output. Integrated circuits led every device category with 81.2% revenue share in 2024; they also clocked the highest 7.9% CAGR because AI training clusters, vehicle autonomy, and 5G phones required denser logic and advanced memory. Although legacy nodes of ≥65 nm still represented 54.4% of production in 2024, the ≤5 nm segment was growing 15.2% a year as cloud providers demanded higher performance per watt. Silicon remained dominant, but silicon-carbide devices logged a 19.6% CAGR, reflecting electrified transport and renewable-energy inverters that favour wide-band-gap efficiency gains.

Key Report Takeaways

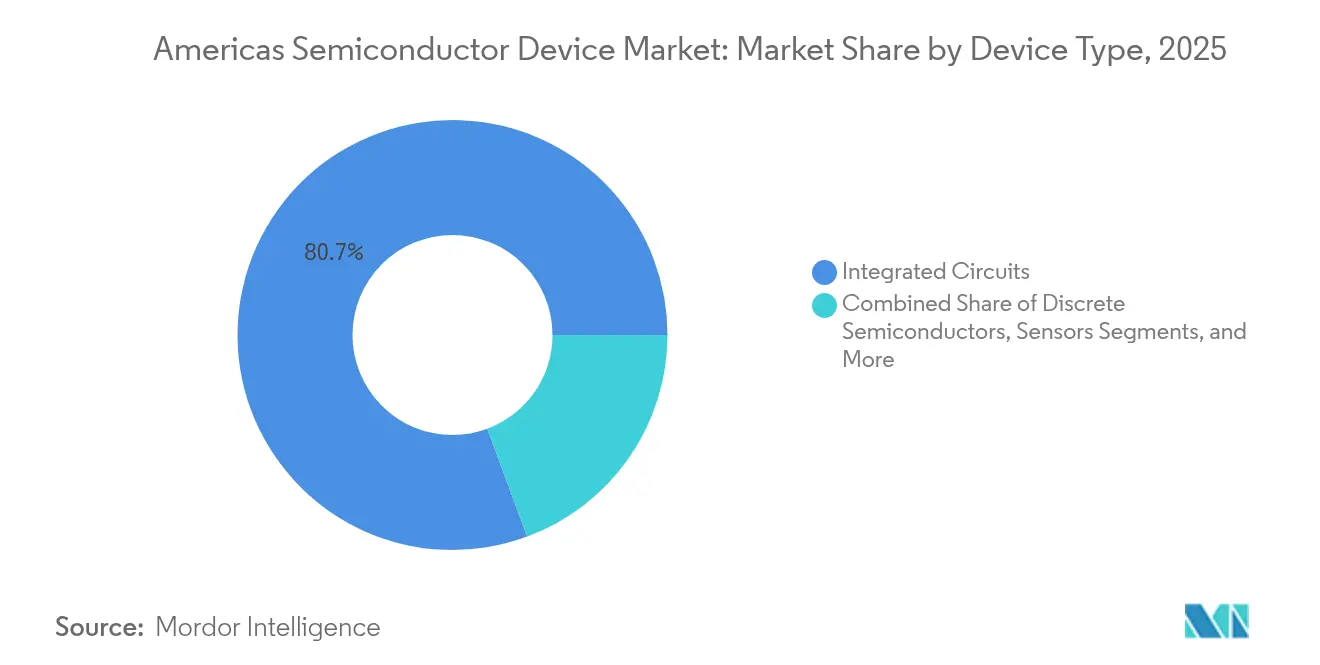

- By device type, integrated circuits held 80.65% of the Americas semiconductor device market share in 2025; the segment was forecast to expand at a 7.45% CAGR through 2031.

- By region, North America accounted for 94.10% revenue in 2025, while South America was set to grow at 7.7% CAGR over 2026-2031.

- By technology node, ≥65 nm processes retained a 53.85% share in 2025, yet ≤5 nm capacity was projected to climb at a 14.3% CAGR to 2031.

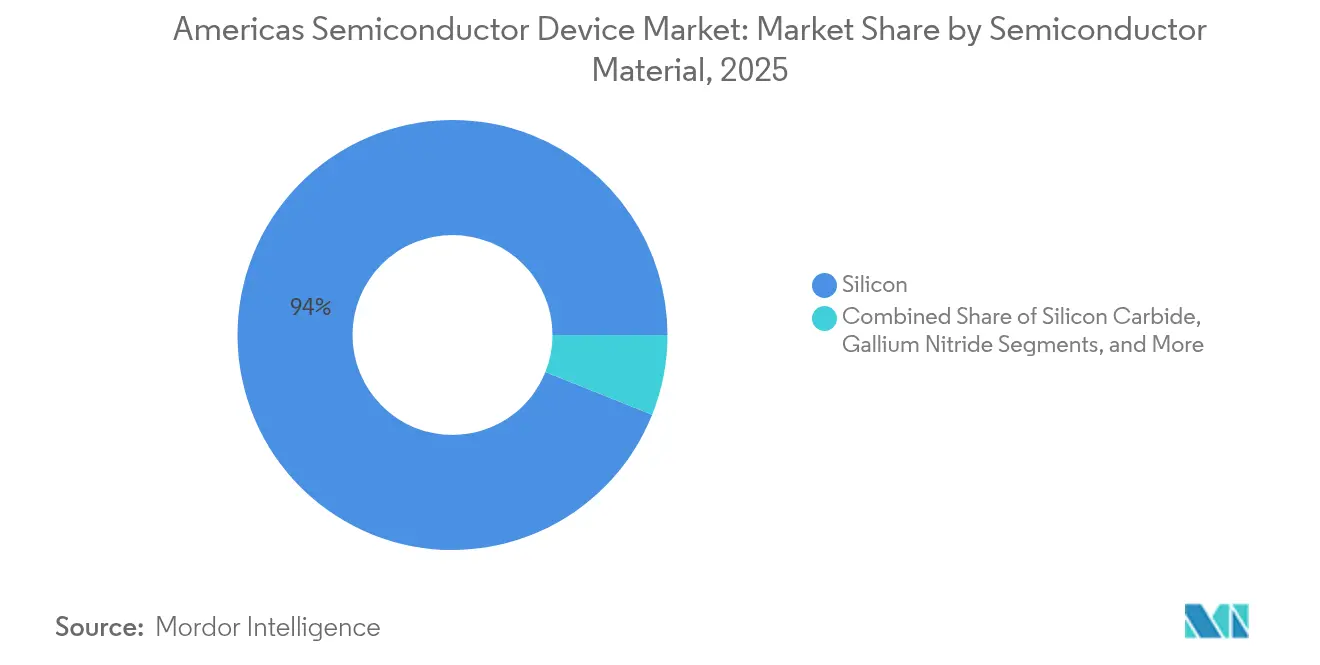

- By semiconductor material, silicon commanded 93.95% share in 2025, whereas silicon-carbide devices were advancing on a 18.7% CAGR to 2031.

- By end-user vertical, the communication sector led with 30.15% revenue in 2025; automotive semiconductors were forecast to grow at 8.75% CAGR to 2031.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of 2026.

Americas Semiconductor Device Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| CHIPS Act-Driven Fabrication Capacity Expansion in North America | +1.8% | North America, with spillover effects to Mexico | Medium term (2-4 years) |

| ADAS-Enabled Vehicle Demand in Mexico and Brazil | +0.9% | Mexico, Brazil | Medium term (2-4 years) |

| 5G Stand-Alone Roll-out Elevating RF Front-End IC Consumption | +1.2% | North America, with gradual adoption in South America | Short term (≤ 2 years) |

| Hyperscale AI Server Build-out Increasing HBM and GPU Requirements | +1.5% | North America | Short term (≤ 2 years) |

| Renewable-Energy Incentives Boosting Power Semiconductor Adoption in Brazil and Chile | +0.7% | Brazil, Chile | Medium term (2-4 years) |

| Nearshoring of Backend Assembly and Test to Mexico | +0.6% | Mexico | Medium term (2-4 years) |

| Source: Mordor Intelligence | |||

CHIPS Act-Driven Fabrication Capacity Expansion in North America

Massive federal incentives under the CHIPS and Science Act unlocked more than USD 450 billion in private commitments that aimed to triple domestic wafer output by 2032.[1]U.S. Department of Commerce, “CHIPS Act Preliminary Funding Terms,” commerce.gov Intel secured USD 8.5 billion in grants for multistate expansions, while TSMC received USD 6.6 billion for its two Arizona megafabs. Supplier ecosystems clustered around those projects, as over 40 tier-one chemical and equipment firms co-located nearby to shorten lead times. These clusters improved logistics costs and accelerated knowledge transfer, yet a 60% dependence on imported specialty gases and chemicals still forced new capital outlays for on-shore materials capacity. Ultimately, the investment surge positioned the Americas semiconductor device market for higher self-sufficiency without fully insulating it from resource constraints.

ADAS-Enabled Vehicle Demand in Mexico and Brazil

Electrification and Level-2 driver-assistance adoption pushed automotive semiconductor content per vehicle up 35% in leading Mexican and Brazilian assembly lines during 2024. Local plants integrated radar, lidar, and image-sensor arrays that required high-reliability microcontrollers and power devices. Bosch and Continental pursued joint ventures for on-shore packaging lines to mitigate import tariffs that could rise to 25%. Policymakers signalled additional fiscal credits for auto-grade chips, encouraging further capacity moves. As a result, automotive orders buffered the Americas semiconductor device market against consumer-electronics cyclicality and created a dependable mid-term revenue uplift.

5G Stand-Alone Roll-out Elevating RF Front-End IC Consumption

North American carriers budgeted more than USD 35 billion for 5G networks in 2025 alone as millimetre-wave nodes densified urban coverage while mid-band filled suburban gaps. Each 5G handset carried 25% more RF value than its 4G predecessor, multiplying demand for acoustic filters, power amplifiers, and antenna tuners. Gallium-nitride technology captured share because it sustained higher voltages at mmWave frequencies, yet defense and automotive buyers competed for the same GaN wafer inventory. Supply tightness pushed lead times on select RF front-end devices past 40 weeks in early 2025, demonstrating how wireless upgrades directly amplified revenue momentum for the Americas semiconductor device market.

Hyperscale AI Server Build-out Increasing HBM and GPU Requirements

AI model-training clusters required unprecedented bandwidth and memory density, sending high-bandwidth memory (HBM) unit shipments up 70% year over year in 2025. A single new U.S. data center installed 10,000 AI accelerators and 80,000 HBM stacks, translating into more than USD 500 million of incremental chip content. TSMC introduced System-on-Wafer production to triple compute density by 2027, an innovation that compounded demand for leading-edge logic and advanced packaging. Traditional CPU vendors raced to redesign products around heterogenous compute, while Qualcomm entered the data-centre processor arena with devices tuned to Nvidia accelerator fabrics. The hyperscale capex wave, therefore, reinforced the high-growth outlook embedded in the Americas semiconductor device market.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Water and Power Supply Constraints in US Southwest Fabs | -0.8% | U.S. Southwest (Arizona, New Mexico, Texas) | Long term (≥ 4 years) |

| Scarcity of Skilled Semiconductor Engineers across the Americas | -1.1% | North America, with an emerging impact in South America | Medium term (2-4 years) |

| Export Controls on Advanced Equipment and IP | -0.7% | North America | Medium term (2-4 years) |

| Volatile Silicon Wafer Pricing due to Limited Regional Supply | -0.5% | Americas-wide | Short term (≤ 2 years) |

| Source: Mordor Intelligence | |||

Water and Power Supply Constraints in U.S. Southwest Fabs

New fabs in Arizona and Texas consumed up to 10 million gallons of ultrapure water daily, creating direct competition with municipal users. Intel invested USD 200 million in reclamation systems that recycled 90% of process water, yet those eco-projects added 2% to operating expenses and did not fully mitigate long-term drought risk. Rising electricity demand forced utilities to accelerate grid upgrades, further lifting production costs. These constraints reduced effective capacity gains from CHIPS Act incentives and threatened the cost competitiveness of the Americas semiconductor device market over the long horizon.

Scarcity of Skilled Semiconductor Engineers across the Americas

The Semiconductor Industry Association projected a 33% rise in chip-sector employment by 2030, yet warned that 67,000 vacancies could remain unfilled. Field-service engineer shortages delayed tool installations by 45 days, slowing ramp schedules at greenfield fabs. Universities expanded chip curricula—Purdue’s enrolment in semiconductor design courses rose eightfold—but the talent pipeline lagged investment timetables. Firms accelerated automation and cross-training programs to extract productivity from limited human capital, but wage inflation persisted. Unless immigration hurdles ease or vocational initiatives scale rapidly, workforce scarcity will continue to subtract growth potential from the Americas semiconductor device market.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Device Type: Integrated Circuits Extend Leadership Amid AI Upsurge

Integrated circuits captured 80.65% revenue in 2025 and advanced on a 7.45% CAGR projection, keeping the Americas semiconductor device market size firmly weighted toward complex logic and memory. AI training, autonomous driving, and industrial edge computing each increased silicon content per system, lifting average selling prices for high-bandwidth memory and inference accelerators. Discrete power devices, though smaller in value, gained strategic importance as silicon-carbide and gallium-nitride switches replaced silicon IGBTs in electric vehicles, improving powertrain efficiency and thermal margins. The Americas semiconductor device industry also saw optoelectronics broaden into lidar and image-sensing, providing incremental diversification against the cyclic smartphone segment.

A widening array of embedded applications drove resilient sensor volumes, yet price pressure persisted because many designs relied on mature process lines with fully depreciated assets. Analog ICs offered stable cash flow due to legacy automotive and industrial sockets that require decades-long supply continuity. Meanwhile, logic and memory displayed higher volatility in line with hyperscale capex cycles. Despite those swings, the integrated-circuits category delivered steady ecosystem investment, reinforcing design talent retention inside the Americas semiconductor device market.

By Wafer Size: 300 mm Entrenchment and 450 mm Ambition

In 2025, 300 mm lines accounted for 57.60% of production and underpinned nearly every leading-edge node, anchoring the largest slice of the Americas semiconductor device market size. Foundries noted 30% lower unit costs after migrating mature analog products from 200 mm to 300 mm substrates, widening gross-margin cushions. Equipment makers concurrently refined 450 mm pilot tools; although that diameter remained niche, it logged a 16.4% CAGR outlook to 2031 as manufacturers chased further economies of scale.

≤200 mm fabs preserved relevance because automotive and industrial buyers valued proven reliability over raw compute density. These fabs also benefited from the near-shoring of backend assembly in Mexico, which reduced cycle times for legacy components. The Americas semiconductor device market continued to balance investments across diameters to hedge against cyclical oversupply at any single node or wafer size.

By Technology Node: Legacy Resilience Beside ≤5 nm Sprint

The ≥65 nm category preserved 53.85% of Americas semiconductor device market share in 2025, leveraging fully depreciated tools and long-established design ecosystems that kept unit costs low. In contrast, the ≤5 nm segment was forecast to surge at a 14.3% CAGR from 2026 to 2031, driven by AI accelerators, graphics processors and high-performance mobile chipsets that demand extreme-ultraviolet lithography. This bifurcation helped stabilize the Americas semiconductor device market size because mature nodes served industrial and automotive customers while leading-edge capacity captured premium margins from cloud providers.

Mid-range nodes between 45 nm and 16 nm provided a cost-performance bridge for advanced driver assistance systems and secure microcontrollers, ensuring design optionality across price points. Foundries and equipment makers formed joint pilot lines to spread the USD 15 billion capex burden required for next-generation lithography tools. TSMC’s forthcoming A16 nanosheet process, announced for 2026 production, promised an 8-10% speed uplift and up to 20% power reduction over its prior node, underscoring the cadence of innovation at the leading edge. Meanwhile, an industrial-automation supplier migrated control ICs to 90 nm silicon and cut bill-of-material costs 40% without sacrificing performance, illustrating that optimal node choice remains application-specific. This coexistence of legacy, mid-range and bleeding-edge processes diversified revenue streams and cushioned the Americas semiconductor device market against single-node volatility.

By Semiconductor Material: Silicon-Carbide Gains in Power Electronics

Silicon devices still controlled 93.95% revenue in 2025, but silicon-carbide volumes expanded on a 18.7% CAGR path, propelled by EV inverters and high-power solar installations. A leading automaker replaced silicon IGBTs with SiC MOSFETs, improving driving range 3% and trimming cooling weight 25%, an outcome that reinforced the performance narrative for wide-band-gap adoption. The U.S. Commerce Department earmarked USD 79 million for SiC substrate expansion to address material bottlenecks.

Gallium-nitride meanwhile took early market share in 5G power amplifiers and fast chargers. Gallium-arsenide and indium-phosphide preserved niche positions in photonics and high-frequency defense systems. The wider material palette increased supply-chain complexity, yet it unlocked differentiated performance tiers that raised blended average selling prices within the Americas semiconductor device market.

By End-User Vertical: Automotive Outpaces Communication

Communication infrastructure recorded 30.15% revenue in 2025 on persistent 5G rollouts, but automotive electronics now posted the fastest 8.75% CAGR to 2031. EV drivetrains, lidar sensor arrays and zonal architectures multiplied chip counts above USD 2,000 per premium vehicle. Industrial automation sustained steady demand as manufacturers deployed Industry 4.0 retrofits that required robust microcontrollers and edge AI inference. Consumer electronics volumes remained large, though growth moderated because handset refresh cycles lengthened.

Computing and storage rebounded thanks to AI servers adopting HBM and custom accelerators, lifting memory bit demand. Aerospace-and-defense remained a smaller slice yet paid premium margins for radiation-hardened or ultra-reliable components. Healthcare adoption of semiconductor-rich imaging systems added a future upside lever. Collectively, vertical diversification lessened cyclical swings for the Americas semiconductor device market.

Geography Analysis

North America dominated the Americas semiconductor device market with 94.10% revenue in 2025, a position reinforced by CHIPS Act incentives that sought to triple wafer capacity by 2032. Arizona, Texas, and New York attracted multi-billion-dollar fab commitments and fostered supplier agglomerations that shortened development cycles. Nevertheless, water scarcity and a looming 67,000-engineer talent gap threatened to dilute the long-term ROI of that capacity build.

South America strengthened its role as a growth engine with an 7.7% CAGR outlook for 2026-2031. Brazil’s automotive electrification surge and industrial IoT upgrades increased local chip demand, while its universities nurtured design centers for region-specific microcontrollers. Mexico leveraged USMCA trade certainty and cost advantages to absorb backend assembly and test lines relocating from Asia, trimming time-to-market and logistics charges for North American customers. Chile’s renewable-energy boom further amplified SiC and GaN imports, supporting new regional demand pools that broadened the Americas semiconductor device market size.

Cross-border policy collaboration also intensified. The U.S. State Department and Mexico formalized a semiconductor supply-chain working group that addressed skills, infrastructure, and security requirements. Regional governments explored synchronized incentives to avoid subsidy competition, reflecting the strategic importance of supply resilience for the Americas semiconductor device market.

Competitive Landscape

Market structure varied by segment. Memory and ≤5 nm logic remained highly concentrated because few firms managed the USD 15 billion capex per fab needed for extreme-ultraviolet lithography. Conversely, discrete and sensor categories were fragmented as entry costs were lower, and technology cycles were slower. To secure differentiated performance, hyperscalers, automotive OEMs, and even industrial firms invested in custom-silicon programs that deepened vertical integration.

Partnership models evolved in response to soaring tape-out and equipment costs. Foundries collaborated with equipment makers on jointly funded pilot lines that derisked technology ramps. System companies joined multi-party packaging consortia to accelerate chiplets and 3D integration. These alliances re-distributed capital intensity across the ecosystem, reinforcing the innovation cadence that underpinned the Americas semiconductor device market.

Mergers and acquisitions continued. Synopsys agreed to acquire Ansys for USD 35 billion to merge simulation with electronic-design-automation workflows, an action expected to streamline chip-package-system co-optimization. Qualcomm’s launch of data center CPUs interoperable with Nvidia accelerators signalled fresh rivalry in AI infrastructure. Infineon preserved a 13.5% share of the global automotive chip revenue, confirming leadership in vehicle power and connectivity solutions.[4]Infineon Technologies AG, “Infineon Automotive Market Share Release,” infineon.com Competitive intensity, therefore, remained high, yet collaborative frameworks emerged to temper financial risk.

Americas Semiconductor Device Industry Leaders

Intel Corporation

Qualcomm Incorporated

NVIDIA Corporation

Texas Instruments Incorporated

Broadcom Inc.

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- April 2025: TSMC unveiled its A14 process at the North America Technology Symposium, promising 15% speed or 30% power gains and a 20% logic-density jump over prior nodes.

- April 2025: Intel’s new CEO outlined a manufacturing and AI overhaul aimed at strengthening the company’s competitive stance in advanced logic and accelerators.

- March 2025: SK hynix committed USD 4 billion for an advanced-packaging and R&D complex in Purdue Research Park to serve AI memory demand.

- January 2025: The U.S. Department of Commerce announced preliminary terms for up to USD 105 million in CHIPS Act support for Analog Devices and USD 79 million for Coherent to expand domestic substrate and materials capacity.

Research Methodology Framework and Report Scope

Market Definitions and Key Coverage

Our study defines the Americas semiconductor device market as the value of all newly manufactured discrete, optoelectronic, sensor, and integrated-circuit chips shipped by IDMs and fabless vendors into North and South America across automotive, communication, consumer, industrial, computing, aerospace, and medical end uses.

Excluded are capital equipment, wafer-foundry services, outsourced assembly, design IP royalties, and any revenue earned a second time through resale.

Segmentation Overview

- By Device Type

- Discrete Semiconductors

- Optoelectronics

- Sensors

- Integrated Circuits

- Analog ICs

- Logic ICs

- Memory ICs

- Micro ICs

- Microprocessors (MPU)

- Microcontrollers (MCU)

- Digital Signal Processors (DSP)

- By Wafer Size

- ≤ 200 mm

- 300 mm

- ≥ 450 mm

- By Technology Node

- ≥ 65 nm

- 45–28 nm

- 22–16 nm

- 10–7 nm

- ≤ 5 nm

- By Semiconductor Material

- Silicon (Si)

- Silicon Carbide (SiC)

- Gallium Nitride (GaN)

- Others (GaAs, InP, etc.)

- By End-User Vertical

- Automotive

- Communication (Wired and Wireless)

- Consumer Electronics

- Industrial

- Computing and Data Storage

- Aerospace and Defense

- Healthcare and Medical Devices

- By Region

- North America

- United States

- Canada

- South America

- Brazil

- Argentina

- Mexico

- Rest of South America

- North America

Detailed Research Methodology and Data Validation

Primary Research

To validate desk inputs, we interview foundry planners, fabless design leads, OSAT procurement heads, and tier-one OEM component buyers in the United States, Canada, Mexico, Brazil, and Argentina.

Structured surveys capture wafer-start intent, average selling-price drift, and inventory corrections, letting us stress-test preliminary estimates and assumptions with on-the-ground insight.

Desk Research

Mordor analysts first map the addressable pool using public datasets such as World Semiconductor Trade Statistics, UN Comtrade customs codes, the US Census ICT survey, Brazil's MDIC export tables, and Statistics Canada manufacturing shipments.

Company filings, investor decks, and association yearbooks (SIA Factbook, SEMI WWSEMS) enrich technology-node splits, while patent intensity trends are reviewed through Questel, and headline financials through D&B Hoovers.

These sources anchor historical demand signals and check regional share splits.

Additional context flows from peer-reviewed journals tracking GaN and SiC adoption, central-bank GDP outlooks, and government incentive trackers (CHIPS Act grant ledgers, Brazil PADIS).

The sources named illustrate our approach and do not represent an exhaustive list.

Market-Sizing & Forecasting

A top-down and bottom-up hybrid model is applied.

Regional production plus net imports reconstruct the demand pool, which is then corroborated with sampled vendor roll-ups and channel checks.

Key variables include wafer-start capacity, die yield by node, EV penetration in light-vehicle sales, hyperscale GPU attach rates, CHIPS Act subsidy disbursements, and smartphone replacement cycles.

Multivariate regression projects each driver; scenario analysis adjusts for policy or supply shocks.

Where bottom-up gaps emerge, normalized ASP benchmarks are imputed from verified trade data before final aggregation.

Data Validation & Update Cycle

Outputs pass variance checks against WSTS quarterly sales, SIA regional growth, and major vendor guidance.

Peer review precedes sign-off, and the model refreshes annually, with interim updates triggered by material fab announcements or demand shocks.

A last-minute analyst sweep ensures clients receive the freshest view.

Why Mordor's Americas Semiconductor Device Baseline Commands Reliability

Published numbers rarely match because firms differ on scope, input variables, refresh cadence, and currency translation.

By isolating pure device revenue and updating every year, Mordor delivers a balanced baseline decision-makers can trust.

Gap drivers typically stem from whether equipment and services are bundled, how aggressively ASP erosion is applied, and if South America is fully captured.

Benchmark comparison

| Market Size | Anonymized source | Primary gap driver |

|---|---|---|

| USD 188.46 B (2025) | Mordor Intelligence | - |

| USD 161.4 B (2024) | Regional Consultancy A | North America only, equipment bundled, static ASP assumption |

| USD 10.18 B (2025) | Trade Journal B | Tracks only US compound and power devices; ICs excluded; vendor survey not adjusted for missing firms |

The comparison shows that scope width and refresh rigor largely explain headline gaps. By tethering forecasts to verifiable trade flows and periodically re-contacting industry participants, Mordor Intelligence provides a dependable, transparent starting point for strategic planning.

Key Questions Answered in the Report

What is the current value of the Americas semiconductor device market?

The market was valued at USD 198.07 billion in 2026, with a forecast to reach USD 253.99 billion by 2031 on a 5.1% CAGR trajectory.

Which device type leads revenue in the Americas semiconductor device market?

Integrated circuits dominated with 80.65% revenue share in 2025 and are projected to grow fastest at an 7.45% CAGR through 2031.

Why is silicon-carbide attracting investment attention?

Silicon-carbide enables higher power density and efficiency for electric vehicles and renewable-energy inverters; its revenue is expanding at a 18.7% CAGR in the region.

How does the CHIPS Act influence regional capacity?

Federal incentives unlocked more than USD 450 billion in private commitments, aiming to triple U.S. wafer capacity by 2032 and deepen supply-chain localisation.

Which end-user vertical will grow fastest?

Automotive electronics are projected to register a 8.75% CAGR to 2031 as vehicles integrate electrified drivetrains and ADAS features.

What risks could slow market growth?

Key restraints include water scarcity in the U.S. Southwest, a projected shortfall of 67,000 skilled engineers by 2030, and tighter export-control regimes on advanced equipment.

Page last updated on: