France Semiconductor Market Size and Share

Market Overview

| Study Period | 2019 - 2030 |

|---|---|

| Forecast Data Period | 2025 - 2030 |

| Historical Data Period | 2019 - 2023 |

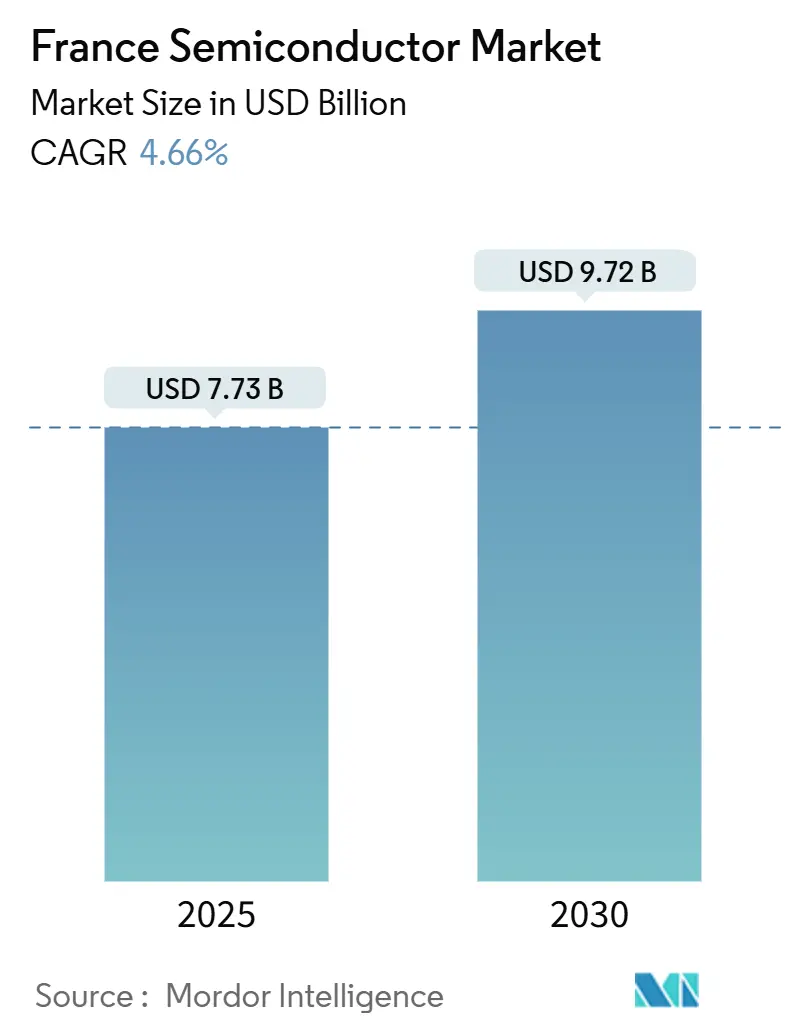

| Market Size (2025) | USD 7.73 Billion |

| Market Size (2030) | USD 9.72 Billion |

| Growth Rate (2025 - 2030) | 4.66% CAGR |

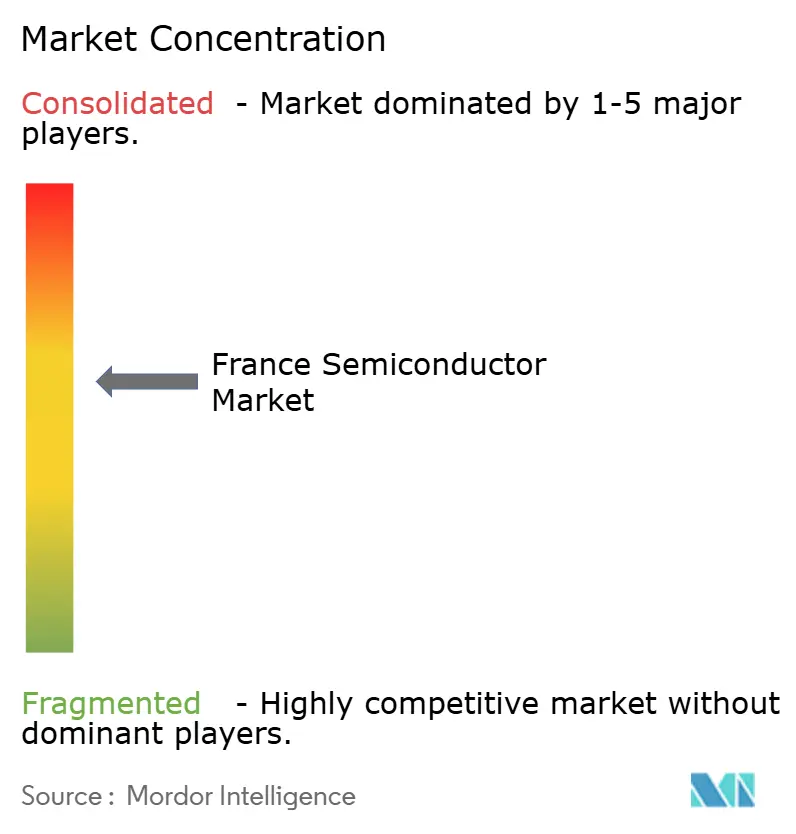

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

France Semiconductor Market Analysis by Mordor Intelligence

The France semiconductor market size stood at USD 7.73 billion in 2025 and is forecast to reach USD 9.72 billion by 2030, advancing at a 4.66% CAGR. Momentum stems from the EU Chips Act, national incentives for sub-10 nm process technologies, and strategic moves by domestic champions to shorten supply chains. Strong capital spending on 300 mm wafer lines, an expanding FD-SOI substrate ecosystem, and rising orders from automotive electrification programs collectively reinforce growth. Competitive pressure is intensifying as fabless startups gain design wins in AI acceleration, while integrated-device manufacturers (IDMs) re-tool legacy fabs to serve new power-device and heterogenous-integration demand.[1]European Commission, “European Chips Act – Update on the Latest Milestones,” digital-strategy.ec.europa.eu

Key Report Takeaways

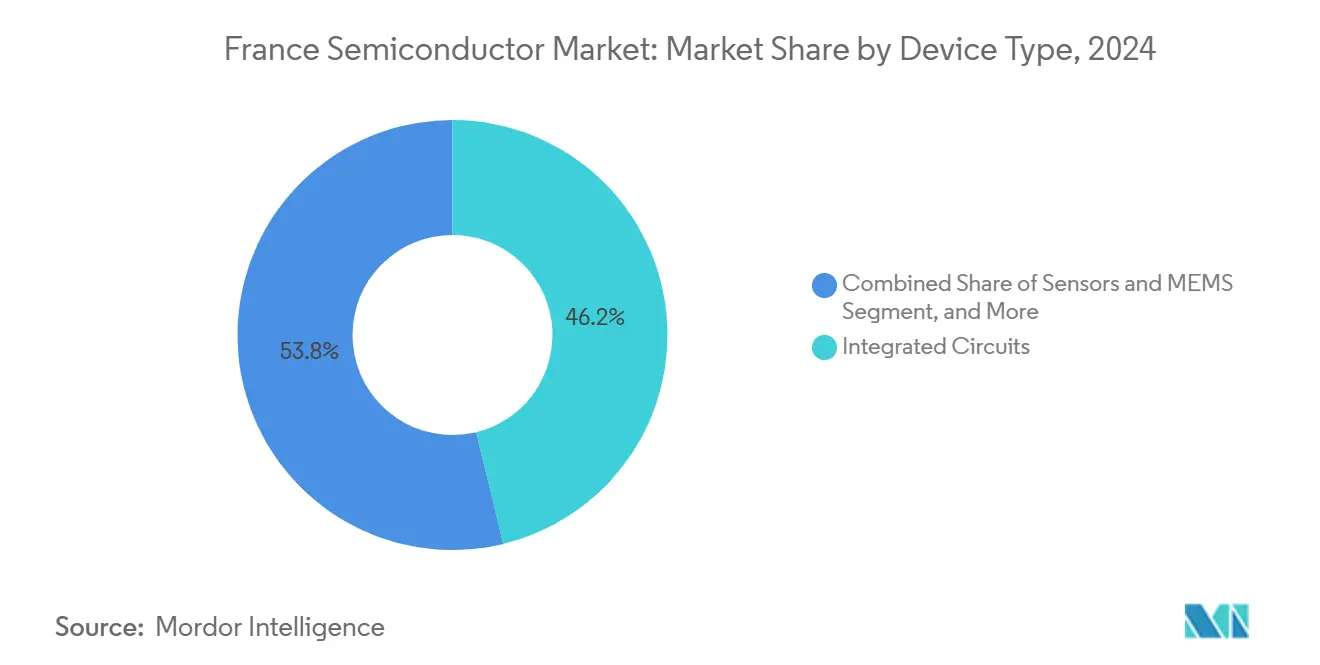

- By device type, Integrated Circuits led with 46.20% revenue share in 2024; Sensors and MEMS is projected to expand at a 7.59% CAGR through 2030.

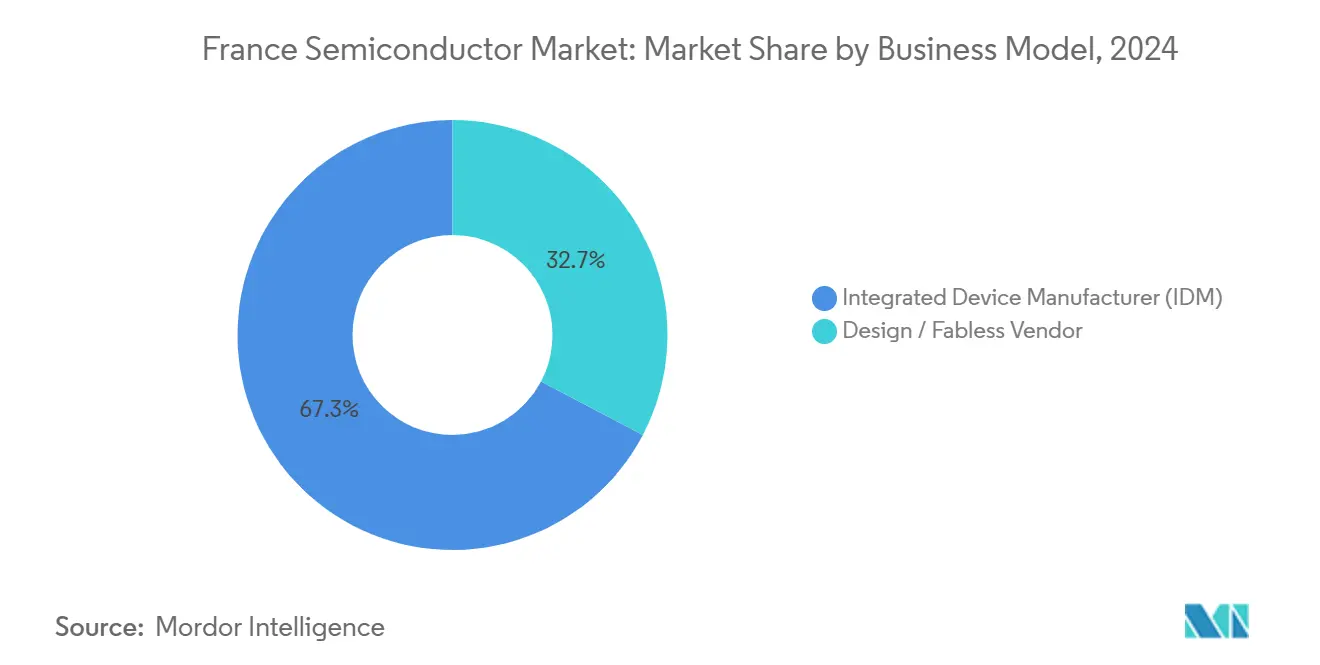

- By business model, IDM players held 67.31% of the France semiconductor market share in 2024, while fabless vendors are set to grow at 7.11% CAGR to 2030.

- By end-user industry, Automotive accounted for 31.40% share of the France semiconductor market size in 2024 and AI applications are advancing at an 8.01% CAGR through 2030.

France Semiconductor Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| EU Chips Act investment flow | +1.20% | France, with spillover to EU | Medium term (2-4 years) |

| Vehicle electrification push | +0.80% | France, Germany automotive hubs | Long term (≥ 4 years) |

| AI and data-center chip demand surge | +1.50% | Global, concentrated in France tech centers | Short term (≤ 2 years) |

| 5G and fiber network rollout | +0.60% | France national coverage | Medium term (2-4 years) |

| FD-SOI ecosystem expansion | +0.40% | France, with Soitec leadership | Long term (≥ 4 years) |

| Diamond/GaN/SiC power-device R&D consortia | +0.20% | France research centers | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

EU Chips Act Investment Flow

France secured EUR 2.9 billion in state support for STMicroelectronics’ Crolles expansion, targeting 14,000 300 mm wafers per week by 2027.[2]STMicroelectronics, “Q4 and FY 2024 Financial Results,” stmicroelectronics.com Linked public-private funding has opened a pipeline of advanced-packaging, OSAT and substrate projects that collectively amplify domestic capacity. Mandatory workforce-development clauses inside grant agreements tie disbursements to new vocational-training seats, ensuring the talent base grows alongside fabs. Ancillary startups such as Keysom, which raised EUR 4 million for processor-design automation, illustrate how mainline funding is spawning a wider innovation halo.

Vehicle Electrification Push

France’s 2035 zero-tailpipe target is raising SiC and GaN content per vehicle. Renault and STMicroelectronics co-develop traction inverters expected to cut power losses by 45% from 2026, translating into cheaper battery packs and longer range. Multi-year orders from ZF worth EUR 30 billion confirm a persistent pipeline for 1200 V SiC MOSFETs. Domestic policy sweeteners, including purchase subsidies and charging-network grants, secure steady pull-through for high-voltage ICs, gate drivers and on-board-charger solutions.

AI and Data-Center Chip Demand Surge

Brookfield’s EUR 20 billion data-center program allocates EUR 5 billion directly to semiconductor-intensive power and cooling systems.[3]Brookfield Asset Management, “Brookfield and French Government Announce €20 Billion Investment in AI Infrastructure,” brookfield.com Fabless newcomer SiPearl raised EUR 130 million to tape out its 61-billion-transistor “Rhea-1” CPU, built on Samsung’s 4 nm process and paired with HBM3E stacks. Domestic supercomputing projects such as the 70-petaFLOP Jean Zay upgrade lock in early anchor customers, while tax credits under France 2030 lower TCO for AI hardware procurement.

5G and Fiber Network Rollout

Free Mobile operates 18,699 live 5G sites, enabling 94% population coverage and driving demand for GaN MMIC power amplifiers, RF switches and beamforming ICs. Orange’s standalone-5G plan for SMEs adds low-latency slices that rely on custom accelerator cards and fronthaul optics, spurring local assembly work at MACOM’s Nantes facility. Concurrent fiber-to-the-home upgrades require coherent DSPs and photonic-integrated circuits that leverage France’s optoelectronics heritage.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Engineering-talent shortage | -1.10% | France, with EU-wide implications | Short term (≤ 2 years) |

| Global supply-chain volatility | -0.70% | Global, affecting France operations | Medium term (2-4 years) |

| High industrial energy prices | -0.90% | France manufacturing centers | Short term (≤ 2 years) |

| Limited sub-7 nm domestic fab capacity | -0.50% | France, broader EU context | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

Engineering-Talent Shortage

Vacancies for lithography, process-integration and EDA specialists outpace graduates, prompting STMicroelectronics to launch dual-degree apprenticeships with Grenoble INP while SEMI’s Chips Skills Academy rolls out micro-credential courses. Smaller design houses struggle to match salary packages offered by cloud providers, elongating project schedules and increasing reliance on overseas contractors.

High Industrial Energy Prices

Average industrial-power tariffs climbed to EUR 199 /MWh in 2023, doubling fab utilities bills and squeezing gross margins even as ASPs eroded in commodity logic ICs. Firms lock in multi-year green-power PPAs; STMicroelectronics targets 100% renewable electricity before 2027, aiming to cap variable costs and meet client carbon scorecards.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Device Type: Integrated Circuits Anchor Leadership

Integrated Circuits delivered 46.20% of the France semiconductor market revenue in 2024, underpinned by automotive MCU pull-through and data-center memory upticks. Analog power-management ICs enjoy premium pricing due to stricter vehicle efficiency rules, while digital signal processors ride 5G base-station densification. The France semiconductor market size for Sensors and MEMS is primed to outpace overall demand, advancing at 7.59% CAGR as Lidar, tire-pressure monitoring and predictive-maintenance modules proliferate across transport and manufacturing lines. Steady orders in Discrete and Optoelectronic categories balance volume cyclicality, while niche diamond device prototypes target rail inverters with record 1,500 °C junction limits.

STMicroelectronics’ FD-SOI roadmap anchors domestic IC competitiveness; its 18 nm MCU series embeds phase-change xMemory that halves code-flash latency. Soitec’s Smart-Cut substrates solidify export receipts, giving fabless customers reliable wafers amid global shortages. Despite the lack of a local sub-7 nm logic fab, France leverages mature-node expertise to integrate complex power, RF and sensor dies inside advanced packages, mitigating reliance on leading-edge lithography and sustaining value capture within national borders.

By Business Model: IDM Scale Meets Fabless Agility

IDMs controlled 67.31% of 2024 revenue because automotive and industrial clients prize single-vendor accountability and longevity guarantees. STMicroelectronics and X-Fab Lyon combine design, front-end and back-end, delivering BIST-enabled ASICs with 20-year lifecycle support. Nevertheless, the fabless cohort is expanding at 7.11% CAGR thanks to venture-backed design houses such as SiPearl and Kalray, which tap TSMC and Samsung for 5 nm or 4 nm shuttles. The France semiconductor market share held by fabless firms is expected to widen as RISC-V accelerators, neuromorphic chips and domain-specific AI engines favour lightweight asset structures.

Hybrid variants are also emerging substrate supplier Soitec licenses IP and codesigns reference flows with partners, blurring lines between foundry, IDM and fabless roles. Public policy supports both models manufacturing subsidies lower capex for IDMs, while R&D tax credits and Bpifrance seed rounds fuel fabless IP creation. Such dual support helps hedge systemic risk and ensures every innovation stage retains some domestic footprint.

By End-User Industry: Automotive Leads, AI Gains Pace

Automotive consumed 31.40% of France semiconductor market demand in 2024, reflecting rising semiconductor content per vehicle from powertrain electrification, ADAS and zonal-architecture migrations. Battery-electric models now embed more than USD 1,000 worth of semiconductors, double the 2020 figure, and local Tier 1s favour French suppliers to shore up traceability. The France semiconductor market size for AI compute is climbing fastest, clocking an 8.01% CAGR through 2030 as sovereign-cloud providers deploy liquid-cooled GPU pods and universities spin up exascale research clusters.

Telecom infrastructure remains the second-largest draw, absorbing GaN RF power amplifiers, baseband SoCs and coherent optics for nationwide 5G and fiber rollouts. Industrial-automation lines upgrade PLCs and machine-vision cameras under France Relance incentives, lifting demand for ruggedized MCUs and time-of-flight sensors. Defense and space procurements, protected under national-security carve-outs, channel steady volumes to radiation-hardened IC suppliers located in Occitanie and Nouvelle-Aquitaine.

Geography Analysis

France dominates regional demand owing to its USD 3 trillion economy and robust policy framework backing semiconductor self-reliance. Greater Grenoble, home to CEA-LETI, Soitec and a lattice of 70+ fab-adjacent SMEs, concentrates one-third of national fab employment. The France semiconductor market benefits from proximity to Alpine hydro-power and skilled engineering graduates, sustaining competitive cost-per-wafer metrics even as energy tariffs fluctuate. Paris-Saclay specializes in AI architectures and EDA software, feeding a virtuous cycle between cloud-service buyers and chip-design innovators.

Cross-border linkages under the nine-nation Semicon Coalition allow joint procurement of chemicals and shared pilot lines at IMEC-France, diffusing capex risk and standardizing qualification flows. Franco-German powertrain alliances accelerate SiC device characterization on both sides of the Rhine, while Dutch lithography OEMs station field engineers at Crolles to support 0.33 NA EUV tool upgrades. Such cooperation raises collective bargaining power against overseas raw-material suppliers and secures larger EU-wide lots for critical consumables.

Internationally, French research institutes partner with Vietnamese, South Korean and Canadian fabs to co-develop photonics, HBM and cryogenic-CMOS IP blocks, extending value chains without exporting core know-how. Export-credit guarantees, and a revamped €200 million sovereign-patent fund facilitate outbound licensing, ensuring that high-margin IP streams flow back into domestic R&D budgets. Geographic resilience thus stems from a balanced blend of local manufacturing scale, EU diversification and global co-innovation.[4]EE Times Europe, “STMicroelectronics Picks 18-nm FD-SOI for Next-Gen MCUs,” eetimes.eu

Competitive Landscape

The France semiconductor market hosts a balanced field where the top five companies collectively hold roughly 58% revenue, signifying moderate concentration. STMicroelectronics retains pole position via its breadth of automotive, industrial and power-discrete offerings and by expanding its Crolles fab from 130 k to 200 k wafer starts per month. Soitec commands a near-monopoly in FD-SOI and RF-SOI substrates, achieving 70% global share in 2025 shipments. Fabless hopeful SiPearl targets exascale CPU sockets, while Kalray and Edgehog focus on PCIe acceleration cards for cloud-to-edge AI inference.

Strategic moves highlight specialization over scale. Soitec and Powerchip Semiconductor Manufacturing Company co-developed ultra-thin transistor-layer-transfer (TLT) stacks that trim die-to-wafer bonding defects by 30%, preparing the ground for chiplet-based radar modules. Thales, Radiall and Foxconn tabled a EUR 250 million OSAT proposal to secure local advanced-packaging capacity for defense and automotive customers, lowering logistic risk and enabling ITAR-free export variants. Diamfab closed a grant to pilot CVD diamond wafers, betting on the rail and grid-storage boom.

Restructuring is equally pivotal. STMicroelectronics plans up to 1,000 voluntary departures in France but offsets the exodus with 1,200 new roles focused on SiC epitaxy, spin-transfer-torque MRAM and 8-inch GaN lines. X-Fab consolidates MEMS back-end in Corbeil-Essonne to unlock 15% opex savings and funnel proceeds into 200 mm Si-on-Insulator trench-MOSFET upgrades. Venture investment remains abundant; SEMCO Technologies’ oversubscribed IPO raised EUR 225.7 million earmarked for e-chuck and atomic-layer-etch tool expansion.

France Semiconductor Industry Leaders

STMicroelectronics N.V.

Soitec S.A.

Teledyne e2v Semiconductors SAS

Sequans Communications S.A.

Kalray S.A.

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- July 2025: SiPearl raised EUR 130 million Series A funding to accelerate Rhea-1 AI processor industrialization

- July 2025: SEMCO Technologies completed an oversubscribed IPO on Euronext Growth Paris, attracting EUR 225.7 million in demand

- June 2025: Soitec partnered with PSMC to deploy ultra-thin TLT technology for 3D chip stacking

- May 2025: Thales, Radiall and Foxconn opened talks on a EUR 250 million OSAT facility slated for 100 million SiP units annually

France Semiconductor Market Report Scope

| Discrete Semiconductors | Diodes | ||

| Transistors | |||

| Power Transistors | |||

| Rectifier and Thyristor | |||

| Other Discrete Devices | |||

| Optoelectronics | Light-Emitting Diodes (LEDs) | ||

| Laser Diodes | |||

| Image Sensors | |||

| Optocouplers | |||

| Other Device Types | |||

| Sensors and MEMS | Pressure | ||

| Magnetic Field | |||

| Actuators | |||

| Acceleration and Yaw Rate | |||

| Temperature and Others | |||

| Integrated Circuits | By Integrated Circuit Type | Analog | |

| Micro | Microprocessors (MPU) | ||

| Microcontrollers (MCU) | |||

| Digital Signal Processors | |||

| Logic | |||

| Memory | |||

| By Technology Node (Shipment Volume Not Applicable) | Less than 3nm | ||

| 3nm | |||

| 5nm | |||

| 7nm | |||

| 16nm | |||

| 28nm | |||

| 28nm | |||

| Integrated Device Manufacturer (IDM) |

| Design / Fabless Vendor |

| Automotive |

| Communication (Wired and Wireless) |

| Consumer |

| Industrial |

| Computing / Data Storage |

| Data Center |

| AI |

| Government (Aerospace and Defense) |

| By Device Type (Shipment Volume for Device Type is Complementary) | Discrete Semiconductors | Diodes | ||

| Transistors | ||||

| Power Transistors | ||||

| Rectifier and Thyristor | ||||

| Other Discrete Devices | ||||

| Optoelectronics | Light-Emitting Diodes (LEDs) | |||

| Laser Diodes | ||||

| Image Sensors | ||||

| Optocouplers | ||||

| Other Device Types | ||||

| Sensors and MEMS | Pressure | |||

| Magnetic Field | ||||

| Actuators | ||||

| Acceleration and Yaw Rate | ||||

| Temperature and Others | ||||

| Integrated Circuits | By Integrated Circuit Type | Analog | ||

| Micro | Microprocessors (MPU) | |||

| Microcontrollers (MCU) | ||||

| Digital Signal Processors | ||||

| Logic | ||||

| Memory | ||||

| By Technology Node (Shipment Volume Not Applicable) | Less than 3nm | |||

| 3nm | ||||

| 5nm | ||||

| 7nm | ||||

| 16nm | ||||

| 28nm | ||||

| 28nm | ||||

| By Business Model | Integrated Device Manufacturer (IDM) | |||

| Design / Fabless Vendor | ||||

| By End-user Industry | Automotive | |||

| Communication (Wired and Wireless) | ||||

| Consumer | ||||

| Industrial | ||||

| Computing / Data Storage | ||||

| Data Center | ||||

| AI | ||||

| Government (Aerospace and Defense) | ||||

Key Questions Answered in the Report

What is the current value of the France semiconductor market?

It reached USD 7.73 billion in 2025 and is forecast to grow to USD 9.72 billion by 2030.

How fast is automotive electrification increasing semiconductor demand in France?

Automotive applications held 31.40% of 2024 revenue, and SiC power-device orders linked to EV programs continue to climb.

Which segment shows the highest growth through 2030?

AI compute hardware is advancing at an 8.01% CAGR, outpacing all other end-user segments.

Why are Sensors & MEMS important for future growth?

They carry a 7.59% CAGR thanks to ADAS, industrial IoT and consumer-device integration.

How does the EU Chips Act support French companies?

It provides direct grants, advanced-packaging funds and workforce-training mandates that collectively add roughly 1.2 percentage points to the forecast CAGR.

What are the main challenges facing French semiconductor makers?

Talent shortages, energy-price volatility, supply-chain disruptions and the lack of domestic sub-7 nm capacity are the key headwinds.

How does Singapore differ from regional peers?

Singapore specializes in advanced packaging, R&D, and high-value test, while nearby Malaysia and Thailand focus on cost-effective volume assembly.

Page last updated on: