Brazil Semiconductor Market Size and Share

Market Overview

| Study Period | 2019 - 2030 |

|---|---|

| Forecast Data Period | 2025 - 2030 |

| Historical Data Period | 2019 - 2023 |

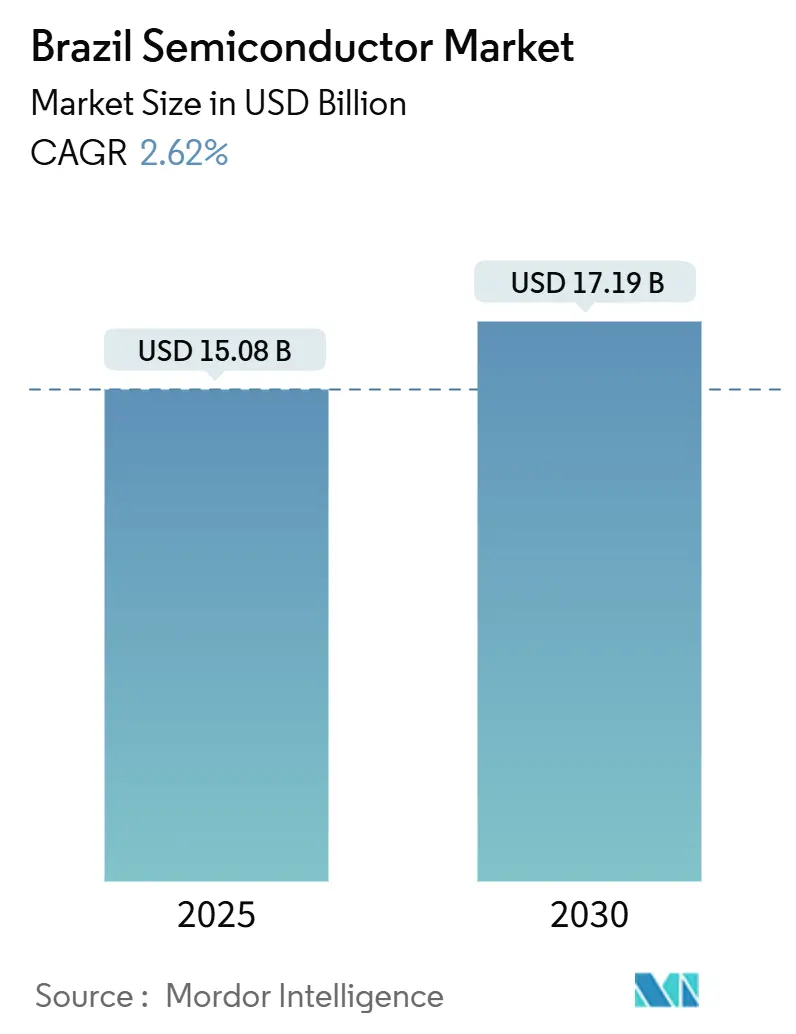

| Market Size (2025) | USD 15.08 Billion |

| Market Size (2030) | USD 17.19 Billion |

| Growth Rate (2025 - 2030) | 2.62% CAGR |

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

Brazil Semiconductor Market Analysis by Mordor Intelligence

The Brazil semiconductor market size stood at USD 15.08 billion in 2025 and is forecast to reach USD 17.19 billion by 2030, advancing at a 2.62% CAGR during the period. Growth reflects the government’s continued fiscal incentives, expanding automotive-electronics demand, and large-scale 5G roll-outs that jointly anchor production scale-up and design activity. Integrated circuits for vehicle electrification and telecom back-haul dominate current demand, while emerging sensor and data-center requirements open new value pools. Government funding under Nova Indústria Brasil and the annual BRL 7 billion Brazil Semicon Act has reduced capital risk for both domestic IDMs and overseas entrants, encouraging local assembly, packaging, and test capacity. Foreign-exchange volatility, unresolved PADIS renewal beyond 2028, and the lack of sub-28 nm fabs still temper medium-term capex momentum, yet rare-earth resource leverage and supply-chain friend-shoring keep the long-range outlook constructive.

Key Report Takeaways

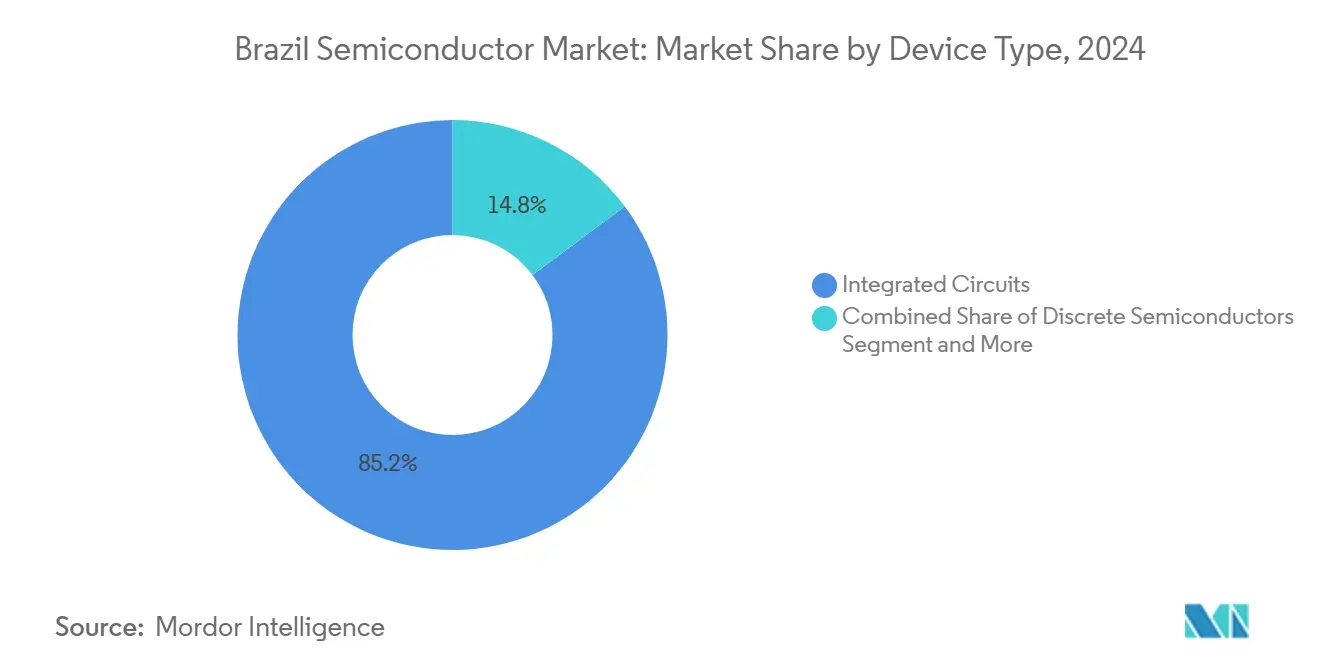

- By device type, integrated circuits captured 85.22% of Brazil's semiconductor market share in 2024; sensors and MEMS are projected to expand at a 4.3% CAGR through 2030.

- By business model, the IDM segment held 61.3% share of the Brazil semiconductor market size in 2024, while design/fabless vendors are forecast to register a 4.1% CAGR to 2030.

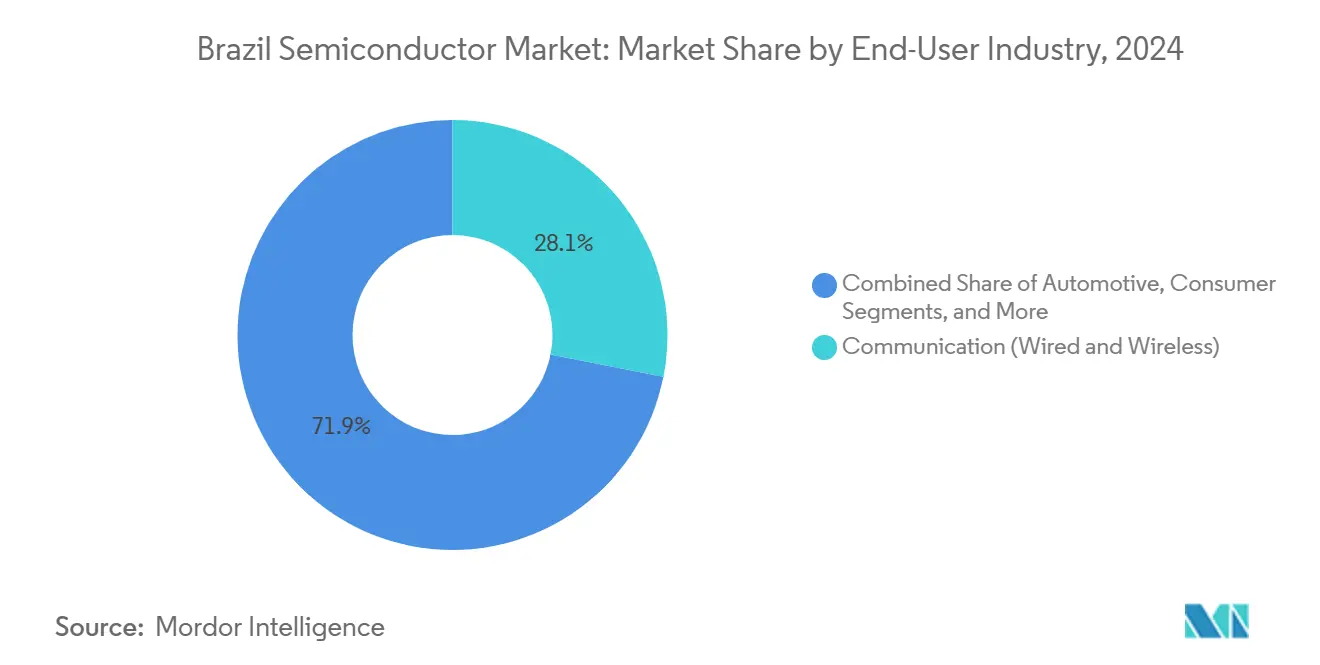

- By end-user industry, communication applications accounted for 28.11% of the Brazil semiconductor market size in 2024, and data-center applications are advancing at a 4.5% CAGR through 2030.

- HT Micron, Ceitec, and Padtec jointly controlled 12% of 2024 revenue, underscoring a fragmented structure that allows emerging fabless houses to scale quickly within government-sponsored R&D clusters.

Brazil Semiconductor Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| PADIS and Lei da Informática tax-credit extensions | +0.8% | National – most projects in São Paulo and Rio Grande do Sul | Medium term (2-4 years) |

| Domestic automotive-electronics demand (EVs and ADAS) | +0.6% | National – early traction in São Paulo, Minas Gerais, Rio de Janeiro | Medium term (2-4 years) |

| 5G and fiber-to-home roll-outs | +0.5% | National – priority in state capitals | Short term (≤ 2 years) |

| Memory back-end reshoring amid US-China frictions | +0.4% | Manaus and São Paulo industrial zones | Long term (≥ 4 years) |

| Rare-earth magnet pilots for SiC power devices | +0.3% | Minas Gerais and Goiás mining belts | Long term (≥ 4 years) |

| RISC-V adoption via CI-Innovator | +0.2% | Academic networks in São Paulo and Rio de Janeiro | Medium term (2-4 years) |

| Source: Mordor Intelligence | |||

Government PADIS and Lei da Informática Tax-Credit Extensions

Continuity of PADIS import-duty waivers and the complementary Lei da Informática income-tax offsets remains pivotal for capital outlays into new assembly lines and pilot fabs. Since 2020, these incentives have attracted more than USD 2.5 billion in semiconductor projects, including Zilia Technologies’ fast-tracked USD 120 million encapsulation upgrade that secured benefits before the 2028 sunset. [1]BNamericas, “What’s behind Zilia’s US$120mn Brazil semiconductors investment?” bnamericas.com The Nova Indústria Brasil facility adds BRL 300 billion in soft-loan firepower through 2026, lowering entry hurdles for local design houses converting to small-batch production. Yet uncertainty over a post-2028 framework keeps large multinationals cautious, with internal modelling showing cost uplifts near 18% if the scheme lapses. This policy overhang drives lobbying for a rolling five-year renewal mechanism to anchor long-horizon depreciation schedules.

Acceleration of Domestic Automotive-Electronics Demand (EVs and ADAS)

Electric-vehicle sales doubled in 2024 to 177,360 units, prompting BYD, Great Wall, and GAC to localize traction inverter and battery-management assembly lines inside new car plants. These facilities require silicon-carbide MOSFETs, gate drivers, and robust microcontrollers certified for −40 °C to 150 °C operation. The 35% import tariff on fully built EVs, effective July 2026, further inflates local-content mandates, steering Tier-1 suppliers to on-shore power module packaging. Automotive-grade semiconductor lots benefit from the automotive Rota 2030 program that refunds up to 10.2% of incremental R&D spending, directly linking chip innovation with CO₂-fleet targets. Ancillary ADAS roll-outs—radar, lidar, and camera fusion—boost demand for 32-bit MCUs and edge AI accelerators tailored to congested-city driving scenarios. [2]KrASIA, “Chinese automakers rush to beat Brazil’s EV tariffs,” kr-asia.com

5G and Fiber-to-Home Roll-Outs Boosting RF and Optical IC Uptake

Brazil covered 1,025 municipalities with 5G by 2025, serving 47.2 million subscribers and completing 73% of scheduled macro-cell sites. Each new site integrates high-band RF power amplifiers, beam-forming ICs, and low-noise transceivers optimized for the 3.5 GHz band. Nokia’s ReefShark-enabled refresh at TIM Brasil alone consumes several million mid-band RF front-end modules, illustrating near-term pull-through. Parallel fiber-to-home projects add optical transceiver demand as Brisanet extends 61,000 km of cable in underserved Northeast corridors. The BRL 47 billion spectrum auction earmarked the bulk of proceeds for infrastructure, effectively underwriting semiconductor uptake in both wireless and fixed networks.

RISC-V Open-Hardware Adoption Led by the CI-Innovator Program

Brazil achieved Premier Member status in RISC-V International in 2024 and has since embedded open-instruction set coursework in 22 universities. The CI-Innovator grant targets 4,000 new chip-design engineers by 2030, giving fabless startups royalty-free processor IP to tailor AI, IoT, and automotive safety MCUs. Cost avoidance relative to proprietary cores averages USD 4 million per design tape-out, accelerating breakeven for venture-backed firms. Early commercial proof comes from Renesas, which released RISC-V embedded controllers that Brazilian ODMs can now license locally. The government positions the architecture as a route to digital sovereignty while keeping export-control constraints minimal.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Absence of sub-28 nm front-end fabs in-country | -0.7% | National, affecting advanced technology access | Long term (≥ 4 years) |

| FX volatility inflating imported wafer costs | -0.5% | National, impacting all semiconductor manufacturers | Short term (≤ 2 years) |

| IC-design talent gap below 16 nm node | -0.4% | National, concentrated in São Paulo and Rio de Janeiro tech hubs | Medium term (2-4 years) |

| Uncertain continuity of PADIS incentives beyond 2028 | -0.3% | National, affecting investment decisions | Medium term (2-4 years) |

| Source: Mordor Intelligence | |||

Absence of Sub-28 nm Front-End Fabs In-Country

Brazil’s process-technology ceiling remains 65/90 nm for logic and 130 nm for analog, compelling companies to outsource advanced wafers to Asia. This dependence raises logistics lead-times and exposes purchasers to export-control licensing. Capital outlays for a 12-inch EUV-capable fab exceed USD 20 billion, a figure that dwarfs current incentive pools. Consequently, domestic players confine efforts to power discretes, mixed-signal ASICs, and SiC substrates that can be processed on 150/200 mm lines. The capability gap widens as AI inference chips and 5G mmWave arrays migrate to 7 nm and below, forcing high-value IP to leave Brazil during fabrication and raising data-security concerns. [3]BusinessToday, “Can 28 nm catapult India to semiconductor manufacturing leadership?” businesstoday.in

FX Volatility Inflating Imported Wafer Costs

The Brazilian real swung more than 16% against the U.S. dollar between 2024 and 2025, complicating bill-of-materials budgeting for wafer starts and deposition chemicals priced in foreign currency. Local fabs hedge exposure through short-term non-deliverable forwards, but smaller design houses cannot sustain the premium. Central-bank SELIC rate hikes to 14.75% elevate working-capital charges, prompting inventory contraction that increases the risk of line-down scenarios. Although the Ex-Tarifário regime temporarily waives import duties on capital items, its annual renewal cycle injects planning uncertainty. Without a broader currency-risk pooling mechanism, margin volatility will restrain aggressive price-performance moves, especially in commodity MCU and discrete lines.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Device Type: Integrated Circuits Dominate Amid Emerging Sensor Upside

Integrated circuits generated 85.22% of 2024 revenue, underscoring their foundational role in data-path processing across telecom and vehicle electrification. This dominance positions the segment as the prime contributor to Brazil's semiconductor market growth over the forecast window. Power-efficient microcontrollers, baseband SoCs, and driver ICs supplied by IDMs such as HT Micron benefit from localized assembly lines that capture PADIS tax credits. Discrete semiconductors retain stable utility in traction inverters and grid-tie converters, yet lack comparable margin expansion. Optoelectronics profit from 5G fronthaul and dense fiber back-haul that consume high-bit-rate optical transceivers.

Sensors and MEMS expand at a 4.3% CAGR, the fastest pace across device classes. Factory-automation projects deploy pressure and vibration sensors to optimize predictive maintenance, while automotive OEMs integrate MEMS gyroscopes into ADAS safety stacks. Brazil's semiconductor market size for sensors is forecast to reach USD 1.12 billion by 2030, helped by domestic rare-earth availability that eases permanent-magnet sourcing for magnetic-field sensors. Packaging advances toward wafer-level chip-scale packages improve shock resistance, positioning local OSATs for value capture.

By Business Model: IDM Leadership Faces Fabless Momentum

IDM players represented 61.3% of 2024 sales as they control vertically integrated lines in testing, burn-in, and reliability qualification—capabilities prized by automotive and telecom buyers. Their scale delivers procurement leverage for imported wafers, partially buffering FX shocks. Consequently, the IDM slice maintains dominant Brazil semiconductor market share through 2030 even as fabless challengers rise.

Fabless and design-only houses grow at a 4.1% CAGR, propelled by university incubators that provide EDA access and shuttle runs to Asian foundries. Government grants cover up to 80% of first-silicon costs for nationally aligned projects, allowing rapid prototyping of RISC-V-based controllers. The Brazil semiconductor market size accruing to fabless firms is poised to top USD 3.2 billion by 2030 as they target AI edge-nodes, industrial IoT, and secure payment modules. Multiple tape-out hubs in Campinas and Porto Alegre accelerate the concept-to-mask cycle, gradually eroding IDM share in mid-volume specialty ASICs.

By End-User Industry: Communication Leads, Data Centers Accelerate

Communication infrastructure supplied 28.11% of the 2024 demand, validating the capital intensity of nationwide 5G and fiber expansion. Operators Claro, TIM, and Vivo consume RF, optical, and network-processor silicon in multi-year volume contracts that anchor fab cycle planning. This installed base underpins recurring upgrade revenue, sustaining the communication share of the Brazil semiconductor market size above USD 4.6 billion through the outlook period.

Hyperscale data centers post the fastest 4.5% CAGR as cloud providers build regional availability zones to satisfy data-residency rules. Rising inference workloads trigger high-core-count CPU and GPU orders alongside DDR5 memory, and CXL interconnect switch ASICs. The Brazil semiconductor market share captured by data-center silicon suppliers is forecast to rise from 6% in 2024 to 9% in 2030, translating into USD 1.55 billion incremental revenue. Automotive, industrial automation, and government aerospace projects each maintain steady double-digit percentage contributions, diversifying end-market risk for suppliers.

Geography Analysis

The Southeast corridor—anchored by São Paulo and Rio de Janeiro—accounts for almost two-thirds of the Brazil semiconductor market due to dense automotive, telecom, and financial-services clusters that absorb high-value IC content. São Paulo alone hosts more than 45 design houses and OSAT facilities that leverage proximity to the Viracopos cargo hub for wafer logistics. Rio Grande do Sul adds MEMS innovation fueled by university R&D grants, while Minas Gerais supplies critical rare-earth feedstock that supports magnet and SiC substrate initiatives.

The North hosts the Manaus Free Trade Zone, whose duty-free framework drives smartphone, set-top box, and memory-module assembly. Realme’s new line producing 28,000 units daily exemplifies how consumer-electronics OEMs enter to exploit tax holidays, indirectly stimulating discrete and PMIC demand upstream. Northeast states progress swiftly on submarine-cable landings that necessitate optical amplifiers and network ASICs, with Meta’s Project Waterworth elevating Fortaleza and Belém to global traffic hubs.

Central-West Goiás emerges as a strategic materials node following Serra Verde’s 2024 rare-earth commissioning; downstream magnet pilot plants could enable localized power-module manufacturing. Federal policy steers complementary talent programs to smaller cities to distribute economic gains, suggesting a gradual dispersion of the Brazil semiconductor market beyond entrenched southern states over the next decade.

Competitive Landscape

Brazil’s supplier base remains fragmented—top five vendors combined held roughly 32% of 2024 revenue—yielding abundant whitespace for niche specialists. IDMs such as HT Micron and CEITEC differentiate through AEC-Q100-qualified products essential for domestic EV lines, while Padtec leverages system-level expertise to pull through optical components into carrier accounts. Zilia Technologies’ BRZ 650 million expansion underlines how incentive timelines drive capex pacing.

Fabless entrants concentrate on RISC-V MCUs and FPGA-accelerated edge AI, using overseas foundries for 22/28 nm wafers and domestic OSATs for flip-chip packaging. Mbochip’s export push following B3’s injection demonstrates the scalability of design-first models when tied to capital markets funding. [4]Pipeline, “Após aporte da B3, Mbochip avança no exterior,” pipelinevalor.globo.com

Strategic collaborations between global equipment vendors and local academia—e.g., ASML-USP lithography fellowship—aim to upskill engineers for future sub-28 nm ambitions. Competitive focus will intensify around automotive power modules, SiC substrate preparation, and hybrid bonding packaging lines as OEMs demand higher energy efficiency and thermal performance.

Brazil Semiconductor Industry Leaders

SMART Modular Technologies Brasil Ltda.

HT Micron Semicondutores S.A.

Ceitec S.A.

Unitec Semicondutores S.A.

Padtec S.A.

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- July 2025: Meta committed BRZ 347 billion to Project Waterworth, a 50,000 km submarine cable linking South America, Europe, and Africa, lifting demand for ultra-high-capacity optical semiconductors.

- July 2025: Zilia Technologies finalized a BRZ 650 million capacity expansion across Atibaia and Manaus, adding memory and industrial-storage product lines.

- June 2025: The federal government shortlisted 56 strategic mineral projects and unlocked BRZ 5 billion, prioritizing rare-earth extraction for semiconductor inputs.

- April 2025: Brazil and Vietnam set up a Joint Committee on semiconductors with a target of training 50,000 ICT specialists through a bilateral center.

- April 2025: Adata and Giga Computing agreed to co-build server production sites in Brazil, cutting reliance on imported assemblies.

- March 2025: A BRZ 5 billion national quantum-computing roadmap earmarked BRZ 3 billion for fab infrastructure and skills by 2029.

Brazil Semiconductor Market Report Scope

| Discrete Semiconductors | Diodes | ||

| Transistors | |||

| Power Transistors | |||

| Rectifier and Thyristor | |||

| Other Discrete Devices | |||

| Optoelectronics | Light-Emitting Diodes (LEDs) | ||

| Laser Diodes | |||

| Image Sensors | |||

| Optocouplers | |||

| Other Device Types | |||

| Sensors and MEMS | Pressure | ||

| Magnetic Field | |||

| Actuators | |||

| Acceleration and Yaw Rate | |||

| Temperature and Others | |||

| Integrated Circuits | By IC Type | Analog | |

| Micro | Microprocessors (MPU) | ||

| Microcontrollers (MCU) | |||

| Digital Signal Processors | |||

| Logic | |||

| Memory | |||

| By Technology Node (Shipment Volume Not Applicable) | < 3 nm | ||

| 3 nm | |||

| 5 nm | |||

| 7 nm | |||

| 16 nm | |||

| 28 nm | |||

| > 28 nm | |||

| IDM |

| Design/Fabless Vendor |

| Automotive |

| Communication (Wired and Wireless) |

| Consumer |

| Industrial |

| Computing/Data Storage |

| Data Centre |

| Artificial Intelligence |

| Government (Aerospace and Defence) |

| Other End-user Industries |

| By Device Type (Shipment Volume for Device Type is Complementary) | Discrete Semiconductors | Diodes | ||

| Transistors | ||||

| Power Transistors | ||||

| Rectifier and Thyristor | ||||

| Other Discrete Devices | ||||

| Optoelectronics | Light-Emitting Diodes (LEDs) | |||

| Laser Diodes | ||||

| Image Sensors | ||||

| Optocouplers | ||||

| Other Device Types | ||||

| Sensors and MEMS | Pressure | |||

| Magnetic Field | ||||

| Actuators | ||||

| Acceleration and Yaw Rate | ||||

| Temperature and Others | ||||

| Integrated Circuits | By IC Type | Analog | ||

| Micro | Microprocessors (MPU) | |||

| Microcontrollers (MCU) | ||||

| Digital Signal Processors | ||||

| Logic | ||||

| Memory | ||||

| By Technology Node (Shipment Volume Not Applicable) | < 3 nm | |||

| 3 nm | ||||

| 5 nm | ||||

| 7 nm | ||||

| 16 nm | ||||

| 28 nm | ||||

| > 28 nm | ||||

| By Business Model | IDM | |||

| Design/Fabless Vendor | ||||

| By End-user Industry | Automotive | |||

| Communication (Wired and Wireless) | ||||

| Consumer | ||||

| Industrial | ||||

| Computing/Data Storage | ||||

| Data Centre | ||||

| Artificial Intelligence | ||||

| Government (Aerospace and Defence) | ||||

| Other End-user Industries | ||||

Key Questions Answered in the Report

How large is the Brazil semiconductor market in 2025 and what growth is expected?

The market is valued at USD 15.08 billion in 2025 and is projected to reach USD 17.19 billion by 2030, reflecting a 2.62% CAGR.

Which device category generates the most revenue today?

Integrated circuits dominate with 85.22% share, fueled by telecom and automotive demand.

What segment is growing fastest through 2030?

Data-center applications lead with a 4.5% CAGR as hyperscale cloud operators expand regional capacity.

How important are government incentives to investors?

PADIS and Lei da Informática tax programs currently offset up to 18% of operating costs, making them pivotal to near-term capex decisions.

Does Brazil possess critical raw materials for chips?

Yes, the country holds the world’s second-largest rare-earth reserves and is piloting magnet supply chains that support SiC power-device production.

Page last updated on: