Mexico IT Services Market Size and Share

Market Overview

| Study Period | 2019 - 2030 |

|---|---|

| Forecast Data Period | 2025 - 2030 |

| Historical Data Period | 2019 - 2023 |

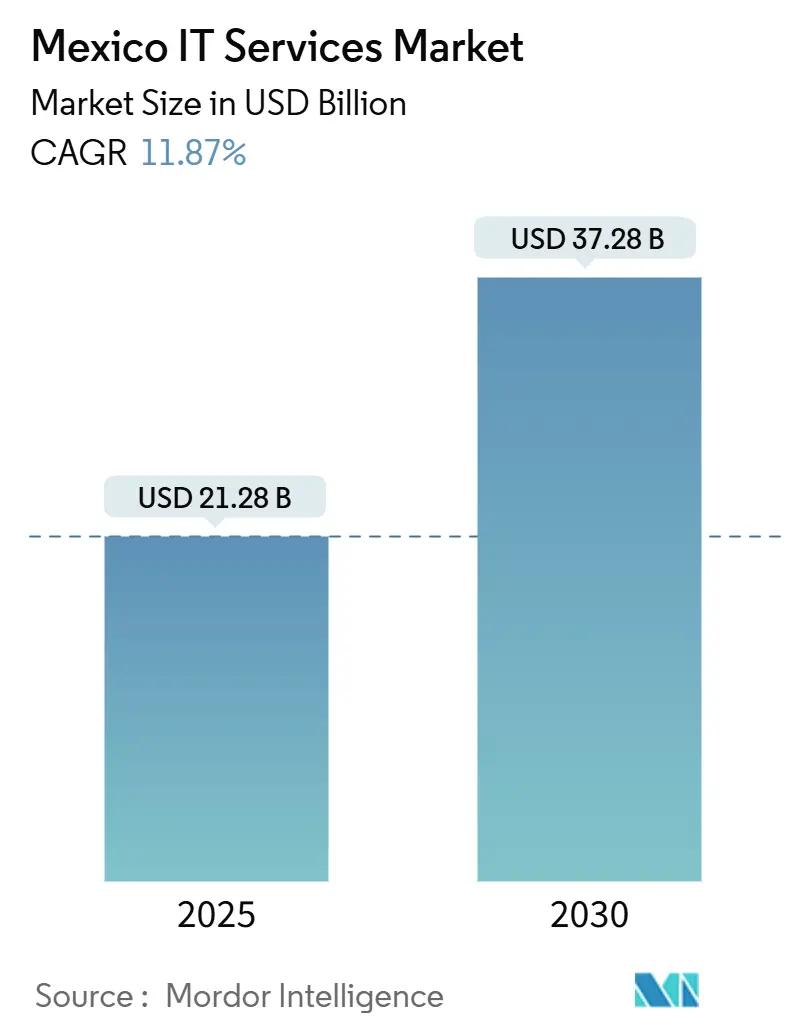

| Market Size (2025) | USD 21.28 Billion |

| Market Size (2030) | USD 37.28 Billion |

| Growth Rate (2025 - 2030) | 11.87% CAGR |

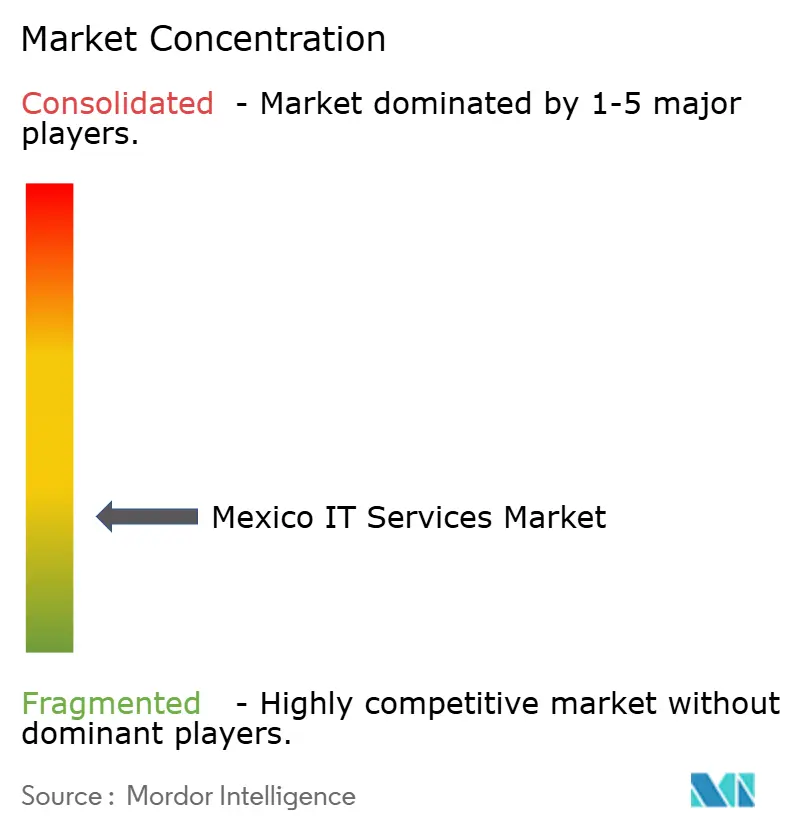

| Market Concentration | Low |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

Mexico IT Services Market Analysis by Mordor Intelligence

The Mexico IT Services market size stands at USD 21.28 billion in 2025 and is projected to climb to USD 37.28 billion by 2030, registering an 11.87% CAGR over the forecast period. This upward trajectory is underpinned by strong nearshoring demand, sustained cloud CAPEX, and targeted government digital policies. Multinational investments in hyperscale infrastructure, combined with a 300,000-job boost linked to Microsoft’s Querétaro region, illustrate how foreign direct investment is redefining domestic service capabilities.[1]BNamericas Editorial Team, “Microsoft launches its first hyperscale cloud datacenter region in Mexico,” BNamericas, bnamericas.com Competitive differentiation rests on cloud-first strategies, managed security depth, and localized delivery models that compress project lead times by as much as 30% relative to distant offshore alternatives. Simultaneously, mandatory CFDI 4.0 e-invoicing and the National AI Agenda accelerate enterprise digitalization, positioning providers that offer compliance consulting and AI integration to capture incremental wallet share. Nevertheless, cyber-talent shortages and federal budget tightening restrain short-term momentum, requiring vendors to rebalance pricing and recruitment tactics to maintain margins.

Key Report Takeaways

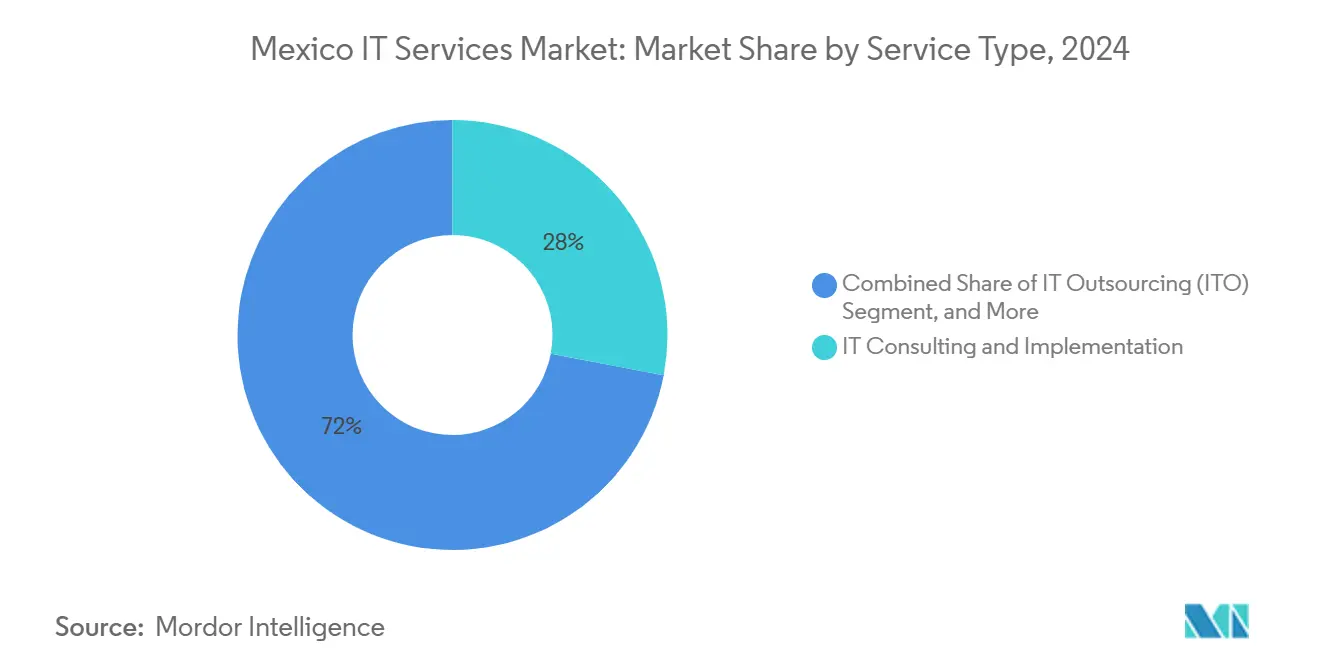

- By service type, IT consulting and implementation led with a 28% Mexico IT Services market share in 2024, while cloud and platform services are set to expand at a 14.21% CAGR through 2030.

- By enterprise size, large enterprises commanded 66% of the Mexico IT Services market size in 2024; SMEs represent the fastest-growing cohort with a 14.90% CAGR through 2030.

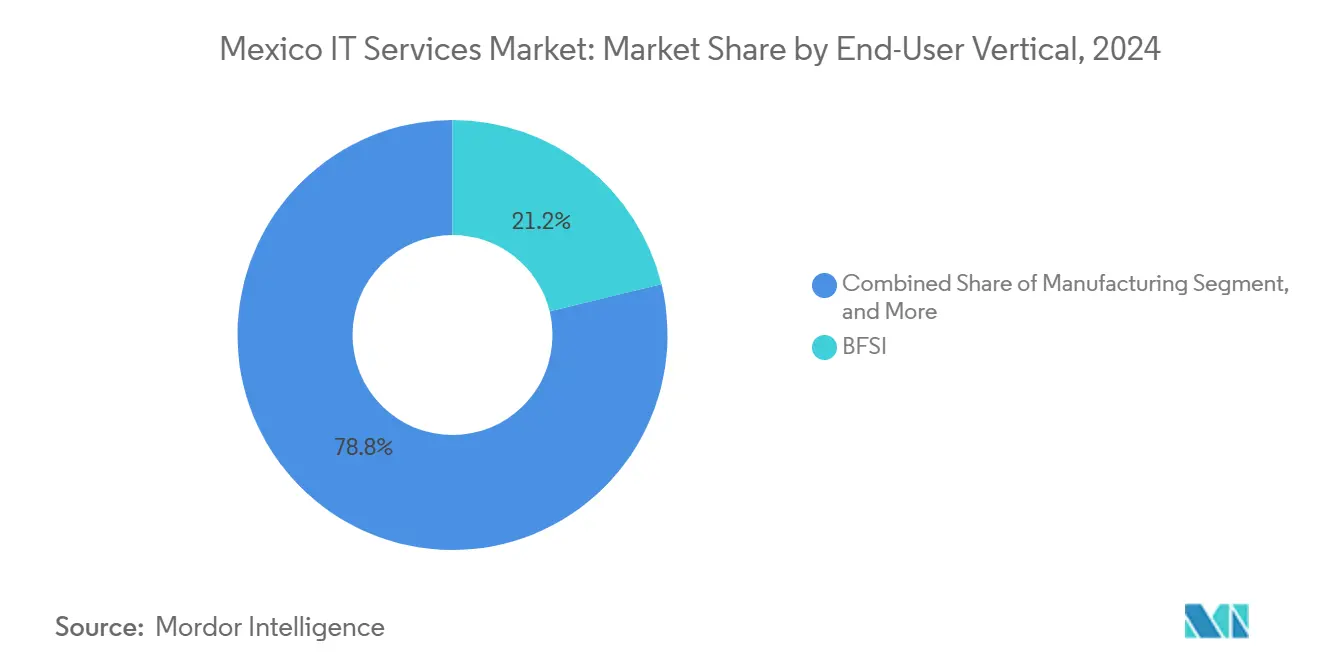

- By end-user vertical, BFSI held 21.2% of the Mexico IT Services market share in 2024, whereas healthcare and life sciences are forecast to advance at a 15.33% CAGR to 2030.

- By delivery model, on-site services captured 55% of the Mexico IT Services market size in 2024, and near-shore or hybrid delivery is poised for a 15.61% CAGR through 2030.

Mexico IT Services Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Soaring near-shoring demand from US enterprises | +2.80% | National, with concentrations in Guadalajara, Mexico City, Monterrey | Medium term (2-4 years) |

| Accelerated cloud/datacenter CAPEX (Microsoft, KIO, Equinix) | +2.10% | National, with primary hubs in Querétaro, Mexico City | Short term (≤ 2 years) |

| National Digital Transformation and AI Agenda 2025-2030 | +1.90% | National, with government sector focus | Long term (≥ 4 years) |

| Mandatory e-invoicing (CFDI 4.0) adoption | +1.40% | National, affecting all business sectors | Short term (≤ 2 years) |

| SME digital-payments penetration via CoDi and SPEI rails | +1.20% | National, with rural expansion potential | Medium term (2-4 years) |

| Emergence of 5G private networks for Industry 4.0 | +1.00% | Manufacturing corridors, automotive clusters | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

Soaring Near-shoring Demand from US Enterprises

Elevated geopolitical tension in Asia and supply chain resilience mandates have pushed US corporates to rebalance delivery footprints toward Mexico. Nearshoring commitments are projected to unlock USD 46 billion in new capital inflows over five years, potentially lifting GDP growth from 1.9% to 3%.[2]Schneider National Insights, “Mexico is poised for GDP growth from nearshoring,” Schneider, schneider.com Proximity provides synchronized working hours that reduce sprint cycle delays by up to 30%, while travel times of under four hours support agile governance. Tech Mahindra, HCLTech, and SLK Software have collectively announced more than 3,000 new technical hires through 2025, validating confidence in the Mexico IT Services market. The resulting pipeline of transformation programs ranges from supply-chain visibility dashboards to bilingual customer-experience deployments that leverage Mexico’s 197,000 full-time IT professionals. Providers pairing domain expertise with Spanish English fluency are therefore well placed to win multiyear statements of work.

Accelerated Cloud and Datacenter CAPEX

Microsoft’s USD 1.1 billion hyperscale region in Querétaro is forecast to add MXN 3.8 trillion to national output by 2030 through ecosystem multiplier effects. Equinix’s Azure ExpressRoute rollout and KIO Networks’ 40-site upgrade program together lift carrier-neutral capacity and provide low-latency access for hybrid workloads. Datacenter floor space is expected to expand fivefold by 2028, steering companies toward cloud migration roadmaps that bundle re-platforming, DevSecOps, and AI model hosting. Ninety percent of surveyed Mexican firms already employ AI in operations, and 66% intend to raise IT budgets in 2025, confirming robust demand for advisory and managed services attached to the Mexico IT Services market.

National Digital Transformation and AI Agenda 2025-2030

The Digital Transformation Agency (ATDT) centralizes data governance and promotes interoperability across federal entities, creating a USD 1.1 billion public-sector IT spend pool in 2025.[3]AI Regula Solutions Analysts, “The Digital Transformation Agency in Mexico,” AI Regula Solutions, airegulasolutions.com Mexico holds 95% of Latin America’s AI patents and ranks sixth globally by research talent, giving providers an indigenous knowledge base to support algorithm tuning and policy alignment. The agenda mandates cybersecurity frameworks and open-data standards, so vendors fluent in zero-trust architecture and compliance mapping stand to gain recurring revenue streams. Long-term opportunities converge around identity management, AI-driven citizen services, and analytics centers of excellence that can be exported across Latin America.

Mandatory CFDI 4.0 E-invoicing Adoption

CFDI 4.0 generated 10.3 billion e-invoices in 2023 alone, forcing businesses to retrofit ERP and tax compliance engines. Penalties that start at MXN 17,020 per erroneous invoice elevate urgency, particularly among SMEs that still rely on spreadsheets. Service providers specializing in integration with authorized certification bodies (PACs) now enjoy a captive audience for cloud-based accounting and workflow automation packages. Parallel demand for data-analytics dashboards has emerged, as reconciled invoice data can improve working-capital decisions and supplier negotiations.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Cyber-talent shortage and 35% wage inflation | -1.80% | National, acute in Mexico City, Guadalajara | Medium term (2-4 years) |

| Federal IT procurement budget contraction (-1.6% YoY) | -1.10% | Government sector, national impact | Short term (≤ 2 years) |

| Rising cybersecurity-incident insurance premiums | -0.70% | Enterprise sector, major metropolitan areas | Medium term (2-4 years) |

| High last-mile fiber costs outside Tier-1 cities | -0.60% | Rural and secondary urban markets | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

Cyber-talent Shortage and 35% Wage Inflation

Sixty-three percent of CIOs report chronic difficulty sourcing security architects, pushing wages up by 35% in the capital region. Senior cyber roles now command salaries above MXN 600,000, eroding the labour-cost arbitrage that underpins many fixed-price managed-services contracts. Mexico logged 31 million cyberattack attempts in 2024, equalling 55% of Latin America’s total. Demand far outstrips supply in cloud security, AI model assurance, and OT protection, forcing vendors to accelerate training academies and regional talent rotation schemes. Without structural talent pipelines, the Mexico IT Services market could miss high-margin project opportunities.

Federal IT Procurement Budget Contraction (-1.6% YoY)

The 2025 national budget trims IT allocations by 1.6% even as public agencies face a projected 260% jump in cyber threats. Projects tied to citizen-facing portals and AI pilots risk slippage, reducing near-term contract flow for system integrators. Firms must pivot toward outcome-based pricing and partner financing to sustain government pipelines until fiscal space improves. Private-sector activity offers partial relief, yet vendors relying heavily on federal programs may encounter utilization dips.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Service Type: Consulting Dominates While Cloud Surges

IT consulting and implementation captured 28% of the Mexico IT Services market share in 2024, buoyed by demand for ERP upgrades, AI roadmaps, and CFDI 4.0 compliance projects. The segment’s billing rates benefit from scarce bilingual architects who bridge global frameworks with local tax nuances. In contrast, cloud and platform services are forecast to post a 14.21% CAGR, leveraging Microsoft’s regional launch and Equinix interconnect fabric that cuts latency below 5 milliseconds for central Mexico clients. The Mexico IT Services market size tied to cloud projects is predicted to expand from USD 4.8 billion in 2025 to USD 9.5 billion by 2030.

Managed security services receive budget prioritization as attack volumes rise, producing double-digit revenue growth across SOC-as-a-service offerings. Conversely, traditional IT outsourcing shows flat growth as customers migrate toward agile pods and outcome-linked contracts, though BPO workstreams that bundle CX automation continue to secure nearshoring inflows.

By Enterprise Size: SME Digitalization Accelerates

Large enterprises still anchor 66% of 2024 spending, but SME outlays are rising faster, aided by pay-as-you-go cloud stacks and fintech-driven credit access. The Mexico IT Services market size attributed to SMEs is projected to jump from USD 7.1 billion in 2025 to USD 14.1 billion by 2030, reflecting 14.90% CAGR. Multicloud reference architectures packaged for five-seat to fifty-seat deployments lower entry barriers. Solution providers that embed regulatory compliance templates into off-the-shelf bundles win rapid traction among retailers and micro-manufacturers adjusting to e-invoicing rules.

By End-User Vertical: Healthcare Outpaces BFSI

BFSI led with 21.2% of 2024 revenue as banks raced to digitize onboarding and AML analytics. Adoption proves sticky; Banorte’s productivity gains exceeded 50% after migrating to Google Cloud. Yet healthcare and life sciences exhibit the steepest runway, expected to compound at 15.33% annually to 2030. Telemedicine volume remains high post-pandemic, and EHR implementations supported by government interoperability mandates anchor multi-year engagements. The Mexico IT Services market share for healthcare is poised to climb from 8% in 2025 to nearly 12% by 2030.

By Delivery Model: Hybrid Nearshore Gains Steam

On-site delivery accounted for 55% of 2024 spend, sustained by banking and public-sector regulatory needs. Still, nearshore-hybrid delivery is primed for a 15.61% CAGR as U.S. buyers re-route work from Asia to align time zones and soften geopolitical risk. Providers leveraging two-in-a-box governance (nearshore PM, onshore solution owner) report 20% faster defect resolution and 10-15% opex savings. Salary benchmarks reveal 50-70% savings versus U.S. equivalents, ensuring hybrid’s long-term stickiness within the Mexico IT Services market.

Geography Analysis

Mexico City, Guadalajara, and Monterrey collectively account for roughly 70% of national demand. Mexico City anchors federal and banking contracts, drawing global integrators such as Accenture and Deloitte. Guadalajara, branded the Silicon Valley of Mexico, houses Intel’s R&D hub and multiple Google-aligned centers established by Tech Mahindra, reinforcing its stature as a cloud-native talent pool. Monterrey’s manufacturing corridor hosts Blue Yonder’s 600-person AI facility, channelling Industry 4.0 requirements across auto and machinery clusters.

Emergent nodes include Querétaro, catalysed by Microsoft’s hyperscale site and Sparkle’s submarine cable backhaul that together reduce round-trip times to Dallas to under 25 milliseconds. Tijuana leverages border adjacency, capturing logistics and CX assignments from U.S. retailers. Secondary metros such as Puebla and León show rising demand, yet last-mile fibre costs constrain latency-sensitive workloads, delaying adoption of edge analytics and private 5G.

Cross-border synergies under USMCA keep service flows tariff-free, and investors pledge USD 40-50 billion annually toward nearshoring. This creates corridors of integrated supply and digital services along highways and rail links, positioning the Mexico IT Services market for sustained regional diversification so long as energy reliability and security frameworks keep pace.

Competitive Landscape

The landscape is moderately fragmented; the top five vendors hold under 35% combined share, limiting pricing power and fostering specialization. IBM, Accenture, and Deloitte secure high-complexity transformation deals through C-suite relationships, while TCS, Infosys, and HCLTech scale rapidly via cost-competitive nearshore centres in Guadalajara and Monterrey. Local champions Softtek and KIO Networks differentiate via Spanish-first delivery and government familiarity, capturing Tier-2 and public-sector projects.

Technology partnerships shape client perception: Wipro’s alliance with HPE strengthened hybrid-cloud credentials, earning Global Momentum GSI Partner of the Year recognition.[4]Hewlett Packard Enterprise Alliance Program, “HPE and Wipro partnership announcement,” HPE, hpe.com Microsoft’s 25% annual enterprise growth fuels a certification arms race, with partners racing to expand Azure benchmarks. Cybersecurity boutiques emerge as niche disruptors, offering zero-trust accelerators to fill gaps left by global MSSPs.

M&A activity intensifies: CoreX’s acquisition of Volteo Digital augments ServiceNow depth, while Concentrix’s Querétaro hub adds AI-powered CX capacity. Logistics giants like UPS buying Estafeta generate fresh system integration demand around warehouse and fleet digitization. As nearshore traction rises, new foreign entrants should be expected, heightening the competition for bilingual cloud architects and SOC analysts.

Mexico IT Services Industry Leaders

IBM de México, S. de R.L.

Servicios Administrados Softtek, S.A. de C.V.

Accenture, S. de R.L. de C.V.

Servicios KIO Networks, S.A.P.I. de C.V.

Tata Consultancy Services México, S.A. de C.V.

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- March 2025: Tech Mahindra expanded Google Cloud partnership, launching Guadalajara delivery centers for AI projects.

- February 2025: CoreX acquired Volteo Digital, adding 100+ ServiceNow consultants and a Guadalajara COE.

- February 2025: UPS bought Estafeta, signalling logistics consolidation linked to nearshoring.

- January 2025: Banorte launched Bineo, Mexico’s first fully digital bank, onboarding 10,000 clients in three months.

Mexico IT Services Market Report Scope

| IT Consulting and Implementation |

| IT Outsourcing (ITO) |

| Business Process Outsourcing (BPO) |

| Managed Security Services |

| Cloud and Platform Services |

| Small and Medium Enterprises (SMEs) |

| Large Enterprises |

| BFSI |

| Manufacturing |

| Government and Public Sector |

| Healthcare and Life-Sciences |

| Retail and Consumer Goods |

| Telecom and Media |

| Logistics and Transport |

| Energy and Utilities |

| Other End-User Verticals |

| On-site / Domestic Delivery |

| Near-shore / Hybrid |

| Offshore |

| By Service Type | IT Consulting and Implementation |

| IT Outsourcing (ITO) | |

| Business Process Outsourcing (BPO) | |

| Managed Security Services | |

| Cloud and Platform Services | |

| By End-User Enterprise Size | Small and Medium Enterprises (SMEs) |

| Large Enterprises | |

| By End-User Vertical | BFSI |

| Manufacturing | |

| Government and Public Sector | |

| Healthcare and Life-Sciences | |

| Retail and Consumer Goods | |

| Telecom and Media | |

| Logistics and Transport | |

| Energy and Utilities | |

| Other End-User Verticals | |

| By Delivery Model | On-site / Domestic Delivery |

| Near-shore / Hybrid | |

| Offshore |

Key Questions Answered in the Report

How large is the Mexico IT Services market in 2025 and what CAGR is expected?

The market totals USD 21.28 billion in 2025 and is projected to grow at an 11.87% CAGR to 2030.

Which service type grows fastest through 2030?

Cloud and platform services lead with a 14.21% CAGR as enterprises migrate workloads to new hyperscale regions.

Why are SMEs a key growth engine?

Regulatory e-invoicing, digital payments, and affordable cloud subscriptions drive a 14.90% CAGR for SME spending.

What vertical shows the strongest expansion?

Healthcare and life sciences record a 15.33% CAGR due to telemedicine and electronic health records adoption.

How do nearshore delivery models benefit U.S. clients?

Proximity reduces time-zone gaps, cuts travel costs, and compresses development cycles by up to 30% compared with offshore alternatives.

What is the main challenge facing providers?

A 35% surge in cybersecurity wages and a limited talent pool strain capacity and threaten margin sustainability.

Page last updated on: