South Africa IT Services Market Size and Share

Market Overview

| Study Period | 2019 - 2030 |

|---|---|

| Forecast Data Period | 2025 - 2030 |

| Historical Data Period | 2019 - 2023 |

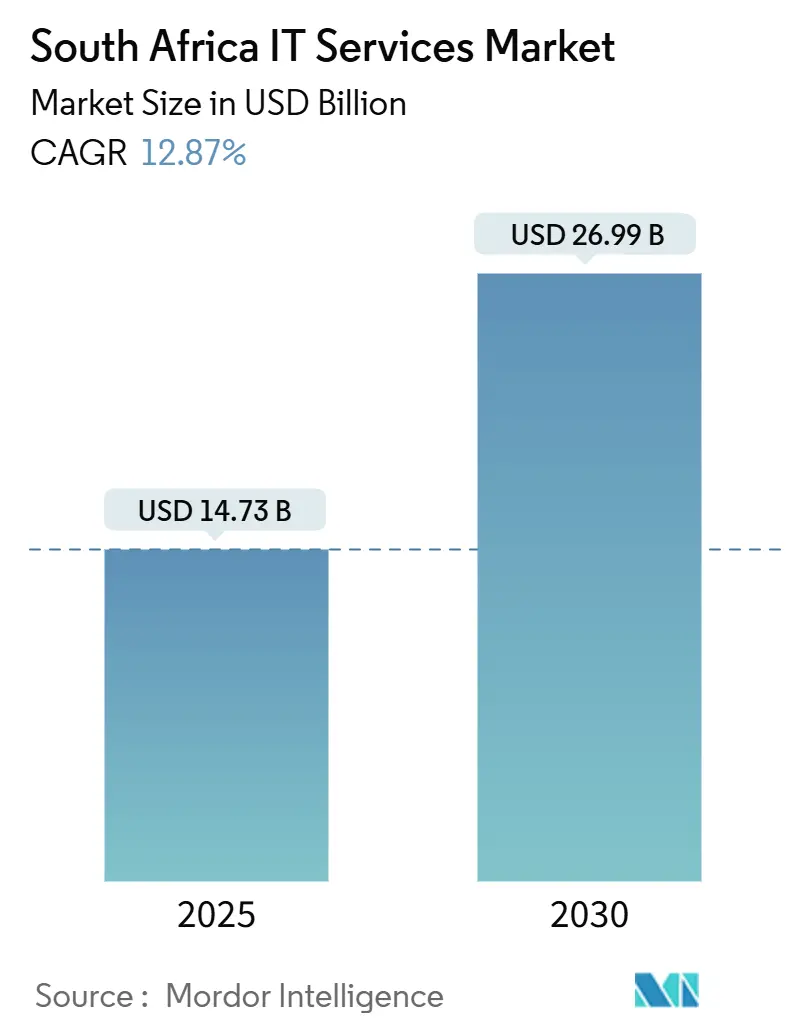

| Market Size (2025) | USD 14.73 Billion |

| Market Size (2030) | USD 26.99 Billion |

| Growth Rate (2025 - 2030) | 12.87% CAGR |

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

South Africa IT Services Market Analysis by Mordor Intelligence

The South Africa IT Services market size totaled USD 14.73 billion in 2025 and is projected to reach USD 26.99 billion by 2030, reflecting a 12.87% CAGR. Rapid broadband roll-out under the SA Connect program, sizeable hyperscale cloud investments from Google, AWS, Microsoft, and Huawei, and an upswing in enterprise cloud migration together underpin the market’s momentum. Rising cyber-risks have elevated spending on managed security services, while cost-competitive outsourcing rates—often 50-80% below U.S. benchmarks—continue to pull global ITO and BPO contracts into the country. [1]BPESA, “Driving Growth: BPESA’s Strategic Initiatives and Collaborations in 2024,” bpesa.org.za Although load-shedding and talent shortages temper growth, onshore and nearshore delivery resilience, favorable time-zone alignment, and widespread English proficiency sustain strong deal pipelines across financial services, healthcare, and mining-automation use cases.

Key Report Takeaways

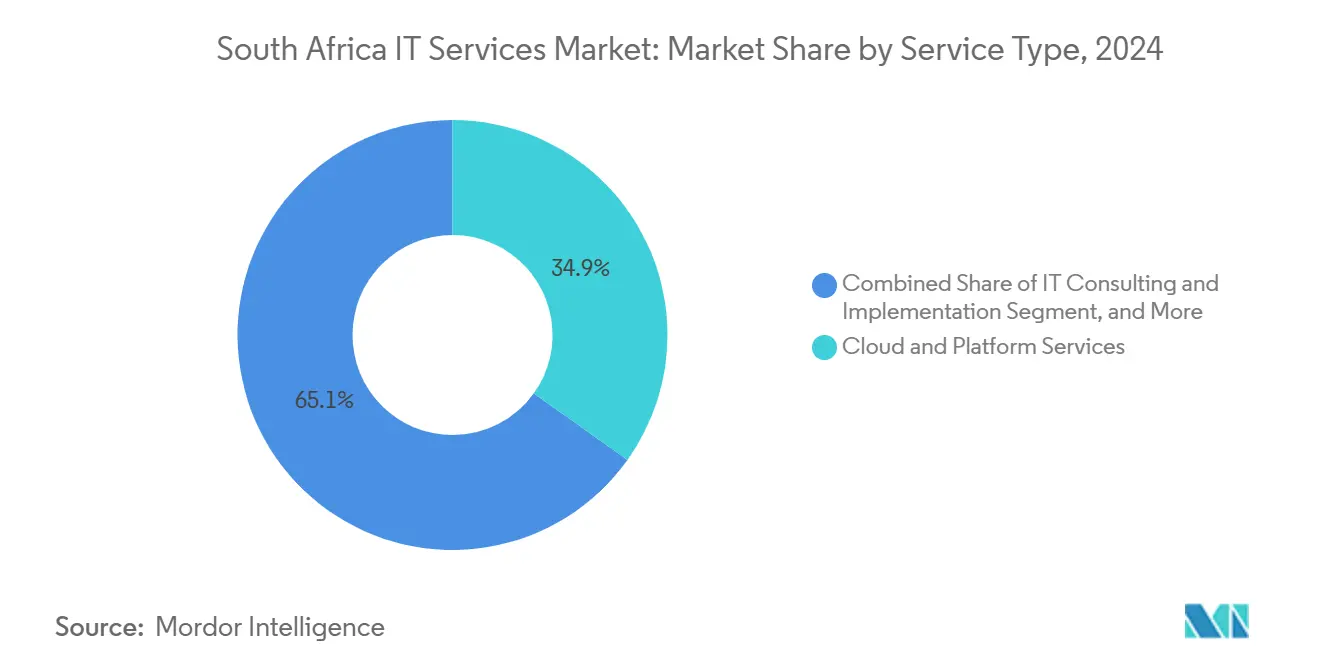

- By service type, Cloud and Platform Services led with 34.88% of South Africa's IT Services market share in 2024, while Managed Security Services posted a 14.2% CAGR through 2030.

- By end-user enterprise size, large enterprises held 67.41% of the South African IT Services market size in 2024; SMEs are expanding at a 13.8% CAGR to 2030.

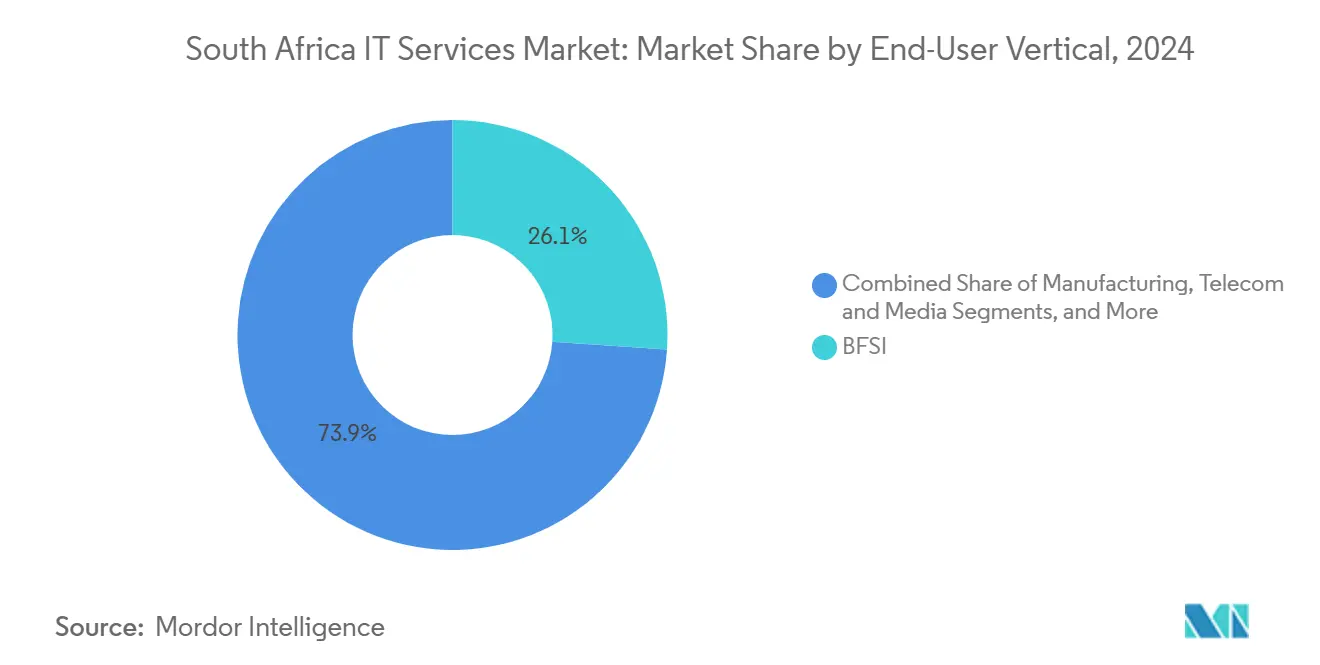

- By end-user vertical, the BFSI segment captured 26.08% share of the South Africa IT Services market size in 2024, whereas healthcare and life sciences are advancing at a 14.3% CAGR through 2030.

- By deployment model, onshore delivery accounted for 50.12% of South Africa's IT Services market share in 2024, yet offshore delivery is forecast to expand at 14.0% CAGR between 2025-2030.

South Africa IT Services Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Government "SA Connect" digital-infrastructure push | +2.1% | National, with early gains in Gauteng, Western Cape, KwaZulu-Natal | Medium term (2-4 years) |

| Enterprise cloud-migration wave | +3.2% | Global, concentrated in Johannesburg, Cape Town financial hubs | Short term (≤ 2 years) |

| Escalating cyber-threat environment | +2.8% | Global, with South Africa ranking 59th on global cyber attack index | Short term (≤ 2 years) |

| Cost-optimisation focus fuelling ITO/BPO demand | +1.9% | Global, with US and European clients targeting South African providers | Medium term (2-4 years) |

| Fintech-led core-banking modernisation surge | +2.3% | National, spilling over to broader African markets | Medium term (2-4 years) |

| Mining sector's edge-IT and automation rollout | +1.4% | National, concentrated in Gauteng, North West, Limpopo mining regions | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

Government “SA Connect” Digital Infrastructure Acceleration

Phase 2 of SA Connect intends to light up 32,055 community Wi-Fi hotspots and connect 5.5 million households by 2026, after linking 970 public facilities during Phase 1. These roll-outs create immediate systems integration and managed services engagements across rural districts. Provincial governments are bundling connectivity contracts with cybersecurity assessments, boosting consulting demand. Systems integrators see strong pipelines for edge routers, SD-WAN upgrades, and last-mile fiber civil-works supervision. Public-sector appetite for cloud-based productivity suites has also increased because connected schools and clinics now require secure collaboration platforms.

Enterprise Cloud Migration Imperative

Seventy-seven percent of large South African corporates have adopted cloud in some form, and the domestic cloud market is poised for a USD 6.3 billion value by 2030. Financial institutions spearhead adoption, evidenced by FirstRand’s choice of Fiserv’s Finxact core banking platform. [2]Financial IT, “FirstRand Group selects Fiserv to accelerate growth and innovation,” financialit.net Hybrid multicloud blueprints dominate RFPs as CIOs seek vendor diversification and sovereign-cloud controls. The surge fuels demand for lift-and-shift orchestration, cloud-native DevOps pipelines, and FinOps cost-governance services. Talent scarcity in Kubernetes, serverless architectures, and IaC tools is prompting providers to invest in local cloud academies.

Cybersecurity Threat Landscape Intensification

South Africa ranked 59th on the global cyber-attack index in 2024, with a Normalized Risk Index score of 42%. Large data breaches at retail chains and municipal utilities heightened executive awareness. Boards increasingly view security posture as a brand differentiator: 68% of enterprises surveyed treat cybersecurity investments as a competitive advantage. Demand for managed detection and response, SIEM optimization, and identity-as-a-service contracts has surged. Hyperscalers are adding sovereign-cloud controls to address POPIA requirements. Service providers with SOC presence in Johannesburg now bundle threat-hunting retainers, which command premium margins.

Cost Optimization Through Strategic Outsourcing

Global enterprises redirect work to South Africa due to 50-80% lower delivery costs than U.S. rates, while preserving cultural alignment and English fluency. In Q4 2023 alone, 4,569 new international BPO jobs were created. Telecom and banking contact-center wins from AT&T and Citibank highlight scale potential. Providers combine robotic process automation with human-in-the-loop governance to raise productivity. The GMT+2 time zone allows overlap with Europe and half-day coverage for North America, improving SLA adherence. Strategic investors are now financing new CX “mega-campuses” in Cape Town and Durban, integrating on-premises renewable power to mitigate load-shedding disruptions.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Load-shedding risk to data-centre uptime | -2.4% | National, with severe impact on Gauteng, Western Cape data centers | Short term (≤ 2 years) |

| Acute advanced-skills shortage | -1.8% | National, with international recruitment intensifying brain drain | Medium term (2-4 years) |

| Data-sovereignty anxiety limiting offshore delivery | -1.1% | National, affecting cross-border data processing under POPIA | Long term (≥ 4 years) |

| Rand volatility compressing IT budgets | -0.9% | National, with secondary effects on procurement cycles | Short term (≤ 2 years) |

| Source: Mordor Intelligence | |||

Load-Shedding Infrastructure Disruption

The grid recorded more than 200 load-shedding days in 2024, compelling data-center operators to procure diesel generators, battery storage, and on-site solar at elevated capital cost. [3]Data Centre Magazine, “South Africa calls for data centres to cut grid reliance,” datacentremagazine.com Although hyperscalers deploy N+1 redundancy, smaller co-location providers struggle with fuel price spikes. Government is fast-tracking wheeling agreements to let facilities buy renewable energy from independent power producers, yet interim instability raises SLAs and insurance premiums. Enterprises increasingly consider hybrid workloads, placing non-critical data in offshore regions while retaining latency-sensitive databases locally.

Critical Skills Shortage Intensification

Specialist vacancies in cloud architecture, DevSecOps, and data science persist despite university STEM output. International recruiters now advertise 2% of all South African tech vacancies as remote foreign roles, luring talent abroad with hard-currency salaries. Providers respond by establishing graduate academies and collaborating with coding-boot-camp operator HyperionDev, which secured ZAR 95 million in funding to scale training. Immigration reforms that prioritize critical-skills work visas could ease constraints, yet near-term wage inflation squeezes margins on fixed-price contracts.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Service Type: Cloud Platforms Anchor Digital Transformation

The South Africa IT Services market size for Cloud and Platform Services reached USD 5.14 billion in 2024 and accounted for 34.88% of the overall South Africa IT Services market share. Multi-region launches by Google and AWS stimulated system integrator pipelines across data migration, observability, and FinOps governance. Traditional hosting contracts are transitioning into Kubernetes-based managed platforms, lifting average contract values.

Providers differentiate by vertical clouds, BFSI-ready landing zones, health-data compliant vaults, or mining-edge templates bundling security and compliance accelerators. Managed Security Services, although a smaller base, is the fastest-growing line at 14.2% CAGR as boards elevate cyber-risk. IT Outsourcing now bundles SRE principles, while Business Process Outsourcing players embed generative AI to optimize call-center workflows.

By End-User Enterprise Size: SME Digitization Gains Pace

Large enterprises commanded 67.41% of the South African IT Services market size in 2024, reflecting complex multivendor estates within banking, telecom, and public utilities. They contract portfolio deals that span consulting, systems integration, and managed services, providing annuity revenue for tier-one vendors.

SMEs, while contributing only one-third of revenue, are scaling rapidly at 13.8% CAGR. Cloud SaaS suites, pay-as-you-go cybersecurity, and outsourced help desks lower adoption barriers. Government tax incentives for renewable energy allow SMEs to redirect capital toward IT modernization. Local MSPs craft bundles combining solar-storage leasing with virtual-desktop workspaces to mitigate power and productivity losses.

By End-User Vertical: Financial Services Leads, Healthcare Accelerates

The BFSI sector retained a 26.08% South Africa IT Services market share in 2024, supported by open-banking APIs, ISO 20022 payment modernization, and surging mobile adoption. Banks outsource AI-driven fraud prevention and digital-onboarding KYC workflows to service partners, driving multi-year advisory and managed contracts.

Healthcare and life sciences logged a 14.3% CAGR as hospitals embrace telemedicine platforms, AI-aided diagnostics, and e-pharmacy logistics. Providers partner with pharmaceutical traceability pilots such as IBM’s Pulse project to secure supply chains. Meanwhile, manufacturing digital twins and predictive maintenance adds Industry 4.0 workloads, sustaining demand for edge-compute and analytics at plants across Gauteng.

By Deployment Model: Onshore Trust Meets Offshore Efficiency

Onshore delivery represented 50.12% South Africa's IT Services market share in 2024, driven by POPIA compliance and client comfort with co-located teams. Local champions BCX and Altron capitalize on governmental preference for domestic vendors.

Offshore delivery, though smaller, is rising at 14.0% CAGR as global clients tap South African talent pools. BPO campuses integrate fiber redundancy and captive renewable power to ensure uptime. Nearshore delivery into SADC neighbors sees banks exporting mobile money core systems, with South African service firms providing managed-platform support.

Geography Analysis

Gauteng anchors the South Africa IT Services market with dense financial-services demand, Tier-IV data centers, and the Johannesburg Internet Exchange, which handles over 40% of domestic traffic. Western Cape contributes a vibrant tech startup ecosystem in Cape Town, hosting Google’s cloud region and multiple CX campuses that cater to European clients. KwaZulu-Natal leverages Durban’s port logistics to pilot blockchain-based trade-finance platforms, broadening application-modernization work.

The South Africa IT Services market size benefits from exports; almost 25% of managed service revenue originates from Europe and North America, where time-zone alignment supports agile ceremonies and 24/7 support rotations. [4]TDS Global Solutions, “South Africa Call Center Outsourcing & BPO Services,” tdsgs.com Providers open satellite hubs in Kenya, Nigeria, and Ghana to access tertiary talent, creating a nearshore mesh that strengthens continental deal credibility. The African Continental Free Trade Area framework simplifies the movement of specialists, encouraging cross-border staff augmentation engagements.

International expansion also includes Asia-Pacific: a new South Africa-China Trade and Investment Package pledges digital-economy cooperation, positioning Johannesburg as the regional headquarters for Chinese fintechs entering Africa. This dynamic feeds back into domestic demand for bilingual cloud support teams and SOC analysts versed in global compliance mandates.

Competitive Landscape

Market concentration is moderate, with the five largest players—BCX, NTT DATA, Altron Digital Business, IBM, and Accenture—collectively controlling just over 45% of South Africa's IT Services market share. BCX leverages Telkom parentage to win public-sector WAN and data-center contracts. NTT DATA’s rebrand from Dimension Data signals deeper alignment with global consulting and platform offerings.

Altron’s AI Community of Practice seeds cross-vertical proofs-of-concept; its EBITDA surged 49% in FY 2024, validating a pivot toward cloud, security, and data analytics. IBM bolsters sector depth through the acquisition of Oracle consultancy Applications Software Technology, extending public-sector reach.

Strategic alliances blossom between hyperscalers and integrators; Google co-develops sovereign-cloud blueprints with selected MSPs, while AWS collaborates with independent software vendors to localize fintech solutions. Vendors invest in data-center micro-grid projects to mitigate load-shedding, a differentiator in RFP scoring. Outcome-based pricing tied to uptime and business KPIs gains favor, reshaping contract risk-sharing models.

South Africa IT Services Industry Leaders

Dimension Data (Pty) Ltd.

BCX (Pty) Ltd.

EOH Holdings Ltd.

Altron TMT (Pty) Ltd.

Datacentrix (Pty) Ltd.

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- February 2025: FirstRand selected Fiserv’s Finxact core to accelerate product launch cycles.

- January 2025: Standard Bank partnered with Volante Technologies on a continent-wide Payments-as-a-Service initiative.

- January 2025: IBM agreed to acquire Applications Software Technology to grow its Oracle Cloud expertise.

- November 2024: Altron posted a 49% EBITDA rise on strong platform-segment performance.

- November 2024: IBM launched the Pulse pharma-tracing pilot to enhance medical-supply visibility.

South Africa IT Services Market Report Scope

| IT Consulting and Implementation |

| IT Outsourcing (ITO) |

| Business Process Outsourcing (BPO) |

| Managed Security Services |

| Cloud and Platform Services |

| Small and Medium Enterprises (SMEs) |

| Large Enterprises |

| BFSI |

| Manufacturing |

| Government and Public Sector |

| Healthcare and Life-Sciences |

| Retail and Consumer Goods |

| Telecom and Media |

| Logistics and Transport |

| Energy and Utilities |

| Other End-User Verticals |

| Onshore Delivery |

| Nearshore Delivery |

| Offshore Delivery |

| By Service Type | IT Consulting and Implementation |

| IT Outsourcing (ITO) | |

| Business Process Outsourcing (BPO) | |

| Managed Security Services | |

| Cloud and Platform Services | |

| By End-User Enterprise Size | Small and Medium Enterprises (SMEs) |

| Large Enterprises | |

| By End-User Vertical | BFSI |

| Manufacturing | |

| Government and Public Sector | |

| Healthcare and Life-Sciences | |

| Retail and Consumer Goods | |

| Telecom and Media | |

| Logistics and Transport | |

| Energy and Utilities | |

| Other End-User Verticals | |

| By Deployment Model | Onshore Delivery |

| Nearshore Delivery | |

| Offshore Delivery |

Key Questions Answered in the Report

What is the current value of the South Africa IT Services market?

The market was valued at USD 14.73 billion in 2025 and is expected to grow at a 12.87% CAGR to USD 26.99 billion by 2030.

Which service segment holds the largest share in South African IT services?

Cloud and Platform Services leads with 34.88% market share, fueled by hyperscaler data-center launches and enterprise cloud migration.

Why are global firms choosing South Africa for outsourcing?

Companies benefit from 50-80% cost savings, strong English proficiency, and GMT+2 time-zone overlap that supports real-time collaboration.

How is load-shedding affecting technology operations?

Frequent power cuts raise data-center operating costs and SLA risks, prompting investments in on-site renewables and hybrid workload architectures.

Which vertical is forecast to grow fastest through 2030?

Healthcare and life sciences is projected to expand at a 14.3% CAGR as providers adopt telemedicine, AI diagnostics, and e-pharmacy platforms.

Page last updated on: