Market Overview

| Study Period | 2019 - 2030 |

|---|---|

| Forecast Data Period | 2025 - 2030 |

| Historical Data Period | 2019 - 2023 |

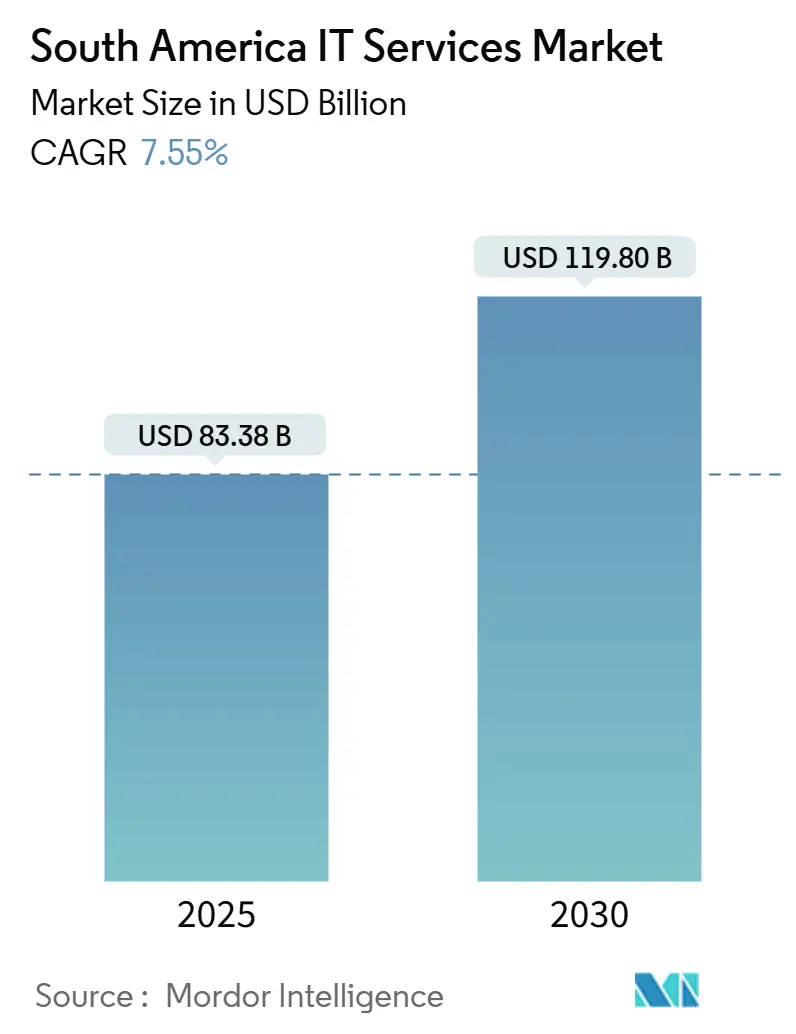

| Market Size (2025) | USD 83.38 Billion |

| Market Size (2030) | USD 119.80 Billion |

| Growth Rate (2025 - 2030) | 7.55% CAGR |

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

South America IT Services Market Analysis by Mordor Intelligence

The South America IT Services market size stood at USD 83.38 billion in 2025 and is forecast to reach USD 119.80 billion by 2030, expanding at a 7.55% CAGR. Nearshoring incentives, USD 6 billion-plus hyperscaler capital expenditure in the Santiago and São Paulo edge zones, and sovereign AI programs that exploit Spanish-Portuguese language automation keep demand buoyant. Sustained cloud migration programs at tier-1 banks, expanding cybersecurity budgets after a wave of 2023 breaches, and green-IT regulations that reward renewable-powered data centers collectively strengthen purchasing momentum. Providers able to align talent supply with fast-rising AI, cybersecurity, and hybrid-cloud workloads capture the largest opportunities while currency volatility and senior-architect shortages test operating margins.

Key Report Takeaways

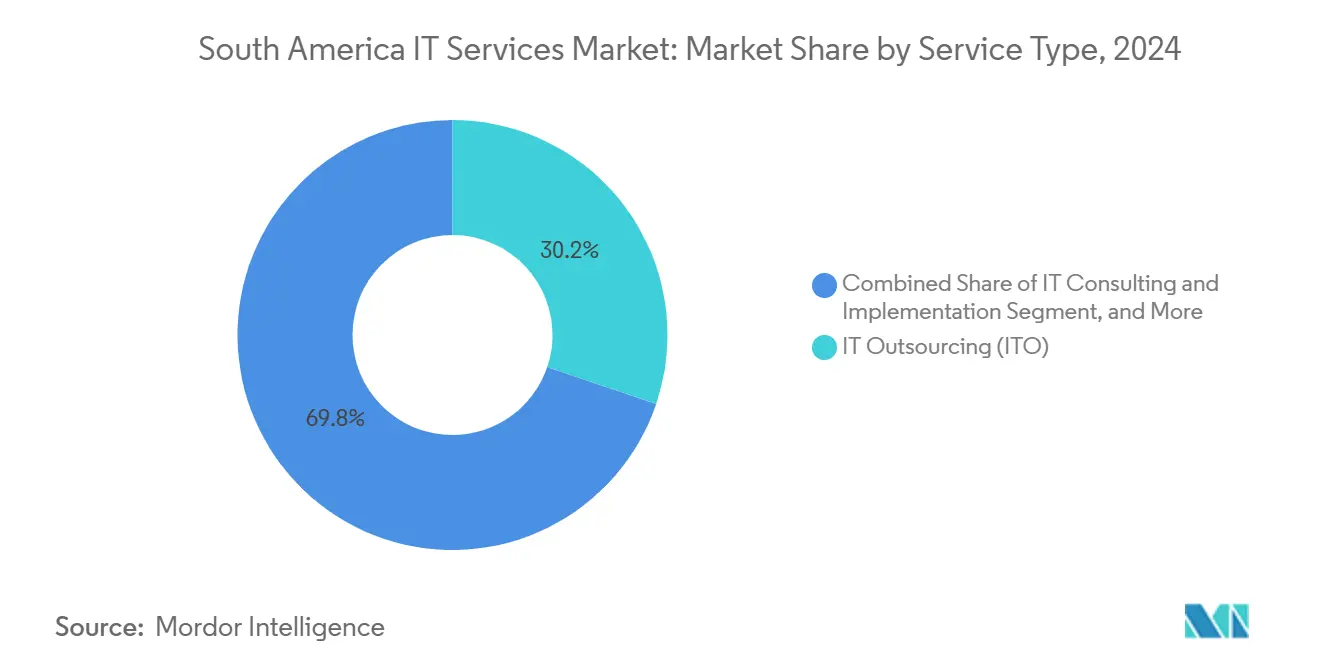

- By service type, IT Outsourcing led with 30.2% of the South America IT Services market share in 2024; Cloud and Platform Services are advancing at a 9.7% CAGR through 2030.

- By enterprise size, Large Enterprises accounted for 67.2% of the South America IT Services market size in 2024, while Small and Medium Enterprises are projected to grow at a 9.1% CAGR to 2030.

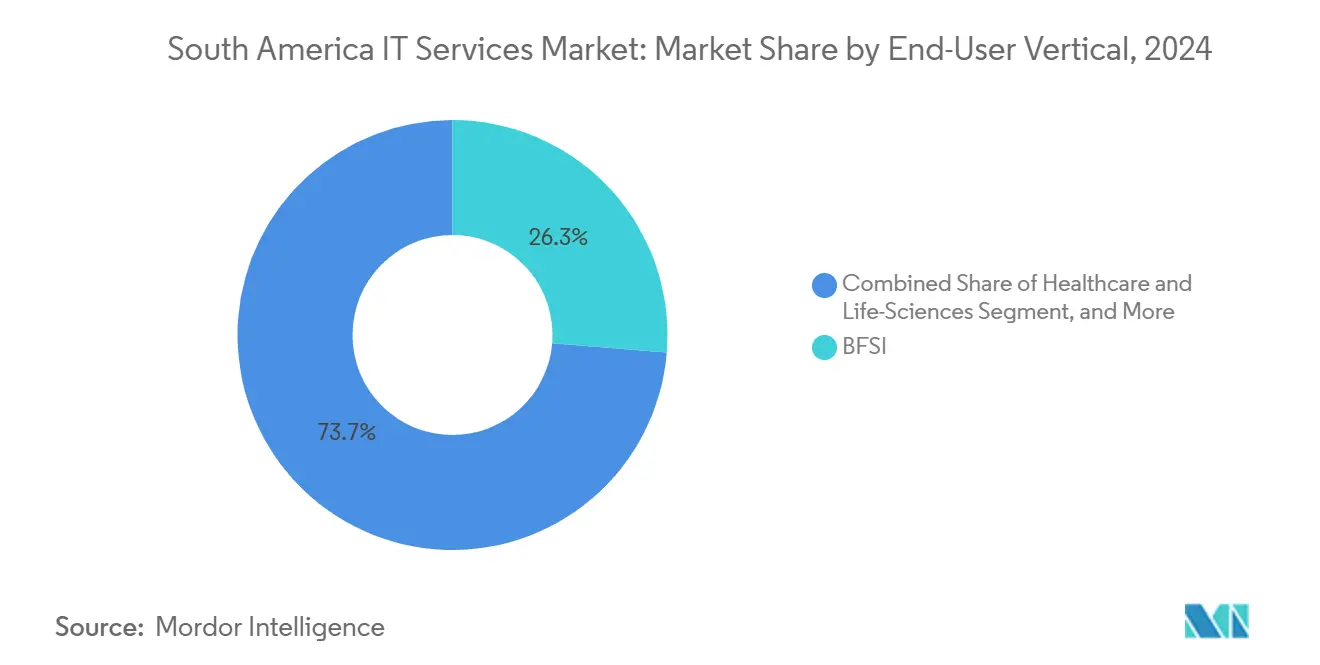

- By end-user vertical, the BFSI segment held 26.3% revenue share in 2024, whereas Healthcare and Life-Sciences are forecast to expand at a 10.5% CAGR between 2025-2030.

- By country, Brazil commanded 54.1% of the South America IT Services market share in 2024, and Colombia is expected to post the fastest growth at a 9.8% CAGR through 2030.

South America IT Services Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Near-shoring incentives and digital-talent programs | +1.2% | Brazil, with spillover to Argentina and Colombia | Medium term (2-4 years) |

| Cloud-first mandates by top-10 South American banks | +0.9% | Brazil, Chile, Colombia | Short term (≤ 2 years) |

| Accelerated cybersecurity spending after 2023 breaches | +0.8% | Region-wide, strongest in Brazil and Chile | Short term (≤ 2 years) |

| Hyperscaler CAPEX in Santiago and São Paulo edge zones | +0.7% | Brazil and Chile, benefits to Peru and Argentina | Medium term (2-4 years) |

| AI-led Spanish/Portuguese language CX automation | +0.6% | Brazil, Argentina, Colombia | Long term (≥ 4 years) |

| Green-IT regulations driving datacenter modernization | +0.3% | Brazil and Chile | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

Near-shoring Incentives and Digital-Talent Programs in Brazil

Brazil’s federal initiatives generate over 50,000 new IT graduates every year and underpin more than 90 tech parks nationwide. The country ranks fifth in the Kearney Global Services Location Index, thanks to cultural proximity and real-time overlap with U.S. clients. These advantages, coupled with a 500,000-strong developer pool, give Brazil enduring nearshoring appeal even as 5,000-10,000 high-skill vacancies stay unfilled due to northbound brain drain. Regional public-sector funds, including USD 200 million in StartUp Peru and Innovate Peru programs, export the model across neighboring economies while bolstering a workforce of 900,000 developers in the wider LatAm corridor.[1]BNamericas, “Banco Itaú planning to migrate 100% of its infrastructure to the cloud by 2028,” bnamericas.com

Cloud-First Mandates by Top-10 South American Banks

Banco Itaú plans to shift 100% of workloads to cloud platforms by 2028. Banco de Crédito del Perú committed USD 650 million to a Microsoft Azure-based overhaul scheduled for completion in 2026. While under 25% of core applications currently sit in cloud environments, leading institutions expect to lift that ratio above 60% within three years. Legacy-system lock-ins and regulatory scrutiny complicate the transition, sparking demand for specialized migration, security, and compliance services. Workforce-upskilling initiatives and AI-infused banking apps reinforce services pull-through across consulting, integration, and managed security specializations.

Accelerated Cybersecurity Spending after 2023 Breaches

Latin America logs roughly 1,600 cyberattacks every second, with attack frequency running 40% higher than global averages. Chile’s Cybersecurity Framework Law of 2024 created a National Cybersecurity Agency and formalized incident-reporting rules, making Chile an early adopter of region-wide regulation. Average regional breach costs rose 32% between 2022 and 2023, climbing to USD 4.45 million per event. TIVIT opened Latin America’s largest security operations center in São Paulo, reflecting rising managed-security demand, while a 28,000-person skills gap in Chile alone highlights the urgency for talent development.

Hyperscaler CAPEX in Santiago and São Paulo Edge Zones

Amazon earmarked USD 4 billion for a new Chile cloud region that will add three availability zones by 2026. Google pledged USD 850 million for Uruguay’s second hyperscale facility, and ongoing Brazilian projects have already drawn more than USD 4 billion, with São Paulo hosting 80% of national capacity. Combined with Microsoft and Scala Data Centers’ multi-gigawatt roadmaps, these outlays lift total Latin American data-center value from USD 5-6 billion in 2023 to an anticipated USD 8-10 billion by 2029. Higher local compute density multiplies opportunities for edge analytics, hybrid-cloud orchestration, and AI-as-a-service offerings.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Persistent regional macro volatility and FX risk | -1.1% | Argentina, Brazil; moderate in Colombia and Chile | Short term (≤ 2 years) |

| Shortage of senior cloud architects despite a large STEM base | -0.8% | Brazil, Argentina, Colombia | Medium term (2-4 years) |

| Delay in 5G spectrum auctions outside Brazil and Chile | -0.4% | Peru, Argentina, Colombia | Medium term (2-4 years) |

| High payroll-tax burden on near-shore delivery centers | -0.3% | Brazil, Argentina | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

Persistent Regional Macro Volatility and FX Risk

Currency instability deters foreign direct investment, with empirical studies confirming negative correlations between exchange-rate volatility and IT-services expansion. Argentina’s devaluation cycles exacerbate wage-pressure and talent-retention challenges, leaving thousands of roles vacant and inflating project timelines. OECD data show South American average tax-to-GDP ratios slipped from 21.5% in 2022 to 21.3% in 2023, reducing public-sector tech budgets.[2]OECD, “Estadísticas tributarias en América Latina y el Caribe 2025,” oecd.org Providers hedge exposures through multi-currency billing, diversified delivery locations, and contingency pricing, yet FX headwinds still shave margins and complicate multi-year contract valuation.

Shortage of Senior Cloud Architects Despite Large STEM Base

Chile alone falls short by 28,000 cybersecurity specialists, and similar deficits exist for cloud architects across Brazil and Colombia. Bloomberg reported 64% of public-sector managers cited analytics and programming shortages as major project risks. Wall Street Journal coverage underscored that Brazilian firms sometimes source Eastern European contractors to handle advanced workloads. While entry-level coders are plentiful, expertise in Kubernetes, DevSecOps, and AI architecture remains scarce, prolonging migrations and constraining provider capacity during peak demand cycles.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Service Type: Cloud Platforms Drive Digital Transformation

Cloud and Platform Services grow at a 9.7% CAGR through 2030, while IT Outsourcing retains a 30.2% share of the South America IT Services market size in 2024. Enterprises accelerating modernization programs move from lift-and-shift steps toward refactoring legacy workloads for multicloud environments. Providers bundle infrastructure, managed security, and FinOps disciplines to meet price-performance targets. Generative-AI pilots dominate 2025 statements of work as Spanish-Portuguese large-language models enhance contact-center automation. Managed Security Services experience double-digit pipeline expansion as ransomware defenses evolved beyond perimeter monitoring. Edge-computing demand rises in retail and telecom, requiring hybrid blueprints that blend on-premises latency management with public-cloud elasticity.

In the out-years, platform revenues exceed professional-services billings as consumption models replace fixed-fee milestones. Microsoft-aligned integrators open practice centers across Bogotá and Santiago to fast-track Azure landing zones. Kyndryl’s Latin American Center of Excellence illustrates the pivot by incumbents to consulting-plus-managed stacks. White-space persists in Spanish-Portuguese conversational AI, encouraging boutique providers to build proprietary corpora. Cloud and Platform Services, therefore, remain the anchor for sustainable expansion across the South America IT Services market.

By Enterprise Size: SMEs Accelerate Digital Adoption

Large Enterprises generated 67.2% of 2024 revenue, framing a strategy for global system integrators that pursue multi-tower contracts across cloud, cybersecurity, and data analytics. This cohort demands complex vendor-neutral solutions that comply with stringent data-sovereignty and uptime requirements. They also co-create AI governance frameworks to align with evolving Brazilian and Chilean AI bills. In contrast, Small and Medium Enterprises grow at a 9.1% CAGR to 2030, catalyzed by subscription-priced SaaS, simplified tax regimes, and digital-public-infrastructure rollouts in payments and identification. Providers gain scale by productizing support bundles and automating low-touch onboarding.

Cost-effective marketplace templates for e-commerce, accounting, and HR accelerate SME cloud adoption, narrowing capability gaps with larger peers. Fintech proliferation in Peru and Colombia pushes SMEs toward embedded-finance APIs, further expanding addressable workloads. The shift widens the customer pyramid, allowing mid-tier integrators to build volume around standardized managed-service catalogs. The resulting diffusion of demand safeguards the long-term resilience of the South America IT Services market.

By End-User Vertical: Healthcare Leads Growth Trajectory

Healthcare and Life-Sciences record a 10.5% CAGR through 2030, underpinned by telemedicine infrastructure grants and stricter digital-records compliance. Investments in hospital-edge clouds and AI-assisted diagnostics foster a growing pipeline for HIPAA-grade managed-hosting and integration services. BFSI, while retaining 26.3% share of 2024 spending, advances cloud-native core-bank conversions and open-banking APIs, generating sustained demand for legacy-migration and DevSecOps expertise. Manufacturing adopts Industry 4.0 edge analytics for predictive maintenance, whereas Government agencies pursue citizen-service portals and cybersecurity hardening after high-profile breaches.

Vertical diversification mitigates macro shocks. Retail deploys AI personalization engines to prolong wallet-share, Telecom accelerates 5G platform integration, and Energy utilities adopt IoT for grid balancing. Cross-sector pressure for demonstrable ESG metrics elevates demand for green-IT audits and renewable-power-aligned hosting. The intricate mosaic of vertical use-cases anchors multi-year revenue visibility for providers across the South America IT Services market.

Geography Analysis

Brazil owned 54.1% of the South America IT Services market share in 2024, propelled by 500,000 developers and more than USD 6 billion in hyperscaler deployments.

São Paulo alone concentrates 80% of Brazil’s data-center megawattage, giving providers localized low-latency options for multicloud orchestration. Colombia, registering a 9.8% CAGR through 2030, leverages 2024 spectrum concessions to seven licensees, fueling 5G rollout and next-gen service models. Advent International’s purchase of ERP-specialist Siesa affirms investor confidence in Colombia’s digital-economy trajectory.

Brazil sustains its leadership through deep talent pools, pro-investment regulations, and a robust partner ecosystem aligned to hyperscale roadmaps. Corporate cloud outlays, boosted by Banco Itaú’s full migration timetable, keep professional-services pipelines full. Local AI spend is forecast to top USD 2.4 billion in 2025, amplifying demand for data-engineering and model-ops talent.

Colombia’s double-digit trajectory stems from policy-backed infrastructure upgrades and the clustering of 13% of Latin America’s digital-solution providers in Bogotá and Medellín.[3]World Bank, “Digital Economy for Latin America and the Caribbean – Country Diagnostic: Colombia,” worldbank.org Near-U.S. geography and bilingual talent give it a strategic edge for agile, sprint-based projects. Foreign-capital flows, typified by Advent’s Siesa deal, accelerate the maturity of the partner landscape.

Argentina faces shorter Planning horizons amid currency swings, yet niche studios continue to excel in gaming, blockchain, and high-performance computing. Chile’s datacenter corridor spanning Santiago to Valparaíso modernizes regional interconnectivity, while its cybersecurity agency orchestrates best-practice frameworks for incident response. Peru’s start-up scene, spearheaded by 154 fintechs, embraces cloud-native architectures, escalating managed-services adoption. Rest-of-South-America markets, including Ecuador, Paraguay, and Uruguay, add incremental volumes through public-sector digitization and small-enterprise SaaS projects. Across the bloc, providers hedge volatility by distributing delivery centers, stabilizing billings, and ensuring service continuity within the South America IT Services market.

Competitive Landscape

The market remains moderately fragmented. Global system integrators combine scale, brand, and cross-industry reference cases, while regional champions win on cultural intimacy and Spanish-Portuguese language IP. Accenture bolstered Brazilian CX capabilities via the SOKO acquisition.[4]Outsource Accelerator, “Accenture expands Brazil footprint with SOKO purchase,” outsourceaccelerator.com IBM and Tata Consultancy Services rely on long-standing transformation deals with energy and financial majors, leveraging multizone cloud alliances.

Globant orchestrates growth through vertical studios targeting financial services, retail, and gaming across Brazil, Chile, and Mexico. Stefanini pursues inorganic expansion, scouting acquisitions across the Americas and Europe to deepen AI and cybersecurity offerings. Advent International and Carlyle funnel private-equity funds into mid-tier specialists, foreshadowing faster consolidation of fragmented sub-segments like ERP modernization and analytics platforms.

Competitive positioning hinges on advanced analytics credentials, AI accelerators trained on regional idioms, and documented sustainability roadmaps that align with green-IT regulations. Providers that package cybersecurity, multicloud orchestration, and AI automation within outcome-based contracts differentiate effectively. The absence of a single dominant player sustains pricing discipline as customers wield multi-vendor strategies to extract innovation and cost savings across the South America IT Services market.

South America IT Services Industry Leaders

Accenture plc

IBM Corp.

Tata Consultancy Services Ltd.

Globant S.A.

Stefanini Consultoria e Assessoria em Informática S.A.

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- June 2025: Visma strengthened its HR tech offering in Latin America by acquiring Talana, adding 5 million users across Chile and Peru.

- May 2025: Amazon pledged more than USD 4 billion for a new AWS region in Chile, slated for completion by late 2026.

- April 2025: Stefanini announced acquisition scouting across the Americas and Europe to scale AI and cybersecurity footprints.

- January 2025: EPAM completed its purchase of NEORIS, integrating 4,700 professionals across Spanish- and Portuguese-speaking markets.

South America IT Services Market Report Scope

South America IT services leverage technology and business expertise to help organizations create, manage, and optimize information and business processes.

The South America IT Services Market is segmented by Type (IT Consulting and Implementation, IT Outsourcing, Business Process Outsourcing), End-user (Manufacturing, Government, BFSI, Healthcare, Retail and Consumer Goods, Logistics), and Country.

The market sizes and forecasts are provided in terms of value (USD) for all the above segments.

By Service Type

| IT Consulting and Implementation |

| IT Outsourcing (ITO) |

| Business Process Outsourcing (BPO) |

| Managed Security Services |

| Cloud and Platform Services |

By Enterprise Size

| Small and Medium Enterprises (SMEs) |

| Large Enterprises |

By End-user Vertical

| BFSI |

| Manufacturing |

| Government and Public Sector |

| Healthcare and Life-Sciences |

| Retail and Consumer Goods |

| Telecom and Media |

| Logistics and Transport |

| Energy and Utilities |

| Other End-user Verticals |

By Country

| Brazil |

| Argentina |

| Colombia |

| Chile |

| Peru |

| Rest of South America |

| By Service Type | IT Consulting and Implementation |

| IT Outsourcing (ITO) | |

| Business Process Outsourcing (BPO) | |

| Managed Security Services | |

| Cloud and Platform Services | |

| By Enterprise Size | Small and Medium Enterprises (SMEs) |

| Large Enterprises | |

| By End-user Vertical | BFSI |

| Manufacturing | |

| Government and Public Sector | |

| Healthcare and Life-Sciences | |

| Retail and Consumer Goods | |

| Telecom and Media | |

| Logistics and Transport | |

| Energy and Utilities | |

| Other End-user Verticals | |

| By Country | Brazil |

| Argentina | |

| Colombia | |

| Chile | |

| Peru | |

| Rest of South America |

Key Questions Answered in the Report

How large is the South America IT Services market in 2025?

The South America IT Services market is valued at USD 83.38 billion in 2025 and is projected to reach USD 119.80 billion by 2030.

Which country delivers the highest revenue in regional IT services?

Brazil contributes 54.1% of the total 2024 revenue, leveraging the region’s largest developer ecosystem and extensive hyperscaler infrastructure.

What segment is expanding fastest through 2030?

Cloud and Platform Services record the strongest forward CAGR at 9.7%, driven by aggressive migration roadmaps at leading banks and hyperscaler investment.

Why is Colombia considered a growth hotspot?

Government spectrum allocations, bilingual talent resources, and proximity to the U.S. market support a 9.8% CAGR, the fastest among South American nations.

What are the biggest operational risks for providers?

Exchange-rate volatility and a shortage of senior cloud architects pose the most significant threats to profitability and delivery timelines.

Which industries will drive demand over the next five years?

Healthcare, banking, and manufacturing are expected to anchor incremental spending through telemedicine, cloud-native core banking, and Industry 4.0 initiatives, respectively.

Page last updated on: