Market Overview

| Study Period | 2020 - 2031 |

|---|---|

| Forecast Data Period | 2026 - 2031 |

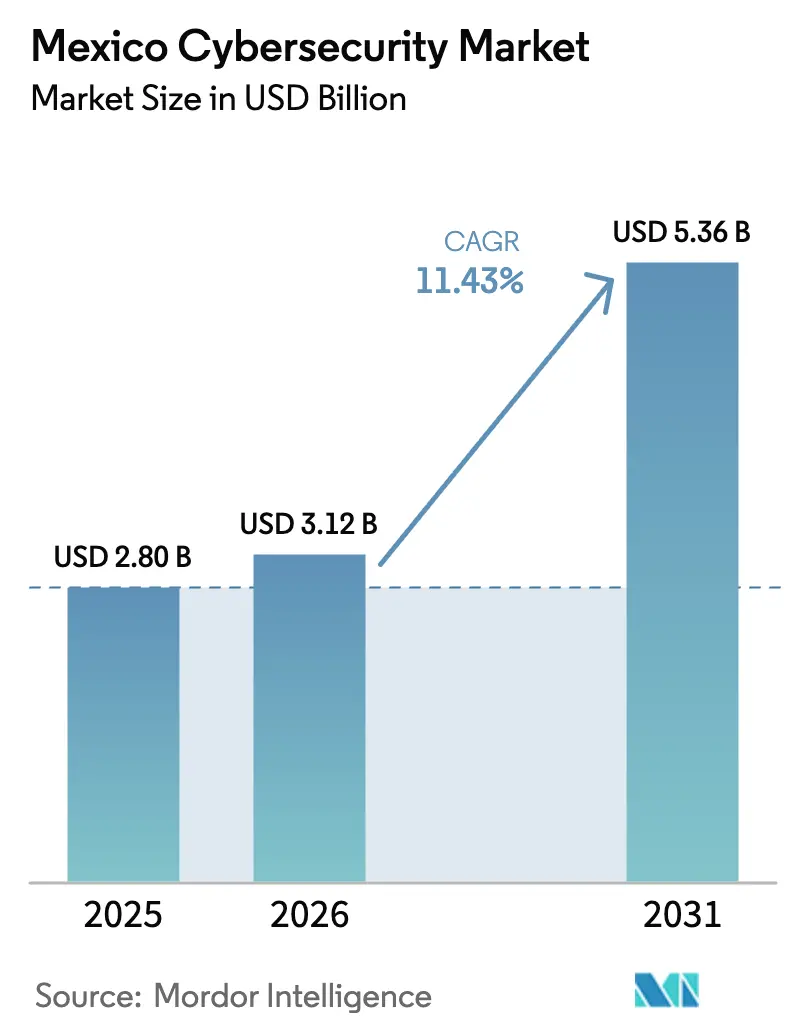

| Base Year Market Size (2025) | USD 2.80 Billion |

| Market Size (2026) | USD 3.12 Billion |

| Market Size (2031) | USD 5.36 Billion |

| Growth Rate (2026 - 2031) | 11.43% CAGR |

| Market Concentration | Medium |

Major Players

*Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. |

|

Mexico Cybersecurity Market Analysis by Mordor Intelligence

The Mexico cybersecurity market size was valued at USD 2.80 billion in 2025 and estimated to grow from USD 3.12 billion in 2026 to reach USD 5.36 billion by 2031, at a CAGR of 11.43% during the forecast period (2026-2031). Rising nation-state espionage, cartel-linked ransomware, and an expanding cloud footprint across manufacturing, finance, and government are fuelling security investments. Large enterprises remain the primary buyers, yet rapidly digitizing SMEs are narrowing the gap as nearshoring injects new factories and data centers into the threat landscape. Regulatory reforms—including Mexico City’s incident-reporting mandate and Banco de México’s resilience tests—elevate compliance spending. Severe skills shortages and limited federal cyber budgets temper growth but reinforce demand for managed services.

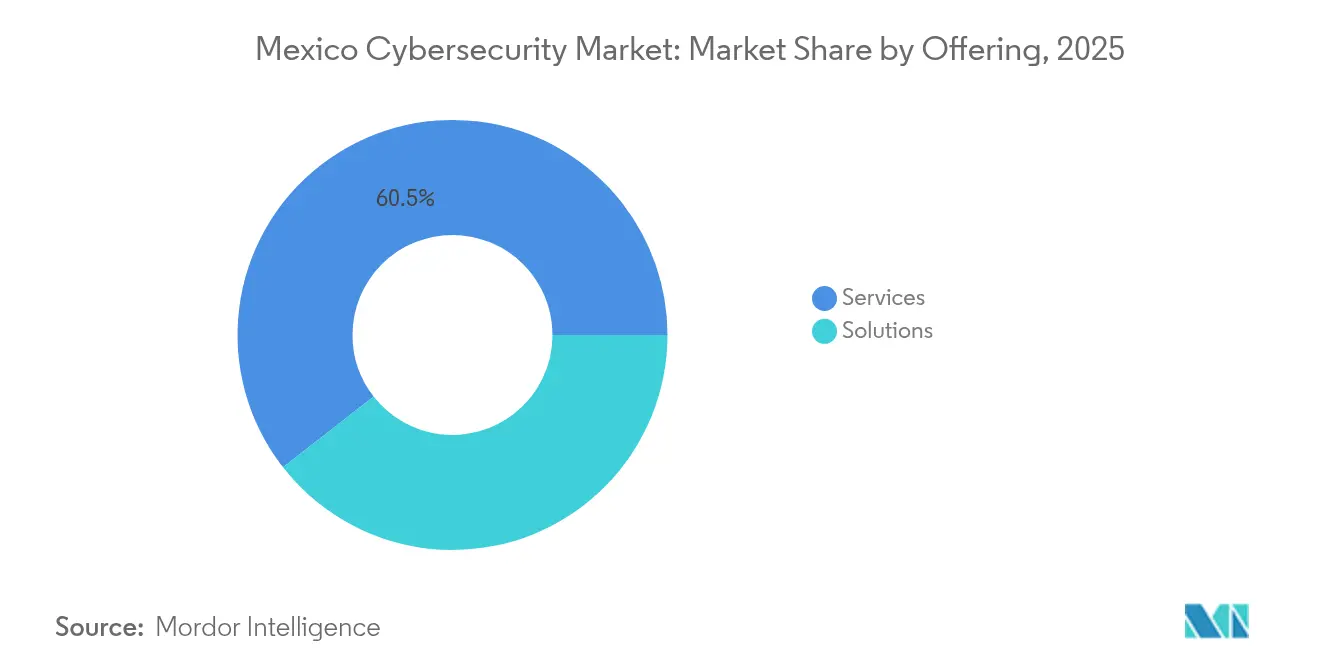

- By offering, services held 60.55% of Mexico cybersecurity market share in 2025, while cloud security solutions are projected to post a 17.53% CAGR to 2031.

- By deployment mode, on-premises solutions commanded 54.20% of the Mexico cybersecurity market size in 2025; cloud deployment is advancing at a 14.12% CAGR through 2031.

- By organization size, large enterprises captured 67.10% of Mexico cybersecurity market share in 2025; SMEs are the fastest-growing group at 13.55% CAGR to 2031.

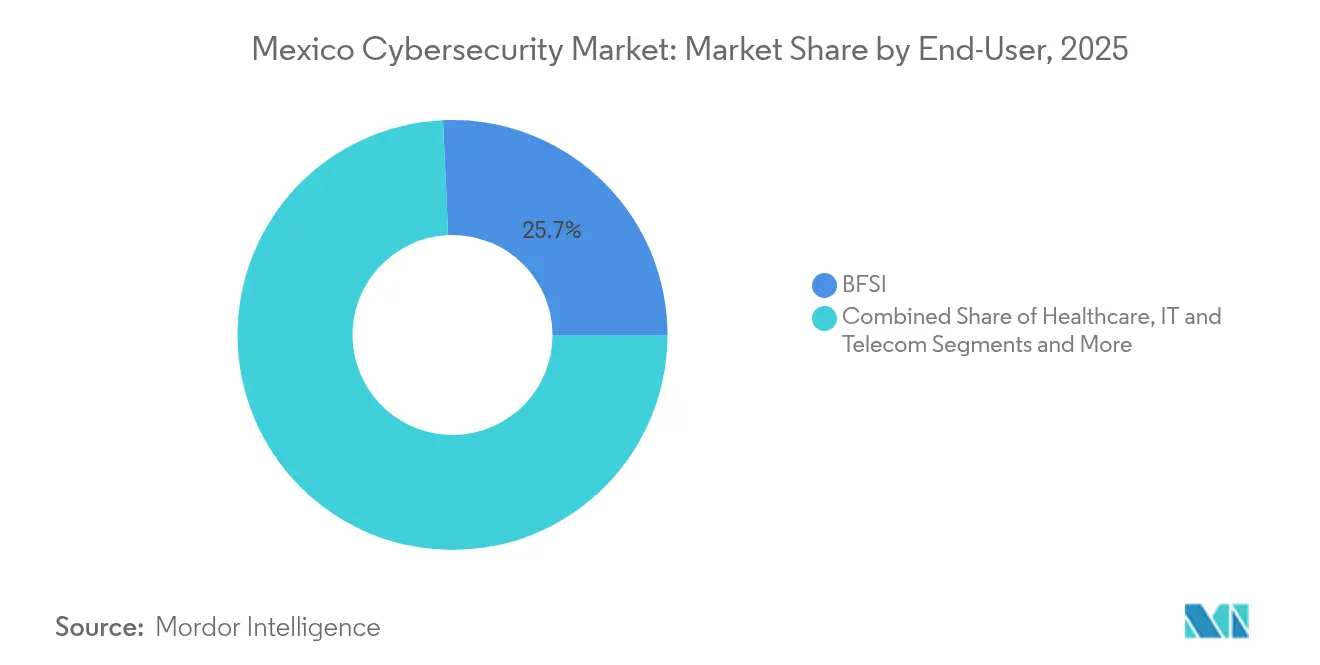

- By end user, BFSI led with 25.70% revenue share in 2025, whereas manufacturing is forecast to record the highest 12.41% CAGR through 2031.

- By geography, the Central region contributed 39.35% of 2025 revenue, but the Bajío-West corridor is set to expand at a 13.18% CAGR to 2031.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of 2026.

Mexico Cybersecurity Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Escalating nation-state & cartel-linked ransomware campaigns | 2.10% | National, with concentration in Central & Norte regions | Short term (≤ 2 years) |

| Mandated incident-reporting rules in proposed CDMX Cybersecurity Law | 1.80% | Central region, potential national expansion | Medium term (2-4 years) |

| Cloud-first IT modernization among Mexico's Top-500 firms | 2.30% | National, led by Central & Bajío-West regions | Medium term (2-4 years) |

| Near-shoring spike in smart-factory build-outs (Bajío & Norte) | 1.90% | Bajío-West & Norte regions | Long term (≥ 4 years) |

| Banxico 2024–27 mandatory resilience tests for regulated FIs | 1.40% | National, concentrated in financial centers | Short term (≤ 2 years) |

| Quantum-readiness spending race (post-RSA50 crack) | 0.80% | National, priority in BFSI & government sectors | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

Escalating Nation-State & Cartel-Linked Ransomware Campaigns

Drug cartels now collaborate with sophisticated cybercriminals, pushing ransom demands to an average USD 400,000 for industrial victims. Government-backed groups from China, Russia, and North Korea account for 77% of phishing activity tracked since 2020. Breaches at the Mexican Stock Exchange and Carbon Platform MEXICO2 highlighted gaps in market-critical infrastructure. The dual pressure from criminal and foreign actors propels spending on threat intelligence, managed detection, and incident response services. [1]Google Cloud Threat Intelligence Team, “Insights on Cyber Threats Targeting Users and Enterprises in Mexico,” Google Cloud, cloud.google.com

Mandated Incident-Reporting Rules in Proposed CDMX Cybersecurity Law

Mexico City’s draft law imposes 72-hour breach notifications, ISMS adoption, and workforce training, becoming Latin America’s most stringent sub-national framework. Officials disclosed that 70% of local agencies operate with critical vulnerabilities. Anticipation of parallel statutes in other states stimulates demand for governance, risk, and compliance tools. [2]Google Cloud Threat Intelligence Team, “Insights on Cyber Threats Targeting Users and Enterprises in Mexico,” Google Cloud, cloud.google.com

Cloud-First IT Modernization Among Mexico’s Top 500 Firms

Half of large enterprises now channel 10-30% of IT budgets to cloud and AI programs. Microsoft’s USD 1.3 billion commitment and Alibaba Cloud’s 2025 region launch catalyse cloud migration. Yet 62% of firms lack robust AI access controls, exposing new vulnerabilities that accelerate adoption of zero-trust and cloud-native security solutions.

Near-Shoring Spike in Smart-Factory Buildouts (Bajío & Norte)

Querétaro alone expects USD 42 billion in datacenter and manufacturing inflows, while Jalisco brands itself Mexico’s Silicon Valley with Bosch expanding to 2,000 engineers by 2026. Smart-factory deployments blend OT and IT networks, raising demand for industrial control system security and IoT hardening.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| 400k-person cyber-talent gap | -2.80% | National, acute in Norte & Bajío-West regions | Long term (≥ 4 years) |

| <0.5% federal IT budget earmarked for cyber | -1.90% | National, affecting public sector adoption | Medium term (2-4 years) |

| Fragmented legal framework → compliance uncertainty | -1.20% | National, with varying state-level implementations | Medium term (2-4 years) |

| Low SOC adoption in SMEs (<40%) | -1.60% | National, concentrated in Central & Norte regions | Short term (≤ 2 years) |

| Source: Mordor Intelligence | |||

400 K-Person Cyber-Talent Gap

Employers report 57% vacancy rates in security roles, pushing average specialist salaries to MXN 112,500 per month in 2025. Universities struggle to meet demand, forcing firms toward managed security service providers and automation.

Less than 0.5% Federal IT Budget Earmarked for Cyber

Federal allocations remain below 0.5% of total IT spend, even as Mexico ranked 14th globally for breach volume in 2024. The austerity-focused 2025 budget constrains agency upgrades and dampens overall market momentum.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Offering: Services Drive Market Leadership

Security services led with 60.55% of Mexico cybersecurity market share in 2025. Managed service providers thrive amid the skills crunch, with unified monitoring platforms posting triple-digit growth among finance, retail, and education clients. Regulatory complexity—spanning the new federal data law and city-level rules—intensifies demand for advisory and professional services. Cloud security is the fastest-growing solution at a 17.53% CAGR to 2031, propelled by hyperscale investments and zero-trust adoption. Application security and IAM gain traction, while hardware-centric network defenses face competition from software-defined alternatives. Integrated risk management tools benefit as 67.5% of firms rank cyber and data protection as their top risk.

Services growth underpins Mexico cybersecurity market expansion by addressing immediate talent shortages and compliance hurdles. Cloud-native controls, threat-intelligence feeds, and incident-response retainers dominate procurement roadmaps. Vendors bundle professional and managed offerings to deliver continuous protection, positioning services as the backbone of the Mexico cybersecurity market through 2031.

By Deployment Mode: On-Premises Legacy Meets Cloud Acceleration

On-premises deployments retained 54.20% of Mexico cybersecurity market size in 2025, reflecting data-sovereignty sensitivities in finance and public-sector environments. Nevertheless, cloud-based defenses are advancing at 14.12% CAGR as domestic regions from Google, Microsoft, and Alibaba improve latency and compliance alignment. Hybrid architectures dominate the banking sector, balancing Banxico resilience mandates with agility needs.

Cloud momentum stems from SME adoption—99.8% of Mexican firms are SMEs, yet most lacked automation until affordable cloud security emerged. Built-in governance, encryption, and monitoring accelerate regulatory alignment under the 2025 federal data law. Telecom operators’ elevated incident rates highlight the parallel need for robust on-premises perimeter controls, sustaining a dual-track deployment landscape within the Mexico cybersecurity market.

By End User: BFSI Leadership Amid Manufacturing Surge

BFSI held a 25.70% revenue share in 2025, shaped by strict Banxico oversight and the rise of 773 fintech. Digital payment adoption by 80 million smartphone users magnifies the attack surface, spurring investments in fraud analytics and identity verification.

Manufacturing shows the sharpest 12.41% CAGR, correlating with its 29.77% share of national cyberattacks. Nearshoring introduces thousands of connected robots and sensors, demanding OT segmentation and anomaly detection. Healthcare, energy, and retail contribute steady growth as critical-infrastructure defense and e-commerce expansion continue.

By Organization Size: Large Enterprises Lead, SMEs Accelerate

Large enterprises accounted for 67.10% of Mexico cybersecurity market share in 2025, underpinned by dedicated SOCs in 72% of big firms versus 40% among smaller peers. BFSI institutions, industrial conglomerates, and telecom giants anchor spending, driven by resilience tests and nearshoring upgrades.

SMEs register the highest 13.55% CAGR as cloud-delivered security lowers entry barriers. Smart-factory mandates and supply-chain requirements compel smaller manufacturers to fortify defenses. AI investment plans—2.4 × budget increases by 2025—drive new threat vectors that only enterprise-grade cloud security can mitigate. Managed detection and response offerings tailored for SMEs are expected to unlock significant incremental revenue within the Mexico cybersecurity market.

Geography Analysis

The Mexico cybersecurity market, anchored by federal agencies, corporate headquarters, and highly connected urban infrastructure. Mexico City’s landmark cyber law and the Llave MX biometric identity platform intensify the need for next-generation defenses. High breach volumes position threat-intelligence and incident-response services as priority purchases.

Querétaro’s cluster of hyperscale data centers and Jalisco’s engineering talent pool attract multinational factories, widening the Mexico cybersecurity market size in these states. Smart-manufacturing projects combine IoT, AI, and cloud, elevating demand for industrial security gateways, secure SD-WAN, and zero-trust OT overlays.

Further, cross-border supply chains and increased data-center footprints such as KIO’s MTY2 facility. Elevated industrial attack rates fuel uptake of OT monitoring and ransomware containment. The South-Southeast lags due to infrastructure gaps, though government initiatives around the Tehuantepec isthmus may unlock future potential.

Competitive Landscape

The Mexico cybersecurity market features mid-level concentration. Global platform vendors-Cisco, IBM, Palo Alto Networks, and Fortinet-dominate large-enterprise accounts, whereas SMEs rely on dozens of regional MSSPs and point-solution providers.

Recent consolidation signals a pivot toward integrated platforms: Palo Alto took over IBM’s QRadar SaaS assets, while Fortinet added Lacework’s cloud-native application protection to its Secure Access Service Edge stack. Strategic alliances, such as CrowdStrike-Fortinet endpoint-firewall integration, underline the trend toward AI-powered interoperability.

Local innovators are carving niches: Delta Protect supplies startup-focused security assessments, and Metabase Q raised USD 14 million to extend affordable solutions across Latin America. Hyperscalers embed native security features in their Mexican regions, intensifying competition around cloud-workload protection.

Talent scarcity continues to shift demand to MSSPs, enabling service-centric challengers to erode share from hardware-centric incumbents. Price competition remains moderate as compliance requirements and advanced threat complexity favour capability breadth over cost. [4]Arturo Solís, “30 Promesas 2024: Delta Protect, la Empresa que Blinda a las Startups,” Forbes México, forbes.com.mx

Mexico Cybersecurity Industry Leaders

-

Scitum, S.A. de C.V.

-

Cisco Systems México

-

IBM de México, S. de R.L.

-

KIO Cyber (Unidad de KIO Networks, S.A.B.)

-

Palo Alto Networks México, S. de R.L.

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- April 2025: Mexico City approved its Cybersecurity and Personal Data Protection Law, mandating 72-hour incident reporting.

- March 2025: Mexico enacted a new Federal Data Protection Law, dissolving INAI and imposing stricter accountability measures.

- February 2025: Alibaba Cloud launched its first Latin American region in Mexico, pairing infrastructure with local talent programs.

- January 2025: TransUnion agreed to acquire 94% of Trans Union de Mexico for USD 560 million, expanding credit-risk analytics and fraud-mitigation offerings.

Mexico Cybersecurity Market Report Scope

IT advancement, communication technologies, and smart energy grids are changing the landscapes of almost every country's critical infrastructure and business networks. However, with rapidly changing technology comes rapidly advancing threats. Cybersecurity solutions help an organization monitor, detect, report, and counter cyber threats, which are internet-based attempts to damage or disrupt information systems and hack critical information using spyware and malware and by phishing to maintain data confidentiality. The market sizing for the study has been provided based on the end-user spending on Cybersecurity solutions and services.

Mexico's cybersecurity market is segmented by offerings (solutions [application security, cloud security, data security, identity access management, infrastructure protection, integrated risk management, network security, end-point security, and other solution types] and services [professional services and managed services]), by deployment (On-premise, and cloud), by organization size (SMEs, large enterprises), by end-user vertical (BFSI, healthcare, IT and telecom, industrial and defense, retail, energy and utilities, manufacturing, and other end-user industries). The market sizes and forecasts are provided in terms of value in (USD) for all the above segments.

By Offering

| Solutions | Application Security |

| Cloud Security | |

| Data Security | |

| Identity and Access Management | |

| Infrastructure Protection | |

| Integrated Risk Management | |

| Network Security Equipment | |

| Endpoint Security | |

| Other Solutions | |

| Services | Professional Services |

| Managed Services |

By Deployment Mode

| Cloud |

| On-Premise |

By Organization Size

| Small and Medium Enterprises |

| Large Enterprises |

By End User

| BFSI |

| Healthcare |

| IT and Telecom |

| Industrial and Defense |

| Retail |

| Energy and Utilities |

| Manufacturing |

| Others |

| By Offering | Solutions | Application Security |

| Cloud Security | ||

| Data Security | ||

| Identity and Access Management | ||

| Infrastructure Protection | ||

| Integrated Risk Management | ||

| Network Security Equipment | ||

| Endpoint Security | ||

| Other Solutions | ||

| Services | Professional Services | |

| Managed Services | ||

| By Deployment Mode | Cloud | |

| On-Premise | ||

| By Organization Size | Small and Medium Enterprises | |

| Large Enterprises | ||

| By End User | BFSI | |

| Healthcare | ||

| IT and Telecom | ||

| Industrial and Defense | ||

| Retail | ||

| Energy and Utilities | ||

| Manufacturing | ||

| Others | ||

Key Questions Answered in the Report

What is the current size of the Mexico cybersecurity market?

The market stands at USD 3.12 billion in 2026 and is projected to reach USD 5.36 billion by 2031.

Which segment dominates spending in the Mexico cybersecurity market?

Security services lead with 60.55% revenue share, reflecting a strong preference for outsourced expertise.

How fast is cloud-based security growing in Mexico?

Cloud security solutions are forecast to expand at a 17.53% CAGR through 2031 as hyperscale data centers proliferate.

Which region is growing fastest for cybersecurity demand?

The Bajío-West corridor, anchored by Querétaro and Jalisco, is advancing at a 13.18% CAGR on the back of nearshoring investments.

What is the biggest restraint on Mexico’s cybersecurity growth?

A 400 K-person talent shortage is the most significant barrier, subtracting an estimated 2.8 percentage points from forecast CAGR.

How are new regulations affecting cybersecurity spending?

Mexico City’s 72-hour breach-reporting rule and the new federal data law are driving investments in governance, risk, and compliance solutions across all sectors.

Page last updated on: