South America IT Market Size and Share

Market Overview

| Study Period | 2019 - 2030 |

|---|---|

| Forecast Data Period | 2025 - 2030 |

| Historical Data Period | 2019 - 2023 |

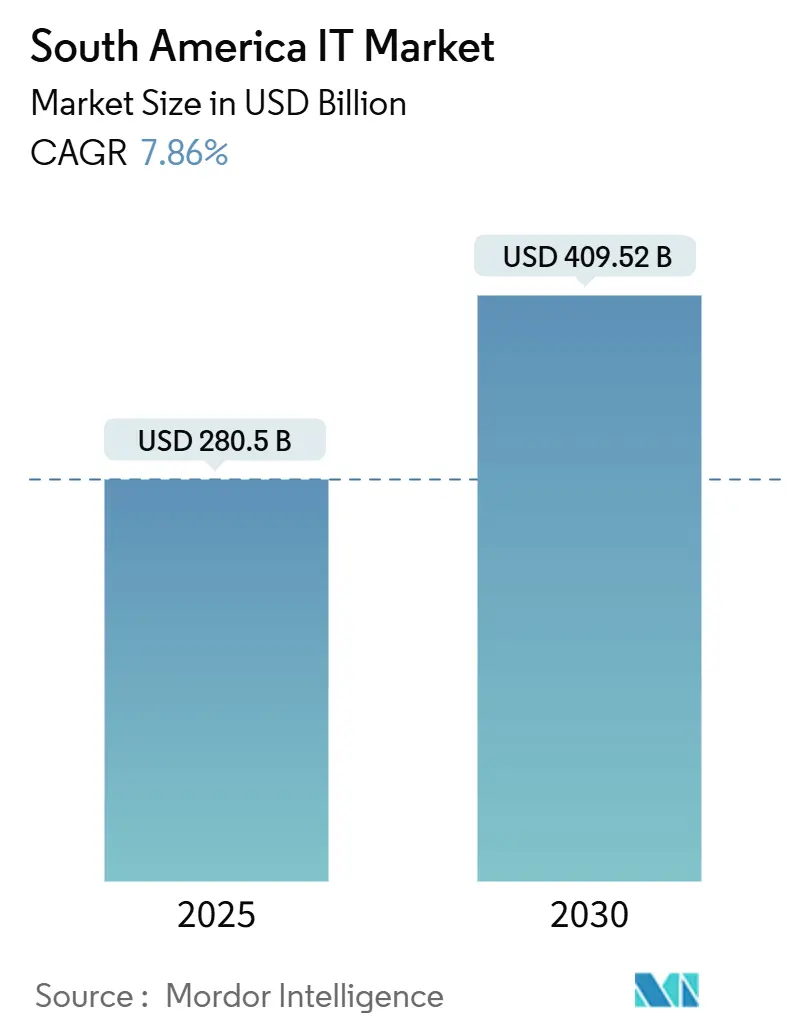

| Market Size (2025) | USD 280.5 Billion |

| Market Size (2030) | USD 409.52 Billion |

| Growth Rate (2025 - 2030) | 7.86% CAGR |

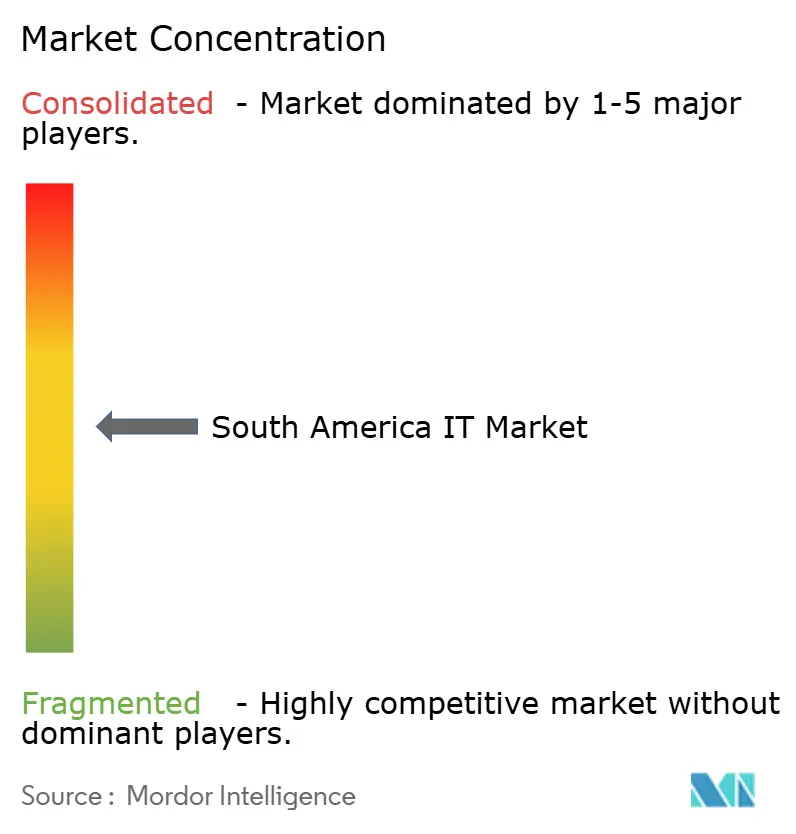

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

South America IT Market Analysis by Mordor Intelligence

The South America IT Market size is estimated at USD 280.5 billion in 2025, and is expected to reach USD 409.52 billion by 2030, at a CAGR of 7.86% during the forecast period (2025-2030).

Robust post-pandemic digitization, hyperscaler capital expenditure, and government‐backed data-sovereignty policies underpin the expansion of the South America IT market. Software remains the revenue anchor, but services post the fastest gains as enterprises outsource complex cloud migrations and AI deployments. Cloud adoption accelerates in parallel with on-premise upgrades, creating a long-term hybrid model. Submarine-cable additions, renewable-powered data centers, and low-earth-orbit (LEO) satellites reduce historical connectivity gaps, enabling the South America IT market to serve both local and nearshoring demand. Tight labor pools and energy-grid bottlenecks temper the overall growth outlook but do not alter the region’s strategic pull for multinationals.

Key Report Takeaways

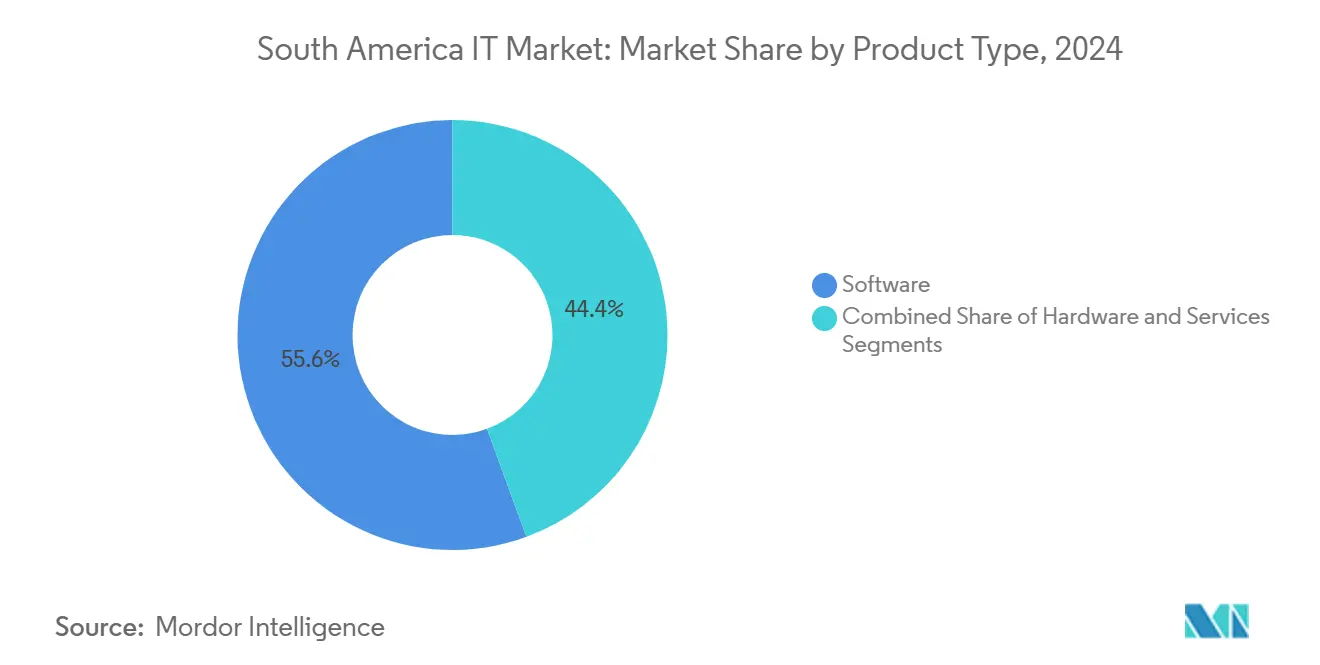

- By product type, software led with 55.6% revenue share in 2024, while services are forecast to expand at an 8.7% CAGR through 2030.

- By deployment model, on-premise solutions held 68.5% of the South America IT market share in 2024; cloud deployments are projected to climb at a 9.3% CAGR to 2030.

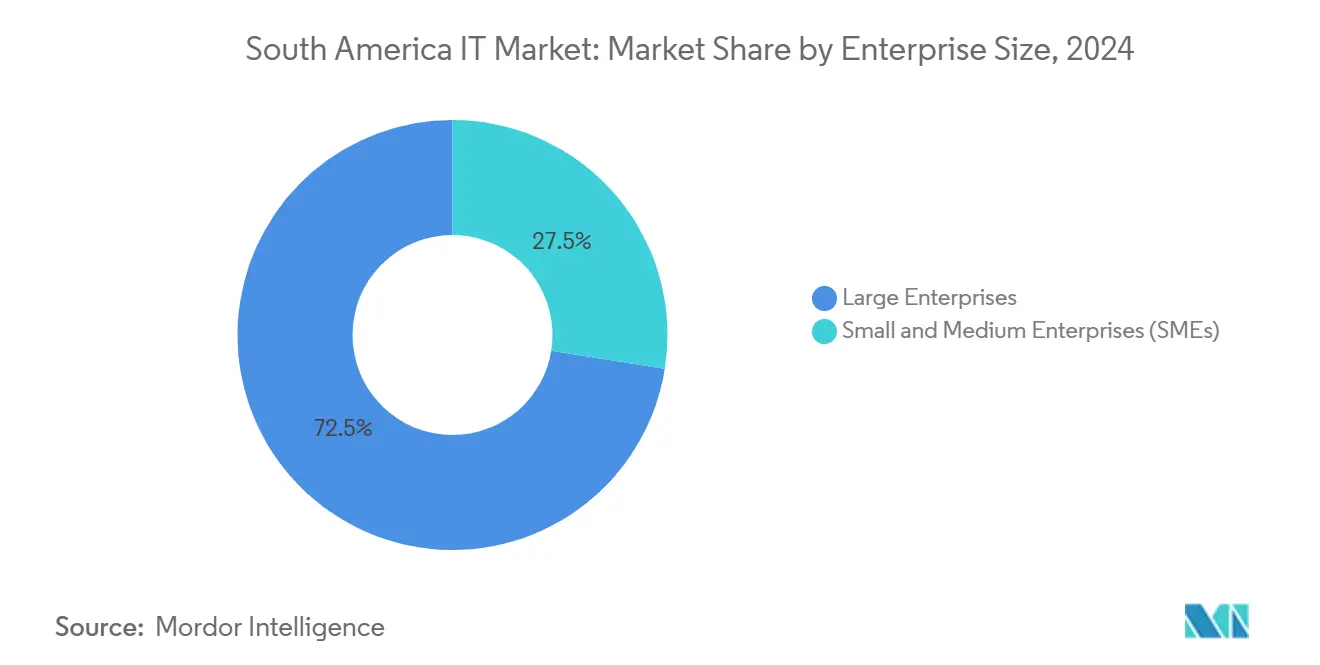

- By enterprise size, large enterprises accounted for 72.5% share of the South America IT market size in 2024, whereas SMEs are advancing at a 9.0% CAGR through 2030.

- By end-user industry, IT and telecom captured 31.5% of the South America IT market in 2024; retail and e-commerce is the fastest-growing vertical at an 8.2% CAGR to 2030.

- By country, Brazil dominated with 35.4% revenue share in 2024; Argentina records the highest projected CAGR at 8.5% through 2030.

South America IT Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Digital-transformation budgets post-COVID | +1.8% | Brazil, Mexico | Medium term (2-4 years) |

| Cloud-first strategies in mid-market segment | +1.5% | Brazil, Argentina, Colombia | Long term (≥ 4 years) |

| Fintech and retail-media SaaS wave | +1.2% | Brazil, Mexico, Argentina, Chile | Short term (≤ 2 years) |

| Hyperscaler data-center CAPEX | +1.0% | Brazil, Chile, Mexico | Long term (≥ 4 years) |

| E-invoicing and open-banking mandates | +0.8% | Brazil, Colombia, Mexico | Medium term (2-4 years) |

| LEO satellites for rural connectivity | +0.5% | Rural areas region-wide | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

Accelerating Digital-Transformation Budgets Post-COVID

South American firms now treat cloud migration, cybersecurity, and automation as board-level imperatives. ECLAC notes that broader internet access can lift regional productivity by 3%–9%. Brazil’s mobile ecosystem added USD 550 billion to GDP in 2024, with GSMA projecting USD 680 billion by 2030[1]. These data points signal a structural, not cyclical, shift in IT budgets. Enterprise demand stretches from secure remote-work enablement to AI-driven supply-chain visibility, locking in multi-year spending commitments.

Cloud-First Strategies Among Mid-Market Enterprises

The mid-market pivot toward cloud platforms continues to accelerate. CSIS estimated regional cloud spending at USD 10.9 billion in 2021, led by Brazil at USD 4.2 billion. Microsoft’s first hyperscale region exemplifies provider commitment, shaving latency while satisfying data-residency rules. Regulatory frameworks such as Brazil’s LGPD further motivate companies to adopt modern, compliance-ready architectures.

Fintech and Retail-Media Boom Boosting SaaS Uptake

Brazil’s PIX system achieved 95% consumer adoption within four years, creating a vast transaction dataset for SaaS vendors. Plug and Play recorded 1,500 Brazilian fintechs in 2024, up 47% year over year. The same payment rails power retail-media networks, which depend on real-time analytics and ad-tech integrations to monetize first-party data. SaaS providers focusing on fraud prevention, customer intelligence, and omnichannel orchestration are capturing this spend.

Hyperscalers’ Data-Center CAPEX Wave

Amazon earmarked USD 4 billion for Chilean cloud zones, the largest tech investment in the nation’s history. Google is building a USD 850 million facility in Uruguay to anchor its Southern Cone footprint. Renewables account for over 80% of Brazil’s grid mix, giving hyperscalers carbon-neutral capacity for compute-intensive AI workloads. New submarine cables linking Fortaleza, Punta Arenas, and Valparaíso reduce latency and place the South America IT market on global routing maps.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| IT-skills shortage and wage inflation | −1.4% | Brazil, Mexico, Colombia | Long term (≥ 4 years) |

| Power-grid and fiber bottlenecks in Tier-2 cities | −0.9% | Mexico, Argentina, others | Medium term (2-4 years) |

| Fragmented data-sovereignty regulations | −0.7% | Brazil, Argentina, Colombia | Medium term (2-4 years) |

| Water-scarcity limits on hyperscale cooling | −0.5% | Chile, Mexico, Argentina | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

Persistent IT-Skills Shortage and Wage Inflation

South America produces 20,000 new engineers annually, far below demand. Firms still scramble for AI, cybersecurity, and cloud architects. Terminal reports that 87% of developers consider compensation the primary job factor. Scarcity lengthens project timelines and lifts salary baselines, curbing the pace at which the South America IT industry can deliver transformation.

Power-Grid and Fiber-Backbone Bottlenecks Outside Tier-1 Cities

Reliable power remains uneven. Secondary Mexican cities face lengthy interconnection queues, while Brazil leverages surplus hydro and wind capacity. Patchy terrestrial fiber forces some enterprises to keep workloads on-premises. These infrastructure gaps slow market penetration for cloud platforms, even as the South America IT market continues to diversify geographically.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Product Type: Services Momentum Outpaces Software Scale

The services segment of the South America IT market is projected to grow at an 8.7% CAGR, eclipsing hardware and even the dominant software category over the forecast window. Software still controlled 55.6% revenue share in 2024, underscoring its core role in digital strategies. Enterprises increasingly bundle managed services with licenses, driving demand for consultative migration, AI model training, and ongoing optimization. VARs and system integrators are repositioning toward outcome-based contracts that fuse proprietary IP with vendor ecosystems. As a result, the South America IT market size attributable to services is expected to surpass USD 150 billion by 2030.

The hardware slice continues to post steady but muted gains, reflecting a transition from capital-heavy server rooms to asset-light cloud OPEX. Vendors are pivoting toward edge appliances, HCI systems, and AI accelerators to stay relevant. Meanwhile, the convergence of DevSecOps tooling and managed detection-and-response services illustrates how software and services are becoming inseparable buying motions in the South America IT market.

By Deployment Model: Cloud Adoption Rises Within a Hybrid Reality

On-premise deployments retained 68.5% of the South America IT market share in 2024, an outgrowth of existing assets and compliance concerns. Yet cloud workloads exhibit a 9.3% CAGR to 2030, signaling sustained momentum. Brazil’s proposed renewable-energy tax credits for local data centers are catalyzing hyperscaler builds that keep data resident while meeting ESG targets. As CIOs balance sovereignty, latency, and cost, hybrid architectures dominate roadmaps.

Multi-cloud tooling, automated FinOps, and secure connectivity platforms are in high demand as enterprises orchestrate workloads across AWS, Azure, Google Cloud, and regional players. For most organizations, the question is not whether to migrate but which workloads to migrate first. Consequently, the South America IT market size tied to cloud-delivered services is forecast to breach USD 200 billion by 2030, while on-premise refresh cycles concentrate on mission-critical and edge-computing use cases.

By Enterprise Size: SME Acceleration Erodes Large-Enterprise Monopoly

Large enterprises generated 72.5% of 2024 revenue, asserting budgetary dominance. Nonetheless, SMEs are growing at a 9.0% CAGR, narrowing the gap through cloud subscriptions and platform as a service (PaaS). PIX and open-banking regulations compel even micro-retailers to incorporate secure digital payments[2]Bank for International Settlements, “Fast Payments and Open Banking in Brazil,” bis.org. SaaS billing models eliminate upfront costs, letting SMEs access ERP, CRM, and AI tooling once reserved for Fortune 500 peers.

Vendor go-to-market strategies now target partner channels, fintech integrations, and self-service marketplaces to capture the expanding SME wallet. Focus on low-code/no-code and template-driven analytics accelerates time to value for smaller teams. As the decade ends, SMEs are expected to command over one-third of the South America IT market, reinforcing the democratization narrative.

By End-User Industry: Retail and E-Commerce Narrow the Gap With IT and Telecom

IT and telecom led 2024 spending with 31.5%, propelled by 5G rollouts, fiber backhaul, and telco cloud initiatives. However, retail and e-commerce are advancing at an 8.2% CAGR—double the pace of several traditional verticals. MercadoLibre alone announced USD 13.2 billion in 2025 capex to scale logistics, payments, and AI-driven advertising. Retailers seek unified inventory views, hyper-personalized marketing, and fraud-free checkouts, fueling SaaS demand.

Financial services, manufacturing, and energy sectors continue steady digitization. Cross-industry convergence is evident as retailers launch fintech arms and telcos monetize data via advertising platforms. This interlacing of verticals expands addressable demand for horizontal cloud services, reinforcing the resiliency of the South America IT market.

Geography Analysis

Brazil anchors the South America IT market with 35.4% revenue share, backed by 80% renewable energy penetration and a submarine-cable-rich coastline. São Paulo functions as the primary interconnection node for hyperscalers and content-delivery networks, lowering latency for domestic users. The General Data Protection Law (LGPD) has become a de facto standard for foreign investors, ensuring predictable compliance regimes. PIX’s 95% consumer adoption exemplifies Brazil’s capacity to scale digital innovations rapidly. These conditions justify the government’s USD 350 billion data-center roadmap, which further cements Brazil’s infrastructural edge through 2030.

Argentina is the fastest-growing geography with an 8.5% CAGR. The Large Investment Incentive Regime (RIGI) offers 25% corporate tax and 30-year stability for tech investments above USD 200 million, providing legal clarity uncommon in the region[3]Gobierno de la República Argentina, “Ley de Incentivo a Grandes Inversiones (RIGI),” argentina.gob.ar. Coupled with energy prices as low as USD 0.03 per kWh and skilled STEM talent, Argentina attracts both hyperscaler data halls and nearshoring software labs. The anticipated expansion of fiber routes between Buenos Aires and Santiago further integrates the country into regional traffic grids.

Colombia, and Chile round out the core markets. Colombia benefits from 18 free-trade accords and a 150,000-strong tech workforce, positioning Bogotá and Medellín as bilingual service hubs. Chile’s solar-rich Atacama region supplies cost-efficient green power for data centers, while coastal Valparaíso hosts new trans-Pacific cable landings. Together, these countries diversify demand and reduce the single-market concentration risk for investors in the South America IT market.

Competitive Landscape

Competition is intensifying as global hyperscalers carve out infrastructure moats while regional specialists leverage cultural familiarity and regulatory agility. Amazon Web Services, Microsoft Azure, and Google Cloud dominate IaaS but must partner with local telcos and software vendors to tailor offerings. For instance, AWS committed an additional USD 4 billion to expand its Chilean footprint in June 2025.

Regional champions such as TOTVS, Globant, and Softtek are consolidating niche players to scale AI, cybersecurity, and vertical SaaS capabilities. Softtek’s USD 60 million Colombian delivery center highlights nearshoring as a defensive and offensive tactic by incumbents. Meanwhile, solution verticalization—banking core modernization, retail-media orchestration, and smart-factory automation—has become critical to differentiation.

Start-ups cluster around fraud-proof payments, Spanish-language generative AI, and telecom OSS/BSS modernization, often receiving capital from corporate VC arms tied to telcos or retailers. Strategic alliances between hyperscalers and local ISPs accelerate last-mile fiber and 5G small-cell deployments, reshaping the South America IT market’s economics of scale. The competitive equilibrium remains fluid, with mergers and acquisitions expected to remain the principal path to capacity and talent acquisition.

South America IT Industry Leaders

International Business Machines (IBM) Corporation

SAP

Oracle Corporation.

Microsoft Corporation

Odoo

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- June 2025: Amazon Web Services received approval for its second Chilean data center, deepening a USD 4 billion infrastructure plan.

- April 2025: MercadoLibre committed USD 13.2 billion across six countries, including USD 6.2 billion in Brazil, to expand logistics and fintech capacity.

- March 2025: IBM closed its acquisition of Accelalpha, strengthening Oracle-stack services in Chile.

- February 2025: Panduit announced 9.4% 2024 growth and a new Monterrey plant opening in 2025 to meet cabling demand.

- January 2025: Softtek unveiled a USD 60 million service center investment in Colombia, adding 1,000 tech jobs.

South America IT Market Report Scope

IT services leverage technical and business expertise to help organizations create, manage, and optimize information and business processes. The market scope includes an analysis by size, end-user industry, and country throughout the forecast period.

| Hardware |

| Software |

| Services |

| On-premise |

| Cloud |

| Small and Medium Enterprises |

| Large Enterprises |

| Retail and E-commerce |

| Manufacturing |

| BFSI |

| Government and Public Sector |

| IT and Telecom |

| Healthcare |

| Energy and Utilities |

| Others |

| Brazil |

| Argentina |

| Colombia |

| Chile |

| Peru |

| By Product Type | Hardware |

| Software | |

| Services | |

| By Deployment Model | On-premise |

| Cloud | |

| By Enterprise Size | Small and Medium Enterprises |

| Large Enterprises | |

| By End-user Industry | Retail and E-commerce |

| Manufacturing | |

| BFSI | |

| Government and Public Sector | |

| IT and Telecom | |

| Healthcare | |

| Energy and Utilities | |

| Others | |

| By Country | Brazil |

| Argentina | |

| Colombia | |

| Chile | |

| Peru |

Key Questions Answered in the Report

What is the current size of the Latin America IT market?

The Latin America IT market stands at USD 280.5 billion in 2025 and is projected to reach USD 409.52 billion by 2030.

Which product category is growing fastest?

Services are expanding at an 8.7% CAGR as enterprises outsource cloud migrations and AI integration.

How quickly is cloud adoption rising in the region?

Cloud deployments are forecast to grow at a 9.3% CAGR through 2030, even though on-premise still holds 68.5% share.

Why is Argentina considered an IT growth hotspot?

Argentina offers 25% corporate tax, 30-year stability guarantees, and ultra-low energy prices under the RIGI program, supporting an 8.5% market CAGR.

What are the main constraints on market expansion?

Key restraints include IT-talent shortages, power-grid limitations in secondary cities, divergent data-sovereignty rules, and water scarcity affecting data-center cooling.

Which industry vertical will gain the most share by 2030?

Retail and e-commerce, driven by digital payments and omnichannel investments, is set to outpace other sectors at an 8.2% CAGR.

Page last updated on: