Sweden IT Services Market Size and Share

Market Overview

| Study Period | 2019 - 2030 |

|---|---|

| Forecast Data Period | 2025 - 2030 |

| Historical Data Period | 2019 - 2023 |

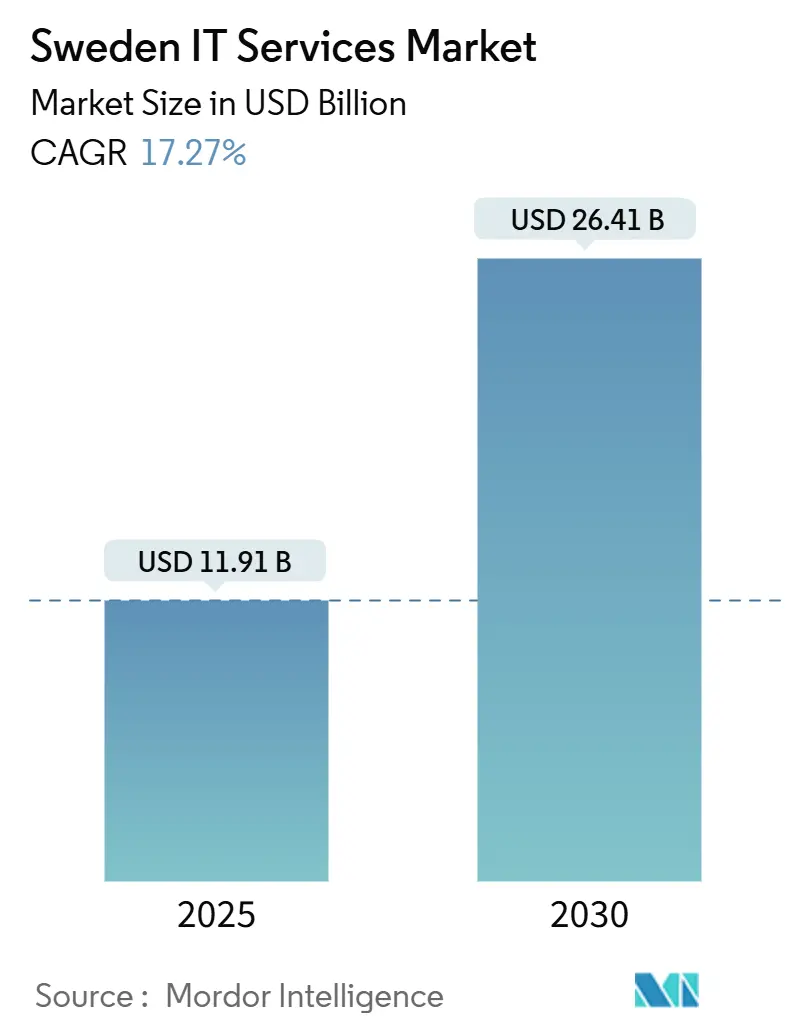

| Market Size (2025) | USD 11.91 Billion |

| Market Size (2030) | USD 26.41 Billion |

| Growth Rate (2025 - 2030) | 17.27% CAGR |

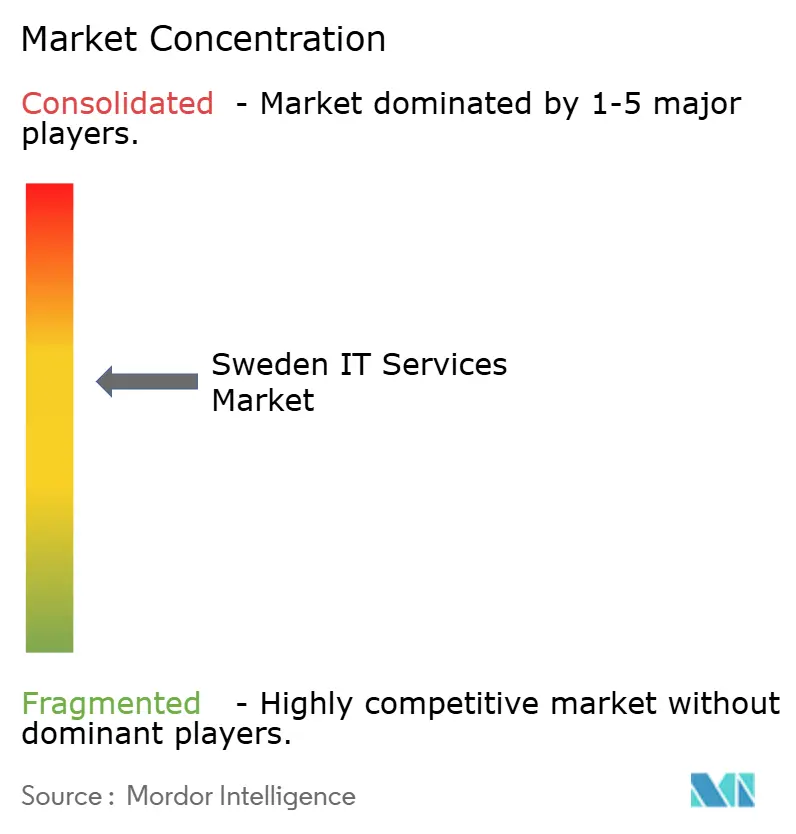

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

Sweden IT Services Market Analysis by Mordor Intelligence

The Sweden IT Services market size stands at USD 11.91 billion in 2025 and is forecast to reach USD 26.41 billion in 2030, expanding at a 17.27% CAGR during the forecast period. Growth reflects sustained public-sector digitalization, an enterprise rush to cloud platforms, and heightened cyber-risk awareness that fuels managed security demand. Government framework agreements worth SEK 1.5 billion, Microsoft’s SEK 33.7 billion hyperscale investment, and rising AI adoption across manufacturing clusters all converge to reshape service delivery models. Acute talent shortages elevate outsourcing volumes, while EU-level directives such as NIS2 and the Digital Operational Resilience Act tighten compliance requirements that only mature providers can meet. Labor cost inflation and data-sovereignty mandates temper short-term competitiveness, yet the Swedish IT Services market retains clear momentum as Nordic organizations pivot from cost savings toward digital differentiation.

Key Report Takeaways

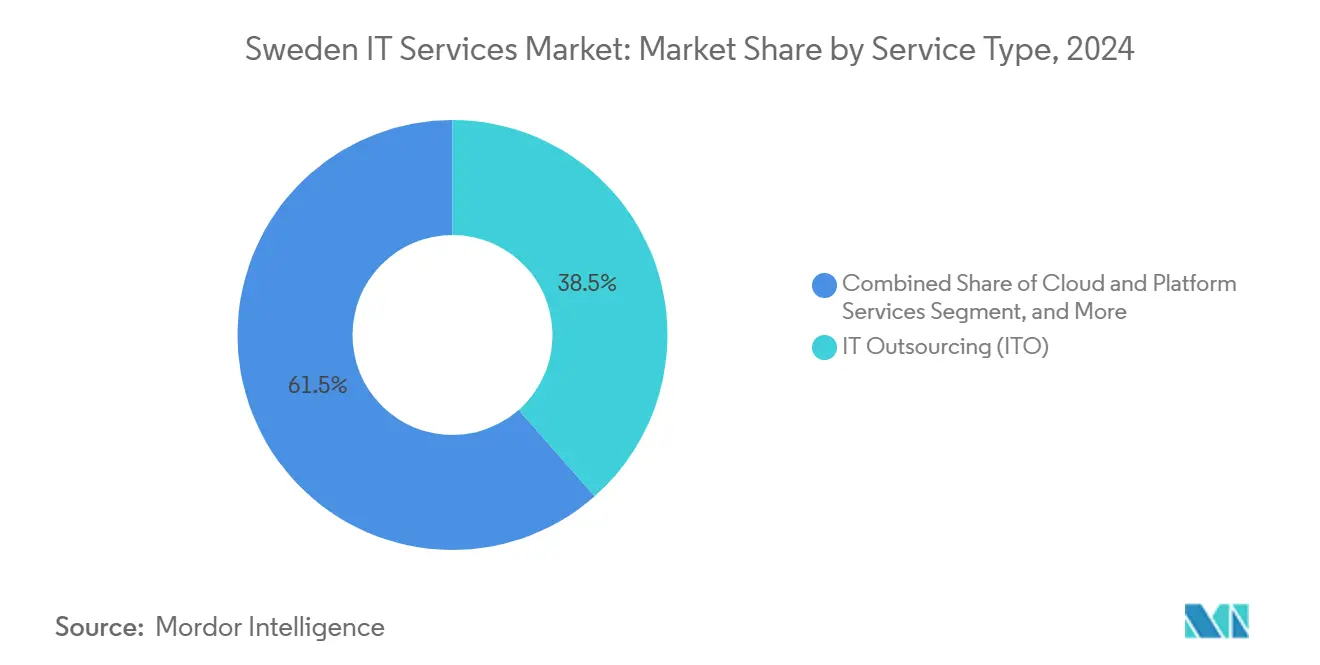

- By service type, IT Outsourcing led with 38.5% of Sweden's IT Services market share in 2024; Cloud and Platform Services are projected to advance at an 18.42% CAGR through 2030.

- By end-user enterprise size, Large Enterprises accounted for 68.3% share of the Sweden's IT Services market size in 2024, while Small and Medium Enterprises are growing at an 18.2% CAGR to 2030.

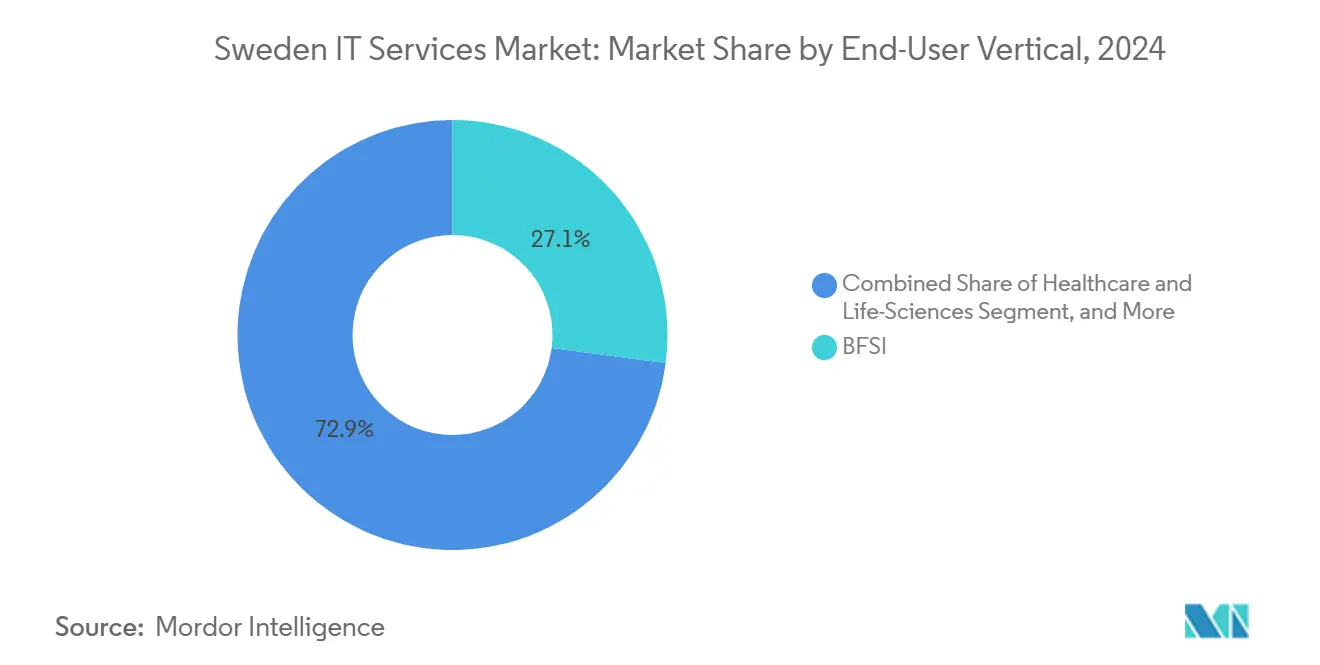

- By end-user vertical, BFSI held 27.07% of Sweden's IT Services market share in 2024; Healthcare and Life Sciences display the fastest 18.51% CAGR to 2030.

Sweden IT Services Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Government digitalization agenda accelerating public-sector IT spend | +3.2% | National, with concentration in Stockholm and Gothenburg | Medium term (2-4 years) |

| Rapid enterprise cloud adoption across industries | +4.1% | National, with Nordic spillover effects | Short term (≤ 2 years) |

| Escalating cyber threats driving managed security services uptake | +2.8% | National, with critical infrastructure focus | Short term (≤ 2 years) |

| Acute domestic talent shortage fueling IT outsourcing demand | +3.5% | National, with rural area emphasis | Long term (≥ 4 years) |

| Green IT procurement mandates promoting sustainability-focused services | +1.9% | National, with EU regulatory alignment | Medium term (2-4 years) |

| AI-driven automation momentum in mid-sized manufacturing clusters | +2.2% | Regional, concentrated in Västra Götaland and Skåne | Medium term (2-4 years) |

| Source: Mordor Intelligence | |||

Government Digitalization Agenda Accelerating Public-Sector IT Spend

The Digital First! Reform mandates digital-by-default service delivery across 290 agencies and allocates EUR 2.8 billion to standardized building blocks such as AI services, API management, and identity frameworks. [1]Digital Government Agency, “Ansvar och finansiering,” digg.se Capgemini’s logistics and finance contract with the Swedish Armed Forces and AFRY’s SEK 1.5 billion framework underline how defense digitalization cascades into civilian spending. Frameworks now span up to seven years with ESG clauses, rewarding providers that combine sustainability capabilities with local regulatory insight. Interoperability and data-sovereignty demands further tilt awards toward Nordic firms able to deliver culturally aligned solutions. This structured procurement environment turns Sweden into a reference market for scalable public-sector modernization and drives recurring revenue for qualified suppliers.

Rapid Enterprise Cloud Adoption Across Industries

Enterprise investment in cloud services doubled in 2024, shifting focus from lift-and-shift migrations to platform-native development and AI-enabled workloads. [2]Nordlo, “Swedish companies’ investments in cloud services have doubled,” nordlo.com SaaS providers expect cloud to underpin 25% of Sweden’s basic IT infrastructure by 2025, indicating a decisive architectural pivot. Uddeholm’s AI-driven defect-reduction project with CGI shows the industry moving from theory to measurable outcomes. Multi-cloud strategies prevent vendor lock-in and strengthen local data-residency assurances, favoring Nordic integrators with global hyperscale alliances. As basic infrastructure commoditizes, premium growth moves to industry-specific platforms and consulting that translate cloud economics into competitive advantage.

Escalating Cyber Threats Driving Managed Security Services Uptake

Cyber attacks on Swedish critical infrastructure and financial institutions jumped 35% in 2024, pushing the domestic cybersecurity market toward USD 2.19 billion by 2029. The National Cybersecurity Strategy 2025-2029 aligns public and private risk frameworks, while the Digital Operational Resilience Act imposes immediate ICT-risk mandates on banks. Organizations lacking in-house expertise now source AI-enhanced threat detection, zero-trust architectures, and 24×7 monitoring from managed security providers. With a shortfall of 300,000 cybersecurity professionals nationally, demand for outsourced protection is structural rather than cyclical.

AI-Driven Automation Momentum in Mid-Sized Manufacturing Clusters

Mid-sized manufacturers in Västra Götaland and Skåne adopt AI for predictive maintenance, quality inspection, and supply-chain control, aiming at SEK 500-550 billion added GDP over ten years. AFRY’s project with Hydro shows AI delivering both climate-footprint reduction and operational gains. Providers with industrial domain skills package turnkey AI solutions plus workforce training, lowering entry barriers for plants without large IT staffs. Regional universities and government grants further stimulate pilot activity, signaling sustained services demand over the medium term.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| High labor costs eroding price competitiveness | -2.1% | National, with Stockholm metropolitan area most affected | Short term (≤ 2 years) |

| Stringent data sovereignty and compliance requirements | -1.8% | National, with EU regulatory spillover | Medium term (2-4 years) |

| Saturation of ERP modernization among large enterprises | -1.3% | National, with manufacturing sector concentration | Medium term (2-4 years) |

| Mid-tier provider consolidation squeezing niche players | -0.9% | National, with rural market emphasis | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

High Labor Costs Eroding Price Competitiveness

Average monthly IT salaries reached EUR 4,000 in 2024, up 12% since 2022, outpacing productivity and inflating project rates. [3]Computer Weekly, “Rising IT talent costs shadow Sweden’s skills shortage,” computerweekly.com Talent shortages of 18,000 specialists per year intensify bidding wars, especially in Stockholm, where multinationals cluster. Smaller firms struggle to match pay scales and instead offload delivery to lower-cost partners, reducing direct participation. Government plans to liberalize work permits and fund reskilling worth SEK 5.3 billion will help only gradually, leaving short-term margin pressure intact.

Stringent Data Sovereignty and Compliance Requirements

NIS2 transposition as Sweden’s Cybersecurity Act broadens mandatory security controls for essential-service providers, while GDPR enforcement, the AI Act, and the European Accessibility Act stack additional obligations. Compliance spending soaks up budgets that could fund innovation and strains SMEs lacking legal expertise. Yet the same complexity acts as a moat for established Nordic suppliers with mature governance frameworks, nudging buyers toward vendors that guarantee local data residency.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Service Type: Cloud Platforms Drive Market Evolution

Cloud and Platform Services are projected to deliver the fastest 18.42% CAGR, outpacing the 17.27% headline rate for the Sweden IT Services market. IT Outsourcing retains 38.5% of Sweden's IT Services market share by value in 2024 as enterprises still rely on external partners for core infrastructure and application upkeep. Microsoft’s SEK 33.7 billion hyperscale program and Sogeti’s EUR 220 million public-sector award underscore cloud’s primacy. The rising Swedish IT Services market size for managed security and consulting shows buyers shifting from cost-centric contracts toward outcome-based partnerships that combine automation, AI, and domain expertise. Providers unable to embed cloud-native capabilities face price commoditization.

Cross-selling between service lines accelerates as platform migrations create downstream needs for security hardening and business process redesign. Preem’s AI road-map with EY illustrates how consulting revenues grow alongside infrastructure deals. Providers bundle cloud hosting with continuous compliance monitoring to meet NIS2 obligations, increasing average contract value and length. The Sweden IT Services market continues to pivot from resource augmentation toward integrated transformation programs, raising entry barriers for niche firms with narrow scope.

By End-User Enterprise Size: SME Digitalization Accelerates

Large Enterprises command 68.3% of Sweden's IT Services market share in 2024, but SMEs offer the highest 18.2% CAGR through 2030, supported by simplified procurement portals and EU funds earmarked for small-business digital maturity. The Sweden IT Services market size attributable to SMEs expands as cloud subscriptions, cybersecurity bundles, and low-code platforms shrink upfront costs. Government vouchers and digital-skills training further unlock demand outside metropolitan cores.

Providers craft modular packages that combine infrastructure, security, and regulatory compliance in a single monthly fee, appealing to resource-constrained owners. Consid’s geographic expansion strategy targets European banking SMEs with templated yet customizable solutions that scale without heavy onsite consulting. As cloud democratizes advanced capabilities, the historical divide between large and small buyers narrows, fostering a more balanced revenue mix for vendors able to productize services.

By End-User Vertical: Healthcare Leads Digital Innovation

BFSI held 27.07% Sweden IT Services market share in 2024, anchored by payment modernization and new EU resilience mandates. Healthcare and Life Sciences however post the leading 18.51% CAGR as telemedicine, electronic health records, and genomics platforms attract sustained investment. The national 1177 healthcare portal and full EHR coverage create fertile ground for platform upgrades and patient-centric analytics.

Manufacturing follows closely, with AI-enhanced quality control and predictive maintenance gaining traction in export-oriented clusters. Energy and Utilities adopt digital twins to optimize asset performance, while Retail deploys AI customer analytics to fend off international e-commerce entrants. Across sectors, ESG reporting drives uptake of data-collection and carbon-accounting services, carving a horizontal revenue stream for vendors that master sustainability metrics.

Geography Analysis

Stockholm anchors over 50% of Sweden's IT Services market revenues, thanks to proximity to government agencies and financial institutions that spearhead digital adoption. The capital’s dense startup ecosystem supplies continuous innovation and amplifies demand for cloud, security, and AI talent. Gothenburg and Malmö contribute rising volumes through automotive, logistics, and e-commerce activities that need specialized IT support. Northern regions such as Umeå experience steady gains as remote work normalizes and public programs subsidize broadband expansion, widening provider footprints beyond major metros.

Nordic benchmarking shows Denmark and Norway outpacing Sweden in short-term services growth, yet Sweden retains regional leadership in cloud maturity and AI experimentation, offering stable long-range prospects. Domestic providers leverage Sweden’s rigorous privacy stance to win cross-border contracts where data residency is paramount, transforming national capability into export revenue. McKinsey projects Nordic software output will reach seven times domestic demand by 2030, placing Swedish firms at the heart of a USD 44 billion export wave.

International hyperscalers and consulting giants view Sweden as a Nordic beachhead, reinforcing local ecosystems through investments and acquisitions. This inflow elevates competition yet also upskills the labor pool and broadens partner networks for indigenous vendors. The geographic dispersion of talent and projects continues to equalize as virtual delivery proves effective, though Stockholm’s critical mass ensures it remains the prime hub for large strategic deals.

Competitive Landscape

The Sweden IT Services market remains moderately concentrated, with Tietoevry’s EUR 3 billion revenue leading but not dominating service lines. Atea, CGI, and IBM round out the top tier, each combining product resale with growing managed services to offset hardware commoditization. Mid-cap specialists such as Knowit and HiQ carve defensible spaces in UX design, agile development, and embedded systems.

Technology differentiation now eclipses sheer scale. Providers invest heavily in AI accelerators, sovereign-cloud offerings, and automated security orchestration to win transformation-focused contracts. The acute talent shortage forces creative delivery models that mix Nordic consulting, near-shore centers, and automation to maintain margins. Cross-border mergers like ARICOMA’s purchase of Stratiteq illustrate rising consolidation as pan-European groups seek critical mass. [4]KKCG, “ARICOMA acquires Stratiteq,” kkcg.com

Regulation shapes competition by rewarding firms with certified local data centers and advanced compliance tooling. International entrants partner with Swedish specialists to navigate legal nuance, while Nordic incumbents leverage cultural familiarity and language skills to defend their share. White-space opportunities arise in sustainability consulting, AI governance, and SME-focused subscription bundles, areas where agile players can still out-innovate giants.

Sweden IT Services Industry Leaders

Tietoevry Create AB

CGI Sverige AB

Capgemini Sverige AB

Telefonaktiebolaget LM Ericsson

IBM Svenska AB

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- May 2025: Tietoevry published restated 2024 financials after divesting Tech Services, repositioning around software and digital engineering.

- April 2025: Atea posted a record Q1 2025 operating profit as hardware, software, and services all rose double digits.

- March 2025: Sogeti Sweden won an exclusive EUR 220 million public-sector framework, one of the largest Nordic IT deals.

- March 2025: AFRY signed a SEK 1.5 billion framework with the Swedish Armed Forces for strategic IT and security consulting.

- February 2025: Adventure Box acquired Lion Gaming for SEK 467 million, expanding into iGaming technology.

- February 2025: White Pearl Technology Group acquired Lumin4ry AB to broaden its service reach.

- January 2025: CGI secured a five-year SEK 300 million outsourcing agreement with Bankgirot, transitioning staff to its Östersund center.

Sweden IT Services Market Report Scope

| IT Consulting and Implementation |

| IT Outsourcing (ITO) |

| Business Process Outsourcing (BPO) |

| Managed Security Services |

| Cloud and Platform Services |

| Small and Medium Enterprises (SMEs) |

| Large Enterprises |

| BFSI |

| Manufacturing |

| Government and Public Sector |

| Healthcare and Life-Sciences |

| Retail and Consumer Goods |

| Telecom and Media |

| Logistics and Transport |

| Energy and Utilities |

| Other End-User Verticals |

| By Service Type | IT Consulting and Implementation |

| IT Outsourcing (ITO) | |

| Business Process Outsourcing (BPO) | |

| Managed Security Services | |

| Cloud and Platform Services | |

| By End-User Enterprise Size | Small and Medium Enterprises (SMEs) |

| Large Enterprises | |

| By End-User Vertical | BFSI |

| Manufacturing | |

| Government and Public Sector | |

| Healthcare and Life-Sciences | |

| Retail and Consumer Goods | |

| Telecom and Media | |

| Logistics and Transport | |

| Energy and Utilities | |

| Other End-User Verticals |

Key Questions Answered in the Report

How large is the Sweden IT Services market in 2025?

The market is valued at USD 11.91 billion in 2025 and is projected to reach USD 26.41 billion by 2030.

Which service segment is expanding the fastest?

Cloud and Platform Services show the highest 18.42% CAGR through 2030, reflecting enterprise migration to hyperscale platforms.

What drives SME demand for IT services in Sweden?

Government incentives, simplified procurement frameworks, and cloud subscriptions that lower upfront costs collectively fuel SME adoption.

Why are managed security services growing quickly?

A 35% rise in cyber attacks and new EU resilience rules push organizations to outsource advanced security monitoring and response.

Which vertical exhibits the strongest growth momentum?

Healthcare and Life Sciences lead with an 18.51% CAGR, supported by nationwide telemedicine and digital health investments.

How do labor costs affect provider competitiveness?

Average salaries of EUR 4,000 per month raise delivery costs, pressuring margins and accelerating interest in automation and offshore models.

Page last updated on: