Market Overview

| Study Period | 2020 - 2031 |

|---|---|

| Forecast Data Period | 2026 - 2031 |

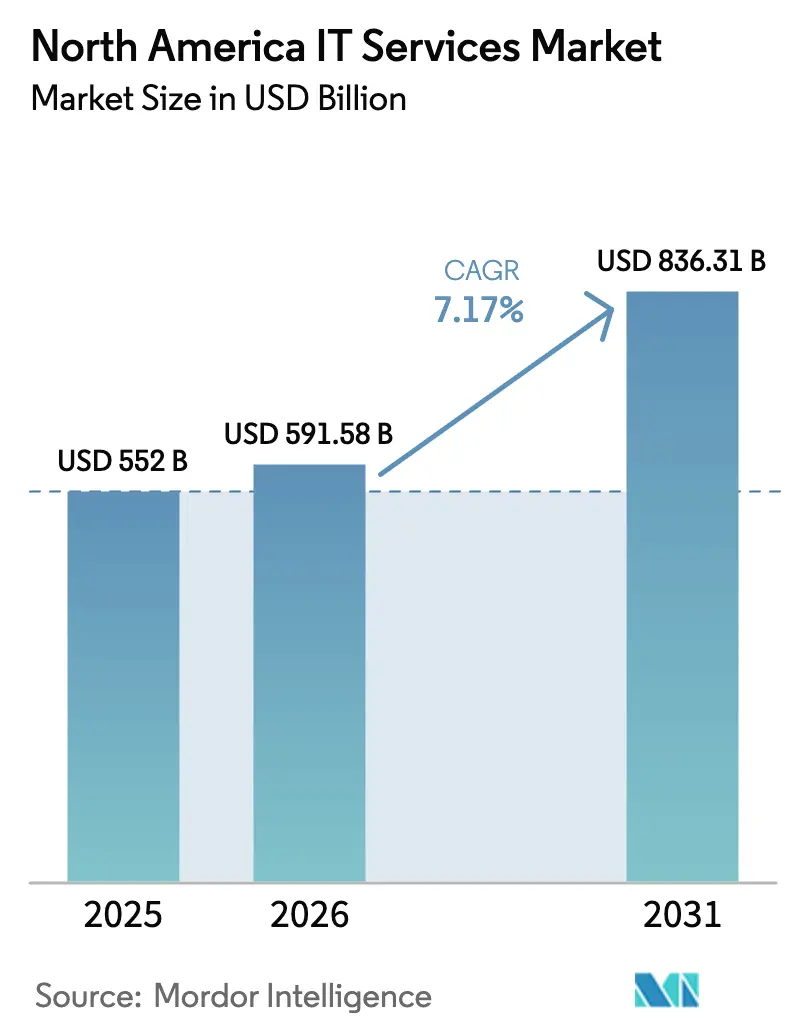

| Base Year Market Size (2025) | USD 552 Billion |

| Market Size (2026) | USD 591.58 Billion |

| Market Size (2031) | USD 836.31 Billion |

| Growth Rate (2026 - 2031) | 7.17% CAGR |

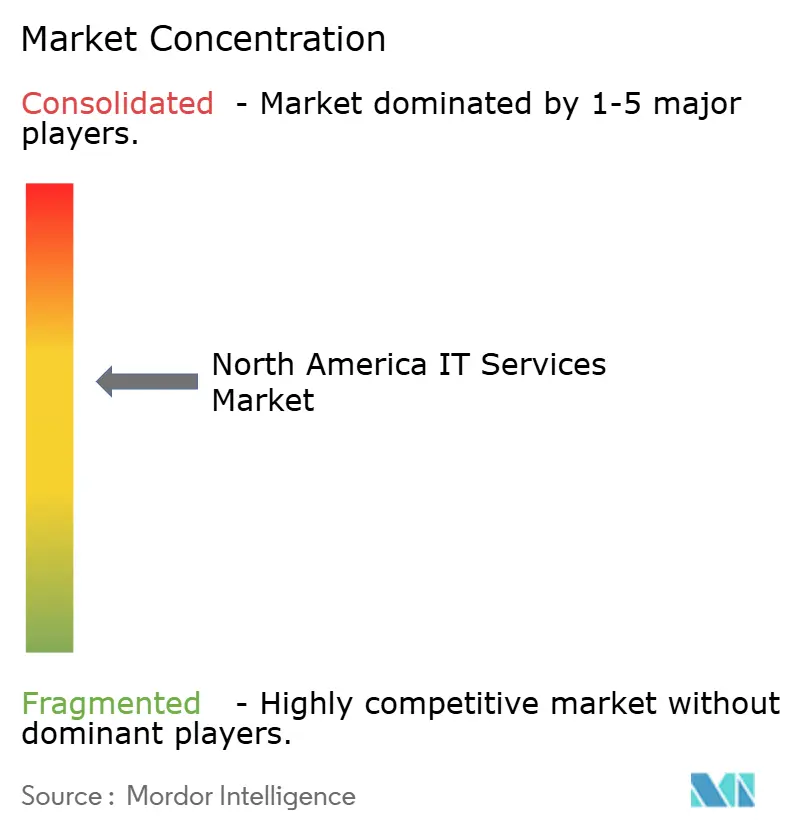

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

North America IT Services Market Analysis by Mordor Intelligence

The North America IT Services market size was valued at USD 552 billion in 2025 and estimated to grow from USD 591.58 billion in 2026 to reach USD 836.31 billion by 2031, at a CAGR of 7.17% during the forecast period (2026-2031). Record enterprise outlays on large-scale cloud migration, intensifying adoption of AI-enabled platforms, and wide-scale zero-trust roll-outs underpin this momentum. North America accounts for 40% of global IT spending and posted a 10.2% increase in 2025, highlighting the region’s centrality to worldwide digital transformation. Boards are demanding technology projects that translate directly into revenue lift or cost take-out, steering contracts toward providers that can tie technical delivery to measurable outcomes. Near-shore talent hubs in Latin America, offering 25%-40% cost savings versus US rates, are easing the skills crunch while preserving real-time collaboration. Heightened cyber-threats, evolving data-sovereignty mandates, and higher capital costs introduce execution complexity but simultaneously create advisory opportunities for compliance-savvy providers.

Key Report Takeaways

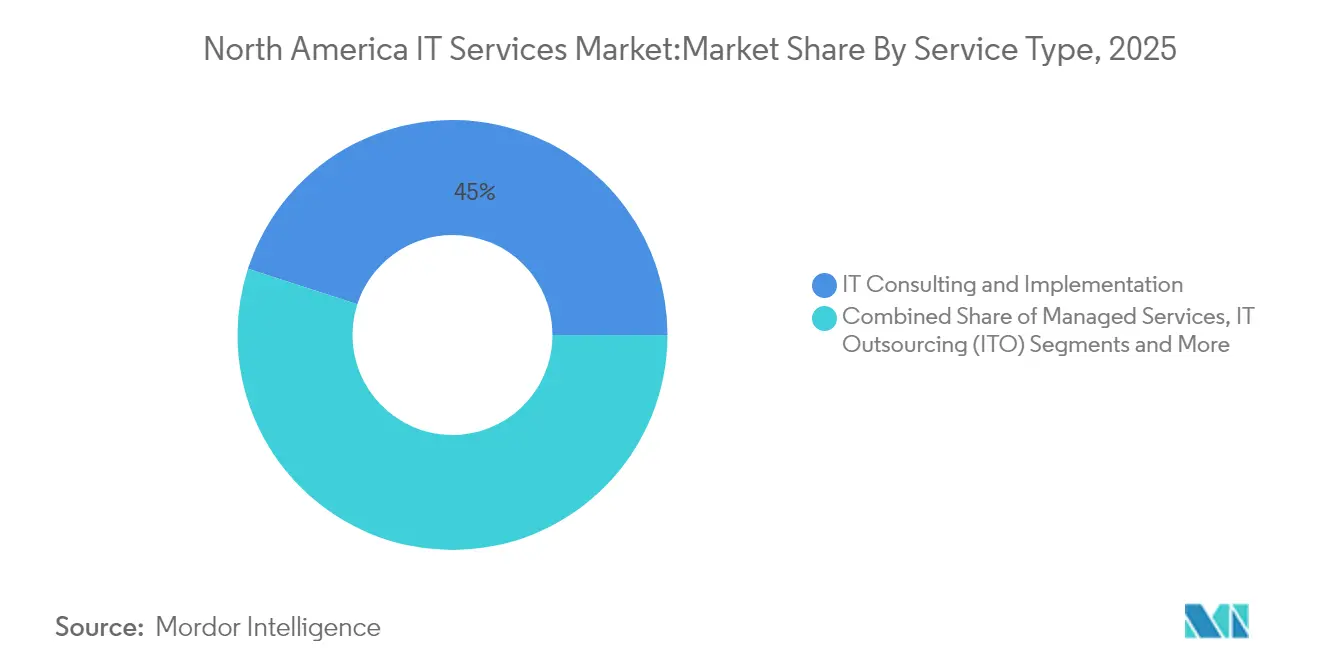

- By service type, IT consulting and implementation led with 45.02% of North America IT Services market share in 2025, while managed services is expanding fastest at an 8.22% CAGR through 2031.

- By deployment model, on-premise solutions commanded 67.12% share of the North America IT Services market size in 2025, but cloud deployment is advancing at a 8.71% CAGR.

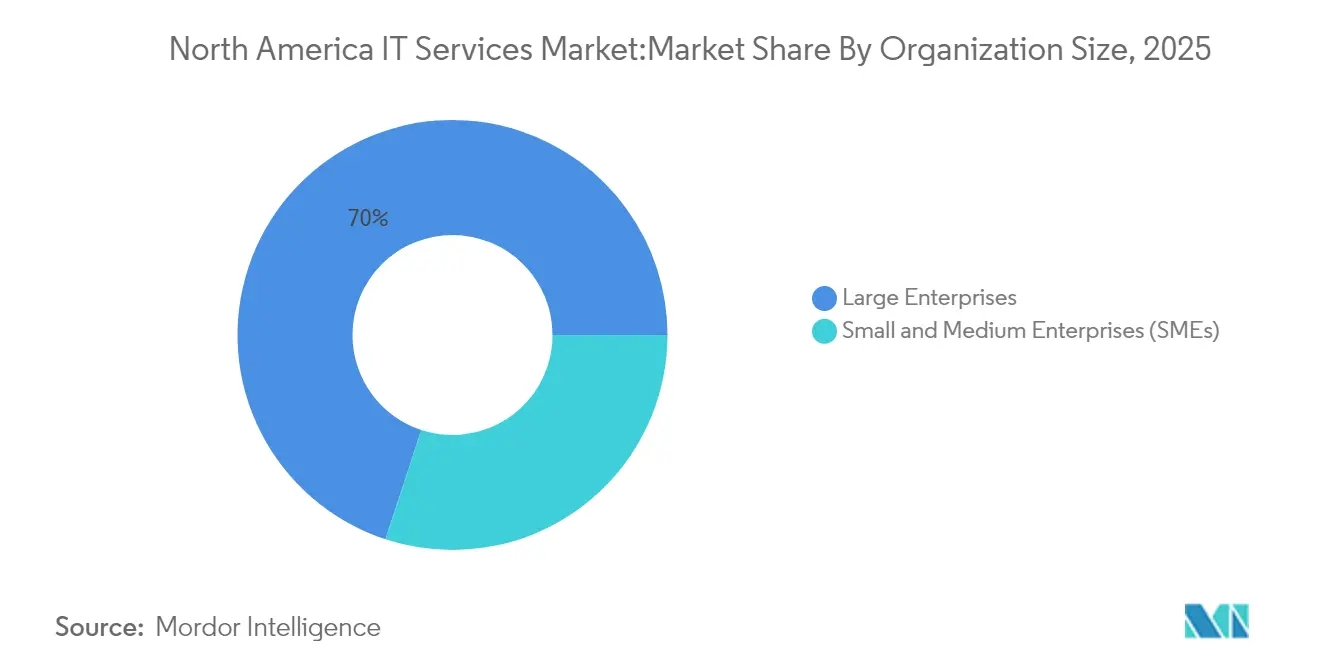

- By organization size, large enterprises held 69.95% revenue share in 2025, whereas SMEs are poised to grow at an 8.36% CAGR through 2031.

- By end-user industry, BFSI captured 29.55% of the North America IT Services market size in 2025; healthcare and life sciences is tracking the highest CAGR at 7.42% through 2031.

- By country, the United States retained 40.60% of North America IT Services market share in 2025, while Canada is projected for an 7.86% CAGR to 2031.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of 2026.

North America IT Services Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Acceleration of enterprise-wide digital transformation | +2.1% | North America and EU | Medium term (2-4 years) |

| Rapid cloud and hybrid-multi-cloud migration | +1.8% | Global, early gains in US, Canada | Short term (≤2 years) |

| Escalating cyber-security and zero-trust adoption | +1.4% | North America core, spill-over LATAM | Medium term (2-4 years) |

| Near-shore talent hubs ease US skills gap | +0.9% | US-LATAM corridor, Canada-Mexico | Long term (≥4 years) |

| Outcome-based pricing unlocks mid-market demand | +0.7% | North America, expanding Mexico | Medium term (2-4 years) |

| Managed GenAI accelerators as a service | +1.2% | US-led, Canada following | Short term (≤2 years) |

| Source: Mordor Intelligence | |||

Acceleration of Enterprise-Wide Digital Transformation

Seventy-two percent of digital leaders expect bigger 2025 budgets, signaling that transformation has evolved into full business-model reinvention. North American firms spend an average of USD 33 million annually on IT, reflecting higher adoption rates and labor costs. Contracts increasingly embed AI-driven decision support, autonomous operations, and real-time customer-engagement platforms, granting providers multi-year revenue visibility.

Rapid Cloud and Hybrid-Multi-Cloud Migration

Hybrid architectures balance performance, compliance, and cost across hyperscalers; 75% of IT workloads are forecast to run in the cloud by 2027. Enterprises adopt multi-cloud to avoid vendor lock-in, prompting demand for orchestration and governance services. The top three hyperscalers hold 67% market share, yet users diversify to lower concentration risk.

Escalating Cyber-Security and Zero-Trust Adoption

Ninety percent of cloud-migrating organizations embrace zero-trust, but only 22% of IT leaders feel confident about their cloud security posture[1]Zscaler, “Zero-Trust State of Adoption 2024,” zscaler.com. US federal Executive Order 14028 requires agencies to implement zero-trust, catalyzing private-sector adoption.

Near-Shore Talent Hubs Ease US Skills Gap

The US faces a projected 1.2 million developer shortfall by 2026, motivating enterprises to tap Latin American hubs where Mexico alone supports 723,000 software engineers. Near-shoring delivers 25%-40% savings and aligns working hours, accelerating 20% annual outsourcing growth.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Data-sovereignty and compliance complexity | -1.6% | US-EU corridors, global | Long term (≥4 years) |

| Acute talent shortage and wage inflation | -2.3% | North America core, near-shore hubs | Medium term (2-4 years) |

| Carbon-disclosure rules hinder data-center outsourcing | -0.8% | North America and EU | Medium term (2-4 years) |

| Higher interest-rate-driven contract risk aversion | -1.1% | North America, spill-over Canada | Short term (≤2 years) |

| Source: Mordor Intelligence | |||

Data-Sovereignty and Compliance Complexity

Fragmented privacy rules are forcing enterprises to operate overlapping frameworks that raise cost and architectural complexity. Region-specific mandates such as enhanced AI transparency rules in the EU and state-level statutes in California, Oregon, and Texas demand localized processing and real-time auditability. Multi-cloud environments must integrate data-localization controls, adding orchestration overhead[2]Secure Privacy, “US State-Level Privacy Tracker,” secureprivacy.ai. Specialized governance platforms and legal advisory services are increasingly bundled into transformation deals, influencing project timelines and pricing in the North America IT Services market.

Acute Talent Shortage and Wage Inflation

Median IT wages are projected to rise 3.3% in 2025, with AI and software engineering premiums exceeding 5%. Scarcity-driven salary inflation squeezes provider margins and lifts project costs for clients. Upskilling programs, low-code automation, and academic alliances are mitigating the gap but cannot fully offset near-term pressure. Labor scarcity remains the single largest brake on delivery capacity across the North America IT Services industry.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Service Type: Consulting Drives Transformation Complexity

IT consulting and implementation held 45.02% of North America IT Services market share in 2025, underlining the premium placed on strategic guidance and change management. Engagements now encompass AI-infused business-process redesign, regulatory alignment, and data-governance blueprints. Managed services, forecasting an 8.22% CAGR, capture demand for predictable, outcome-linked operations across hybrid estates. Growth is fueled by AI-enabled service desks, AIOps platforms, and proactive incident prevention. The IT outsourcing segment remains resilient, offering cost optimization and access to scarce skills, while BPO is evolving toward intelligent automation. Emergent categories such as AI-as-a-service and quantum advisory signal future white-space, though they collectively account for a modest slice of the current North America IT Services market.

Providers are reshaping portfolios via M&A, deploying roughly USD 20 billion annually to bolt on automation, cybersecurity, and vertical-domain capabilities. Successful integrators standardize delivery frameworks early, accelerate cross-selling, and embed unified service catalogs. Those who stumble on post-merger integration leave value on the table for nimble competitors.

By Deployment Model: Hybrid Architectures Reshape Infrastructure

On-premise installations still represent 67.12% of 2025 revenue, but their role has shifted to anchor nodes within highly distributed fabrics. The cloud cohort, slated for parity by 2031 on a 8.71% CAGR, centers on workload portability, data-resident compliance, and elastic scaling for AI training. The North America IT Services market size for cloud services is expanding fastest in regulated verticals, where sovereign-cloud variants provide compliance assurance without sacrificing hyperscale benefits.

Market-leading providers differentiate through end-to-end observability, edge-to-core data integration, and cross-platform policy enforcement. Demand is especially strong for re-platforming legacy applications onto Kubernetes, implementing service mesh architectures, and instituting FinOps practices that optimize spend against value benchmarks.

By Organization Size: SMEs Accelerate Digital Adoption

Large enterprises generated 69.95% of 2025 revenue by orchestrating multi-tower transformation programs spanning cloud modernization, AI analytics, and zero-trust security. Yet SMEs, propelled by an 8.36% CAGR, are the fastest-expanding customer cohort as self-service cloud portals and outcome-based contracts level the playing field. The North America IT Services market size for SME-focused offerings is buoyed by bundled managed services that simplify compliance and cybersecurity.

Providers targeting this segment streamline onboarding through automation, standardized templates, and verticalized best-practice libraries. Price transparency, modular add-ons, and pay-as-you-grow options resonate with budget-conscious owners, driving penetration in manufacturing, professional services, and digital-native retail.

By End-User Industry: Financial Services Lead Digital Investment

BFSI contributed 29.55% of North America IT Services market size in 2025, driven by mandates to modernize payment rails, combat fraud, and comply with evolving regulations. Banks are embedding AI into underwriting and KYC, adopting blockchain for settlement, and migrating core platforms to cloud environments certified for high-risk workloads. Healthcare and life sciences, posting a 7.42% CAGR, accelerates digital front-door initiatives, clinical decision support, and data-driven research. Providers with HIPAA-aligned architectures and FDA-compliant validation services win share.

Government programs prioritize citizen-experience portals, cybersecurity hardening, and open-data initiatives, sustaining stable spend despite budget scrutiny. Manufacturing invests in Industry 4.0—IoT sensors, digital twins, and predictive maintenance—while retail focuses on supply-chain visibility and omnichannel personalization. Cross-industry, demand converges on AI governance, data-trust frameworks, and sustainability analytics.

Geography Analysis

The United States anchors the North America IT Services market, delivering unabated demand across Fortune 500 modernization programs, mid-market cloud migrations, and federal-agency cyber mandates. Project pipelines concentrate on AI-assisted DevOps, low-code platform roll-outs, and secure software supply chain frameworks. Government incentives for semiconductor reshoring and critical-infrastructure hardening amplify spending on edge computing and OT security.

Canada’s growth outpaces regional averages as public-sector modernization dovetails with private-sector AI experimentation in fintech, clean-tech, and digital commerce. The Canadian cybersecurity space, valued at USD 12.96 billion in 2024, is driving vendor investment in SOC-as-a-service and zero-trust consulting. Government sponsorship of quantum research labs seeds next-generation opportunities, although a 3.2% pullback in federal S&T budgets for 2024 introduces short-term funding pressure.

Mexico’s momentum stems from its expanding engineer base, stable macro-fundamentals, and proximity to US demand centers. Hybrid-cloud adoption in the country is forecast to rise from 45% in 2024 to 58% by 2026, fueling demand for migration, managed security, and latency-optimized network services. Hyperscaler commitments from Microsoft, Google, and AWS are turning the region into a data-center hub, although energy-supply constraints and skills availability remain watchpoints. With AI spending expected to rise 2.4 times by 2025, Mexico offers providers both delivery-center leverage and a growing domestic client base.

Competitive Landscape

Competitive intensity remains high yet structurally nuanced. Global integrators—IBM, Accenture, and Microsoft—maintain breadth across consulting, cloud, and managed services, capturing scale efficiencies and wallet share. Mid-tier challengers leverage deep vertical expertise and platform-centric delivery to outmaneuver larger rivals in specific niches. Annual deal flow of roughly 100 acquisitions worth USD 20 billion underscores a race to secure advanced analytics, cybersecurity, and automation capabilities.

Despite the volume, fewer than 20% of acquisitions fully unlock cross-sell synergies, creating an opening for agile firms with disciplined integration playbooks. Cloud-native entrants harness infrastructure-as-code, AIOps, and DevSecOps pipelines to deliver faster, cheaper, and more transparent services. Near-shore specialists combine cost competitiveness with aligned time zones, while AI-native consultancies exploit proprietary large-language-model frameworks to accelerate delivery and differentiate intellectual property.

Strategic investments focus on outcome-based service frameworks, AI-driven service catalogs, and sustainability dashboards that quantify carbon savings. Providers embedding predictive analytics into managed contracts can guarantee uptime and performance, translating technical SLAs into board-level KPIs. Emerging battlegrounds include hybrid-cloud data-fabric orchestration, AI ethics and compliance advisory, and industry-specific digital twins.

North America IT Services Industry Leaders

IBM

Microsoft Corporation

TCS Limited

Wipro Limited

Amazon Web Services (AWS) Professional Services

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- June 2025: Shield Technology Partners raised over USD 100 million to expand its US network and AI-enabled managed services, partnering initially with four regional firms.

- June 2025: NWN Corporation acquired InterVision Systems to bolster customer-experience, cybersecurity, and intelligent-infrastructure offerings.

- April 2025: H.I.G. Capital merged Converge Technology Solutions and Mainline Information Systems, forming Pellera Technologies in a USD 910 million deal.

- March 2025: CGI purchased Momentum Technologies, adding 250 analytics professionals to strengthen AI and BI services.

North America IT Services Market Report Scope

North America IT services leverage technology and business expertise to help organizations create, manage, and optimize the information and business processes.

The North America IT Services Market is segmented by Type (IT Consulting & Implementation, IT Outsourcing, Business Process Outsourcing), End-user (Manufacturing, Government, BFSI, Healthcare, Retail & Consumer Goods, Logistics), and Country.

The market sizes and forecasts are provided in terms of value (USD million) for all the above segments.

By Service Type

| IT Consulting and Implementation |

| Managed Services |

| IT Outsourcing (ITO) |

| Business Process Outsourcing (BPO) |

| Other Service Types |

By Deployment Model

| On-premise |

| Cloud |

By Organization Size

| Large Enterprises |

| Small and Medium Enterprises (SMEs) |

By End-user Industry

| BFSI |

| Government and Public Sector |

| Manufacturing |

| Healthcare and Life Sciences |

| Retail and Consumer Goods |

| Logistics and Transportation |

| Other End-user Industries |

By Country

| United States |

| Canada |

| Mexico |

| By Service Type | IT Consulting and Implementation |

| Managed Services | |

| IT Outsourcing (ITO) | |

| Business Process Outsourcing (BPO) | |

| Other Service Types | |

| By Deployment Model | On-premise |

| Cloud | |

| By Organization Size | Large Enterprises |

| Small and Medium Enterprises (SMEs) | |

| By End-user Industry | BFSI |

| Government and Public Sector | |

| Manufacturing | |

| Healthcare and Life Sciences | |

| Retail and Consumer Goods | |

| Logistics and Transportation | |

| Other End-user Industries | |

| By Country | United States |

| Canada | |

| Mexico |

Key Questions Answered in the Report

What is the current size of the North America IT Services market?

The market reached USD 591.58 billion in 2026 and is projected to grow to USD 836.31 billion by 2031 at a 7.17% CAGR.

Which service type holds the largest share?

IT consulting and implementation leads with 45.02% of 2025 revenue, reflecting demand for strategic guidance in complex transformation programs.

Why are managed services growing faster than other segments?

Outcome-based pricing, AI-powered service automation, and the need for 24/7 hybrid-cloud management are driving an 8.22% CAGR in managed services.

Which country is the fastest-growing market?

Canada is forecast to expand at an 7.86% CAGR through 2031 thanks to supportive government digital strategies and rising cybersecurity investment.

What is the biggest restraint on market growth?

A severe talent shortage is inflating wages and limiting delivery capacity, trimming the CAGR outlook by an estimated 2.3%.

How are providers differentiating in a crowded competitive landscape?

Leading firms embed AI into service delivery, invest in near-shore talent hubs, and adopt outcome-based contracts that tie fees to client business results.

Page last updated on: