Market Overview

| Study Period | 2020 - 2031 |

|---|---|

| Forecast Data Period | 2026 - 2031 |

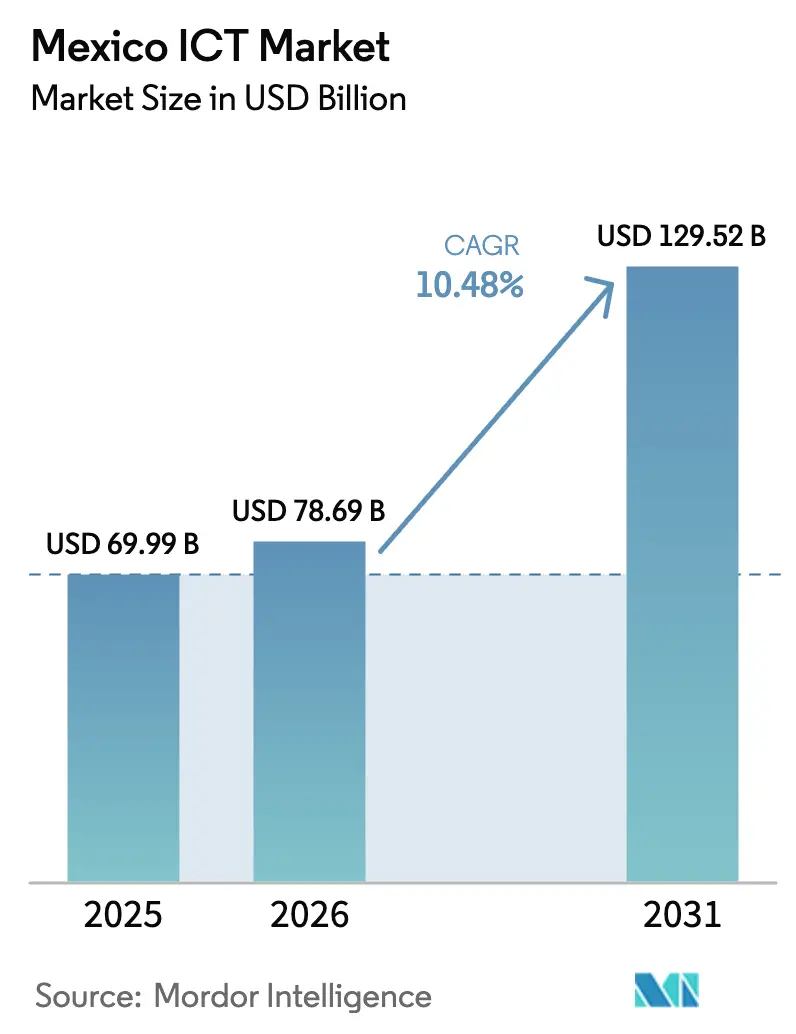

| Base Year Market Size (2025) | USD 69.99 Billion |

| Market Size (2026) | USD 78.69 Billion |

| Market Size (2031) | USD 129.52 Billion |

| Growth Rate (2026 - 2031) | 10.48% CAGR |

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

Mexico ICT Market Analysis by Mordor Intelligence

The Mexico ICT Market size is projected to expand from USD 69.99 billion in 2025 and USD 78.69 billion in 2026 to USD 129.52 billion by 2031, registering a CAGR of 10.48% between 2026 to 2031. Rapid nearshoring, a centralized National Digital Strategy, and hyperscaler commitments worth more than USD 6 billion have tilted enterprise budgets toward cloud, cybersecurity, and managed services. Federal funding of MXN 3.85 billion (USD 193 million) for the new Agencia de Transformación Digital y Telecomunicaciones is streamlining spectrum policy and accelerating e-government rollouts. Foreign direct investment related to nearshoring reached USD 35 billion in 2023, and IT services captured almost one-fifth of that inflow. Hyperscaler regions in Querétaro and Monterrey are drawing workloads out of on-premises silos, while Spanish-language AI models are expanding the software addressable market and heightening demand for data-sovereign platforms.

Key Report Takeaways

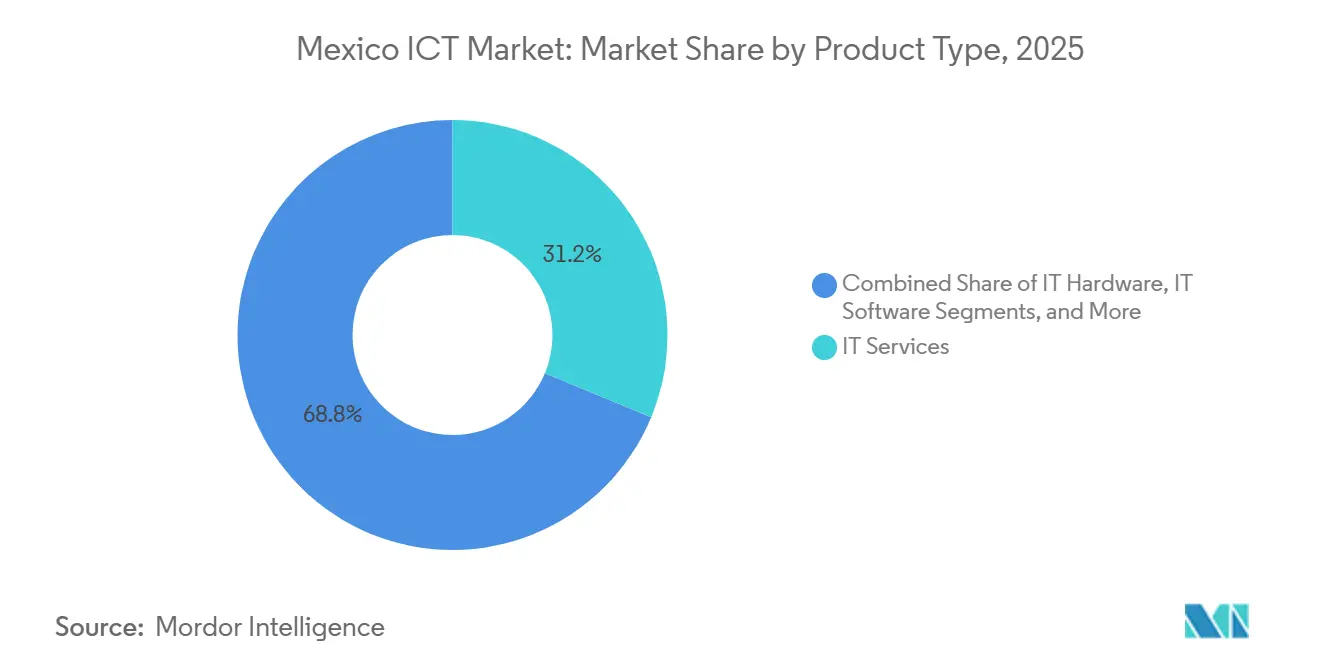

- By product type, IT Services led with 31.24% of Mexico ICT market share in 2025, while IT Security and Cybersecurity is projected to expand at an 11.28% CAGR through 2031.

- By enterprise size, Large Enterprises held 58.91% of spending in 2025, and Small and Medium-sized Enterprises are advancing at an 11.76% CAGR through 2031.

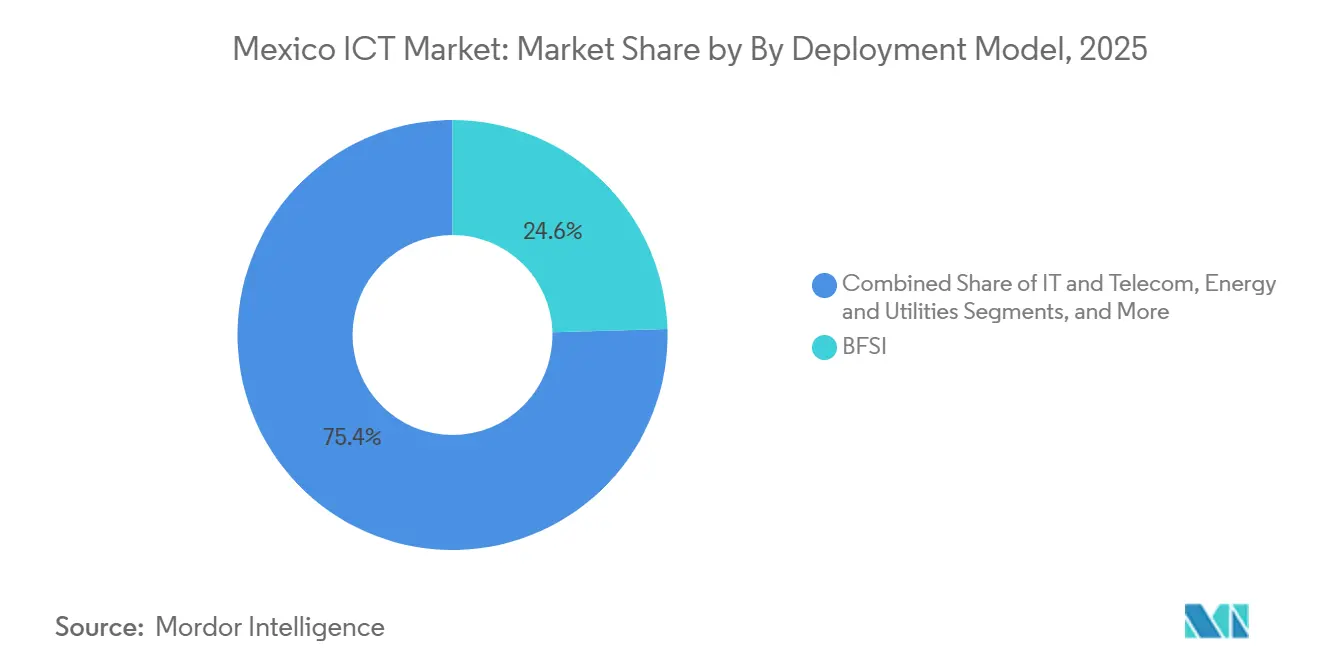

- By industry vertical, BFSI accounted for 24.56% of the Mexico ICT market size in 2025 and Healthcare and Life Sciences is forecast to grow at a 12.41% CAGR to 2031.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of 2026.

Mexico ICT Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Government Digital Transformation Push Through National Digital Agenda | +1.8% | National, with early gains in Mexico City, Jalisco, Nuevo León | Medium term (2-4 years) |

| Rapid Expansion of Fiber Optic Backbone and 5G Rollout | +2.1% | National, concentrated in Querétaro, Monterrey, Guadalajara, Mexico City | Short term (≤ 2 years) |

| Accelerating Cloud Adoption Among Mexican SMEs | +1.5% | National, with higher penetration in urban centers | Medium term (2-4 years) |

| Nearshoring of IT Services as US Companies Diversify Supply Chains | +2.3% | National, strongest in border states and Bajío region | Long term (≥ 4 years) |

| Growth of Fintech Sandbox Regulations Fueling BFSI IT Spending | +1.2% | National, concentrated in Mexico City, Monterrey, Guadalajara | Short term (≤ 2 years) |

| Rise of Spanish-Language AI Models Driving New Software Demand | +0.9% | National, with spillover to Central America | Medium term (2-4 years) |

| Source: Mordor Intelligence | |||

Nearshoring of IT Services as US Companies Diversify Supply Chains

Nearshoring is the single largest external tailwind for the Mexico ICT market, channeling 18% of USD 35 billion in 2023 FDI directly into IT services.[1]International Monetary Fund, “Regional Economic Outlook - Western Hemisphere,” imf.org Automotive and electronics clusters in Querétaro and Guanajuato demand bilingual support, cloud-based ERP, and security operations that align with United States compliance norms. Global integrators expanded Mexican delivery centers to match U.S. time zones, but rising wages in Guadalajara have pushed vendors toward Mérida and Puebla for secondary capacity. Softtek’s January 2025 alliance with Intel adds AI-accelerated toolkits for edge workloads and cements Mexico’s positioning in regional Industry 4.0 supply chains. As the United States raises reshoring incentives, the Mexico ICT market is likely to lock in multi-year contracts that hedge geopolitical risk for North American enterprises.

Rapid Expansion of Fiber Optic Backbone and 5G Rollout

America Móvil’s 5G footprint in 125 cities and private-sector fiber routes exceeding 4,000 kilometers give the Mexico ICT market nationwide low-latency coverage. AWS, Microsoft, and Oracle selected Querétaro because new cross-border links deliver sub-25 millisecond round-trip times to Texas workloads. Dedicated wholesale network Red Compartida already reaches 92% of the population, although restructuring talks underline the importance of sustainable wholesale models. New fiber corridors slash transport costs for hyperscalers, encourage regional edge nodes for manufacturing analytics, and pull traditional MPLS networks toward software-defined alternatives. Combined, these investments lift bandwidth supply faster than demand, depressing per-megabit pricing but widening the feasible customer base for cloud and cybersecurity subscriptions.

Government Digital Transformation Push Through National Digital Agenda

The 2025 dissolution of the Instituto Federal de Telecomunicaciones and the birth of the Agencia de Transformación Digital y Telecomunicaciones signaled political commitment to a unified digital agenda. A new MXN 3.85 billion budget emphasizes spectrum auctions, rural broadband, and a national cybersecurity framework aligned with ISO 27001. The one-stop Ventanilla Única Nacional portal cut business registration time from eight days to two hours, showcasing how process re-engineering can rapidly spike e-government demand. Uncertainty around agency independence persists, yet vendors report shorter procurement cycles and clearer RFP scopes. As ministries modernize, the Mexico ICT market benefits from predictable project pipelines and mandated interoperability standards.

Accelerating Cloud Adoption Among Mexican SMEs

Cloud platforms have lowered capital barriers for SMEs, driving an 11.76% CAGR in their ICT outlays. Microsoft found that 64% of Mexican SMEs embedded AI tools in 2024, and 73% plan to continue investment. Hyperscaler startup credits further dilute onboarding costs, while Aprendices Digitales México aims to upskill 200,000 workers by 2026. Nevertheless, only 44% of micro and small businesses maintain an internet connection, highlighting a ceiling on cloud addressability. As fiscal reform nudges these enterprises into formal channels, latent demand could convert rapidly, providing a sizable upside for the Mexico ICT market during the next planning cycle.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Persistent Informal Economy Limiting IT Formalization | -1.4% | National, most acute in rural and semi-urban areas | Long term (≥ 4 years) |

| Cybersecurity Skills Shortage and High Talent Turnover | -1.1% | National, concentrated in Mexico City, Monterrey, Guadalajara | Short term (≤ 2 years) |

| Electricity Grid Instability in Industrial Clusters | -0.7% | Nuevo León, Guanajuato, Estado de México | Medium term (2-4 years) |

| Bureaucratic Procurement Cycles Slowing Public IT Projects | -0.6% | National, federal and state agencies | Medium term (2-4 years) |

| Source: Mordor Intelligence | |||

Persistent Informal Economy Limiting IT Formalization

The informal sector clouds revenue visibility for roughly half of Mexican micro and small enterprises, limiting the pool of potential customers for software-as-a-service and managed IT solutions.[2]Instituto Nacional de Estadística y Geografía, “National Survey on Micro, Small and Medium Enterprises,” inegi.org.mx The Régimen Simplificado de Confianza attracted only 2.1 million taxpayers by mid-2024, far below potential, limiting incentives to adopt formal digital tools. Platform usage often stalls at social media messaging rather than integrated commerce or ERP, shrinking the immediate TAM for the Mexico ICT market. Credit scarcity reinforces the cycle, as subscription financing hinges on verifiable income streams. Until compliance simplification or stricter enforcement shifts the calculus, informality will dilute growth outside major urban corridors.

Cybersecurity Skills Shortage and High Talent Turnover

Fortinet reported that 61% of Mexican organizations could not hire required cybersecurity staff in 2024, with turnover surpassing 25% annually as U.S. firms poach remote talent. Universities produce fewer than 5,000 specialists each year, while national demand calls for triple that number. Outsourcing to managed security service providers plugs immediate gaps but prolongs incident-response cycles and erodes in-house know-how. Rising attack frequency, federal agencies expect a 260% spike through 2025, magnifying risk exposure. Without a deep bench of analysts, enterprises will continue to pay premium retainers, pushing cost ratios higher even as the Mexico ICT market expands.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Product Type: Security Spending Outpaces Legacy Infrastructure

IT Security and Cybersecurity is the fastest-moving slice of the Mexico ICT market, advancing at an 11.28% CAGR on the back of a projected 260% jump in government-targeted cyberattacks and an enduring talent gap. IT Services, which commanded 31.24% of Mexico ICT market share in 2025, still drives the bulk of consulting and outsourcing revenue, buoyed by hyperscaler launches that require migration and optimization expertise. Hardware growth lags as enterprises pivot from capex-heavy servers to opex-based public clouds, yet demand for ruggedized edge devices in manufacturing keeps the market alive. Software uptake is accelerating because Spanish-language AI models eliminate linguistic bottlenecks and satisfy data-residency mandates.

Hyperscalers subsidize onboarding, shrinking payback periods, and opening multi-cloud orchestration opportunities for integrators. Telecom incumbents have responded by embedding AI assistants into mobile ecosystems to defend shrinking voice and data margins. As clients consolidate vendors, integrated managed services and security bundles are becoming table stakes, reshaping account-retention strategies. Consequently, the Mexico ICT market size for managed detection and response platforms is projected to rise in tandem with zero-trust adoption, while appliance-centric network spending continues to taper.

By Enterprise Size: SMEs Narrow the Digital Divide

Large Enterprises controlled 58.91% of 2025 spend, but Small and Medium-sized Enterprises are the fastest-growing buyers, expanding 11.76% annually. Reduced hardware obligations, tiered cloud pricing, and government-sponsored upskilling have chipped away at historical barriers. Yet only 44% of SMEs connect to the internet, underscoring how core infrastructure deficits still fence off portions of the Mexico ICT market.

The SME surge gives hyperscalers a long-tail growth engine, while fintech sandboxes encourage the development of payment, lending, and invoicing apps designed for resource-constrained businesses. Credit bottlenecks and cyber-risk awareness remain hurdles, but SaaS vendors are countering with micro-subscriptions, pay-as-you-grow tiers, and bundled endpoint security. If connectivity gaps close, SME digitalization could lift the Mexico ICT market size by several billion dollars beyond current projections.

By Industry Vertical: Healthcare Surges on Regulatory Mandates

Healthcare and Life Sciences is the speed leader, expanding at a 12.41% CAGR as NOM-024 mandates electronic health record interoperability and teleconsultations reach 45% of physicians.[3]Coalition for Digital Health Mexico, “Telemedicine Adoption and NOM-024 Compliance Study,” cosadim.org BFSI retained a 24.56% share in 2025, propped up by 89 fintech sandbox approvals and aggressive mobile banking rollouts. Core banking modernization and anti-fraud analytics remain evergreen spending categories, yet growth has moderated where digital wallets already saturate urban consumers.

Manufacturing’s pivot to nearshoring is driving demand for industrial IoT and predictive maintenance, bolstering edge computing sales. Retail and logistics invest in omnichannel stacks to support nationwide same-day delivery, while energy and utilities adopt SCADA upgrades to hedge against grid instability. Across these sectors, AI-powered Spanish-language software lowers localization costs, offering a silver lining amid regulatory data-sovereignty constraints. The Mexico ICT market continues to draw cross-vertical interest, but healthcare’s mandate-driven urgency keeps it at the forefront of growth.

Geography Analysis

Hyperscaler investments have concentrated the Mexico ICT market in the Bajío corridor and northern industrial states, leaving a governance and connectivity gap in the south. Querétaro hosts three AWS availability zones, Microsoft’s Azure region, and one of two Oracle Cloud Infrastructure sites, making the state a Tier-1 cloud nucleus. Datacenter clustering has catalyzed auxiliary ecosystems of managed service providers, integrators, and ISPs that co-locate to trim latency.

Monterrey complements this core with cross-border fiber paths to Texas, a dense pool of engineering talent, and Oracle’s second OCI region, attracting automotive and financial workloads that require sub-20 millisecond round-trip times. Guadalajara, the historic tech hub, still hosts major R&D centers but faces wage inflation that is driving secondary-city expansion to Mérida and Puebla. Mexico City dominates financial and federal IT budgets, yet seismic risk, water scarcity, and real estate costs curb hyperscaler construction, explaining the capital’s smaller share of recent data center announcements.

Rural and semi-urban areas lag; only 44% of SMEs are online, and Red Compartida’s 92% population coverage has not translated into proportional subscription uptake.[4]Center for Strategic and International Studies, “Mexico’s Telecommunications Regulatory Reform,” csis.org The imbalance mirrors GDP concentration, five states account for roughly 60% of ICT outlays. New cross-border fiber routes, such as C3ntro Telecom’s 2,500-kilometer Phoenix-to-Querétaro line due in 2026, are prioritizing export corridors over last-mile rural access. Unless shared infrastructure models improve rural economics, the Mexico ICT market will continue to be an urban-skewed opportunity.

Competitive Landscape

Competition inside the Mexico ICT market is intensifying but remains moderately fragmented. Hyperscalers own the infrastructure-as-a-service layer, using sovereign data commitments and training programs to deepen local roots. Global integrators such as IBM and Accenture wrap consulting, DevOps, and managed security around those platforms, blending onsite governance with offshore cost efficiency. Domestic champions Softtek, KIO Networks, and Alestra leverage cultural fluency and public-sector ties, although migration incentives from larger cloud providers are compressing reseller margins.

Telecom incumbents are reinventing revenue lines, embedding generative AI into mobile offerings to offset stagnant voice and data growth. Edge computing and Spanish-language LLMs are emerging white spaces. LatAmGPT’s open-access release enables sector-specific software for legal, medical, and customer service workflows without cross-border data exposure. Cybersecurity-as-a-service is also scaling quickly, as 61% of organizations cannot fill in-house roles, driving double-digit growth in managed detection and response bookings.

Oracle’s Guadalajara development center, which filed 48 patents in 2025, underscores a strategy to embed proprietary innovation, raising switching costs in a multi-cloud era. Regulatory uncertainty following the regulator’s consolidation in 2025 could tilt the playing field toward incumbents, but the overall trend points to a more competitive, services-heavy Mexico ICT market as clients seek vendor neutrality and cost visibility.

Mexico ICT Industry Leaders

América Móvil S.A.B. de C.V.

IBM Corporation

Microsoft Corporation

Softtek Servicios Corporativos S.A. de C.V.

Oracle Corporation

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- January 2026: Amazon Web Services opened the Mexico Central region in Querétaro, part of a USD 5 billion investment that also funds cloud-skills training for 200,000 workers by 2026.

- December 2025: KIO Networks launched its 12 MW QRO2 datacenter in Querétaro, bringing its state footprint to 19 MW under a USD 400 million regional expansion plan.

- September 2025: Microsoft committed USD 1.3 billion to scale its Querétaro cloud region and AI services, reinforcing data-residency assurances.

- May 2025: Microsoft activated its Querétaro data center region, providing in-country Azure availability for latency-sensitive workloads.

Mexico ICT Market Report Scope

Information and Communication Technologies or ICT is a broader term for Information Technology (IT). It refers to all communication technologies, such as wireless networks, the internet, computers, cell phones, software, videoconferencing, middleware, social networking, and other media applications and services enabling users to store, access, transmit, retrieve, and manipulate information in a digital form.

The Mexico ICT Market Report is Segmented by Product Type (IT Hardware, IT Software, IT Services, IT Infrastructure, IT Security/Cybersecurity, Communication Services), Enterprise Size (Small and Medium-sized Enterprises, Large Enterprises), Industry Vertical (Government and Public Administration, BFSI, IT and Telecom, Energy and Utilities, Retail E-commerce and Logistics, Manufacturing and Industry 4.0, Healthcare and Life Sciences, Oil and Gas, Other Industry Verticals), and Geography (Mexico). The Market Forecasts are Provided in Terms of Value (USD).

By Product Type

| IT Hardware | Computer Hardware |

| Networking Equipment | |

| Peripherals | |

| IT Software | |

| IT Services | IT Consulting and Implementation |

| IT Outsourcing (ITO) | |

| Business Process Outsourcing (BPO) | |

| Managed Security Services | |

| Cloud and Platform Services | |

| IT Infrastructure | |

| IT Security/Cybersecurity | |

| Communication Services |

By Enterprise Size

| Small and Medium-sized Enterprises |

| Large Enterprises |

By Industry Vertical

| Government and Public Administration |

| BFSI |

| IT and Telecom |

| Energy and Utilities |

| Retail, E-commerce, and Logistics |

| Manufacturing and Industry 4.0 |

| Healthcare and Life Sciences |

| Oil and Gas |

| Other Industry Verticals |

| By Product Type | IT Hardware | Computer Hardware |

| Networking Equipment | ||

| Peripherals | ||

| IT Software | ||

| IT Services | IT Consulting and Implementation | |

| IT Outsourcing (ITO) | ||

| Business Process Outsourcing (BPO) | ||

| Managed Security Services | ||

| Cloud and Platform Services | ||

| IT Infrastructure | ||

| IT Security/Cybersecurity | ||

| Communication Services | ||

| By Enterprise Size | Small and Medium-sized Enterprises | |

| Large Enterprises | ||

| By Industry Vertical | Government and Public Administration | |

| BFSI | ||

| IT and Telecom | ||

| Energy and Utilities | ||

| Retail, E-commerce, and Logistics | ||

| Manufacturing and Industry 4.0 | ||

| Healthcare and Life Sciences | ||

| Oil and Gas | ||

| Other Industry Verticals | ||

Key Questions Answered in the Report

What is the current value of the Mexico ICT market?

The market stands at USD 78.69 billion in 2026 and is projected to climb to USD 129.52 billion by 2031.

Which product segment is growing fastest?

IT Security and Cybersecurity leads with an 11.28% CAGR through 2031, fueled by heightened attack volumes and a talent shortage.

How is nearshoring affecting Mexican ICT spending?

Nearshoring channeled about USD 6.3 billion of FDI into IT services in 2023, boosting demand for bilingual support, cloud ERP, and cybersecurity.

Why is Querétaro emerging as a cloud hub?

Dense fiber routes, new hyperscaler regions, and proximity to U.S. markets make Querétaro the lowest-latency option for regional workloads.

What challenges slow ICT adoption among SMEs?

Limited internet connectivity, credit constraints, and cybersecurity skill gaps restrict digital-tool uptake by smaller firms.

Which vertical shows the highest growth rate?

Healthcare and Life Sciences grows at 12.41% CAGR to 2031, propelled by mandatory electronic health-record standards and telemedicine adoption.

Page last updated on: