Chile IT Services Market Size and Share

Market Overview

| Study Period | 2019 - 2030 |

|---|---|

| Forecast Data Period | 2025 - 2030 |

| Historical Data Period | 2019 - 2023 |

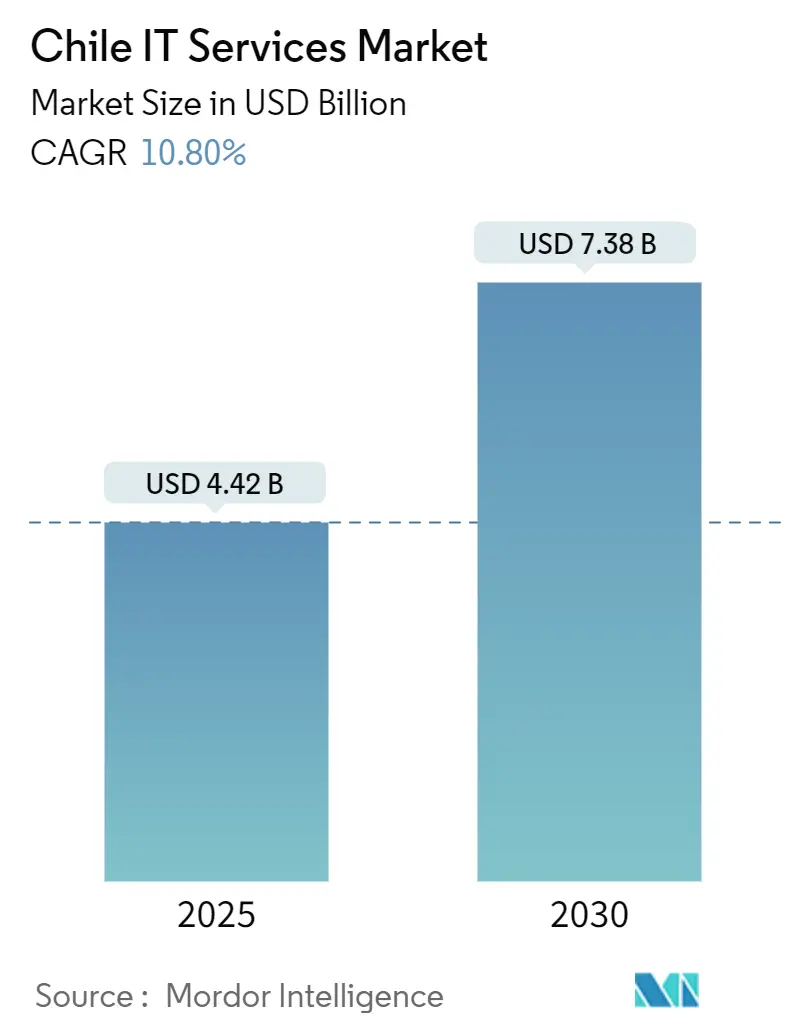

| Market Size (2025) | USD 4.42 Billion |

| Market Size (2030) | USD 7.38 Billion |

| Growth Rate (2025 - 2030) | 10.80% CAGR |

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

Chile IT Services Market Analysis by Mordor Intelligence

The Chile IT Services market size reached USD 4.42 billion in 2025 and is projected to grow to USD 7.38 billion by 2030, reflecting a strong 10.8% CAGR. This expansion underscores the country’s emergence as a regional technology hub, accelerated by public cloud migration, government digitization mandates, and sustained near-shore demand from United States West Coast clients. Enterprises continue to shift workloads toward cloud platforms to improve flexibility and resilience, while the new Cybersecurity Framework Law is driving a parallel surge in demand for managed security offerings. Competitive pricing of USD 50-65 per developer hour and Chile’s well-established intellectual-property protections strengthen the country’s attractiveness for offshore engagements. Meanwhile, fast-growing sectors such as healthcare, retail, and mining automation are widening the scope of domestic technology spending and creating opportunities for multi-service providers.[1]Library of Congress, “Chile: Framework Law on Cybersecurity Comes into Force,” loc.gov

Key Report Takeaways

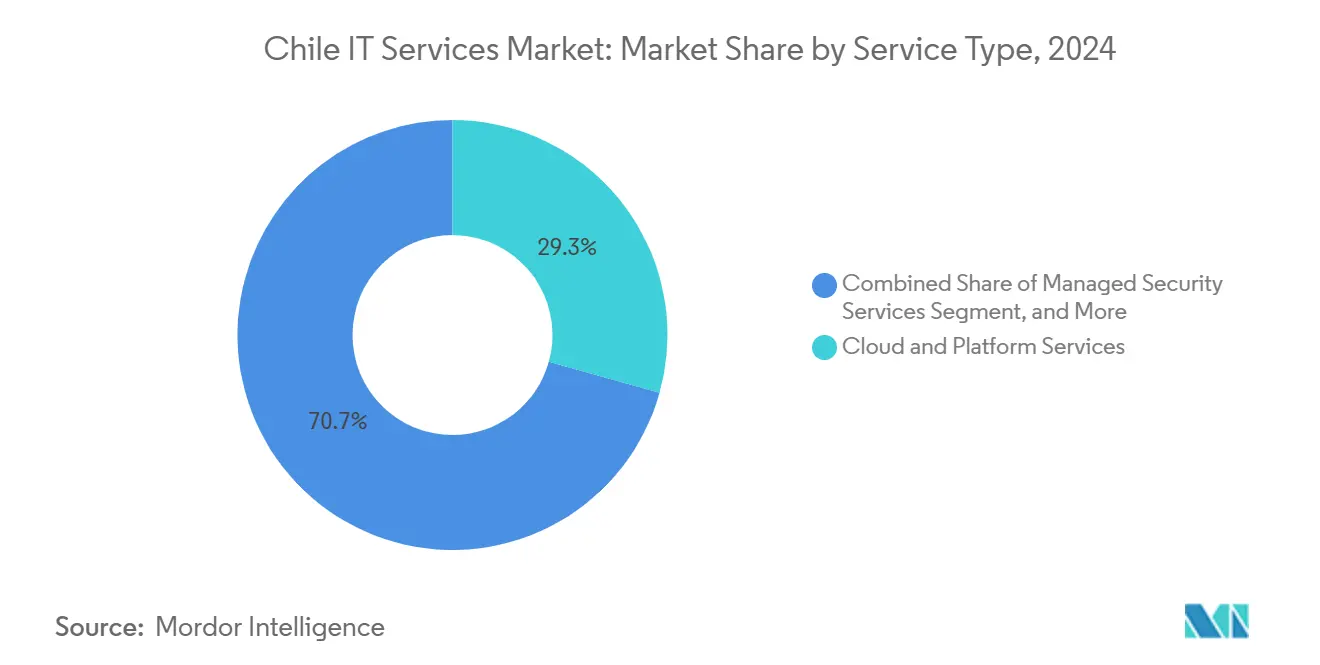

- By service type, Cloud and Platform Services led with 29.33% revenue share of the Chile IT Services market in 2024, and Managed Security Services is advancing at a 15.31% CAGR through 2030.

- By enterprise size, Large Enterprises commanded 63.11% of the Chile IT Services market share in 2024, while Small and Medium Enterprises are forecast to expand at a 13.76% CAGR to 2030.

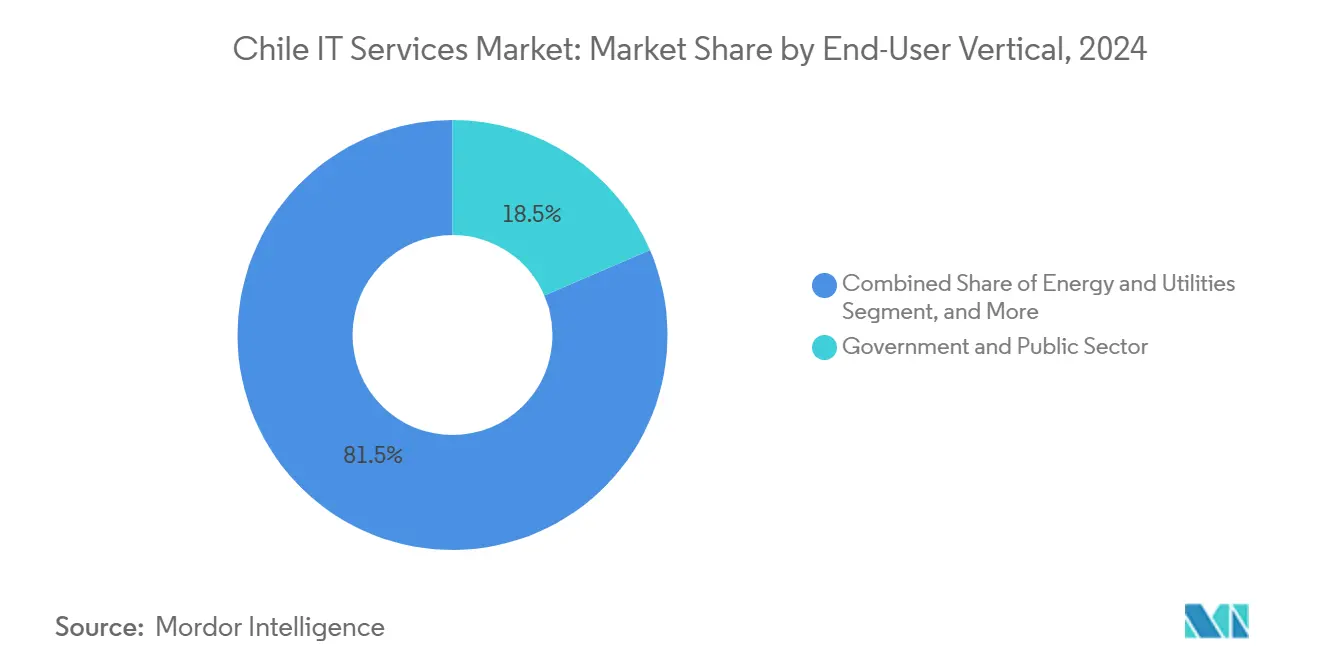

- By end-user vertical, Government and Public Sector held 18.53% of the Chile IT Services market size in 2024 and Healthcare and Life-Sciences is progressing at a 14.5% CAGR through 2030.

- By deployment model, Hybrid or Multi-cloud configurations controlled 46.67% of the Chile IT Services market share in 2024 and Public Cloud workloads are projected to rise at a 15.67% CAGR to 2030.

Chile IT Services Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Accelerated public-cloud migration in regulated verticals | +2.80% | National, with early gains in Santiago, Valparaíso, Concepción | Medium term (2-4 years) |

| National "Digital Government 2025" program spend-outs | +2.10% | National | Short term (≤ 2 years) |

| Near-shore delivery demand from US West Coast clients | +1.90% | National, concentrated in Santiago tech corridor | Long term (≥ 4 years) |

| Rapid 5G roll-out unlocking edge-services projects | +1.60% | National, prioritizing urban centers | Medium term (2-4 years) |

| Copper-mining automation mandates (OT-IT convergence) | +1.40% | Northern regions (Antofagasta, Atacama) | Long term (≥ 4 years) |

| Gen-AI pilots across Spanish-language contact-centers | +1.20% | National | Short term (≤ 2 years) |

| Source: Mordor Intelligence | |||

Accelerated Public-Cloud Migration in Regulated Verticals

Financial institutions are moving core platforms to public cloud to lower operating cost and introduce real-time analytics capabilities. Banco Itaú plans a full infrastructure migration by 2028 and Bci already runs a cloud-based data platform that ingests customer data for generative AI models.[2]BNamericas, “Amazon to invest US$4bn in Chile cloud infrastructure,” bnamericas.com A new data-protection statute effective December 2026 clarifies cross-border processing rules and encourages hybrid architectures that combine hyperscaler regions with local data centers. Energy providers are using similar frameworks to expand cloud-native security operations centers.

National Digital Government 2025 Program Spend-Outs

Public procurement exceeded USD 16 billion in 2023, and the Digital Transformation of the State Law mandates cloud, analytics, and cybersecurity adoption across agencies.[3]ChileCompra, “Compras públicas superaron los US$16 mil millones en 2023,” chilecompra.cl The Mercado Público platform already lists more than 5,000 IT opportunities annually and introduces ethical guidelines for AI projects, creating predictable pipelines for service firms.

Near-Shore Delivery Demand from United States West Coast Clients

Around 50,000 software developers work in greater Santiago, offering time-zone alignment and English proficiency that exceeds most regional peers. Competitive hourly rates provide 60-70% savings over U.S. benchmarks while Chile’s intellectual-property safeguards meet stringent client requirements. Startup Chile graduate companies bolster a culture of agile delivery, further raising the city’s profile as a near-shore alternative.

Rapid 5G Roll-Out Unlocking Edge-Services Projects

Entel committed USD 618 million to mobile and optical backbone upgrades that support 800 Gbit-per-second throughputs, underpinning ultra-low latency workloads. Mining majors such as BHP now deploy Azure-based IoT edge nodes at the Escondida mine for predictive maintenance and autonomous haulage decisions.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Peso-USD volatility squeezing ITO contract margins | -1.80% | National | Short term (≤ 2 years) |

| Cyber-talent attrition to Miami and Madrid hubs | -1.20% | National, concentrated in Santiago | Medium term (2-4 years) |

| Data-sovereignty ambiguity for cross-border cloud BPO | -0.90% | National, affecting multinational clients | Medium term (2-4 years) |

| IT project delays tied to 2023-2024 constitutional reforms | -0.70% | National, concentrated in public sector | Short term (≤ 2 years) |

| Source: Mordor Intelligence | |||

Peso-USD Volatility Squeezing ITO Contract Margins

Sudden exchange-rate swings compress profit on fixed-price outsourcing engagements. Large firms hedge with multi-currency revenue streams, while smaller providers lack the scale to absorb volatility, prompting consolidations.

Cyber-Talent Attrition to Miami and Madrid Hubs

Chile needs roughly 6,000 more cybersecurity professionals yet faces mounting salary competition that pulls talent overseas. The shortage limits provider capacity to deliver managed security solutions even as the new framework law mandates higher compliance.[4]Telefonica Tech, “Profesionales de la Ciberseguridad demandados en 2025,” telefonicatech.com

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Service Type: Cloud Platforms Drive Digital Transformation

Cloud and Platform Services accounted for 29.33% of the Chile IT Services market share in 2024. Managed Security Services are projected to expand at a 15.31% CAGR, benefiting from mandatory breach-reporting rules in the new cybersecurity law. The Chile IT Services market size for Cloud and Platform Services is slated to reach USD 2.3 billion by 2030, while the market size for Managed Security Services could surpass USD 1.2 billion in the same year. Hyperscaler entrants such as Amazon are adding local regions and sparking ecosystem buildouts with ISVs and advisory partners. Domestic integrators answer margin pressure by packaging consulting, outsourcing, and cloud brokerage into unified propositions that accelerate migration and de-risk compliance.

IT Consulting continues to service large-scale ERP rationalization, whereas Business Process Outsourcing leverages bilingual support strength for multinationals. AI enablement layers on top of these traditional lines, especially in voice analytics and robotic process automation that optimize back-office workflows.

By End-User Enterprise Size: SMEs Accelerate Digital Adoption

Large Enterprises held 63.11% of the Chile IT Services market in 2024, underpinned by heavy capex cycles in mining and retail modernization. The Chile IT Services market size for Large Enterprises is projected to touch USD 4.6 billion by 2030. In contrast, SME spending is rising fastest at a 13.76% CAGR as cloud subscription models remove capital barriers. Payment-fintech initiatives spotlight a USD 448 billion regional addressable opportunity, nudging small retailers online. Vendors have responded with modular service bundles and consumption-based billing that align with tight operating cash flows.

SME momentum also stems from pro-innovation tax incentives and subsidized digital upskilling programs. These measures foster SaaS adoption for accounting, e-invoicing, and omnichannel commerce, areas historically under-served by traditional IT outsourcers.

By End-User Vertical: Healthcare Leads Growth Trajectory

Government and Public Sector retained 18.53% of 2024 revenue, propelled by the Digital Government 2025 roadmap. The Chile IT Services market share within Healthcare and Life-Sciences is expected to rise from 7.4% in 2024 to 10.2% by 2030 as telehealth platforms proliferate. Clinics deploy secure video consultations and electronic prescription modules to counter clinician shortages in remote areas. Pharmaceutical sponsors see Chile’s regulatory clarity as a differentiator for regional clinical-trial digitization hubs.

Mining remains a high-value use case for 5G-enabled edge analytics, supporting predictive maintenance and autonomous haulage. Retailers such as Walmart Chile scale AI-based smart cart pilots, while banking majors leverage cloud data platforms to train conversational AI agents that cut call-center wait times.

By Deployment Model: Hybrid Strategies Dominate Enterprise Choices

Hybrid or multi-cloud architectures captured 46.67% of 2024 spend, indicating enterprise preference for workload portability and disruption mitigation. The Chile IT Services market size attached to Hybrid deployment could cross USD 3.5 billion by 2030. Public Cloud exhibits the fastest trajectory at 15.67% CAGR, triggered by Amazon’s USD 4 billion region launch and maturing confidence in hyperscale security benchmarks.

On-premises models sustain a niche in highly regulated or low-latency environments, especially in mining where near-equipment processing cuts transmission costs. The national data-center roadmap targets USD 2.5 billion in sustainable facilities investment, setting green-energy benchmarks that attract ESG-conscious buyers.

Geography Analysis

Santiago accounts for the majority of the Chile IT Services market due to concentrated corporate headquarters and a deep developer talent pool. The metro area also hosts the landing station for the Southern Cross and upcoming Humboldt subsea cables, cementing low-latency global connectivity. Northern districts of Antofagasta and Atacama anchor specialized demand from copper extraction firms deploying digital twins and autonomous truck fleets. Service providers must address rugged terrain and limited fiber backhaul by integrating private LTE and edge micro-data centers.

Valparaíso and Concepción represent emerging secondary hubs where universities align curricula with cloud certification tracks, helping expand the skilled labour base beyond the capital. These cities attract small and medium enterprises seeking competitive wages and lower real-estate cost. Government incentives that grant tax rebates for new tech parks in these regions support distributed delivery models and mitigate Santiago-centric congestion risks.

Chile’s geographic alignment with Pacific Time enables real-time collaborations with Silicon Valley clients, a key differentiator over Asian offshore options. Providers leverage direct flight routes and bilingual account teams to deliver agile sprints, driving continued expansion of the Chile IT Services market across both metropolitan and resource-rich provinces.

Competitive Landscape

The Chile IT Services market shows moderate concentration. Top global vendors including Amazon, Microsoft, and IBM have built large local teams and infrastructure footprints yet face stiff rivalry from regional champions such as SONDA and Entel Digital that understand nuanced regulatory and cultural contexts. Amazon’s planned cloud-region inauguration spurs smaller firms to specialize in migration tooling, FinOps advisory, and security posture management to ride hyperscaler tailwinds.

Strategic differentiation hinges on domain-specific depth. Entel leverages its network backbone to bundle connectivity with managed services for edge analytics projects, while SONDA’s Latin American footprint helps multinationals orchestrate regional rollouts from a Chilean base. The acute cybersecurity talent gap rewards firms that invest in apprenticeship programs and university partnerships. Newer entrants like Trust Journey focus on generative AI chatbots for retail and telecom, underscoring the shift toward data-centric customer experience offerings.

Mergers and alliances are expected as peso volatility intensifies cost pressure. Equinix’s acquisition of three Entel data centers in 2024 demonstrates the value investors place on scalable colocation capacity linked to renewable power contracts, a trend likely to shape future capacity expansion strategies.

Chile IT Services Industry Leaders

SONDA S.A.

Entel S.A. (Entel Digital)

Accenture plc

IBM Chile SpA

Tata Consultancy Services Ltd.

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- May 2025: Amazon confirmed a USD 4 billion cloud-region investment scheduled for service launch in 2026.

- January 2025: The Cybersecurity Framework Law became effective, creating the National Cybersecurity Agency and mandatory reporting rules.

- December 2024: Chile introduced the National Data Centers Plan targeting USD 2.5 billion in green infrastructure investment.

- October 2024: ABB and Codelco signed a partnership to deploy digital and electrification solutions for mine decarbonization.

Chile IT Services Market Report Scope

| IT Consulting and Implementation |

| IT Outsourcing (ITO) |

| Business Process Outsourcing (BPO) |

| Managed Security Services |

| Cloud and Platform Services |

| Small and Medium Enterprises (SMEs) |

| Large Enterprises |

| BFSI |

| Manufacturing |

| Government and Public Sector |

| Healthcare and Life-Sciences |

| Retail and Consumer Goods |

| Telecom and Media |

| Logistics and Transport |

| Energy and Utilities |

| Other End-User Verticals |

| On-Premise |

| Public Cloud |

| Hybrid / Multi-cloud |

| By Service Type | IT Consulting and Implementation |

| IT Outsourcing (ITO) | |

| Business Process Outsourcing (BPO) | |

| Managed Security Services | |

| Cloud and Platform Services | |

| By End-User Enterprise Size | Small and Medium Enterprises (SMEs) |

| Large Enterprises | |

| By End-User Vertical | BFSI |

| Manufacturing | |

| Government and Public Sector | |

| Healthcare and Life-Sciences | |

| Retail and Consumer Goods | |

| Telecom and Media | |

| Logistics and Transport | |

| Energy and Utilities | |

| Other End-User Verticals | |

| By Deployment Model | On-Premise |

| Public Cloud | |

| Hybrid / Multi-cloud |

Key Questions Answered in the Report

How large is the Chile IT Services market in 2025?

It stands at USD 4.42 billion with a 10.8% CAGR outlook to 2030.

Which service type contributes most to spending?

Cloud and Platform Services led with 29.33% of 2024 revenue.

What drives rapid growth among Chilean SMEs?

Subscription-based cloud tools, tax incentives, and government upskilling programs fuel a 13.76% CAGR in SME IT spending.

Why is Public Cloud adoption accelerating?

A domestic hyperscaler region, clarified security rules, and cost agility are boosting Public Cloud workloads at a 15.67% CAGR.

Which vertical shows the fastest expansion?

Healthcare and Life-Sciences advances at a 14.5% CAGR due to telemedicine and digital clinical trials.

How will the Cybersecurity Framework Law impact providers?

It mandates breach reporting and critical-infrastructure safeguards, increasing demand for managed security services.

Page last updated on: