Brazil IT Services Market Size and Share

Market Overview

| Study Period | 2020 - 2031 |

|---|---|

| Forecast Data Period | 2026 - 2031 |

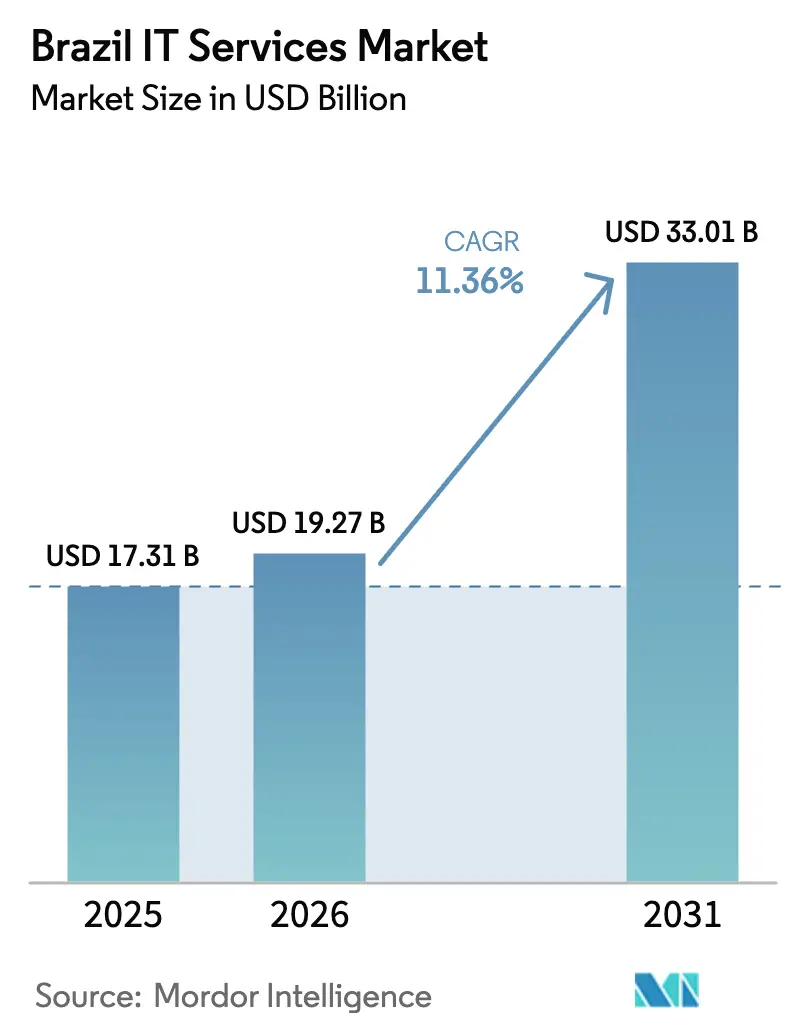

| Base Year Market Size (2025) | USD 17.31 Billion |

| Market Size (2026) | USD 19.27 Billion |

| Market Size (2031) | USD 33.01 Billion |

| Growth Rate (2026 - 2031) | 11.36% CAGR |

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

Brazil IT Services Market Analysis by Mordor Intelligence

Brazil IT services market size in 2026 is estimated at USD 19.27 billion, growing from 2025 value of USD 17.31 billion with 2031 projections showing USD 33.01 billion, growing at 11.36% CAGR over 2026-2031. Enterprise-wide digitization, a R$23 billion (USD 3.8 billion) federal AI program, and multi-cloud adoption underpin the growth trajectory of the Brazil IT services market, while structural currency weakness creates favorable cost arbitrage for export-oriented providers. Spending momentum is reinforced by the GOV.BR platform, whose 4,752 digital services deliver annual savings of R$5.1 billion (USD 0.94 billion), and by data-center investments exceeding USD 4 billion that expand sovereign-cloud capacity. Rising cyber-risk elevates managed security to board-level priority, and the energy sector’s industrial IoT pilots validate high-value use cases for analytics and AI. Simultaneously, Brazilian SMEs fast-track cloud adoption as simplified tax regimes and embedded-finance platforms lower the barriers to enterprise-grade technology. Heightened M&A—169 tech deals valued at R$26 billion (USD 4.2 billion) in 2024—signals that the Brazil IT services market is consolidating capabilities in AI, cybersecurity, and cloud to meet surging enterprise demand.

Key Report Takeaways

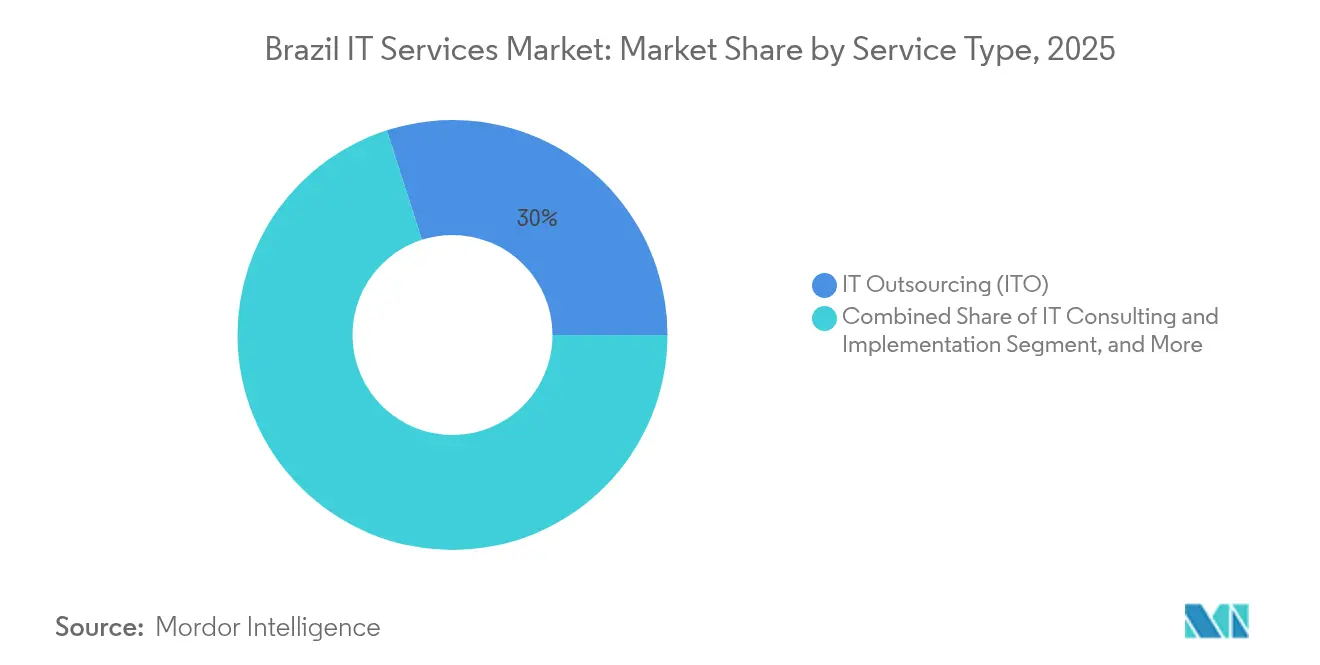

- By service type, IT Outsourcing (ITO) captured 29.95% of Brazil's IT services market share in 2025, while Managed Security Services is projected to expand at a 14.53% CAGR through 2031.

- By enterprise size, Large Enterprises held 67.55% of the Brazil IT services market size in 2025, whereas Small and Medium Enterprises are growing fastest at a 12.55% CAGR through 2031.

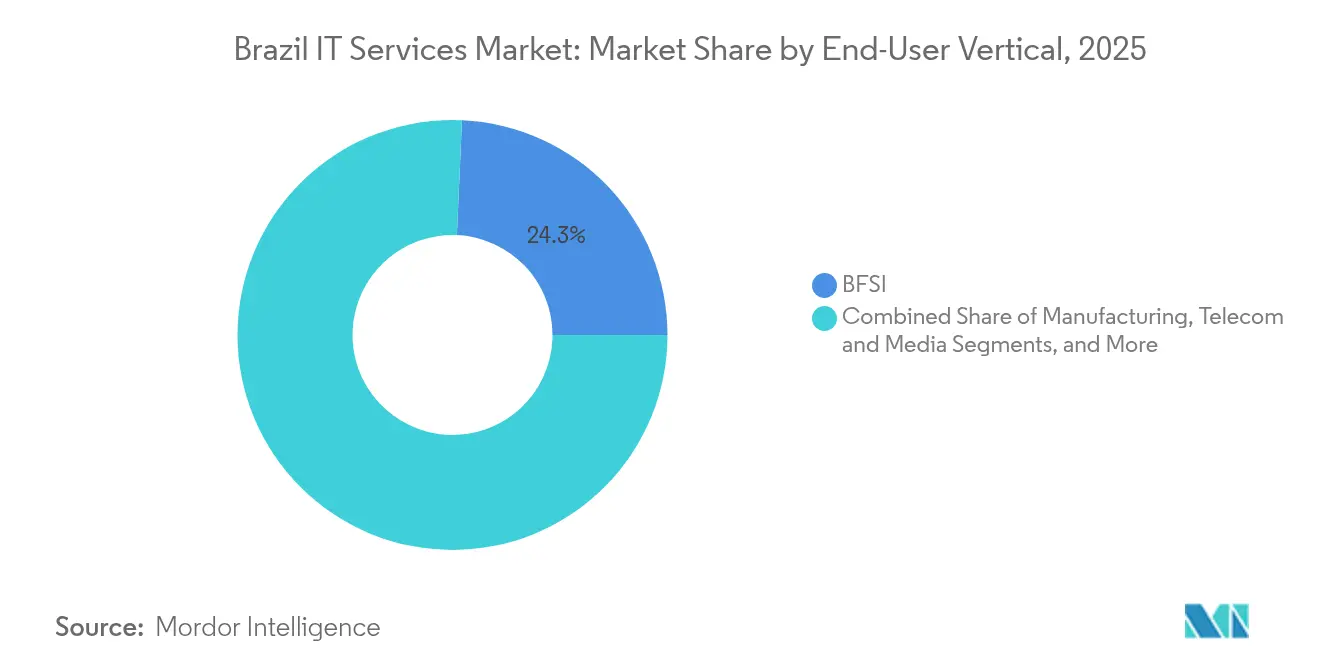

- By vertical, BFSI led with 24.30% revenue share of Brazil's IT services market size in 2025, but Healthcare and Life-Sciences are advancing at a 12.24% CAGR to 2031.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of 2026.

Brazil IT Services Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Digital-first transformation programmes among Brazilian enterprises | +2.8% | National, with concentration in São Paulo and Rio de Janeiro | Medium term (2-4 years) |

| Government incentives and tax reforms for IT modernization | +2.1% | National, with federal programs extending to municipalities | Long term (≥ 4 years) |

| Accelerating migration to hybrid and multi-cloud architectures | +2.4% | National, with emphasis on the Southeast region | Short term (≤ 2 years) |

| Surge in sophisticated cyber-attacks driving MSS demand | +3.2% | National, with a higher impact on the financial and energy sectors | Short term (≤ 2 years) |

| Portuguese-language AI/ML localisation unlocking new service lines | +1.8% | National, with spillover to Portuguese-speaking markets | Long term (≥ 4 years) |

| Industrial IoT pilots led by the Petrobras-centred energy cluster | +1.4% | Southeast region, with expansion to the Northeast energy corridor | Medium term (2-4 years) |

| Source: Mordor Intelligence | |||

Digital-first transformation programmes among Brazilian enterprises

Corporate leaders increasingly treat technology as a growth engine, lifting consulting, implementation, and managed-services demand across the Brazil IT services market. The national Digital Transformation Index climbed from 3.3 in 2023 to 3.7 in 2024, yet still trails mature economies, encouraging firms to seek external expertise.[1]PwC Brazil, “Índice Transformação Digital Brasil 2024,” pwc.com.br M&A spending on tech targets jumped 115% year over year, signaling a strategic rush to acquire digital capabilities. The local IT sector’s 13.3% growth forecast for 2025—versus the global 8.9% baseline—underscores the outsize momentum of the Brazil IT services market. E-commerce sales headed for R$224.7 billion (USD 41.33 billion) in 2025 intensify backend-integration projects, while the Pix instant-payment rail, already handling 47% of online transactions, accelerates cloud and API investments.

Government incentives and tax reforms for IT modernization

The National Digital Government Strategy (2024-2027) seeks to digitize 95% of federal services by 2027 through 93 initiatives, expanding addressable public-sector spend for the Brazil IT services market.[2]Presidency of Brazil, “Decreto 12.069/2024,” planalto.gov.br SERPRO channels more than 70% of its R$1 billion (USD 0.18 billion) budget into sovereign-cloud infrastructure, creating new workloads for private partners. Dual-VAT adoption from 2026 raises compliance complexity, spurring demand for specialist ERP, tax engine, and API services. Digital-identity programs could lift GDP by up to 13%, reinforcing a virtuous cycle of digital-services uptake across citizen-facing industries.

Accelerating migration to hybrid and multi-cloud architectures

An estimated 54% of Brazilian enterprises already use multiple public-cloud platforms, surpassing regional norms and fueling growth in the Brazil IT services market. Hyperscalers respond with multi-billion-dollar data-center expansions; AWS alone plans USD 1.8 billion of new capacity. Fifty-two grid-connection requests registered by June 2025 highlight infrastructure readiness for hybrid models. FinOps adoption rises as firms optimize cloud spend and align with carbon-reduction targets. Generative-AI pilots in roughly 150 enterprises intensify workload portability requirements, making multi-cloud orchestration a strategic imperative.

Surge in sophisticated cyber-attacks driving MSS demand

Managed security spending expands as threat volumes and regulatory mandates outpace in-house defenses. TIVIT’s 63% revenue leap in cybersecurity shows enterprises turning to outsourcing to manage LGPD obligations and 24×7 monitoring. Financial-sector rules—Brazilian National Monetary Council Resolution 4,893 and Central Bank Resolution 85—require robust cyber policies for any cloud contract. Domestic vendors such as Asper leverage local threat intelligence to expand into the U.S. market, proving the export potential of Brazilian cybersecurity expertise. AI-driven video analytics at Petrobras and Shell sites illustrate convergence between OT security and AI services in the Brazil IT services market.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Shortage of senior-level IT talent and high salary inflation | -2.1% | National, with an acute impact in São Paulo and Rio de Janeiro | Short term (≤ 2 years) |

| FX volatility is adding pricing risk to long-term outsourcing deals | -1.4% | National, with a higher impact on international service providers | Medium term (2-4 years) |

| LGPD-driven data-residency provisions are complicating cross-border delivery | -0.9% | National, with a specific impact on multinational service delivery | Long term (≥ 4 years) |

| Elevated electricity tariffs are limiting hyperscale DC expansion outside the SE region | -0.8% | Regional, primarily affecting the Northeast and North regions | Medium term (2-4 years) |

| Source: Mordor Intelligence | |||

Shortage of senior-level IT talent and high salary inflation

Brazil may face a deficit of 530,000 IT professionals by 2025, with only 53,000 new graduates annually, creating wage inflation that erodes service-provider margins.[3]SEGS, “Déficit de Talentos em TI,” segs.com.br Foreign employers pay up to 180% salary premiums, intensifying domestic brain drain. Providers respond with aggressive hiring—CI&T plans a 1,200-person expansion—and by deploying automation to offset labor gaps. However, AI tools introduce new skill requirements, perpetuating the talent shortfall cycle in the Brazil IT services market.

FX volatility adding pricing risk to long-term outsourcing deals

A real projected at R$6.00 per USD in 2025 injects currency risk into multi-year contracts, complicating margin management for providers and clients alike. Service-import-related dollar outflows of USD 49.7 billion in 2024 amplify pressure on the exchange rate. Currency hedging raises contract prices, while unhedged deals expose providers to margin swings. Outsourcing strategies at telecoms such as TIM highlight operational adjustments undertaken to mitigate volatility.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Service Type: Security Services Outpace Traditional Outsourcing

Managed Security Services captured attention by registering a 14.53% CAGR forecast through 2031, a pace that exceeds every other offering within the Brazil IT services market. Enterprises under regulatory and threat-environment pressure prioritize 24×7 SOC, incident response, and AI-driven analytics, allowing security services to command premium pricing and reduce churn. Meanwhile, IT Outsourcing preserves its leadership with 29.95 of % Brazil IT services market share in 2025, mainly anchored in application management and infrastructure support for large banks and industrial groups.

Demand dispersion favors niche innovators; for example, AI-enabled visual-monitoring vendor Pix Force lifted revenue to R$13 million (USD 2.39 million) in 2024 by targeting energy-sector clients. Cloud and Platform Services build on 54% multi-cloud adoption, yet hyperscaler competition caps margins. BPO confronts automation headwinds as low-complexity processes become bot-driven. These dynamics collectively reshape Brazil's IT services market size allocations across service lines and compel providers to cross-sell security, cloud, and data offerings to sustain growth.

By End-User Enterprise Size: SME Digital Awakening Drives Growth

Large Enterprises accounted for 67.55% of Brazil's IT services market size in 2025, reflecting complex, multi-tower contracts across finance, energy, and telecom. Yet the fastest CAGR belongs to SMEs at 12.55% to 2031, supported by 48% of small businesses planning digital-portfolio expansion. Cloud PBX studies estimate 6.3 million SMEs represent USD 315 million latent demand, illustrating the greenfield opportunity for SaaS and managed-services vendors.

Providers adapt tiered go-to-market models: Stefanini earmarked R$2 billion (USD 0.37 billion) for AI-centric acquisitions to serve both corporate and SME clients, while ContaAzul’s platform leverages Simples Nacional tax automation to lower onboarding friction. As wage pressures escalate, automation offsets limited IT staff at small firms, driving a proliferation of AI-powered help-desk and low-code solutions across the Brazil IT services market.

By End-User Vertical: Healthcare Digitalization Accelerates Beyond BFSI

BFSI retained 24.30 of % Brazil IT services market share in 2025, thanks to continuous core-bank modernization, but Healthcare and Life-Sciences are projected to outstrip it at a 12.24% CAGR. Telemedicine adoption produced 7.5 million remote consultations in two years, while 76% of healthcare CEOs plan AI investments. Platforms such as Galileu Health demonstrated a 41% reduction in emergency-room visits through analytics-driven patient monitoring, elevating the vertical’s appetite for cloud, data, and security services.

In BFSI, digital-banking maturity tempers growth, yet AI chatbots like Bradesco’s BIA and Banco do Brasil’s Ari create fresh demand for natural-language models and algorithm-audit services. Manufacturing receives a tailwind from Industry 4.0 policies; the industrial-automation market is heading toward USD 5.62 billion by 2028 at a 21% CAGR. Energy utilities digitize grids, exemplified by CPFL’s roll-out of 1.6 million smart meters backed by Siemens software. These sector-specific trends diversify revenue streams and deepen specialization across the Brazil IT services market.

Geography Analysis

The Brazil IT services market shows marked regional concentration: São Paulo accounts for roughly 80% of installed data-center capacity and houses enterprise headquarters, making it the primary delivery hub. Scala Data Centers’ R$6.2 billion (USD 1.14 billion) expansion in Barueri and Microsoft’s continued outlays illustrate capital intensity focused on the Southeast. Rio de Janeiro follows as a secondary cluster, supporting energy-sector analytics through newly commissioned 70 MW of capacity and 500 MW in the pipeline.

Investment disperses northward as Ceará secures Tecto’s R$550 million (USD 101.15 million) facility under a USD 1 billion multiyear plan, leveraging competitive renewable energy and submarine-cable links to attract hyperscalers. Bahia’s BA.GOV.BR platform demonstrates provincial innovation: 10 million site accesses and AI-driven payment verification that cut processing times from three days to five minutes. However, electricity tariffs are 20% higher than in the Southeast, hindering hyperscale expansion in the North and Northeast, reinforcing regional disparities within the Brazil IT services market.

In the Amazon region, Zona Franca de Manaus tax incentives draw Industry 4.0 pilots despite logistical challenges, while fiber-deployment projects seek to close the infrastructure gap. National programs that abolish import duties on data-center equipment are expected to accelerate dispersion, but the concentration of skilled labor and connectivity in the Southeast remains a near-term competitive moat.

Competitive Landscape

Competition in the Brazil IT services market is intensifying yet remains moderately fragmented, giving both multinational and domestic firms room to expand. Global integrators leverage scale and partner ecosystems, while local players differentiate through Portuguese-language AI, regional delivery centers, and vertical expertise. Stefanini reorganized into seven business units and plans R$2 billion (USD 0.37 billion) in acquisitions to deepen AI capabilities after delivering R$8 billion (USD 1.47 billion) in revenue in 2024. BRQ’s merger with Weme broadens design-thinking and hyper-personalization offerings, underscoring consolidation momentum.

Cybersecurity specialists gain market share; Asper’s U.S. entry showcases the export potential of Brazilian threat-intelligence services. Meanwhile, Compass UOL reached 1,000 AWS certifications and bought Oak Rocket, signaling cloud-skills depth that appeals to multinational clients. Hyperscalers embed local service arms to accelerate AI workload adoption, intensifying rivalry in consulting and managed-cloud services. Talent acquisition emerges as a competitive lever, with providers offering remote-work benefits and reskilling programs to mitigate labor shortages.

White-space opportunities persist in industrial-IoT services for energy clusters, Portuguese-language LLM training, and SME-focused managed services. Providers that bundle cybersecurity, AI, and cloud orchestration are best positioned to capture share as clients seek one-stop partners. Market-entry barriers remain moderate given currency advantage and fragmenting demand, but brand credibility, delivery quality, and compliance expertise increasingly dictate contract wins in the Brazil IT services market.

Brazil IT Services Industry Leaders

Accenture do Brasil Ltda.

IBM Brasil – Indústria, Máquinas e Serviços Ltda.

Stefanini Consultoria e Assessoria em Informática S.A.

Tivit Terceirização de Processos, Serviços e Tecnologia S.A.

Totvs S.A.

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- August 2025: BRQ merged with Weme, expanding hyper-personalization capabilities across Latin America and the United States.

- July 2025: Hitachi Energy engaged by Petrobras to study electrification of offshore platforms via renewable power.

- May 2025: TIVIT posted 12.2% revenue growth to R$ 2.1 billion (USD 370 million), powered by a 63% jump in managed cybersecurity services.

- April 2025: Eletrobras allocated R$100 million (USD 18.39 million) to expand its AI monitoring center to accelerate meteorological modeling.

Brazil IT Services Market Report Scope

| IT Consulting and Implementation |

| IT Outsourcing (ITO) |

| Business Process Outsourcing (BPO) |

| Managed Security Services |

| Cloud and Platform Services |

| Small and Medium Enterprises (SMEs) |

| Large Enterprises |

| BFSI |

| Manufacturing |

| Government and Public Sector |

| Healthcare and Life-Sciences |

| Retail and Consumer Goods |

| Telecom and Media |

| Logistics and Transport |

| Energy and Utilities |

| Other End-user Verticals |

| By Service Type | IT Consulting and Implementation |

| IT Outsourcing (ITO) | |

| Business Process Outsourcing (BPO) | |

| Managed Security Services | |

| Cloud and Platform Services | |

| By End-User Enterprise Size | Small and Medium Enterprises (SMEs) |

| Large Enterprises | |

| By End-user Vertical | BFSI |

| Manufacturing | |

| Government and Public Sector | |

| Healthcare and Life-Sciences | |

| Retail and Consumer Goods | |

| Telecom and Media | |

| Logistics and Transport | |

| Energy and Utilities | |

| Other End-user Verticals |

Key Questions Answered in the Report

How large is the Brazil IT services market in 2026?

It stands at USD 19.27 billion and is projected to hit USD 33.01 billion by 2031.

Which service line is growing fastest?

Managed Security Services lead with a 14.53% CAGR forecast to 2031.

Why are SMEs important to providers?

SMEs are expanding digital portfolios and are forecast to grow IT-services spending at 12.55% annually, outpacing large enterprises.

What is the biggest regional hub?

São Paulo hosts roughly 80% of national data-center capacity and remains the primary delivery base.

How is talent scarcity affecting the sector?

A projected shortfall of 530,000 IT professionals by 2025 drives wage inflation and accelerates automation investments.

What role does government play?

The National Digital Government Strategy aims to digitize 95% of public services by 2027, fueling demand for cloud, security, and integration solutions.

Page last updated on: