Medical Tubing Market Size and Share

Market Overview

| Study Period | 2020 - 2031 |

|---|---|

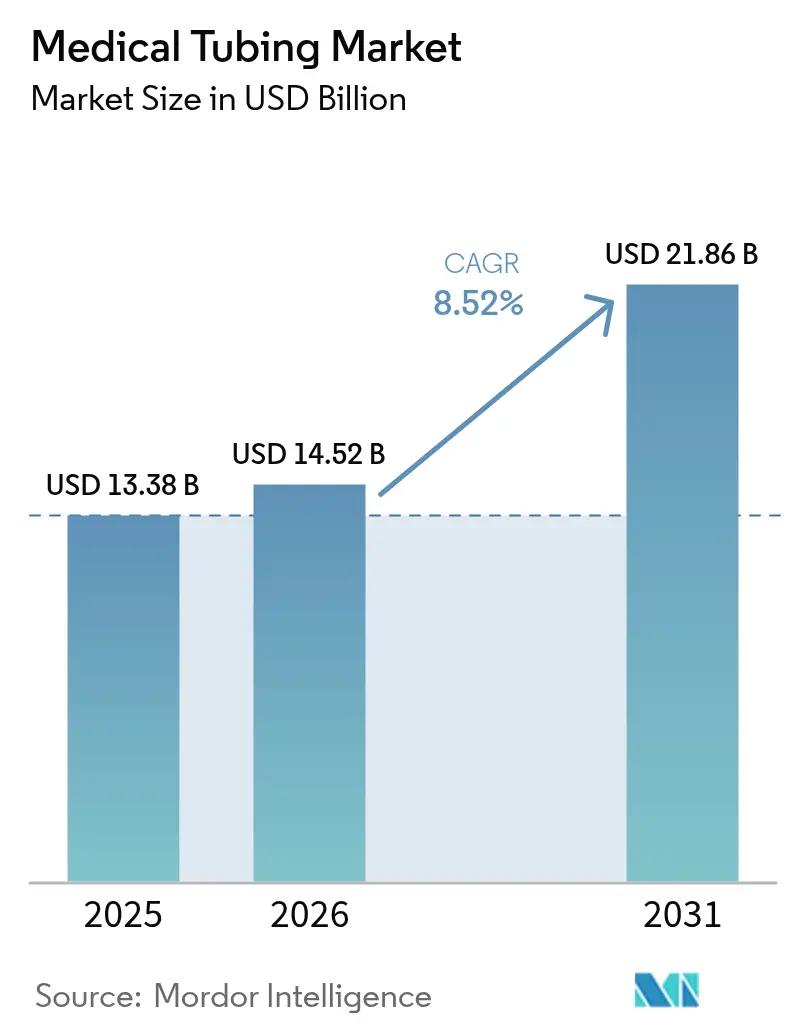

| Market Size (2026) | USD 14.52 Billion |

| Market Size (2031) | USD 21.86 Billion |

| Growth Rate (2026 - 2031) | 8.52% CAGR |

| Fastest Growing Market | Asia-Pacific |

| Largest Market | North America |

| Market Concentration | Medium |

Major Players*Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

Medical Tubing Market Analysis by Mordor Intelligence

The medical tubing market size was valued at USD 13.38 billion in 2025 and estimated to grow from USD 14.52 billion in 2026 to reach USD 21.86 billion by 2031, at a CAGR of 8.52% during the forecast period (2026-2031). Robust demand arises from minimally invasive procedures, rapid expansion of home-based care, and the integration of smart sensors that turn formerly passive conduits into active data channels. Premium-priced specialty polymers, micro-extrusion technologies, and sensor-ready designs headline the next phase of growth, while hospitals continue to anchor high-volume consumption. At the same time, supply chain exposure for medical-grade PVC and silicone and mounting environmental regulations inject strategic risk that producers must navigate. Competitive intensity is set to climb as mid-tier companies pursue M&A to secure extrusion capacity and regulatory expertise.

Key Report Takeaways

- By application, drug delivery systems led with 29.31% revenue share in 2025, while smoke evacuation and suction tubing is advancing at an 11.45% CAGR through 2031.

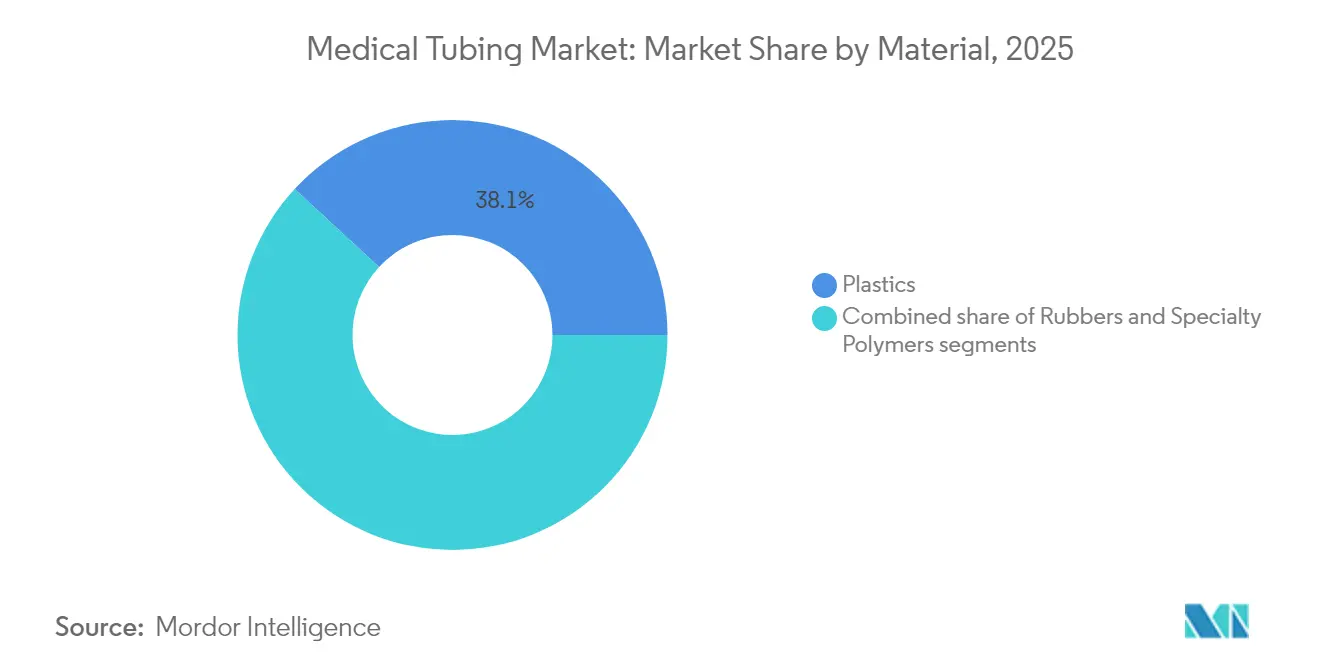

- By material, plastics commanded 38.12% of the medical tubing market share in 2025 and specialty polymers are projected to expand at a 10.18% CAGR between 2026-2031.

- By structure, single-lumen products held 40.92% share of the medical tubing market size in 2025, whereas micro-extruded tubing shows the fastest 11.02% CAGR to 2031.

- By manufacturing process, single-screw extrusion secured 48.05% share of the medical tubing market size in 2025, while micro-extrusion is set to move at a 10.51% CAGR.

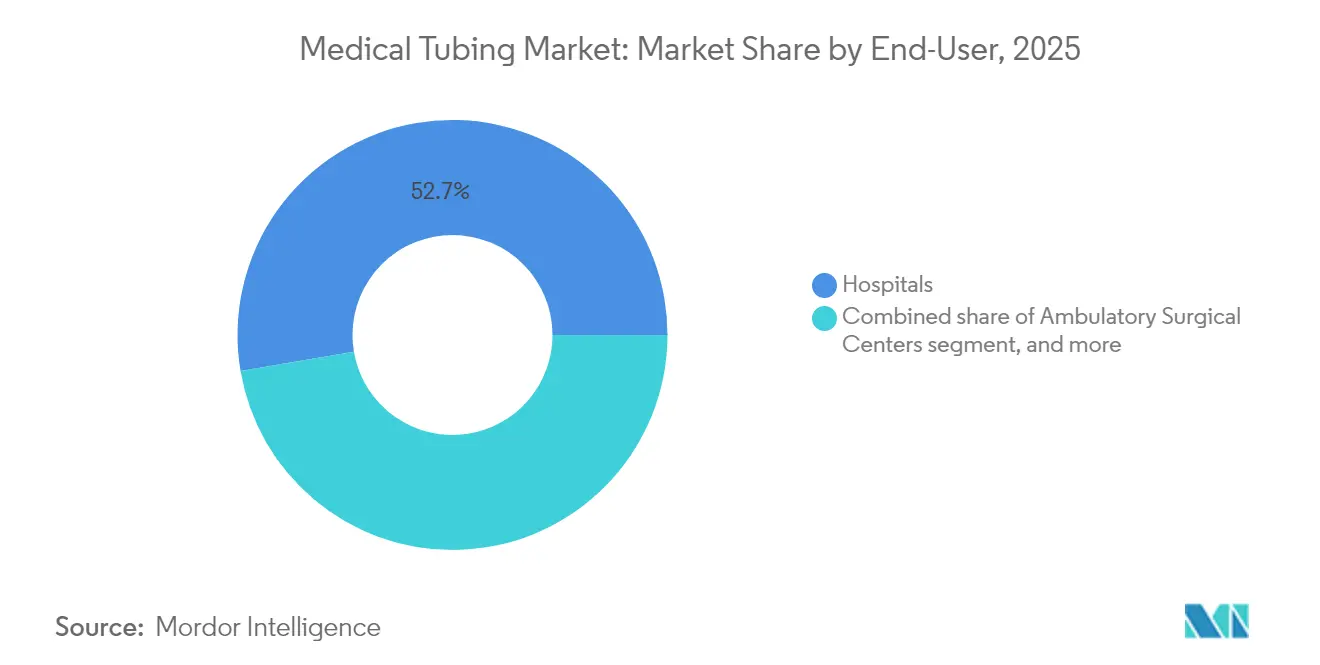

- By end-user, hospitals held 52.68% revenue in 2025, yet home-care environments are pacing at 11.24% CAGR.

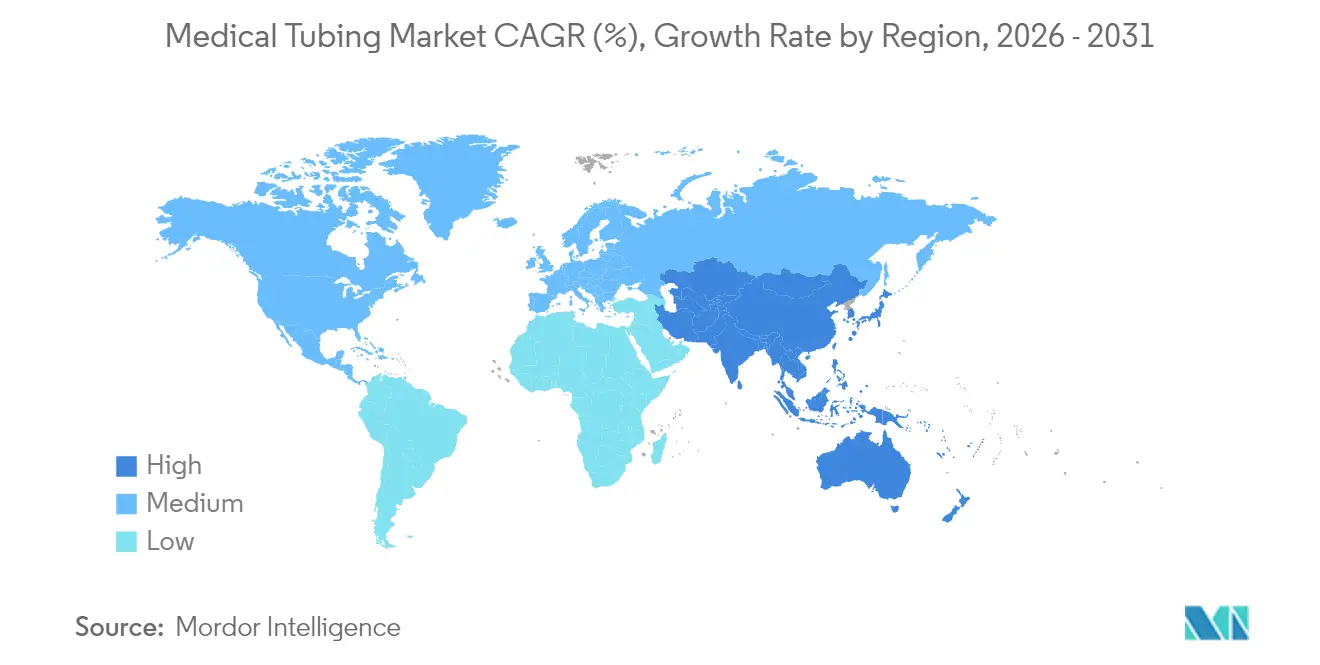

- By geography, North America occupied 41.02% of the medical tubing market share in 2025, and Asia-Pacific is forecast to grow at a 9.38% CAGR to 2031.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of 2026.

Global Medical Tubing Market Trends and Insights

Drivers Impact Analysis*

| Driver | % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Expanding Global Healthcare Expenditure | +1.8% | Global, strongest in North America & Asia-Pacific | Medium term (2-4 years) |

| Rising Prevalence of Chronic and Age-Related Diseases | +2.1% | Mature economies worldwide | Long term (≥ 4 years) |

| Growing Demand for Minimally Invasive Therapeutic Procedures | +1.5% | North America & Europe lead, Asia-Pacific catching up | Medium term (2-4 years) |

| Increased Adoption of Disposable Medical Devices for Infection Prevention | +1.3% | Global, accelerated post-COVID | Short term (≤ 2 years) |

| Continuous Advancements in Medical Polymer and Extrusion Technologies | +1.0% | R&D hubs in North America & Europe | Long term (≥ 4 years) |

| Emerging Home-Based and Point-of-Care Treatment Modalities | +0.9% | Initially developed markets, spreading globally | Medium term (2-4 years) |

| Source: Mordor Intelligence | |||

Rising Prevalence of Chronic and Age-Related Diseases

CDC data show 76.4% of U.S. adults living with at least one chronic condition[1]Centers for Disease Control and Prevention, “Chronic Disease Indicators,” cdc.gov. Long-term therapies such as dialysis, cardiovascular interventions, and sustained drug infusion depend on reliable tubing able to remain in-body or in-home for extended periods. An aging population magnifies at-home treatment, prompting need for user-friendly sets with audible alarms and kink-resistant lumens. Cardiovascular disease growth boosts adoption of advanced catheter tubing designed for pulsed-field ablation and transcatheter valve replacement. Disposable lines protect immunocompromised patients by minimizing infection risk in frequent infusion scenarios.

Growing Demand for Minimally Invasive Therapeutic Procedures

Interventional radiology alone is projected to exceed USD 43 billion by 2029 and requires ultra-slim catheters with high torsional stability[2]Frontiers in Radiology, “Market Outlook for Interventional Radiology Devices,” frontiersin.org. Thermally drawn polymer fibers now permit MR-guided therapy that avoids ionizing radiation, shifting design goals toward non-ferromagnetic materials and tight tolerances[3]arXiv, “Thermally Drawn Fibers for MRI-Guided Interventions,” arxiv.org. Device leaders such as Medtronic have incorporated modified diamond frames that improve access during transcatheter valve deployment. Tip geometry innovation further refines aspiration and stent delivery, all increasing demand for precision micro-extrusion.

Increased Adoption of Disposable Medical Devices for Infection Prevention

Post-pandemic protocols lock in single-use preference across central venous, enteral, and suction lines. Hospitals calculate that disposables offset sterilization labor, capital equipment depreciation, and litigation risk. Antimicrobial coatings and low-protein-binding materials limit biofilm growth, while updated FDA guidance clarifies the biocompatibility test suite and accelerates clearances. Simplified supply chains further appeal to procurement teams that aim to slash reprocessing complexity.

Continuous Advancements in Medical Polymer and Extrusion Technologies

AI-assisted Extrusion 4.0 platforms monitor wall thickness in real time, trimming scrap and enabling <0.1 mm inner diameters with ±2 µm tolerance. Hot-melt methods support continuous pharmaceutical tubing production with improved drug solubility. Specialty grades such as ultra polyimide extend thermal and chemical resistance envelopes for electrosurgical and neurovascular devices. Bio-circular polyamide 11 reduces carbon footprint while meeting ISO 10993 expectations.

Restraints Impact Analysis*

| Restraints Impact Analysis | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Stringent Regulatory Compliance and Validation Requirements | −1.2% | North America & Europe | Long term (≥ 4 years) |

| High Capital Investment for Medical-Grade Extrusion Facilities | −0.8% | Major manufacturing hubs in Asia-Pacific & North America | Medium term (2-4 years) |

| Supply Chain Vulnerabilities in Medical-Grade Polymers | −0.7% | Global, most acute in import-dependent regions | Short to medium term (≤ 4 years) |

| Environmental Sustainability Pressures on PVC and Silicone Usage | −0.6% | Europe leads, regulations expanding worldwide | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

Stringent Regulatory Compliance and Validation Requirements

Manufacturers must align quality systems with ISO 13485:2016 by February 2026 under the FDA’s amended regulation. Updated guidance now demands exhaustive chemical characterization, pushing extractable and leachable studies into multi-month projects that lengthen R&D cycles. In Europe, MDR, REACH, and RoHS layers elevate documentation effort, especially for PVC lines containing stabilizers. The emergent crackdown on PFAS adds uncertainty for fluoropolymer users, forcing pipeline audits and potential material swaps. High user fees amplify overhead, and smaller firms without in-house regulatory teams face margin squeeze or exit decisions.

High Capital Investment for Medical-Grade Extrusion Facilities

Cleanroom space, laser micrometers, multilayer dies, and real-time SPC systems drive start-up budgets well into tens of millions. Currency fluctuations and rising interest expenses further stress ROI models. Asian clusters mitigate some cost via labor savings, yet demand tight process validation that often imports Western consultants. The capital hurdle encourages joint ventures or outright acquisition by diversified conglomerates seeking market entry without greenfield risk.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Material: Specialty Polymers Drive Innovation

Plastics retained 38.12% share of the medical tubing market in 2025 owing to mature supply chains and competitive cost structures. Specialty polymers, however, are advancing at a 10.18% CAGR as complex cardiovascular, neurovascular, and drug delivery devices require superior lubricity, kink resistance, and bio-inertness. The sustainability debate has accelerated substitution of conventional PVC with TPEs that deliver comparable clarity and softness absent DEHP plasticizers. Ultra polyimide, PEBAX, and bio-circular PA11 are now mainstream in premium catheter assemblies. Suppliers that can scale these resins under ISO 13485-compliant conditions gain pricing power. Regulatory scrutiny surrounding PFAS is encouraging early moves toward fluorine-free alternatives in high-pressure angiographic lines.

Polymer innovation also answers recyclability mandates, with advanced depolymerization research aiming at closed-loop medical PVC recovery. Specialty elastomers command higher ASPs yet prove cost-neutral over life cycle due to fewer device failures. Material data sheets now include embodied carbon metrics that hospital sustainability officers review during tenders. As a result the medical tubing market size attributed to specialty polymers is projected to headline absolute gains through 2031.

By Application: Drug Delivery Systems Lead Market

Drug delivery systems accounted for 29.31% of 2025 revenue, underscoring the central role tubing plays in precision dosing and infusion accuracy. Chemotherapy, biologics, and long-acting injectables depend on tight inner-diameter tolerances and low extractables to maintain compound integrity. Smoke evacuation and suction lines, growing at 11.45% CAGR, reflect heightened surgeon awareness of airborne particulate hazards in operating theatres. Catheter-based cardiovascular therapy remains an anchor, yet product life cycles shorten as hospitals seek next-generation devices that cut fluoroscopy time and radiation dose.

Dialysis and extended IV therapies spur demand for kink-resistant silicone-free lines safe for overnight use. Enteral feeding sets incorporate antimicrobial layers and RFID tags to combat misconnections. Peristaltic pump demand remains stable as lab automation expands. 3D-printed, patient-matched airway stents illustrate early clinical adoption of additive tubing, hinting at wider customization potential. Together these dynamics secure drug delivery’s leadership while enabling high-growth niches that elevate overall medical tubing market value.

By Structure: Micro-Extruded Solutions Gain Momentum

Single-lumen formats still capture 40.92% of the medical tubing market size because they meet generic fluid-transfer needs at low cost. Yet micro-extruded tubing, expanding 11.02% annually, represents the innovation frontier where inner diameters below 0.1 mm enable neurovascular guidewires and pediatric interventions. Multilayer designs pair lubricious inner cores with torque-stable outers, optimizing pushability without raising profile. Braided reinforcements provide burst integrity for high-pressure angiography while maintaining cross-sectional thinness.

Sensor-integrated smart tubing embeds micro-electrodes and fiber-optic elements that stream flow and temperature data to clinicians. Co-extrusion allows radiopaque stripes for fluoroscopic visibility without secondary coating. Manufacturers that master concentricity below 3% variation improve trackability and reduce clinical friction. These advances position structural differentiation as a significant pricing lever inside the medical tubing market.

By End-User: Home-Care Settings Show Rapid Expansion

Hospitals held 52.68% revenue in 2025, reflecting steady baseline demand for bulk disposables and advanced surgical kits. Yet home-care environments are pacing at 11.24% CAGR as payors incentivize shorter inpatient stays. Remote monitoring devices with cellular gateways rely on leak-free tubing that activates alarms upon occlusion, empowering patients to manage dialysis or drug infusion independently. Ambulatory surgical centers seek quick-connect tubing to minimize turnover time between cases.

Diagnostic labs prioritize chemical resistance and low sorption to safeguard assay integrity. Healthcare consolidation shifts bargaining power toward integrated delivery networks that audit supplier environmental profiles. Tubing producers able to certify e-IFU compliance and sustainable packaging gain an edge as procurement teams broaden evaluation criteria beyond unit price.

By Manufacturing Process: Micro-Extrusion Technologies Advance

Single-screw extrusion preserved 48.05% share in 2025 thanks to high throughput and low tooling cost. Micro-extrusion, growing 10.51% per year, satisfies escalating demand for ultra-small lumens and multi-durometer profiles used in neurovascular catheters. Twin-screw lines enable precise pigment and radiopaque filler dispersion, critical for multilayer products. AI-enabled Extrusion 4.0 platforms deploy closed-loop laser gauges that correct die swell in real time, driving CpK improvements above 1.67.

Additive manufacturing offers rapid prototypes and limited-run niche items, trimming concept-to-clinic cycles by months. Continuous hot-melt extrusion in pharma tubing removes solvents from the production chain, meeting increasingly stringent environmental norms. Investment in these processes reinforces supply continuity and differentiates producers within the medical tubing market.

Geography Analysis

North America retained 41.02% of 2025 revenue, propelled by high per-capita healthcare spend, a mature device manufacturing base, and a reimbursement climate that rewards advanced catheter systems. U.S. hospitals lead global adoption of sensor-ready lines that link seamlessly to electronic medical records, while Canada’s universal coverage sustains steady baseline demand. The medical tubing market size in North America also benefits from concentrated R&D clusters and close industry–faculty collaboration that accelerates commercialization.

Asia-Pacific represents the fastest-growing region at 9.38% CAGR through 2031. China and India spearhead expansion due to broad population bases, chronic disease incidence, and domestic production scale-ups supported by multinational joint ventures. Lubrizol’s USD 350 million investment near Chennai exemplifies inbound capital directed at regional extrusion capacity that cuts lead times for local OEMs. ASEAN’s 620 million inhabitants and harmonized regulatory work-sharing further entice suppliers eager to diversify beyond legacy Western demand.

Europe maintains moderate growth driven by regulatory harmonization under MDR and a strong push for recyclable medical polymers. Germany anchors manufacturing, while Nordic innovation focuses on low-carbon materials compatible with hospital sustainability goals. The EU Packaging and Packaging Waste Regulation, which sets 2030 recyclability targets, is accelerating shift toward bio-circular resins and closed-loop designs. Overall regional progress remains steady despite Brexit-related complexity affecting United Kingdom certification pathways.

Competitive Landscape

The market shows moderate fragmentation as top multinationals pursue vertical integration and process automation, yet hundreds of regional extrusion specialists serve local OEMs. Saint-Gobain leverages silicone molding depth and proprietary PEBAX blends to equip high-performance neurovascular catheters. W. L. Gore fields ePTFE-based grafts and obtained FDA breakthrough status for its EXCLUDER TAMBE system, reinforcing leadership in complex aortic repair. Freudenberg expanded with a new Galway plant that adds 100 jobs and broadens balloon catheter capacity.

M&A activity is reshaping the field. Integer paid USD 140 million for Pulse Technologies to secure laser-machining expertise, while MMT added GenX Medical to deepen micro-extrusion reach. Such deals bundle regulatory files, intellectual property, and capacity, enabling broader customer lock-in. Concurrently, AI-driven Extrusion 4.0 and antimicrobial coating IP differentiate bidders in high-value proposals.

White-space opportunities involve sensor-integrated smart tubing, additive manufacturing for patient-specific airway guides, and PFAS-free high-pressure lines. Suppliers that master recyclable formulations and document carbon savings win inclusion on hospital sustainability scorecards. Vertical integration that marries resin compounding, cleanroom extrusion, tip forming, and final assembly shortens lead times, cementing the strategic advantage for full-service providers within the medical tubing market.

Medical Tubing Industry Leaders

Saint-Gobain

Freudenberg Medical

W. L. Gore & Associates, Inc.

The Lubrizol Corporation

Raumedic AG

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- May 2025: Freudenberg posted FY 2024 sales of €11.95 billion and invested €604.4 million in R&D, including catheter and thermoplastic molding capacity in Costa Rica.

- May 2025: Stryker received FDA clearance for OptaBlate BVN Basivertebral Nerve Ablation System featuring steerable introducer and microinfusion-enabled tubing.

- January 2025: Zimmer Biomet announced acquisition of Paragon 28 for USD 1.1 billion to deepen its orthopedic offering with tubing-intensive surgical kits.

- January 2025: Medical Manufacturing Technologies acquired GenX Medical to strengthen its extrusion portfolio.

- January 2025: Teleflex completed acquisition of BIOTRONIK’s Vascular Intervention business for €760 million (USD 830 million), broadening its interventional cardiology portfolio.

- December 2024: Abbott completed first leadless left bundle branch pacing procedures using investigational AVEIR Conduction System incorporating specialized delivery tubing.

Global Medical Tubing Market Report Scope

As per the scope of the report, medical tubing is designed for a number of applications that allow clinicians to administer fluid and devices or allow for gas flow. Common applications of medical tubing include ventilators and IVs, but tubing also finds uses in supporting access devices and as a delivery method for other devices. The Medical Tubing Market is Segmented by Material (Plastics, Rubbers, and Specialty Polymers), by Application (Bulk Disposable Tubing, Drug Delivery Systems, Catheters and Cannulas, and Others (Peristaltic Pump Tubing, Gas Supply Tubing, and Smoke Evacuation Tubing)), by Structure (Single Lumen, Co-Extruded, Multi Lumen, and Braided Tubing) and by Geography (North America, Europe, Asia Pacific, Middle-East and Africa, and South America). The market report also covers the estimated market sizes and trends for 17 countries across major regions globally. The report offers the value (in USD million) for the above segments.

| Plastics |

| Rubbers |

| Specialty Polymers |

| Bulk Disposable Tubing |

| Drug Delivery Systems |

| Catheters & Cannulas |

| Dialysis & IV Infusion |

| Peristaltic Pump Tubing |

| Gas Supply & Ventilation Tubing |

| Smoke Evacuation & Suction Tubing |

| Enteral & Feeding Tubes |

| Single Lumen |

| Co-Extruded / Multilayer |

| Multi Lumen |

| Braided / Reinforced |

| Micro-extruded |

| Sensor-integrated (Smart) |

| Hospitals |

| Ambulatory Surgical Centers |

| Diagnostic Laboratories |

| Home-care Settings |

| Single-screw Extrusion |

| Twin-screw Extrusion |

| Micro-extrusion |

| 3-D Printing / Additive Manufacturing |

| North America | United States |

| Canada | |

| Mexico | |

| Europe | Germany |

| United Kingdom | |

| France | |

| Italy | |

| Spain | |

| Rest of Europe | |

| Asia-Pacific | China |

| Japan | |

| India | |

| Australia | |

| South Korea | |

| Rest of Asia-Pacific | |

| Middle East & Africa | GCC |

| South Africa | |

| Rest of Middle East & Africa | |

| South America | Brazil |

| Argentina | |

| Rest of South America |

| By Material | Plastics | |

| Rubbers | ||

| Specialty Polymers | ||

| By Application | Bulk Disposable Tubing | |

| Drug Delivery Systems | ||

| Catheters & Cannulas | ||

| Dialysis & IV Infusion | ||

| Peristaltic Pump Tubing | ||

| Gas Supply & Ventilation Tubing | ||

| Smoke Evacuation & Suction Tubing | ||

| Enteral & Feeding Tubes | ||

| By Structure | Single Lumen | |

| Co-Extruded / Multilayer | ||

| Multi Lumen | ||

| Braided / Reinforced | ||

| Micro-extruded | ||

| Sensor-integrated (Smart) | ||

| By End-User | Hospitals | |

| Ambulatory Surgical Centers | ||

| Diagnostic Laboratories | ||

| Home-care Settings | ||

| By Manufacturing Process | Single-screw Extrusion | |

| Twin-screw Extrusion | ||

| Micro-extrusion | ||

| 3-D Printing / Additive Manufacturing | ||

| Geography | North America | United States |

| Canada | ||

| Mexico | ||

| Europe | Germany | |

| United Kingdom | ||

| France | ||

| Italy | ||

| Spain | ||

| Rest of Europe | ||

| Asia-Pacific | China | |

| Japan | ||

| India | ||

| Australia | ||

| South Korea | ||

| Rest of Asia-Pacific | ||

| Middle East & Africa | GCC | |

| South Africa | ||

| Rest of Middle East & Africa | ||

| South America | Brazil | |

| Argentina | ||

| Rest of South America | ||

Key Questions Answered in the Report

What is the expected value of the medical tubing market in 2031?

The market is forecast to reach USD 21.86 billion by 2031.

Which application currently leads revenue?

Drug delivery systems generated the largest 29.31% share in 2025.

Which region is growing fastest?

Asia-Pacific shows the fastest 9.38% CAGR through 2031.

Why are specialty polymers gaining traction?

They deliver superior kink resistance, lubricity, and sustainability credentials valued in advanced catheter systems.

How is regulation affecting material choices?

Stricter FDA and EU rules plus PFAS limits are pushing manufacturers toward fluorine-free and recyclable alternatives.

What manufacturing technology is expanding quickest?

Micro-extrusion is growing at a 10.51% CAGR thanks to demand for ultra-small, multi-layer tubing used in minimally invasive devices.

Page last updated on: