IV Tubing Sets And Accessories Market Size and Share

Market Overview

| Study Period | 2020 - 2031 |

|---|---|

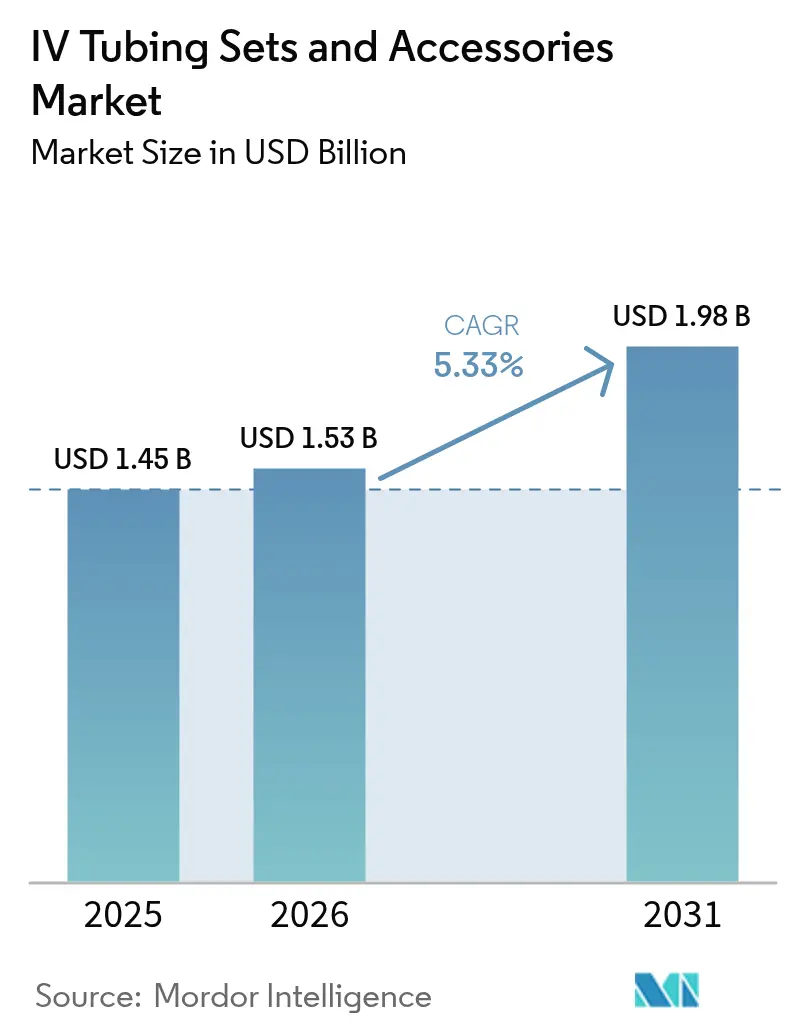

| Market Size (2026) | USD 1.53 Billion |

| Market Size (2031) | USD 1.98 Billion |

| Growth Rate (2026 - 2031) | 5.33% CAGR |

| Fastest Growing Market | Asia Pacific |

| Largest Market | North America |

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

IV Tubing Sets And Accessories Market Analysis by Mordor Intelligence

IV tubing sets & accessories market size in 2026 is estimated at USD 1.53 billion, growing from 2025 value of USD 1.45 billion with 2031 projections showing USD 1.98 billion, growing at 5.33% CAGR over 2026-2031. Growth rests on the migration of infusion therapy from inpatient wards to ambulatory and home-care settings, where demand shifts from episodic to continuous consumption [1]Fresenius SE & Co. KGaA, “Fresenius Company Presentation,” fresenius.com. Hospitals and outpatient centers now favor integrated tubing and connector systems that align with closed-system safety mandates, while smart pumps that authenticate each set at the bedside reduce medication errors. Manufacturers also benefit from vertical integration strategies that lock in recurring consumable revenue through proprietary tubing designs. At the same time, competitive pressure intensifies as Asian producers scale high-quality offerings that meet Western regulatory requirements.

Key Report Takeaways

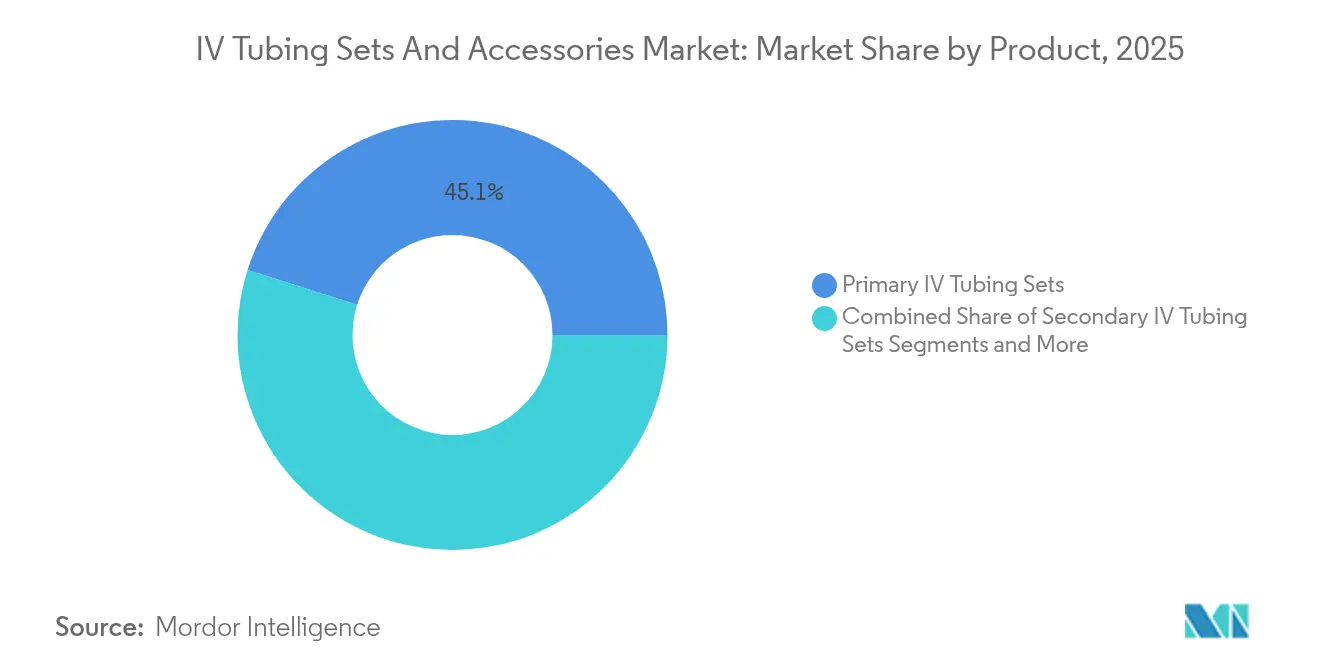

- By product, Primary IV Tubing Sets led with 45.12% revenue share in 2025; Secondary IV Tubing Sets are projected to expand at a 6.11% CAGR through 2031.

- By application, Peripheral Intravenous Catheter Insertion accounted for 40.95% of the IV tubing sets & accessories market share in 2025, while Central Venous Catheter Placement is set to grow at 6.18% CAGR to 2031.

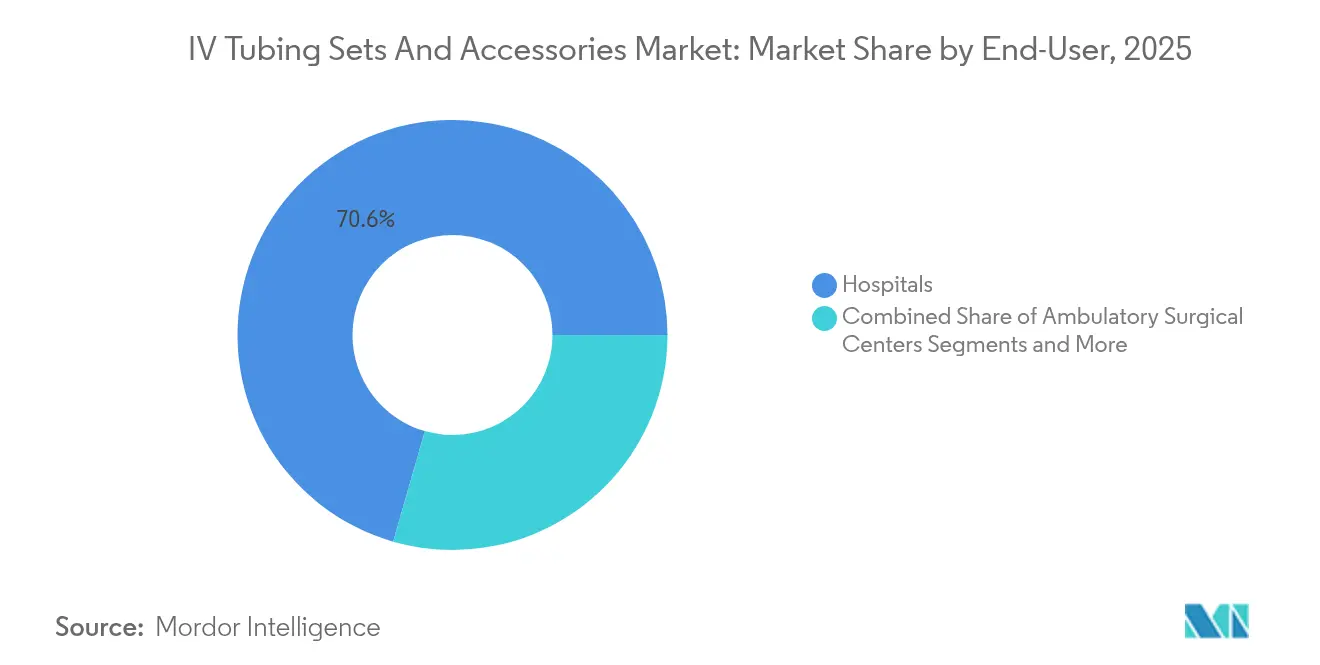

- By end user, Hospitals held 70.55% of the IV tubing sets & accessories market size in 2025; Ambulatory Surgical Centers will advance at a 6.32% CAGR between 2026 and 2031.

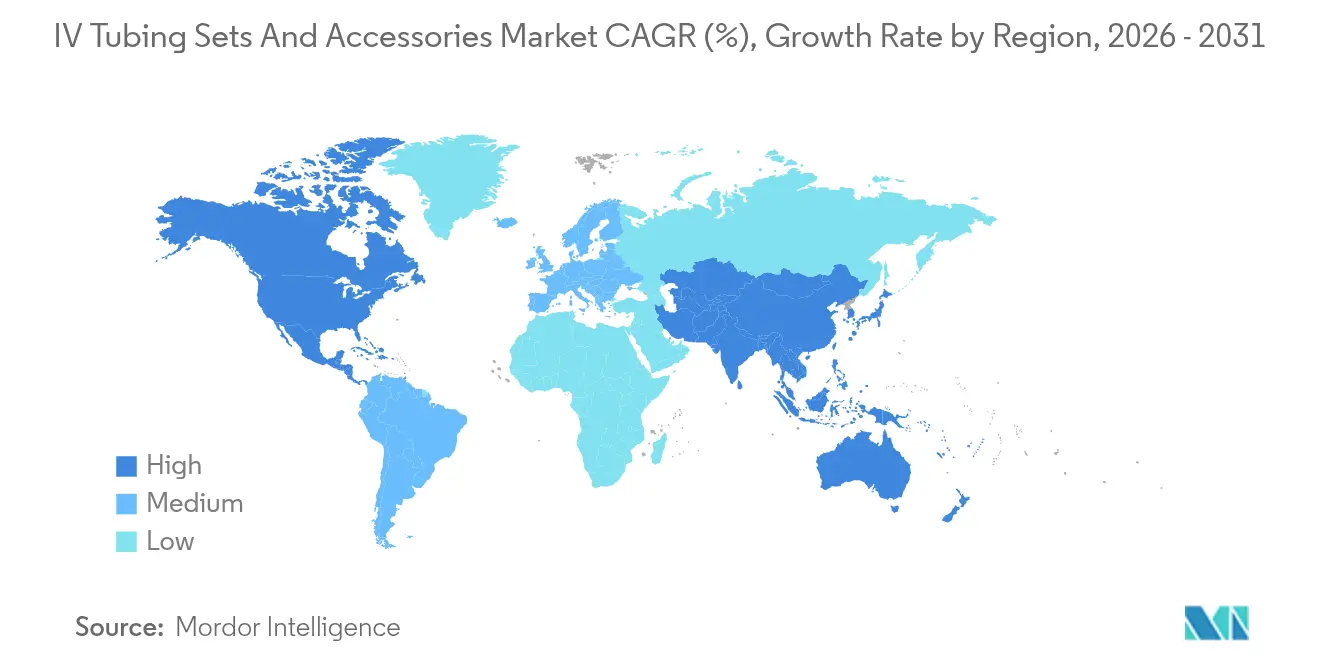

- By geography, North America captured 41.55% revenue share in 2025; Asia-Pacific is positioned for the fastest regional CAGR of 6.27% from 2026 to 2031.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of 2026.

Global IV Tubing Sets And Accessories Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Rapid growth in home-infusion therapies | +1.2% | Global, with early gains in North America & Europe | Medium term (2-4 years) |

| Shift toward needle-free closed IV systems | +1.0% | Global, spill-over from North America to APAC | Short term (≤ 2 years) |

| Rising surgical volumes in emerging economies | +0.9% | APAC core, spill-over to MEA | Long term (≥ 4 years) |

| Increasing natality rate | +0.6% | Global, concentrated in APAC & MEA | Long term (≥ 4 years) |

| Government initiatives improving vascular-access safety | +0.8% | North America & EU, expanding to APAC | Medium term (2-4 years) |

| AI-enabled predictive maintenance of IV equipment | +0.4% | North America & EU initially | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

Rapid Growth in Home-Infusion Therapies

Home infusion has shifted the IV tubing sets & accessories market by moving demand from short hospital stays to prolonged outpatient use. Payers now reimburse parenteral nutrition and chemotherapy administered at home, which requires tubing with higher durability and user-friendly connectors. The FDA has released guidance emphasizing closed pathways and needle-free valves to prevent contamination in settings without continuous clinical supervision. Smart pumps paired with RFID-tagged tubing allow remote monitoring, so caregivers receive alerts when flow deviates from prescribed parameters. As providers adopt these systems, manufacturers that bundle consumables with cloud-connected pumps secure sticky revenue streams. The shift also reduces inpatient costs, a point that aligns with health system strategies focused on lowering readmission penalties.

Shift Toward Needle-Free Closed IV Systems

Needle-free connectors reduce occupational exposure and cut the number of breach points that can harbor pathogens. California’s AB 2300 law sparked broader adoption by mandating closed systems in acute-care facilities, a template many states and countries now emulate [2]California Legislative Information, “Assembly Bill No. 2300,” leginfo.legislature.ca.gov . Clinical studies show decreased catheter-related bloodstream infections when connectors incorporate mechanical valves that stay closed unless positively displaced. Market leaders respond with antimicrobial coatings and color-change indicators that confirm proper disinfection. Training remains essential because poor scrubbing technique negates device benefits. Early adopters in the United States influence purchasing behavior in Asia-Pacific, where hospitals upgrading to Joint Commission International standards must include closed-system components.

Rising Surgical Volumes in Emerging Economies

Infrastructure projects across China, India, and Southeast Asia add operating suites that require full IV ecosystems. Governments invest in universal coverage, and growing middle-class populations opt for elective procedures. These markets favor cost-effective primary sets but quickly shift to secondary sets as case complexity rises. Complex cardiac and oncologic surgeries demand multi-lumen central lines, stimulating the IV tubing sets & accessories market, especially premium accessories such as pressure transducers. Manufacturers entering these markets localize supply to avoid tariffs and meet certification timelines, locking in volume contracts with public procurement agencies [3]Asian Development Bank, “Health Care Financing in Asia and the Pacific,” adb.org.

Government Initiatives Improving Vascular-Access Safety

WHO guidelines published in 2025 call for closed infusion pathways, connector disinfection protocols, and staff certification programs. Public hospitals that implement these standards influence private facilities via shared labor pools and reference pricing. Procurement specifications now list compatibility with needle-free valves as a mandatory requirement, which narrows the vendor list and elevates compliance as a competitive differentiator. Manufacturers that fund clinician education enjoy preferred-supplier status because training aligns with value-based purchasing goals that tie reimbursement to infection metrics.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Stringent regulatory framework | -0.8% | Global, most restrictive in North America & EU | Short term (≤ 2 years) |

| Plasticizer & PVC-phthalate bans | -0.6% | North America & EU, expanding globally | Medium term (2-4 years) |

| Supply-chain fragility for medical-grade resins | -0.7% | Global, acute in North America | Short term (≤ 2 years) |

| Increasing recalls tied to flow-rate inaccuracy | -0.4% | Global, concentrated in North America | Medium term (2-4 years) |

| Source: Mordor Intelligence | |||

Stringent Regulatory Framework

The FDA and European MDR both demand real-world evidence before approving new tubing materials, lengthening development cycles and raising compliance costs. Notified-body bottlenecks in Europe delay market entry for smaller innovators. Cybersecurity clauses extend to any tubing that communicates with connected pumps, adding penetration testing and documentation steps unheard of a decade ago. While these rules favor entrenched firms with dedicated regulatory teams, they also slow innovation in niche segments such as pediatric oncology where specialized tubing could lower error rates. Start-ups often partner with established OEMs to piggyback on existing quality systems, but profit sharing erodes their margins.

Plasticizer and PVC-Phthalate Bans

Legislation in several U.S. states and the European Union restricts di-ethylhexyl phthalate (DEHP) use in devices that contact fluids for extended periods. Manufacturers must reformulate PVC blends or switch to alternative polymers like TPU. Reformulation drives up raw-material costs and necessitates new biocompatibility testing. Hospitals, though concerned about endocrine disruption, resist price hikes without demonstrated clinical benefit. Long-term, the bans encourage innovations in bio-based plastics, yet supply remains limited, so transition adds volatility to the IV tubing sets & accessories market.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Product: Secondary Sets Ignite Growth Amid Primary Set Dominance

Primary IV tubing sets accounted for 45.12% of revenue in 2025, underpinning the procedural backbone of routine hydration and antibiotic administration across all care settings. Their high installed base and standardized connectors keep them indispensable, anchoring bulk-purchase contracts that underpin the IV tubing sets & accessories industry. Yet the same contracts increasingly bundle secondary tubing, a category forecast to grow at 6.11% CAGR as clinicians adopt multi-drug regimens that call for parallel infusions without pausing the primary line. This rise dovetails with smart pumps that auto-adjust flow through each lumen, ensuring precise dosing even in home settings. Manufacturers add value by integrating anti-siphon valves and back-check features, enhancing safety while justifying moderate price premiums.

Extension sets and accessory portfolios expand as providers seek ergonomic options that reduce line restarts when repositioning patients. Demand intensifies in critical-care units where equipment density requires flexible routing solutions. Blood administration sets and chemotherapy-grade lines fall under the Others category, where chemical compatibility and light-blocking materials command premium prices. RFID tagging within select tubing ranges allows the pump to authenticate each set, reducing misload events. As digital traceability becomes routine, proprietary connectors strengthen lock-in effects, influencing the IV tubing sets & accessories market size tied to replacement cycles.

By Application: Central Access Surges as Therapies Grow Complex

Peripheral catheter insertion maintained 40.95% share in 2025, reflecting its ubiquity and nurse-driven placement at bedside. Short-term antibiotics and hydration keep demand steady. However, central venous catheter placement is rising swiftly, predicted to outpace peripheral growth and register a 6.18% CAGR. Oncologic and critical-care protocols that rely on high-osmolar infusates prefer central access to prevent vessel damage, which in turn pulls through multi-lumen compatible tubing. The IV tubing sets & accessories market share benefits when hospitals replace one-size-fits-all kits with procedure-specific bundles that reduce setup time.

PICC line insertion bridges the gap between short and chronic therapy, gaining ground as ultrasound guidance improves success rates. Specialty sets with minimal priming volume and anti-reflux valves lower infection risk, broadening outpatient usage. The Others segment encompasses arterial lines and neonatal applications where pressure tolerance and micro-bore dimensions are critical. Advances in polyurethane formulations that combine flexibility with high tensile strength help minimize thrombosis, encouraging adoption in long-dwell scenarios. Emerging evidence from neonatal intensive care units highlights reduced complication rates when tubing materials match catheter chemistry, driving cross-selling opportunities for integrated vendors.

By End User: Ambulatory Centers Outpace Hospital Giants

Hospitals remained the primary consumer, gripping 70.55% of the IV tubing sets & accessories market size in 2025 due to their broad procedure mix and need for high inventory turnover. Central supply departments favor bulk packaging and standardized connectors that simplify logistics across intensive care, oncology, and surgery. Yet ambulatory surgical centers (ASCs) are rapidly narrowing the gap with a 6.32% forecast CAGR. ASCs rely on rapid room turnover and minimal staffing ratios, so they invest in tubing that combines quick-connect ports with visual anti-free-flow indicators, cutting setup time per case. Bundled infusion kits tailored to common outpatient procedures, such as orthopedic arthroscopy, align with reimbursement models that penalize delays.

Home-care settings, although still a smaller slice, post consistent growth as aging populations opt for therapy at home. Portable elastomeric pumps paired with low-weight, kink-resistant tubing extend dwell times and reduce emergency department visits, reinforcing payer support. The Others segment includes dialysis centers and long-term care facilities where infection-control standards mirror hospital requirements yet budget constraints drive preference for cost-optimized, high-volume tubing. Value-based care contracts incentivize providers to select systems with proven durability, helping reduce line replacement costs over the episode of care.

Geography Analysis

North America held 41.55% of global revenue in 2025, strengthened by early adoption of closed-system connectors, stringent OSHA mandates, and bundled multi-product contracts that include pumps, solutions, and disposables. Hurricanes and pandemic-related freight disruptions exposed supply chain weaknesses, prompting U.S. manufacturers to invest almost USD 1 billion in domestic capacity that cushions against future shocks. Regional payers now reimburse infection-prevention add-ons, which encourages hospitals to pay a premium for antimicrobial ports and RFID-enabled sets.

Asia-Pacific posts the fastest regional CAGR at 6.27% through 2031, fueled by rising surgical caseloads and expansion of public insurance schemes in China and India. Volume-based procurement models encourage bulk orders of standardized tubing, yet regulators simultaneously tighten safety criteria, creating a two-tier market. Local firms win spot tenders on price, whereas multinational brands capture tertiary hospitals that prioritize infection metrics for medical tourism. APAC governments also channel grants into smart-pump pilots, driving accompanying demand for compatible tubing coded with GS1 identifiers.

Europe occupies the second-largest share, anchored by evidence-based procurement guidelines that stress clinical data over headline price. The post-Brexit regulatory split raised compliance costs, compelling manufacturers to maintain parallel EU and UK submissions. Germany and France continue to favor premium closed systems, while Eastern European hospitals climb the maturity curve. Middle East and Africa register early-stage adoption, yet Gulf Cooperation Council investments in flagship medical cities generate pockets of high-value demand. South America’s growth is steadier; Brazil’s economic rebound and Argentina’s currency stabilization unlock new device purchases, though import duties influence price positioning.

Competitive Landscape

The IV tubing sets & accessories market shows moderate concentration. The firms cement relationships through multi-year contracts that bundle consumables with infusion pumps, software licenses, and maintenance services. The strategy locks providers into proprietary connector geometries, raising switching costs. ICU Medical’s completion of the Smiths Medical acquisition combined complementary pump and tubing portfolios, enabling cross-selling to 7,000 newly aligned customer accounts.

Investment now favors digital capabilities that integrate hardware and informatics. Fresenius Kabi’s Ivenix pump, cleared by FDA in 2024, supports tubing encoded with chip-based data that populates dosing libraries, reducing manual entry errors. Hospitals adopting the platform often sign exclusive consumables contracts, improving forecast accuracy for manufacturers. Mid-tier competitors such as Terumo and Nipro differentiate through specialty sets for oncology and blood products, areas where margin remains high. Chinese entrants leverage scale to win commodity bids in APAC; however, they struggle to penetrate North American and European markets due to quality-system gaps.

Recalls remain a reputational risk. Baxter’s 2024 tubing notice for flow variances triggered temporary formulary switches at large IDNs, benefiting competitors with proven uptime records. Meanwhile, suppliers that co-locate resin molding and final assembly mitigate recall impacts by shortening investigation timelines. Regulatory pressure on environmental sustainability catalyzes collaboration across the value chain to develop phthalate-free materials that do not compromise flexibility.

IV Tubing Sets And Accessories Industry Leaders

B. Braun Medical Inc.

Zyno Medical LLC

Nipro

Polymedicure

Baxter International

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- May 2025: Fresenius transferred its Anápolis production site to EMS, aligning with Vision 2026 network optimization.

- April 2025: Fresenius Kabi completed further site transfers in Santiago de Chile and Halden to third-party partners.

- February 2025: WHO issued updated bloodstream-infection prevention guidelines emphasizing closed-system connectors.

- January 2025: FDA cleared Fresenius Kabi’s Adaptive Nomogram algorithm for the Aurora Xi plasmapheresis platform.

Global IV Tubing Sets And Accessories Market Report Scope

As per the scope of the report, IV tubing sets & accessories are used to deliver fluids and nutrition to the patients. The IV Tubing Sets & Accessories Market is Segmented by Product (Primary IV Tubing Sets, Secondary IV Tubing Sets, IV Tubing Accessories, Extension IV Tubing Sets, and Others), Application (Central Venous Catheter Placemen, Peripheral Intravenous Catheter Insertion, and PICC Line Insertion), End User (Hospitals, Ambulatory Surgical Centers, and Others) and Geography (North America, Europe, Asia-Pacific, Middle East and Africa, and South America). The market report also covers the estimated market sizes and trends for 17 different countries across major regions, globally. The report offers the value (in USD million) for the above segments.

| Primary IV Tubing Sets |

| Secondary IV Tubing Sets |

| Extension IV Tubing Sets |

| IV Tubing Accessories |

| Others |

| Central Venous Catheter Placement |

| Peripheral Intravenous Catheter Insertion |

| PICC Line Insertion |

| Others |

| Hospitals |

| Ambulatory Surgical Centers |

| Home-care Settings |

| Others |

| North America | United States |

| Canada | |

| Mexico | |

| Europe | Germany |

| United Kingdom | |

| France | |

| Italy | |

| Spain | |

| Rest of Europe | |

| Asia-Pacific | China |

| Japan | |

| India | |

| Australia | |

| South Korea | |

| Rest of Asia-Pacific | |

| Middle East and Africa | GCC |

| South Africa | |

| Rest of Middle East and Africa | |

| South America | Brazil |

| Argentina | |

| Rest of South America |

| By Product | Primary IV Tubing Sets | |

| Secondary IV Tubing Sets | ||

| Extension IV Tubing Sets | ||

| IV Tubing Accessories | ||

| Others | ||

| By Application | Central Venous Catheter Placement | |

| Peripheral Intravenous Catheter Insertion | ||

| PICC Line Insertion | ||

| Others | ||

| By End User | Hospitals | |

| Ambulatory Surgical Centers | ||

| Home-care Settings | ||

| Others | ||

| By Geography | North America | United States |

| Canada | ||

| Mexico | ||

| Europe | Germany | |

| United Kingdom | ||

| France | ||

| Italy | ||

| Spain | ||

| Rest of Europe | ||

| Asia-Pacific | China | |

| Japan | ||

| India | ||

| Australia | ||

| South Korea | ||

| Rest of Asia-Pacific | ||

| Middle East and Africa | GCC | |

| South Africa | ||

| Rest of Middle East and Africa | ||

| South America | Brazil | |

| Argentina | ||

| Rest of South America | ||

Key Questions Answered in the Report

What is the projected value of the IV tubing sets & accessories market in 2031?

The market is forecast to reach USD 1.98 billion by 2031, growing at a 5.33% CAGR.

Which product category is expanding the fastest?

Secondary IV tubing sets will post a 6.11% CAGR through 2031 because they enable simultaneous multi-drug infusions.

Why are ambulatory surgical centers attracting attention?

ASCs show the highest end-user growth at 6.32% CAGR as more procedures shift from inpatient wards to cost-efficient outpatient suites.

How significant is Asia-Pacific in future demand?

Asia-Pacific will deliver the fastest regional CAGR of 6.27%, propelled by infrastructure expansion and rising surgical volumes.

What safety trend is reshaping purchasing decisions?

Hospitals increasingly require needle-free closed systems, which lower catheter-related infection rates and protect staff from sharps injuries.

Page last updated on: