Global Catheters Market Size and Share

Market Overview

| Study Period | 2020 - 2031 |

|---|---|

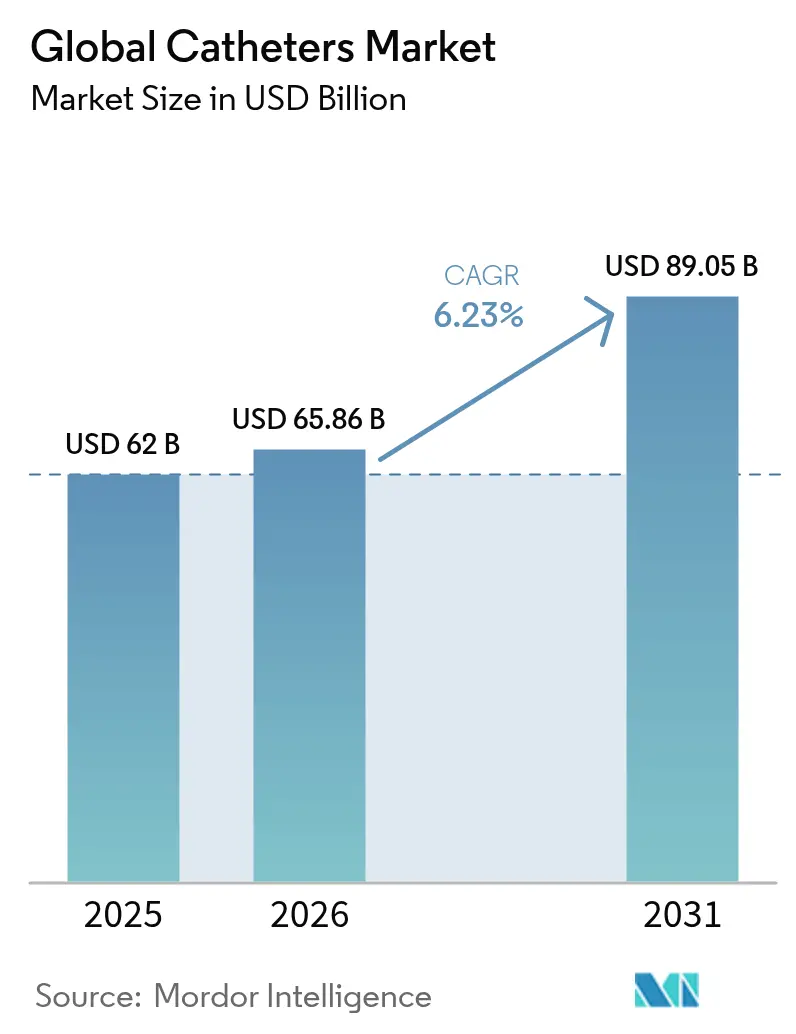

| Market Size (2026) | USD 65.86 Billion |

| Market Size (2031) | USD 89.05 Billion |

| Growth Rate (2026 - 2031) | 6.23% CAGR |

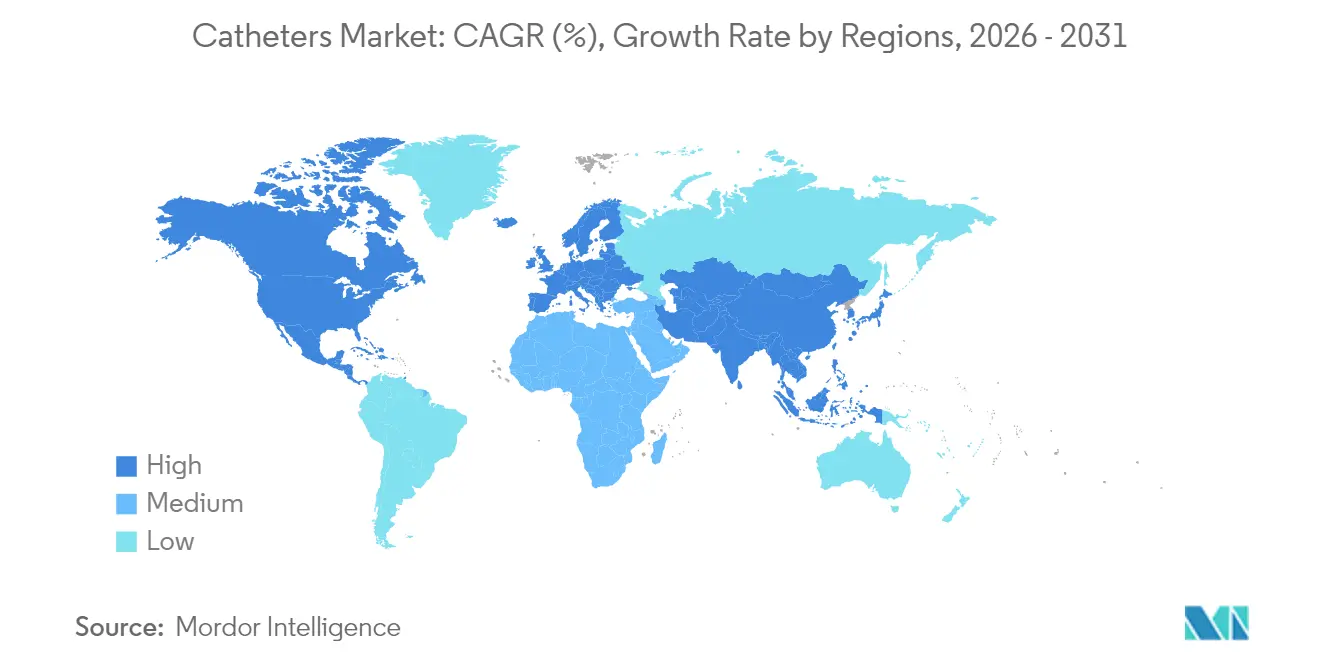

| Fastest Growing Market | Asia Pacific |

| Largest Market | North America |

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

Global Catheters Market Analysis by Mordor Intelligence

Catheters market size in 2026 is estimated at USD 65.86 billion, growing from 2025 value of USD 62.0 billion with 2031 projections showing USD 89.05 billion, growing at 6.23% CAGR over 2026-2031. Demographic aging, a rising burden of chronic cardiovascular and renal disease, and broader acceptance of minimally invasive procedures continue to stimulate demand. Technology cycles that deliver smarter coatings, embedded sensors, and AI-aided designs further widen the clinical utility of catheter products. At the same time, supply-chain re-engineering for specialty polymers and silicone has become a strategic focus as manufacturers strive to maintain consistent quality and pricing. Competitive positioning pivots on innovation pipelines, as firms look to consolidate fragmented product niches and defend intellectual property. Opportunities remain strong in home-based self-care, where supportive reimbursement and telehealth services enable non-institutional treatment pathways, extending the addressable catheters market well beyond traditional hospital settings.

Key Report Takeaways

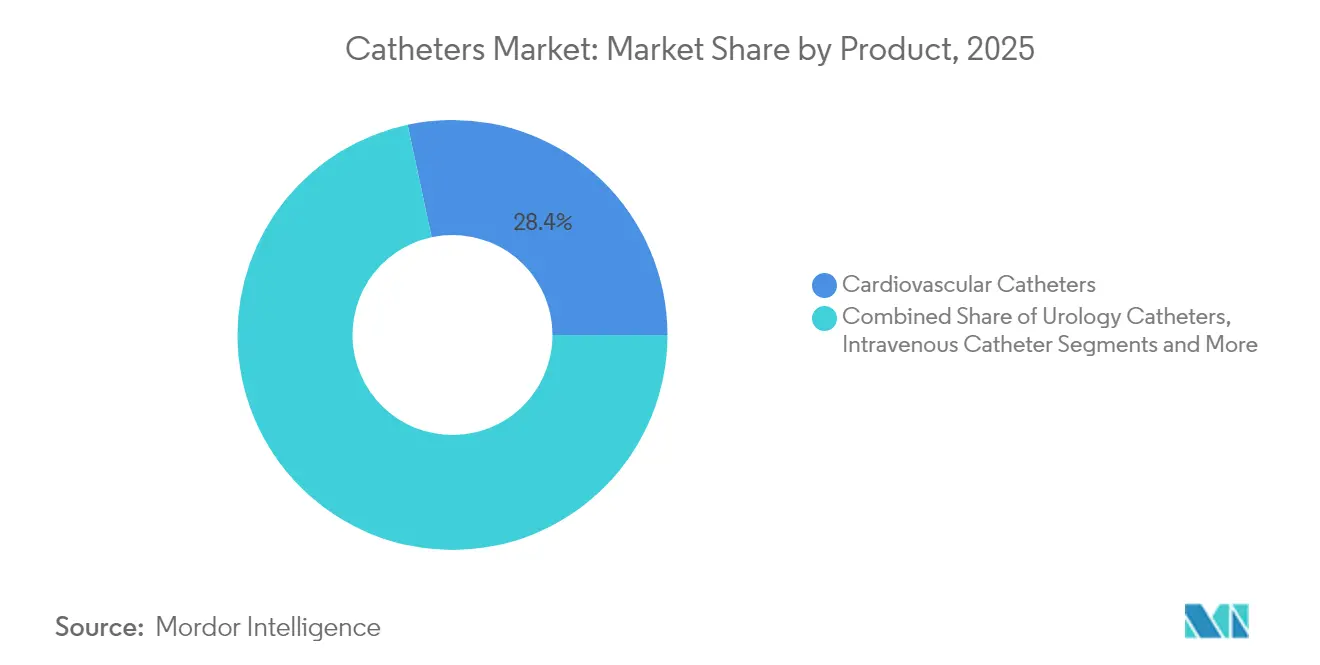

- By product type, cardiovascular catheters led with 28.35% of catheters market share in 2025, whereas neurovascular catheters are projected to grow at a 7.05% CAGR through 2031.

- By end user, hospitals controlled 67.65% of the catheters market in 2025; home-care settings show the fastest expansion at a 7.22% CAGR to 2031.

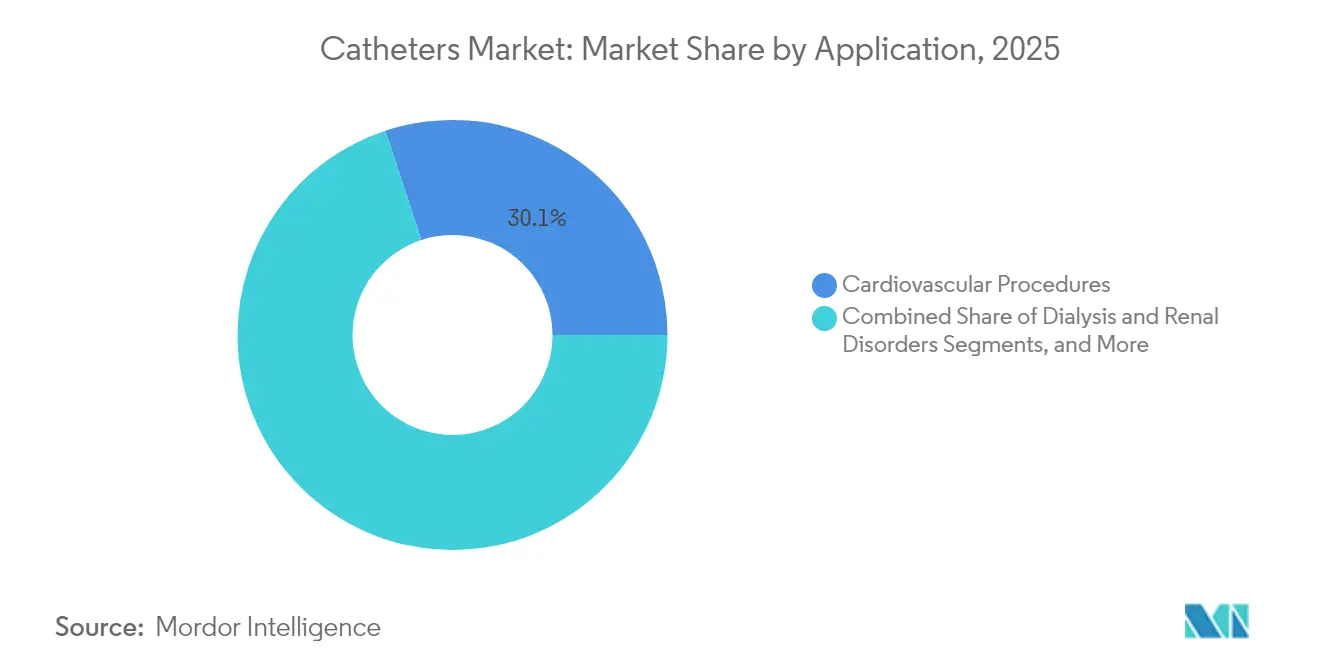

- By application, cardiovascular procedures accounted for a 30.05% share of the catheters market size in 2025, while dialysis applications are set to advance at a 7.49% CAGR during the forecast period.

- By geography, North America held 42.85% of the catheters market in 2025, yet Asia-Pacific is on track to rise at an 8.02% CAGR through 2031.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of 2026.

Global Catheters Market Trends and Insights

Drivers Impact Analysis*

| Driver | ( ~ ) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Rising prevalence of cardiovascular, neurological & urological disorders | +1.8% | Global, aging populations | Long term (≥ 4 years) |

| Increasing uptake of minimally invasive interventions | +1.5% | North America & EU leading; APAC accelerating | Medium term (2–4 years) |

| Surge in demand for antimicrobial & hydrophilic-coated catheters | +1.2% | Global | Short term (≤ 2 years) |

| Rapid adoption of home-based self-catheterization | +0.9% | Developed markets first; expanding to emerging economies | Medium term (2–4 years) |

| Integration of smart/connected sensor catheters | +0.7% | US, EU, Japan | Long term (≥ 4 years) |

| Growth of ambulatory surgical centers in emerging markets | +0.6% | APAC core, MEA & Latin America spill-over | Medium term (2–4 years) |

| Source: Mordor Intelligence | |||

Rising Prevalence of Cardiovascular, Neurological & Urological Disorders

Cardiovascular disease now affects 655 million individuals, while stroke incidence climbed 15% from 2019–2024, driving adoption of neurovascular catheters for thrombectomy procedures [1]Editorial Team, “Stroke Incidence and Global Burden,” Nature, nature.com. Chronic kidney disease impacts 850 million people and lifts demand for dialysis access catheters as hemodialysis populations in developed regions expand 6% annually. This epidemiological momentum makes catheter volumes less sensitive to economic cycles and underscores their role as essential care tools within the broader catheters market.

Increasing Uptake of Minimally Invasive Interventions

Catheter-based techniques represent 75% of cardiovascular procedures in developed healthcare systems, up from 45% ten years ago. Medtronic’s PulseSelect pulsed-field ablation platform posted 30% revenue growth in 2024, reflecting a system-wide push to lower hospital stays and improve outcomes [2]Investor News, “PulseSelect Achieves 30% Revenue Growth,” Medtronic, medtronic.com. Robotic navigation solutions such as Stereotaxis EMAGIN also enhance precision while curbing radiation exposure. These dynamics reinforce sustained demand across the catheters market as payers seek greater procedural efficiency.

Surge in Demand for Antimicrobial & Hydrophilic-Coated Catheters

Catheter-associated infections account for 40% of hospital-acquired infections that cost global systems USD 35 billion annually. Hydrophilic coatings can cut urinary tract infection rates by 64% over uncoated devices. New US HCPCS codes effective January 2026 reimburse hydrophilic catheters, building an economic case for rapid uptake. The convergence of proven clinical efficacy and favorable payment terms broadens premium coating adoption across the catheters market.

Rapid Adoption of Home-Based Self-Catheterization

Self-catheterization enhances quality of life and reduces facility dependence. Patient education programs and lighter, single-use devices increase adherence, with satisfaction levels rising despite higher unit costs. Telemedicine adds remote oversight, while a 25% jump in home dialysis use from 2020-2024 signals durable demand for home-ready catheter systems. As policy makers favor care decentralization, the home segment becomes a meaningful growth channel within the catheters market.

Restraints Impact Analysis*

| Restraint | ( ~ ) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Catheter-associated infections & biofilm formation | -0.8% | Global, acute care | Short term (≤ 2 years) |

| Availability of non-catheter substitutes | -0.6% | Technology-advanced markets | Medium term (2–4 years) |

| Polymer & silicone supply-chain volatility | -0.5% | Global manufacturing | Short term (≤ 2 years) |

| Reimbursement pressure in mature markets | -0.4% | North America & EU | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

Catheter-Associated Infections & Biofilm Formation

Indwelling catheter infection rates touch 25% in some settings, with catheter-related bloodstream infections carrying mortality rates up to 25%. As regulators tighten infection control protocols, device dwell time restrictions and more frequent replacements raise costs and complicate clinical workflows, curbing short-term momentum in the catheters market.

Polymer & Silicone Supply-Chain Volatility

PTFE shortages have lifted material costs to 20% of device revenue, up from 12% in 2020. Manufacturers are pursuing vertical integration and alternative materials, yet qualification testing and regulatory clearances lengthen timelines, creating intermittent product shortages across the catheters market.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Product: Cardiovascular Leadership Amid Neurovascular Acceleration

Cardiovascular catheters delivered 28.35% of the catheters market in 2025, supported by entrenched clinical protocols across angiography, ablation, and electrophysiology. This maturity ensures stable volumes as hospitals routinely stock multiple sizes and configurations. The catheters market size for cardiovascular interventions is projected to widen at a steady clip in line with coronary disease prevalence. Neurovascular catheters, while still smaller by revenue, advance at a 7.05% CAGR as stroke centers expand and mechanical thrombectomy devices prove efficacy. Stanford’s milli-spinner technique posts 90% success versus 50% for legacy systems, underscoring technology-led upside.

Innovation pipelines remain active. Steerable tips, refined braiding, and softer polymers elevate neurovascular navigation, narrowing risk profiles and opening new procedural indications. Intravenous catheters stay the highest-volume consumable in hospital supply chains, but margin pressures persist given commoditized pricing. Specialty designs—ranging from occlusion balloons to drug-eluting configurations—command premium pricing and cushion profitability. Across categories, clinical evidence, reimbursement clarity, and material availability shape share shifts inside the broader catheters market.

By End User: Hospital Dominance Challenged by Home-Care Growth

Hospitals represented 67.65% of 2025 sales, reflecting their central role in emergent and complex procedures that demand surgical suites and imaging infrastructure. This top position illustrates the catheters market size concentration within institutional care. However, home-care settings expand 7.22% annually as telehealth monitoring and simplified devices enable chronic-care patients to manage treatment without repeated admissions. The new 2026 HCPCS codes incentivize home-use devices, which could tilt procurement budgets toward community channels .

Ambulatory surgical centers capture incremental share by performing routine catheter procedures in cost-controlled environments. Providers value fast patient turnaround and lower overhead compared with tertiary hospitals. Insurers steer appropriate cases to these facilities, ensuring sustained volume. Over the forecast horizon, end-user dynamics will hinge on the pace of care decentralization and on how swiftly payers adapt reimbursement frameworks, ultimately redefining sales channels for the catheters market.

By Application: Cardiovascular Procedures Lead, Dialysis Accelerates

Cardiovascular interventions accounted for 30.05% of the catheters market size in 2025, spanning angioplasty, structural heart, and electrophysiology. Clinical familiarity and robust evidence bases keep demand resilient, even amid cost-containment pressures. Dialysis access emerges fastest at 7.49% CAGR on the back of rising renal disease prevalence and expanded home dialysis programs. BD’s Pristine long-term hemodialysis catheter achieved 100% patency at 30 days and 91% at 180 days, signaling design improvements that enhance clinical confidence.

Urological applications maintain steady mid-single-digit growth fueled by aging populations and improved patient acceptance of intermittent catheterization. Complex neurovascular and structural cardiac uses, although smaller, provide outsized margin opportunities as sophisticated designs attract premium pricing. Application trends therefore diversify revenue streams and underline the multi-faceted demand drivers sustaining the catheters market.

Geography Analysis

North America retained 42.85% of global revenue in 2025, underpinned by advanced hospital networks, early technology adoption, and favorable reimbursement. The FDA’s breakthrough-device pathway has quickened market entry for novel catheters, while Medicare coverage expansions offer tailwinds for high-value devices. Even so, mature-market price compression and hospital budget scrutiny put a ceiling on volume growth. Regulatory stability and predictable payment landscape still make the region a testing ground for premium catheter technologies, cementing its influence on the catheters market.

Europe stands as the second-largest cluster, shaped by the Medical Device Regulation. Stringent technical documentation and post-market surveillance raise compliance costs, especially for small firms, potentially consolidating supplier bases. Infection-prevention priorities and antimicrobial stewardship stimulate demand for coated and single-use devices. Brexit-related logistics challenges and shifts in public-tender rules, including moves to exclude certain foreign suppliers, complicate supply-chain planning yet may favor local manufacturing. The net impact is a cautious but quality-focused European catheters market.

Asia-Pacific is the fastest-growing theater, expanding at an 8.02% CAGR through 2031. Health-system modernization, rising surgical volumes, and government investment in universal care strengthen underlying demand. The region’s medical-technology spending is projected to hit USD 225 billion by 2030. Local manufacturing incentives, technology-transfer agreements, and a burgeoning private-hospital segment in India and Southeast Asia lower entry barriers. Nevertheless, heterogeneous regulatory regimes and price-cap policies require nuanced go-to-market strategies for firms seeking to scale in the APAC catheters market.

Competitive Landscape

The catheters market remains moderately fragmented, with multinational corporations and specialized developers jostling for share. Industry leaders exploit scale advantages in sterile manufacturing, distribution, and clinical education while pumping funds into R&D to maintain technological edges. Consolidation gathers pace: Stryker’s USD 4.9 billion acquisition of Inari Medical and BD’s USD 4.2 billion purchase of Edwards Lifesciences’ Critical Care division spotlight the premium assigned to innovation pipelines and therapeutic adjacencies.

Technology differentiation is a decisive lever. Players race to integrate antimicrobial coatings, embedded sensors, and AI-assisted modeling to deliver catheters that lower complication rates and enable real-time analytics. Teleflex’s plan to split into two pure-play companies—one focused on vascular access and interventional products—illustrates strategic sharpening around high-growth niches. Patent applications in catheter technologies have risen 25% each year, indicating intense efforts to lock in competitive moats.

Emerging companies seize white-space opportunities in neurovascular, dialysis, and home-care segments where incumbent product lines lag evolving clinical protocols. At the same time, polymer sourcing challenges and regulatory overheads push smaller outfits to seek contract-manufacturing alliances or become acquisition targets. Overall, sustained investment in material science, sensor fusion, and user-centric design will dictate the pecking order across the catheters market.

Global Catheters Industry Leaders

Hollister

Medtronic Plc

Coloplast

Becton, Dickinson and Company

B. Braun Melsungen AG

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- January 2025: B. Braun Medical introduced the Clik-FIX Epidural/Peripheral Nerve Block catheter securement device, aimed at reducing displacement during regional anesthesia.

- January 2025: Radical Catheter Technologies secured FDA 510(k) clearance for its 8F neurovascular catheter built on proprietary ribbon technology.

- January 2025: Sanford Health’s Dr. Bruce Gardner received FDA approval for a catheter design that auto-deflates its retention balloon when excessive tension occurs.

- December 2024: Terumo Interventional Systems launched the R2P NaviCross peripheral support catheter in the US, featuring double-braided stainless-steel construction for enhanced torque control.

Research Methodology Framework and Report Scope

Market Definitions and Key Coverage

Our study defines the global catheters market as the aggregated value of new, single-use or reusable flexible tubes that are inserted into the body for diagnostic or therapeutic purposes across cardiovascular, urological, intravenous, neurovascular, and specialty applications. The value pool tracks sales from original device makers to first-level healthcare facilities, expressed in USD at prevailing annual exchange rates.

Scope exclusion: After-market refurbishment services and rental income are kept outside the sizing.

Segmentation Overview

- By Product

- Cardiovascular Catheters

- Urology Catheters

- Intravenous Catheters

- Neurovascular Catheters

- Specialty / Other Catheters

- By End User

- Hospitals

- Ambulatory Surgical Centres

- Home-care Settings

- Others

- By Application

- Cardiovascular Procedures

- Urinary Incontinence & Retention

- Dialysis & Renal Disorders

- Others

- By Geography

- North America

- United States

- Canada

- Mexico

- Europe

- Germany

- United Kingdom

- France

- Italy

- Spain

- Rest of Europe

- Asia-Pacific

- China

- Japan

- India

- Australia

- South Korea

- Rest of Asia-Pacific

- Middle East & Africa

- GCC

- South Africa

- Rest of Middle East & Africa

- South America

- Brazil

- Argentina

- Rest of South America

- North America

Detailed Research Methodology and Data Validation

Primary Research

Mordor analysts interviewed interventional cardiologists, infection-control nurses, purchasing managers, and regulatory reviewers across North America, Europe, and Asia Pacific. These conversations validated usage frequencies, typical selling prices, and emerging shifts toward home-based self-catheterization, filling gaps left by desk research and fine-tuning model assumptions.

Desk Research

We began by mapping baseline demand from open datasets such as the WHO Global Health Observatory, OECD health statistics, United States CMS procedure volumes, Eurostat hospital discharge files, and trade databases like UN Comtrade. Company 10-Ks, device recall notices, and peer-reviewed journals on catheter-associated infection trends supplied product-level benchmarks. Paid databases, D&B Hoovers for company revenues and Dow Jones Factiva for deal tracking, helped us cross-check pricing corridors and recent capacity additions. The sources listed illustrate the wider pool consulted; many additional publications informed data cleaning and clarification.

Market-Sizing & Forecasting

An initial top-down reconstruction converted national procedure counts, dialysis patient registries, and chronic disease prevalence into demand pools, which were then multiplied by verified utilization and replacement rates. Supplier roll-ups and sampled average selling price × volume checks provided a bottom-up sense-check before final calibration. Key model drivers include cardiac intervention volumes, urinary incontinence prevalence, elective surgery deferrals, polymer price trends, and hospital capital budget growth. Five-year forecasts apply multivariate regression with ARIMA overlays, guided by expert consensus on technology adoption curves and reimbursement outlooks. Where country-level data were patchy, regional proxy ratios from primary interviews bridged gaps.

Data Validation & Update Cycle

Outputs pass through variance checks against independent shipment indices, followed by two-step analyst review and senior sign-off. The report refreshes every twelve months, while material events, major recalls, policy shifts, or pandemic waves trigger an interim update before client delivery.

Why Mordor's Catheters Baseline Commands Reliability

Published numbers frequently diverge because firms adopt different product mixes, price points, and refresh cadences. Our disciplined scope alignment and dual-path modeling narrow these gaps and give decision makers a figure they can trace back to clear variables.

Key gap drivers include whether specialty drainage catheters are counted, if retail mark-ups are layered, the currency conversion year, and how aggressively future infection-control mandates are baked into volumes.

Benchmark comparison

| Market Size | Anonymized source | Primary gap driver |

|---|---|---|

| USD 62.0 B (2025) | Mordor Intelligence | - |

| USD 61.9 B (2025) | Global Consultancy A | Excludes drainage catheters and home-care channels, applies constant 2023 exchange rates |

| USD 30.5 B (2025) | Global Consultancy B | Focuses on ex-factory revenues for cardiovascular and urology only, omits intravenous segment |

The comparison shows that once definitions and input variables are harmonized, figures cluster more closely, and Mordor's balanced middle path, neither overly conservative nor inflated, offers a dependable baseline for strategic planning.

Key Questions Answered in the Report

What is the current Global Catheters Market size?

The catheters market was valued at USD 65.86 billion in 2026 and is projected to reach USD 89.05 billion by 2031.

Who are the key players in Global Catheters Market?

Hollister, Medtronic Plc, Coloplast, Becton, Dickinson and Company and B. Braun Melsungen AG are the major companies operating in the Global Catheters Market.

Which is the fastest growing region in Global Catheters Market?

Asia Pacific is estimated to grow at the highest CAGR over the forecast period (2026-2031).

Which product segment leads the catheters market?

Cardiovascular catheters hold the top spot, representing 28.35% of global revenue in 2025.

Page last updated on: