Anal Irrigation Systems Market Size and Share

Market Overview

| Study Period | 2020 - 2031 |

|---|---|

| Market Size (2026) | USD 357.73 Million |

| Market Size (2031) | USD 423.39 Million |

| Growth Rate (2026 - 2031) | 3.42% CAGR |

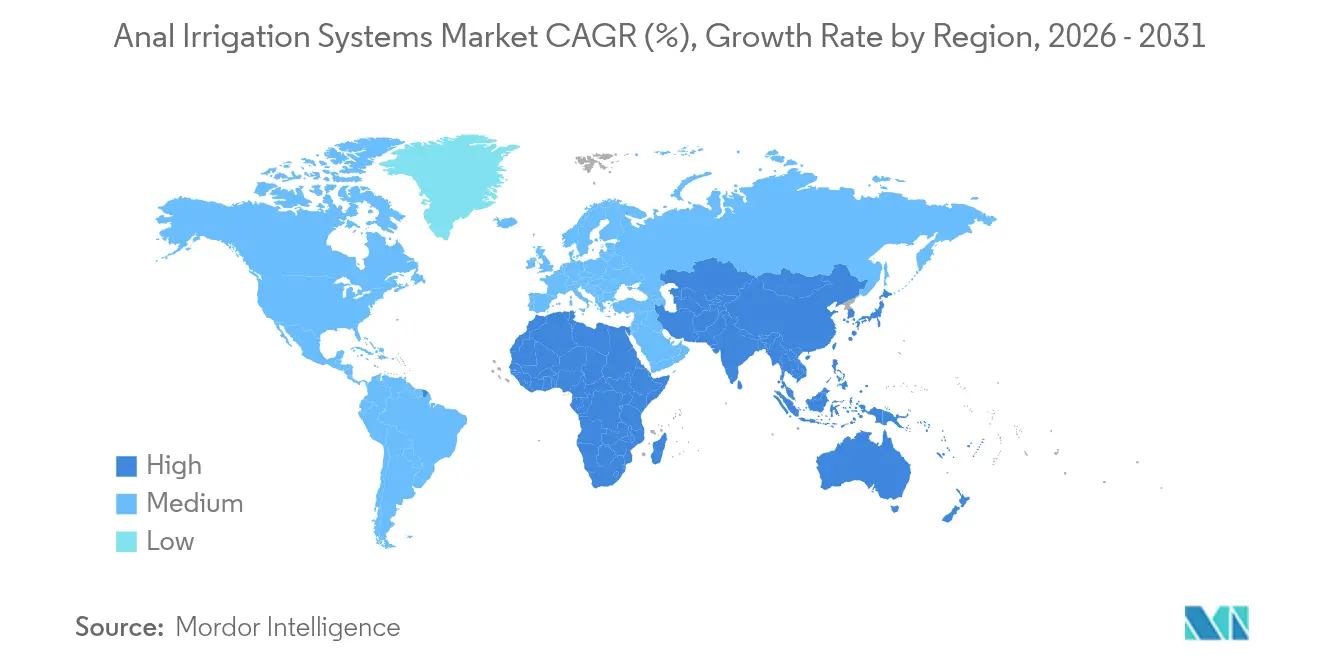

| Fastest Growing Market | Asia Pacific |

| Largest Market | North America |

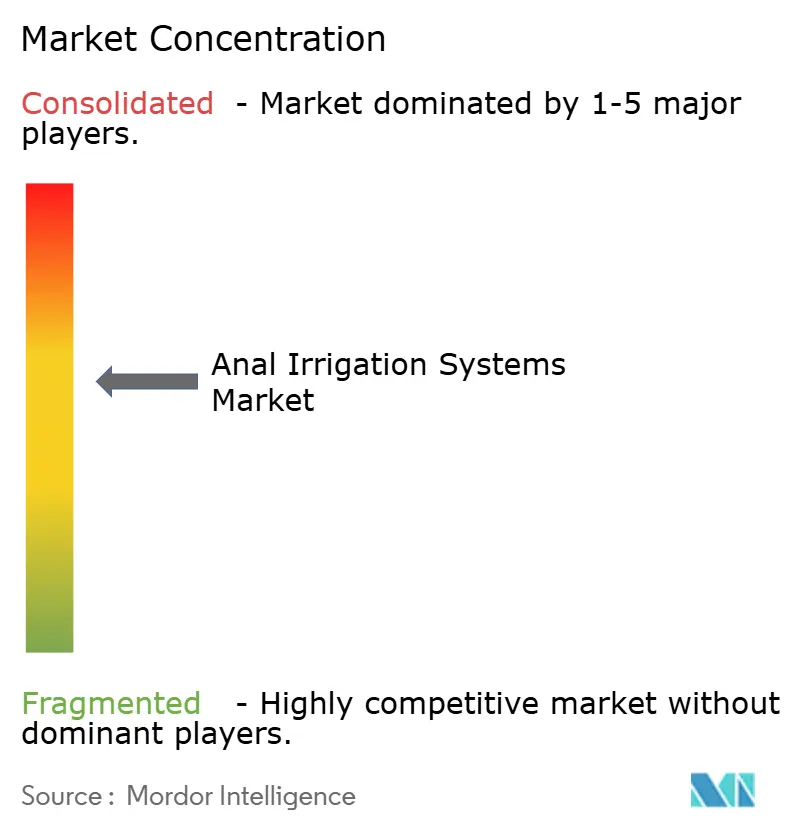

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

Anal Irrigation Systems Market Analysis by Mordor Intelligence

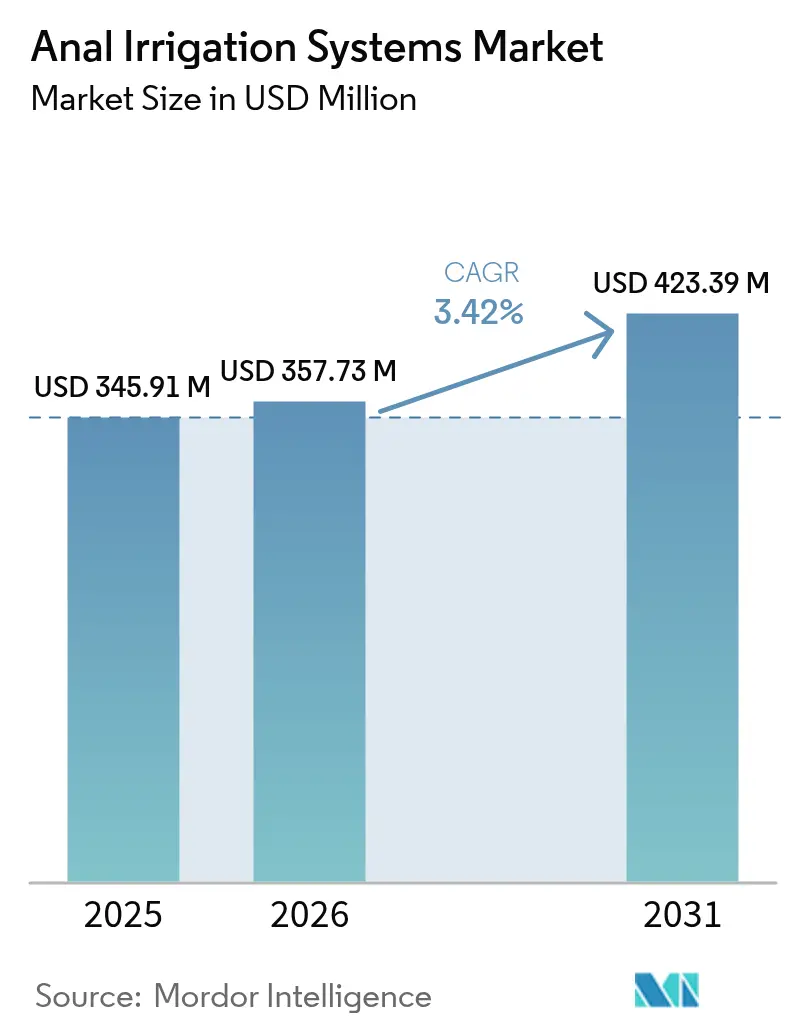

The Anal Irrigation Systems market size is expected to grow from USD 345.91 million in 2025 to USD 357.73 million in 2026 and is forecast to reach USD 423.39 million by 2031 at 3.42% CAGR over 2026-2031.

Growth rests on healthcare payers embracing transanal irrigation as a cost-saving alternative to conservative bowel care, alongside technological shifts that make devices easier to use and monitor at home. A steadily ageing population, earlier onset of colorectal cancer, and expanding reimbursement codes for neurogenic bowel dysfunction ensure a predictable demand baseline. Manufacturers are responding with electronic pump systems that automate pressure and volume control, helping clinicians curb adverse events while freeing nursing time. Geographic diversification further underpins expansion as Asia-Pacific health systems modernize long-term continence care.

Key Report Takeaways

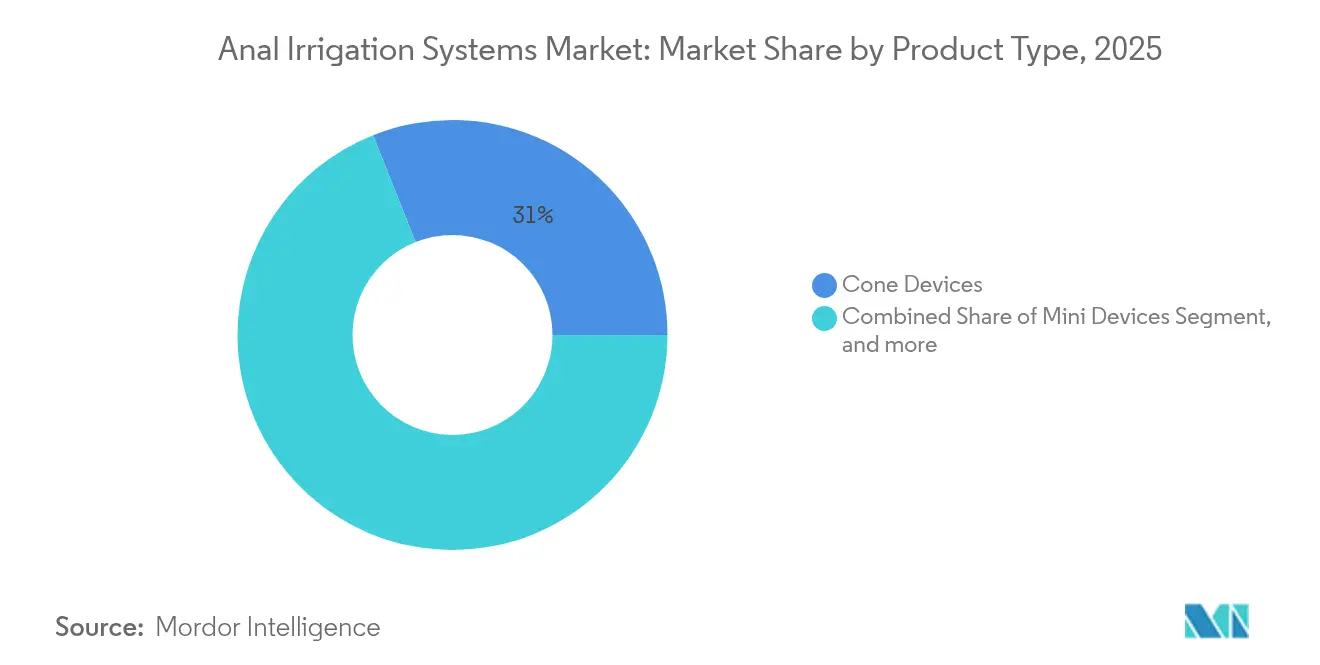

- By product type, cone devices led with 31.02% revenue share in 2025; electronic pump systems are forecast to advance at a 5.41% CAGR through 2031.

- By irrigation volume, the 300-1000 mL range accounted for 52.55% of the anal irrigation systems market share in 2025, whereas treatments exceeding 1,000 mL will grow at a 6.05% CAGR to 2031.

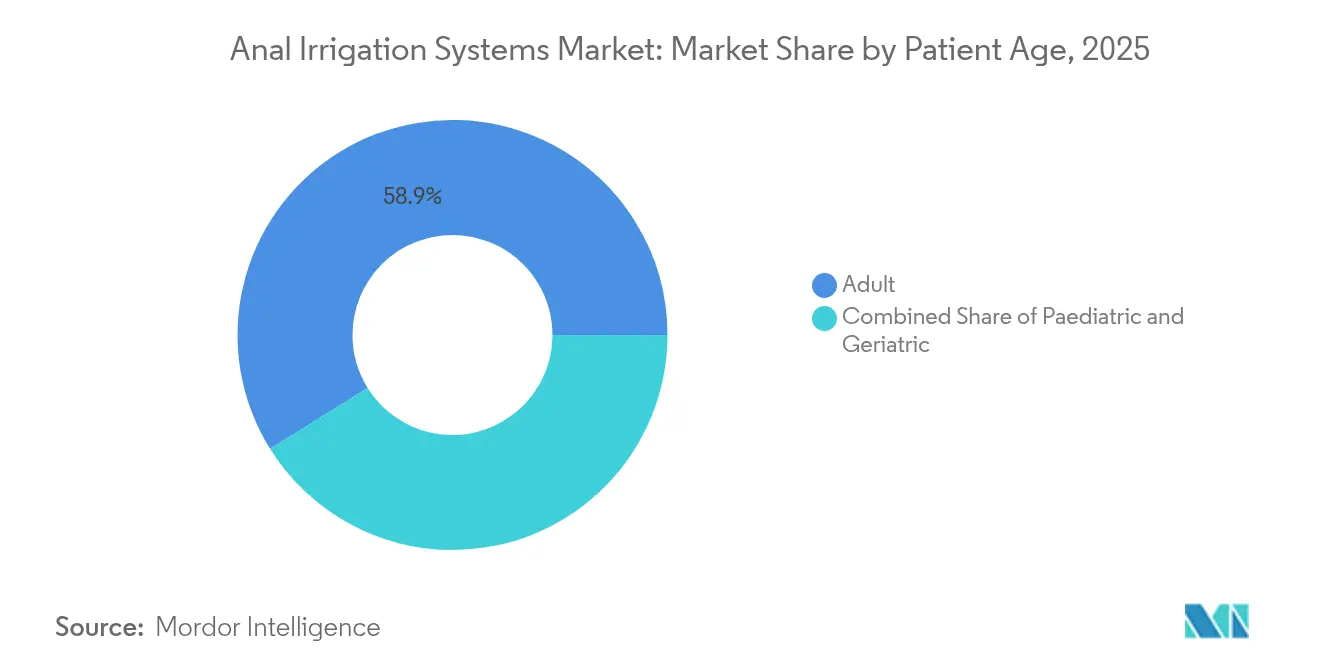

- By patient age, adults captured 58.87% share of the anal irrigation systems market size in 2025, while the pediatric segment is set to expand at 6.32% CAGR between 2026-2031.

- By end user, hospitals held 42.72% of 2025 revenue yet home-care settings are projected to register a 7.02% CAGR through 2031.

- By geography, North America maintained 39.28% share in 2025; Asia-Pacific is poised for the fastest 5.76% CAGR to 2031.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of 2026.

Global Anal Irrigation Systems Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Growing Incidence of Colorectal Cancer & IBD | +0.8% | Global, With Higher Impact In North America & Europe | Medium Term (2-4 Years) |

| Rising Preference For Minimally-Invasive Bowel Management | +0.6% | Global, Particularly Developed Markets | Short Term (≤ 2 Years) |

| Reimbursement Expansion For Neurogenic Bowel Dysfunction | +0.5% | North America & Eu, Expanding To Apac | Medium Term (2-4 Years) |

| Shift Toward Home-Care & Tele-Nursing Delivery Models | +0.7% | Global, Led By North America | Short Term (≤ 2 Years) |

| Device Miniaturisation & Electronic Pump Integration | +0.4% | Global, Technology-Driven Markets First | Long Term (≥ 4 Years) |

| Emergence Of Digital-Twin Clinician Training Simulators | +0.2% | North America & Europe Initially | Long Term (≥ 4 Years) |

| Source: Mordor Intelligence | |||

Growing Incidence of Colorectal Cancer & IBD

Earlier-age colorectal cancer diagnoses and rising inflammatory bowel disease prevalence among citizens aged 60 years and above are steadily enlarging the eligible patient pool for transanal irrigation. Post-surgical survivors rely on structured irrigation to regain continence, cutting emergency visits by 40-60% when compared with conservative laxative regimens.[1]Science Daily, “Early-Onset Colorectal Cancer Trends,” sciencedaily.com The dual demographic pressures of ageing and earlier disease onset force hospitals to balance immediate postoperative needs with lifelong symptom control. These patterns favor automated electronic pumps because the technology minimizes manual handling and lowers infection-risk touchpoints. As patient cohorts broaden, payers find irrigation a budget-relief lever that averts costly ostomies.

Rising Preference for Minimally-Invasive Bowel Management

Healthcare professionals frame transanal irrigation as a bridge therapy that can defer or even negate permanent colostomy procedures. Remote patient-monitoring platforms covered 81% of US clinicians by 2023, making it straightforward to supervise home irrigation sessions from a distance. For payers, at-home care shaves 30% off facility costs and raises satisfaction scores, thus spurring coverage decisions. Patient surveys reveal 85% of neurogenic bowel dysfunction sufferers would choose irrigation over surgery once educated on outcomes. Pediatric uptake quickens as caregivers pursue non-invasive management for spina bifida and related anomalies, pointing to sustained unit demand.

Reimbursement Expansion for Neurogenic Bowel Dysfunction

The 2024-2025 Medicare HCPCS updates widened coverage for irrigation consumables, trimming out-of-pocket expense and prompting more prescriptions.[2]Emergo by UL, “Medicare Home Health PPS Final Rule 2025,” emergobyul.com A concurrent 2.7% rise in the Home Health Prospective Payment System further funds house-based training sessions. Across Europe, transanal irrigation already holds “essential therapy” status, a benchmark that emerging markets reference when rewriting benefit catalogs. Private actuaries quantify 3-year savings of USD 15,000-25,000 per patient relative to surgical diversion, emboldening insurers to reimburse high-volume (exceeding 1,000 mL) systems that achieve stronger cleansing.

Shift Toward Home-Care & Tele-Nursing Delivery Models

Roughly 50 million Americans engage with remote patient-monitoring gadgets, a foundation that supports connected irrigation platforms fitted with flow and pressure sensors. Fifth-generation wireless networks allow real-time guidance, meaning complex bowel protocols no longer require clinic visits. Telehealth usage multiplied 38x through recent years, familiarizing patients with virtual coaching and easing rollouts of irrigation programs. Health-workforce shortages heighten demand for devices that reduce bedside workload yet uphold safety through automated shut-offs. Electronic pumps equipped with data loggers feed adherence metrics to clinicians, ensuring ongoing care quality without intensive labor inputs.

Restraints Impact Analysis*

| Restraint | (~) % Impact On CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Risk of Bowel Perforation & Other Adverse Events | -0.4% | Global, Higher Impact in Emerging Markets | Short Term (≤ 2 Years) |

| Low Disease Awareness in Low- & Middle-Income Countries | -0.6% | APAC, MEA, Latin America | Medium Term (2-4 Years) |

| High Per-Patient Cost from Single-Use Disposables | -0.3% | Global, Cost-Sensitive Markets | Short Term (≤ 2 Years) |

| Sustainability Pressure on Single-Use Plastics | -0.2% | Europe & North America Initially | Long Term (≥ 4 Years) |

| Source: Mordor Intelligence | |||

Risk of Bowel Perforation & Other Adverse Events

Although serious complications occur at merely 0.1-0.3% of procedures, fear of liability deters some hospitals, especially in regions lacking specialist oversight. The US FDA’s 2024 guidance tightened post-market surveillance, nudging vendors to integrate multi-sensor pressure shut-offs that cut tissue-damage risk.[3]Starfish Medical, “FDA Guidance on Bowel Device Safety,” starfishmedical.com Broader dissemination into general practice amplifies training requirements because operators outside tertiary centers may be unfamiliar with nuanced protocols. Rigorous patient screening therefore remains a pivotal safety net, limiting therapy to anatomically suitable candidates.

Low Disease Awareness in Low- & Middle-Income Countries

In many emerging economies, neurogenic bowel dysfunction remains under-diagnosed and commonly routed to surgical diversion due to limited knowledge of alternative care. Regulatory fragmentation forces device companies to pursue separate national approvals, slowing product launches. Rural infrastructure shortages hamper post-purchase training, and cultural taboos can stifle patient demand. These gaps particularly affect pediatric cases, where early intervention could avert lifelong complications yet seldom reaches caregivers in time.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Product Type: Innovation Accelerates Electronic Pump Adoption

Electronic pumps registered the quickest 5.41% CAGR from 2026-2031, even as cone devices retained a 31.02% slice of 2025 revenue. Automated pressure and volume algorithms enhance consistency and lower manual dexterity needs, aligning with clinician mandates for standardized outcomes. Coloplast’s July 2024 digital leakage notification release illustrates how mobile connectivity elevates irrigation from a stand-alone tool into a real-time continence platform. Balloon catheters persist in high-risk cohorts needing gentle pressure regulation, particularly frail geriatric and pediatric groups. Mini devices satisfy active lifestyles by prioritizing discretion, while bed-mounted rigs remain fixtures in long-term care wards. Improvement in lithium-ion energy density and piezoelectric micropumps allows battery-powered units to deliver higher flow volumes without inflating device weight, thus widening adult home-care eligibility. Sensor fusion technologies further mitigate perforation risk through live feedback loops, an advance that calms provider liability concerns and ultimately spurs wider prescribing.

Clinical outcomes evidence underpins this momentum. Studies link electronic systems to 20% shorter irrigation sessions and 15% fewer incomplete evacuations versus manual cones, translating into robust adherence rates. As hospital staffing shortages intensify, administrators appreciate the time savings and remote-monitoring dashboards that electronic units supply. These value propositions directly influence procurement in North America and the European Union, markets that collectively account for most global device tenders. In lower-income geographies, first-generation cones still dominate owing to price sensitivity, yet vendor finance programs are lowering acquisition hurdles for pump-based kits. The resulting competitive dynamic pushes suppliers to broaden portfolios, ensuring that every care setting can access an appropriate device tier without sacrificing safety.

By Irrigation Volume: Clinical Protocols Trend Toward Higher Dosages

Volumes in the 300-1000 mL bracket maintained 52.55% of global revenue during 2025, a reflection of long-standing balance between efficacy and patient comfort. However, data correlating exceeding 1,000 ml irrigation with steeper reductions in fecal impaction episodes is driving a measurable 6.05% CAGR in that bracket through 2031. Institutions are revising care pathways to start patients on moderate dosages before stepping up to larger volumes once tolerance improves. Electronic pumps facilitate that transition, as firmware sets graduated flow ramps preventing cramping. Higher-dosage uptake also ties into payer economics, given evidence that robust cleansing cuts readmissions tied to obstruction.

Sub-300 mL protocols remain vital for pediatrics and adults with limited rectal capacity. Clinicians frequently favor balloon catheters in these cases because precision seals prevent retrograde leakage at low volumes. Despite slower revenue growth, this cohort offers recurring consumable sales, particularly catheter sleeves and valves. Device makers thus treat volume segmentation not as mutually exclusive silos but as patient-journey milestones, designing kits that allow nozzle swaps or firmware updates when advancing from 300 mL to 1 000 mL regimens. Such modular pathways help preserve brand loyalty, an intangible yet crucial differentiator in a maturing competitive field.

By Patient Age: Pediatrics Display the Sharpest Uptrend

Adults aged 18-64 represented 58.87% of the anal irrigation systems market size in 2025, primarily stemming from colorectal cancer survivors, spinal cord injuries, and inflammatory bowel disease sufferers. In contrast, the pediatric cohort under 18 will expand at 6.32% CAGR thanks to proactive bowel programs for spina bifida and anorectal malformations. Children’s device adherence hinges on portability and noise reduction, prompting R&D into micro-pumps and child-friendly user interfaces. Hospitals tailoring family education sessions report 25% higher compliance versus facilities delivering generic adult-graphic manuals. Such findings reveal that market volume growth is as much about behavioral science as hardware.

The geriatric band ≥65 years continues to witness moderate, steady demand as age-linked constipation and neurological diseases accumulate. Yet frailty often complicates independent use, necessitating caregiver involvement or simplified design. Manufacturers answer with low-force hand pumps and enlarged touchscreens. Although these interventions raise bill of materials, they help safeguard share in an aging world. Taken together, age segmentation keeps revenue risk diversified. While adult cases dominate absolute numbers, the pediatric and senior categories carry enough incremental momentum to stabilize vendor cash flows over business cycles.

By End User: Home-Care Transition Redefines Service Models

Hospitals retained 42.72% of 2025 revenue because they initiate therapy, conduct colon physiology tests, and teach first-time users. Even so, home-care channels are growing at 7.02% CAGR as reimbursement frameworks fund domiciliary equipment bundles. Digital telemetry gives nurses visibility into dwell time, refill volumes, and adherence without physical visits, slicing service costs. Health systems keen to optimize bed capacity consequently shift stable patients to self-management within two weeks of first instruction.

Ambulatory surgery centers and specialty gastroenterology clinics bridge the gap by conducting follow-ups and nozzle fittings. Their throughput depends on fast device set-ups, a factor pushing manufacturers to deliver color-coded kits that minimize assembly errors. The rise of home-care dovetails with broader consumerism in healthcare: patients value autonomy and discreet routines. Suppliers thus bundle mobile apps that send refill reminders and connect users to 24-hour helplines. This ecosystem orientation converts single-unit sales into lifetime customer relationships, amplifying the long-tail revenue potential of consumables such as irrigation sleeves and sterile water cartridges.

Geography Analysis

North America’s 39.28% share traces to Medicare code expansions enacted in 2024 that sliced patient copayments and galvanized clinician prescriptions. A 2.7% home-health payment bump in 2025 further incentivizes care managers to transition suitable cases from hospital wards to living rooms, supported by remote dashboards that track pressure, duration, and leakage metrics. Staffing shortages amplify uptake of connected pumps, which can cut nurse time per session by 15%. Payers consider this a lever against rising overtime costs and potential union friction.

In Europe, national health systems formally designate transanal irrigation an essential neurogenic bowel therapy, ensuring device and consumable funding across primary and tertiary care. The bloc’s sustainability agenda spurs R&D into biodegradable plastics, an area where corporate alliances between polymer chemists and device OEMs are intensifying. Hospitals generate 34 pounds of waste per patient daily, putting device makers under regulatory and reputational pressure to cut single-use content. Nordic countries serve as living laboratories: Sweden’s e-prescription portals are already integrating irrigation data feeds, an early signal that connected devices could become reimbursement prerequisites.

Asia-Pacific’s 5.76% CAGR springs from two forces ageing populations and policy-backed infrastructure upgrades. Market research forecasts a USD 225 billion regional med-tech arena by 2030, of which bowel management will claim a rising slice. China’s oncology burden alone creates millions of ostomy-avoidance candidates. Yet commercial success demands culturally sensitive education campaigns to overcome stigma. Local distributors that bundle training with device rental packages achieve higher reorder rates than those selling hardware alone. Governments also pivot towards outcome-based procurement, rewarding vendors whose pumps document reduced readmissions, thereby reinforcing integration of data analytics modules.

Competitive Landscape

The anal irrigation systems market occupies a middle ground on the consolidation spectrum. Three multinationals—Coloplast, Wellspect Healthcare, and Convatec Group—together hold a meaningful slice of global revenue, but numerous niche entrants press margins with specialized designs or regional footprints. Competitive intensity has tilted toward digital augmentation: Coloplast’s July 2024 sensor-based leakage alert converts passive bags into proactive monitoring assets, a template that rivals are fast emulating . Integrated software platforms not only differentiate products but also forge data streams attractive to payers looking for objective adherence metrics.

White-space opportunities cluster in pediatric devices, still underserved by standard adult-sized cones or balloons. Hospitals such as the Children’s Hospital of Philadelphia originate bespoke solutions like the Indepenema, drawing attention to family-centric ergonomics that mass manufacturers now rush to replicate. Sustainability concerns equally open doors. Start-ups collaborate with university polymer labs to develop compostable catheters, hedging against European plastic levies slated for full enforcement after 2028. Patent analysis shows heightened filings in pressure-feedback algorithms and clog detection, territories where Motus GI Medical Technologies and other innovators are active.

Strategic alliances proliferate as manufacturers recognize that raw hardware profits are narrowing. Wellspect rolled out a subscription model bundling consumables, nurse hotline access, and predictive analytics, thereby securing annuity streams that buffer price competition. Distributors in emerging markets negotiate performance-based contracts, tying quarterly volumes to training milestones verified through cloud dashboards. Equity investors view such service overlays as valuation multipliers because they facilitate double-digit recurring revenue growth even when capital-equipment sales plateau.

Anal Irrigation Systems Industry Leaders

Consure Medical Pvt. Ltd.

ConvaTec Group PLC

Coloplast A/S

Becton, Dickinson, and Company

Renew Medical Pty Ltd. (Aquaflush Medical Limited)

- *Disclaimer: Major Players sorted in no particular order

Market Opportunities and Future Outlook

Opportunities center on expanding transanal irrigation (TAI) beyond traditional neurogenic bowel dysfunction pathways, while tightening adherence and safety in home-care settings. A 2025 clinical consensus on safe initiation and monitoring codifies structured follow-ups, with early reviews at 1-2 weeks and additional checkpoints around 4 weeks and 6-8 weeks. That workflow creates room for manufacturers and providers to package standardized training, tele-nursing support, and digital adherence tools alongside devices.

This direction also fits the report’s home-care shift and the move toward connected electronic pump systems that automate pressure and volume control. It further supports stepped protocols that start patients on moderate volumes (300-1000 mL, the largest 2025 share) and escalate to higher-dose regimens (>1,000 mL) when tolerance improves. Portfolio expansion into lower-volume, easier-to-start options can also broaden eligible use cases and reduce drop-off during the trial period. Coloplast’s introduction of Peristeen Light in February 2024 reflects ongoing vendor focus on simplifying access and use, and NICE’s December 2025 update migrating Medical Technologies Guidance 36 to HealthTech Guidance 462 for the Peristeen Plus system provides an evidence-based reference point that procurement teams and continence services use in adoption decisions. On compliance and quality, 2026 US FDA GUDID listings for established systems indicate continued product availability and refresh cycles in regulated markets, reinforcing the need for suppliers to keep device master data, labeling, and post-market documentation current as hospital and payer pathways standardize home initiation and monitoring.

Recent Industry Developments

- June 2026: US FDA device registry updates (GUDID) continued to list established transanal irrigation systems used in home and clinical settings, supporting ongoing availability of core platforms such as Peristeen and Navina. Keeping these listings current helps manufacturers sustain distribution continuity and supports procurement requirements that increasingly depend on up-to-date device identification and documentation.

- December 2025: NICE updated its UK guidance for Coloplasts Peristeen Plus by migrating Medical Technologies Guidance 36 to HealthTech Guidance 462, maintaining evidence-based support for use in managing bowel dysfunction. The change reinforces an appraisal anchor for NHS continence services and purchasing bodies when standardizing pathways and training around TAI.

- April 2024: Medline and Consure Medical announced an exclusive distribution agreement for the QiVi MEC male external urine management device in US acute care settings. While adjacent to anal irrigation, the deal highlights how access to large hospital procurement networks and bundled continence portfolios can influence competitive positioning for specialty bowel and continence device suppliers.

Research Methodology Framework and Report Scope

Market Definition and Coverage

This market covers the value of anal irrigation systems used to support bowel management through controlled rectal irrigation, across clinical and home care use. The sizing reflects device systems and related components sold for these procedures, tracked in USD at the global level.

Scope exclusions: We exclude general continence consumables, stoma-care products, and non-irrigation bowel management devices that do not deliver rectal irrigation.

Segmentation Overview

- By Product Type

- Mini Devices

- Cone Devices

- Balloon Catheter Systems

- Bed / Stationary Systems

- Electronic Pump Systems

- By Irrigation Volume

- <300 mL

- 300–1000 mL

- >1000 mL

- By Patient Age

- Paediatric

- Adult

- Geriatric

- By End User

- Hospitals

- Ambulatory Surgical Centres

- Specialty Clinics

- Home-Care Settings

- By Geography

- North America

- United States

- Canada

- Mexico

- Europe

- Germany

- United Kingdom

- France

- Italy

- Spain

- Rest of Europe

- Asia-Pacific

- China

- Japan

- India

- Australia

- South Korea

- Rest of Asia-Pacific

- Middle East & Africa

- GCC

- South Africa

- Rest of Middle East & Africa

- South America

- Brazil

- Argentina

- Rest of South America

- North America

Data Sources, Market Sizing, and Validation

Desk Research

Desk work started with public health and regulatory context so the demand pool could be kept realistic. We referred to sources such as the World Health Organization for relevant burden indicators, the US CDC for related condition signals, and the NIH PubMed database for clinical evidence and adoption discussion.

To ground commercial assumptions, we also reviewed sources such as the US FDA device database and labeling references, the European Commission MDR context pages, and selected national statistics portals where procedure and care-setting data is available. Company annual reports, investor presentations, and reputable medical press were used to map product availability, channel mix, and likely price bands. We also used paid subscriptions focused on company financials and patent databases to cross-check innovation intensity and product pipelines. These desk research sources are not exhaustive, and we consulted other public materials for data collection, validation, and clarification during the study.

Primary Interviews and Surveys

Primary inputs were collected through expert interviews and structured surveys with clinicians involved in bowel management, distributors, and manufacturer-side product and commercial teams. Because demand patterns vary by reimbursement and care setting, we covered major regions to validate adoption rates, replacement cycles, and the practical split between hospital use and home care.

Distribution of primary research fieldwork respondents

| Company type | Respondent position | Region |

|---|---|---|

| Top tier: 37% | CXOs: 14% | APAC: 39% |

| Mid tier: 47% | Functional/Unit leaders: 38% | EMEA: 37% |

| Smaller Players: 16% | Managers: 48% | Americas: 24% |

Market-Sizing & Forecasting

Sizing was built using a top-down approach where population and care-setting indicators were translated into an addressable irrigation user pool, and then converted into annual system demand using usage and replacement logic. To keep the totals realistic, we corroborated results with selective bottom-up checks, like sampled price points by device category and channel checks on typical unit throughput.

The model was informed by inputs such as the treated share for constipation and fecal incontinence cohorts that are eligible for irrigation, home care penetration rates, average system life and replacement intervals, typical irrigation kit refill attachment rates, and regional price bands after accounting for reimbursement and tendered pricing. Where direct volume indicators were thin, we handled gaps by using proxy adoption curves validated by clinicians, followed by sensitivity checks on price and replacement assumptions.

For forecasting, we used scenario analysis supported by expert views on reimbursement stability, training availability, and home care shift, then applied those scenarios to the core demand pool and price trajectory by region. Growth was not assumed to be linear, and step changes were modeled only when corroborated by policy, guideline, or channel feedback.

Data Validation & Update Cycle

Outputs were validated through triangulation across independent signals, including whether implied unit volumes align with adoption levels in key care settings and whether pricing sits within observed bands from desk research and interviews. When large variances appeared, analysts re-checked assumptions, revisited the input sources, and re-contacted selected respondents to confirm what changed and what stayed stable.

Before sign-off, the model and its drivers go through multi-step internal reviews so calculation errors and inconsistent regional logic can be caught early. The report is refreshed annually, and interim updates are made when material events occur, such as meaningful reimbursement changes, major product launches, or regulatory shifts. Right before delivery, a final pass is completed so clients receive the most current view available at that time.

Mordor Intelligence's Anal Irrigation Systems Market Estimate Compared With Other Published Estimates

Published market sizes for anal irrigation systems can look different even when the same headline name is used, because the underlying inclusions, pricing assumptions, and the year used as the comparison point are not always consistent. In practice, these gaps show up when one study mixes adjacent bowel management items into the same value pool or uses a faster adoption curve without matching it to real-world care delivery constraints.

General bowel management systems and stoma-care consumables sit outside Mordor Intelligence's scope for this market, which reduces overcounting when other figures bundle broader continence supplies into the same total. Differences also come from whether the model ties demand to treated and trained patient pools, how fast average selling prices are allowed to rise in reimbursed channels, and how often currency and inflation assumptions are refreshed across regions.

Benchmark comparison

| Source | Market Size | Gaps in Research Methodology |

|---|---|---|

| Mordor Intelligence | USD 345.91 M (2025) | |

| Industry Research Publisher A | USD 365.10 M (2025) | The higher value likely reflects broader inclusions around bowel management solutions and a looser split between irrigation kits and adjacent continence supplies, which can inflate the addressable revenue base. |

| Global Research Publisher B | USD 450.00 M (2024) | This estimate uses an earlier reference year and implies a steeper growth curve into 2031, which typically requires higher assumed adoption and price expansion without clear linkage to reimbursement and trained-user constraints. |

Taken together, the spread is mainly explained by what is counted as an irrigation system versus a broader bowel management basket, and by how aggressively adoption and pricing are pushed forward year to year. Our sizing stays traceable because each step ties back to a defined eligible user pool, care-setting penetration, and realistic replacement and pricing checks.

Key Questions Answered in the Report

Which companies lead the anal irrigation systems segment?

Coloplast, Wellspect Healthcare, and Convatec Group collectively command the largest revenue share, supported by broad portfolios and ongoing digital upgrades.

How fast is Asia-Pacific demand for irrigation devices expanding?

Regional revenue is forecast to rise at about 5.76% CAGR through 2031 as health systems modernize continence care and aging populations grow.

Why are electronic pump systems gaining popularity?

Automated pressure control, remote monitoring features, and shorter procedure times make pumps attractive to both clinicians and patients seeking reliable home therapy.

What role does reimbursement play in adoption?

Updated Medicare HCPCS codes and EU coverage policies reduce patient costs, prompting more prescriptions and accelerating home-based therapy transitions.

Are higher irrigation volumes clinically advantageous?

Evidence shows volumes exceeding 1,000 mL can further reduce fecal impaction and emergency visits, leading clinicians to escalate dosages when patient tolerance permits.

Page last updated on: