Home Medical Equipment Market Size and Share

Market Overview

| Study Period | 2020 - 2031 |

|---|---|

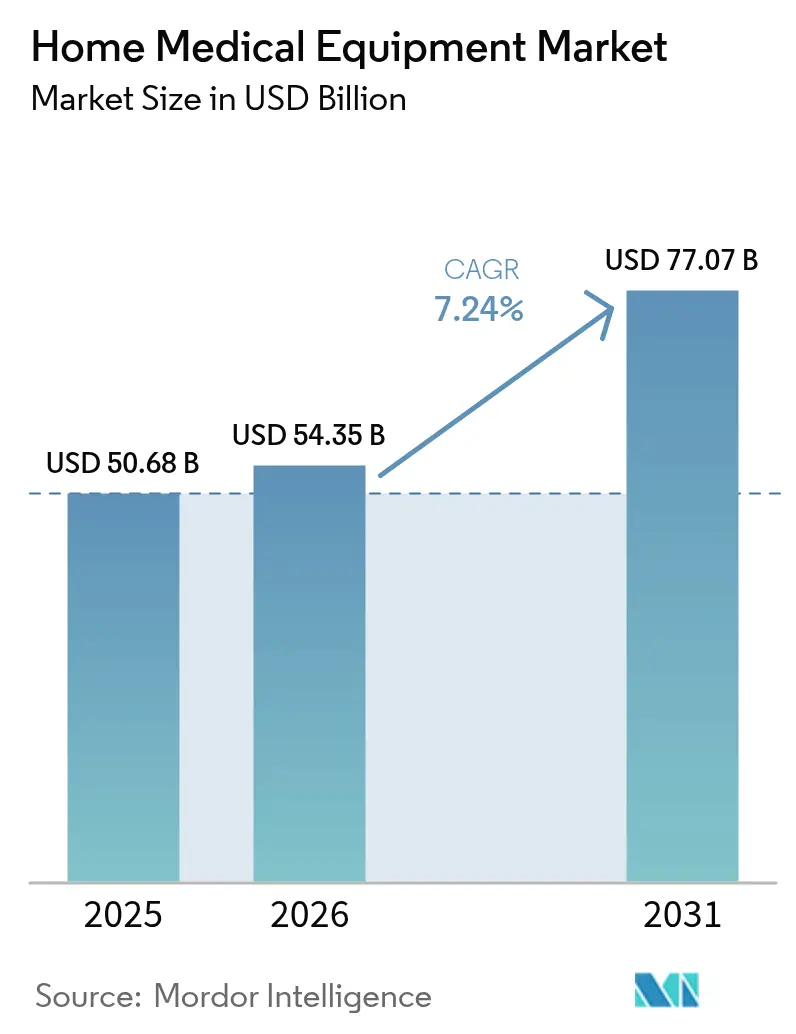

| Market Size (2026) | USD 54.35 Billion |

| Market Size (2031) | USD 77.07 Billion |

| Growth Rate (2026 - 2031) | 7.24% CAGR |

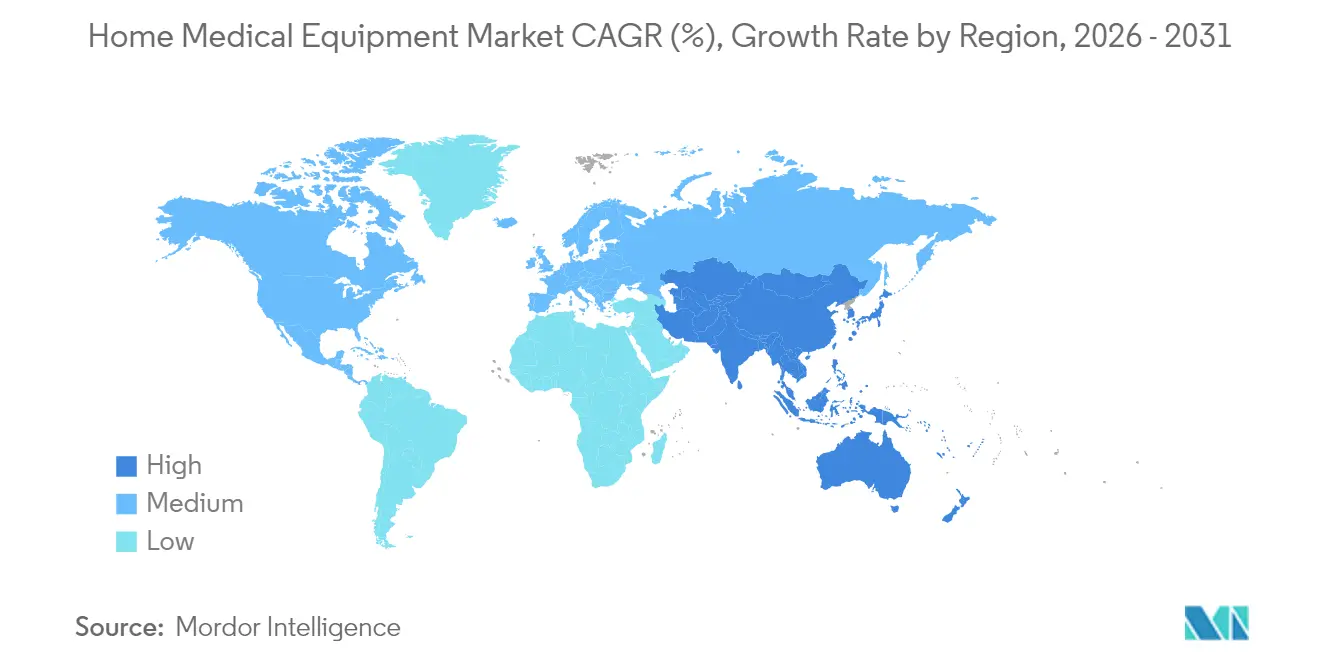

| Fastest Growing Market | Asia-Pacific |

| Largest Market | North America |

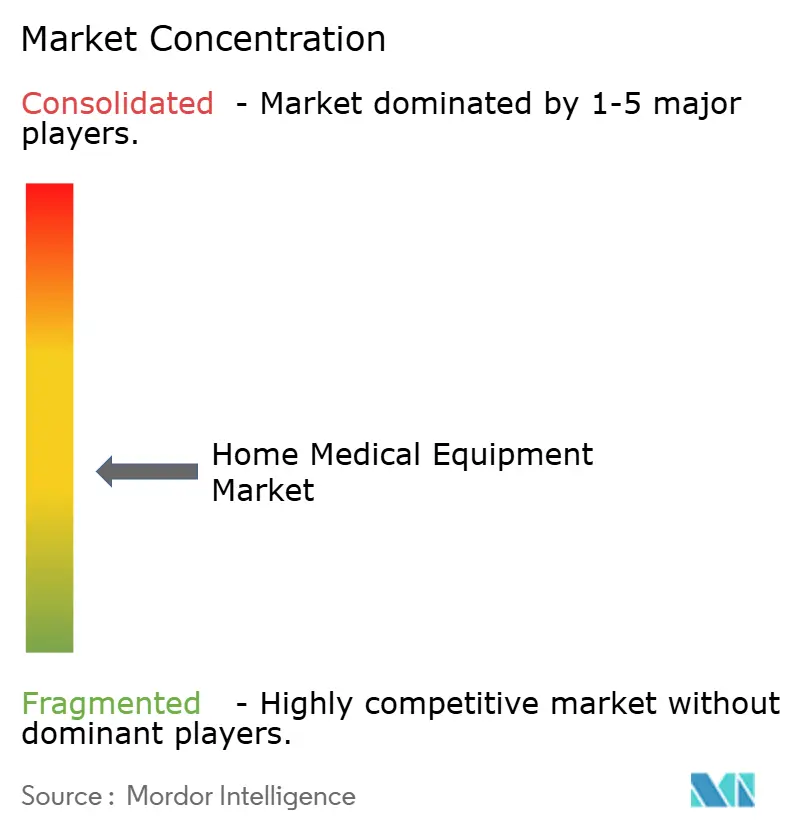

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

Home Medical Equipment Market Analysis by Mordor Intelligence

home medical equipment market size in 2026 is estimated at USD 54.35 billion, growing from 2025 value of USD 50.68 billion with 2031 projections showing USD 77.07 billion, growing at 7.24% CAGR over 2026-2031. Robust growth stems from an accelerating shift of care delivery to patient homes, cost-containment mandates, and sustained innovation in portable, connected therapeutic solutions. Demand momentum is particularly strong for devices that support chronic-disease management, remote monitoring, and long-term mobility, while policy makers widen reimbursement coverage to curb hospital utilization. Manufacturers that harmonize with evolving global quality standards, deploy data-enabled services, and scale omnichannel distribution gain a measurable competitive edge. Asia-Pacific’s rapid infrastructure build-out, North America’s favorable payer mix, and Europe’s stringent but predictable regulatory ecosystem collectively shape the geographic opportunity set for the home medical equipment market.

Key Report Takeaways

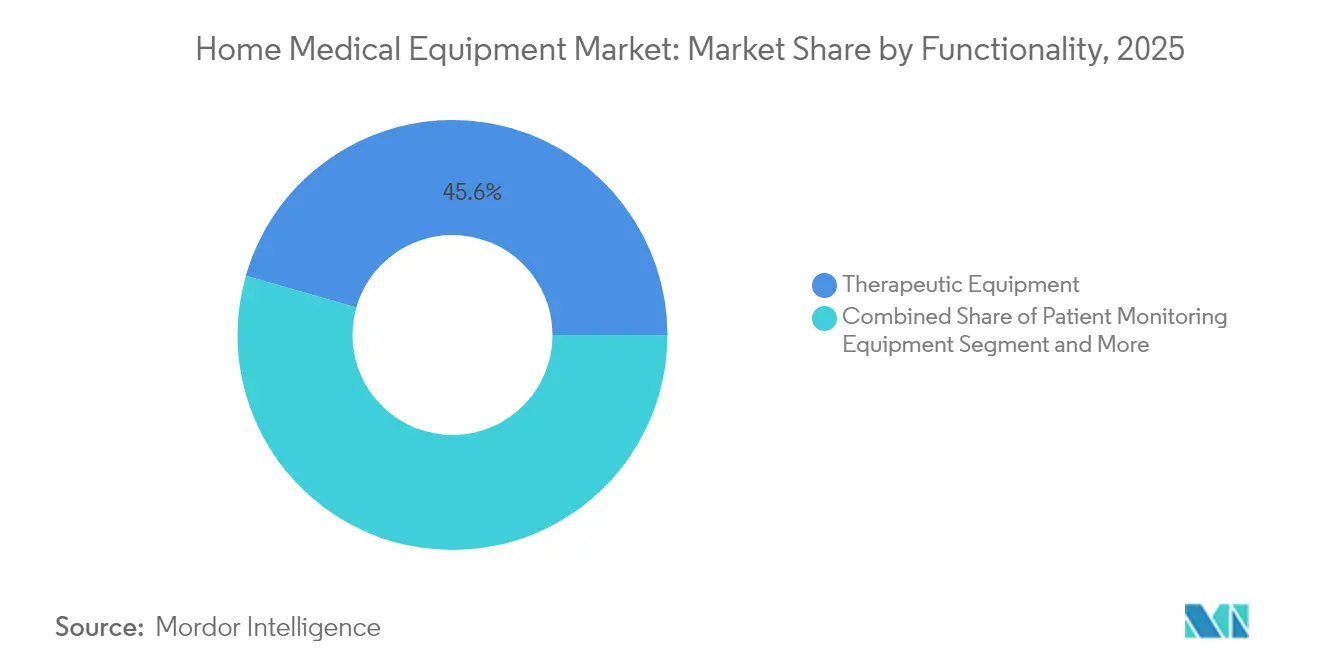

- By functionality, therapeutic equipment led with 45.55% revenue share in 2025; mobility assist and patient support is advancing at an 8.55% CAGR through 2031.

- By geography, North America commanded 37.75% of the home medical equipment market share in 2025, while Asia-Pacific is forecast to expand at a 10.25% CAGR to 2031.

- By connectivity, conventional products accounted for 54.20% of the home medical equipment market size in 2025; connected/smart devices are projected to grow at a 9.75% CAGR between 2026-2031.

- By distribution channel, retail medical stores commanded 39.85% of the market size in 2025 and online retailers is advancing at a 12.15% CAGR over 2026-2031.

- By therapeutic area, diabetes care contributed 39.35% of segment revenue in 2025 and remains the largest value pool of the home medical equipment market.

- By end-user, the elderly and assisted-living commanded a 34.35% revenue share in 2025, while chronic-disease home-care is forecast to expand at an 8.95% CAGR to 2031.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of 2026.

Global Home Medical Equipment Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Rising chronic disease burden | +2.1% | North America, Europe | Medium term (2-4 years) |

| Rapid expansion of the geriatric population | +1.8% | Japan, Western Europe, North America | Long term (≥ 4 years) |

| Cost-containment shift from in-patient to home-care | +1.5% | North America, Europe, developed APAC | Medium term (2-4 years) |

| Technological advances in portable & connected devices | +1.9% | North America, Europe, developed APAC | Short term (≤ 2 years) |

| Broadening reimbursement for home therapies | +1.2% | North America, Europe | Medium term (2-4 years) |

| Growth of e-commerce & rental models | +0.8% | Global | Short term (≤ 2 years) |

| Source: Mordor Intelligence | |||

Rising Chronic Disease Burden Accelerates Home Monitoring Adoption

Global prevalence of diabetes, COPD, and cardiovascular disorders is reshaping therapeutic priorities in the home medical equipment market. Continuous glucose monitoring systems now anchor 40% of therapeutic-area revenue, propelled by FDA clearances that allow factory-calibrated sensors and automated insulin-delivery algorithms. Portable oxygen concentrators and home dialysis units follow similar growth trajectories as payers incentivize self-management to prevent costly acute episodes. Healthcare providers increasingly integrate device-generated data into telehealth workflows, enhancing longitudinal care coordination and reinforcing adherence[1]Center for Devices and Radiological Health, “FDA Launches Health Care at Home Initiative to Help Advance Health Equity,” fda.gov.

Aging Population Drives Demand for Mobility and Monitoring Solutions

Adults aged 65+ will represent 21% of the U.S. population by 2030, and most prefer to age in place. That demographic shift materially enlarges the addressable base for wheelchairs, patient lifts, fall-prevention sensors, and non-invasive vital sign monitors. Lightweight composite frames, power-assist motors, and radar-based occupancy detection reduce caregiver burden and broaden use beyond post-acute scenarios. Long-term services providers expand home-based offerings to capture this persistent demand pool, reinforcing the growth outlook for the home medical equipment market.

Home-Care Shift Transforms Healthcare Delivery Models

Payers and regulators frame the home as an extension of the clinical continuum. The FDA’s “Home as a Health Care Hub” initiative (April 2024) formally recognizes residences as active sites of medical care and prioritizes technology that can close gaps created by workforce shortages and hospital bed constraints. Hospital-at-home programs, remote therapeutic monitoring codes, and bundled payments for post-discharge episodes further cement this structural pivot and safeguard long-term growth of the home medical equipment market.

Technological Advances Enable Remote Patient Monitoring Revolution

Connectivity, miniaturization, and embedded analytics elevate home devices from episodic tools to real-time clinical assets. Nearly 1,000 AI-enabled medical devices had FDA clearance by early-2025, covering diagnostics, dosage optimization, and early warning alerts. Radar-based sensors that operate contact-free detect respiration and heart rate, while cloud portals push anomalies to clinicians within seconds. Industry alliances, such as GE HealthCare’s partnership with Biofourmis to create virtual care-at-home pathways, exemplify how platform integration accelerates product adoption and extends revenue beyond hardware[2]GE HealthCare, “GE HealthCare and Biofourmis Collaborate to Extend Patient Monitoring Outside the Hospital,” biofourmis.com.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Stringent regulatory & quality compliance | -1.3% | Global | Short term (≤ 2 years) |

| Semiconductor & sensor supply-chain volatility | -0.9% | Global | Short term (≤ 2 years) |

| Safety-related recalls undermining confidence | -0.4% | North America | Medium term (2-4 years) |

| High up-front costs & limited coverage in emerging markets | -0.7% | APAC, Latin America, MEA | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

Regulatory Complexity Creates Market Entry Barriers

In January 2024 the FDA finalized its Quality Management System Regulation, aligning U.S. requirements with ISO 13485:2016. Manufacturers must update design, supplier, and post-market surveillance processes before enforcement begins February 2, 2026. Simultaneously, the EU Battery Regulation 2023/1542 adds cradle-to-grave obligations for portable-device power sources, impacting infusion pumps and glucose meters alike. Compliance costs and documentation workload weigh heaviest on small firms, trimming near-term expansion pacing within the home medical equipment market.

Supply Chain Vulnerabilities Threaten Production Continuity

Geopolitical tensions, natural disasters, and cyclical demand swings disrupt semiconductor and sensor supply, leaving connected device manufacturers exposed to unpredictable lead times. Strategic responses include dual-sourcing, on-shoring of mature-node fabrication, and modular design that allows component substitution without re-validation. While these initiatives shore up resiliency, they also inflate bill-of-materials costs in the short term, tempering price competitiveness in the home medical equipment market.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Functionality: Therapeutic Equipment Anchors Value While Mobility Solutions Accelerate

Therapeutic equipment retained a 45.55% revenue contribution in 2025, reflecting the indispensable role of respiratory therapy devices, dialysis systems, and infusion pumps in chronic-disease management. Conversely, mobility assist and patient support equipment is the fastest-expanding cohort at 8.55% CAGR through 2031, mirroring rising demand for aging-in-place services. AI-driven respirators, peritoneal dialysis cyclers outfitted with telemetric modules, and sensor-enabled hospital beds enhance adherence and streamline clinician oversight. The home medical equipment market size for mobility solutions is on track to add USD 6.25 billion between 2026 and 2031, buoyed by reimbursement enhancements and ergonomic advances.

Autonomous vital-sign technologies such as radar-based monitors illustrate ongoing convergence across functionality categories. These contactless systems integrate seamlessly with electronic health records, flagging deterioration events sooner than conventional point-in-time devices. Device neutrality—ability to pair with multiple data platforms—emerges as a principal buying criterion among health systems and large home-care agencies, reinforcing the strategic importance of interoperability within the home medical equipment market.

By Therapeutic Area: Diabetes Care Leads; Neuro-Rehabilitation Exhibits Outsize Momentum

Diabetes care holds 39.35% of therapeutic-area revenue, supported by widespread deployment of factory-calibrated continuous glucose monitors and hybrid closed-loop insulin pumps. The home medical equipment market size for diabetes management is projected to surpass USD 29.4 billion by 2031 on the back of newer biosensor chemistries and extended-wear adhesives. Neuro-rehabilitation, although smaller in absolute terms, posts the highest forecast CAGR at 9.15%. Robotic exoskeletons, wearable motion-capture sleeves, and interactive VR therapy suites deliver quantifiable functional gains, hastening coverage among workers’ compensation plans and neuro-specialty clinics.

Respiratory and cardiovascular applications maintain double-digit revenue shares, driven by COPD prevalence and heart failure hospitalizations. Integrated wound-care kits and home hemodialysis platforms display steady uptake as device makers miniaturize components and embed wireless diagnostics, preventing service interruptions and elevating treatment fidelity across the home medical equipment market.

By Connectivity: Smart Devices Outpace Conventional Equipment

Conventional products represented 54.20% of 2025 shipments, yet connected and smart devices are tracking a 9.75% CAGR through 2031—nearly 3 percentage points above the total home medical equipment market. Embedded Bluetooth LE, cellular IoT, and edge AI processors transform standalone apparatus into continuous data streams. Remote firmware upgrades mitigate recall risk by allowing cyber-patches without field technician visits. The cybersecurity provision in the Consolidated Appropriations Act of 2023 obliges pre-market submissions to include Software Bills of Materials, prompting vendors to embed secure-by-design protocols from concept stage.

By Distribution Channel: Online Retailers Disrupt Traditional Models

Brick-and-mortar medical stores captured 39.85% of 2025 revenue, but e-commerce platforms are set to grow 12.15% annually as consumers prize doorstep delivery and transparent pricing. Large device makers now operate brand-owned web shops, supplementing authorized resellers and subscription refill programs. Hospitals discharge planners increasingly route durable equipment orders through integrated digital portals, collapsing ordering friction and reducing readmission penalties. The omnichannel imperative reshapes logistics footprints and elevates last-mile performance standards throughout the home medical equipment market.

By End-User: Elderly Care Dominates; Chronic-Disease Home-Care Grows Fastest

The elderly and assisted-living cohort commanded 34.35% share in 2025, loaned momentum by demographic aging and value-based care metrics that favor low-acuity settings. AI dashboards that predict falls or urinary-tract infections enable caregivers to escalate interventions promptly, aligning perfectly with payer goals around avoidable event reduction. Chronic-disease home-care follows with a 8.95% CAGR, bolstered by remote therapeutic monitoring reimbursements and widening payer recognition of self-dialysis and insulin-pump supplies. Pediatric and post-operative segments each deepen addressability as miniaturization and child-specific user interfaces alleviate historically limiting size and usability barriers. The expansion multiplies medium-term volume tributaries of the home medical equipment market.

Geography Analysis

North America retained 37.75% share in 2025, underpinned by Medicare’s Durable Medical Equipment benefit set, private payer parity laws, and prolific early adoption of connected devices. The region’s home medical equipment market size for AI-enabled patient monitoring exceeded USD 4.3 billion in 2026 and is pacing double-digit growth as clinical staffing gaps widen. Strategic policy initiatives like Hospital-at-Home waivers extend inpatient-equivalent reimbursement into residential settings, catalyzing further uptake.

Asia-Pacific is the fastest-growing geography with a 10.25% CAGR through 2031. China’s Healthy China 2030 roadmap, Japan’s Community-Based Integrated Care System, and India’s Production-Linked Incentive scheme collectively expand local manufacturing depth and equipment accessibility. A rising middle class, coupled with high mobile broadband penetration, accelerates direct-to-consumer acquisition and regional cloud-hosted telehealth scale-up. The resulting home medical equipment market share uplift is most pronounced in connected glucometers and motorized wheelchairs adapted for smaller dwelling sizes.

Europe maintains substantive volume, leveraging universal coverage and community nursing programs that formalize device deployment protocols. The EU Battery Regulation introduces carbon footprint disclosure and mandatory replaceability for portable device batteries, nudging manufacturers toward modular designs that simplify serviceability and align with the bloc’s circular-economy goals. Nordic countries showcase the highest per-capita expenditure owing to strong social-insurance backing, while Southern Europe advances at an accelerated clip from a lower baseline, collectively reinforcing continent-wide stability in the home medical equipment market.

The Middle East & Africa and South America contribute smaller slices but report quickening momentum as health ministries invest in primary-care networks and private insurers launch disease-specific home-care bundles. GCC nations prioritize long-term ventilator procurement amid local respiratory disease prevalence, whereas Brazil’s supplementary-health segment contracts direct-to-patient equipment leases. Currency volatility and fragmented reimbursement remain headwinds yet expected infrastructure upgrades promote longer-term penetration gains for the home medical equipment market.

Competitive Landscape

The sector exhibits moderate fragmentation: top conglomerates—Medline Industries, Omron Healthcare, and ResMed—control significant global revenue. Their advantages include broad portfolios, proprietary algorithms, and high-service distribution footprints that reinforce stickiness among large provider systems. Mid-tier specialists focus on niche innovations such as radar-based vitals monitoring or AI-guided rehabilitation robotics, resulting in differentiated value propositions that attract strategic partnerships with payers and health systems.

Consolidation remains a defining theme. Cardinal Health introduced the Kendall SCD SmartFlow compression platform with embedded sensor analytics in November 2024, strengthening its thrombosis-prevention franchise[3]Cardinal Health, “Kendall SCD™ SmartFlow Compression System,” cardinalhealth.com. Abbott scaled continuous glucose monitoring capacity to meet escalating U.S. and EU demand following FDA clearances of next-generation sensors. ResMed outlined a profitability roadmap that integrates data-driven coaching services into its ventilator ecosystem, underscoring the growing service-revenue mix. Investment activity highlights strategic appetite for vertically integrated home-care solutions as value-based payment models spread globally.

Disruptive entrants leverage cloud-native architectures, subscription pricing, and user-centric design to capture share. Several pursue FDA De Novo pathways for AI-augmented monitoring categories, compressing time-to-market and preserving premium pricing. Strategic alliances among hardware vendors, software analytics firms, and logistics providers increasingly set competitive benchmarks around holistic solution delivery in the home medical equipment market. Price competition intensifies within commodity sub-segments such as basic walkers and bath-safety aids, pressuring low-margin manufacturers to differentiate via warranties and rapid delivery guarantees.

Home Medical Equipment Industry Leaders

Rotech Healthcare Inc.

ARKRAY, INC.

Medline Industries, Inc.

Omron Healthcare, Inc.

ResMed Corporation

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- January 2025: Guthrie and DASCO Home Medical Equipment formed a joint venture to manage Guthrie Med Supply Depot locations and streamline distribution services for regional patient population.

- November 2024: Cardinal Health launched the Kendall SCD SmartFlow Compression System in the U.S. with Patient Sensing technology that individualizes compression cycles.

Global Home Medical Equipment Market Report Scope

As per the scope of the report, home medical equipment can be referred to as the devices that are used to perform patient care at home or other private facilities managed by a nonprofessional caregiver or a family member. The equipment is used for a wide range of applications such as cardiology and urology and other applications. The Home Medical Equipment Market is Segmented by Equipment Type (Therapeutic Equipment, Patient Monitoring Equipment, and Mobility Assist and Patient Support Equipment), Distribution Channel (Retail Medical Stores, Online Retailers, and Hospital Pharmacies), and Geography (North America, Europe, Asia-Pacific, Middle East, and Africa, and South America). The market report also covers the estimated market sizes and trends for 17 different countries across major regions, globally. The report offers the value (in USD million) for the above segments.

| Therapeutic Equipment | Respiratory Therapy Equipment |

| Dialysis Equipment | |

| Intravenous / Infusion Pumps | |

| Negative-Pressure Wound-Therapy Systems | |

| Patient Monitoring Equipment | Blood Glucose Monitors |

| Blood-Pressure Monitors | |

| Multi-parameter & Wearables | |

| Mobility Assist & Patient Support | Wheelchairs (Manual, Powered) |

| Mobility Scooters | |

| Patient Lifts | |

| Medical Furniture | |

| Bathroom Safety Products |

| Respiratory Care |

| Diabetes Care |

| Cardiovascular Care |

| Renal Care |

| Wound & Skin Management |

| Neuro-rehabilitation |

| Connected / Smart Devices |

| Conventional Devices |

| Retail Medical Stores |

| Online Retailers |

| Hospital & Clinic Pharmacies |

| Other Channels |

| Chronic-Disease Home-Care |

| Elderly & Assisted-Living |

| Post-operative Care |

| Pediatric Home-Care |

| Palliative & Hospice |

| North America | United States |

| Canada | |

| Mexico | |

| Europe | Germany |

| United Kingdom | |

| France | |

| Italy | |

| Spain | |

| Rest of Europe | |

| Asia-Pacific | China |

| Japan | |

| India | |

| South Korea | |

| Australia | |

| Rest of Asia-Pacific | |

| Middle East and Africa | GCC |

| South Africa | |

| Rest of Middle East and Africa | |

| South America | Brazil |

| Argentina | |

| Rest of South America |

| By Functionality | Therapeutic Equipment | Respiratory Therapy Equipment |

| Dialysis Equipment | ||

| Intravenous / Infusion Pumps | ||

| Negative-Pressure Wound-Therapy Systems | ||

| Patient Monitoring Equipment | Blood Glucose Monitors | |

| Blood-Pressure Monitors | ||

| Multi-parameter & Wearables | ||

| Mobility Assist & Patient Support | Wheelchairs (Manual, Powered) | |

| Mobility Scooters | ||

| Patient Lifts | ||

| Medical Furniture | ||

| Bathroom Safety Products | ||

| By Therapeutic Area | Respiratory Care | |

| Diabetes Care | ||

| Cardiovascular Care | ||

| Renal Care | ||

| Wound & Skin Management | ||

| Neuro-rehabilitation | ||

| By Connectivity | Connected / Smart Devices | |

| Conventional Devices | ||

| By Distribution Channel | Retail Medical Stores | |

| Online Retailers | ||

| Hospital & Clinic Pharmacies | ||

| Other Channels | ||

| By End-User | Chronic-Disease Home-Care | |

| Elderly & Assisted-Living | ||

| Post-operative Care | ||

| Pediatric Home-Care | ||

| Palliative & Hospice | ||

| Geography | North America | United States |

| Canada | ||

| Mexico | ||

| Europe | Germany | |

| United Kingdom | ||

| France | ||

| Italy | ||

| Spain | ||

| Rest of Europe | ||

| Asia-Pacific | China | |

| Japan | ||

| India | ||

| South Korea | ||

| Australia | ||

| Rest of Asia-Pacific | ||

| Middle East and Africa | GCC | |

| South Africa | ||

| Rest of Middle East and Africa | ||

| South America | Brazil | |

| Argentina | ||

| Rest of South America | ||

Key Questions Answered in the Report

What is the current value of the global home medical equipment market?

The market is valued at USD 54.35 billion in 2026 and is forecast to reach USD 77.07 billion by 2031.

Which region is expanding the fastest in home-based medical devices?

Asia-Pacific posts the highest forecast CAGR at 10.25% due to infrastructure expansion and rising middle-class healthcare spending.

Which functional segment leads revenue?

Therapeutic equipment retains leadership with 45.55% of 2025 revenue, anchored by respiratory and dialysis products.

How are connected devices transforming home care?

IoT-enabled monitors stream real-time data to clinicians, enabling preventive interventions and fueling a 9.75% CAGR for connected products.

What regulatory changes should manufacturers prioritize?

The FDA's Quality Management System Regulation, effective February 2026, aligns U.S. rules with ISO 13485 and mandates updates to quality processes.

What is the outlook for diabetes-care devices?

Diabetes care represents 39.35% of therapeutic-area revenue and continues to grow on rising CGM adoption and automated insulin delivery innovations.

Page last updated on: