Hollow Fiber Filtration Market Size and Share

Market Overview

| Study Period | 2020 - 2031 |

|---|---|

| Market Size (2026) | USD 1.07 Billion |

| Market Size (2031) | USD 2.09 Billion |

| Growth Rate (2026 - 2031) | 14.28% CAGR |

| Fastest Growing Market | Asia-Pacific |

| Largest Market | North America |

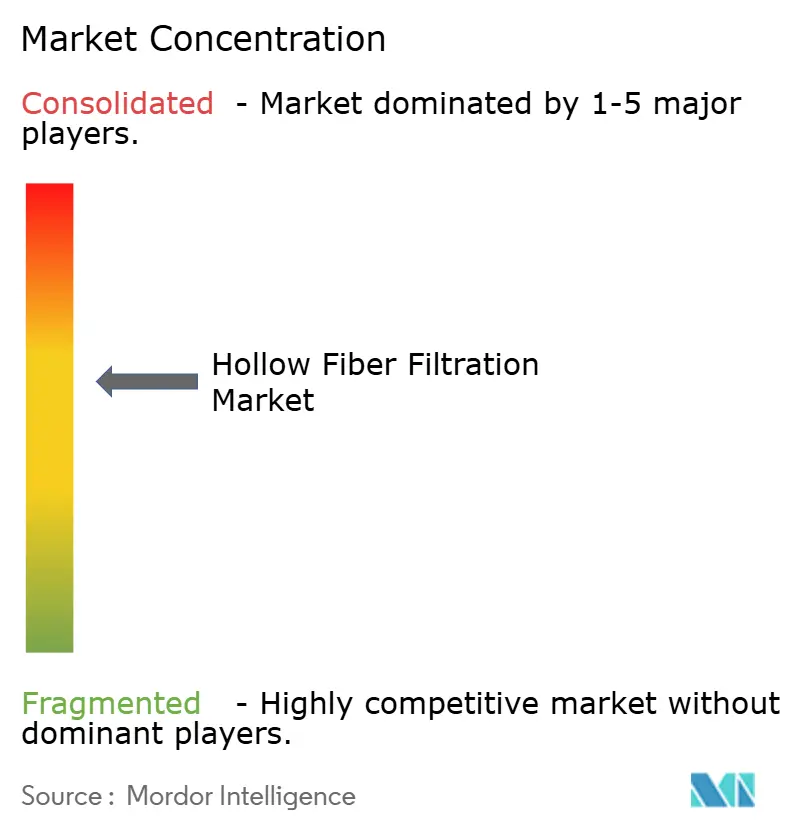

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

Hollow Fiber Filtration Market Analysis by Mordor Intelligence

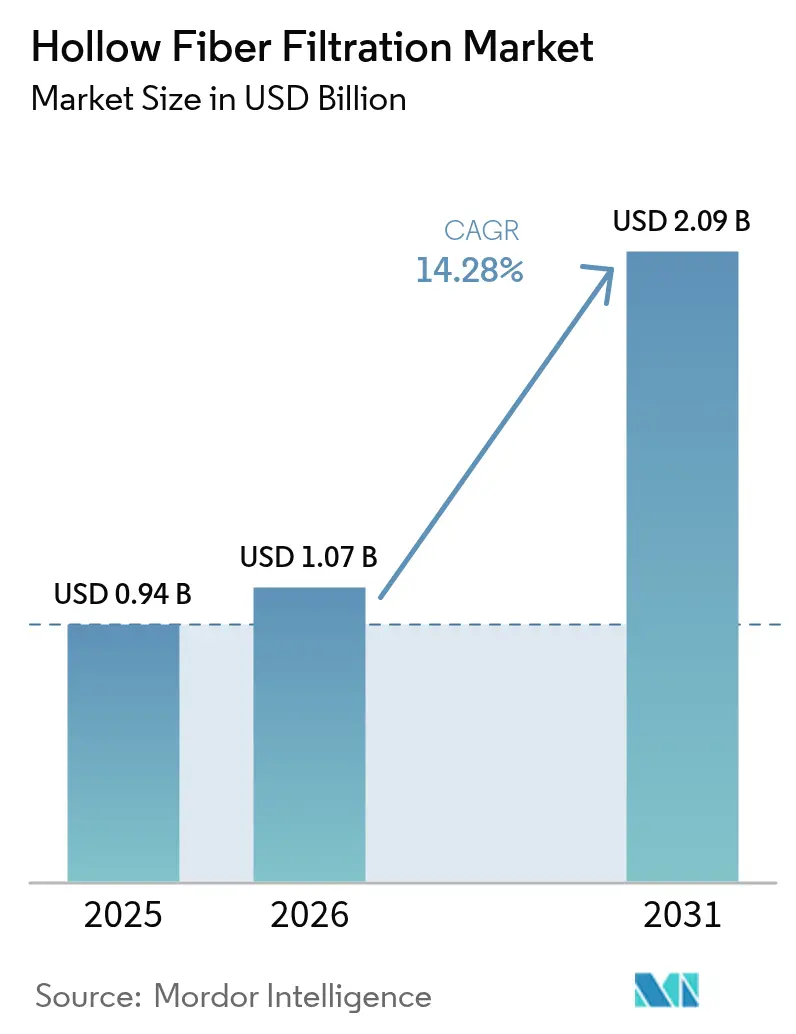

The hollow fiber filtration market size is expected to grow from USD 0.94 billion in 2025 to USD 1.07 billion in 2026 and is forecast to reach USD 2.09 billion by 2031 at 14.28% CAGR over 2026-2031. Intensifying biologic pipelines, the pivot toward continuous manufacturing, and the migration to single-use equipment collectively reinforce demand for robust membrane platforms that maintain high cell density and product quality. Synthetic polymer membranes currently dominate, but ceramic variants are scaling quickly as manufacturers look to extend membrane lifetimes under harsher process conditions. On the process front, ultrafiltration is displacing microfiltration in critical separations, while contract development and manufacturing organizations (CDMOs) shift procurement toward modular, multi-product filtration skids. Regionally, North America still commands the largest installed base; however, escalating Asia-Pacific investments signal a geographic re-balancing of the hollow fiber filtration market in the next five years. Competitive intensity is rising as leading suppliers assemble end-to-end downstream portfolios through mergers and targeted R&D.

Key Report Takeaways

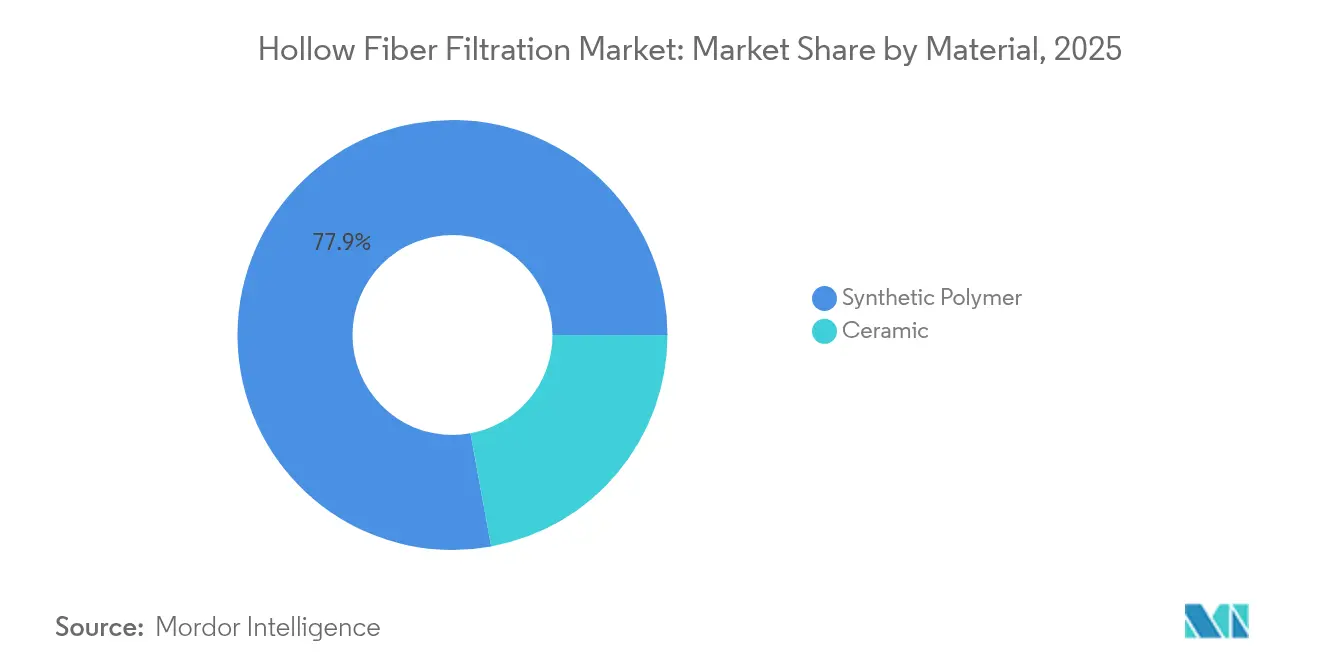

- By material, synthetic polymer membranes held 77.88% of hollow fiber filtration market share in 2025, whereas ceramic membranes are forecast to expand at a 16.48% CAGR to 2031.

- By technique, microfiltration led with 61.72% revenue share in 2025; ultrafiltration is projected to post a 16.55% CAGR through 2031.

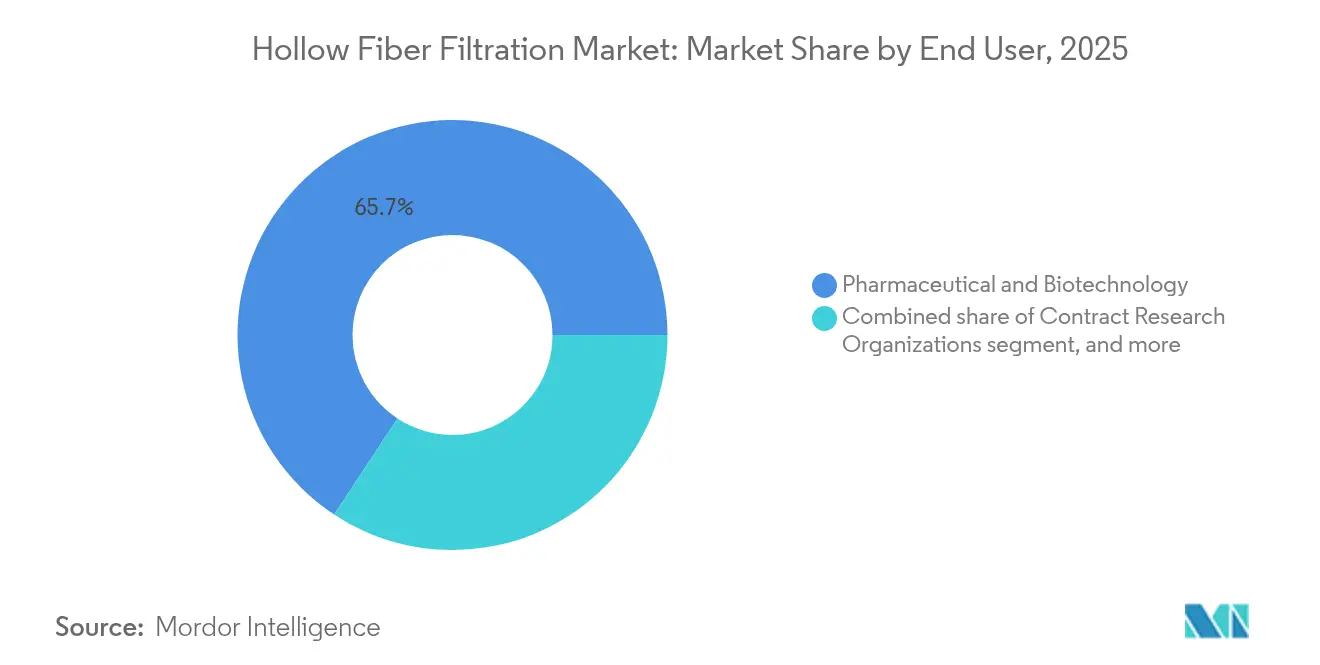

- By end user, the pharmaceutical and biotechnology segment accounted for 65.72% of the hollow fiber filtration market size in 2025, while CROs and CDMOs are set to grow at a 17.23% CAGR between 2026-2031.

- By application, protein concentration and diafiltration captured 55.05% share of the hollow fiber filtration market size in 2025; raw material filtration advances at a 17.54% CAGR over the same period.

- By geography, North America captured 40.88% share of the hollow fiber filtration market size in 2025; whereas, Asia-Pacific is projected to grow at fastest CAGR 15.42%.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of 2026.

Global Hollow Fiber Filtration Market Trends and Insights

Drivers Impact Analysis*

| Driver | % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Rapid Expansion of Global Biologic Drug Pipeline | +3.2% | Global (North America & EU focal) | Medium term (2-4 years) |

| Rising Adoption of Single-Use Bioprocess Equipment | +2.8% | Global, led by North America, expanding to APAC | Short term (≤ 2 years) |

| Shift Toward Continuous and Perfusion Manufacturing | +2.1% | North America & EU core, spill-over to APAC | Long term (≥ 4 years) |

| Growing Outsourcing to Contract Development and Manufacturing Organizations | +1.9% | Global, with APAC gaining prominence | Medium term (2-4 years) |

| Surge in Advanced Therapy Medicinal Product Commercialization | +1.7% | North America & EU, early adoption in APAC | Long term (≥ 4 years) |

| Emerging Demand for High-Purity Plant and Cultured Protein Processing | +1.4% | Global, with early gains in North America, EU, Singapore | Medium term (2-4 years) |

| Source: Mordor Intelligence | |||

Rapid Expansion of Global Biologic Drug Pipeline

More than 6,500 monoclonal antibodies were in clinical development in 2025 versus 360 commercialized molecules in 2024, triggering a step-change in filtration run volumes and development batches. Each therapeutic candidate requires scalable filtration solutions through clinical and commercial phases, intensifying orders for flexible hollow fiber modules that switch quickly between development scales. Complex formats—bispecifics and antibody-drug conjugates—raise selectivity needs that conventional microfiltration cannot meet consistently, prompting ultrafiltration adoption. Most pipeline growth now stems from Asia-Pacific sponsors, driving suppliers to build local technical support and membrane production hubs to stay competitive. Technology providers therefore prioritize integrated systems combining membrane modules with in-line sensing to support process validation and comparability across global sites.

Rising Adoption of Single-Use Bioprocess Equipment

Global single-use system sales expanded at more than 10% CAGR between 2019-2024, and hollow fiber cartridges optimized for disposability are capturing the upside. Eliminating clean-in-place cycles lowers capital outlay and validation costs, making advanced filtration affordable for emerging biotechs and cell therapy developers. Investments by Cytiva and Pall totaling USD 1.5 billion—including USD 300 million earmarked for single-use lines—demonstrate supplier commitment to pre-sterilized, gamma-stable membrane assemblies. Uptake accelerates in greenfield Asian plants that can specify single-use architectures from day one. Environmental scrutiny over plastic waste, however, is spurring R&D into recyclable housings and compostable polymers, inserting sustainability criteria into procurement decisions.

Shift Toward Continuous and Perfusion Manufacturing

Perfusion bioreactors attain roughly 10× higher viable-cell density than conventional fed-batch, demanding membranes that resist fouling during uninterrupted operation. Suppliers are refining lumen geometries, surface chemistries, and module hydraulics to sustain steady-state, 60-day campaigns without integrity breaches. Continuous processes also encourage inline monitoring: pressure-drop sensors and UV absorption probes feed control loops that trigger preventive maintenance, curbing unscheduled downtime. Regulators support the model because tighter control reduces lot variability, yet the switch brings higher upfront equipment spend and data-management overhead. Economic benefits are compelling; reported facilities achieve 30–35 g/L yields against 3 g/L in fed-batch over identical timeframes, cutting cost-of-goods even with premium membranes.

Surge in Advanced Therapy Commercialization

Advanced therapy medicinal products (ATMPs) are projected to climb from USD 8.4 billion in 2022 to USD 20.63 billion by 2031, ushering in small-batch, high-value workflows that depend on low-shear, high-selectivity hollow fiber filtration steps[1]“ATMP Cleanroom Facilities: A Roadmap for Success,” ISPE, ispe.org. ATMPs often require cell-friendly processing under strict aseptic controls, and hollow fibers provide gentle hydrodynamics compared with plate-and-frame devices. As regulators clarify ATMP guidelines, demand for validated, closed-loop filtration modules capable of handling living cells and viral vectors will intensify, positioning the hollow fiber filtration market for disproportionate upside in this segment.

Restraints Impact Analysis*

| Restraints Impact Analysis | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Stringent Regulatory Validation and Documentation Requirements | -2.3% | Global, highest impact in North America & EU | Long term (≥4 years) |

| Membrane Fouling Leading to Recurrent Replacement Costs | -1.8% | Global, particularly affecting high-volume lines | Short term (≤2 years) |

| High Capital Expenditure for Large-Scale Filtration Skids | -1.6% | Global, most acute for greenfield commercial plants | Medium term (2-4 years) |

| Performance Limitations with High-Viscosity Gene Vector Solutions | -1.2% | Global, pronounced in cell and gene therapy hubs | Short term (≤2 years) |

| Source: Mordor Intelligence | |||

Stringent Regulatory Validation and Documentation Requirements

FDA and EMA guidelines mandate exhaustive performance evidence for every membrane configuration, driving validation spend beyond USD 1 million per step on complex biologics[2]“Lifetime Studies for Membrane Reuse: Principles and Case Studies,” BioPharm International, biopharminternational.com. Smaller innovators lack specialized teams and often defer to CDMOs with proven filings, which slows direct equipment sales. Divergent regional rules—particularly around pre-use integrity testing—force dual studies, lengthening timelines by up to 18 months. Vendors with audit-ready data packages now enjoy preferential supplier status, but generating those dossiers is resource-intensive and raises barriers for new entrants.

Membrane Fouling Leading to Recurrent Replacement Costs

Protein deposits, cell debris, and lipid aggregates progressively clog pores, shortening module life and inflating variable costs. A single large-scale replacement can exceed USD 1 million, nullifying throughput gains if change-outs occur mid-campaign. Material scientists are experimenting with helical carbon nanotube-reinforced ceramic supports that maintain flux for extended runs and hit 99.99% oil-in-water separation in analogous tests[3]“Fabrication of Composite Membrane by Constructing Helical Carbon Nanotubes in Ceramic Support Channels,” Membranes Journal, mdpi.com. Pricing, however, remains premium and adoption concentrates in high-margin therapeutics. Broader roll-out hinges on validated anti-fouling coatings and cost-effective cleaning agents that do not trigger re-qualification protocols.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Material: Ceramic Membranes Challenge Polymer Dominance

Synthetic polymers held 77.88% of hollow fiber filtration market share in 2025 thanks to mature supply chains and attractive unit costs. Within this cohort, polyethersulfone remains preferred for antibody purification owing to 4.52 L/m²·h·atm clean-water permeability and stable pH tolerance. Polyvinylidene fluoride gains in solvent-rich feeds, while polysulfone supports higher-pressure steps. Polypropylene persists where protein adsorption risk is low. Ceramic membranes, although still niche, are scaling at a 16.48% CAGR as plants seek longer life cycles and aggressive cleaning compatibility. Alumina and zirconia variants withstand caustic regimes and back-pulse procedures, reducing downtime in perfusion lines. Cost amortization over multi-year campaigns makes ceramics increasingly attractive as continuous processing expands, a trend that should raise their revenue share materially within the hollow fiber filtration market by 2031.

By Technique: Ultrafiltration Gains Precision Advantage

Microfiltration kept 61.72% revenue in 2025, driven by cell harvest and broth clarification tasks that fit its 0.1–0.45 µm cut-off range. Tangential-flow microfiltration (TFF) reigns in large-scale antibody plants, offering higher throughput than dead-end modes and proven regulatory lineage. The pivot to ultrafiltration, however, is unmistakable: at 16.55% CAGR, operators increasingly rely on 10–100 kDa membranes for buffer exchange and concentration, achieving >99.75% retention while trimming diafiltration volume. Single-pass configurations embedded in fully continuous platforms slash hold times and accelerate batch release testing, making ultrafiltration central to next-gen plant layouts. Suppliers differentiate via low-fouling chemistries and inline analytics that certify pore integrity in real time.

By End User: CROs Drive Market Expansion

Pharmaceutical and biotechnology manufacturers controlled 65.72% of hollow fiber filtration market size in 2025, leveraging deep regulatory know-how to operate in-house purification suites. Big Pharma megasite expansions—Novo Nordisk’s USD 4.1 billion US build-out among them—cement baseline demand for high-capacity modules. CDMOs and CROs, conversely, are edging toward 17.23% CAGR as outsourcing rationalizes capital deployment. These firms prefer standardized skid footprints compatible across monoclonal antibodies, recombinant proteins, and viral vectors, thereby fueling orders for plug-and-play hollow fiber cassettes. Academic and research institutes represent a strategic seeding ground: early adoption in cell therapy studies supplies critical performance data that often migrates into commercial specs, reinforcing vendor presence.

By Application: Raw Material Processing Accelerates

Protein concentration and diafiltration sustained 55.05% revenue in 2025, reflecting regulatory mandates for precise formulation of injectable biologics. Here, hollow fiber modules routinely enable 10-fold concentration with minimal shear, preserving IgG integrity and glycosylation profiles. Yet raw material filtration is surging at 17.54% CAGR as manufacturers tighten control over media and buffer inputs to pre-empt contamination events. High-flux fibers strip particulates and bioburden from cell culture components, improving downstream yield predictability. Virus and VLP production add further impetus: next-generation filters such as Asahi Kasei’s Planova FG1 operate at seven-times the flow rate of prior models, raising productivity for vaccine lines. Coupled with automation, these advances strengthen the hollow fiber filtration market’s role in upstream-to-downstream integration.

Geography Analysis

North America accounted for 40.88% of hollow fiber filtration market share in 2025 as decades of investment in Boston, San Francisco, and the Research Triangle reinforced a sophisticated supplier–user ecosystem. FDA guidance—clear on microbial retention, extractables, and integrity testing—speeds qualification of novel membrane chemistries. Fujifilm’s USD 1.2 billion expansion in North Carolina adding 160,000 L of bioreactor volume exemplifies continued regional capacity growth.

Europe sustains a sizeable presence led by Germany’s engineering strength and the United Kingdom’s cell-and-gene therapy cluster. The EMA’s environmental leanings promote ceramic membranes and reusable housings, while Horizon Europe funding channels pour capital into low-carbon bioprocess technologies. This policy framework both disciplines supplier claims and cultivates technology differentiation in sustainability metrics.

Asia-Pacific remains the fastest-growing area at 15.42% CAGR. China’s biopharma market is forecast to exceed 1.4 trillion yuan by 2029, and state grants favor domestic membrane manufacturing scale-ups, trimming lead times for local biotech startups. South Korea emerges as a regional export hub, underscored by MilliporeSigma’s EUR 300 million Daejeon plant that delivers sterile filtration consumables to a wider Asian customer base. Japan leverages precision ceramics expertise to supply ultra-smooth lumen surfaces for continuous lines, whereas Singapore positions itself as a regulatory sandbox for first-in-class filtration materials through fast-track approvals. Together these dynamics will gradually rebalance global revenue shares in the hollow fiber filtration market before 2030.

Regulatory Landscape

Hollow fiber filtration systems used in bioprocessing and extracorporeal blood treatment operate under stringent quality and performance-control regimes, and the US FDA and the European Union remain key reference jurisdictions for global suppliers. In the United States, the FDA Quality Management System Regulation (QMSR) took effect on February 2, 2026, amending 21 CFR Part 820 to incorporate ISO 13485:2016 by reference. The update increases the weight placed on ISO-aligned design controls, supplier management, and risk-based documentation for membrane modules, single-use assemblies, and filtration skids.

In Europe, Regulation (EU) 2017/745 (MDR) continues as the governing framework for medical devices, with consolidated updates effective January 1, 2026, sustaining expectations for clinical evaluation, post-market surveillance, and technical documentation for hollow fiber-based extracorporeal devices. Standards and device-specific test methods also shape compliance, and ISO 8637-3:2024 introduced requirements and test methods for single-use plasmafilters. That complements broader extracorporeal blood purification standards and reinforces the need for validated biocompatibility, integrity testing, and traceable manufacturing controls across global supply chains.

Competitive Landscape

Industry consolidation is quickening, pushing the hollow fiber filtration market toward integrated solution models. Thermo Fisher’s USD 4.1 billion purchase of Solventum’s purification division folds membrane cartridges, chromatography resins, and single-use assemblies into one portfolio, reinforcing one-stop bid capabilities for large capital projects. Danaher’s earlier fusion of Cytiva and Pall forged a USD 7.5 billion bioprocess powerhouse spanning upstream media through virus filtration, elevating cross-selling potential and after-sales support width.

Product innovation runs in parallel. Repligen channels R&D into smart hollow fiber modules embedded with optical sensors and cloud-connected controllers that monitor flux decline and trans-membrane pressure drift. Sartorius is localizing production via its new Center for Bioprocess Innovation in Greater Boston, trimming time-to-customer for customized membrane cassettes. In Asia, domestic challengers—Boln BioTech among them—secure venture funding to upscale ceramic and nanofiltration specialties, aiming to undercut imports while meeting regional GMP standards.

Service capabilities now differentiate front-runners: on-site validation, electronic batch-record integration, and 24/7 spare-part logistics weigh heavily in procurement scores. Suppliers that can shoulder regulatory documentation burdens for novel therapies win preferred-supplier status with resource-constrained developers, further concentrating share at the top.

Hollow Fiber Filtration Industry Leaders

Repligen Corporation

Parker Hannifin Corp

Asahi Kasei Co Ltd

Danaher Corporation

Sartorius AG

- *Disclaimer: Major Players sorted in no particular order

Market Opportunities and Future Outlook

A clear whitespace is in filtration platforms and consumables that reduce validation and quality friction while matching the shift toward modular, multi-product operations. The FDA QMSR effective February 2, 2026, aligns US device quality requirements to ISO 13485:2016. For suppliers, this creates a more direct route to audit-ready documentation packages, standardized extractables/leachables support for single-use assemblies, and digitally accessible validation evidence that can be reviewed through remote assessment workflows.

In the technology stack, outside-in filtration (OIF) architectures in hollow fiber blood applications are a development focus aimed at reducing clogging and inflammatory response versus inside-out designs. This opens room for next-generation membrane surface chemistries and more compact housings that fit home and portable care concepts. At the same time, computational modeling is increasingly used to optimize hollow fiber dialyzer geometry and flow fields, supporting faster design iterations and clearer links between operating conditions and blood component damage. Vendors that pair membrane innovation with modeling-enabled design services and application data can differentiate across medical-device and bioprocess use cases.

Recent Industry Developments

- July 2026: Asahi Kasei Life Science began construction activities tied to its announced Planova hollow-fiber virus removal filter spinning plant project in Nobeoka City, Japan, following the prior year plan disclosure. The project supports long-horizon capacity availability for virus filtration, a critical step for biologics and plasma-derived therapeutics manufacturing. Establishing additional spinning capacity also reduces supply risk for customers standardizing on Planova hollow-fiber formats.

- November 2025: Parker Hannifin announced a definitive agreement to acquire Filtration Group Corporation for USD 9.25 billion. The transaction expands Parker's filtration portfolio breadth and scale, strengthening its position across high-value filtration applications that overlap with life sciences manufacturing needs. A larger installed base and aftermarket platform also increases bundling leverage for filtration hardware and consumables.

- May 2024: Asahi Kasei Medical completed construction of its third assembly plant for Planova virus removal filters in Nobeoka, Japan. The added assembly footprint increases manufacturing resilience and throughput for hollow-fiber virus filtration products used in biologics and blood-derived product purification. The expansion supports faster fulfillment and reduces bottlenecks for customers running validation-heavy processes.

Research Methodology Framework and Report Scope

Market Definition and Coverage

For this study, the hollow fiber filtration market covers revenue earned from hollow-fiber membrane filtration used to separate, clarify, concentrate, or sterilize liquids in industrial and life science workflows. Value is captured at the point of sale of filtration modules and membrane-based units supplied to end users.

Scope exclusions: We exclude filtration products that do not use hollow-fiber membranes, and we also exclude lab consumables that are not part of the filtration unit itself.

Segmentation Overview

- By Material

- Synthetic Polymer

- Polyethersulfone (PES)

- Polyvinylidene Fluoride (PVDF)

- Polysulfone (PS)

- Polypropylene (PP)

- Ceramic

- Alumina

- Zirconia

- Synthetic Polymer

- By Technique

- Microfiltration

- Dead-end

- Tangential Flow (TFF)

- Ultrafiltration

- Dead-end

- Tangential Flow (TFF)

- Microfiltration

- By End User

- Pharmaceutical & Biotechnology

- Contract/Clinical Research Organizations

- Academic & Research Institutes

- By Application

- Protein Concentration & Diafiltration

- Cell Clarification / Harvest

- Virus / VLP Production

- Raw Material Filtration

- Other Applications

- Geography

- North America

- United States

- Canada

- Mexico

- Europe

- Germany

- United Kingdom

- France

- Italy

- Spain

- Rest of Europe

- Asia-Pacific

- China

- Japan

- India

- Australia

- South Korea

- Rest of Asia-Pacific

- Middle East & Africa

- GCC

- South Africa

- Rest of Middle East & Africa

- South America

- Brazil

- Argentina

- Rest of South America

- North America

Data Sources, Market Sizing, and Validation

Desk Research

Desk research starts with setting clear counting rules for hollow fiber filtration, and then mapping the main demand pools that typically procure these units. We reference public sources that help validate activity signals, such as US FDA and EMA guidance linked to sterile and bioprocess operations, US EPA and WHO publications for water and wastewater trends, and UN Comtrade for import and export direction checks tied to membrane and filtration equipment trade.

We also review company annual reports, investor presentations, product catalogs, and reputable press to understand where revenues sit (membranes versus modules) and how pricing tends to move by format. When needed, we pull comparable company financials and news signals from a paid subscription database, and we use patent databases to check the direction of membrane material and module design activity. The sources listed above are illustrative only, and many other public documents were also used for data collection, validation, and clarification.

Primary Interviews and Surveys

Primary work is used to confirm the market boundary and translate demand into a revenue view that matches how filtration modules are priced and sold in real contracts. We speak with suppliers, distributors, integrators, and end users across biopharma processing, research organizations, and water treatment teams, then re-check assumptions across regions so local adoption and price bands are represented.

Distribution of primary research fieldwork respondents

| Company type | Respondent position | Region |

|---|---|---|

| Top tier: 26% | CXOs: 14% | APAC: 42% |

| Mid tier: 53% | Functional/Unit leaders: 31% | EMEA: 31% |

| Smaller Players: 21% | Managers: 55% | Americas: 27% |

Market-Sizing & Forecasting

Sizing is built using top-down and bottom-up approach, where end-user demand pools are reconstructed from activity indicators and then cross-checked with supplier-side signals. On the top-down side, we translate workflow activity into unit demand, for example bioprocess steps that use protein concentration and diafiltration, virus or VLP related filtration needs, and water treatment capacity additions that typically use hollow-fiber modules.

To keep totals realistic, we corroborate outputs using selective bottom-up approximations like sampled ASP ranges by module type, channel checks on procurement patterns, and a sanity roll-up from publicly visible revenue exposures where they can be separated. Inputs that matter in this market include the mix shift between microfiltration and ultrafiltration, the split of synthetic polymer versus ceramic material, single-use adoption in bioprocessing, cleaning and replacement cycles that drive repeat purchases, and region-wise capacity additions across life science and municipal treatment. For forecasting, we run scenario analysis around a core demand path, and then use expert feedback to keep assumptions grounded when growth accelerates or slows by end use. When data gaps show up in a country or end-user slice, we bridge the share using closely related indicators (such as import direction, installed capacity, and peer market ratios) and then validate again through follow-up calls.

Data Validation & Update Cycle

Validation is handled through repeated cross-checks so the final number is not driven by one assumption. We compare modeled totals against independent signals like trade direction, visible capacity additions, and documented adoption in regulated bioprocess steps, then review outliers for unit mix, pricing, or currency timing issues.

A second analyst review is completed before sign-off, and any large variance triggers a re-contact with selected experts to confirm whether the change is real or model-driven. Reports refresh annually, with interim updates for material events that can shift pricing, supply availability, or demand timing. Before delivery, an analyst performs a fresh pass on the core inputs so clients receive the latest updated view.

Mordor Intelligence's Hollow Fiber Filtration Marker Market Size Versus Other Published Estimates

Market size numbers for hollow fiber filtration can vary across publications, even when the product name looks similar, because counting rules and timing assumptions differ. The largest drivers usually relate to what is included as hollow-fiber revenue, which year is treated as the current sizing point, and how pricing is applied across biopharma versus water applications.

By tracking scope at the technique and module level and refreshing interview-based ASP bands by end use, Mordor Intelligence keeps the 2026 total focused on hollow-fiber filtration modules rather than including adjacent membrane formats or full filtration systems. Differences also show up when a source uses a shorter window that emphasizes near-term demand spikes, applies a different currency conversion timing, or does not re-check replacement cycle assumptions against end-user maintenance practices.

Benchmark comparison

| Source | Market Size | Gaps in Research Methodology |

|---|---|---|

| Mordor Intelligence | USD 1.07 B (2026) | |

| Global Market Publisher A | USD 0.64 B (2024) | Uses an earlier base year and appears to apply broader demand drivers, which can shift revenue capture toward non-module spend and reduce comparability with module-only counting. |

| Industry Analytics Firm B | USD 0.78 B (2025) | Anchors on a different base year and likely applies a wider membrane filtration interpretation, which can change what is counted under hollow-fiber versus other membrane geometries and alter the implied price-per-unit curve. |

Across the three sources, most of the gap is explained by the year selected for sizing and the exact product boundary being counted. When scope is held steady around hollow-fiber modules and checked against technique mix, end-use adoption, and realistic price bands, the resulting value is easier to trace and repeat in planning work.

Key Questions Answered in the Report

What is the projected value of the hollow fiber filtration market in 2031?

It is expected to reach USD 2.09 billion, rising from USD 0.94 billion in 2025 at a 14.28% CAGR.

Which material segment is expanding fastest in hollow fiber membranes?

Ceramic membranes are growing at a 16.48% CAGR through 2031 due to durability in harsh cleaning cycles.

Why are CDMOs important to future filtration demand?

They are forecast to hold 54% of global biologics capacity by 2028, consolidating purchasing power and favoring platformable filtration skids.

How does continuous manufacturing influence filtration design?

Perfusion bioreactors require membranes that resist fouling over multi-week campaigns, pushing vendors to develop smart, long-life modules with inline monitoring.

What is driving Asia-Pacific growth in this sector?

Government investment, rapid capacity expansion by local CDMOs, and multinational plants in South Korea and China are propelling a 15.42% regional CAGR.

Page last updated on: