Microcatheters Market Size and Share

Market Overview

| Study Period | 2022 - 2031 |

|---|---|

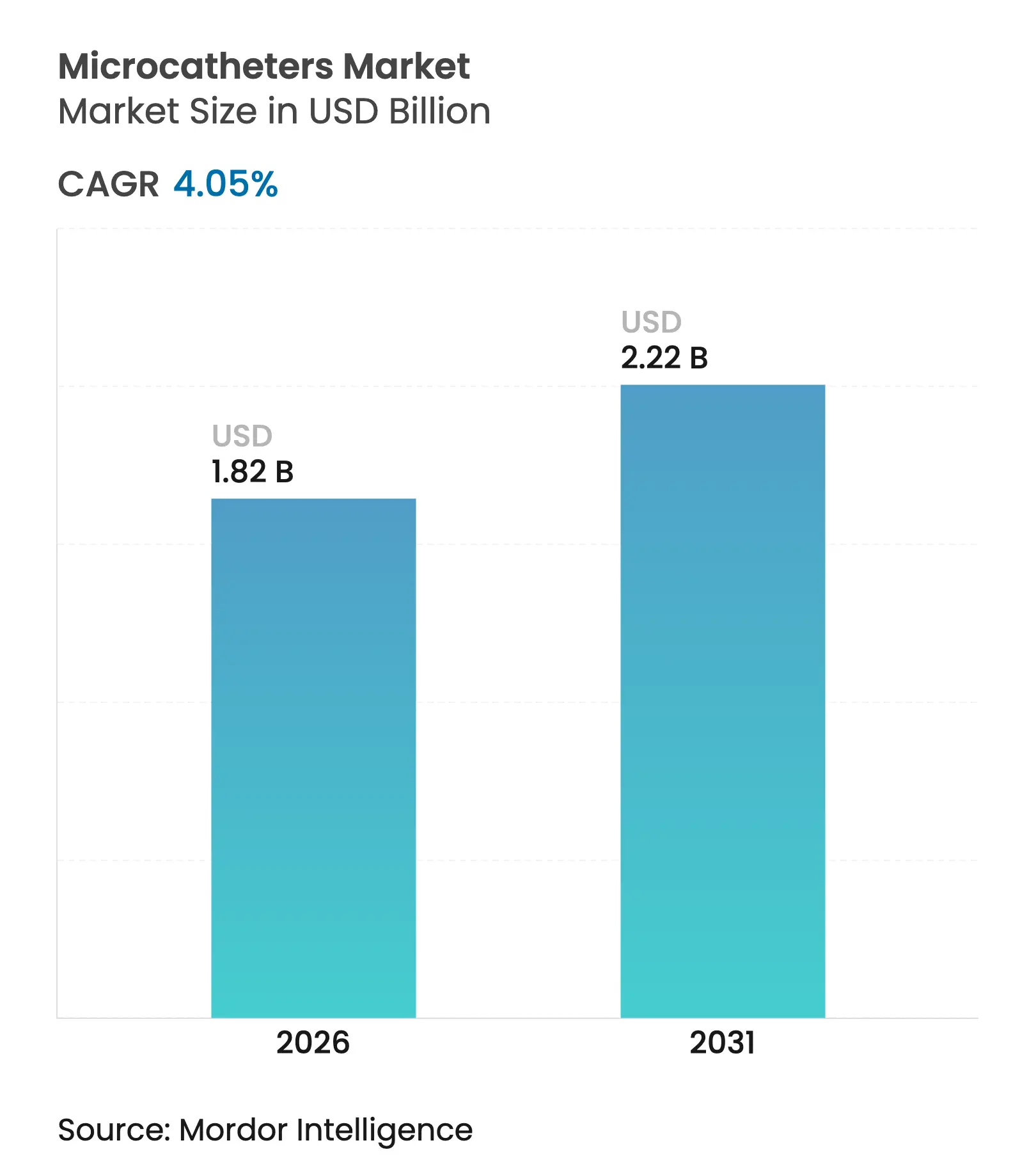

| Market Size (2026) | USD 1.82 Billion |

| Market Size (2031) | USD 2.22 Billion |

| Growth Rate (2026 - 2031) | 4.05 % CAGR |

| Fastest Growing Market | Asia Pacific |

| Largest Market | North America |

| Market Concentration | Medium |

Major Players*Disclaimer: Major Players sorted in no particular order. Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. |

Microcatheters Market Analysis by Mordor Intelligence

The microcatheter market size was valued at USD 1.75 billion in 2025 and estimated to grow from USD 1.82 billion in 2026 to reach USD 2.22 billion by 2031, at a CAGR of 4.05% during the forecast period (2026-2031). This expansion reflects steadily rising procedure volumes in cardiovascular, neurovascular, and oncological settings as clinicians favor minimally-invasive treatments that shorten recovery times and lower overall care costs. Greater regulatory support for next-generation devices, widening clinical indications for renal denervation and stroke thrombectomy, and rapid material innovations that enhance steerability and tip-tracking accuracy are reinforcing demand. At the same time, the migration of interventional procedures to ambulatory surgery centers (ASCs) broadens distribution channels and intensifies competition among manufacturers seeking to supply cost-sensitive outpatient facilities. Strategic acquisitions—most notably Stryker’s USD 4.9 billion purchase of Inari Medical and Teleflex’s €760 million acquisition of BIOTRONIK’s vascular intervention unit—highlight a shift toward portfolio breadth and integrated delivery platforms, while supply-chain vulnerabilities around high-performance polymers remind stakeholders of persistent production risks.

Key Report Takeaways

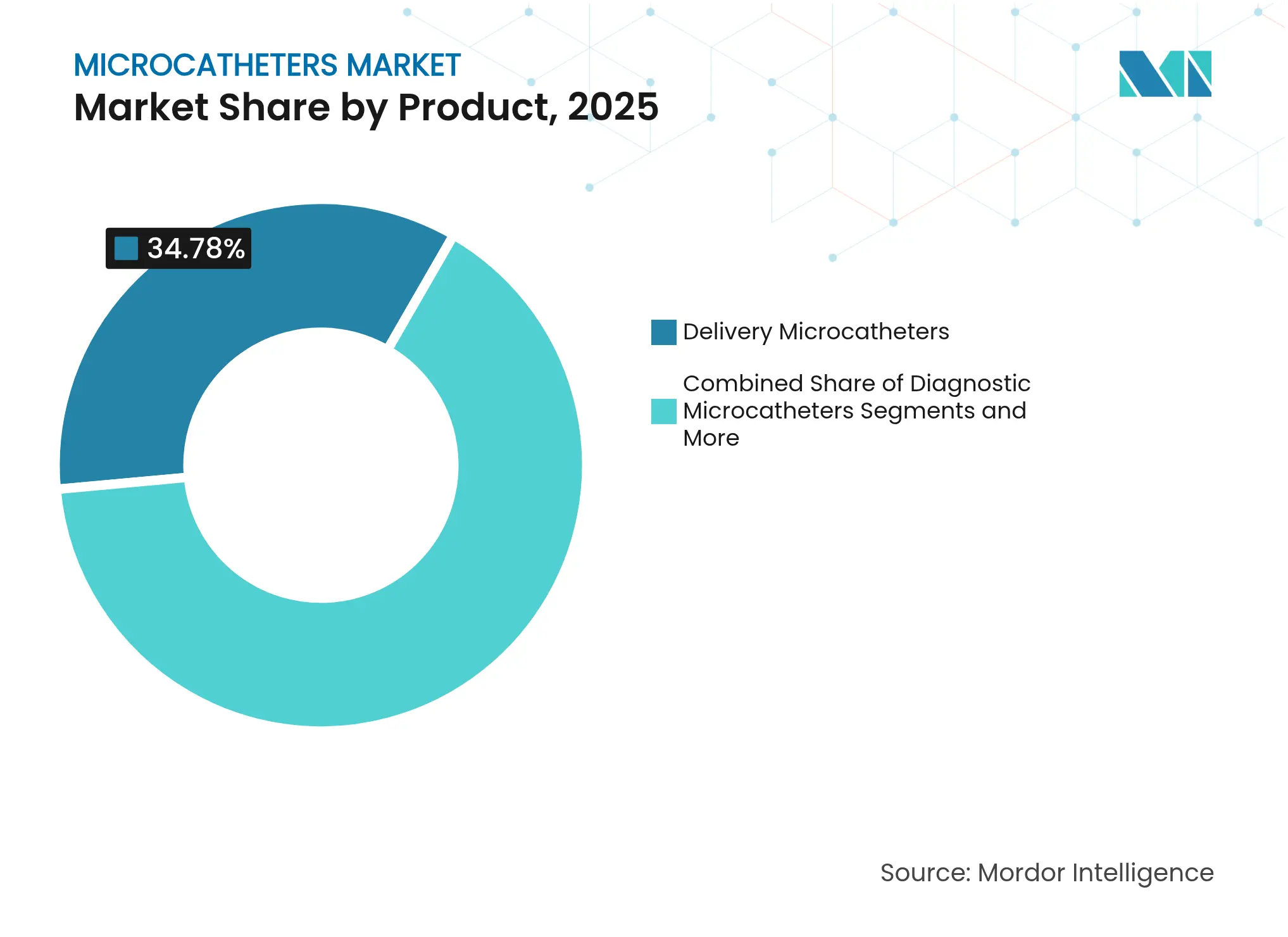

- By product category, delivery microcatheters led with 34.78% revenue share in 2025, whereas steerable devices are projected to advance at a 5.05% CAGR through 2031.

- By design, single-lumen systems held 65.62% of the microcatheter market share in 2025; dual-lumen solutions record the fastest expansion at 5.41% CAGR to 2031.

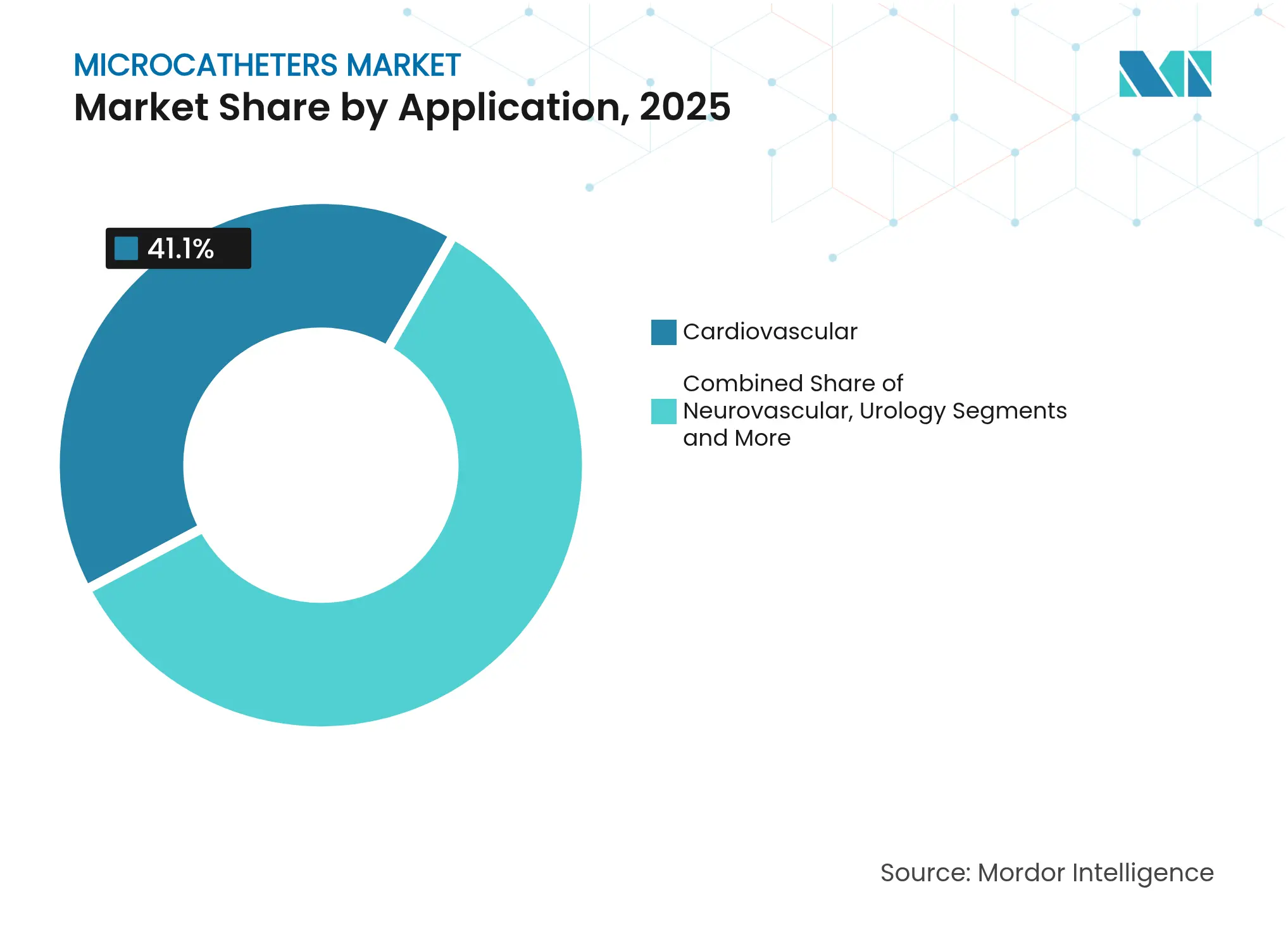

- By application, cardiovascular procedures accounted for 41.10% of the microcatheter market size in 2025, while neurovascular uses are forecast to grow at an 5.78% CAGR.

- By end-user, hospitals retained 74.10% share in 2025, but ASCs represent the quickest-growing channel at 5.56% CAGR.

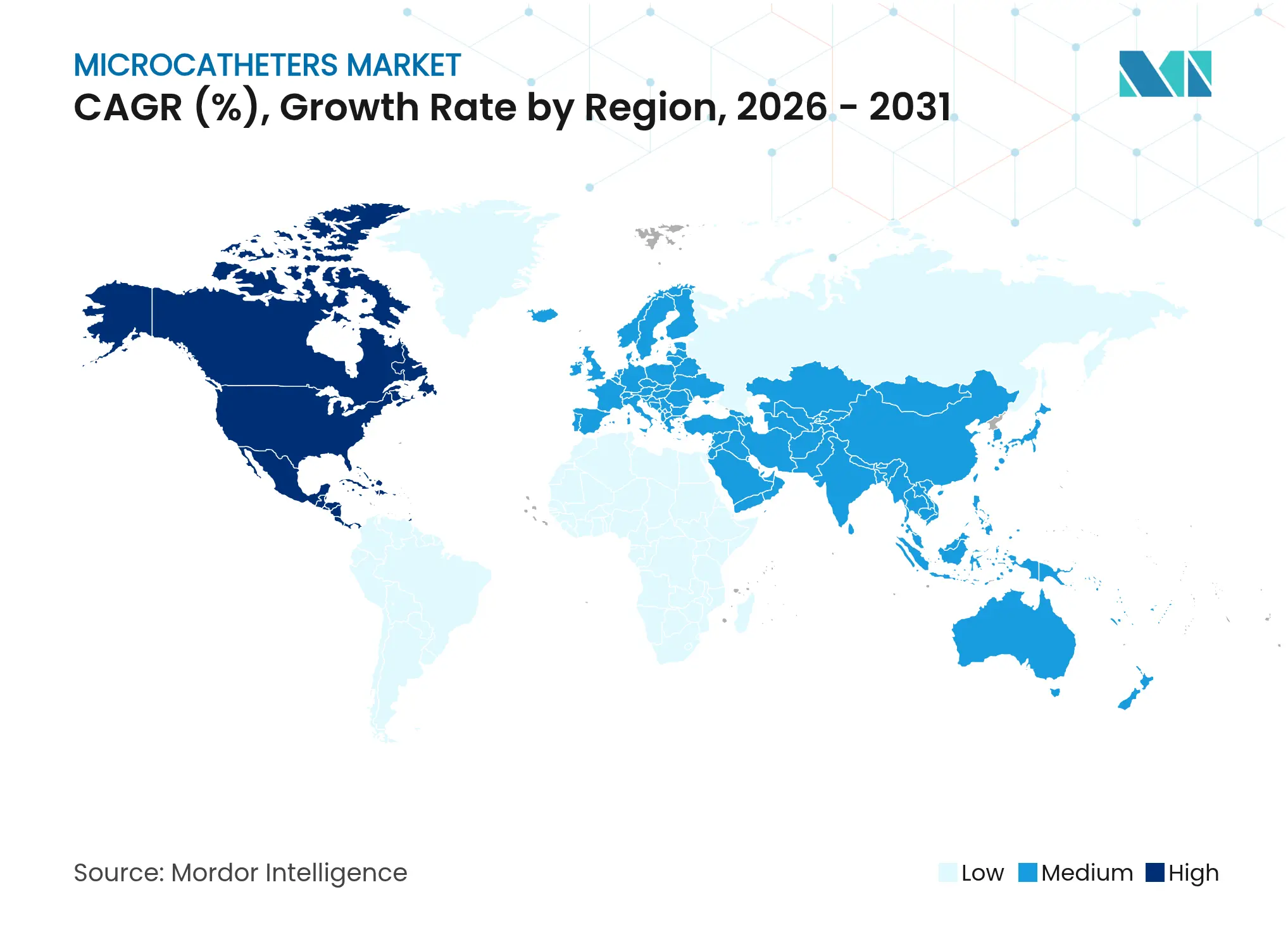

- By geography, North America commanded 41.30% share in 2025; Asia-Pacific posts the highest regional CAGR of 6.05% through 2031.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence's proprietary estimation framework, updated with the latest available data and insights as of 2026.

Global Microcatheters Market Trends and Insights

Drivers Impact Analysis

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline | |||

|---|---|---|---|---|---|---|

Rising incidence of chronic cardiovascular & neurovascular

diseases

Rising incidence of chronic cardiovascular & neurovascular

diseases

| +1.8% | Global; concentrated in North America & Europe | Long term (≥ 4 years) | (~) % Impact on CAGR Forecast:

+1.8%

|

Geographic Relevance

:

Global; concentrated in North America & Europe

|

Impact Timeline

:

Long term (≥ 4 years)

|

Growing geriatric population & minimally-invasive

procedure demand

Growing geriatric population & minimally-invasive

procedure demand

| +1.2% | Global; strongest in APAC & North America | Medium term (2-4 years) | |||

Regulatory approvals and supportive treatment guidelines

Regulatory approvals and supportive treatment guidelines

| +0.9% | North America & EU | Short term (≤ 2 years) | |||

Technological advances in steerability, tip-tracking &

composites

Technological advances in steerability, tip-tracking &

composites

| +1.1% | Global innovation hubs in US, Japan, Germany | Medium term (2-4 years) | |||

Greater adoption of minimally-invasive renal denervation

procedures

Greater adoption of minimally-invasive renal denervation

procedures

| +0.7% | North America & EU | Medium term (2-4 years) | |||

Venture funding for integrated microcatheter–delivery

systems

Venture funding for integrated microcatheter–delivery

systems

| +0.5% | North America | Short term (≤ 2 years) | |||

| Source: Mordor Intelligence | ||||||

Rising Incidence Of Chronic Cardiovascular & Neurovascular Diseases

Cardiovascular disease prevalence is expanding procedure volumes worldwide, placing pressure on care systems and accelerating adoption of catheter-based therapies. The American Heart Association projects cardiovascular care expenditures to escalate from USD 393 billion in 2020 to USD 1.490 trillion by 2050. Stroke intervention protocols now prioritize endovascular thrombectomy for large ischemic cores, reflecting outcome improvements reported in multicenter trials [1]New England Journal of Medicine, “Thrombectomy in Large Infarct,” nejm.org. Market research shows neurovascular device revenues rising from USD 3.6 billion in 2023 to USD 5.5 billion by 2028, illustrating robust demand for advanced navigation systems. This epidemiological momentum underpins long-term growth across the microcatheter market.

Growing Geriatric Population & Minimally-Invasive Procedure Demand

Global life expectancy gains enlarge the pool of patients requiring complex vascular interventions while favoring low-trauma access routes. Geriatric studies in thoracic endovascular aortic repair document lower morbidity over open surgery despite higher baseline risk. Transcatheter aortic valve replacement protocols increasingly incorporate frailty metrics, driving design refinements for ultra-flexible microcatheter shafts that navigate tortuous anatomies. Rising outpatient preference supports a USD 59 billion ASC segment by 2028, magnifying procurement opportunities for compact, single-use microcatheter kits.

Regulatory Approvals And Supportive Treatment Guidelines

The FDA’s Predetermined Change Control Plan framework allows iterative device changes without new 510(k) submissions, shortening time-to-market for refreshed microcatheter models. Harmonized Quality System Regulation amendments effective February 2026 ease global roll-outs by aligning US and ISO requirements. Parallel progress in Europe through Eudamed boosts transparency and post-market surveillance. These policy shifts create a tailwind for rapid adoption of precision delivery systems that address unmet therapeutic needs.

Technological Advances In Steerability, Tip-Tracking & Composites

Robotic shaping methods achieve 96% first-pass success in intricate cerebral aneurysm cases, vastly outperforming manual techniques. The Bendit steerable microcatheter demonstrated guidewire-free navigation in nearly half of studied cases, lowering procedural complexity. Novel polymeric fibers enable magnetic-resonance guidance, eliminating radiation exposure for certain cardiovascular interventions. Such breakthroughs optimize navigation accuracy and reduce fluoroscopy times, enhancing operator confidence and patient safety.

Greater Adoption Of Minimally-Invasive Renal Denervation Procedures

FDA approvals for the Symplicity Spyral and Paradise systems validate catheter-based renal denervation, which has shown 26% reductions in major adverse cardiovascular events in resistant hypertension cohorts. Early commercial use is concentrated in North America and Europe, yet emerging guidelines forecast broader uptake, spurring dedicated microcatheter designs capable of delivering ablation and pressure-sensing functions in a single pass.

Venture Funding For Integrated Microcatheter–Delivery Systems

North American venture ecosystems continue to back start-ups developing dual-lumen architectures and sensor-enabled catheters. Vantis Vascular’s recent USD 10 million financing round targets US commercialization of its CrossFast platform, reflecting investor appetite for multi-functional delivery technologies.

Restraints Impact Analysis

| Restraint | ( ~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline | |||

|---|---|---|---|---|---|---|

High manufacturing cost & complex regulatory clearance

High manufacturing cost & complex regulatory clearance

| -0.8% | Global; most acute in emerging markets | Long term (≥ 4 years) | ( ~) % Impact on CAGR Forecast:

-0.8%

|

Geographic Relevance

:

Global; most acute in emerging markets

|

Impact Timeline

:

Long term (≥ 4 years)

|

Catheter-related complications & recalls

Catheter-related complications & recalls

| -0.6% | North America & EU | Medium term (2-4 years) | |||

Supply-chain constraints for high-performance polymers

Supply-chain constraints for high-performance polymers

| -0.4% | Asia-Pacific production hubs | Short term (≤ 2 years) | |||

Shortage of interventionists trained in ultra-low-profile

devices

Shortage of interventionists trained in ultra-low-profile

devices

| -0.3% | Emerging markets & rural areas | Long term (≥ 4 years) | |||

| Source: Mordor Intelligence | ||||||

High Manufacturing Cost & Complex Regulatory Clearance

PTFE shortages in 2024 forced firms to insource extrusion and raised production costs across the microcatheter industry. Compliance burdens tied to Europe’s Medical Device Regulation further elevate certification expenses, squeezing smaller suppliers. Nitinol raw material disruptions complicate production of steerable shafts relying on shape-memory alloys. These pressures can slow device launches and limit price flexibility.

Catheter-Related Complications & Recalls

FDA Class I actions on several prominent systems, including Medtronic’s Pipeline Vantage and Route 92 Medical’s revascularization catheter, underscore safety concerns that can erode clinician trust [2]FDA, “Pipeline Vantage Embolization Device Recall,” fda.gov. Adverse event publicity mandates stringent quality controls and rapid design corrections, potentially delaying growth in certain product niches.

Segment Analysis

By Product: Delivery Systems Drive Market Foundation

Delivery microcatheters captured 34.78% of 2025 revenues, underlining their central role in device deployment for stent placement, embolization, and drug delivery. Boston Scientific’s MAMBA line demonstrated 36.8% lower force requirements in tortuous channels than peer offerings, reinforcing preference for high-pushability shafts . The microcatheter market size tied to delivery variants is expected to expand steadily as case volumes rise in ASCs and developing economies. Demand for steerable microcatheters is climbing at a 5.05% CAGR, aided by computer-assisted shaping and guidewire-free navigation that cut fluoroscopy exposure and procedure times.

Aspiration microcatheters continue to gain traction in mechanical thrombectomy. The SOFIA 6F achieved 97.2% successful revascularization with a 75% first-pass rate in large-vessel occlusions. Diagnostic microcatheters maintain relevance for angiographic mapping, whereas micro-guide catheters cater to flow-directed access in delicate neurovascular territories. The FreeClimb 88 combined with Tenzing 8 delivery platforms posted 94.3% device advancement success, underscoring interoperability benefits.

Note: Segment shares of all individual segments available upon report purchase

By Design: Single-Lumen Dominance Faces Dual-Lumen Innovation

Single-lumen devices held 65.62% share in 2025, favored for routine embolization where simplicity and cost control prevail. However, surgeons increasingly request dual-lumen formats that permit simultaneous infusion and device passage, propelling a 5.41% CAGR. CrossFast’s DuoPro interlocking technology exemplifies this trend, offering enhanced pushability while retaining dual-monorail functionality. The microcatheter market size for dual-lumen systems should widen as complex oncology and neurovascular procedures migrate to outpatient suites where reduced exchange steps save time.

By Application: Cardiovascular Leadership Challenged by Neurovascular Growth

Cardiovascular interventions dominated 41.10% of 2025 spending, buoyed by high percutaneous coronary intervention volumes and mature reimbursement models. The microcatheter market share within cardiology remains large, yet neurovascular indications are expanding fastest at 5.78% CAGR as miniaturized catheters enable distal-vessel access for stroke rescue. Growing evidence that outpatient centers can safely perform PCI is further stimulating equipment purchases for community-based operators. Oncology and tumor embolization represent another high-growth niche as interventional radiologists adopt targeted drug-delivery catheters to reduce systemic toxicity.

Peripheral vascular and urology segments add steady contributions, with renal denervation catheters carving a new subcategory following recent approvals. Otolaryngology procedures, though comparatively small, see rising adoption of microcatheters for preoperative devascularization of head and neck tumors, achieving near-total angiographic occlusion in 74.5% of cases.

Note: Segment shares of all individual segments available upon report purchase

By End-User: Hospital Dominance Faces ASC Disruption

Hospitals retained 74.10% revenue share in 2025 thanks to comprehensive service lines and established purchasing frameworks. Yet ASCs, expanding at 5.56% CAGR, present a pivotal growth frontier as payers incentivize lower-cost venues. ASC networks now perform complex cardiology cases with clinical outcomes comparable to tertiary hospitals, driving procurement of compact, disposable catheter kits. Clinics and specialty centers complement these channels by addressing niche neurovascular and interventional oncology workflows. Training programs at large academic centers performing over 6,000 procedures annually fill pipeline gaps of skilled interventionists.

Geography Analysis

North America led with 41.30% microcatheter market share in 2025, propelled by advanced health systems, supportive reimbursement, and swift uptake of innovation. Boston Scientific posted 31.1% cardiovascular segment growth in Q1 2025, signaling robust US demand for high-performance device platforms. Projected rises in cardiovascular expenditure to USD 1.490 trillion by 2050 ensure continued demand for cost-efficient, minimally-invasive solutions.

Europe follows as a mature yet opportunity-rich arena. Implementation of the Medical Device Regulation improves product traceability and heightens quality expectations, benefiting established manufacturers able to meet stringent data requirements. Terumo reported 17.1% overseas sales growth in 2024, buoyed by European demand for complex microcatheter systems. Aging demographics and concentrated stroke networks further accelerate device utilization.

Asia-Pacific registers the fastest expansion at 6.05% CAGR through 2031. India’s medical-technology market is forecast to triple to USD 50 billion by 2030 amid production-linked incentive schemes. China’s ongoing healthcare reforms and rising middle-income cohorts fuel premium-device consumption, while Vietnam’s 10%+ annual growth elevates the region’s supply-chain role. Lubrizol’s five-fold capacity increase at its Chennai tubing facility illustrates global firms’ resolve to localize polymer supply and mitigate raw-material risk. Collectively, these dynamics support sustained escalation of the microcatheter market across Asia-Pacific.

Competitive Landscape

Market Concentration

The microcatheter industry exhibits moderate consolidation as leading firms pursue technological differentiation and inorganic expansion to sustain share. Established players emphasize integrated delivery systems combining steerable shafts, sensors, and imaging modalities into single-use kits that shorten procedure times. Patent filings covering automated positioning algorithms, ultrasound-guided catheters, and composite sheaths underscore an innovation race focused on precision and operator ergonomics.

Stryker’s acquisition of Inari Medical extends its reach into peripheral thrombectomy while adding complementary venous capabilities. Teleflex’s purchase of BIOTRONIK’s vascular intervention division enhances its coronary and peripheral portfolio breadth, improving cross-selling potential within large hospital networks. Venture-backed entrants such as Bendit and Vantis Vascular target niche applications with specialty steerable or dual-lumen architectures, forcing incumbents to accelerate R&D cycles.

Supply-chain resilience has become a strategic differentiator since 2024 polymer shortages. Companies investing in vertical integration—for example, in-house PTFE extrusion or exclusive Nitinol sourcing contracts—are better positioned to guarantee delivery schedules to ASCs and distributors. Across the board, marketing strategies emphasize clinical-evidence generation through multicenter trials to secure reimbursement and reinforce brand credibility.

Microcatheters Industry Leaders

*Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- June 2024: MicroVention (Terumo) launched the LVIS EVO coil-assist intracranial stent in the United States, broadening options for wide-neck aneurysm repair.

- February 2024: BIOTRONIK and IMDS introduced the Micro RX, a flexible microcatheter engineered for challenging coronary anatomies.

- November 2023: Transit Scientific received FDA approval for its microcatheter to deliver diverse embolic agents precisely and help healthcare professionals improve patient care with better tools.

- October 2023: Merit Medical Systems expanded its Maestro microcatheter product line. The Maestro product line offers embolotherapy devices with Embosphere microspheres. These 165 cm microcatheters come in various diameters, such as 2.1 F, 2.4 F, 2.8 F, and 2.9 F, to support a wider range of embolization procedures.

Table of Contents for Microcatheters Industry Report

1. Introduction

- 1.1Study Assumptions & Market Definition

- 1.2Scope of the Study

2. Research Methodology

3. Executive Summary

4. Market Landscape

- 4.1Market Overview

- 4.2Market Drivers

- 4.2.1Rising Incidence Of Chronic Cardiovascular & Neurovascular Diseases

- 4.2.2Growing Geriatric Population & Minimally-Invasive Procedure Demand

- 4.2.3Regulatory Approvals And Supportive Treatment Guidelines

- 4.2.4Technological Advances In Steerability, TIP-Tracking & Composites

- 4.2.5Greater Adoption Of Minimally-Invasive Renal Denervation Procedures

- 4.2.6Venture Funding For Integrated Microcatheter–Delivery Systems

- 4.3Market Restraints

- 4.3.1High Manufacturing Cost & Complex Regulatory Clearance

- 4.3.2Catheter-Related Complications & Recalls

- 4.3.3Supply-Chain Constraints For High-Performance Polymers

- 4.3.4Shortage Of Interventionists Trained In Ultra-Low-Profile Devices

- 4.4Value / Supply-Chain Analysis

- 4.5Regulatory Landscape

- 4.6Technological Outlook

- 4.7Porter’s Five Forces Analysis

- 4.7.1Threat of New Entrants

- 4.7.2Bargaining Power of Buyers

- 4.7.3Bargaining Power of Suppliers

- 4.7.4Threat of Substitutes

- 4.7.5Intensity of Competitive Rivalry

5. Market Size & Growth Forecasts (Value, USD)

- 5.1By Product

- 5.1.1Delivery Microcatheters

- 5.1.2Diagnostic Microcatheters

- 5.1.3Aspiration Microcatheters

- 5.1.4Steerable Microcatheters

- 5.1.5Micro-guide Catheters (Over-the-wire, Flow-directed)

- 5.2By Design

- 5.2.1Single-Lumen

- 5.2.2Dual-Lumen

- 5.3By Application

- 5.3.1Cardiovascular

- 5.3.2Neurovascular

- 5.3.3Peripheral Vascular

- 5.3.4Oncology & Tumor Embolization

- 5.3.5Urology

- 5.3.6Otolaryngology

- 5.4By End-User

- 5.4.1Hospitals

- 5.4.2Clinics & Specialty Centers

- 5.4.3Ambulatory Surgery Centers

- 5.5By Geography

- 5.5.1North America

- 5.5.1.1United States

- 5.5.1.2Canada

- 5.5.1.3Mexico

- 5.5.2Europe

- 5.5.2.1Germany

- 5.5.2.2United Kingdom

- 5.5.2.3France

- 5.5.2.4Italy

- 5.5.2.5Spain

- 5.5.2.6Rest of Europe

- 5.5.3Asia-Pacific

- 5.5.3.1China

- 5.5.3.2Japan

- 5.5.3.3India

- 5.5.3.4Australia

- 5.5.3.5South Korea

- 5.5.3.6Rest of Asia-Pacific

- 5.5.4Middle East & Africa

- 5.5.4.1GCC

- 5.5.4.2South Africa

- 5.5.4.3Rest of Middle East & Africa

- 5.5.5South America

- 5.5.5.1Brazil

- 5.5.5.2Argentina

- 5.5.5.3Rest of South America

6. Competitive Landscape

- 6.1Market Concentration

- 6.2Market Share Analysis

- 6.3Company Profiles (includes Global level Overview, Market level overview, Core Segments, Financials as available, Strategic Information, Market Rank/Share for key companies, Products & Services, and Recent Developments)

- 6.3.1Medtronic PLC

- 6.3.2Boston Scientific Corporation

- 6.3.3Terumo Corporation

- 6.3.4Stryker Corporation

- 6.3.5Cardinal Health Inc.

- 6.3.6Becton, Dickinson and Company

- 6.3.7Teleflex Incorporated

- 6.3.8Merit Medical Systems Inc.

- 6.3.9Asahi Intecc Co., Ltd.

- 6.3.10Cook Group Incorporated

- 6.3.11B. Braun Melsungen AG

- 6.3.12Koninklijke Philips N.V.

- 6.3.13Penumbra Inc.

- 6.3.14MicroPort Scientific Corp.

- 6.3.15Acandis GmbH & Co. KG

- 6.3.16Phenox GmbH

- 6.3.17Vantis Vascular Inc.

- 6.3.18Evasc Neurovascular

- 6.3.19Rapid Medical

- 6.3.20Integer Holdings (CardiaCath)

7. Market Opportunities & Future Outlook

- 7.1White-space & Unmet-need Assessment

Global Microcatheters Market Report Scope

Microcatheters are long, extremely thin tubes used in minimally invasive procedures to access and navigate through narrow blood vessels or other delicate areas within the body. They are thin, flexible, steerable, and multifunctional.

The microcatheters market is segmented by product, design, application, end user, and geography. By product, the market is segmented into delivery microcatheters, diagnostic microcatheters, aspiration microcatheters, and steerable microcatheters. By design, the market is segmented into single-lumen microcatheters and dual-lumen microcatheters. By application, the market is segmented into cardiovascular, neurology, oncology, otolaryngology, and other applications. By end user, the market is segmented into hospitals, clinics, and ambulatory surgical centers. The report also covers the estimated market sizes and trends for 17 countries across major regions globally. The report offers market size and forecast in terms of value (USD) for the above segments.